IWM $18.2M Bear Put Spread - Institutions Hedge Small-Cap Rally at All-Time Highs!

January 15, 2026 | Unusual Activity Detected

The Quick Take

Someone just deployed $18.2 MILLION in a coordinated bear put spread on IWM this morning at 10:59:21! This massive 4-leg trade bought $253 strike puts while selling $250 strike puts - a classic bearish structure betting on the Russell 2000 pulling back to the $250-253 range by February 20th. With IWM hitting fresh 52-week highs at $266.93 and the "Great Rotation" into small caps in full swing (+6.1% YTD), smart money is positioning for a potential pullback before the January FOMC meeting. Translation: Big players are betting the small-cap rally needs to catch its breath!

ETF Overview

iShares Russell 2000 ETF (IWM) is the most liquid and widely-traded small-cap ETF, tracking the Russell 2000 Index:

- AUM: $76.05 billion

- Expense Ratio: 0.19%

- Index: Russell 2000 (2,000 smallest companies in Russell 3000 Index)

- Current Price: $266.53 (near 52-week high of $266.93)

- 52-Week Low: $171.73 (April 7, 2025)

- YTD Performance: +6.11% (outpacing S&P 500's +1.8%)

- 1-Year Total Return: +22.60% including dividends

- Dividend Yield: 0.96% ($2.55 annual)

What is the Russell 2000? The Russell 2000 Index measures the performance of approximately 2,000 small-cap companies in the United States, representing roughly 10% of the total U.S. equity market capitalization. Unlike the mega-cap dominated S&P 500, the Russell 2000 provides exposure to domestically-focused companies across diverse sectors including financials, healthcare, industrials, and technology - making it a key barometer for the broader U.S. economy and small business health.

The Option Flow Breakdown

What Just Happened

The Tape (January 15, 2026 @ 10:59:21) - 4 Coordinated Legs:

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Z-Score | Vol/OI Ratio |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:59:21 | IWM | BID | SELL | PUT $250 | 2026-02-20 | $4.6M | $250 | 58K | 9.5K | 7.51 | 6.1x |

| 10:59:21 | IWM | ASK | BUY | PUT $253 | 2026-02-20 | $5.9M | $253 | 53K | 5K | 49.27 | 10.6x |

| 10:59:21 | IWM | ASK | BUY | PUT $253 | 2026-02-20 | $4.3M | $253 | 23K | 5K | 21.04 | 4.6x |

| 10:59:21 | IWM | BID | SELL | PUT $250 | 2026-02-20 | $3.4M | $250 | 28K | 9.5K | 3.50 | 2.9x |

Total Premium: ~$18.2M combined activity

What This Actually Means

This is a BEAR PUT SPREAD - a defined-risk bearish strategy! Here's the breakdown:

- Long leg: Bought 76,000 contracts of $253 puts ($10.2M premium paid)

- Short leg: Sold 86,000 contracts of $250 puts ($8.0M premium received)

- Net debit: Approximately $2.2M net cost for the spread structure

- Max profit zone: IWM below $250 by February 20th expiration

- Target pullback: 5-6% decline from current $266.53 to $250-253 range

- Expiration timing: 36 days, capturing January 27-28 FOMC meeting and Q4 earnings season

Why a bear put spread? This trader is NOT betting on a crash - they're positioning for a measured pullback to specific gamma support levels. By selling the $250 puts against their $253 long puts, they cap their profit but dramatically reduce their cost basis. This is classic institutional risk management: defined risk, defined reward, specific price target.

Unusual Score: EXTREMELY UNUSUAL - The $253 put leg registered a Z-score of 49.27, meaning this volume is roughly 49 standard deviations above average. The Vol/OI ratio of 10.6x indicates opening new positions, not closing existing ones. This level of activity happens maybe a handful of times per year on IWM.

Technical Setup / Chart Check-Up

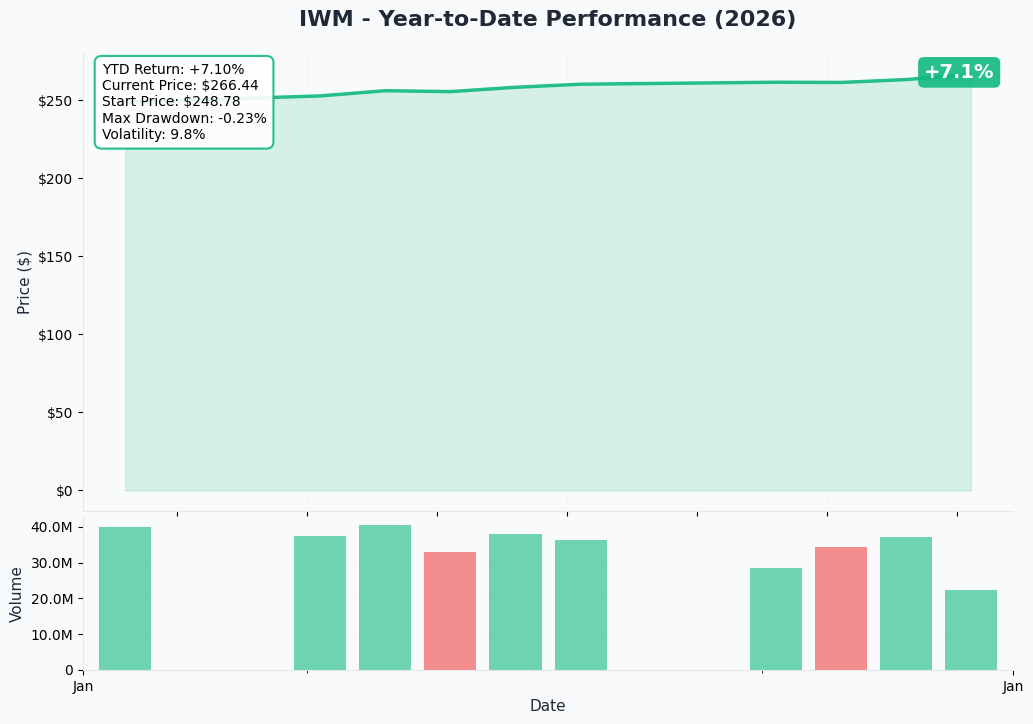

YTD Performance Chart

IWM is crushing it in early 2026 - up +6.11% YTD and leading all major indices. The Russell 2000 broke out to new all-time highs on January 8, 2026, and hasn't looked back. This "Great Rotation" from mega-cap tech to small caps represents a potential regime change in market leadership after 15 years of large-cap dominance.

Key observations:

- Breakout above 2,500 index level (psychologically significant barrier) confirmed

- 50-day moving average ($248.23) providing strong trend support

- 200-day moving average ($238.86) well below - clear uptrend established

- RSI at 71.6 indicates overbought conditions - near-term consolidation likely

- Volume elevated at 36.49M shares on January 14th showing institutional participation

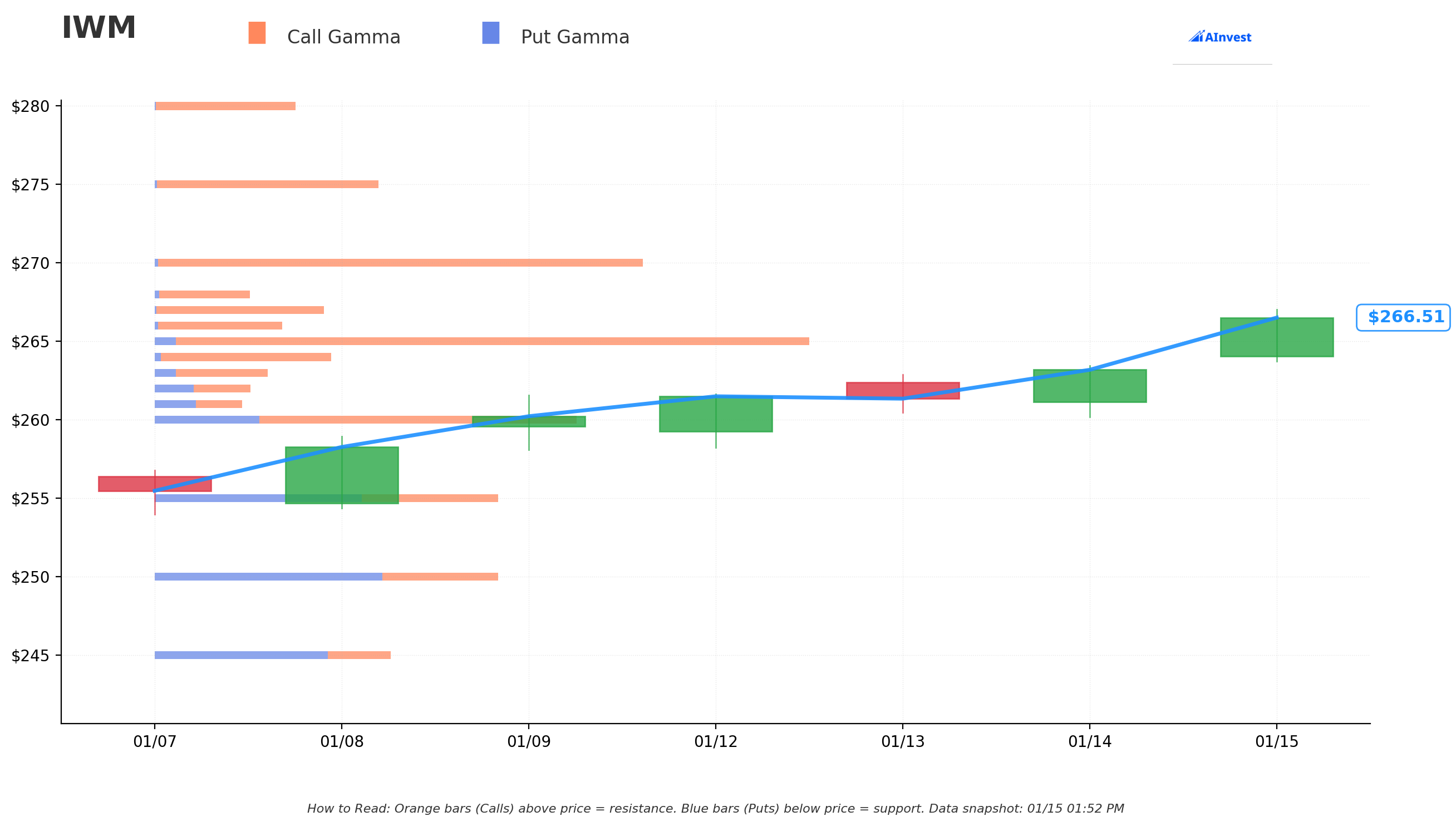

Gamma-Based Support & Resistance Analysis

Current Price: $266.53

The gamma exposure map reveals critical price magnets that could govern near-term price action:

Support Levels (Put Gamma Below Price):

- $265 - Immediate support with 202.4B total gamma (strongest nearby floor!)

- $264 - Secondary support at 54.7B gamma

- $260 - Major structural floor with 131.9B gamma (this is the first LINE IN THE SAND)

- $255 - Deep support at 106.3B gamma

- $250 - Extended support at 106.2B gamma (THE PUT SPREAD TARGET!)

- $245 - Disaster scenario floor at 72.6B gamma

- $240 - Extreme downside at 68.4B gamma

Resistance Levels (Call Gamma Above Price):

- $267 - Immediate ceiling with 51.4B gamma (just above current price!)

- $270 - Major resistance at 148.6B gamma (STRONGEST RESISTANCE - 1.3% overhead)

- $275 - Extended ceiling at 68.3B gamma (3.2% above current)

What this means for traders: IWM is trading RIGHT at immediate support ($265) with massive resistance at $270. The gamma data shows market makers holding enormous positions at $270 which creates natural selling pressure as price approaches. Notice the put spread is targeting exactly the $250-253 zone where significant gamma support exists - the trader expects that IF IWM pulls back, it gravitates to this high-gamma area where dealer hedging creates price stickiness.

Net GEX Bias: Bullish (1,109B call gamma vs 669B put gamma) - Overall positioning remains bullish, but the overbought technical condition and overhead resistance at $270 suggest consolidation before any further advance.

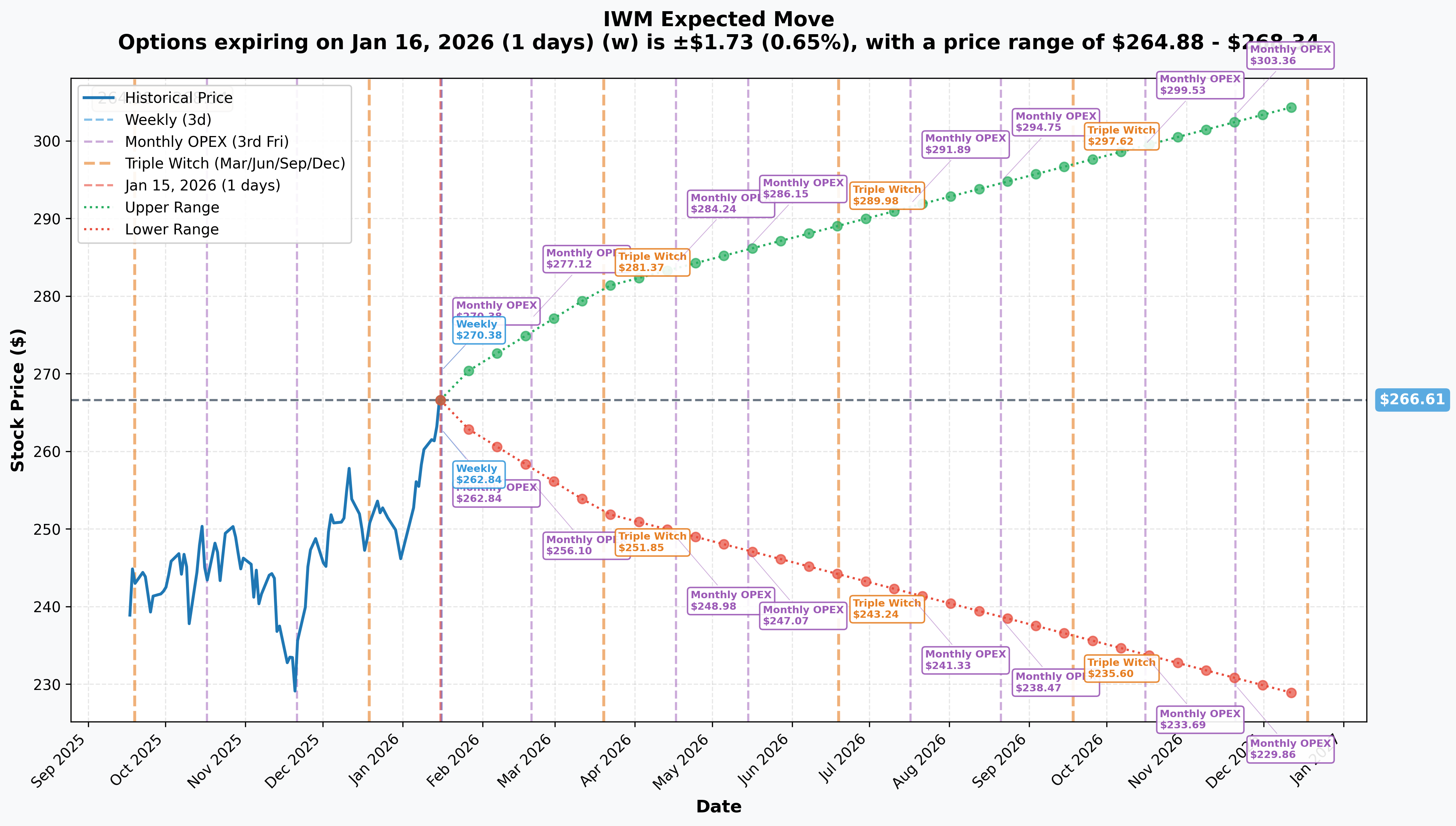

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 1 day): 0.65% ($1.73) - Range: $264.88 - $268.34

- February Monthly OPEX (Feb 20 - THIS TRADE!): 3.95% ($10.51) - Range: $256.10 - $277.12

- Quarterly Triple Witch (Mar 20): 5.47% ($14.59) - Range: $252.02 - $281.20

- Yearly LEAPS (Dec 18): 14.37% ($38.31) - Range: $228.30 - $304.92

Translation for regular folks: The options market expects IWM to move roughly 4% by February 20th (when this put spread expires). That means the market-implied range is $256.10 to $277.12. The put spread's $250-253 target sits BELOW the implied lower range - suggesting this trader believes the market is underpricing downside risk. They're betting on a 5-6% pullback when the market is only pricing in 4%.

Key insight: The February OPEX lower bound of $256.10 sits right at major gamma support. If IWM breaks that level, the cascade to $250-253 becomes much more likely - exactly what this put spread needs to profit.

Catalysts

Upcoming Catalysts (Next 36 Days)

FOMC Meeting - January 27-28, 2026 (12 DAYS AWAY!)

The Federal Reserve is expected to hold rates steady at 3.50-3.75% according to NPR. Key dynamics:

- Futures markets show only 16% odds of a cut in January per Morningstar UK

- Minneapolis Fed President Kashkari stated it was "just way too soon" to cut rates in January per Yahoo Finance

- Philadelphia Fed President Paulson sees room for modest cuts "later this year" per Bloomberg

- Morgan Stanley now projects one rate cut in June and another in September

Why this matters for the trade: Small caps are highly sensitive to interest rates - approximately 41% of Russell 2000 companies rely on floating-rate debt per Janus Henderson. If the FOMC signals a more hawkish stance than expected, small caps could sell off sharply.

Q4 2025 Earnings Season (Late January - February 2026)

Russell 2000 constituents begin reporting Q4 results in late January. According to Financial Content:

- Consensus forecasts project 5-7% earnings growth for small caps in Q1 2026

- Small-cap earnings growth for full-year 2026 projected at 17-22% per AInvest

- Approximately 40% of Russell 2000 remains unprofitable - quality divide emerging

February CPI Release - February 11, 2026

The Consumer Price Index for January 2026 per BLS will be critical for Fed policy expectations. December 2025 CPI showed core inflation at 2.6% annually (above Fed's 2% target) per CNBC.

Recent Catalysts (Last 30 Days)

Russell 2000 All-Time High - January 8, 2026

The Russell 2000 surged to a new record high at 2,603.90 with a 1.4% daily gain per Financial Content. This breakout above 2,500 signaled potential regime change in market leadership.

December CPI Relief - January 13, 2026

The cooler-than-expected inflation reading (core CPI 2.6% vs 2.7% expected) provided support for the small-cap rally per CNBC.

Temporary Setback - January 7, 2026

The Russell 2000 plunged 2.4% - its worst single-day performance in months - on sticky inflation fears per Financial Content. This proved temporary but shows how quickly sentiment can shift.

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20th expiration:

Bull Case (30% probability)

Target: $275-$285

How we get there:

- FOMC meeting on January 27-28 signals dovish surprise, rate cut hints for March

- Q4 earnings from Russell 2000 constituents beat expectations, margins expand

- Continued rotation from mega-cap tech into small caps accelerates

- Breakout above $270 gamma resistance triggers technical rally to implied upper range ($277-281)

- "Great Rotation" thesis validated by fund flows turning strongly positive

Put spread outcome: Total loss of ~$2.2M net debit (spread expires worthless)

Base Case (45% probability)

Target: $258-$270 range (CONSOLIDATION)

Most likely scenario:

- FOMC holds steady as expected, no major surprises either direction

- Small-cap earnings mixed - some beats, some misses, average performance

- IWM consolidates between gamma support ($260-265) and resistance ($267-270)

- February CPI comes in roughly in-line, maintaining status quo on rate expectations

- RSI cools from overbought 71.6 to neutral 50-60 range over 5-6 weeks

- Volatility compression post-January FOMC reduces option premiums

Put spread outcome: Partial loss to breakeven (~$253 breakeven level not reached)

Bear Case (25% probability)

Target: $250-$258 (PUT SPREAD PROFITS!)

What triggers the pullback:

- FOMC meeting delivers hawkish surprise - "higher for longer" rhetoric returns

- Sticky inflation data in February CPI report crushes rate cut hopes

- Q4 earnings disappoint - 40% unprofitable Russell 2000 companies struggle with refinancing

- Supreme Court tariff ruling creates uncertainty, risk-off sentiment per Bloomberg

- Break below $260 gamma support triggers cascade selling to $250-255 zone

- "2026 Refinancing Wall" fears resurface - $225B high-yield refinancing per PitchBook

- RSI divergence from overbought levels confirms momentum reversal

Put spread outcome:

- IWM at $252: Spread worth ~$1 ($3 width minus losses) - modest profit

- IWM at $250: Spread worth $3 (max profit) - ~$2.6M gross profit minus $2.2M cost = ~$400K net gain

- IWM below $250: Max profit locked in at ~$400K (capped by short $250 put)

Trading Ideas

Conservative: Stay Patient, Wait for Pullback Entry

Play: Stay on sidelines until IWM pulls back to gamma support levels

Why this works:

- RSI at 71.6 is overbought territory - historical pattern suggests 5-10% pullbacks from these levels

- IWM already up 6.1% YTD in just 2 weeks - strong gains already captured by early movers

- FOMC meeting in 12 days creates binary event risk - better entry likely after volatility spike

- Gamma support at $260-265 provides logical entry zone with defined stop below $255

- The $18M put spread signals smart money expects consolidation - why fight that?

Action plan:

- Set alerts for $260-262 zone (first pullback target, 5-day SMA support)

- If FOMC delivers hawkish surprise, look for $255-258 entry with stop at $250

- Target position size: Use pullback to build 50% position, add on further weakness to $255

- Long-term thesis remains intact: Small caps offer 31% valuation discount to S&P 500 per Benzinga

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Copy the Put Spread Structure (Smaller Size)

Play: Enter similar bear put spread structure after FOMC for defined-risk downside exposure

Structure: Buy IWM $260 puts / Sell IWM $255 puts (February 20 expiration)

Why this works:

- Mirrors institutional positioning but at levels closer to current price

- $5-wide spread = $500 max risk per spread (defined and manageable)

- Captures potential post-FOMC volatility spike

- February expiration captures both FOMC (Jan 27-28) and February CPI (Feb 11)

- Gamma support at $260 and $255 provides logical strike selection

Estimated P&L:

- Cost: ~$1.50-2.00 per spread (adjust based on post-FOMC IV)

- Max profit: $3.00-3.50 if IWM below $255 at expiration

- Max loss: $1.50-2.00 (limited to debit paid)

- Breakeven: ~$258

- Risk/Reward: ~1:1.5 to 1:2

Entry timing:

- Wait for FOMC meeting outcome (January 28)

- Enter if IWM trades $263-267 range with elevated IV

- Skip if IWM already below $260 (spread too close to at-the-money)

Position sizing: Risk only 2-3% of portfolio per spread position

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Aggressive: Fade the Rally with Naked Puts (ADVANCED ONLY!)

Play: Sell cash-secured puts at gamma support to collect premium from elevated IV

Structure: Sell IWM $255 puts (February 20 expiration)

Why this could work:

- Premium collection strategy that profits from time decay

- $255 strike sits at major gamma support (106.3B gamma) - dealers will defend

- If assigned, buying IWM at $255 represents 4.3% discount from current price

- IV likely elevated post-FOMC creating rich premium opportunity

- Small-cap fundamentals remain strong - earnings growth 17-22% for 2026

Why this could hurt (SERIOUS RISKS):

- UNDEFINED RISK: If IWM crashes to $230-240, losses could be $15-25 per share ($1,500-2,500 per contract)

- MARGIN INTENSIVE: Requires significant buying power to hold position

- ASSIGNMENT RISK: Early assignment possible if puts go deep in-the-money

- TIMING RISK: Selling puts before FOMC is dangerous - wait for event to pass

Estimated P&L:

- Premium received: ~$2.00-3.00 per contract (adjust based on IV)

- Max profit: Keep entire premium if IWM above $255 at expiration

- Max loss: Theoretically unlimited (IWM to $0 = $255 loss per share)

- Breakeven: ~$252-253 (strike minus premium)

CRITICAL REQUIREMENTS - DO NOT attempt unless you:

- Have cash to purchase 100 shares of IWM per contract sold ($25,500+ per contract)

- Can afford significant drawdown if IWM drops 10-15%

- Understand assignment mechanics and margin requirements

- Wait until AFTER January FOMC meeting to reduce binary event risk

- Have stop-loss plan if IWM breaks below $250 gamma support

Risk level: HIGH (undefined risk, requires margin) | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

FOMC binary event in 12 days: The January 27-28 meeting creates significant volatility risk. While consensus expects rates held steady, any hawkish surprise ("higher for longer" language, inflation concerns) could trigger 3-5% single-day decline in rate-sensitive small caps. Conversely, dovish surprise could send IWM above $270 resistance quickly.

-

Overbought technical condition: RSI at 71.6 is extended territory. Historical pattern for IWM shows mean-reversion from these levels within 2-3 weeks. The +6.1% YTD gain in just 10 trading days is statistically extreme - regression to the mean suggests consolidation ahead.

-

40% of Russell 2000 is unprofitable: Despite the rotation narrative, approximately 40% of Russell 2000 constituents remain unprofitable per Financial Content. These "zombie companies" face the 2026 refinancing wall with $225B of high-yield refinancing needed this year.

-

Fund flows still negative: Despite strong YTD performance, IWM has seen -$6.72 billion in net outflows over the past 12 months per ETF Database. The rally has occurred despite, not because of, institutional buying - suggesting potential fragility.

-

Tariff policy wildcard: The Supreme Court ruling on tariff legality could arrive in H1 2026 per Bloomberg. This binary event could cause significant volatility in either direction.

-

Inflation remains sticky: Core CPI at 2.6% (above Fed's 2% target) per CNBC could delay rate cuts further than market expects. Small caps with floating-rate debt are particularly vulnerable to "higher for longer" scenarios.

-

Manufacturing weakness: There has been "no manufacturing recovery" per Investment News. The Russell 2000 may be pricing in ISM data that's better than current reality.

-

$18.2M institutional put spread: This significant institutional positioning signals sophisticated players expect downside risk despite bullish fundamentals. When institutions pay millions for downside protection at all-time highs, retail traders should take note.

The Bottom Line

Real talk: Someone just deployed $18.2 MILLION betting IWM pulls back to $250-253 over the next 36 days. This isn't a crash call - it's a disciplined bet that the small-cap rally needs to consolidate after an explosive start to 2026. The bear put spread structure shows they expect a measured 5-6% pullback, not a disaster.

What this trade tells us:

- Sophisticated players see the January FOMC meeting (12 days away) as a potential volatility catalyst

- They're targeting the $250-253 gamma support zone - a logical technical target for any pullback

- The February 20 expiration captures multiple risk events: FOMC, Q4 earnings season, February CPI

- They're using defined-risk structure (put spread) not naked puts - suggesting controlled bearishness, not panic

This is NOT a "sell everything" signal - it's a "expect some consolidation" signal.

If you own IWM:

- Consider trimming 20-30% at current levels near all-time highs - lock in YTD gains

- Set mental stop at $260 (first major gamma support) to protect remaining position

- If bullish long-term, use any pullback to $255-260 to add back shares at better prices

- The 17-22% earnings growth outlook for small caps remains intact - this is about entry timing, not thesis

If you're watching from sidelines:

- January 27-28 FOMC is the moment of truth - don't chase at all-time highs before binary event

- Target entry zone: $255-262 post-FOMC or on any pullback to gamma support

- Looking for confirmation: Fed language, Q4 earnings quality, inflation trajectory

- Long-term thesis compelling: 31% valuation discount, domestic focus, earnings inflection

If you're bearish:

- Put spread structure makes sense: defined risk, specific target, reasonable probability

- First support at $265, then $260, deeper floor at $255 - these are your targets

- Don't overstay welcome: Small-cap fundamentals remain solid, pullbacks likely to be buying opportunities

Mark your calendar - Key dates:

- January 16 (Tomorrow) - Weekly options expiration, January monthly OPEX

- January 27-28 - FOMC meeting (hold rates expected, watch language closely)

- February 11 - January CPI release

- February 20 - Put spread expiration (THIS TRADE!)

- March 18-19 - March FOMC meeting (rate cut probability rising)

- March 20 - Triple Witch quarterly expiration

Final verdict: The "Great Rotation" into small caps is real - IWM is up 6.1% YTD while the S&P 500 is up just 1.8%. The valuation discount (31% below large caps) and earnings growth outlook (17-22% for 2026) support the bullish thesis per Benzinga and JPMorgan. BUT, at RSI 71.6 with FOMC looming and $18.2M in institutional put spreads hitting the tape, the risk/reward favors patience over chasing. Wait for the pullback, get a better entry, and let this trade run its course.

Be patient. Let FOMC clear. Look for entry at $255-262. The small-cap rotation will still be here in 3-4 weeks, and you'll own it at better prices.

This is a marathon, not a sprint. Protect your capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores (7.51 to 49.27) reflect this trade's unusual size relative to recent IWM history - this level of activity occurs perhaps a handful of times per year. Always do your own research and consider consulting a licensed financial advisor before trading. The put spread buyer may have complex portfolio hedging needs not applicable to retail traders.

About iShares Russell 2000 ETF: IWM tracks the Russell 2000 Index, providing exposure to approximately 2,000 small-cap U.S. companies across diverse sectors. With $76.05 billion in AUM and a 0.19% expense ratio, it remains the most liquid vehicle for small-cap exposure and a key barometer for domestic economic health.