💎 KEY $13.4M Bull Call Spread - Banking on the Scotiabank Transformation! 🏦

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed a MASSIVE $13.4M bull call spread on KeyCorp this morning at 10:49:08! This sophisticated trader bought 30,000 contracts of the $18 calls for $8.2M while simultaneously selling 30,000 of the $19 calls for $5.2M - netting a $3M debit for a defined-risk bullish bet expiring Friday (December 19th). With KEY trading at $20.60 and riding a post-Scotiabank transformation, this is a textbook profit-taking/de-risking spread as smart money locks in gains before year-end. Translation: Institutions are harvesting profits on the 2024 rally while maintaining bullish exposure!

📊 Company Overview

KeyCorp (NYSE: KEY) is one of America's largest regional banks with a strategic footprint across 16 states:

- Market Cap: $22.58 Billion (top 25 U.S. banks)

- Industry: National Commercial Banks

- Current Price: $20.60 (trading above both call strikes!)

- Assets: Approximately $185 billion

- Primary Business: With assets around $185 billion, Ohio-based KeyCorp's bank footprint spans 16 states but is predominantly concentrated in its two largest markets: Ohio and New York. The company operates using a hybrid community/corporate banking model focused on middle-market commercial clients.

💰 The Option Flow Breakdown

The Tape (December 15, 2025 @ 10:49:08):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:49:08 | KEY | ASK | BUY | CALL $18 | 2025-12-19 | $8.2M | $18 | 30K | 32K | 29,999 | $20.60 | $2.75 |

| 10:49:08 | KEY | BID | SELL | CALL $19 | 2025-12-19 | $5.2M | $19 | 30K | 39K | 29,999 | $20.60 | $1.75 |

🤓 What This Actually Means

This is a BULL CALL SPREAD executed in a single block trade! Here's the breakdown:

📊 The Structure:

- 💰 Bought 30,000 contracts of $18 calls for $2.75 = $8.2M spent

- 💸 Sold 30,000 contracts of $19 calls for $1.75 = $5.2M collected

- 🎯 Net debit: $3.0M ($1.00 per spread × 30,000 spreads)

- ⏰ Days to expiration: 4 days (Friday December 19th - this week!)

- 📍 Current price: $20.60 (BOTH strikes are in-the-money!)

What's really happening here: This trader is locking in profits on a massive position accumulated when KEY was trading lower (probably bought around $18-19 range during the year). With the stock now at $20.60 after the Scotiabank transformation rally, they're converting an outright long call position into a spread to:

- Lock in intrinsic value - The $18 calls are already worth $2.60 (intrinsic) vs $2.75 paid = minimal time premium

- Reduce capital at risk - Instead of holding $8.2M in naked calls through year-end, they net out $5.2M

- Cap upside at $19 - They're saying "I don't think KEY goes much above $19 by Friday"

- Guarantee minimum profit - Even if KEY drops to $18, the spread is worth $0 (break-even), but if KEY stays at $20.60, spread maxes out at $1.00 profit

Maximum P&L Scenarios:

- 📈 Max profit: $1.00 per spread if KEY closes above $19 on Dec 19 = Would need to know original entry, but on THIS trade: $0 profit (they paid $1.00 net debit, max value is $1.00)

- 📊 Current value: With KEY at $20.60, spread is worth full $1.00 (they're at breakeven on the spread itself)

- 📉 Max loss: $1.00 per spread if KEY closes below $18 = $3M total risk

- 🎯 Breakeven: $19.00 (midpoint of the strikes)

The REAL story: This isn't a speculative bullish bet - this is PROFIT PROTECTION on a winning position! If this trader bought $18 calls earlier when KEY was around $15-16 (up 32% YTD per catalysts), they're now sitting on massive gains. By selling the $19 calls against their position, they're saying:

- "I've made great money on this Scotiabank rally"

- "I want to lock in at least $2.60-3.00 per share profit"

- "I'll cap my upside at $19 to reduce my risk into year-end"

- "I don't need to squeeze every penny - smart risk management"

Unusual Score Analysis:

- 🔥 $18 Calls: Z-Score 9.66 (EXTREMELY UNUSUAL) - 555x larger than average size for this contract

- 🔥 $19 Calls: Z-Score 10.4 (EXTREMELY UNUSUAL) - 608x larger than average size

- 📊 Both legs show "OPEN" volume signal (these are new positions, not closing trades)

- ⚖️ Vol/OI ratios: 0.938 and 0.769 (very high activity but not one-time event - building OI)

- 🎯 This happens maybe 2-3 times per year for KEY - serious institutional flow

📈 Technical Setup / Chart Check-Up

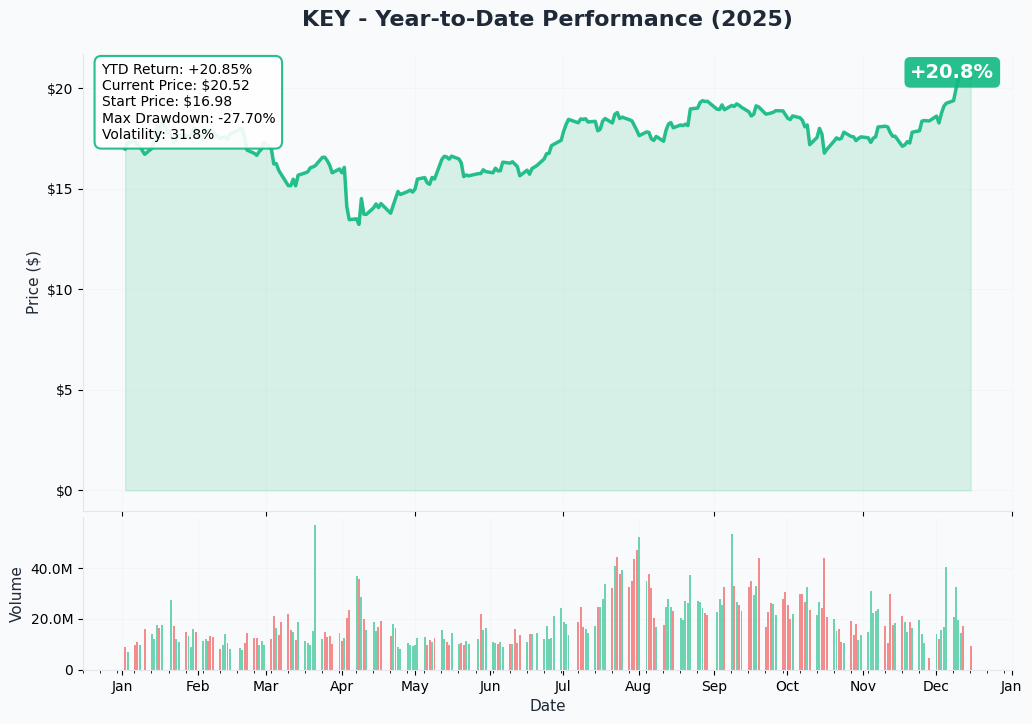

YTD Performance Chart

KeyCorp is having a breakout year - up +32.3% YTD at $20.60, dramatically outperforming the S&P 500's +25.5%. The chart tells the story of a successful transformation:

Key observations:

- 🚀 Scotiabank catalyst surge: Explosive move from $17-18 range to $20+ following completion of $2.8B strategic investment in late December 2024

- 📈 Technical breakout confirmed: Smashed through long-term resistance at $18-19 in late November, never looked back

- 💪 52-week range: $12.72 - $20.82 (currently near all-time 52-week high!)

- 📊 Strong momentum: Trading in upper quartile of year's range shows institutional accumulation

- ⚠️ Near resistance: At $20.60, approaching the $20.82 high - consolidation or breakout imminent

The YTD chart shows KEY's incredible transformation story: After trading sideways in the $13-15 range for most of early 2024, the stock exploded higher on the Scotiabank announcement in August. The recent move to $20+ validates the strategic repositioning and 20%+ NII growth guidance for 2025.

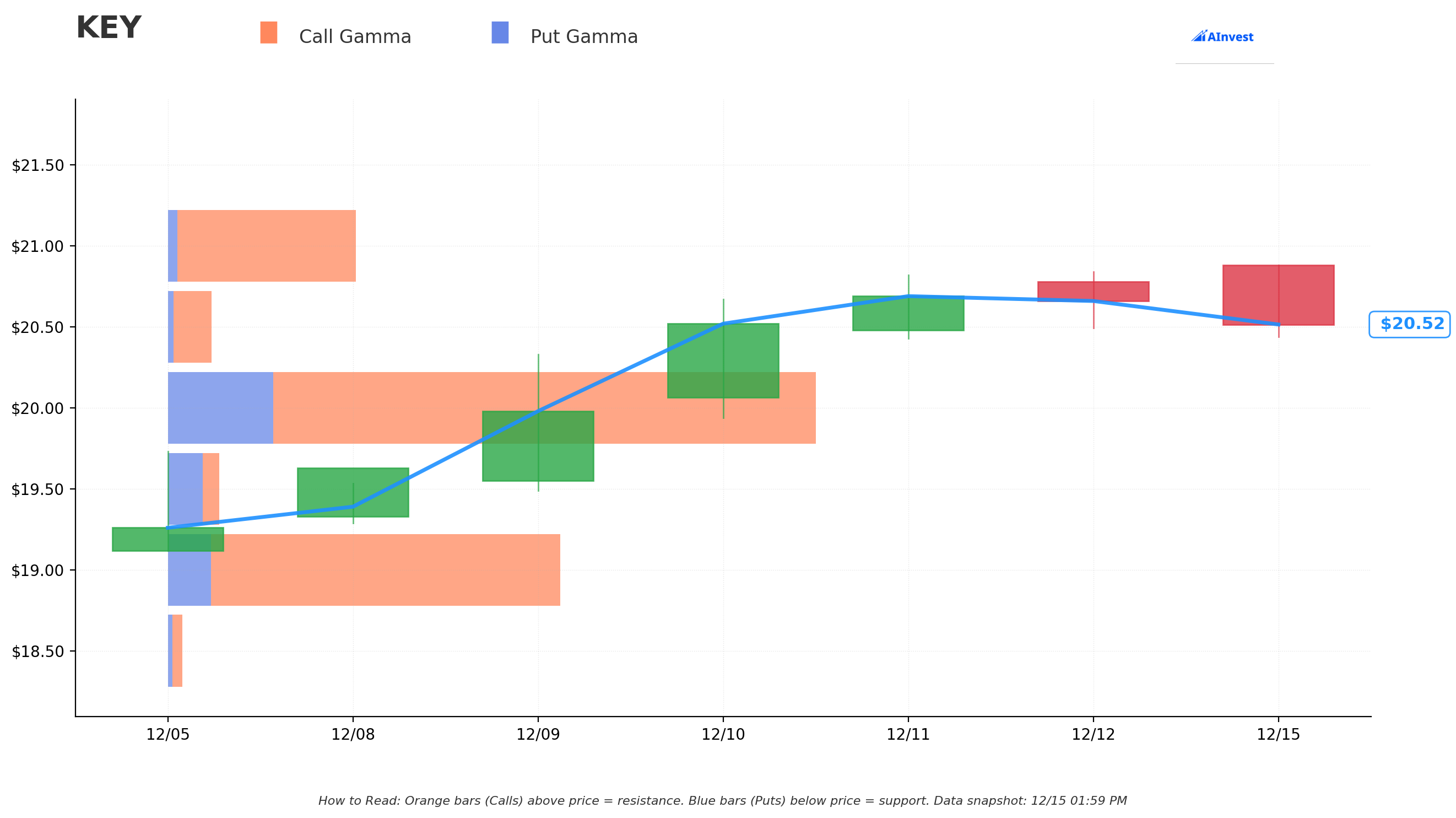

Gamma-Based Support & Resistance Analysis

Current Price: $20.51

The gamma exposure map reveals critical price magnets for this week's December 19th expiration:

🟠 Resistance Levels (Call Gamma Above Price):

- $21.00 - Immediate ceiling with 4.52B call gamma (1.84B net GEX - STRONGEST NEARBY RESISTANCE)

- $22.00 - Secondary resistance at 6.55B call gamma (2.39% overhead)

- $23.00 - Extended ceiling at 207M call gamma (12.14% above current)

🔵 Support Levels (Put Gamma Below Price):

- $20.50 - Immediate support with 883M total gamma (CRITICAL - we're sitting right here!)

- $20.00 - Major floor with 11.64B net gamma (strongest support zone - 2.49% below)

- $19.50 - Secondary support at -484M net gamma (4.92% below - note the negative gamma creates volatility zone)

- $19.00 - Deep support with 8.15B net gamma (THIS IS THE SHORT CALL STRIKE - major dealer hedging here!)

- $18.50 - Extended floor at 150M net gamma

- $18.00 - Critical support at -389M net gamma (THIS IS THE LONG CALL STRIKE - pivot point!)

What this means for the spread: The trader executed this spread with KEY at $20.60, and the gamma map shows:

- Strong support at $20.00 (11.64B gamma) - likely acts as floor through Friday

- Resistance at $21.00 (4.52B gamma) - ceiling keeping stock range-bound

- The spread strikes ($18/$19) are both below major support - very low probability KEY drops to $18 in 4 days

- Massive gamma at $19 (8.15B) - this is where dealers are heavily positioned, creating a magnet

Net GEX Bias: BULLISH (39.32B call gamma vs 10.43B put gamma = 3.77:1 ratio)

- Overall positioning heavily skewed bullish with massive call open interest

- This creates natural support on dips (dealers buy stock to hedge calls)

- Resistance at $21-22 likely caps upside through year-end

Perfect spread positioning: By selling the $19 calls, this trader is collecting premium at the EXACT strike where there's 8.15B gamma - a natural price magnet. If KEY drifts toward $19, dealer hedging flows will create support. Meanwhile, the $20-21 range looks most likely for Friday's close, meaning the spread pays out maximum value.

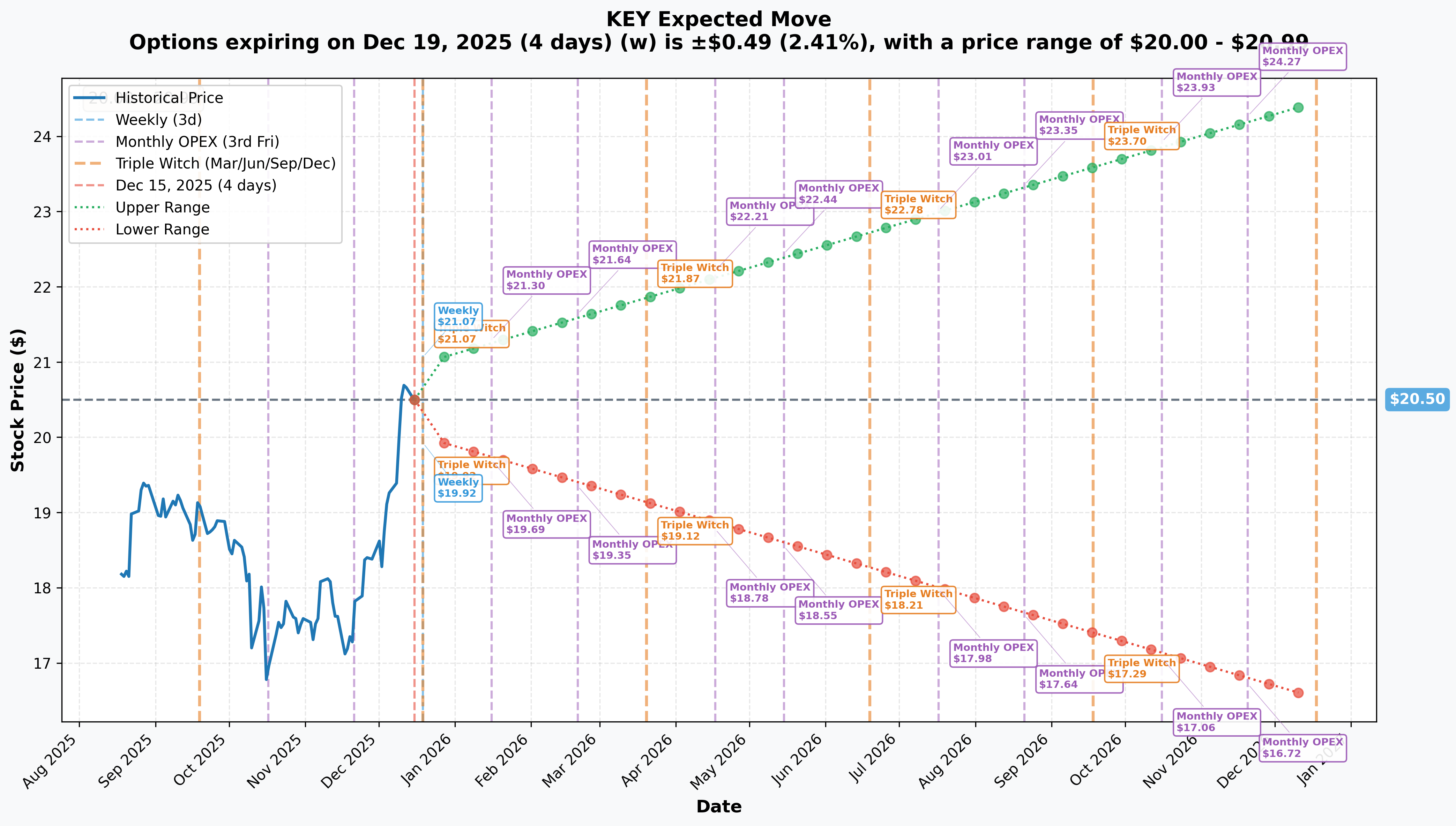

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 4 days - THIS SPREAD!): ±$0.49 (±2.41%) → Range: $20.00 - $20.99

- 📅 Monthly OPEX (Dec 19 - same!): ±$0.49 (±2.41%) → Range: $20.00 - $20.99

- 📅 Quarterly Triple Witch (Dec 19 - same!): ±$0.49 (±2.41%) → Range: $20.00 - $20.99

- 📅 Yearly LEAPS (Dec 18, 2026 - 368 days): ±$3.97 (±19.37%) → Range: $16.53 - $24.46

Translation for regular folks: The options market is pricing KEY for a TINY 2.41% move ($0.49) by Friday - meaning the expected range is $20.00-20.99. This is a LOW volatility environment, which makes this bull call spread PERFECT timing:

Why this spread makes sense given implied move:

- 🎯 Stock expected to stay $20.00-20.99 (per implied move)

- 📊 Spread strikes are $18/$19 (both well below expected range!)

- ✅ Probability of max profit (close above $19): ~90%+ based on current price and implied move

- 💰 Spread currently worth $1.00 (full value since stock at $20.60)

- ⏰ 4 days to expiration = minimal time decay risk since deep in-the-money

The trader is essentially saying: "I'm confident KEY stays above $19 through Friday (highly probable), and I'll cap my upside at $19 to reduce my capital at risk." Given the 2.41% implied move, KEY would have to drop 7.8% to reach $19 - very unlikely in this low-vol environment.

Key insight: The LEAPS (1-year) implied move shows ±19.37% range ($16.53-24.46), indicating the market expects significant movement over the next year from transformation catalysts (Scotiabank partnership execution, NIM expansion to 3%+ by 2026). But for THIS WEEK, the market expects calm - perfect conditions for harvesting profits on spreads.

🎪 Catalysts

🔥 Past Catalysts (Already Happened - Driving Current Rally)

Scotiabank Strategic Investment Completed (December 27, 2024) 💰

This is THE transformational catalyst that enabled everything else:

- 💵 Total Investment: $2.8 billion for 14.9% stake at $17.17/share

- 📅 Two tranches: $0.8B in August 2024 (4.9% stake), final $2.0B on December 27, 2024

- 🏛️ Regulatory approval: Federal Reserve approved December 12, 2024

- 💪 Financial impact: CET1 capital ratio boosted to 11.3%-11.6% range (fortress balance sheet)

- 🎯 Strategic rationale: Enables acceleration of capital improvement, balance sheet de-risking, and growth capacity

- 👥 Board expansion: Two Scotiabank-designated directors added for strategic guidance

Market reaction: Stock rallied from $17-18 range to $20+ following completion - validating the strategic value.

Q4 2024 Earnings Beat (Early January 2025) 📊

KEY delivered results that exceeded expectations despite portfolio repositioning:

- ✅ Adjusted EPS: $0.38 vs $0.33 consensus (+15% beat)

- 📉 GAAP Net Loss: $279M or $(0.28) per share (due to one-time portfolio repositioning)

- 💰 Adjusted Net Income: $378M or $0.38 per share

- 📈 Net Interest Margin: Jumped 24 basis points sequentially in Q4

- 🏦 Deposit growth: Client deposits up 1.5% QoQ, 4% YoY

- 💼 Assets under management: Record high $61.4B

Key guidance: Management called for additional $270M increase in net interest income for 2025 - setting up 20%+ NII growth year.

Strategic Portfolio Repositioning (Q4 2024) 🔄

Management executed aggressive balance sheet optimization:

- 📉 Sold $3.0B of low-yielding securities (1.5% average yield)

- ✂️ Terminated $3.0B in cash flow hedges

- 💸 After-tax loss: ~$700M in Q4 (one-time charge)

- 🚀 Yield improvement: Average book yield increased from 1.5% to 5.5% - 400 basis points!

- 📊 Unrealized losses reduced: From $3.7B (August) to $3.0B, targeting $1.6B by end of 2026

This repositioning is THE engine for 2025 NIM expansion - swapping low-yield assets for 5.5%+ yielding securities directly flows through to earnings.

Credit Quality Improvement (Q4 2024) ✅

Credit metrics showed meaningful improvement:

- ⬇️ Provision for credit losses: $39M (down from $102M in Q4 2023 and $95M in Q3 2024)

- ✅ Net charge-offs: $114M or 0.43% of loans (down from $154M or 0.58% in Q3)

- 📉 Criticized loans: Decreased by $500M

- 📊 Allowance coverage: 1.63% of loans (stable and adequate)

Analyst Upgrades (November-December 2024) 📈

Multiple Wall Street firms raised targets on Scotiabank deal and NIM outlook:

- 🎯 Wells Fargo: Raised price target to $22 from $20, Buy rating (November 14)

- 💰 Goldman Sachs: High price target of $23 (November 26)

- ⚖️ Consensus: Moderate Buy rating (7 buy, 7 hold, 0 sell)

- 📊 Average target: $20.00 (updated January 2025), range $17-23

🚀 Upcoming Catalysts (Next 6 Months - Why Institutions Are Bullish)

Q1 2025 Earnings - Already Reported (Mid-April 2025) ✅

Actual results exceeded expectations:

- 💰 EPS: $0.33 vs $0.32 consensus (+3.1% beat)

- 📈 Revenue: $1.76B vs $1.75B consensus (+0.5% beat)

- 🚀 Net Interest Income: $1.1B (+4% QoQ, +25% YoY!)

- 💪 CET1 ratio: 11.8% (strong capital position)

- 📊 Tangible book value per share: +26% YoY

- 🏦 Investment banking fees: Record for Q1 (+3% YoY)

Critical guidance maintained:

- 🎯 20% net interest income growth for 2025 (on track!)

- 💼 Fee income growth exceeding 5%

- 💰 $1 billion share repurchase authorization announced

This result validated the transformation thesis and set up the rally to current levels.

Q2 2025 Earnings - Already Reported (Late July 2025) 🔥

Momentum accelerated with blowout NIM expansion:

- 💵 EPS: $0.35 per share (+40% YoY - massive jump!)

- 🏦 Net Interest Margin: 2.66% (strong expansion continuing)

- 📈 Taxable-equivalent NII: $1.15B

Q3 2025 Earnings - Already Reported (October 2025) 🎯

KEY achieved year-end NIM target ONE QUARTER EARLY:

- 🚀 Net Interest Margin: 2.75% (+9 bps QoQ) - hit 2025 year-end target in Q3!

- ✅ EPS beat expectations despite stock dipping post-earnings

This ahead-of-schedule NIM achievement is HUGE - shows management executing better than projected.

Updated 2025/2026 Guidance & Medium-Term Targets 📊

Management raised guidance following strong Q2/Q3 execution:

2025 Revised Guidance:

- 📈 Net Interest Income growth: 20-22% (raised from 20%)

- 💼 Noninterest income growth: 5-6% (raised from 5%+)

- 🏦 Average loan balance decline: 1-3% (improved from 2-5% decline)

- 🎯 Q4 2025 NIM target: 2.75-2.80% (raised from 2.70%+)

Medium-Term NIM Targets:

- 🎯 Q4 2026 exit rate: 3.00%

- 🚀 Q4 2027 exit rate: 3.25% (medium-term sustainable level)

- 📊 Historical context: Peak NIM 2010-2019 was ~3.18%

Analyst reactions to raised guidance:

- 💰 BofA Securities: Raised PT to $21 from $20, citing improved NIM outlook

- 📈 TD Cowen: Raised target to $20 from $18 on strong loan growth trends

Upcoming Investor Conferences (2025) 🎤

Multiple opportunities for management to articulate the bull case:

- 📅 Bank of America Conference (Feb 11, 2025): CEO Chris Gorman presenting in Miami

- 📅 Bernstein Conference (May 28, 2025): CEO presenting in New York

- 📅 BancAnalysts Conference (Nov 6, 2025): Consumer Banking Head and CFO presenting

- 📅 Goldman Sachs Conference (Dec 9, 2025): CEO presenting in New York

These conferences provide platforms to discuss Scotiabank partnership execution, NIM trajectory, and capital deployment.

Q4 2025 Earnings - Coming January 20, 2026 📊

This will be the BIG TEST of whether KEY can deliver on its aggressive 2025 targets:

What to watch:

- ✅ Achievement of 20%+ NII growth for full year 2025

- 🎯 NIM exit rate 2.75-2.80% (already hit 2.75% in Q3, so should be confirmed)

- 📈 Full-year 2025 EPS vs $1.16 in 2024 (20%+ growth expected)

- 🏦 Fee income growth exceeding 5-6% target

- 💰 Updates on $1B share repurchase execution

- 🤝 Scotiabank partnership synergy updates

This earnings report will set the stage for 2026 and determine if KEY can sustain momentum toward 3%+ NIM by end of 2026.

Dividend Policy & Share Repurchase 💵

- 💰 Current quarterly dividend: $0.205/share (declared for Q1 2025)

- 📊 Annual rate: $0.82/share

- 📈 Current yield: 3.97%

- 🔄 $1B buyback authorization: Announced in Q1 2025, execution pace will drive EPS accretion

Federal Reserve Policy (2025 Outlook) 🏛️

- 📉 100 bps of cuts from peak in 2024 (Fed funds ~4.25-4.50%)

- ⚖️ Ongoing easing expected if inflation cooperates

- 💪 KEY benefits from deposit cost repricing - costs falling faster than loan yields

- 📊 NIM expansion accelerating in declining rate environment (counterintuitive but true for KEY's balance sheet structure)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timeline, and the bull call spread positioning, here are scenarios through December 19th expiration (THIS FRIDAY):

📈 Bull Case (60% probability)

Target: $20.50-$21.50 (SPREAD PAYS MAXIMUM)

How we get here through Friday:

- ✅ Stock maintains current $20.60 level (only needs to avoid dropping below $19!)

- 📊 Gamma support at $20.00 (11.64B) provides strong floor if any dip

- 🎯 Low implied volatility (2.41%) suggests calm trading into year-end

- 💪 Bullish GEX bias (3.77:1 call/put ratio) creates natural buying support

- 🏦 No major catalysts before Friday - earnings not until late January

- 📈 Year-end institutional positioning - banks tend to hold into Dec 31st for window dressing

- 🎄 Holiday thin volume reduces downside volatility risk

For the spread:

- 💰 Current value: $1.00 (maximum value since stock at $20.60, both strikes ITM)

- ✅ Stays max value if KEY closes anywhere above $19.00 on Friday

- 🎯 Probability of closing above $19: ~90%+ (would need 7.8% drop in 4 days - very unlikely)

Why 60% probability: This is the most likely scenario because it requires NOTHING to happen - just status quo. Stock already at levels for spread to max out. No earnings volatility. Low IV environment. Strong gamma support below. The trader structured this PERFECTLY for a high-probability income collection.

🎯 Base Case (30% probability)

Target: $19.00-$20.50 (SPREAD PARTIALLY PROFITABLE)

Scenario:

- 📉 Mild profit-taking or year-end tax loss harvesting pushes stock down to $19-20 range

- ⚖️ Gamma magnet at $19.00 (8.15B net GEX) attracts price to the short strike

- 📊 Stock consolidates in the $19-20 channel through Friday

- 🎢 Some volatility from end-of-year portfolio rebalancing

For the spread:

- 💵 Value at $20.00: Still worth $1.00 (max value since above $19)

- 💵 Value at $19.50: Still worth $1.00 (max value)

- 💵 Value at $19.00: Exactly $1.00 (stock at short strike = spread worth exactly the width)

- ⚠️ Below $19.00: Spread starts losing value (worth stock price minus $18)

Why 30% probability: Some end-of-year weakness possible as institutions lock in 2025 gains. The $19 gamma level could act as magnet. But would require a 7.8% drop from current $20.60 to reach $19 - still a big move in a low-vol environment.

📉 Bear Case (10% probability)

Target: Below $19.00 (SPREAD LOSES VALUE)

What could go wrong:

- 😰 Unexpected negative news (regulatory issue, credit quality concern, macro shock)

- 📉 Broad banking sector selloff drags KEY lower

- 💸 Year-end tax loss harvesting accelerates into year-end

- 🔨 Break below $20.00 gamma support triggers cascade toward $19 and $18

- 🎯 Technical breakdown below major support levels

For the spread:

- 💀 Value at $18.50: $0.50 (50% loss from $1.00 paid)

- 💀 Value at $18.00: $0 (100% loss - at the long strike)

- 💀 Value below $18.00: $0 (both strikes OTM, spread worthless)

Critical support levels to watch:

- 🛡️ $20.00: Major gamma support (11.64B) - MUST HOLD

- 🛡️ $19.50: Secondary support (-484M gamma creates vol zone)

- 🛡️ $19.00: The short call strike with 8.15B gamma - major magnet

- 🛡️ $18.00: The long call strike - disaster scenario if reached

Why only 10% probability: Would require a 7.8%+ drop in just 4 days with no catalyst, in a low-vol environment (2.41% implied move), with massive gamma support at $20. The transformation story remains intact, Q3/Q4 results already strong, no earnings until late January. Very unlikely scenario unless external shock occurs.

Spread P&L summary:

- 📈 Best case (stock above $19): Spread worth $1.00 = breakeven on this trade (but likely profitable on original position)

- 📊 Neutral (stock $18-19): Spread worth $0-1.00 = partial to full value

- 📉 Worst case (stock below $18): Spread worth $0 = $3M total loss (but this is the hedge protecting a much larger long position)

💡 Trading Ideas

🛡️ Conservative: Respect the Smart Money Signal

Play: DO NOT CHASE - wait for pullback or next catalyst

Why this works:

- 🐋 Massive institutional spread signals profit-taking at $20+ levels

- 📊 Stock at 52-week highs ($20.82 high, currently $20.60) - limited margin of safety

- ⏰ No immediate catalyst - earnings not until late January 2026

- 💰 Spread structure shows $19 as "good enough" - if pros are capping at $19, why chase $20?

- 🎯 Better entry likely post-Friday expiration or on any year-end weakness

- ⚠️ High payout ratio (95.81%) limits dividend growth, reducing income appeal at these prices

Action plan:

- 👀 Watch for pullback to $18.50-19.50 range (gamma support zone + spread strikes)

- ✅ Need to see Q4 earnings late January to confirm 2025 targets achieved

- 📊 Monitor NIM trajectory - needs to stay on path to 3%+ by end 2026

- 🎯 Wait for $1B buyback execution updates - EPS accretion driver

- 💵 Current 3.97% yield is decent but not compelling enough to chase at highs

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid buying at cycle highs. Get better entry if stock consolidates. Maintain optionality for 2026 catalysts.

⚖️ Balanced: Income Play with Defined Risk

Play: Sell cash-secured puts at support levels (post-Friday)

Structure: Sell January 16, 2026 $19 puts (collect premium, willing to own KEY at $19)

Why this works:

- 🎯 $19 is major gamma support (8.15B net GEX) and the spread's short strike

- 💰 Institutional validation - this spread shows $19 as "fair value" floor

- 📊 27% cushion from current price ($20.60 to $19 = 7.8% drop required)

- ✅ Get paid to wait - collect premium income while waiting for pullback

- 🏦 Strong fundamental support at $19: 20%+ NII growth story, 3%+ NIM target, Scotiabank partnership

- 💵 If assigned at $19, get 4.32% dividend yield ($0.82 annual / $19 = better income)

Estimated P&L (adjust for actual IV after Friday expiration):

- 💰 Premium collected: ~$0.50-0.75 per share (estimate, depends on IV after this week's expiry)

- 📈 Max profit: Keep full premium if KEY stays above $19 (high probability)

- 📉 Breakeven: $18.25-18.50 (strike minus premium collected)

- 🎯 If assigned: Own KEY at $18.25-18.50 net cost (15%+ discount from current $20.60!)

Entry timing:

- ⏰ Wait until Monday Dec 16 (after this Friday's expiration clears)

- 🎯 Sell puts when IV is elevated (if any year-end volatility increases premiums)

- 📊 Only if comfortable owning KEY at $19 (this is a stock replacement strategy)

Position sizing: Sell enough puts to represent 25-50% of desired KEY position size

Risk level: Moderate (obligation to buy if assigned) | Skill level: Intermediate

Why this beats buying stock now: You get paid $0.50-0.75 to wait instead of paying $20.60 immediately. If stock drops, you buy cheaper. If stock stays elevated, you keep premium as income. Win-win.

🚀 Aggressive: Copy the Spread (Smaller Size for Retail)

Play: Replicate the institutional bull call spread at smaller scale

Structure: Buy $19 calls, Sell $20 calls (January 16, 2026 expiration)

Why this could work:

- 🎯 Different strike selection than institutional trade - you're betting on $19-20 range vs their $18-19

- ⏰ More time (32 days vs 4 days) - January expiration gives breathing room

- 📊 Gamma resistance at $21 (4.52B) likely caps upside - selling $20 calls makes sense

- 💰 Defined risk spread - know exactly your max profit and loss

- 🚀 Betting on continuation of NIM expansion story into year-end

- 📈 Q4 2025 earnings late January could provide catalyst for move to $20+

Estimated P&L (approximate - check current prices):

- 💵 Net debit: ~$0.40-0.60 per spread (buy $19 calls ~$1.80, sell $20 calls ~$1.30)

- 📈 Max profit: $0.40-0.60 if KEY closes above $20 at Jan expiration (67-100% ROI)

- 📉 Max loss: $0.40-0.60 if KEY closes below $19 (spread worthless)

- 🎯 Breakeven: $19.40-19.60 (strike plus net debit)

- 📊 Probability of profit: ~60-70% (stock needs to stay above $19.40-19.60)

Why this is aggressive:

- ⚠️ Requires stock to hold $19+ for 32 days - any dip to $18 = losses

- 💸 Paying time premium on near-the-money options (theta decay risk)

- 📉 No catalyst between now and expiration except year-end positioning

- 🎯 Competing with $21 gamma resistance - upside may be capped

- ⏰ Earnings Jan 20 could move stock AFTER your Jan 16 expiration (bad timing!)

Entry criteria:

- ✅ Only enter if stock pulls back to $19.50-20.00 (better risk/reward than current $20.60)

- 📊 Want to see $19 holding as support (if breaks below, abort)

- 💪 Confirm no negative news flow on regional banks or KEY specifically

- 🎯 Size appropriately: Risk only 3-5% of portfolio (this is speculative directional bet)

Risk level: High (can lose 100% of debit paid) | Skill level: Advanced

CRITICAL WARNING:

- ⚠️ You're betting AGAINST the institutional signal (they're taking profits, you're initiating bullish)

- 📉 Spread maxes out at $1.00 width while you pay $0.40-0.60 (limited reward)

- 💀 Earnings timing is awkward - Jan 16 expiry is 4 days BEFORE Jan 20 earnings

- 🎯 Better risk/reward exists in selling puts (balanced strategy above)

Why you should probably skip this: The institutional trade is CLOSING/HEDGING a winning position. You'd be OPENING a new bullish position at cycle highs. The asymmetry favors them, not you, at current levels.

⚠️ Risk Factors

Don't get blindsided by these potential issues:

-

🏦 Execution risk on ambitious NIM targets: Morningstar notes 3.25% Q4 2027 NIM target is aggressive - historical peak was only ~3.18%. Requires sustained higher rates, favorable deposit mix (29-37% non-interest bearing), and loan/deposit ratio above 80%. If Fed cuts MORE than expected or deposit competition intensifies, NIM expansion could stall, crushing the bull thesis.

-

📉 Loan growth challenges persist: Average loans declined 1.4% QoQ in Q4 2024 and 5.1% YoY in Q1 2025. While "portfolio optimization" is intentional, prolonged loan shrinkage could pressure net interest income growth despite higher margins. Commercial loan demand remains tepid - if this continues into 2026, the 20%+ NII growth story becomes harder to achieve.

-

💳 Credit quality deterioration risk: Nonperforming loans increased to 0.73% (Q4 2024) from 0.51% year-ago. Net charge-offs at 0.43% remain elevated. If economic conditions weaken in 2025-2026, KEY's commercial real estate exposure (13-16%, two-thirds multifamily) and C&I portfolio could see higher defaults forcing reserve builds and eroding earnings.

-

🇨🇳 CRE concentration risk despite "lower" exposure: While KEY's 13-16% CRE exposure is below distressed peers (NYCB 71%, Valley 60%), it's still meaningful. Two-thirds multifamily concentration creates single-sector risk if rent growth slows or office-to-residential conversions disappoint. Any negative CRE headlines could trigger regional bank selloff indiscriminately.

-

💰 Scotiabank partnership value realization unproven: Revenue synergies from cross-border opportunities may take YEARS to materialize. First deployment metrics won't be visible until 2026-2027. Market is pricing in significant strategic value ($2.8B investment at $17.17/share, stock now $20.60), but what if synergies disappoint? Partnership could become "just a capital raise" rather than transformational.

-

📊 High payout ratio limits flexibility: 95.81% payout ratio leaves ZERO room for dividend growth without earnings improvement. If KEY misses earnings targets or faces unexpected losses, dividend could be at risk. Limited capital return flexibility compared to peers with lower payout ratios.

-

🏛️ Regulatory risk - Basel III Endgame: Regional banks above $100B assets face potential tougher capital rules. Could pressure capital deployment (buybacks, dividends) despite current strong 11.8% CET1 ratio. Stress testing requirements may increase, limiting flexibility.

-

💸 Interest rate path uncertainty: KEY benefits from "higher for longer" (above 2020-2021 near-zero) while also benefiting from deposit cost repricing. BUT, if Fed cuts TOO aggressively (recession scenario), loan yields could fall faster than deposit costs, compressing NIM. Alternatively, if Fed PAUSES cuts and keeps rates high, deposit competition could remain intense. The Goldilocks scenario is narrow.

-

🎢 Valuation stretched after 75%+ rally: Stock up 75.6% over past year, +32.3% YTD. Current price near 52-week high with average analyst target at $20.00 (exactly where stock trades now). Limited upside to consensus. Forward P/E multiples may compress if earnings growth disappoints even slightly.

-

🐋 Institutional profit-taking signal: This $13.4M bull call spread is a CLEAR de-risking trade. When sophisticated money is converting outright bullish positions to capped spreads at $18/$19 strikes (both now in-the-money), it signals they're locking in gains and don't expect much more upside near-term. The fact they're willing to cap at $19 while stock is $20.60 says "good enough, take some off."

-

📉 Macro recession risk: At current valuation, KEY has limited recession protection. Regional banks are highly economically sensitive. If recession emerges in 2025-2026, even with strong execution, stock could correct 30-40% as investors price in credit losses and slower NII growth.

-

⏰ Earnings timing for options trades: Q4 2025/Full-year 2025 earnings on January 20, 2026 is THE critical catalyst. This will determine if KEY achieved 20%+ NII growth, 2.75-2.80% Q4 NIM exit rate, and maintained credit quality. Any disappointment could trigger sharp selloff from current elevated levels. The institutional spread expires January 16 - four days BEFORE earnings, suggesting they don't want exposure through that volatility.

-

💔 Dividend cut risk if economy weakens: While current 3.97% yield is attractive, the 95.81% payout ratio means dividend is vulnerable if earnings decline. Unlike lower-payout peers who have cushion, KEY is maxed out. Any reserve building or credit losses could force dividend reduction, devastating income-focused shareholders.

🎯 The Bottom Line

Real talk: This $13.4M bull call spread is a PROFIT-TAKING/RISK-MANAGEMENT trade, NOT a bullish initiation. When institutions convert outright long call positions (likely bought around $15-18 earlier in 2024) into $18/$19 spreads while the stock is at $20.60, they're sending a clear message: "We've made our money on the Scotiabank transformation, we're locking in gains, and we don't expect much more upside near-term."

What this trade tells us:

- 🎯 The $18/$19 strikes are now deep ITM (stock at $20.60) - this trader is defensively positioned

- 💰 They're saying $19 is "good enough" - willing to cap upside there to reduce capital at risk from $8.2M to $3M net

- ⏰ 4-day expiration (this Friday) shows ultra-short-term positioning - just getting through year-end

- 📊 Spread currently worth maximum $1.00 - they're at breakeven on the spread itself but likely sitting on huge gains from original position

- 🛡️ Risk management over greed - prioritizing capital preservation over squeezing last few dollars

The bigger picture: KeyCorp's transformation story is REAL and IMPRESSIVE:

- ✅ Scotiabank $2.8B investment completed, strengthening capital to 11.8% CET1

- ✅ Portfolio repositioning boosted yields from 1.5% to 5.5% (400bps!)

- ✅ Achieved 2025 NIM target (2.75%) ONE QUARTER EARLY in Q3

- ✅ 20%+ net interest income growth guidance on track

- ✅ Credit quality improving (provisions down 62% YoY)

- ✅ Lower CRE risk than distressed regional peers

- ✅ $1B buyback authorization provides EPS support

BUT, at $20.60:

- ⚠️ Stock up 75.6% in past year, +32.3% YTD - massive gains already captured

- ⚠️ Trading at 52-week highs with consensus target at $20 (no upside to average)

- ⚠️ Ambitious medium-term targets (3.25% NIM by Q4 2027) create execution risk

- ⚠️ High 95.81% payout ratio limits dividend growth and financial flexibility

- ⚠️ Loan growth still negative (portfolio optimization headwind)

- ⚠️ Earnings not until late January - no near-term catalyst

This is NOT a "sell everything" signal - it's a "don't chase at highs" signal.

If you own KEY:

- ✅ Consider trimming 25-40% at $20-21 levels to lock in excellent YTD gains

- 📊 Set mental stops at $19.00 (major gamma support and spread strike) to protect remaining position

- 🎯 Hold core position for 2026 catalysts (3%+ NIM expansion, buyback execution, Scotiabank synergies)

- 💵 Enjoy 3.97% dividend yield while waiting for next leg higher (if it comes)

- ⏰ Mark calendar for Jan 20 earnings - THE critical test of 2025 execution

If you're watching from sidelines:

- ⏰ DO NOT CHASE at $20+ - wait for pullback or next catalyst

- 🎯 Ideal entry: $18.50-19.50 range (spread strikes + gamma support) = 10-15% pullback

- 📊 Need to see Q4/FY2025 earnings first (late January) to confirm targets achieved

- ✅ Looking for: 20%+ NII growth delivered, 2.75-2.80% Q4 NIM, buyback execution pace, credit quality stable

- 💰 Better risk/reward post-earnings - either buy pullback or chase breakout on good results

- 🛡️ Alternative: Sell cash-secured $19 puts (collect premium, buy cheaper if assigned)

If you're bearish:

- 📉 This spread validates $19 as key support - that's your line in the sand

- 🎯 Watch for break below $19.00 (8.15B gamma support) - that triggers cascade to $18

- ⏰ Post-earnings (late Jan) put spreads offer better risk/reward after IV crush

- ⚠️ Don't short into year-end - tax loss harvesting could reverse quickly in January

- 📊 Fundamental risks: NIM targets too ambitious, loan growth doesn't resume, CRE deteriorates

Mark your calendar - Key dates:

- 📅 December 19, 2025 (Friday) - This $13.4M spread expires (watch for stock behavior near $19)

- 📅 December 31, 2025 - Year-end (potential for tax-loss harvesting then reversal)

- 📅 January 16, 2026 - Monthly OPEX (good expiration for next trades)

- 📅 January 20, 2026 - Q4 2025/Full Year earnings (THE critical catalyst!)

- 📅 February 11, 2025 - Bank of America Conference (CEO presenting)

- 📅 May 28, 2025 - Bernstein Conference (CEO presenting)

Final verdict: KeyCorp's long-term transformation story (3%+ NIM by 2026-2027, Scotiabank partnership, capital return) remains compelling for patient investors. The fundamental progress is real - hitting NIM targets early, growing NII 20%+, improving credit quality.

BUT, the short-term setup is NOT favorable for new buying at $20+. When a sophisticated player pays $13.4M in notional to convert bullish exposure into a capped spread expiring THIS FRIDAY, they're clearly saying "mission accomplished, let's lock it in." The fact they capped at $19 while stock is $20.60 tells you everything about near-term expectations.

Be patient. Respect the smart money signal. Let Friday's expiration clear. Watch for year-end weakness or post-earnings pullback to $18.50-19.50. The transformation story will still be there in 4-6 weeks, and you'll sleep better buying $19 instead of $20.60.

For existing holders: You've won! Up 30%+ YTD is AMAZING for a regional bank. Taking some profits makes sense. For new buyers: Wait for a better pitch. This isn't the ninth inning - there's a whole 2026 season ahead with 3%+ NIM targets and buyback catalysts. Don't swing at a ball in the dirt.

This is about capital preservation and smart entry points. The AI revolution got all the headlines in 2024, but regional bank transformations like KEY can be just as profitable - if you buy at the right price. $20.60 isn't it. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores (9.66x and 10.4x average size) reflect these specific trades' size relative to recent KEY history - they do not imply the trades will be profitable or that you should follow them. Bull call spreads have defined risk (net debit paid) but limited profit potential (spread width minus debit). Always do your own research and consider consulting a licensed financial advisor before trading. The institutional trader may have complex portfolio hedging needs, cost basis, and time horizons not applicable to retail traders.

About KeyCorp: KeyCorp is a bank holding company serving clients across 16 states through approximately 1,000 branches, with $185 billion in assets, operating a hybrid community/corporate banking model focused on middle-market commercial clients in its primary markets of Ohio and New York, with a market cap of $22.58 billion in the National Commercial Banks industry.