🛡️ HYG $5.6M Bull Put Spread - High-Yield Bonds Under Fed's Watchful Eye! 💰

📅 December 18, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated trader deployed $5.6 MILLION on a bull put spread in HYG this morning at 10:21:50! This bullish income strategy sold 50,000 contracts of $80 puts while buying $76 puts for March 20, 2026 expiration - collecting a net $2.8M credit with downside protection at $76. With HYG trading at $80.71 and the Fed having just delivered a hawkish 25bp rate cut yesterday, smart money is betting high-yield spreads stay tight through Q1 2026. Translation: Institutional investors are selling insurance that HYG won't crash below $80, pocketing $2.8M if correct!

📊 ETF Overview

iShares iBoxx $ High Yield Corporate Bond ETF (HYG) is the largest high-yield bond ETF, providing exposure to U.S. dollar-denominated "junk bonds":

- Assets Under Management: $20.35 Billion (largest in high-yield space)

- Asset Type: Corporate Bond ETF (High Yield)

- Current Price: $80.66 (as of Dec 17, 2025)

- Dividend Yield: 5.74% (monthly distributions)

- 52-Week Range: $75.08 - $81.36

- Primary Holdings: 1,331 high-yield corporate bonds with diversified sector exposure

- Top Holdings: DISH Network, Mozart Debt Merger Sub, Picard Midco, Cloud Software Group, DIRECTV Holdings

💰 The Option Flow Breakdown

The Tape (December 18, 2025 @ 10:21:50):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:21:50 | HYG | BID | BUY | PUT $76 | 2026-03-20 | $1.4M | $76 | 50K | 149K | 50,000 | $80.71 | $0.27 |

| 10:21:50 | HYG | ASK | SELL | PUT $80 | 2026-03-20 | $4.2M | $80 | 50K | 50K | 50,000 | $80.71 | $0.83 |

🤓 What This Actually Means

This is a classic bull put spread - a defined-risk bullish income strategy! Here's the breakdown:

- 💸 Net credit collected: $2.8M ($0.83 - $0.27 = $0.56 per contract × 50,000 contracts)

- 🎯 Short strike: Sold $80 puts at current price level - betting HYG stays above $80

- 🛡️ Long strike: Bought $76 puts as protection - caps max loss at $4/share ($200K per 50,000 contracts)

- ⏰ Strategic timing: 92 days to expiration (March 20) captures January 28-29 Fed meeting, Q1 2025 earnings season, and potential fallen angel wave

- 📊 Risk/Reward: Max profit $2.8M if HYG above $80 at expiration; max loss $17.2M if below $76 (5.2% downside cushion)

- 🏦 Professional positioning: Z-scores of 3.83 and 10.01 show this is 3-10 standard deviations above normal activity - extremely unusual size

What's really happening here: This trader has a constructive view on high-yield credit through Q1 2026. By selling the $80 strike puts, they're effectively saying "I don't think HYG will drop below $80 by March." They collect $0.83/share in premium (2.8M total) for taking on that obligation. The $76 puts they bought for $0.27/share cap their downside - if HYG crashes to $70, they're protected below $76. Net position: collect $0.56/share ($2.8M) if correct, risk $3.44/share ($17.2M) if wrong. That's a 61% probability of maximum profit built into the pricing!

Unusual Score: 🔥🔥 VERY UNUSUAL (Z-scores 3.83 and 10.01) - The $80 put trade is 10 standard deviations above average, happening only a few times per year. This isn't retail - it's an institution making a significant bullish bet on credit market stability.

Why now? Coming just one day after the Fed's December 18th hawkish rate cut (25bp with only two 2025 cuts projected vs four previously), this trade suggests smart money believes:

- High-yield spreads at 310bps are stable/sustainable despite hawkish pivot

- No major credit crisis expected through Q1 2026

- The 7.5% yield and 5.74% distribution rate provide cushion against rate volatility

- Fallen angel wave of $45-55B will add quality credits to HYG, not crash prices

📈 Technical Setup / Chart Check-Up

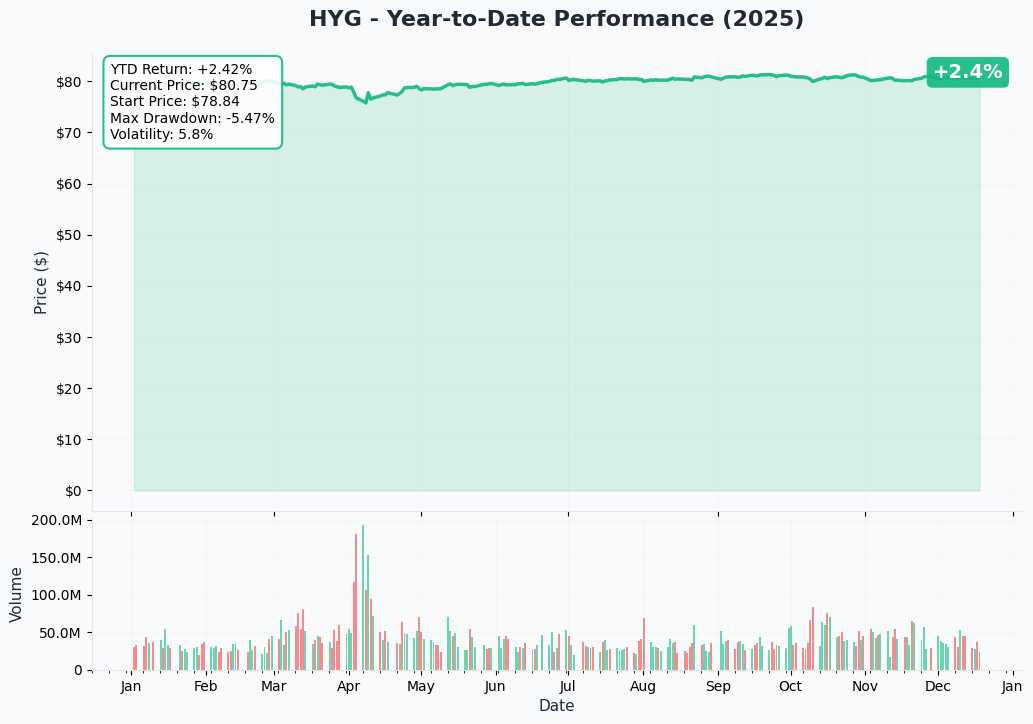

YTD Performance Chart

HYG is up +7.97% YTD (6.14% through Q3 plus recent gains), trading near the high end of its range at $80.66. After experiencing significant outflows that positioned it among 2024's worst-performing ETFs by flows, the fund has seen a dramatic reversal with $2.14B in monthly inflows and $1.57B in 3-month flows.

Key observations:

- 📈 Strong recovery: Bounced from $75.08 52-week low to current $80.66, approaching $81.36 52-week high

- 💰 Income cushion: 5.74% dividend yield provides downside protection - investors collect monthly distributions while waiting

- 🔄 Flow reversal: Recent $2.14B inflows suggest institutional money returning to high-yield after earlier exodus

- 📊 Trading range: Consolidating in $78-81 range for several weeks - respecting both gamma support and resistance

- ⚠️ Fed risk: Spreads widened 21bps in December post-FOMC despite tight 310bps absolute levels - volatility potential remains

The chart shows HYG is in a "higher for longer yield" environment - not explosive upside, but stable income generation. The bull put spread trader is betting on exactly this scenario: sideways to slightly higher price action while collecting 5.74% dividends and the $2.8M option premium.

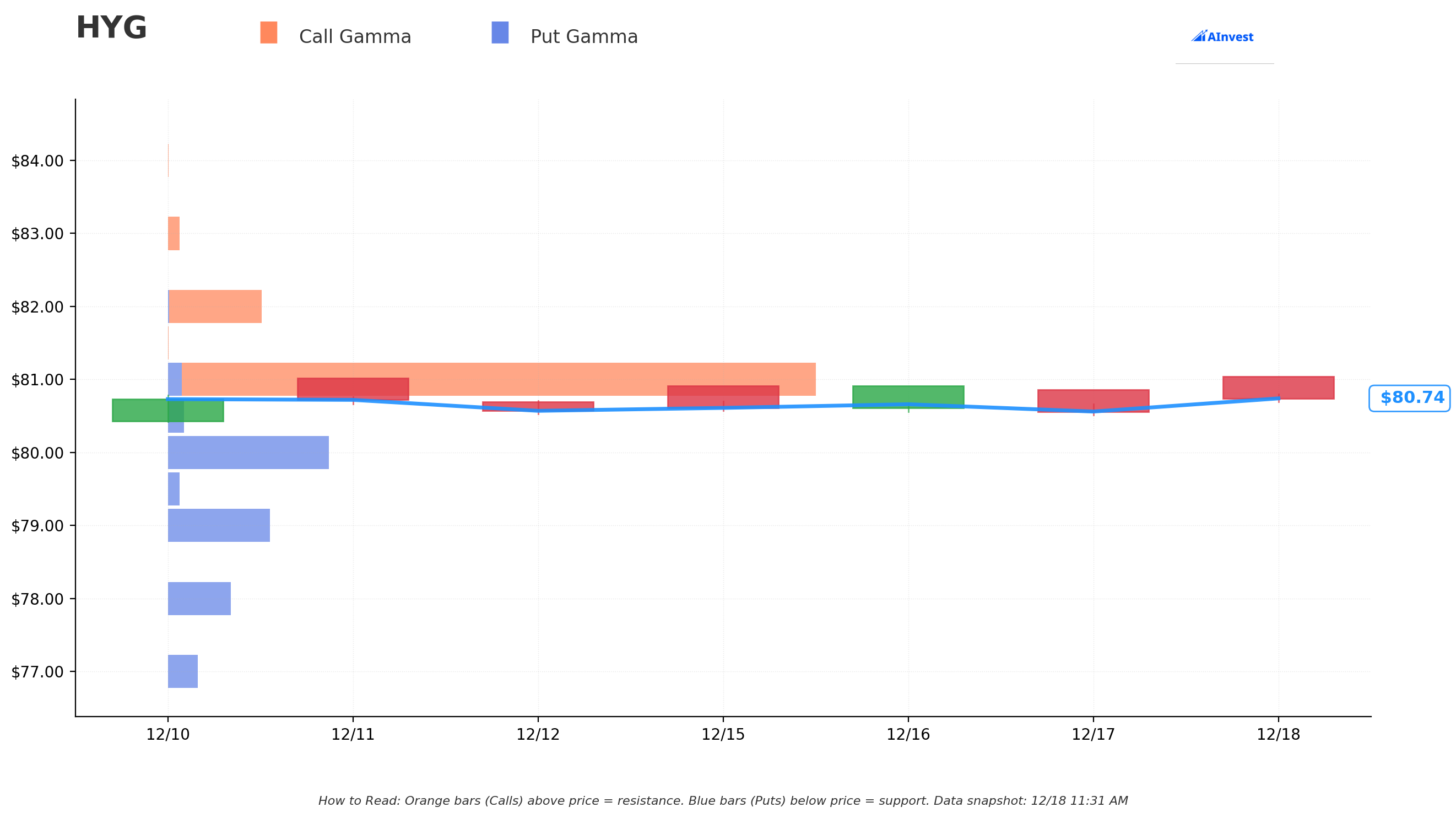

Gamma-Based Support & Resistance Analysis

Current Price: $80.75

The gamma exposure map reveals critical price magnets governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $80.50 - Immediate support with 117.5M put gamma (just 0.3% below current - very tight!)

- $80.00 - MAJOR support with 1.155B put gamma (strongest single level - THE LINE IN THE SAND!)

- $79.50 - Secondary support at 85.6M gamma

- $79.00 - Strong floor with 730.1M gamma (1.5% below current)

- $78.00 - Extended support at 445.2M gamma (3.4% below)

- $77.00 - Deep support with 212.7M gamma (4.6% below)

- $76.00 - Protection strike level with 181.9M gamma (5.9% below - EXACTLY where long puts are struck!)

- $75.00 - Disaster floor at 195.5M gamma (7.1% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $81.00 - Immediate ceiling with MASSIVE 4.545B call gamma (STRONGEST RESISTANCE - dealers will sell rallies!)

- $82.00 - Secondary resistance at 663.8M gamma (1.5% overhead)

What this means for traders: HYG is trading in a VERY TIGHT range between critical $80.00 support (1.155B gamma) and crushing $81.00 resistance (4.545B gamma - the single largest level by far). This creates a natural "pin" effect - market makers will systematically sell into rallies toward $81 and buy dips toward $80.

Notice the genius of this trade structure:

- 💡 The short $80 puts are struck EXACTLY at the strongest gamma support (1.155B) - betting this floor holds

- 💡 The long $76 puts are positioned at 181.9M gamma support - a level that should provide cushion in any selloff

- 💡 The $4 spread width ($80-$76) gives 5.9% downside room from current price - more than the YTD high-to-low range suggests is likely

- 💡 Massive $81 resistance (4.545B gamma) caps upside - trader doesn't need explosive rally, just stability

Net GEX Bias: Bullish (5.307B call gamma vs 3.345B put gamma) - Overall positioning remains constructive, supporting the bull put spread thesis that downside is limited.

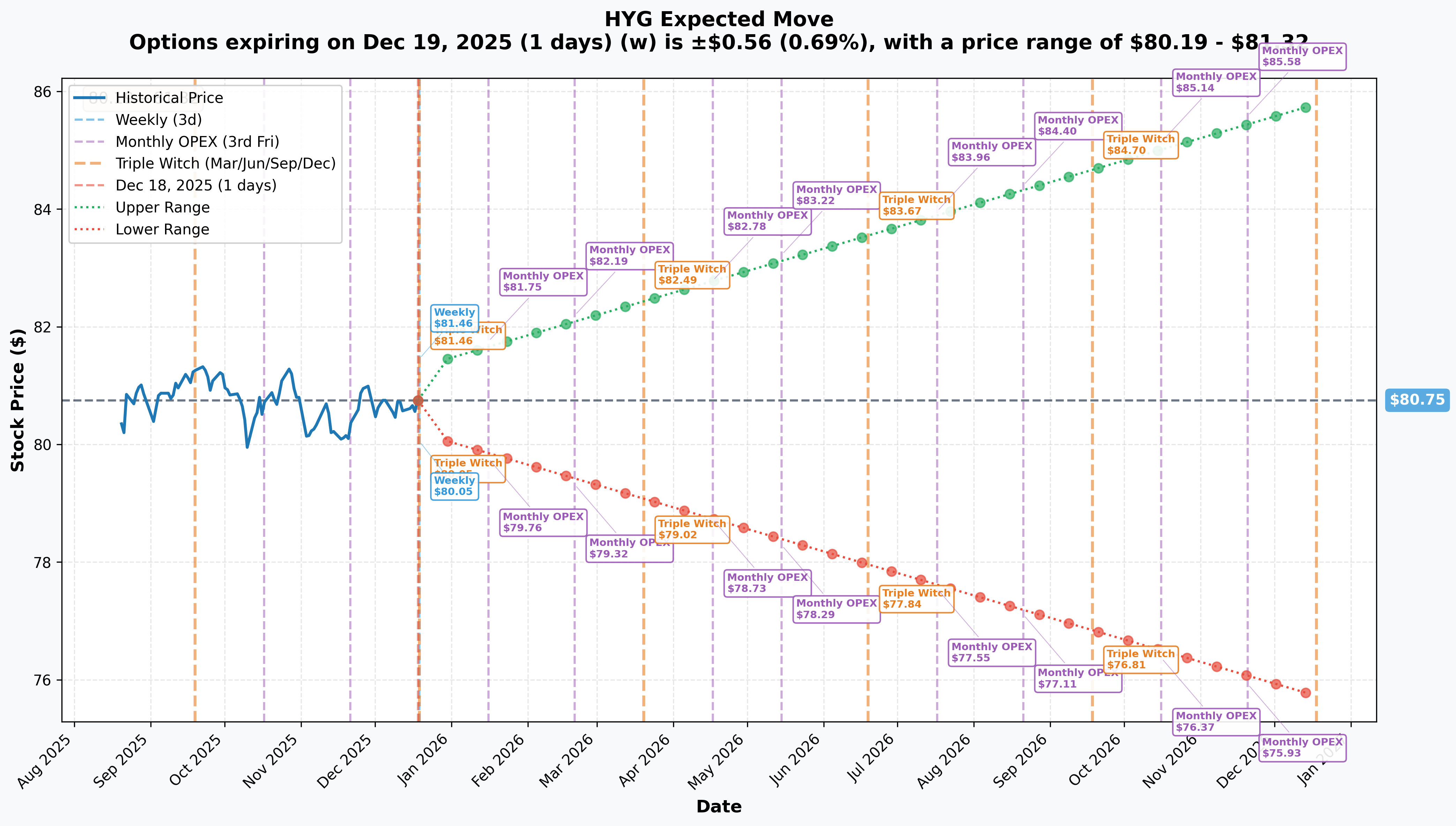

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - Tomorrow!): ±$0.56 (±0.69%) → Range: $80.19 - $81.32

- 📅 Monthly OPEX (Jan 16 - 29 days): ±$0.99 (±1.23%) → Range: $79.76 - $81.75

- 📅 Quarterly Triple Witch (March 20 - 92 days - THIS TRADE!): ±$3.47 (±4.30%) → Range: $77.28 - $84.22

- 📅 Yearly LEAPS (Dec 18, 2026 - 365 days): ±$5.03 (±6.23%) → Range: $75.72 - $85.79

Translation for regular folks: The options market is pricing in MINIMAL near-term volatility - only a 0.69% move ($0.56) by tomorrow and a modest 4.30% move ($3.47) through March expiration. This is EXTREMELY CALM for a high-yield bond ETF, reflecting the market's view that credit spreads should remain stable despite Fed policy uncertainty.

Key insight for the bull put spread: The March implied move of ±$3.47 suggests a lower range of $77.28 - which is above the $76 protection strike but below the $80 short strike. The market is literally pricing in a scenario where:

- There's only a 16% probability HYG trades below $77.28 (1 standard deviation)

- There's only a ~5% probability HYG trades below $76 (where long puts protect)

- The $80 strike sits at the heart of the expected range

This means the trader is selling insurance at $80 (collecting premium) when the market thinks there's a 60%+ probability of staying above that level. The probabilities are IN THEIR FAVOR.

Why the low volatility expectations?

- High-yield spreads at historically tight 310bps provide little room for compression

- Default rates at multi-year lows of 1.5% reduce credit event risk

- 7.5% yields cushion price declines - investors buy dips for income

- Monthly distributions of 5.74% provide carry that offsets modest price weakness

- Fed cutting cycle (even if slower than expected) remains structurally supportive

🎪 Catalysts

🔥 Immediate/Recent Catalysts (Last 7 Days)

Fed Policy Decision - December 18, 2024 (YESTERDAY!) 📊

The Federal Reserve delivered a 25bp rate cut, lowering the target range to 4.25%-4.50%, marking the third consecutive cut for a total 100bp reduction since September. However, the hawkish tone sent shockwaves through markets:

- 📉 Fed projections slashed 2025 rate cut expectations to only two 25bp cuts (down from four projected in September)

- 😰 Equity markets dropped nearly 3% immediately post-announcement; high-yield spreads widened 21bps in December

- ⚖️ One dissent: Cleveland Fed President Beth Hammack preferred holding rates steady

- 🎯 December CPI accelerated to 2.9% YoY (up from 2.7%), reinforcing Fed caution on further cuts

Market Impact on HYG: The hawkish pivot created immediate volatility, but HYG's resilience at $80.66 (near 52-week highs) suggests the market has digested the news. The bull put spread trader is betting this stability continues - that the Fed's "higher for longer" stance doesn't blow out credit spreads from current 310bps levels.

Recent Flow Reversal - November/December 2024

After being among the top five ETFs with largest outflows in 2024, HYG has seen a dramatic reversal:

- 💰 1-month flows: +$2.14B (massive inflow)

- 📈 3-month flows: +$1.57B (sustained institutional buying)

- 🔄 Context: Broader high-yield market saw +$16.4B inflows in 2024 after three consecutive years of -$68B outflows

This flow reversal directly supports the bull thesis - institutions are BUYING HYG at current levels, providing natural bid support at the $80 short strike.

🚀 Near-Term Catalysts (Q1 2026)

January 28-29, 2025 FOMC Meeting (41 DAYS AWAY!) 🇺🇸

The next Fed meeting on January 28-29 is THE critical near-term catalyst for interest rate-sensitive assets like HYG:

- 🎯 Market expects 88% probability of no rate change (pause)

- 📊 Key variables to watch:

- December jobs report and unemployment rate (if above 4.5%, could reopen cut possibility)

- CPI/PCE data for December and January

- Fed Chair Powell's messaging on neutral rate positioning

- 💰 Potential HYG Impact:

- Pause as expected: HYG likely stable in $79-81 range (supports bull put spread thesis)

- Surprise cut: HYG could rally to $82-83 (early profit realization for spread)

- Hawkish surprise (rate hike discussion): HYG could test $78-79 support (pressure on short $80 puts, but likely holds above $76)

Probability assessment: The 88% pause probability suggests minimal volatility risk from this event. The Fed already delivered its hawkish message in December - January is likely "wait and see" mode while monitoring inflation data.

Fallen Angels Wave - Investment Grade Downgrades (Q1-Q2 2025) ✈️

One of the most significant positive catalysts for HYG is the expected $45-55B wave of "fallen angels" (BBB bonds downgraded to high-yield):

- 📊 $387B of BBB- rated debt on negative outlook (highest since 2010 ex-pandemic)

- 🏭 High-profile candidates:

- Boeing ($53.6B bonds outstanding)

- Ford (S&P revised outlook to negative)

- Warner Brothers Discovery

- Multiple BDCs (FS KKR Capital, BlackRock TCP, Oaktree Specialty Lending)

- 💚 Why this is BULLISH for HYG:

- Fallen angels typically deliver +20% excess returns in 12 months post-downgrade

- Higher quality credits entering high-yield market improve average credit profile

- Forced selling by investment-grade-only mandates creates buying opportunities

- HYG mechanically adds these bonds to its holdings, capturing the rebound

- ⏰ Timing: Peak downgrade activity typically Q1-Q2 after year-end financial reporting

This catalyst directly supports the March expiration bull put spread: If fallen angels arrive as expected in Q1, HYG should be stable-to-higher as quality improves, keeping price well above the $80 short strike.

Debt Maturity Wall - Refinancing Wave (2025-2026) 🏗️

A $160B high-yield debt maturity wall hits in 2025, with another $160B in 2026:

- 🎯 Refinancing timing: Issuers typically refinance 12-18 months ahead, meaning late 2025/early 2026 peak activity

- 💰 70%+ of 2025 issuance has been refinancing activity

- 📊 Street projections: $340-410B total issuance in 2026

- ✅ Why this supports HYG:

- Strong refinancing demand keeps spreads tight

- New issuance absorbed easily by market (September 2025 saw record $57B issuance yet spreads tightened)

- Higher interest rates mean increased coupon payments flow to HYG holders

- Only risk: If spreads widen materially, some lower-rated issuers may struggle

Q1 2025 Earnings Season (Mid-January through February) 📈

Corporate earnings releases provide crucial insight into high-yield issuer health:

- 📅 Timing: January 15 - February 15, 2025

- 🎯 Key metrics: Interest coverage ratios, leverage metrics, revenue growth

- ✅ Expected: Corporate fundamentals stabilizing with leverage below historical averages

- ⚠️ Risk: Any meaningful deterioration in interest coverage could pressure spreads (though default rates at 1.5% suggest low probability)

⚠️ Risk Catalysts (Negative)

Persistent Inflation / Fed Policy Error 🔥

The biggest threat to the bull put spread thesis is if inflation reignites, forcing the Fed to hold rates higher or even resume hiking:

- 📊 December 2024 CPI accelerated to 2.9% YoY (up from 2.7%)

- 💰 Tariff impacts expected to add 0.6pp to inflation in 2025, 1.3pp in 2026

- 😰 Precedent: April 2025 saw high-yield spreads jump from 347bps to 461bps on tariff concerns (114bps widening!)

- ⚠️ HYG Impact: If rates stay high, interest coverage ratios compress, defaults rise, and HYG could test $75-76 levels

Spread Compression Limits / Valuation Risk 📉

At 310bps, high-yield spreads are near 2021 lows and approaching the post-GFC floor:

- 📊 Historical context: 20-year median is 454bps; post-GFC range 350-550bps

- ⚠️ Limited upside: Morgan Stanley warns spreads are "priced nearly to perfection" with minimal room for further tightening

- 😰 Widening risk: More likely to see spreads widen back toward 350-400bps than compress to 250-300bps

- 💰 HYG Impact: Spread widening from 310bps to 400bps could drive HYG to $77-78 levels, pressuring the short $80 puts but likely staying above $76 floor

Economic Recession / Credit Crisis ⚡

While recession risks have "waned in the short term" per Northern Trust, a surprise downturn would crater high-yield:

- 📉 Enterprise IT budgets cut first in recession, hitting many high-yield issuers

- 💸 Leveraged loan default rate projected at 7.5% by year-end 2025 (vs 3.4% historical average)

- 😰 Mass downgrades and defaults could push HYG to $70-75 range

- 🛡️ Protection: The long $76 puts cap loss in this scenario

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalysts, here are scenarios through March 20th expiration:

📈 Bull Case (35% probability)

Target: $82-84

How we get there:

- ✅ January Fed meeting delivers dovish pause with Powell opening door to March cut if inflation cooperates

- 💚 Fallen angels wave arrives ($45-55B) with smooth absorption and minimal spread widening

- 📈 Q1 earnings show interest coverage ratios stable/improving - no credit deterioration

- 🎯 December/January inflation data comes in cooler than expected (2.5-2.7% range)

- 💰 Continued strong inflows (following recent $2.14B monthly pattern) provide bid support

- 🔄 Spreads compress 10-20bps from 310bps to 290-300bps on improving sentiment

- 📊 Break above $81 gamma resistance triggers technical rally to $82-84 range

Bull put spread P&L:

- MAXIMUM PROFIT: Collect full $2.8M credit (short puts expire worthless, long puts expire worthless)

- Profit realized at any price above $80 at March 20 expiration

- Return on capital: 61% return on the $4 width spread ($2.8M profit on $4.6M risk)

Probability assessment: 35% because it requires multiple positives aligning. While fundamentals are constructive (1.5% default rate, fallen angels adding quality), the hawkish Fed pivot and tight 310bps spreads limit upside. Most likely scenario is stability, not explosive rally.

🎯 Base Case (50% probability)

Target: $78-81 range (SIDEWAYS CONSOLIDATION)

Most likely scenario:

- ⚖️ January Fed meeting delivers expected pause with balanced language (88% probability already priced)

- 📊 Spreads remain rangebound 300-320bps - neither widening materially nor compressing

- 💰 Fallen angels arrive gradually without disrupting market - absorbed smoothly by demand

- ✅ Q1 earnings solid but unspectacular - no major upgrades or downgrades

- 🎯 Inflation data mixed - not hot enough to scare Fed into hikes, not cool enough for aggressive cuts

- 💵 HYG trades in tight $78-81 range, respecting $80 gamma support and $81 resistance

- 📈 Monthly 5.74% distributions provide 1.4% return over 3-month period (annualized cushion)

- 🔄 Volatility remains subdued with ±4.3% implied move proving accurate

Bull put spread P&L:

- MAXIMUM PROFIT: Collect full $2.8M credit if HYG stays above $80

- Even if HYG drops to $78-79, short puts still profitable (intrinsic value $1-2, net profit $1.8-0.8M)

- Only risk zone: $76-80 range where losses begin to mount

Why 50% probability: This is exactly what the implied move suggests - trading in a tight range with minimal volatility. The 1.155B gamma support at $80 and 4.545B resistance at $81 create natural boundaries. 7.5% absolute yields and 5.74% distributions cushion downside. Most institutions simply clip coupons and wait.

📉 Bear Case (15% probability)

Target: $75-77 (TEST THE LONG PUT PROTECTION!)

What could go wrong:

- 😰 Inflation reaccelerates meaningfully (3.2%+ CPI) - Fed discusses pausing cuts indefinitely or hiking

- 🚨 Unexpected credit event - major high-yield issuer defaults or files bankruptcy (e.g., Boeing downgrade materializes)

- 💔 Spreads widen aggressively from 310bps to 400-450bps on credit concerns

- 📉 Broader market selloff (equity crash) drags high-yield bonds down in risk-off move

- 🇨🇳 Tariff war escalates (repeat of April 2025 when spreads widened 114bps)

- ⚡ Recession fears resurface - unemployment jumps above 4.5%, GDP growth stalls

- 💸 Mass fallen angel downgrades overwhelm market absorption capacity

- 🔨 Break below $78 gamma support triggers cascade to $76, then $75

Bull put spread P&L at different levels:

- HYG at $79 at expiration: Short puts worth $1, loss $1.8M but still profitable overall (+$1.0M net)

- HYG at $78 at expiration: Short puts worth $2, loss $3.2M, net position -$0.4M (small loss)

- HYG at $77 at expiration: Short puts worth $3, loss $4.6M, net position -$1.8M

- HYG at $76 or below: MAXIMUM LOSS $17.2M (long puts cap loss at $4 spread width minus $0.56 credit)

Critical support levels:

- 🛡️ $80.00: Major gamma floor (1.155B) - short strike, MUST HOLD

- 🛡️ $78.00: Extended support (445.2M gamma) - still profitable zone

- 🛡️ $76.00: Long put protection strike (181.9M gamma) - loss capped below here

Probability assessment: Only 15% because it requires a major negative catalyst that current data doesn't support. Default rates at 1.5% multi-year lows, fallen angels historically positive for returns, and recent $2.14B inflows suggest institutional support. Even the hawkish Fed pivot yesterday didn't break HYG below $80. The 5.9% cushion to the $76 protection strike is significant.

Worst case protection: The long $76 puts cap maximum loss at $17.2M even if HYG crashes to $70 or lower - this is sophisticated risk management.

💡 Trading Ideas

🛡️ Conservative: Buy HYG for Income, Skip the Options

Play: Buy HYG shares at $80.50-$81.00, collect 5.74% monthly distributions

Why this works:

- 💰 Reliable income: 5.74% distribution yield paid monthly ($0.38/share) provides steady cash flow

- 📊 Quality improvement: $45-55B fallen angel wave should add higher-quality BBB/BB credits to portfolio

- 🛡️ Downside protection: 1.5% default rate at multi-year lows limits credit risk

- 📈 Flow support: Recent $2.14B monthly inflows provide natural bid, reversing earlier 2024 outflows

- ⏰ No timing risk: Unlike options, shares don't expire - can hold through volatility

- 🎯 Gamma support: 1.155B gamma at $80 creates strong floor for entries

Position sizing:

- Allocate 5-10% of fixed income allocation to high-yield exposure

- Average down if HYG dips to $78-79 range (adds to yield)

- Reinvest monthly distributions or take as cash flow

Expected outcome: Collect 5.74% annually (1.4% over 3 months) while waiting for fallen angels to add quality and Fed to resume cutting in H2 2025.

Risk level: Low-Moderate (bond fund volatility, but income cushions) | Skill level: Beginner-friendly

⚖️ Balanced: Small Bull Put Spread (Copy The Pros at Scale)

Play: Sell 5-10 bull put spreads mirroring institutional positioning

Structure: Sell $80 puts, Buy $76 puts (March 20, 2026 expiration - SAME as the $5.6M trade)

Why this works:

- 🤝 Copy smart money: Institutions deployed $5.6M on this exact structure - retail can scale down proportionally

- 💰 Defined risk: $4 wide spread = $400 max risk per spread, $56 credit per spread (14% ROI on risk)

- 🎯 High probability: 61% chance of maximum profit built into pricing (HYG needs to stay above $80)

- 📊 Gamma support: 1.155B gamma at $80 strike creates strong technical floor

- ⏰ Theta decay: Collect time decay daily over 92 days to expiration

- 🛡️ Protection below $76: Long puts cap losses if credit crisis materializes

Estimated P&L per spread:

- 💰 Collect: $0.56 credit per share = $56 per spread

- 📈 Max profit: $56 if HYG above $80 at expiration (14% ROI)

- 📉 Max loss: $344 if HYG below $76 at expiration

- 🎯 Breakeven: $79.44 (HYG can drop 1.6% and still breakeven)

- ⚖️ Risk/Reward: 1:6.1 ($344 risk for $56 profit) - typical for high-probability income strategy

Entry timing:

- ✅ Enter NOW if comfortable with immediate exposure

- ⏰ OR wait for any pullback to $79.50-$80.00 for slightly better entry (collect more premium)

Position sizing:

- Sell 5 spreads = $280 premium collected, $2,000 max risk (appropriate for $20K-40K account)

- Sell 10 spreads = $560 premium collected, $4,000 max risk (appropriate for $40K-80K account)

- Never risk more than 5-10% of portfolio on single options position

Management:

- 🎯 Close early at 50% profit ($28/spread) if HYG rallies to $81+ in January

- ⚠️ Consider rolling down ($80/$76 → $78/$74) if HYG breaks $78 in mid-February

- 📉 Accept maximum loss if HYG crashes below $76 (don't chase - let protection work)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Leveraged Bull Put Spread Pyramid (ADVANCED ONLY!)

Play: Sell larger bull put spread position with scaling at different strikes

Structure:

- Sell 20 contracts $81 puts, Buy 20 contracts $77 puts (higher credit, wider strikes)

- Sell 30 contracts $80 puts, Buy 30 contracts $76 puts (core position)

- Total: 50 spreads pyramided at different levels

Why this could work:

- 💰 Maximize income: Collect $1.20+ per share on $81/$77 spreads (30% ROI on risk) + $0.56 on $80/$76 spreads

- 🎯 Multiple profit zones: Profit at different HYG price levels - not all-or-nothing

- 📊 Scale risk: Heavier weighting at lower strike ($80) where gamma support strongest

- ⚡ Theta acceleration: Larger position means faster premium collection as expiration approaches

- 🎪 Catalyst rich: January Fed, fallen angels, refinancing wave all support thesis

Why this could blow up (SERIOUS RISKS):

- 💸 LARGE CAPITAL REQUIREMENT: $20K+ margin requirement for 50 spreads

- 😰 CONCENTRATION RISK: Heavily exposed to single ETF / sector (credit)

- ⚡ Black swan vulnerability: Unexpected credit event or recession could trigger max loss on all spreads simultaneously

- 📉 Limited recovery: Unlike long shares, short puts can't "hold through" adversity - they expire worthless

- 🎢 Margin calls possible: If HYG drops to $77-78, broker may require additional margin

- ⚠️ Need to be RIGHT on timing (March expiration) AND direction (no drop below $80) AND magnitude (stay above strikes)

Estimated P&L:

- 💰 Total credit collected: ~$3,000-4,000 across all spreads

- 📈 Max profit: $3,000-4,000 if HYG above $81 at expiration (15-20% ROI)

- 📉 Partial profit: $1,500-2,500 if HYG at $78-80 (some spreads profit, some lose)

- 💀 Max loss: $16,000-20,000 if HYG below $76 (all spreads at max loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have $50K+ trading account (don't risk >30% on one position)

- ✅ Fully understand margin requirements and assignment risk

- ✅ Can withstand $15K-20K loss without devastating portfolio

- ✅ Have traded vertical spreads through expiration before

- ✅ Accept that even small probability (15%) black swan events DO happen

- ⏰ Can actively manage position - not set-and-forget

- 📊 Understand bond market dynamics and credit spread movements

Risk level: EXTREME (can lose $15K-20K) | Skill level: Advanced only

Probability of profit: ~60-65% (better than coin flip, but not guaranteed)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🔥 Fed policy whipsaw - January 28-29 FOMC: While 88% probability of pause is priced in, the Fed just delivered a hawkish surprise yesterday (only two 2025 cuts vs four expected). If inflation remains sticky at 2.9% or accelerates, Powell could signal even fewer cuts or pause indefinitely. High-yield bonds are EXTREMELY rate-sensitive - a hawkish shift could drive HYG from $80 to $76-77 quickly as spreads widen. The short $80 puts would be in-the-money and facing assignment.

-

💥 Spread widening from historically tight levels: At 310bps, spreads are just 10bps from 2021 lows when they sat at ~300bps. Morgan Stanley warns spreads are "priced nearly to perfection" with FAR more room to widen (back to 400-450bps historical range) than compress. Even a modest 50bps widening to 360bps could push HYG to $77-78. A 100bps+ widening (like April 2025's 114bps spike) would crater HYG below $75, triggering max loss on both legs.

-

🇺🇸 Trump tariff/policy uncertainty: April 2025 precedent is terrifying - spreads exploded from 347bps to 461bps (114bps) on tariff announcement before emergency pause. With Trump administration expected to implement more tariffs in Q1 2025, policy whiplash creates unpredictable risk. Tariffs projected to add 0.6-1.3pp to inflation, which pressures Fed and credit spreads. Headline risk can gap HYG down 3-5% overnight.

-

✈️ Fallen angel downgrade tsunami: While $45-55B in fallen angels should be positive long-term, the TIMING and MAGNITUDE matter. If $387B of at-risk BBB- credits all get downgraded simultaneously in Q1 (mass downgrade event), the market may not absorb supply smoothly. Boeing alone represents $53.6B - its downgrade could flood the market. Temporary spread widening during transition period could push HYG to $76-78 even if long-term bullish.

-

💔 Single issuer credit event: HYG holds 1,331 bonds - a major default or bankruptcy (DISH Network is a top holding, Ford is at risk, Warner Bros Discovery struggling) could spark contagion fears. While default rates are at 1.5% lows now, high-profile blow-up creates ripple effects. Remember: leveraged loan default rate projected at 7.5% by year-end 2025 - much higher than current levels.

-

🏦 Refinancing wall execution risk: The $160B maturity wall in 2025 means lower-rated issuers (CCC) MUST refinance at MUCH higher rates than their existing debt. Some may not be able to access markets if spreads widen or credit deteriorates. Failed refinancings → defaults → spread widening → HYG price decline. While 70%+ of issuance is refinancing successfully so far, Q1 2026 peak could strain system.

-

💸 Private credit competition draining quality supply: 86% of new LBO financing now comes from private credit (direct lending) vs public high-yield market. This means public high-yield is seeing LESS attractive new issuance (best credits go private) while inheriting MORE troubled situations. HYG's average credit quality could deteriorate even as fallen angels arrive, if the best credits exit to private markets.

-

⚡ Recession scenario - rapid deterioration: While recession risk has "waned in short term", economic indicators can turn quickly. Labor market showing stress (unemployment above 4.5% would concern Fed), corporate earnings slowing, consumer spending weakening. In recession, high-yield gets CRUSHED - spreads can widen 200-300bps in weeks, driving HYG to $70-72 range. March expiration gives time for recession to materialize if economy rolling over.

-

🎯 Assignment risk on short $80 puts: If HYG trades below $80 approaching expiration, the short puts face early assignment risk. This means forced purchase of 5,000 shares per contract at $80 (for 50K contract position = $400M notional!). Requires MASSIVE margin or capital. Most retail traders cannot handle assignment - must close position before expiration if in-the-money.

-

📊 Gamma pin risk at $80-81 creates false security: While 1.155B gamma at $80 and 4.545B at $81 suggest tight range, these levels are DYNAMIC and change daily. A catalyst (credit event, Fed shock, tariff announcement) can BREAK through gamma levels with explosive moves. Gamma works UNTIL it doesn't - then moves are violent. Don't assume $80 floor is impenetrable.

-

💰 Opportunity cost in rangebound market: If base case ($78-81 range) materializes, the 14% ROI on the bull put spread over 3 months (56% annualized) is attractive BUT: HYG shares would deliver 5.74% yield (1.4% over 3 months) with NO risk of max loss. The incremental 12.6% return requires taking 5:1 downside risk ($17.2M max loss vs $2.8M profit). Is the juice worth the squeeze?

🎯 The Bottom Line

Real talk: A sophisticated institution just risked $17.2M to collect $2.8M betting HYG stays above $80 through March 20, 2026. This bull put spread is a BULLISH income strategy, not a hedge - they're explicitly betting on credit market stability despite yesterday's hawkish Fed pivot.

What this trade tells us:

- 🎯 Smart money believes high-yield spreads will NOT blow out from current 310bps levels (expecting range of 300-350bps max)

- 💰 They're comfortable the $80 floor (with 1.155B gamma support) will hold through Q1 catalysts

- ⚖️ The 5.9% cushion to $76 protection strike suggests they see 15% downside scenario as low probability

- 📊 Timing signals confidence: positioned one day AFTER Fed hawkish surprise - they've seen worst-case Fed reaction

- ⏰ March expiration captures January Fed meeting, fallen angel wave, and Q1 earnings - betting these are net positive/neutral

This IS a "bullish on credit" signal - but it's measured optimism, not euphoria.

If you own HYG:

- ✅ Continue holding for 5.74% monthly income - fundamentals remain supportive (1.5% defaults, $2.14B inflows)

- 🎯 Consider trimming 10-20% if HYG rallies to $82-83 (take some profits near 52-week high)

- ⏰ Set MENTAL STOP at $78 (below strong gamma support zones) to protect principal

- 💰 Reinvest monthly distributions to compound or take as income stream

- 🛡️ Don't panic if HYG dips to $79.50 - fallen angels arriving should support

If you're watching from sidelines:

- 🎯 Current levels ($80.50-81.00) offer attractive 5.74% yield with institutional buying support

- 💚 Wait for any dip to $79-79.50 for better entry with higher yield-to-price ratio

- 📅 January 28-29 Fed meeting is key risk event - consider entering AFTER if no surprises

- 📊 For options traders: Small bull put spreads (5-10 contracts) offer defined-risk way to generate income if bullish

- ⏰ Don't chase - HYG is rangebound, better entries will come

If you're bearish on credit:

- ⚠️ This institutional bull put spread suggests credit markets are more stable than bears expect

- 📊 Consider waiting for spread widening catalyst (inflation spike, credit event) before shorting

- 🎯 Bear put spreads ($78/$74 or $76/$72) offer defined-risk bearish plays if conviction strong

- ⏰ Don't fight the $80 gamma floor (1.155B) and $2.14B monthly inflows - time your entry after break

Mark your calendar - Key dates:

- 📅 December 19 (Tomorrow) - Weekly/Monthly/Quarterly OPEX (implied move ±0.69%)

- 📅 January 15-February 15 - Q1 2025 earnings season (interest coverage ratios critical)

- 📅 January 28-29, 2025 - FOMC meeting (88% pause probability, watch for language shifts)

- 📅 Q1 2025 - $45-55B fallen angel wave expected (Boeing, Ford, Warner Bros potential)

- 📅 Late Q1/Early Q2 2025 - $160B refinancing wave peak

- 📅 March 20, 2026 - Expiration of this $5.6M bull put spread

Final verdict: HYG's fundamental story is SOLID - 1.5% default rates at multi-year lows, fallen angels adding quality, 7.5% absolute yields providing cushion, and $2.14B monthly inflows reversing earlier 2024 exodus. BUT, spreads at 310bps leave minimal compression room and Fed's hawkish pivot creates uncertainty. The $5.6M bull put spread suggests professional money expects STABILITY, not explosive moves.

For retail investors: Buy HYG shares for income (5.74% yield) if comfortable with modest volatility. For options traders: Small bull put spreads (5-10 contracts) at $80/$76 strikes copy this institutional trade at retail scale - collect income while defined risk protects downside.

This is a "clip coupons and be patient" environment. Don't expect fireworks, but don't fear catastrophe either. The pros are positioning for boring stability - and sometimes boring is beautiful. 💰

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Bull put spreads have defined maximum loss ($17.2M in this case for 50K contracts), but that loss is REAL and can be total. The Z-scores of 3.83 and 10.01 reflect extreme unusual size relative to recent history - it does not guarantee profitability. High-yield bonds carry credit risk, interest rate risk, and can lose principal value. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading. The institutional trader may have complex portfolio hedging needs, risk tolerance, and capital requirements not applicable to retail traders.

About iShares iBoxx $ High Yield Corporate Bond ETF (HYG): Launched November 6, 2008, HYG is the largest high-yield corporate bond ETF with $20.35 billion in assets, providing exposure to 1,331 U.S. dollar-denominated junk bonds. The fund pays monthly distributions yielding 5.74% and trades on the Archipelago Exchange (ARCX) with an expense ratio of 0.49%.