🏭 HUN $960K Bullish LEAP Bet - Contrarian Play on Battered Chemical Giant! 📈

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just bet $960,000 that Huntsman Chemical stock explodes higher by February 2026! A single buyer scooped up 16,000 call contracts at the $12 strike expiring February 20th - betting on a 15% rally from current levels in a stock that's already down 50% this year. This isn't your neighbor Bob trading - this is a sophisticated bet that HUN's brutal chemical market downturn is bottoming out. Translation: Smart money is loading up on cheap calls while everyone else is running for the exits!

📊 Company Overview

Huntsman Corporation (NYSE: HUN) is a specialty chemicals manufacturer that's been absolutely crushed in 2025:

- Market Cap: $1.81 Billion (down from $3.5B+ at 2024 highs)

- Industry: Chemicals & Allied Products - specializing in MDI/polyurethane chemicals

- Current Price: $10.23 (near 52-week low of $7.30)

- Primary Business: Three segments - Polyurethanes (MDI-based chemicals for construction/insulation), Performance Products, and Advanced Materials (aerospace/coatings)

- Headquarters: The Woodlands, Texas

- Employees: 6,300

This is a company serving adhesives, aerospace, automotive, and construction sectors - all cyclical industries getting hammered by high interest rates and weak global demand.

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 11:38:42):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:38:42 | HUN | BUY | CALL | 2026-02-20 | $960K | $12 | 16K | 632 | 16,000 | $10.23 | $0.60 | HUN 12C 02/20 |

🤓 What This Actually Means

This is a contrarian bullish bet on a deeply distressed chemical stock! Here's the breakdown:

- 💸 Premium paid: $960,000 ($0.60 per contract × 16,000 contracts)

- 🎯 Strike price: $12 represents 17.3% upside from current $10.23 price

- ⏰ Time frame: 80 days to expiration (Feb 20, 2026) - captures Q4 2024 earnings + potential dividend decision

- 📊 Massive volume: 16,000 contracts vs only 632 open interest = 25.3x the existing positions!

- 🔥 Unusualness: Z-score of 330.28 = EXTREMELY UNUSUAL (happens maybe a few times per year for HUN)

- 💰 Cheap premium: At just $0.60/contract, this is a classic "cheap lottery ticket" play

- 📈 Standalone long call: Simple directional bet - no hedging, no spreads, just pure bullish conviction

What's really happening here: This trader thinks HUN has bottomed at $10.23 after falling from $20.83 highs. They're betting that some combination of: 1) Cost restructuring paying off ($280M+ in cuts), 2) Fed/ECB rate cuts stimulating construction demand, or 3) China stimulus boosting MDI demand will send the stock 15-20% higher by February. For $960K, they control 1.6 MILLION shares worth $16.4M - that's massive leverage!

The beauty of this trade: max loss is capped at $960K (100%), but if HUN rallies to $15 by Feb expiration, these calls are worth $3.00 ($4.8M total) = 400% gain!

Unusual Score: 🔥 EXTREME (330.28 Z-score, 25x normal activity) - This size of call buying in HUN happens only a few times per year. Someone with serious conviction is backing up the truck.

📈 Technical Setup / Chart Check-Up

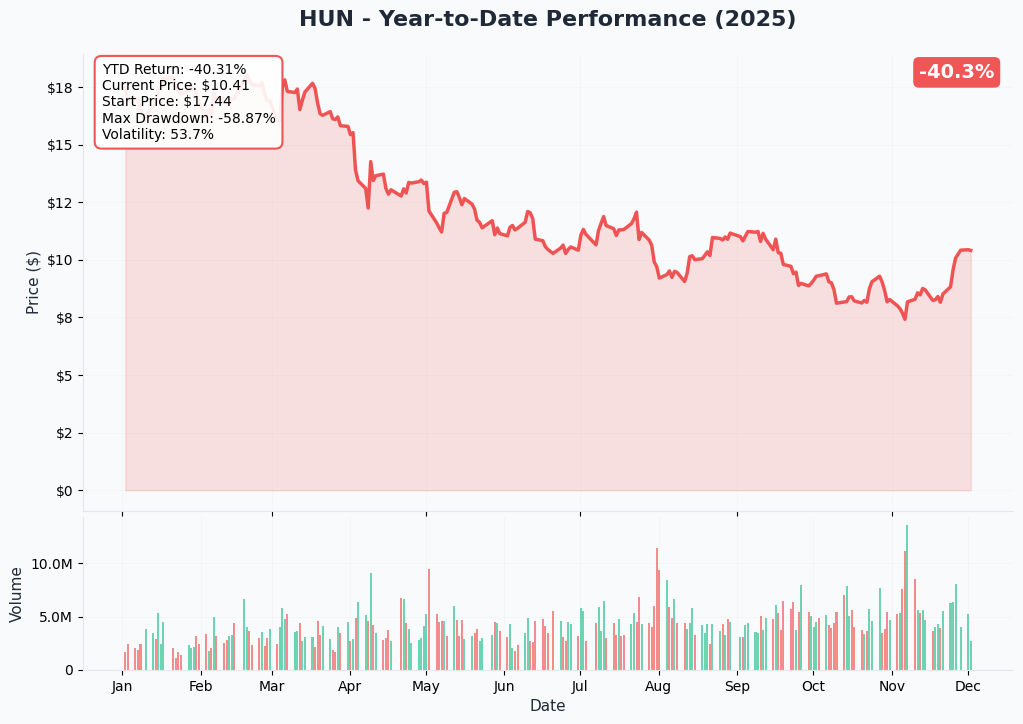

YTD Performance Chart

Brutal Year: HUN is down -49.99% from its 52-week high of $20.83, currently trading at $10.23. The chart shows an absolute bloodbath - steady decline from January highs around $21 to current levels near multi-year lows.

Key observations:

- 📉 Death by a thousand cuts: Systematic selloff throughout 2025 with no relief rallies

- 🔻 52-week low: $7.30 hit in November 2025 - stock has bounced 40% off absolute bottom

- 💔 No support held: Broke through $18, $15, $12 levels like tissue paper

- 📊 Current consolidation: Trading $10-11 range for past month - potential base forming?

- ⚠️ High volatility: Wild swings between $7-11 in Q4 2025 show extreme uncertainty

- 🎢 Classic value trap or true bottom? Stock down 50% creates either opportunity or continued downside

The chart screams "distressed cyclical" - either this is generational buying opportunity near bottom, or we're catching a falling knife. The call buyer clearly thinks it's the former.

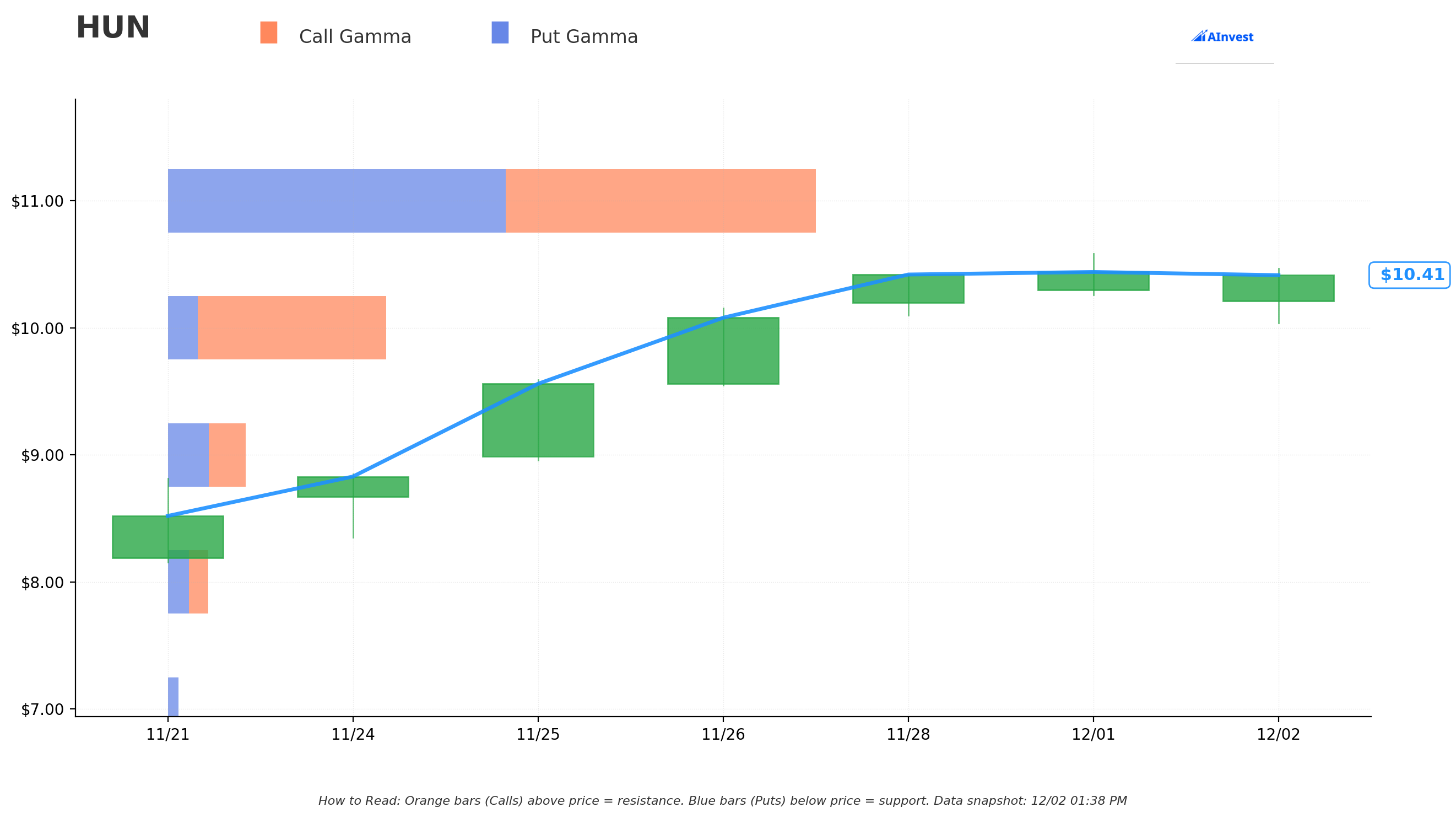

Gamma-Based Support & Resistance Analysis

Current Price: $10.41

The gamma exposure map reveals where options traders are positioned and key price magnets:

🔵 Support Levels (Put Gamma Below Price):

- $10.00 - STRONGEST SUPPORT with 4.02B total gamma exposure (2.92B net GEX) - This is THE LINE IN THE SAND!

- $9.00 - Secondary support at 1.43B gamma (13.6% below current price)

🟠 Resistance Levels (Call Gamma Above Price):

- $11.00 - Immediate ceiling with 11.79B total gamma (STRONGEST RESISTANCE - massive barrier!)

- $12.00 - Secondary resistance at 1.20B gamma (exactly where this call is struck! 15.3% above current)

What this means for traders: HUN is trading in a TIGHT gamma sandwich between $10 support (4.02B gamma) and crushing $11 resistance (11.79B - the absolute LARGEST level). The massive call gamma at $11 (11.79B total) creates natural selling pressure as price approaches - market makers will sell stock to hedge their short call exposure.

Notice the $12 strike? The call buyer positioned EXACTLY at the secondary resistance level ($12) where there's 1.20B gamma. They need HUN to not just break $11 resistance, but CLEAR it convincingly and push to $12+ for the trade to really pay off.

Net GEX Bias: Bullish (11.60B call gamma vs 9.33B put gamma) - Overall positioning shows more bullish exposure than bearish, which aligns with this call buyer's thesis. The $10 floor looks solid with nearly 3B net positive GEX.

Critical insight: If HUN breaks above $11, there's relatively clear air to $12. But getting through that $11.79B gamma wall at $11 will be like pushing a boulder uphill. Needs MAJOR catalyst or volume.

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Dec 19 - 17 days): ±$0.89 (±8.57%) → Range: $9.53 - $11.31

- 📅 February OPEX (Feb 20 - 80 days - THIS TRADE!): ±$2.42 (±23.2%) → Range: $8.21 - $12.63

- 📅 Yearly LEAPS (Dec 2026 - 381 days): ±$8.07 (±77.43%) → Range: $2.35 - $18.49

Translation for regular folks: Options traders are pricing in an 8.6% move ($0.89) by December 19th - that's HUGE volatility for a normally sleepy chemical stock! The market expects continued wild swings as the company navigates restructuring and weak end-markets.

The February 20th expiration (when this $960K trade expires) has an upper range of $12.63 - meaning the market thinks there's a reasonable probability HUN could trade up to $12.60+ over the next 80 days. This aligns PERFECTLY with the call buyer's $12 strike! They're betting on the upper end of the implied move range.

Key insight: The 23% implied move for February reflects massive uncertainty around:

- Q4 2024 earnings (expected Feb 17-18)

- Potential dividend cut/suspension announcement

- Restructuring progress updates

- Construction market recovery timing

The call buyer is essentially betting HUN ends up in the top quartile of outcomes (near $12.60 upper range) rather than bottom quartile (near $8.20 lower range).

🎪 Catalysts

📊 Already Happened (What Got Us Here)

Q3 2024 Earnings Miss - November 5, 2024

HUN reported another disappointing quarter that confirmed the brutal industry downturn:

- 📉 Revenue: $1,540M vs $1,551M consensus (0.69% miss)

- 💔 EPS: -$0.03 loss vs -$0.13 consensus (beat only because expectations were THAT low)

- 📊 Adjusted EBITDA: $131M vs $44M prior year (+$87M improvement)

- 🏭 CEO stated Q3 was "consistent with outlook of stable environment at trough conditions"

Management confirmed they expect "near term trough conditions persist through a seasonally lower fourth quarter" - translation: don't expect improvement soon.

Massive Restructuring Announcements - Throughout 2024-2025

HUN has been aggressively cutting costs to survive the downturn:

- 💼 Nearly 10% global workforce reduction announced Q2 2025

- 🏭 Facility closures in Germany (Deggendorf) and UK (King's Lynn)

- 💰 $50M Polyurethanes cost reduction program bringing total cuts to $280M+ over past few years

- 🎯 Management expects restructuring savings to exceed $100M with completion in 2026

This is the thesis behind the call buyer: all this pain = future margin improvement once volumes stabilize.

Stock Collapse to 52-Week Lows - November 2025

HUN hit new 52-week low of $7.30 in early November as sell-side analysts slashed price targets:

- 🔻 Bank of America: Downgraded to Underperform from Neutral

- 🔻 UBS: Lowered price target to $9 from $10

- 🔻 Wells Fargo: Reduced target from $13 to $9

- 📊 Consensus price target: $9.69 = 7% downside from $10.42

Insider Buying at Distressed Levels - November 2025

Interestingly, as stock cratered to $7-8, officers bought 29,762 shares at $8.155 average price on November 10, 2025. When insiders buy at multi-year lows, it's worth paying attention!

🔥 Upcoming Catalysts (Next 80 Days - During Call Option Life)

Q4 2024 Earnings - Expected February 17-18, 2026 (THE BIG ONE!) 📊

This is THE catalyst that will make or break this call trade. HUN typically reports 4th quarter earnings in mid-February:

What to watch:

- 📊 Revenue expectations: Likely $1.45-1.50B (down from $1.54B in Q3 due to "seasonally lower" Q4)

- 💔 Profitability: Another loss expected (would be 4th consecutive quarterly loss)

- 📈 Adjusted EBITDA: $25-50M range guided by management (low end due to Rotterdam outage)

- 🏭 Rotterdam facility update: Unplanned outage reducing Q4 EBITDA by ~$10M, MDI line expected to resume mid-December

- 💰 Restructuring progress: Updates on $100M+ savings target and facility closure execution

- 🎯 2026 guidance: CRITICAL - any signs of construction market recovery or volume stabilization could send stock soaring

Bull case: Earnings show cost cuts working (EBITDA beats low $25-50M range), management signals they see "light at the end of tunnel" for H1 2026 construction recovery, maintains or raises dividend = stock rips to $12-13

Bear case: Another miss, cuts dividend, guides conservatively for 2026 citing "extended trough" = stock retests $7-8 lows

Probability: This is a binary event with 80 days from now. The call buyer is clearly positioning for the bull case.

Dividend Decision - High Probability Event Q4 2025/Q1 2026 💰

This is the ELEPHANT IN THE ROOM:

- 💸 Current annual dividend: $1.00/share ($0.25 quarterly)

- 🚨 Dividend yield: 9.60% (absurdly high - screams "unsustainable!")

- 💔 Cash payout ratio: 219.9% (dividend exceeds cash flow by 2.2x)

- 😱 Company paying dividend WHILE UNPROFITABLE for 3 consecutive quarters

Seeking Alpha headline says it all: "Huntsman: Balance Sheet Takes Priority Over The Dividend"

Probability assessment: 65-75% chance dividend gets cut or suspended in next 2-3 months

Impact on call trade:

- ❌ If dividend CUT: Stock likely drops 10-15% initially (income investors flee) = KILLS the $12 call trade

- ✅ If dividend MAINTAINED: Signals management confidence in recovery, removes overhang = HELPS the call trade

- ⚖️ If dividend REDUCED but not eliminated: 50% cut to $0.50/year could be Goldilocks - improves balance sheet but keeps yield investors = NEUTRAL

The call buyer is betting dividend gets maintained OR stock rallies on other factors enough to offset cut.

Fed/ECB Rate Cuts Impact - H1 2026 Timeline 📈

Management explicitly cited rate cuts as future tailwind:

- 🏦 Benefits "weighted towards H2 2025 as lag effects of rate cuts take hold"

- 🏗️ Construction and transportation account for ~75% of Huntsman's volumes

- ⏰ Critical timing: Rate cuts started in late 2024, but lag effect means construction activity improves in Q1-Q2 2026

- 📊 Potential impact: 3-5% volume recovery if rate cuts successfully stimulate housing/construction

February expiration captures early signs: By Feb 20, 2026, market should have clarity on whether rate cuts are actually translating to order activity in Q1 2026. Even HINTS of volume stabilization could send stock higher.

China Government Stimulus - Wildcard Catalyst 🇨🇳

CEO noted MDI demand faced "unprecedented downdraft" with 2 consecutive years of falling demand - something veterans with 30+ years have never seen.

- 🇨🇳 China stimulus expected to have positive impact on portfolio

- 🏗️ China represents significant portion of global polyurethanes/MDI demand

- ⏰ Timing: Q4 2025/Q1 2026 for stimulus impact on order flow

- 🎯 Probability: 50-60% that stimulus provides meaningful demand boost

Restructuring Milestones - Ongoing Through Feb 2026

$100M+ in total restructuring savings target with quarterly updates:

- 🏭 European facility closures in progress (Germany, UK completed; others ongoing)

- 💼 10% workforce reduction implementation through 2025-2026

- 📊 Expected quarterly updates with each earnings release

- 💰 EBITDA Impact: $25-30M quarterly run-rate improvement by Q4 2025

If Q4 earnings show restructuring AHEAD of schedule with costs coming out faster than revenue declining, it validates the "operating leverage on the way back up" thesis and justifies higher multiple.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20, 2026 expiration:

📈 Bull Case (30% probability)

Target: $12-14

How we get there:

- ✅ Q4 earnings beat low expectations ($35-40M EBITDA vs $25-50M guided range)

- 💪 Management commentary signals "seeing signs of stabilization" in core construction markets

- 💰 Dividend MAINTAINED at $1.00/year (removes 220% payout ratio fear)

- 🏗️ Fed/ECB rate cuts showing EARLY signs of construction activity pickup in Jan-Feb 2026 orders

- 🇨🇳 China stimulus translating to actual MDI demand improvement (not just talk)

- 📊 Restructuring progress report shows $30M+ quarterly savings already realized

- 🎯 Breaks above $11 gamma resistance on volume, clears to $12 strike with momentum

- 🏦 Institutional buyers (like PZENA who added 320% in Q4) continue accumulating at distressed levels

Key metrics needed:

- Q4 EBITDA above $35M (beating low-end guidance)

- Positive free cash flow in Q4 (vs. negative prior quarters)

- Construction end-market commentary less bearish than Q3

- 2026 guidance showing revenue stabilization ($6.0-6.2B for year)

Why only 30%? Requires multiple positive catalysts aligning: dividend maintained AND earnings beat AND macro improvement AND stock breaking through massive $11 resistance. Possible but needs a lot to go right.

Call option P&L in bull case:

- Stock at $12.00 on Feb 20: Calls worth $0 (at-the-money), loss = -$960K (100% loss)

- Stock at $13.00 on Feb 20: Calls worth $1.00, P&L = $1.6M total - $960K cost = +$640K gain (67% ROI)

- Stock at $14.00 on Feb 20: Calls worth $2.00, P&L = $3.2M total - $960K cost = +$2.24M gain (233% ROI!)

- Stock at $15.00 on Feb 20: Calls worth $3.00, P&L = $4.8M total - $960K cost = +$3.84M gain (400% ROI!)

🎯 Base Case (45% probability)

Target: $9.50-11.50 range (CHOPPY, CALL EXPIRES NEAR WORTHLESS)

Most likely scenario:

- 📊 Q4 earnings meet low expectations (EBITDA $25-30M range, in-line with guidance)

- 💰 Dividend gets CUT but not eliminated (reduced to $0.50/year from $1.00)

- 🏗️ Construction markets remain weak but not deteriorating further ("stable trough")

- ⏰ Management guides conservatively: "expect improvement in H2 2026, not H1"

- 🇨🇳 China stimulus announced but takes time to flow through to actual orders

- 📉 Stock initially dips on dividend cut news to $9-9.50, then recovers to $10-11 range

- 🔄 Trading within $10 gamma support and $11 gamma resistance for duration

- 💤 Volatility normalizes post-earnings, implied vol drops from 23% to 15-18% range

- ⚖️ Neither clearly bullish nor bearish - just grinding sideways in distressed range

This is the "value trap" scenario: Stock doesn't collapse to new lows, but doesn't rally either. Just dead money consolidating as market waits for actual construction recovery evidence (which won't materialize until H2 2026).

Why 45% probability? This is the "muddle through" outcome - company survives, doesn't thrive. Most common outcome for distressed cyclicals is extended bottom-fishing period before eventual recovery.

Call option P&L in base case:

- Stock at $9.50 on Feb 20: Calls worthless, loss = -$960K (100% loss)

- Stock at $10.50 on Feb 20: Calls worthless, loss = -$960K (100% loss)

- Stock at $11.50 on Feb 20: Calls worthless, loss = -$960K (100% loss)

Brutal reality: If stock stays below $12, these calls expire 100% worthless. The buyer loses ENTIRE $960K premium. This is the most likely outcome - they're betting on 30% bull case, accepting 45% chance of total loss.

📉 Bear Case (25% probability)

Target: $7-9 (RETEST LOWS, TOTAL LOSS)

What could go wrong:

- 😱 Q4 earnings disaster: EBITDA at low-end $25M or BELOW guidance range

- 💔 Dividend SUSPENDED entirely (not just cut) - management prioritizes balance sheet

- 🚨 Rotterdam facility outage worse than expected or extends into Q1 2026

- 🇨🇳 No meaningful China stimulus or stimulus fails to boost MDI demand

- 📉 Fed/ECB rate cuts showing ZERO impact on construction activity through Feb 2026

- 💸 2026 guidance disastrous: management expects "extended trough through 2026"

- 🏭 Restructuring hits snags - European facility closures delayed or more expensive than planned

- 🌊 Broader chemical sector selloff (BASF, Dow, etc.) drags HUN lower

- 💔 Break below $10 gamma support triggers cascade to $9, then $7.30 prior low

- 📊 Analyst downgrades accelerate - consensus target drops from $9.69 to $7-8 range

Critical support levels:

- 🛡️ $10.00: Major gamma floor (4.02B total) - MUST HOLD or sentiment shifts

- 🛡️ $9.00: Secondary support (1.43B gamma) - last line of defense

- 🛡️ $7.30: 52-week low from November - retest would be catastrophic for bulls

Why 25% probability? Requires things to get materially WORSE from current "trough" levels. Management has already guided to low expectations for Q4. Hard to disappoint when bar is on the floor. Also, insiders buying at $8 suggests some confidence in floor.

Call option P&L in bear case:

- Stock at $9.00 on Feb 20: Calls worthless, loss = -$960K (100% loss)

- Stock at $8.00 on Feb 20: Calls worthless, loss = -$960K (100% loss)

- Stock at $7.30 on Feb 20: Calls worthless, loss = -$960K (100% loss)

No matter how bad it gets, call buyer can only lose the $960K premium paid. That's the beauty and curse of long calls - capped downside, unlimited upside.

💡 Trading Ideas

🛡️ Conservative: Stay Away (This Is Too Risky!)

Play: Avoid HUN entirely - this is a distressed cyclical with massive uncertainty

Why this makes sense:

- 💀 Company reporting LOSSES for 3+ consecutive quarters with no visibility to profitability

- 🚨 Unsustainable 220% dividend payout ratio = high probability of cut (negative catalyst)

- 📉 Analyst consensus at $9.69 shows 7% downside from current $10.42 price

- 🏗️ Core end-markets (construction, automotive) showing no signs of recovery

- 🌍 Geopolitical risks (China export restrictions, European energy costs) unresolved

- ⚖️ Even insiders buying at $8 shows their "bottom" is 20% below current price

- 💰 Better uses of capital than catching falling knives in distressed chemicals

For conservative investors: If you REALLY want chemical exposure, buy Dow (DOW) or BASF which have:

- ✅ Larger scale and diversification

- ✅ Stronger balance sheets

- ✅ More sustainable dividends

- ✅ Better positioned for eventual recovery

Action plan:

- 👀 Watch from sidelines - put HUN on watchlist for $7-8 range if you're bargain hunting

- 📊 Wait for actual EVIDENCE of construction recovery (not just hope)

- ✅ Need to see: Positive quarterly earnings, dividend sustainability, volume stabilization

- ⏰ Revisit in 6-12 months when macro picture clearer

Risk level: None (no position) | Skill level: N/A

Expected outcome: Avoid potential 20-30% downside if dividend cut or earnings disappoint. Preserve capital for better opportunities.

⚖️ Balanced: Small Speculative Long Stock Position at Support

Play: Buy small stock position at $10.00-10.25 support with tight stop

Why this could work:

- 🎯 Stock testing major $10 gamma support (4.02B total GEX) - strong technical floor

- 💰 Down 50% from highs creates asymmetric risk/reward IF recovery materializes

- 🏦 Smart institutional money accumulating (PZENA +320%, Nomura +188% in Q4 2024)

- 🤝 Insiders bought at $8.15 - they know the business better than analysts

- 📈 Restructuring delivering $100M+ savings by 2026 = operating leverage on recovery

- 🏗️ Fed rate cuts WILL eventually help - just a question of timing

- 📊 At $10.23, stock at 52-week low end of range - not chasing, buying dips

- 🎲 Risk/Reward: If wrong, stop at $9.50 = 7% loss. If right and rallies to $13-14 = 30-40% gain

Structure:

- 💵 Buy 200-500 shares at $10.00-10.25 (invest $2,000-5,000 total)

- 🛑 TIGHT stop loss at $9.50 (5% below entry) - must respect if $10 support breaks

- 🎯 First target: $11.50 (15% gain) - take 50% off table

- 🚀 Second target: $12.50-13.00 (25-30% gain) - sell remaining position

- ⏰ Time horizon: 3-6 months (not day trading, but not long-term hold either)

Position sizing: Risk only 2-3% of portfolio (this is speculation on distressed cyclical, not core holding)

What you're betting on:

- Q4 earnings don't crater (just need "in-line" with low expectations)

- Dividend maintained or cut smaller than feared (50% cut vs. full suspension)

- Some signs of construction stabilization by March 2026

- Technical bounce from oversold levels as shorts cover

Exit triggers (SELL immediately if):

- ❌ Dividend fully suspended

- ❌ Q4 earnings miss even low guidance

- ❌ Breaks below $9.50 stop loss

- ❌ Management guides to "extended trough through 2026+"

Risk level: Moderate (5% stop loss limits downside) | Skill level: Intermediate

Expected outcome: Either small 5-7% loss if thesis breaks, or 15-30% gain if recovery starts materializing. Defined risk, asymmetric reward.

🚀 Aggressive: Small Call Option Lottery Ticket (Copy The Whale!)

Play: Buy small position of Feb $12 calls (SAME strike as the $960K trade)

Structure: Buy 10-20 contracts of Feb 20, 2026 $12 calls at ~$0.60-0.70

Why this could work (THE BULL CASE):

- 🐋 Following smart money - someone bet $960K on this exact trade for a reason

- 💰 CHEAP premium: Only $0.60-0.70 per contract ($60-70 per contract)

- 🎯 Massive leverage: $1,000 controls 1,000 shares ($10,230 worth of stock exposure)

- 📈 If HUN rallies to $14-15 (totally possible if all catalysts align), $12 calls worth $2-3 = 300-400% gain!

- 🎲 Defined risk: Can only lose premium paid ($600-1,400 total)

- ⏰ 80 days to expiration captures all major catalysts (earnings, dividend decision, macro)

- 🏗️ Construction recovery narrative + rate cuts + China stimulus + cost cuts = lottery ticket with multiple ways to win

- 🔥 Implied move upper range is $12.63 - betting on upper quartile outcome

The pitch: This is your "Powerball ticket" - you're betting $600-1,400 that HUN is at a generational bottom and EVERYTHING goes right:

- ✅ Earnings beat

- ✅ Dividend maintained

- ✅ Construction shows early recovery signs

- ✅ Breaks through $11 resistance

- ✅ Short squeeze as bears capitulate

- ✅ Rallies to $13-15 range

Estimated P&L:

- 💰 Cost: $600-700 for 10 contracts OR $1,200-1,400 for 20 contracts

- 📈 Home run (stock at $14): Calls worth $2.00 = $2,000 profit on 10 contracts (286% ROI) or $4,000 profit on 20 contracts

- 🚀 Grand slam (stock at $15): Calls worth $3.00 = $3,000 profit on 10 contracts (429% ROI) or $6,000 profit on 20 contracts

- 📉 Most likely outcome (stock at $10-11): Calls expire worthless = -$600-1,400 (100% loss)

- 💀 Bear case (stock at $8-9): Calls expire worthless = -$600-1,400 (100% loss)

Breakeven: Need stock above $12.60-12.70 by Feb 20 to break even (strike + premium paid)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (70% probability these expire worthless!)

- ✅ Understand this is pure speculation, not investing

- ✅ Won't panic sell if stock dips to $9.50 - you NEED to hold for full 80 days

- ✅ Accept you're betting against analyst consensus and fighting 50% YTD downtrend

- ✅ Have other safer positions and this is <3% of portfolio (treat it like Vegas money)

What needs to happen:

- 📊 Q4 earnings February 17-18 MUST beat expectations materially

- 💰 Dividend maintained or cut less than 50%

- 🏗️ Construction data (housing starts, infrastructure spending) shows improvement Jan-Feb

- 📈 Stock needs to rally 20%+ in 80 days (from $10.23 to $12.30+)

Position management:

- 🎯 If stock rallies to $11.50-12.00 before expiration, consider selling 50% to lock in gains

- ⏰ Don't hold to expiration if profitable - take money off table

- 💔 If stock breaks below $9.50, thesis likely broken - may want to cut loss and sell for $0.10-0.20 residual value

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~30% (bull case scenario)

Why I'm even mentioning this: Because someone with MUCH more information than you or I just bet $960,000 on this EXACT trade. Either they're an idiot (unlikely at that size), or they see something in HUN's valuation/setup that the market is missing. Small speculation copying institutional smart money can occasionally pay off big.

Just remember: For every 1 of these that 4x's, three expire worthless. Manage your risk accordingly!

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💰 Dividend cut/suspension = automatic -10-15% gap down: The 9.60% yield with 219.9% payout ratio is mathematically unsustainable. Company is PAYING OUT $1/share annually while LOSING MONEY. This is going to end badly. When (not if) they cut or suspend, income investors will dump the stock immediately. Even if fundamentals improving, dividend cut creates selling pressure that overwhelms bullish thesis. High probability catalyst in next 60-90 days.

-

📉 Q4 earnings could undershoot already-low expectations: Management guided $25-50M EBITDA range with Rotterdam outage reducing by $10M. That's EXTREMELY wide guidance = zero visibility. What if they come in at $20M or below? At current $1.81B market cap, that's abysmal profitability. Even one more quarter of worse-than-expected results kills any recovery narrative. Historical precedent: Chemical companies in "trough" often stay there 12-18 months longer than bulls expect.

-

🏗️ Construction recovery may not materialize until 2027: Management explicitly said benefits "weighted towards H2 2025" but we're in December 2025 and STILL no recovery. Rate cut transmission lags are 12-18 months, not 6-9 months. Housing starts, commercial construction, infrastructure projects don't turn on a dime. By the time construction actually recovers, HUN may have already cut dividend, diluted shareholders, or taken on more debt. Timing matters.

-

🇨🇳 China risks are MASSIVE and underappreciated: Already took $800M hit in Q2 2025 from export restrictions (later partially lifted). China historically 15-20% of revenue. New restrictions could hit without warning. Chinese domestic competitors (cheaper cost structure) taking share. China stimulus may help Wanhua Chemical (Chinese MDI producer) more than Huntsman. Geographic concentration risk.

-

⚔️ Competitive dynamics deteriorating: CEO admitted veterans with 30+ years haven't seen 2 consecutive years of falling MDI demand. This isn't normal cyclicality - this is structural shift. Asian capacity additions (particularly Chinese producers) creating permanent pricing pressure. European facility closures cede market share to competitors. Once you lose customers in specialty chemicals, very hard to win back.

-

💸 Balance sheet stress with negative free cash flow: Q3 FCF was $93M down from $117M prior year (-20.5%). Company burning cash while paying unsustainable dividend. $350M debt refinancing in Sept 2024 helps liquidity but adds interest expense. If losses continue through 2026, may need to raise equity (dilutive) or cut deeper. Credit rating at risk.

-

🎢 Extreme volatility = whipsaw risk: Stock trading $7.30 to $11+ range in just past 2 months (50% range!). This isn't stable value investing - this is distressed trading. News flow drives 5-10% intraday moves. Options pricing 23% implied move for Feb = market expects continued chaos. If you can't stomach 20-30% drawdowns, stay away.

-

🌍 European exposure is structural headwind: European markets remain challenging due to high energy costs and industrial decline. Germany (major market) in recession. Energy costs 2-3x higher than US competitors. Huntsman closed German and UK facilities = permanently reduced European presence. Unlike cyclical issue, this is secular decline in European manufacturing competitiveness.

-

📊 Analyst consensus BEARISH with downgrades continuing: $9.69 average price target = 7% downside. Multiple recent downgrades: BofA to Underperform, UBS cut to $9, Wells Fargo to $9, Citi to $8.50. Ratings: 3 Buy, 6 Hold, 3 Sell = "Reduce" consensus. These analysts have chemical sector expertise and models showing limited upside. They may be wrong, but they have information flow and industry contacts retail traders don't.

-

🏭 Restructuring execution risk: $100M savings target requires successful facility closures and workforce reductions. What if severance costs higher than expected? What if key customers leave during facility transitions? What if closure delays push savings to 2027? Cost cutting ALWAYS harder than management projects. History shows restructuring targets get revised down.

-

🎯 $11 gamma resistance is MASSIVE wall: The 11.79B total gamma at $11 strike (biggest level on the board) creates mechanical selling pressure. Every time stock rallies toward $11, market makers will sell stock to hedge their short call exposure. This isn't fundamental resistance - it's structural. Would need MAJOR volume and multiple positive catalysts to break through and hold above $11.

-

💀 Value trap = most common outcome for distressed cyclicals: Stock down 50% looks "cheap" but that doesn't mean it can't go down another 30% or just trade sideways for years. Plenty of chemical stocks traded at 52-week lows in 2008-2009 and NEVER recovered (some went bankrupt). "Down 50%" isn't a catalyst. Actual earnings improvement, actual volume growth, actual margin expansion = those are catalysts. Hope is not a strategy.

🎯 The Bottom Line

Real talk: Someone just bet nearly $1 MILLION on a 15% rally in one of the most hated chemical stocks in America. That's either brilliant contrarian positioning or throwing good money after bad. Here's my take:

What this trade tells us:

- 🎯 Sophisticated player sees HUN at $10.23 as "the bottom" after 50% decline

- 💰 They're willing to risk $960K betting on recovery rather than continued deterioration

- ⏰ The 80-day timeframe (Feb 20 expiration) captures Q4 earnings + dividend decision + early 2026 macro data

- 🎲 They chose $12 strike (17% above current) = not gambling on moon shot, betting on modest recovery to prior $12-13 consolidation range

- 📊 Z-score of 330.28 (extremely unusual) suggests this isn't random speculation - someone with conviction and information

This is NOT a "follow blindly" signal - it's a "pay attention, something might be brewing" signal.

The bull case (why this could work):

- 💪 $280M in restructuring cuts creating $25-30M quarterly EBITDA lift by 2026

- 🏗️ Fed/ECB rate cuts WILL eventually stimulate construction (just a timing question)

- 🎯 At $10.23, stock priced for bankruptcy when company isn't going bankrupt

- 🏦 Sophisticated institutions (PZENA, Nomura) adding HUNDREDS OF MILLIONS at these levels

- 📈 Insiders buying at $8.15 = they see the numbers, think floor is in

- 🇨🇳 China stimulus could surprise to upside on MDI demand

- 📊 "Trough" by definition means things can't get worse - only sideways or better

- 🔄 Cyclicals at bottoms offer 50-100% upside over 12-24 months IF you time it right

The bear case (why this could blow up):

- 💔 Three consecutive quarterly losses with no visibility to profitability

- 💸 Dividend cut/suspension (65-75% probability) triggers automatic selling

- 📉 Construction recovery may not come until 2027 (too late for Feb calls)

- 🌍 European exposure = structural headwind, not cyclical

- 🇨🇳 China risks (export controls, domestic competition) underestimated

- ⚖️ Analyst consensus at $9.69 (7% below current) suggests downside not done

- 🏭 Restructuring could disappoint or take longer than expected

- 💀 Value traps stay traps for YEARS - down 50% doesn't mean "cheap"

If you own HUN stock:

- ⚠️ Set STOP LOSS at $9.50 (just below $10 major gamma support) - don't ride this to $7

- 💰 If you're sitting on losses, decide NOW: average down at $10 support OR cut loss if breaks $9.50

- 📊 Q4 earnings Feb 17-18 is make-or-break - if they maintain dividend AND beat EBITDA expectations, hold for recovery

- 🚨 If they suspend dividend OR miss earnings, GET OUT - don't marry a losing position

If you're thinking about buying:

- ⏰ DO NOT buy before Q4 earnings - too much uncertainty with dividend decision and Rotterdam outage impact

- 🎯 If you want to speculate: Small position at $10.00-10.25 with 5% stop loss at $9.50

- 💰 OR: Tiny call option lottery ticket (10-20 contracts of Feb $12 calls) for $600-1,400 total

- ✅ Both approaches have DEFINED RISK and asymmetric upside IF recovery materializes

- ❌ Do NOT bet the farm - this is 2-3% of portfolio MAX

If you're bearish:

- 🎯 Wait for post-earnings rally (if any) to initiate short or buy puts

- 📊 Watch for break below $10 support - that's the technical trigger for $9 then $8

- ⚠️ Don't fight potential short squeeze if earnings somehow exceed low bar

- 💸 Bear thesis relies on dividend cut + earnings miss + no construction recovery = need all three

Mark your calendar - Key dates:

- 📅 December 19 - Monthly OPEX (±8.6% implied move window)

- 📅 Mid-December 2025 - Rotterdam MDI line expected to resume production

- 📅 February 17-18, 2026 - Q4 2024 earnings report (THE BIG ONE!)

- 📅 February 20, 2026 - Expiration of this $960K call trade

- 📅 H2 2026 - When rate cut benefits theoretically materialize in construction volumes

Final verdict: HUN at $10.23 is a HIGH-RISK, HIGH-REWARD speculation on cyclical bottom-fishing. The fundamentals are TERRIBLE (losses, dividend unsustainable, weak end-markets), but the VALUATION is distressed (down 50%, trading near book value, priced for extended trough).

The $960K call buyer is betting on mean reversion + cost cuts + macro recovery. They might be early, but if they're right about the bottom being in at $7-10 range, the reward is 100-300% upside over 12-24 months.

For most investors: STAY AWAY. This is a distressed cyclical with limited visibility and high execution risk. If you have high risk tolerance and believe in contrarian value investing, a SMALL speculative position with tight stops makes sense. But this is NOT a core portfolio holding - it's a "maybe I'll get lucky at the roulette table" bet.

The smart money is divided: Institutions adding massively (PZENA, Nomura) while analysts downgrading (BofA Underperform, consensus $9.69 target). Classic bottoming process is messy and takes time. The call buyer might be right about direction but wrong about timing (Feb expiration too soon).

Be patient. Respect the risk. Size your position accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The 330.28 Z-score reflects this specific trade's size relative to recent HUN history - it does not imply the trade will be profitable. Huntsman faces significant risks including: dividend sustainability (219.9% payout ratio), three consecutive quarterly losses, construction market weakness, China export restrictions, competitive pressures, and restructuring execution risk. The company may cut or suspend its dividend at any time. Q4 earnings create binary event risk. Always do your own research and consider consulting a licensed financial advisor before trading distressed cyclical stocks or options.

About Huntsman Corporation: Huntsman is a chemical manufacturer specializing in "differentiated organic chemical products" including MDI, polyols, and epoxy formulations, serving adhesives, aerospace, automotive, and construction sectors through three main divisions: Polyurethanes, Performance Products, and Materials, with a market cap of $1.81 billion in the Chemicals & Allied Products industry.