🛡️ KMB $822K Call Buyback - Closing Short Ahead of Mega-Merger! 💰

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just spent $822,000 buying to close 2,000 call contracts on Kimberly-Clark (KMB) this morning at 09:51:46! This wasn't a new bullish bet - it's a trader closing out a previous short call position on the $115 strike expiring March 20, 2026. With KMB at $107.87 and sitting in the middle of two massive transformative deals (a $48.7B Kenvue acquisition and a $3.4B Suzano joint venture both closing mid-2026), smart money is taking risk off the table. Translation: Someone who was betting KMB wouldn't rally above $115 is now covering that bet for $4.11 per share.

📊 Company Overview

Kimberly-Clark Corporation (KMB) is a household name in hygiene and personal care with brands you use every day:

- Market Cap: $36.02 Billion

- Industry: Converted Paper & Paperboard Products (consumer staples)

- Current Price: $107.87 (in the middle of 52-week range of $99.22 - $150.45)

- Primary Brands: Huggies (diapers), Kleenex (tissue), Kotex (feminine care), Depend (adult incontinence), Scott (paper products)

- Geographic Mix: 50%+ North America, 10%+ Europe, remainder Asia/Latin America

- Employees: 38,000 globally

Big Picture: KMB is in the middle of a MASSIVE transformation - acquiring Kenvue (the Johnson & Johnson spinoff with brands like Tylenol, Band-Aid, Listerine, Neutrogena) for $48.7 billion while simultaneously selling off its international tissue business to Suzano for $3.4 billion. Both deals are expected to close in the second half of 2026, creating a $32 billion consumer health and wellness powerhouse.

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 09:51:46):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:51:46 | KMB | ASK | BUY | [115C 03/20] | 2026-03-20 | $822K | $115 | 2K | 27K | 2,000 | $107.87 | $4.11 |

🤓 What This Actually Means

This is a closing trade on a short call position - here's what went down:

- 💸 Premium paid: $822,000 ($4.11 per contract × 2,000 contracts)

- 🛡️ Strike price: $115 provides 6.6% cushion above current price of $107.87

- ⏰ Time remaining: 108 days to March 20, 2026 expiration

- 📊 Existing open interest: 27,000 contracts at this strike (this trader bought back 7.4% of total OI)

- 🎯 Confidence level: LOW per classification system

- 📈 Volume/OI ratio: 0.074 (very low activity level)

What's really happening here: This trader previously SOLD these $115 calls (collecting premium upfront) betting that KMB would stay below $115 by March expiration. With the stock at $107.87, those calls are currently worth $4.11 each and are out-of-the-money. So why buy them back now instead of just letting them expire worthless?

Three possible reasons:

- 🚀 Risk management ahead of catalysts: Q4 earnings coming January 27-28 could move the stock significantly, and with 108 days to expiration, there's plenty of time for KMB to rally above $115 if the Kenvue deal gets more clarity or earnings surprise

- 💰 Taking profits early: If the trader sold these for $6-7 back when the stock was higher ($115-120 range in early 2025), they're locking in a $2-3 profit per share rather than waiting for full expiration and risking a rally

- 📊 Freeing up capital/margin: Closing the short calls releases the margin requirement, allowing deployment into other opportunities

Unusual Score: 🔥 TYPICAL (Z-score 0.3) - This is actually NOT unusual activity by recent standards. The trade ranks as typical size with only 5 similar trades in recent history. The volume/OI signal is "LOW_ACTIVITY" and the strategy is classified as "Close Short Call" with LOW confidence. This is routine portfolio management, not a major institutional signal.

📈 Technical Setup / Chart Check-Up

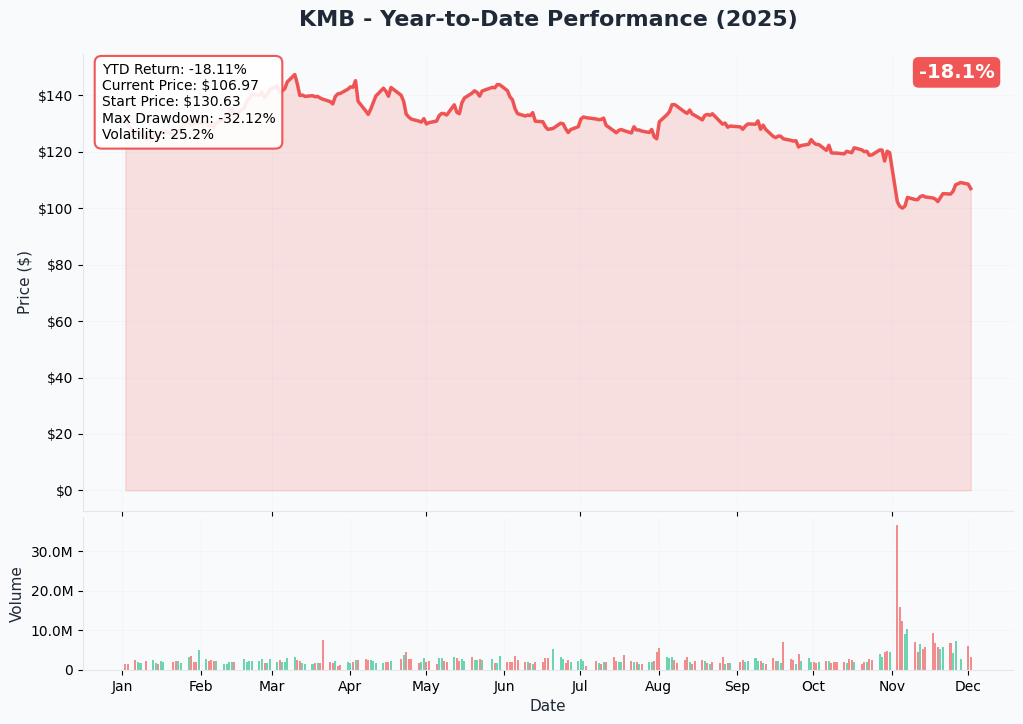

YTD Performance Chart

KMB is having a ROUGH year - currently at $106.84, the stock is down approximately -19.3% over the past year from the 52-week high of $150.45 hit in early 2025. The chart tells a story of optimism turned to caution:

Key observations:

- 📉 Major decline: From $150 peak to $99.22 low - a brutal 34% drawdown

- 🎢 High volatility: The stock has been in a steady downtrend since the Kenvue acquisition announcement on November 3, 2025

- 💔 Market reaction: KMB shares fell 14% the day the $48.7B Kenvue deal was announced (while KVUE surged 12%)

- 📊 Current positioning: Trading near the lower end of the range at $106.84

- ⚠️ Recovery attempt: Slight bounce from the $99 lows, but no clear trend reversal yet

The market is clearly skeptical about the Kenvue mega-merger - investors worried about integration risk, regulatory approval, and the massive debt load required for a $48.7B acquisition that's larger than KMB's entire market cap.

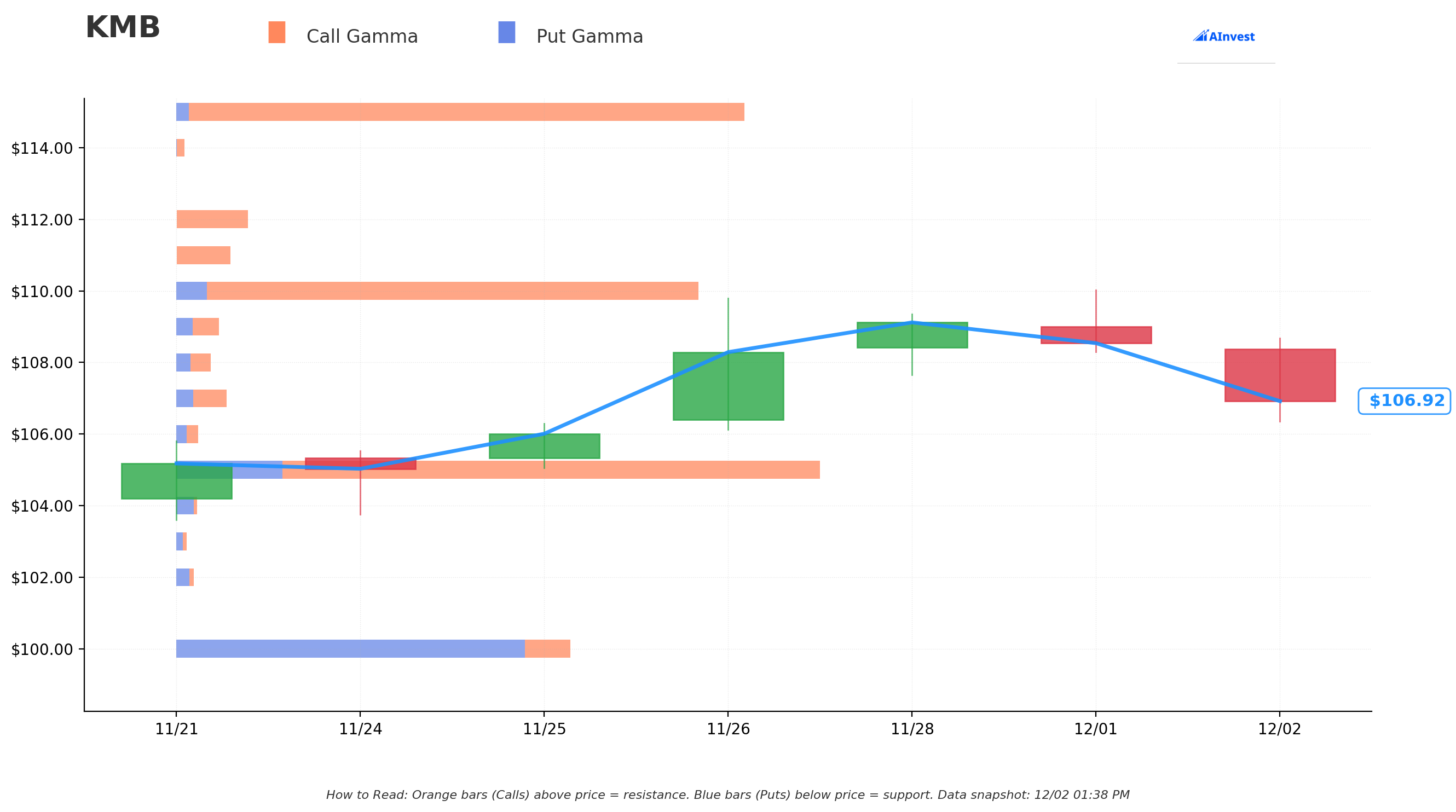

Gamma-Based Support & Resistance Analysis

Current Price: $106.84

The gamma exposure map reveals critical price magnets and barriers for near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $105 - Immediate support with 16.8B total gamma (STRONGEST SUPPORT - massive floor!)

- This is THE critical level to watch - huge call gamma (14.1B) plus put gamma (2.7B)

- Only 1.7% below current price - very nearby safety net

- $100 - Secondary support at 10.2B gamma

- Psychological round number with significant put gamma (9.0B)

- 6.4% below current price - would take a major catalyst to break

- $95 - Deep support at 1.5B gamma

- 11.1% below current - disaster scenario territory

🟠 Resistance Levels (Call Gamma Above Price):

- $107 - Immediate ceiling with 1.3B gamma (very close!)

- Just 0.15% overhead - essentially at current price

- $110 - First major resistance at 13.5B gamma (SIGNIFICANT BARRIER)

- 3.0% above current price - this is where rallies will stall

- Heavy call gamma (12.7B) creates natural dealer selling pressure

- $111-112 - Secondary resistance cluster at 1.4B + 1.8B gamma

- 3.9% to 4.8% above current

- $115 - Major resistance at 14.7B gamma (THIS IS WHERE THE TRADE IS!)

- 7.6% above current price

- Heavy call gamma (14.4B) - the exact strike of this $822K closing trade

- Notice the trader closed shorts HERE for a reason - this is a massive gamma wall

- $120 - Extended resistance at 4.0B gamma

- 12.3% rally required

- $125 - Distant ceiling at 1.2B gamma

- 17.0% above current - would need multiple positive catalysts

What this means for traders: KMB is sitting RIGHT AT the $107 resistance level with massive support just below at $105. The stock is effectively trapped in a tight $105-$110 range, with $110 representing the first serious resistance barrier (13.5B gamma). The fact that the call seller closed at the $115 strike is very telling - that's where 14.7B in gamma creates an almost impenetrable ceiling. To reach $115 from current levels would require a 7.6% rally, and the options market shows that level has the second-highest gamma concentration on the entire chain.

Notice anything? The 115C 03/20 strike where this trader closed their short calls sits at a MASSIVE gamma resistance level with 14.7B total exposure. This trader likely sold these calls when KMB was trading $115-120+ earlier in 2025, and now that the stock has dropped to $107, they're closing for a profit while acknowledging that $115 is a very unlikely target by March 2026 expiration.

Net GEX Bias: Bullish (54.6B call gamma vs 19.1B put gamma) - Overall positioning is bullish with nearly 3:1 call/put gamma ratio, but the stock price action suggests this is mostly protection/resistance rather than aggressive bullish positioning.

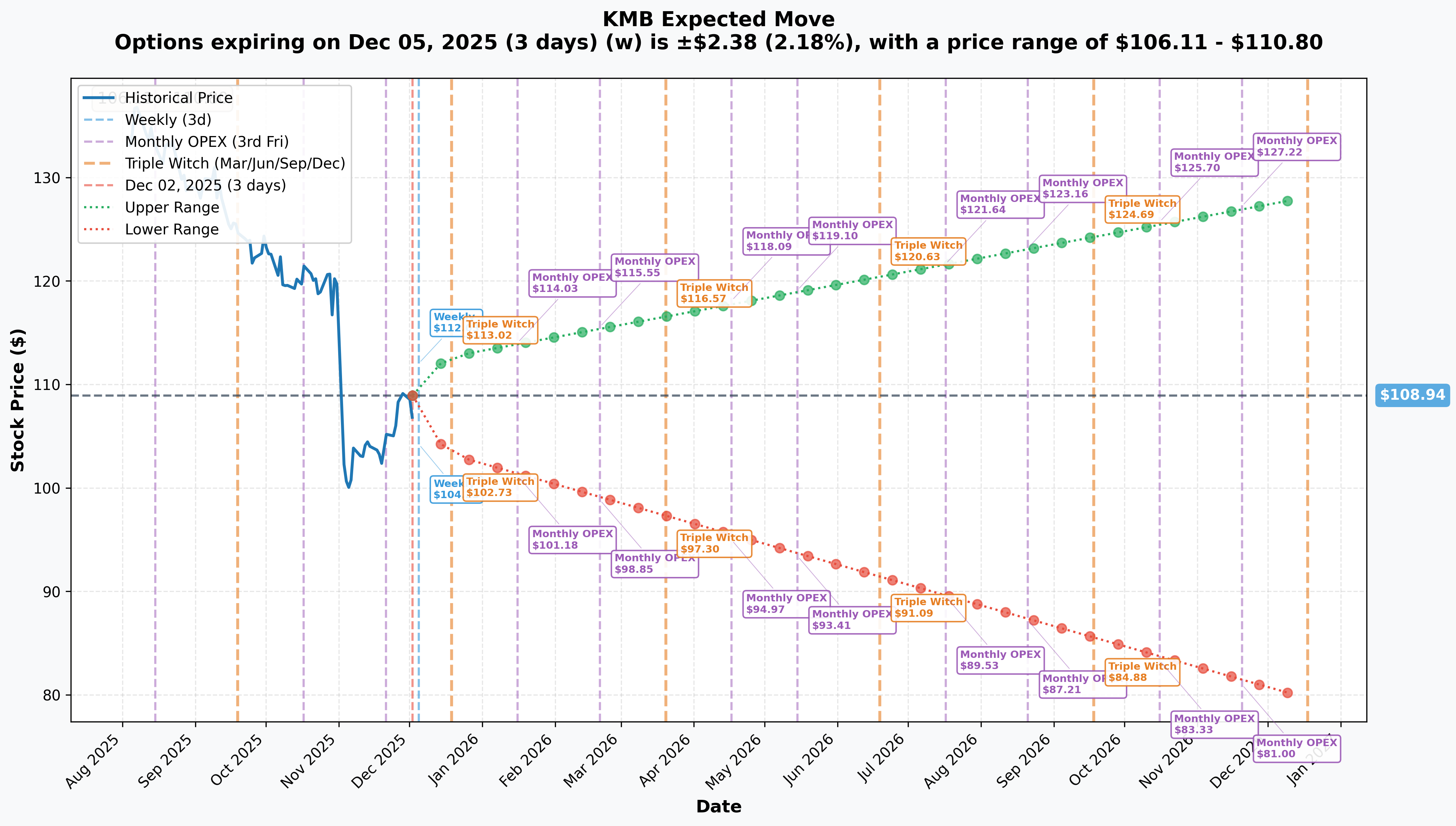

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 5 - 3 days): ±$2.38 (±2.18%) → Range: $106.11 - $110.80

- 📅 Monthly OPEX (Dec 19 - 17 days): ±$4.44 (±4.08%) → Range: $103.18 - $112.72

- 📅 Q4 Earnings (Jan 27-28 - ~56 days): Not directly priced, but falls between monthly periods

- 📅 March OPEX (Mar 20 - 108 days - THIS TRADE!): Estimated ±$8-9 (±7-8%) → Range: $100-116

- 📅 LEAPS (Dec 2026 - 381 days): ±$21.29 (±19.54%) → Range: $79.64 - $128.11

Translation for regular folks: Options traders are pricing in a quiet week ahead with only 2.2% expected movement ($2.38), and a relatively modest 4% move through December monthly expiration. This reflects KMB's status as a stable, boring consumer staples stock with a 4.6% dividend yield.

However, the bigger picture is fascinating: Over the next year (LEAPS), the market is pricing in a MASSIVE 19.5% potential move in either direction - ranging from $79.64 on the downside to $128.11 on the upside. This huge range reflects the binary nature of the Kenvue mega-merger:

- 🚀 Bull case ($128+): Deal closes successfully, $1.9B in synergies materialize, combined $32B revenue powerhouse delivers

- 📉 Bear case ($79-80): Deal falls apart due to regulatory issues or is repriced lower, KMB stuck with declining margins and market share losses

The March 20, 2026 expiration (when this 115C 03/20 expires) falls right in the middle of this uncertainty - after Q4 earnings (Jan 27-28) but BEFORE the Kenvue/Suzano deals close (H2 2026). The call seller who just closed recognized that reaching $115 by March requires a 7.6% rally, which would need very strong earnings AND meaningful deal progress - not impossible, but unlikely enough to justify taking profits now.

🎪 Catalysts

🔥 Immediate Catalysts (Next 60 Days)

Q4 2025 / Full Year 2025 Earnings - January 27-28, 2026 (56 DAYS AWAY!) 📊

KMB reports Q4 and full-year results in late January. This is THE near-term catalyst that could provide direction. Wall Street expectations and key items to watch:

- 📊 Q4 EPS Consensus: $1.65-$1.82 per analyst estimates

- 💰 Full Year 2025 Guidance (from Oct 30): Low-to-mid single-digit constant-currency adjusted EPS growth

- 🚀 Organic Sales Target: Broadly in line with ~2% weighted average category growth

- 💪 Productivity: Target 5-6% of adjusted COGS in savings (Q3 achieved 6.5% - exceeding target!)

- 🌍 Currency Headwind: 100 basis points negative impact expected on reported sales

Q3 2025 results (reported Oct 30) were solid:

- ✅ Revenue: $4.15B vs $4.09B consensus (1.5% beat)

- ✅ EPS: $1.82 vs $1.75 consensus (4% beat)

- ✅ Organic sales growth: 2.5% (up from 1.6% YTD)

- ✅ Volume growth: 2.4%

- ✅ Stock rose 3% in premarket on results

What to watch in Q4:

- 🎯 Tariff mitigation progress: KMB faces $300M in tariff costs in 2025 (two-thirds from 145% China tariffs, one-third from retaliatory tariffs). Management said they'll mitigate one-third in 2025 and the remainder in 2026. Q4 commentary on this progress is critical.

- 📉 Margin trends: Q3 operating margin compressed to 15% from 24.8% YoY. Need to see stabilization.

- 🌏 International market share: Q3 showed strong gains in China diapers (+270 bps), South Korea (+230 bps), Brazil (+90 bps), Indonesia (+150 bps). Continuation is bullish.

- 🛒 Private label pressure: Private label reached 27.8% U.S. market share - need to see KMB defending share

- 💵 Free cash flow: Q3 FCF margin compressed to 8.9% from 19.3% YoY - concerning trend that needs improvement

Why this matters for the options trade: The 115C 03/20 expires March 20, which is ~50 days AFTER earnings. If Q4 results disappoint or guidance is conservative, the stock could easily stay range-bound $100-110, making the call seller's decision to close at $4.11 look very smart. Conversely, if earnings crush and provide Kenvue deal clarity, the stock could rally toward $115, which would have made holding the short calls painful.

🚀 Major Catalysts (H1-H2 2026)

1. Kenvue Acquisition Close - H2 2026 (THE TRANSFORMATIONAL EVENT) 🤝

Announced November 3, 2025, this is the single biggest catalyst in KMB's history:

- 💰 Deal Value: $48.7 billion total, $40 billion equity value

- 📄 Terms: $3.50 cash + 0.14625 KMB shares per KVUE share = $21.01 total consideration

- 🏢 Combined Company: $32 billion in annual revenue (vs KMB standalone ~$16B)

- 💪 Combined EBITDA: $7 billion

- 🎯 Synergies: $1.9 billion expected in first 3 years post-close

- 🏭 Brands Added: Tylenol, Band-Aid, Listerine, Neutrogena joining Huggies, Kleenex, Kotex, Scott (10 billion-dollar brands total!)

- 📊 Ownership: KMB shareholders will own ~54% of combined company

- 🕐 Expected Close: Second half of 2026 (regulatory approval pending)

Market Reaction - Mixed Signals:

- 📈 KVUE shares surged 12% on announcement

- 📉 KMB shares fell 14% on announcement (!!!!)

- ⚠️ Market pricing in significant deal risk and Tylenol litigation uncertainties

- 🎰 KVUE currently trading below $21.01 offer price, suggesting arb spread/deal uncertainty

Why the market is skeptical: The deal is LARGER than KMB's entire market cap ($48.7B vs $36B). This creates massive integration risk, debt concerns, and execution uncertainty. Additionally, Kenvue carries Tylenol-related litigation risks that some investors don't want to inherit. However, if successful, this creates a dominant consumer health powerhouse.

Bull case for the deal:

- 🌐 Creates #1 or #2 player across 10 major consumer categories

- 💪 $1.9B synergies = massive margin expansion opportunity

- 🛒 Better negotiating leverage with retailers (Walmart, Target, etc.)

- 🔬 Combined R&D budgets accelerate innovation

- 🌍 Geographic diversification (Kenvue strong internationally)

Bear case for the deal:

- ⚖️ FTC antitrust review could block or require divestitures

- 💸 Integration of two large companies historically destroys value (50%+ of mega-mergers fail)

- 📉 KMB taking on significant debt to fund $48.7B acquisition at high interest rates

- ⚠️ Tylenol litigation exposure

- 🎯 Execution risk - Mike Hsu (KMB CEO) has to integrate 10 billion-dollar brands

Timeline impact on March calls: The 115C 03/20 expires March 20, 2026 - which is BEFORE the expected H2 2026 close. This means the calls will expire before the deal actually consummates. However, progress updates on regulatory approval (or lack thereof) could significantly impact the stock price between now and March.

2. Suzano Joint Venture Close - Mid-2026 🌲

Announced June 5, 2025, KMB is divesting its international tissue business:

- 💰 Enterprise Value: $3.4 billion

- 🤝 Structure: Suzano 51% ($1.73B cash to KMB), KMB retains 49% stake

- 🏭 Assets: 22 manufacturing facilities in 14 countries, 9,000 employees

- 🌍 Geography: Europe, Asia, Middle East, South America, Central America, Africa, Oceania

- 📦 Brands: Kleenex, Scott, Viva licensed to JV; 40+ regional brands owned

- 💵 2024 Net Sales: $3.3 billion contributed to venture

- ⏰ Expected Close: Mid-2026

- 📉 EPS Impact: $0.30-$0.40 dilutive in first full year post-close

Strategic Rationale: KMB is getting OUT of the low-margin international tissue business (operating at ~10% margins) to focus on higher-margin North American core brands. The transaction is expected to boost KMB's operating margins by 1-2% by shedding the drag of the international tissue unit.

Suzano is a Brazilian pulp giant with vertical integration that could slash costs 20% through optimized pulp sourcing. KMB retains 49% upside if the JV succeeds, plus gets $1.73B in cash to pay down debt from the Kenvue acquisition.

Why this matters: This is the "simplification" side of KMB's transformation - divest complexity, focus on core. Combined with the Kenvue acquisition, KMB is essentially swapping $3.3B in low-margin international tissue sales for much higher-margin consumer health products.

3. $300M Tariff Cost Mitigation Progress (Throughout 2025-2026) 🛡️

This is the silent killer affecting KMB's margins:

- 💸 Total Impact: $300 million incremental costs in 2025

- 🇨🇳 Breakdown: Two-thirds from 145% China tariffs, one-third from retaliatory tariffs by other countries

- 📦 Exposure: 20% of U.S. cost base is imported (80% manufactured locally, which helps)

- ⏰ Mitigation Timeline: One-third mitigated in 2025, remainder in 2026

- 🔧 Strategy: Redesigning logistics and operations (NOT immediate sourcing shifts to avoid tariffs)

CEO Mike Hsu stated the North America business will "bear the brunt" of tariff impacts. This $300M hit is why operating margins compressed so much in Q3 (15% vs 24.8% prior year).

Progress on mitigating these costs - either through operational efficiencies, price increases, or tariff policy changes - will be a key driver of margin recovery and stock performance. Each earnings call will update on this.

4. Productivity Program Milestones (Ongoing) 💪

KMB is executing a multi-year $3 billion efficiency program through network optimization and automation:

- 🎯 2025 Target: 5-6% of adjusted COGS in productivity savings

- ✅ Q3 Achievement: 6.5% (exceeded target!)

- 💰 Long-Term Goal: $3 billion in cumulative savings

- 🏭 Capital Investment: $2 billion over 5 years in North America (Warren, OH facility; Beech Island, SC distribution)

- 📊 Sources: Value stream initiatives, network optimization, scalable automation

The fact that Q3 exceeded the productivity target (6.5% vs 5-6% goal) is encouraging. This is helping offset the $300M tariff hit and private label margin pressure. Continued execution here is critical to reaching the long-term targets of 40% gross margins and 18-20% operating margins.

📊 Upcoming Market Events

Dividend Payment - January 5, 2026

- Amount: $1.26 per share quarterly dividend

- Yield: 4.6%

- Status: Dividend King (decades of consistent dividend growth)

KMB's hefty 4.6% yield provides significant downside protection and is a major reason many institutional investors hold the stock through periods of uncertainty like this mega-merger transition.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20, 2026 expiration (when the 115C 03/20 expires):

📈 Bull Case (20% probability)

Target: $118-125

How we get there:

- 💪 Q4 earnings (Jan 27-28) crush expectations with strong volume growth, margin expansion, and tariff mitigation progress

- 🚀 Kenvue deal regulatory approval progresses smoothly with FTC signaling comfort

- 📊 Management raises 2026 guidance citing confidence in both deals closing

- 🌏 International market share gains continue (China, Korea, Indonesia)

- 💰 Private label pressure eases as innovation pipeline delivers (new product launches gaining traction)

- ✅ Productivity savings continue to exceed targets (6.5%+ of COGS)

- 🎯 Breakout above $110 gamma resistance triggers technical momentum to $115, then $120

Key metrics needed:

- Q4 EPS $1.80+ (vs $1.65-1.82 consensus)

- Full year organic sales growth 3%+ (vs 2% target)

- Gross margins stabilizing or expanding

- Positive FTC commentary on Kenvue deal

- Tariff mitigation ahead of schedule

Probability assessment: Only 20% because it requires multiple things going RIGHT simultaneously while the stock is down 19% YTD and facing massive execution risk on the Kenvue merger. The gamma resistance at $110 (13.5B) and $115 (14.7B) creates significant headwinds. Would need a true fundamental catalyst to break through.

Call seller's P&L in this scenario: If KMB rallies to $120 by March 20, the $115 calls would be worth $5.00 intrinsic value. Since the seller closed at $4.11, they avoided a potential loss if they had originally sold for less than $9.11. However, if they sold these calls for $6-8 when KMB was trading $118-125 earlier in 2025, they locked in a profit of $1.89-3.89 per share by closing early rather than risking the stock rallying back.

🎯 Base Case (60% probability)

Target: $100-112 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Q4 earnings meet consensus (solid but not spectacular - $1.70-1.80 EPS)

- ⚖️ Guidance in-line for 2026, acknowledging Kenvue deal uncertainty

- 📊 Tariff mitigation progressing but slowly (still a headwind in early 2026)

- 🤝 Kenvue deal moving through regulatory process without major red flags, but no approval yet by March

- 💤 Market remains cautious on integration risk - stock stays range-bound

- 🔄 Trading within implied move range of $100-112 through March

- 📈 Gamma support at $105 prevents major downside, gamma resistance at $110 caps upside

- 💰 4.6% dividend yield provides floor for income investors

This is the scenario where closing the short calls makes perfect sense: The trader avoids the risk of a rally to $115+ while locking in profit from the stock's decline from $115-120 levels to current $107. The calls expire worthless or nearly worthless, and the trader can redeploy capital elsewhere.

Why 60% probability: This reflects the high uncertainty around the mega-merger. In the absence of major catalysts (earnings beat, regulatory approval), the stock likely consolidates in the $100-110 range as investors wait for more information. The gamma map supports this - tight range between $105 support and $110 resistance.

Call seller's P&L in this scenario: If KMB trades $100-110 through March 20, the $115 calls expire worthless or worth minimal extrinsic value. The seller who closed at $4.11 essentially gave up $0-4 in potential additional profit (if the stock dropped further) in exchange for eliminating the risk of a rally. This is classic risk management - take the bird in hand.

📉 Bear Case (20% probability)

Target: $90-100 (TEST THE SUPPORT)

What could go wrong:

- 😰 Q4 earnings disappoint - margins compress further, tariff mitigation behind schedule

- 🚨 Kenvue deal hits regulatory snag - FTC raises antitrust concerns or demands major divestitures

- ⚖️ Deal terms renegotiated lower (reducing KVUE consideration from $21.01)

- 💸 Credit rating agencies downgrade KMB due to massive debt load from Kenvue acquisition

- 🛒 Private label market share continues to surge (above 30%), forcing KMB to cut prices

- 🇨🇳 New tariffs announced or existing tariffs extended, adding to cost pressure

- 📉 Broader consumer staples selloff (recession fears, consumer spending weakness)

- 🔨 Break below $105 gamma support triggers cascade to $100, potentially $95

Critical support levels:

- 🛡️ $105: Major gamma floor (16.8B) - MUST HOLD or momentum shifts bearish

- 🛡️ $100: Psychological support (10.2B gamma) - deep floor with heavy put gamma

- 🛡️ $95: Disaster scenario (1.5B gamma)

Probability assessment: 20% because while risks are real, KMB has strong brands, 4.6% dividend yield provides downside support, and the Suzano JV provides $1.73B cash cushion. The company isn't going away - it's just navigating a complex transformation. However, a major Kenvue deal issue could trigger a sharp selloff.

Call seller's P&L in this scenario: In a bear case where KMB drops to $90-100, the $115 calls expire worthless, and the seller who closed at $4.11 looks like a genius. If they originally sold these for $6-8, they banked a $1.89-3.89 profit per share (minus the $4.11 buyback cost). The decision to close early was prudent risk management.

💡 Trading Ideas

🛡️ Conservative: Income Play with Downside Protection

Play: Buy stock at current levels ($107) for 4.6% dividend yield + sell covered calls above resistance

Why this works:

- 💰 Dividend safety: KMB is a Dividend King with decades of consistent growth, 4.6% yield ($1.26 quarterly)

- 🛡️ Strong support: $105 gamma floor just 1.7% below current price provides immediate safety net

- 📊 Low risk entry: Stock down 19% YTD, near 52-week lows - much of bad news priced in

- 🎯 Range-bound: Likely to trade $100-112 through March, perfect for covered call strategy

- ⏰ Time to catalyst: Q4 earnings in 56 days could provide clarity

Structure:

- Buy 100 shares KMB at ~$107 ($10,700 investment)

- Sell 1x March 20, 2026 112C 03/20 for ~$3.00-3.50

- Collect $126 dividend in January (goes ex-div in December)

Estimated P&L:

- 💰 Dividend income: $126 (1.2% return)

- 💵 Call premium: $300-350 (2.8-3.3% return)

- 📈 Total income: $426-476 (4.0-4.5% return in 3.5 months = 13-15% annualized!)

- 📊 Upside capped at $112 (4.7% stock gain) + premium + dividend = 8-9% total if called away

- 🛡️ Downside protected by $105 support and 4.6% yield

Action plan:

- ✅ Enter at $107 or below (wait for any dip to $105 for better entry)

- 📅 Sell March $112 calls (above $110 resistance, captures premium)

- 👀 Monitor Q4 earnings (Jan 27-28) - if stock rallies above $112, you're called away with healthy profit

- 🔄 If stock stays below $112, calls expire worthless, keep stock + premium, repeat next quarter

Risk level: Low (stock holding with income enhancement) | Skill level: Beginner-friendly

Expected outcome: Collect dividend + premium for 13-15% annualized return while waiting for merger clarity. If called away at $112, great! If not, keep collecting income.

⚖️ Balanced: Bull Put Spread at Support Levels

Play: Sell put spread targeting the $105-100 support zone

Structure: Sell 105P 01/16, Buy 100P 01/16 (January 16, 2026 expiration - post-earnings)

Why this works:

- 🎯 Gamma support: $105 strike sits at MASSIVE 16.8B gamma support - strongest level on entire chain

- 📊 Defined risk: $5 wide spread = $500 max risk per spread

- 💰 Post-earnings play: Wait until after Jan 27-28 earnings to enter (IV crush makes puts cheaper)

- 🛡️ High probability: Stock would need to drop 7%+ to reach max loss at $100

- ⏰ Time decay works for you: As seller, theta is in your favor

- 💵 Income generation: Bullish assumption that KMB holds $100+ floor

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$1.50-2.00 net credit per spread (30-40% max profit)

- 📈 Max profit: $150-200 if KMB above $105 at January expiration (keep entire credit)

- 📉 Max loss: $300-350 if KMB below $100 (defined and limited)

- 🎯 Breakeven: ~$103-103.50

- 📊 Risk/Reward: ~1.5:1 (good for defined-risk bullish play)

Entry timing:

- ⏰ Wait for Q4 earnings on January 27-28

- 📊 If earnings are in-line or better AND stock holds $105, enter the put spread

- ❌ Skip if stock breaks below $105 post-earnings (support broken)

- 🎯 Ideal entry: Stock at $107-110 with IV elevated from earnings

Position sizing: Risk only 3-5% of portfolio (this is directional income generation)

Why this is "copying the call seller's logic": Just like the call seller recognized that $115 was too far above current price to worry about, you're recognizing that $100 is too far below current price to worry about. You're selling the fear of a collapse below $100 to income-focused buyers.

Risk level: Moderate (defined risk, moderately bullish) | Skill level: Intermediate

Expected outcome: Collect $150-200 credit while KMB consolidates above $105 support. If earnings disappoint and stock drops toward $100, loss is capped at $300-350.

🚀 Aggressive: Long Call Spread Betting on Merger Clarity (ADVANCED)

Play: Buy call spread targeting $110-115 if Q4 earnings provide Kenvue deal clarity

Structure: Buy 110C 03/20, Sell 115C 03/20 (March 20, 2026 expiration - SAME as the closing trade!)

Why this could work:

- 🎰 Betting that the trader who CLOSED the 115C 03/20 short calls is TOO cautious

- 📊 If Q4 earnings are strong AND Kenvue deal gets FTC approval signaling, stock could rally to $115+

- 💰 Defined risk: Call spread caps max loss (vs buying naked calls)

- 🚀 $110-115 captures the gamma resistance zone breakout

- ⏰ March expiration gives 108 days for deal clarity to emerge

- 📈 Implied move suggests $100-116 range - targeting the upper end

Why this could blow up (SERIOUS RISKS):

- 💸 Expensive entry: Call spreads cost real money, and KMB IV is low for a reason (boring stock)

- ⏰ Execution risk: Kenvue deal could stall in regulatory process

- 😱 Gamma resistance: $110 (13.5B) and $115 (14.7B) are MASSIVE walls - tough to break through

- 📊 Range-bound stock: KMB has been stuck in $100-115 range for months - trend is sideways, not up

- 🎢 Only 20% probability of bull case materializing

Estimated P&L:

- 💰 Cost: ~$2.00-2.50 debit per spread (using March 20 expiration)

- 📈 Max profit: $3.00-3.50 if KMB above $115 at expiration (60-120% ROI)

- 📉 Max loss: $2.00-2.50 if KMB below $110 at expiration (100% loss)

- 🎯 Breakeven: ~$112-112.50

Entry conditions:

- ⏰ ONLY enter if Q4 earnings (Jan 27-28) beat expectations significantly

- 📊 Need to see positive FTC commentary on Kenvue deal

- 🚀 Need stock to hold $107+ and show momentum

- ❌ Do NOT enter if earnings are in-line or disappoint

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Believe Kenvue deal will get regulatory approval ahead of schedule

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand gamma resistance at $110 and $115 creates significant barriers

- ✅ Are betting AGAINST the trader who just closed $115 short calls for $822K

- ⏰ Plan to take profits quickly if stock rallies to $112-113 (don't hold to expiration hoping for $115)

Risk level: HIGH (directional bet against resistance) | Skill level: Advanced only

Probability of profit: ~30% (lower than implied 50% due to gamma resistance)

Why this is the contrarian play: You're essentially taking the OPPOSITE side of the $822K closing trade. That trader said "$115 is too high - I'm closing my short calls." You're saying "I think $115 is reachable if deal progresses." This is high-risk speculation.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🤝 Mega-Merger Integration Risk - THE BIG ONE: The $48.7B Kenvue acquisition is LARGER than KMB's entire $36B market cap. This is a bet-the-company transaction. If it fails regulatory approval, gets repriced lower, or integration destroys value (50%+ of mega-mergers fail historically), the stock could crater to $80-90. KMB shares fell 14% the day it was announced while KVUE surged 12% - the market is skeptical. Any negative regulatory news would trigger sharp selloff.

-

⚖️ FTC Antitrust Review Uncertainty: The combined KMB-Kenvue entity creates a $32B consumer staples giant with 10 billion-dollar brands across multiple categories. The FTC could demand significant divestitures or block the deal entirely. Timeline is unclear - deal won't close until H2 2026 at earliest, creating 12+ months of uncertainty. Current deal spread (KVUE trading below $21.01 offer) shows market pricing in meaningful deal risk.

-

💸 Massive Debt Load from Acquisition: KMB will take on significant debt to fund the $48.7B purchase at a time when interest rates remain elevated. This constrains financial flexibility, limits buyback capacity, and creates refinancing risk if rates stay high. Credit rating agencies could downgrade, raising borrowing costs further.

-

🛒 Private Label Pressure Intensifying: Private label reached 27.8% U.S. market share and continues growing. Retailers like Walmart, Target, and Costco are aggressively pushing store brands that offer 30-50% savings vs KMB's Huggies/Kleenex/Scott. This forces KMB to either cut prices (margin compression) or lose volume (revenue decline). Q3 operating margins already compressed to 15% from 24.8% - trend worsening.

-

💰 $300M Tariff Headwind Persisting: The $300M incremental tariff costs (two-thirds from 145% China tariffs, one-third from retaliatory tariffs) are only being mitigated one-third in 2025. This means $200M headwind carries into 2026. Management stated North America will "bear the brunt". If new tariffs get imposed or existing ones extended, the hit could exceed $300M.

-

📉 Operating Margin Collapse: Q3 operating margin of 15% vs 24.8% prior year is ALARMING. Q2 gross margin declined 180 bps to 35.0%. The combination of tariffs, private label pricing pressure, and unfavorable mix is destroying profitability despite productivity gains. Long-term targets of 40% gross margins and 18-20% operating margins look increasingly unrealistic without major changes.

-

🇨🇳 International Market Weakness: International Personal Care showed YTD organic growth of only 0.8% (though Q3 improved to 2.1%). Q1 2025 saw -2.8% organic sales decline and -19.8% operating profit decline internationally. China's deflationary pricing environment is persisting, compressing margins. China paper imports surged 33% in FY25, intensifying competitive pressure.

-

💔 Free Cash Flow Compression: Q3 FCF margin of 8.9% vs 19.3% prior year is a major red flag. While management attributed this to working capital timing, the trend is concerning. If FCF doesn't recover, dividend safety comes into question despite Dividend King status. The 4.6% yield is only sustainable if cash generation holds up.

-

🎯 Suzano JV Dilution: The $3.4B international tissue sale to Suzano is expected to be $0.30-0.40 dilutive in the first full year post-close. While it improves margins by shedding low-margin business, it's still a $3.3B revenue hole that needs to be filled by the Kenvue acquisition. If Kenvue deal falls apart, KMB will be left smaller and weaker.

-

📊 Dramatic Q1 Guidance Cut Shows Limited Visibility: In Q1 2025, management slashed full-year outlook dramatically from "high single-digit" operating profit growth to "flat to positive." This shows they have poor visibility into the business amid tariff chaos, private label pressure, and FX volatility. Trust in guidance is low - could cut again in 2026.

-

🌍 Currency Translation Headwind: 100 basis points expected negative impact on 2025 net sales from FX translation. Q1 saw 2.4% negative impact. Exposure to hyperinflationary markets (Argentina, Turkey) adds volatility. With Kenvue adding more international exposure, currency becomes an even bigger risk.

-

⚠️ Tylenol Litigation Overhang: Kenvue carries potential Tylenol-related litigation risks. Market is pricing in this uncertainty as one reason for KMB's 14% drop on deal announcement. If major litigation emerges post-acquisition, KMB inherits a massive liability.

-

🏦 P&G Competitive Dominance: Procter & Gamble maintains 42% global baby care share with Pampers vs Huggies' 27-37%. P&G has deeper pockets, stronger R&D, and better marketing. KMB is the perennial #2 player fighting an uphill battle. In adult incontinence, KMB dominates (55% share vs P&G's 12%), but baby care is the bigger market.

-

📉 Technical Breakdown Risk: Stock down 19% YTD from $150 peak to current $107. No clear signs of bottoming - could easily test $100 psychological support or $95 if negative catalyst emerges. The gamma support at $105 provides some floor, but break below that could trigger cascade to $100.

-

🎢 Event Risk Around Earnings: Q4 earnings on January 27-28 could move the stock 5-10% in either direction. With March options expiring 50 days later, there's significant event risk. Even if you're directionally right longer-term, a bad earnings print could cause near-term pain.

🎯 The Bottom Line

Real talk: Someone just spent $822,000 closing out short 115C 03/20 calls on Kimberly-Clark three months before expiration. This isn't a major institutional signal (Z-score 0.3 = typical activity) - it's routine risk management by a trader who likely sold these calls when KMB was trading $115-125 earlier in 2025 and is now taking profits with the stock at $107.

What this trade tells us:

- 🎯 The trader doesn't believe KMB reaches $115 by March 20, 2026 (108 days away)

- 💰 They're locking in profits from KMB's 19% YTD decline rather than waiting for full expiration

- ⚖️ The $115 strike sits at a MASSIVE 14.7B gamma resistance level - the second-strongest barrier on the entire chain

- 📊 With Q4 earnings in 56 days, Kenvue deal uncertainty, and tariff headwinds, the risk/reward of staying short calls didn't make sense

- 🛡️ This is de-risking, not a bearish bet - just taking chips off the table

This is NOT a "avoid KMB" signal - it's a "stock is range-bound, manage your risk" signal.

If you own KMB:

- ✅ Your 4.6% dividend is safe (Dividend King status, strong FCF despite recent compression)

- 📊 Hold through Q4 earnings (Jan 27-28) for clarity on tariff mitigation, margin trends, and Kenvue deal progress

- 🎯 Consider selling covered calls at $110-115 resistance to generate income while waiting for merger

- 🛡️ Set mental stop at $100 (major gamma support floor) if fundamentals deteriorate

- ⏰ Be patient - transformation takes 12-24 months, but if successful, creates $32B consumer health powerhouse

If you're watching from sidelines:

- ⏰ January 27-28 Q4 earnings is the key near-term catalyst - wait for this clarity

- 🎯 Best entry likely at $100-105 if market overreacts to earnings or merger news

- 📈 Looking for: Strong earnings beat, tariff mitigation progress, positive Kenvue FTC commentary

- 🚀 Long-term (18-24 months), if both deals close successfully, $1.9B synergies + margin expansion from Suzano JV could drive stock to $130-140

- ⚠️ Current price $107 offers 4.6% yield + 20% upside IF execution delivers, but risks are real

If you're bearish:

- 🎯 Watch for $105 support break - that triggers cascade to $100, potentially $95

- 📊 Regulatory snag on Kenvue deal would be the catalyst for major selloff

- ⚠️ Bull put spreads at $105-100 support offer defined-risk way to fade downside fears

- 📉 Tariff situation worsening or private label surging above 30% share would pressure margins further

- 💰 At current valuation (18.5x P/E, 4.6% yield), there's support from income investors even if growth stalls

Mark your calendar - Key dates:

- 📅 January 5, 2026 - Quarterly dividend payment ($1.26/share)

- 📅 January 27-28, 2026 - Q4 FY2025 earnings report (56 DAYS!)

- 📅 March 20, 2026 - Expiration of the $115 calls that just got closed (108 days)

- 📅 Mid-2026 - Expected close of Suzano international tissue JV ($1.73B cash to KMB)

- 📅 H2 2026 - Expected close of $48.7B Kenvue acquisition (subject to regulatory approval)

Final verdict: KMB is a classic "show me" story. The company has laid out an AMBITIOUS transformation - acquire Kenvue for $48.7B, divest international tissue for $3.4B, deliver $1.9B in synergies, mitigate $300M in tariffs, fight off private label, and grow margins from 15% to 40% gross/18-20% operating. That's a LOT of execution required.

The $822K call closing trade reflects this reality: In a range-bound, show-me environment, don't fight gamma resistance at $115. Take profits. Wait for proof. The 4.6% dividend and $105 gamma support provide a decent floor, but the upside is capped until Q4 earnings or Kenvue deal clarity emerges.

For most investors: Wait for earnings clarity in late January. The transformation story is compelling, but the risk/reward at $107 isn't compelling enough to rush in. Let the company prove it can execute. The dividend will still be there in 2 months, and you might get a better entry at $100-105 if the market gets nervous.

This is a marathon, not a sprint. Protect your capital. Let the story develop. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 0.3 (typical activity) means this closing trade does not indicate unusual institutional positioning - it's routine risk management. The Kenvue mega-merger faces significant regulatory, integration, and execution risks. Tariff costs of $300M and private label pressure of 27.8% share create ongoing margin headwinds. Always do your own research and consider consulting a licensed financial advisor before trading.

About Kimberly-Clark Corporation: Kimberly-Clark is a leading global manufacturer of hygiene and personal care products with iconic brands including Huggies, Kleenex, Kotex, and Depend. The company has a market cap of $36.02 billion in the Converted Paper & Paperboard Products industry and is currently executing a transformational strategy to acquire Kenvue and divest its international tissue business.