JBS $1.8M LEAP Call Buy - Someone's Betting Big on the World's Largest Meat Processor!

January 20, 2026 | Unusual Activity Detected

The Quick Take

Someone just loaded up on $1.8 MILLION worth of JBS call options expiring in nearly a year! This isn't retail traders nibbling - this is a 20,000 contract position at the $17.50 strike, betting JBS rises about 15% from current levels by January 2027. With Q4 earnings coming February 26 and the company trading at a steep discount to peers (8.8x forward P/E vs. 17.4x industry average), smart money seems to be positioning for a re-rating of the world's largest protein company.

Company Overview

JBS N.V. (NYSE: JBS) is the world's largest protein food company by revenue, processing beef, pork, poultry, and lamb across five continents:

- Market Cap: $16.27 billion

- Industry: Meat Processing / Food Production

- Employees: 280,000 globally

- Current Price: $15.23

- Forward P/E: 8.8x (vs. 17.4x peer average)

- Dividend Yield: 4.75%

JBS operates multiple segments including Beef North America (largest revenue driver), JBS Brazil, Seara (prepared foods), Pork USA, Pilgrim's Pride (poultry), and JBS Australia. The company completed its landmark NYSE dual listing in June 2025, marking a strategic milestone for US investor access.

Key Brands: Swift, Just Bare, Pilgrim's Pride, Seara, and others

The Option Flow Breakdown

What Just Happened

The Tape (January 20, 2026 @ 13:24:19)

| Date | Time | Symbol | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-20 | 13:24:19 | JBS | BUY | CALL | 2027-01-15 | $1,800,000 | $17.50 | 20,000 | 531 | 19,999 | $15.18 | $0.90 | JBS20270115C17.5 |

What This Actually Means

This is a massive bullish bet on JBS over the next year. Let's break it down:

- Premium paid: $1.8M for nearly a year of upside exposure

- Strike price: $17.50 (about 15% above current price of $15.18)

- Breakeven at expiration: $18.40 ($17.50 strike + $0.90 premium)

- Volume vs Open Interest: 20,000 contracts traded vs. only 531 OI - massive new position being established

- Position type: Buy-to-Open (BTO) Long Call - someone establishing a new bullish position

Translation for regular folks: This trader is betting $1.8M that JBS stock will be worth at least $18.40 by January 2027 to break even. But LEAPs like this are typically bought with price targets well above breakeven - suggesting the trader sees potential for JBS to trade into the low $20s, which would be 30%+ upside from here.

Why LEAPs matter: Buying calls with nearly a year to expiration isn't a day trade - it's a thesis on the company's fundamental trajectory. This trader is giving JBS multiple earnings cycles, resolution of the US cattle cycle, and potential re-rating catalysts to play out.

Technical Setup / Chart Check-Up

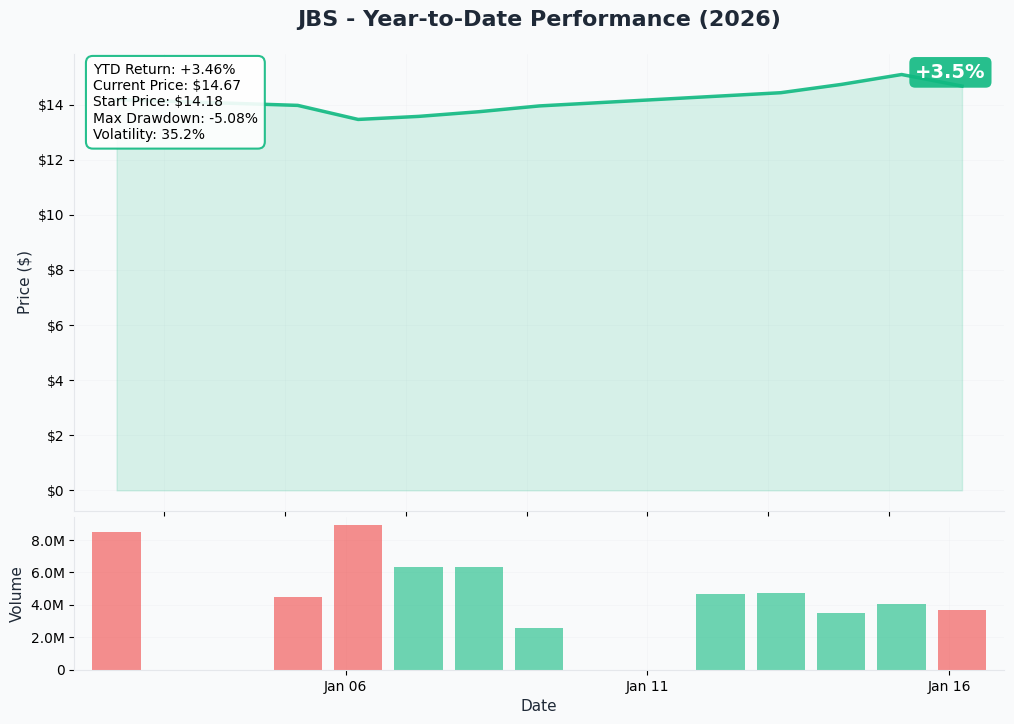

YTD Performance Chart

JBS began NYSE trading in June 2025 at $13.65 and has shown resilience despite challenging conditions in the US beef market. The stock currently trades around $15.23, representing approximately 12% upside from its debut price.

Key observations:

- Stock has held above NYSE debut price despite US cattle herd at smallest size since 1951

- Recent trading range between $14-$16 suggests consolidation before next leg

- Outperforming competitor Tyson Foods on geographic diversification benefits

- Recovery from late-2025 lows after Q3 results exceeded expectations

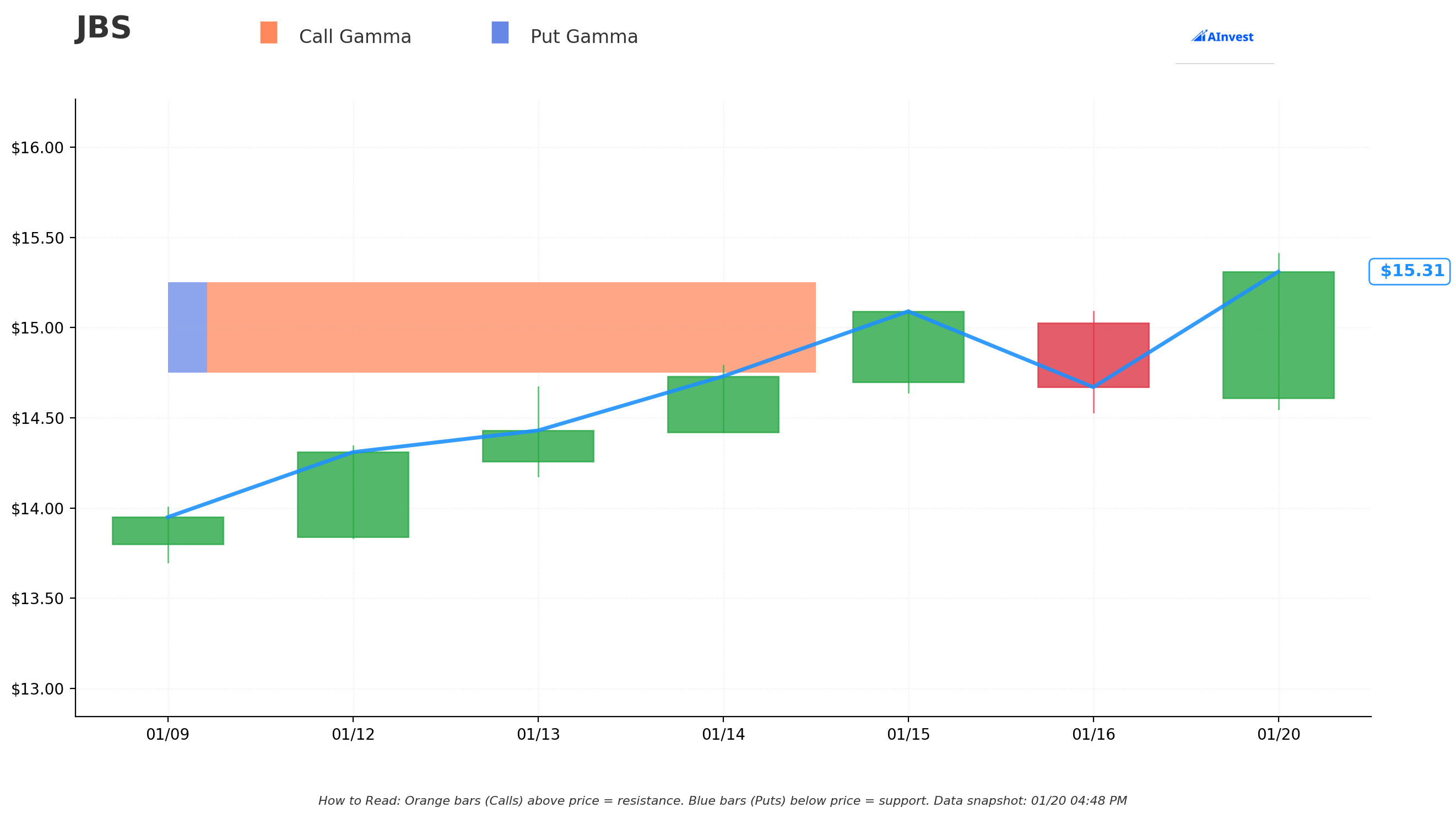

Gamma-Based Support & Resistance Analysis

Current Price: $15.23

The gamma exposure map reveals the key price levels where options positioning creates natural support and resistance:

Support Levels (Put Gamma Below Price):

- $15.00 - Strongest support with 9.65B net gamma exposure (1.5% below current price)

- $12.50 - Secondary deep support at -0.79B gamma (17.9% below current price)

Resistance Levels (Call Gamma Above Price):

- $17.50 - Primary resistance with 0.70B net gamma (14.9% above current price)

What this means for traders: The gamma data shows strong support at $15.00, just below current levels. Market makers will buy stock as price approaches this level to hedge their positions, creating a natural floor. The $17.50 strike - exactly where today's big trade was placed - represents the main overhead resistance. If JBS can break through $17.50, there's relatively clear air above.

Net GEX Bias: Bullish (11.18B call gamma vs. 1.53B put gamma) - overall dealer positioning favors upside moves.

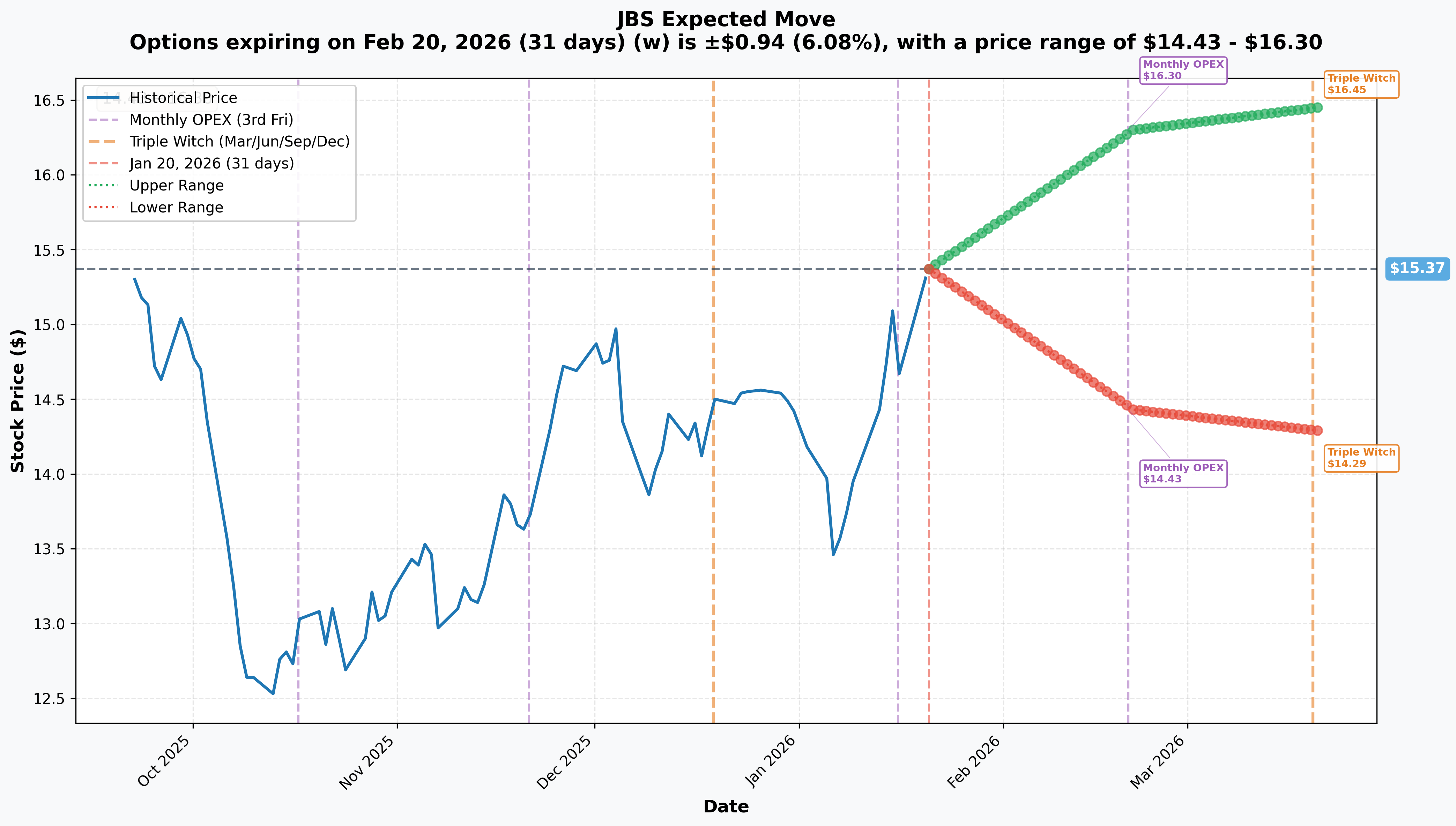

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiration | Days | Implied Move % | Implied Move $ | Upper Range | Lower Range |

|---|---|---|---|---|---|---|

| Monthly OPEX | 2026-02-20 | 31 | 6.08% | $0.94 | $16.30 | $14.43 |

| Triple Witch | 2026-03-20 | 59 | 7.05% | $1.08 | $16.45 | $14.29 |

Translation for regular folks: The options market is pricing in a roughly 6% move by February monthly expiration and 7% by the March quarterly expiration. That's fairly modest volatility for a stock heading into earnings. The implied upper range of $16.30-$16.45 suggests the market doesn't expect a breakout above $17 in the near term - which makes today's $17.50 strike LEAP bet even more interesting as a contrarian play.

Catalysts

Upcoming Catalysts

Q4 2025 Earnings Release - February 26, 2026

- Expected EPS: $0.42 (range: $0.28 - $0.55)

- Key metrics to watch: US beef margin trajectory, Pilgrim's Pride profitability, Australia export volumes, pork normalization

- Previous quarter: Beat estimates with $0.52 EPS vs. $0.49 consensus

China Beef Import Quotas (Effective January 1, 2026)

- China imposed Safeguard TRQ limits on major beef exporters for three years

- Exporters exceeding quota face 55% tariff

- Australia quota: 205,000 tonnes (approximately 75% of 2025 export volume)

- Brazil quota: 1.106 million tonnes (requires 35% reduction from 2025 volumes)

- Industry developing quota management systems to avoid mid-year tariff triggers

US Cattle Cycle Potential Inflection

- USDA suspended live cattle imports from Mexico following New World Screwworm outbreak

- Beef cow herd may have reached cyclical low in 2025

- Management expects US beef margins challenged for 3-4 quarters with gradual improvement from 2027

- USDA moving to reopen Mexican cattle imports, potentially easing supply constraints

Share Buyback Execution

- $400 million buyback program announced - execution timing through 2026

Brazil Supplier Traceability Deadline

- [JBS pledged to require all direct suppliers to declare indirect suppliers by January 2026](https://unearthed.greenpeace.org/2025/04/17/jbs-amazon-deforestation-pledge-ranchers/)

- Para state mandates full animal traceability by end of 2026

- Execution risk as ranchers call timeline "wholly unrealistic"

Recent Catalysts (Already Happened)

Q3 2025 Results (November 14, 2025):

- Record net revenue of $22.6 billion, up 9% YoY (beat consensus by 4.2%)

- Adjusted EBITDA: $1.8 billion with 8.4% margin

- [JBS USA Beef: Record net sales of $7.2 billion](https://www.meatpoultry.com/articles/32745-jbs-reports-record-revenue-lower-profit-in-q3) but margins pressured by unfavorable cattle cycle

- Pilgrim's Pride: Record adjusted EBITDA supported by lower grain costs

- [JBS Australia: 20% revenue growth with EBITDA margin reaching 12.7%](https://www.investing.com/news/transcripts/earnings-call-transcript-jbs-beats-q3-2025-forecasts-with-strong-eps-revenue-93CH-4359627)

NYSE Dual Listing Completion (June 2025):

- [JBS N.V. began trading on NYSE under symbol "JBS" on June 13, 2025](https://www.cnbc.com/2025/06/13/jbs-brazilian-meat-company-goes-public-in-the-us.html)

- Opening trade of $13.65 valued company at roughly $30 billion, exceeding Tyson Foods' market cap

- Class A Conversion Period extends through December 31, 2026

Recent Analyst Activity:

- Grupo Santander (December 9, 2025): Upgraded to Outperform from Neutral

- Goldman Sachs (November 26, 2025): Maintained Buy, lowered target to $18.50 from $21.10

- Consensus: Strong Buy (14 Buy, 1 Hold, 0 Sell)

- Average 12-Month Price Target: $19.93 (38.4% upside)

Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis:

Bull Case (35% probability)

Target: $19-$21

How we get there:

- Q4 earnings beat drives analyst estimate revisions higher

- US cattle cycle shows signs of bottoming, improving margin outlook

- Pilgrim's Pride and Australia segments continue outperformance

- Multiple expansion toward peer valuations (currently 8.8x vs. 17.4x peer average)

- Buyback execution provides support

- China quota management proceeds smoothly

This scenario aligns with the analyst consensus target of $19.93 and would deliver solid profits to today's LEAP buyer.

Base Case (45% probability)

Target: $15-$17

Most likely scenario:

- Stock trades within current consolidation range through Q4 earnings

- US beef margins remain challenged as expected for 3-4 quarters

- Poultry and Australia continue offsetting beef headwinds

- Gradual improvement without significant re-rating

- Stock respects $15 gamma support and $17.50 resistance bands

In this scenario, the LEAP calls slowly gain value through time but don't hit the $17.50 strike until later in 2026 or early 2027.

Bear Case (20% probability)

Target: $12-$14

What could go wrong:

- Amazon deforestation litigation escalates (Global Witness estimates nearly $7 billion in total legal liabilities)

- China quota violations trigger 55% tariff on Australian exports

- US beef margins deteriorate further than expected

- ESG concerns limit institutional buying despite discount valuation

- Brazilian real volatility creates earnings headwinds

- Governance concerns around Batista family return to leadership weigh on stock

Trading Ideas

Conservative: Wait for Earnings Confirmation

Play: Wait until after February 26 Q4 earnings for clearer picture

Why this works:

- Earnings binary event creates uncertainty

- Current implied volatility reflects upcoming catalyst risk

- Better entry if stock pulls back to $14-$14.50 range

- Gamma support at $15 provides clear risk management level

Action plan:

- Monitor Q4 results for US beef margin trajectory

- Look for confirmation that Pilgrim's Pride and Australia strength continues

- Consider entry if stock holds above $15 post-earnings with positive guidance

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Covered Call or Cash-Secured Put

Play A - Covered Call: Own 100 shares at $15.23, sell March 2026 $17.50 calls

Play B - Cash-Secured Put: Sell March 2026 $15 puts, collect premium while waiting for entry

Why this works:

- 4.75% dividend yield provides income while waiting

- Gamma support at $15 gives confidence in put strike selection

- Implied volatility of 6-7% creates reasonable premium

- Defined risk with stock purchase or assignment at attractive levels

Estimated P&L (Play B - CSP):

- Collect ~$0.40-$0.60 per contract premium

- If assigned at $15, effective cost basis: $14.40-$14.60 (attractive entry)

- Keep premium if stock stays above $15 (max profit)

Risk level: Moderate | Skill level: Intermediate

Aggressive: Follow the Whale into LEAPs

Play: Buy January 2027 $17.50 calls at ~$0.90 (similar to today's big trade)

Why this could work:

- Mirrors $1.8M institutional position

- Nearly 12 months for thesis to play out

- Multiple earnings cycles and potential cattle cycle inflection

- Analyst targets averaging $19.93 suggest significant upside

- Discount valuation (8.8x P/E vs. 17.4x peers) leaves room for multiple expansion

Why this could fail:

- Breakeven at $18.40 requires 21% move from current levels

- ESG risks and legal liabilities could cap multiple expansion

- US beef margins may remain challenged longer than expected

- Time decay works against you every day

Estimated P&L:

- Cost: $90 per contract ($9,000 for 100 contracts)

- At $20 stock price: ~$2.50 value = 177% return

- At $17.50 (exactly at strike): Lose most of premium

- Below $17.50 at expiration: Total loss of premium

Risk level: High | Skill level: Intermediate to Advanced

Risk Factors

Don't overlook these potential challenges:

-

US Cattle Cycle Pressure: US cattle herd at smallest size since 1951 with JBS USA Beef operating at near-zero margins. Management expects 3-4 quarters of challenged margins before improvement in 2027.

-

ESG and Legal Liabilities: [Human Rights Watch report alleges JBS fueled illegal Amazon deforestation](https://www.hrw.org/report/2025/10/15/tainted/jbs-and-the-eus-exposure-human-rights-violations-and-illegal). Global Witness estimates nearly $7 billion in total legal liabilities - approaching 2024 EBITDA levels.

-

Governance Concerns: [Joesley and Wesley Batista returned to JBS board despite prior imprisonment](https://globalwitness.org/en/press-releases/experts-issue-warning-to-investors). J&F Investimentos paid $3.2 billion in penalties for corruption in 2017.

-

China Quota Risk: Failure to manage Australian exports within 205,000t quota triggers 55% tariff. Risk of filling quota by mid-year without management system.

-

Currency Volatility: Brazilian real fluctuation between 5.26-6.10 BRL/USD in the past year. Political uncertainty around Brazil presidential election (Oct-Nov 2026) could spike USDBRL.

-

Consumer Demand Risk: Choice beef retail prices averaging over $9.50/lb causing "trade-down" to poultry/pork. Potential demand destruction at elevated beef prices.

The Bottom Line

Here's the deal: Someone with $1.8 million in conviction just bet that JBS, the world's largest protein company, is undervalued. They're giving themselves nearly a year for the thesis to play out - through multiple earnings cycles, potential cattle cycle inflection, and continued execution of the company's multi-protein diversification strategy.

What this trade tells us:

- Institutional confidence in JBS despite near-term US beef headwinds

- Thesis likely based on valuation gap (8.8x vs. 17.4x peer P/E)

- 12-month timeframe suggests catalyst expectations around cattle cycle turn

- Strike at $17.50 aligns with analyst targets of $19.93

If you're considering JBS:

- The valuation discount is real - JBS trades at nearly half the multiple of peers

- Strong Buy consensus with 38% upside to $19.93 target suggests analyst support

- Q3 beat and segment diversification provide fundamental support

- 4.75% dividend yield pays you to wait

- But ESG concerns are legitimate - these aren't small legal risks

If you're on the sidelines:

- February 26 Q4 earnings is the next major catalyst

- Watch for US beef margin commentary and guidance

- Consider entry on any pullback to $14-$14.50 range (near gamma support)

- LEAPs offer leveraged exposure with defined risk if you share the bullish thesis

If you're bearish:

- ESG and legal liabilities provide fundamental case against multiple expansion

- Put spreads offer defined-risk way to express downside view

- $15 gamma support is the level to watch - break below opens $12.50

Mark your calendar - Key dates:

- February 26, 2026 - Q4 2025 earnings release

- January 1, 2026 - China beef import quotas effective (already in force)

- December 31, 2026 - Class A Share conversion period deadline

- January 15, 2027 - LEAP options expiration (today's big trade)

Final verdict: This $1.8M LEAP bet reflects a fundamental thesis that JBS's diversified protein platform, discount valuation, and potential cattle cycle inflection make it an attractive 12-month investment. The trader isn't trying to time earnings - they're betting on a structural re-rating. Whether you follow them depends on your view of the ESG risks and your conviction that the world's largest meat processor deserves a higher multiple. At 8.8x forward earnings with a 4.75% yield and Strong Buy consensus, the valuation support is there - but so are the headline risks.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading.

About [JBS N.V.](https://www.jbs.com.br): JBS is the world's largest protein company with a $16.27 billion market cap and 280,000 employees globally. The company processes beef, pork, poultry, and lamb across North America, South America, Australia, and Europe under brands including Swift, Pilgrim's Pride, Seara, and Just Bare.