🏦 $JPM $2.1M Call Bet - Someone's Loading Up on JPMorgan Ahead of Earnings Season!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.1 MILLION on JPMorgan $305 calls expiring June 18th while the stock trades at $302.31 - that's a near-ATM bet that the world's most valuable bank bounces back from its 10% pullback. With Q1 earnings on April 14, potential Basel III capital relief, and a Fed Chair transition in May all landing before expiration, this institutional player is positioning for a meaningful recovery over the next 3.5 months.

📊 Company Overview

JPMorgan Chase & Co. (JPM) is one of the largest and most complex financial institutions in the United States, with more than $4.4 trillion in assets:

- Market Cap: $802.5B

- Industry: National Commercial Banks (SIC 6021)

- Exchange: NYSE

- Current Price: $302.31 (down ~10% from ATH of $337.25)

- Employees: 318,512

- HQ: 270 Park Avenue, New York, NY

- Primary Business: Consumer Banking, Corporate & Investment Banking, Commercial Banking, Asset & Wealth Management

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 13:39:19):

| Time | Symbol | Side | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Option Symbol | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|

| 13:39:19 | JPM | BUY | CALL | 2026-06-18 | $305 | 2,400 | $2.1M | BTO | JPM20260618C305 | 4.62 |

🤓 What This Actually Means

This is a buy-to-open (BTO) long call - a classic directional bullish bet. Here's what you need to know:

- 💸 Premium paid: $2.1M ($8.75 per contract x 2,400 contracts)

- 🎯 Only $2.69 out-of-the-money: $305 strike with JPM trading at $302.31 - this is almost at the money

- 💰 Breakeven: ~$313.75 (strike + premium per share)

- 📊 Position size: 2,400 contracts = 240,000 shares worth ~$72.6M notional exposure

- 🏦 Vol/OI ratio: 3.675x - meaning volume absolutely dwarfed existing open interest at this strike

What's really happening here:

This trader is making a straight-up directional bet that JPM recovers from its recent 10% pullback and pushes back toward the $315-$330 range by mid-June. The near-ATM strike signals conviction in a moderate rebound rather than a moonshot. The June 18 expiration captures three major catalysts: Q1 earnings (April 14), Basel III Endgame finalization (expected H1 2026), and the Fed Chair transition (May 15). At $2.1M, this is not your neighbor Bob trading from his Robinhood account.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-Score: 4.62) - This kind of trade shows up only a handful of times per year. A Z-Score above 4 means this is roughly 555x more unusual than average activity at this strike. The 2,400-contract BTO clip confirms aggressive buying intent from an institutional or fund-level player.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

JPMorgan is down roughly 6% YTD in 2026, falling from ~$322 at the start of the year to $302.31 today. After hitting an all-time high of $337.25 on January 5, the stock has been in a persistent downtrend, pressured by a "yield curve twist" compressing bank net interest margins and broader banking sector weakness that saw KBE drop ~5% on March 2 in one of its most volatile sessions since 2023.

Key observations:

- 📉 Downtrend from ATH: Stock has retraced ~10% from $337.25 since early January

- 🏦 $300 psychological support: Stock is hovering just above this critical round number

- 🎢 Banking sector selling pressure: Elevated volume in late February/early March across the sector

- 📊 Still well above 52-week lows: Even with the pullback, JPM is trading near its all-time highs relative to historical range

- 💹 Record fundamentals underneath: FY2025 was a record year ($57B net income, $185B revenue)

Implied Move Analysis

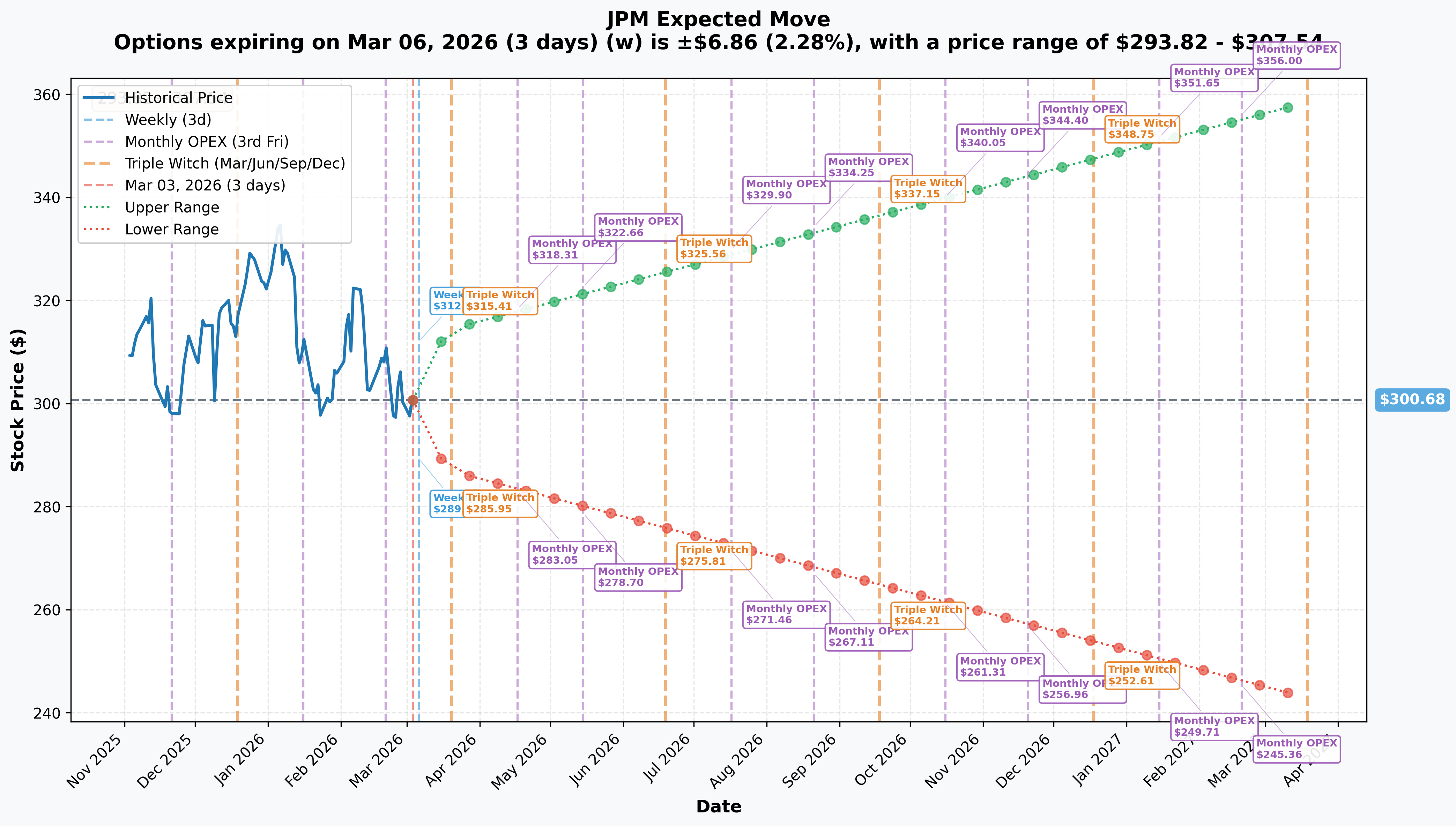

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 3 days): +/-$6.86 (+/-2.28%) --> Range: $293.82 - $307.54

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 17 days): +/-$13.88 (+/-4.61%) --> Range: $286.80 - $314.56

- 📅 June Triple Witch (Jun 19): Implied upper: $325.56 / Implied lower: $275.80

- 📅 LEAPS (Mar 2027): +/-$57.86 (+/-19.24%) --> Range: $242.82 - $358.54

Translation for regular folks:

Options traders are pricing in a 2.28% move (~$7) by Friday and a 4.61% move (~$14) through March expiration. That's elevated for a mega-cap bank stock, reflecting the sector-wide stress right now.

For this specific trade (June 18 expiration), the implied move upper bound sits at $325.56 - right in the analyst consensus target range. The breakeven at $313.75 falls comfortably within the expected range, meaning this buyer doesn't need a miracle. They just need JPM to bounce back roughly 3.8% from here by June.

Gamma-Based Support & Resistance Analysis

Key levels to watch based on options activity and implied moves:

🔵 Support Levels:

- $300 - Major psychological floor; JPM is sitting right on top of this level

- $293.82 - Implied move lower bound for weekly expiration

- $286.80 - Implied move lower bound for March OPEX / Triple Witch

- $275.80 - Implied move lower bound for June Triple Witch - worst-case support zone

🟠 Resistance Levels:

- $305 - The call strike level; this is where the institutional buyer is positioned

- $307.54 - Implied move upper bound for weekly expiration

- $314.56 - Implied move upper bound for March OPEX

- $325.56 - Implied move upper bound for June expiration; aligns with analyst consensus targets

- $330-$340 - Heavy options open interest zone from gamma data; significant resistance cluster

What this means for traders:

The $300-$305 zone is the battleground right now. If JPM holds above $300 and starts to recover toward $305 (the call strike), that's confirmation this institutional buyer is in good shape. The March OPEX upper bound at $314.56 and June upper bound at $325.56 map almost perfectly to analyst consensus targets of $333-$346. The call buyer at $305 is essentially betting that JPM reverts toward fair value as the banking sector shakes off its recent weakness. These are dynamic levels that change throughout the day as options positions are opened and closed.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings - April 14, 2026 (before market open) 📊

The biggest event on the calendar. JPMorgan reports Q1 2026 results on April 14 with consensus EPS of $5.31-$5.37 and revenue of ~$48.3B. Key metrics to watch:

- 📊 NII trajectory vs. $95B full-year guide (ex-Markets)

- 💹 Trading revenue sustainability after record Q4 equities ($2.9B, +40% YoY)

- 🍎 Apple Card reserve adjustments and early credit quality signals

- 💰 Updated buyback pace under the $50B authorization

Basel III Endgame Finalization - Expected H1 2026 🏛️

According to the Atlantic Council, the Fed's revised framework is expected to be capital-neutral, slashing megabank capital requirements by 140 basis points. This could free ~$110B in restricted capital across the industry. For JPM specifically, excess capital above the 11.5% CET1 requirement could fund accelerated buybacks or M&A. Analyst consensus puts the probability of a capital-neutral outcome at 70-80%.

Fed Chair Transition - May 15, 2026 🏛️

Jerome Powell's term expires May 15, with Kevin Warsh nominated as successor. Warsh is viewed as more hawkish on regulation but potentially favorable for bank deregulation. Uncertainty could drive volatility in financials leading into confirmation.

Apple Card Migration Milestones - 2026-2028 🍎

JPMorgan became the new issuer of Apple Card, acquiring $20B+ in card loans from Goldman Sachs. Watch for early adoption metrics and cross-sell revenue signals in Q1/Q2 earnings calls.

Fed Rate Decisions - Ongoing 💹

Market pricing suggests 2 rate cuts in 2026, possibly later in the year. Further cuts would compress NII but could boost IB/trading activity and asset values.

⏪ Recent Catalysts (Already Happened)

Q4 2025 Results Beat (January 13, 2026): Revenue of $46.77B (+7% YoY) beat consensus of $46.20B, with adjusted EPS of $5.23 beating the $5.00 estimate. The equities trading desk absolutely crushed it with $2.9B in revenue, surging 40% YoY. Full-year 2025 was a record: $185B revenue and $57B net income.

Apple Card Takeover Announced (January 7, 2026): Chase became the new issuer of Apple Card, taking over $20B+ from Goldman Sachs. JPM pre-booked a $2.2B provision for credit losses tied to the deal. Worth noting: 34% of the portfolio has FICO scores below 660 - subprime exposure that's atypical for JPM.

Analyst Upgrades (January-February 2026): CICC initiated coverage with Outperform and a $355 target. Baird upgraded from Underperform to Neutral. HSBC upgraded to Hold with a $319 target.

AI & Tech Investment Push (February 2026): JPMorgan boosted its 2026 tech spend to ~$19.8B (+10% YoY), with ~25% tied to AI. Dimon told investors AI is "already reshaping JPMorgan's workforce" with major redeployment plans.

Dimon's Inflation Warning (March 3, 2026): On the very day of this unusual trade, Jamie Dimon warned inflation could be "a skunk at the party", potentially disrupting rate cut expectations.

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, analyst targets, and upcoming catalysts:

📈 Bull Case (30% probability)

Target: $325-$345

How we get there:

- 📊 Q1 earnings on April 14 beat consensus again (JPM has beaten 3 straight quarters), confirming NII growth trajectory toward $95B+ and sustained trading revenue strength

- 🏛️ Basel III Endgame lands capital-neutral as expected, freeing billions for buybacks under the $50B repurchase authorization

- 💹 Banking sector rotation reverses as yield curve stabilizes - sector was oversold on March 2

- 🤖 AI productivity gains from $19.8B tech spend start showing up in operating leverage

- 📈 Stock re-rates toward analyst consensus target of $333-$346 (10-15% upside from current levels)

- 🏛️ Fed Chair transition goes smoothly; Warsh signals bank-friendly deregulation agenda

Impact on the trade: This is the buyer's dream scenario. At $325, the $305 calls would be worth ~$20 per contract, turning the $2.1M bet into roughly $4.8M - a 130% gain. At $345, we're looking at $9.6M - a 357% return.

🎯 Base Case (45% probability)

Target: $300-$320 range-bound

Most likely scenario:

- ✅ Q1 earnings come in roughly at consensus - solid but not spectacular enough to spark a breakout

- 📊 NIM pressure from the yield curve twist continues but is partially offset by trading revenue and fee income

- 🍎 Apple Card integration proceeds on schedule without major credit quality surprises

- 🏛️ Basel III finalization takes longer than expected, pushing into Q3

- 🔄 Stock trades sideways between $300 support and $320 resistance, digesting the pullback

Impact on the trade: Mixed outcome. If JPM is at $310-$315 by June, the calls would be worth $5-$10 per contract, roughly breakeven to modest profit. Below $305 at expiration means the entire $2.1M is lost. The buyer needs at least a 3.8% bounce to break even.

📉 Bear Case (25% probability)

Target: $275-$295

What could go wrong:

- 😰 NIM compression accelerates as the yield curve twist deepens

- 📉 Apple Card credit losses surprise to the upside - 34% subprime exposure could mean charge-off rates above the guided 3.4%

- 🏛️ Basel III finalization comes with higher-than-expected capital requirements (reversal scenario)

- ⚖️ Tariff-driven small business stress leads to higher credit losses in commercial lending

- 💸 Dimon's inflation warnings prove prescient, forcing the Fed to stay higher for longer

- 📉 $300 support breaks, triggering a move toward implied support at $286 (March OPEX lower bound) or worse, $275.80 (June lower bound)

Impact on the trade: The $2.1M is a total loss. The calls expire worthless below $305.

💡 Trading Ideas

🛡️ Conservative: The "Bank Dividend Collector" Cash-Secured Put

Play: Sell the April 17 $290 put on JPM to collect premium while setting up to buy shares at a ~4% discount

Why this works:

- 💰 JPM pays a $1.50/quarter dividend (~2.0% yield) - you want to own this stock at the right price

- 📊 $290 is below both the weekly and monthly implied move lower bounds ($293.82 and $286.80)

- 🛡️ Even if assigned, you're buying the world's most profitable bank at ~14x earnings and a 20% ROTCE

- ⏰ April 17 expiration captures earnings on April 14 - you get to see results before assignment risk peaks

- 📈 Analyst consensus of $333-$346 means even an assigned position has 15%+ upside potential

Estimated P&L:

- 💰 Collect ~$3-5 per contract (~1.0-1.7% return on capital at risk over 45 days)

- 📈 If JPM stays above $290: Keep the full premium, annualized return ~8-14%

- 📉 If assigned: Own JPM at effective price of ~$285-287 (below current price + below implied support)

Risk level: Low (you want to own JPM) | Skill level: Beginner-friendly

⚖️ Balanced: The "Earnings Catalyst" Call Spread

Play: Buy the June 18 $305/$330 call spread to participate in the upside with defined risk

Why this works:

- 🎯 Same expiration as the institutional $2.1M trade - ride the smart money wave

- 📊 $305 lower strike matches the institutional bet; $330 upper strike aligns with gamma resistance and analyst consensus

- 💰 Defined risk: pay ~$6-8 per spread vs. max payoff of $25 per spread at $330+

- 📅 Captures all three major catalysts: Q1 earnings (April 14), Basel III (H1 2026), Fed Chair transition (May 15)

- 🛡️ Capped downside - you can't lose more than the premium paid

Estimated P&L:

- 💰 Cost: ~$600-800 per spread

- 📈 Max profit: ~$1,700-1,900 per spread if JPM closes at or above $330 by June 18

- 🎯 Breakeven: ~$311-$313 (roughly in line with the institutional buyer's breakeven)

- 📉 Max loss: Premium paid if JPM stays below $305

Risk level: Moderate (defined risk, multi-catalyst setup) | Skill level: Intermediate

🚀 Aggressive: The "Follow the Whale" ATM Call

Play: Buy June 18 $305 calls outright - mirroring the institutional trade at a smaller scale

Why this works:

- 🐋 You're riding alongside a $2.1M institutional bet with a Z-Score of 4.62 - this kind of conviction is rare

- 📊 Near-ATM strike gives you strong delta exposure (~0.48-0.52) from day one

- 📅 3.5 months of runway captures earnings, Basel III, and Fed Chair transition

- 📈 13 of 22 analysts rate JPM a Buy with average targets $30-$44 above current price

- 💹 If the banking sector bounces from its oversold condition, JPM leads the way higher as the sector flagship

Why this could go wrong:

- 💥 $300 support fails and JPM drops into the $280s - you lose most or all of your premium

- ⏰ Time decay eats away ~$2-3 per month if the stock goes nowhere

- 📉 The yield curve twist persists and NIM compression worsens through Q2

- ⚠️ Dimon's inflation warnings create sector-wide selling pressure

Estimated P&L:

- 💰 Cost: ~$875 per contract

- 📈 At $320 by June: ~$1,500 per contract (+71% gain)

- 📈 At $335 by June: ~$3,000 per contract (+243% gain)

- 📉 At $305 or below by June 18: Total loss of premium

- 🎯 Breakeven: ~$313.75

Risk level: High (unlimited upside, full premium at risk) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💹 Yield curve twist compressing bank margins: The "2026 Yield Curve Twist" has 10Y Treasury yields at ~4.09% vs. short-term repo at 4.2%, squeezing net interest margins across the entire banking sector. Even JPM's diversified revenue can't fully insulate it from this dynamic.

-

😰 CEO succession overhang: Daniel Pinto is retiring in 2026 and Dimon says he has "a few more years" but no firm timeline. The market typically discounts stocks with unresolved leadership transitions, and the "Dimon premium" could become a "Dimon uncertainty discount."

-

🍎 Apple Card subprime risk: The acquired portfolio has 34% of loans tied to FICO scores below 660 - atypical for JPM's traditionally pristine credit profile. If consumer credit deteriorates amid tariff-driven inflation, charge-off rates could exceed the guided 3.4%.

-

⚖️ Tariff and inflation headwinds: Dimon himself warned on March 3 that inflation could be "like a skunk at the party". If inflation re-accelerates, the Fed stays higher for longer, which could further flatten or invert the curve and pressure bank earnings.

-

📉 Banking sector contagion risk: The KBE dropped ~5% on March 2 in one of its most volatile sessions since the 2023 liquidity scare. If regional bank weakness spreads into sentiment around money center banks, JPM could get dragged down regardless of its fundamentals.

-

🏛️ Basel III reversal risk: While consensus expects a capital-neutral outcome, any surprise increase in capital requirements would restrict JPM's ability to return capital and could force the stock lower. Regulatory outcomes are inherently binary.

-

💸 $19.8B tech spend must deliver ROI: JPM's technology budget exceeds most fintech companies' entire revenue. If AI productivity gains don't materialize into measurable operating leverage by mid-2026, this becomes a cost drag rather than a competitive advantage.

🎯 The Bottom Line

Real talk: An institutional player just put $2.1M on the line betting JPMorgan bounces back from this 10% pullback, and the thesis isn't hard to understand. You've got the world's most valuable bank, coming off a record year ($57B net income!), trading at a modest 14.9x earnings, with a stacked catalyst calendar over the next 3.5 months. The Z-Score of 4.62 tells you this isn't an everyday trade - this level of conviction at a single strike shows up only a handful of times per year.

What this trade tells us:

- 🎯 Institutional money sees the 10% pullback as a buying opportunity, not a warning sign

- 💰 The near-ATM $305 strike signals moderate conviction - this is "recovery to fair value" not "moonshot"

- 📊 The June expiration is strategically chosen to capture earnings, Basel III, and the Fed Chair transition

- 🏦 The $2.1M size and 4.62 Z-Score say this is fund-level capital, not a speculative punt

If you own JPM:

- ✅ The fundamental case remains strong - 20% ROTCE, $50B buyback authorization, 2% dividend yield

- 📊 Consider selling April covered calls at $320-$330 to generate income during the pullback

- 🛡️ Watch $300 support carefully - a decisive break below could trigger the next leg down toward $287

- 📅 Q1 earnings on April 14 is the next major confirmation event for the bull thesis

- 💪 13 Buy ratings, 9 Holds, 0 Sells with an average target of $333-$346 -- no analysts are telling you to sell

If you're watching from the sidelines:

- 🎯 A pullback to $290-$295 (near implied move support) would be an attractive entry point for the long-term

- 📊 Wait for Q1 earnings clarity on NIM trajectory and Apple Card credit quality before sizing in

- 🤝 Basel III finalization is the potential game-changer - a favorable ruling could unleash significant capital returns

- 💡 JPM trades at a premium to BAC (14.9x vs. 13.1x P/E) but the 20% ROTCE justifies it

If you're bearish:

- 📉 The yield curve twist and Dimon's own inflation warnings are legitimate headwinds

- 🎯 Baird's $280 target represents the downside case from a credible analyst

- ⚠️ Bear put spreads ($300/$285) offer defined-risk downside plays through earnings

- ⏰ Wait for a bounce back toward $310-$315 before initiating shorts - selling weakness at $302 is fighting gravity at support

Mark your calendar - Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $293.82-$307.54)

- 📅 March 20 - Triple Witch OPEX (implied range: $286.80-$314.56)

- 📅 April 14 - Q1 2026 earnings report (before market open)

- 📅 May 15 - Fed Chair Powell's term expires; Warsh transition

- 📅 H1 2026 - Basel III Endgame finalization expected

- 📅 June 18 - Expiration of this $2.1M institutional call trade

Final verdict: This $2.1M call buy is a statement trade from smart money: JPMorgan's pullback is overdone, and the catalyst calendar is too loaded to stay down here. The world's most profitable bank at 14.9x earnings with a 20% ROTCE, sitting on excess capital, with earnings, Basel III relief, and a bank-friendly Fed Chair transition all on the horizon? That's a setup worth paying attention to. The institutional buyer doesn't need a home run - just a 3.8% bounce to $313.75 to break even, and the analyst consensus says there's 10-15% of upside from here. Whether you follow the whale or not, the message is clear: the fundamentals haven't changed, even if the price has. 👀

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 4.62 reflects this specific trade's unusualness relative to recent activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About JPMorgan Chase & Co.: JPMorgan Chase is the world's most valuable bank by market cap ($802.5B), operating as the largest U.S. financial institution with $4.4T+ in assets across consumer banking, corporate & investment banking, commercial banking, and asset & wealth management. Headquartered at 270 Park Avenue, New York.