KWEB $1M Bullish Bet - Smart Money Loading Up on China Internet Rally!

January 7, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $1 MILLION on KWEB calls betting China's internet giants rally 15% by September! This isn't your average retail trade - 4,250 contracts bought at the mid with volume crushing open interest 390x (only 11 OI). With Goldman Sachs forecasting 20% upside for Chinese equities in 2026, this trader is positioning for the AI-driven turnaround in Tencent, Alibaba, and the rest of China's tech titans.

Company Overview

KraneShares CSI China Internet ETF (KWEB) provides exposure to China's largest internet companies trading on Hong Kong and US exchanges:

- AUM: $8.99 billion

- Expense Ratio: 0.70%

- Holdings: 33 Chinese internet stocks

- Top Holdings: Tencent (10.3%), Alibaba (8.8%), PDD (7.6%), Meituan (7.2%), NetEase (6.1%)

- 52-Week Range: $27.27 - $43.37

- YTD Return (2025): 32.94%

- Dividend Yield: 2.74%

- P/E Ratio: 17.86 (vs 30x for S&P 500 Tech)

The Option Flow Breakdown

What Just Happened

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:02:36 | KWEB | MID | BUY | CALL $41 | 2026-09-18 | $1M | $41 | 4.3K | 11 | 4,250 | $35.57 | $2.41 |

What This Actually Means

This is an aggressive bullish bet on China's internet sector revival! Here's the breakdown:

- Massive conviction: $1M premium for a 15.3% out-of-the-money call

- Volume vs OI: 4,300 volume vs just 11 open interest - this is NEW positioning, not closing

- Strike selection: $41 strike requires 15.3% rally from $35.57 current price

- Time horizon: September 18, 2026 Triple Witch expiration gives 254 days for thesis to play out

- Breakeven: Needs KWEB at $43.41 (+22% from current) by expiration to profit

- Position value: 4,250 contracts = 425,000 shares worth ~$15.1M notional exposure

What's really happening here: This trader is making a leveraged bet that China's internet stocks are about to EXPLODE higher. At $2.41 per contract, they're paying just 6.8% of the strike price for the right to buy KWEB at $41. If Goldman Sachs' 20% upside forecast materializes and KWEB hits $45 by September, these calls would be worth ~$4 each - a 66% gain. If KWEB rallies 40% to $50 (analyst high target is $54.53 per TipRanks), the calls are worth $9 each - a 273% return on the $1M bet!

Why September Triple Witch expiration?

- Captures Q4 2025 earnings (Jan-Feb)

- Captures "Two Sessions" policy meeting (March 2026)

- Captures Q1 2026 earnings (April-May)

- Captures H1 2026 AI infrastructure deployment milestones

- Captures potential trade agreement developments (expires Nov 2026)

Unusual Activity Alert: Volume/OI ratio of 390x is EXTREMELY unusual. When someone opens 4,250 new contracts at once, paying full mid-price, it signals strong conviction and urgency to get positioned.

Technical Setup / Chart Check-Up

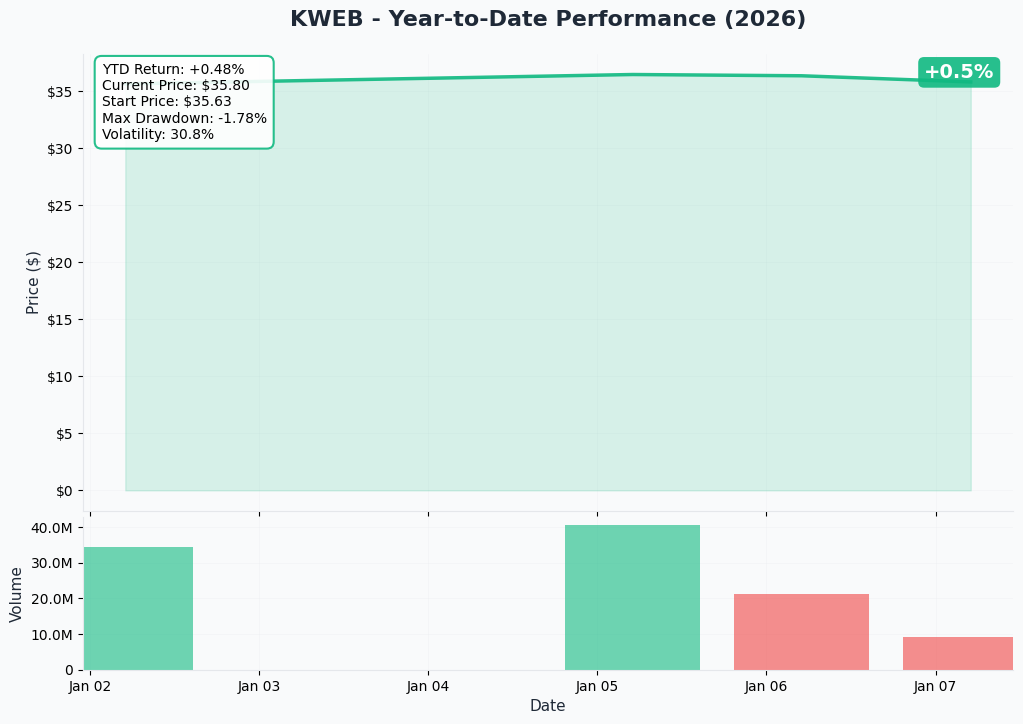

YTD Chart

KWEB has been on a roller coaster - up 32.94% in 2025 after a brutal 2021-2022 regulatory crackdown that saw the ETF plunge from $100+ to under $20. The current price of $35.57 sits roughly in the middle of the 52-week range ($27.27 - $43.37), suggesting room to run in either direction.

Key observations:

- Current price 18% below 52-week high of $43.37

- Trading at massive discount to 2021 peak ($104)

- P/E of 17.86x represents significant value vs US tech (30x+)

- Recent unusual call volume (224,049 contracts on Jan 3) shows institutional interest heating up

- Soros Fund increased stake 30.2% in recent quarters

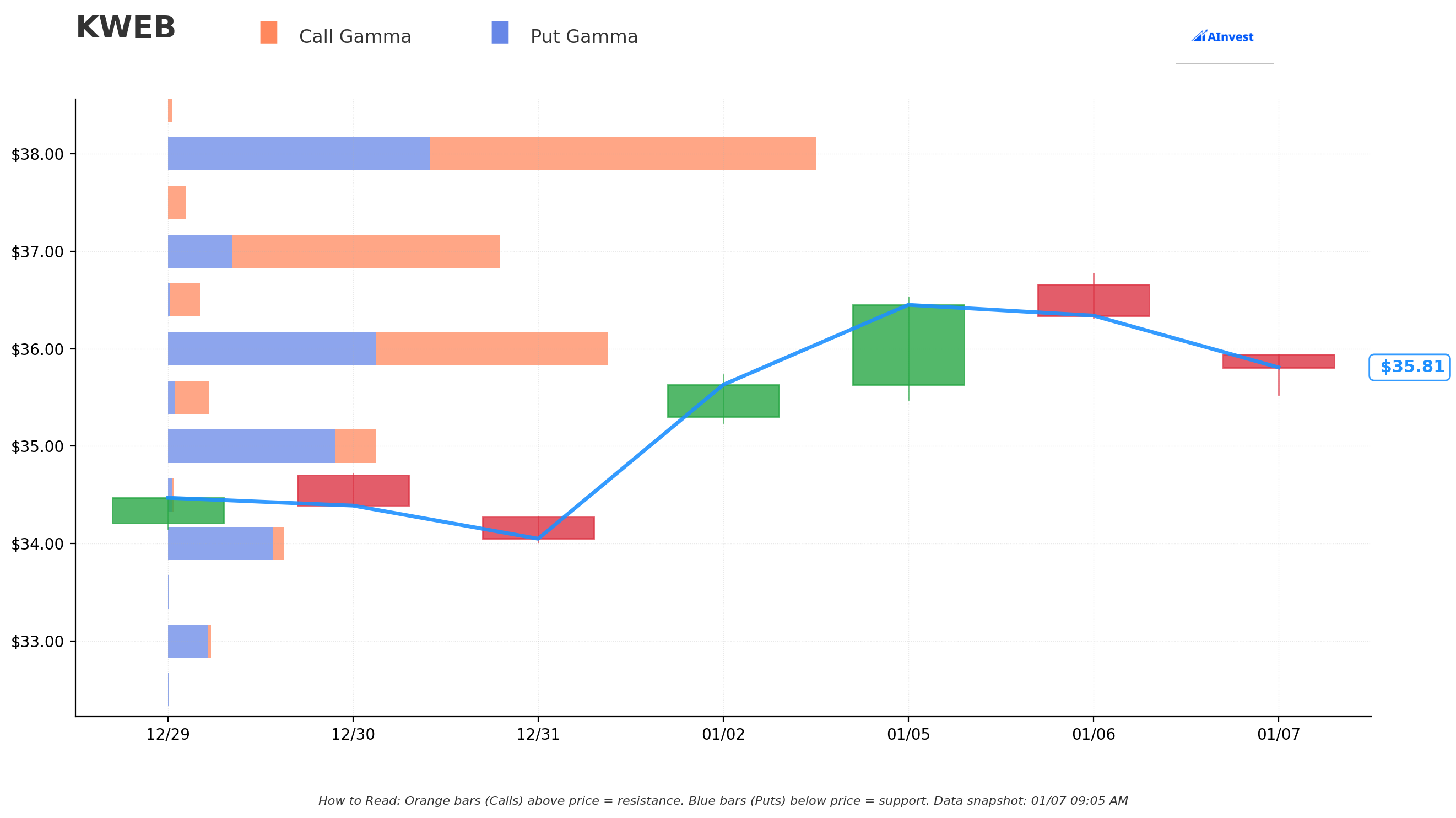

Gamma-Based Support & Resistance Analysis

Current Price: $35.57

The gamma exposure map reveals critical price magnets based on high open interest strikes:

Support Levels (Put Gamma Below Price):

- $35 - Immediate support with significant put positioning

- $34 - Secondary floor with hedging activity

- $33 - Deep support level where buyers step in

Resistance Levels (Call Gamma Above Price):

- $36 - Immediate ceiling, first hurdle to clear

- $37 - Secondary resistance with call concentration

- $38 - Major overhead resistance zone

What this means for traders: KWEB is currently trading just above the $35 support level, with a tight range to $36 resistance overhead. For this $41 strike call to pay off, KWEB needs to smash through $36, $37, and $38 resistance levels first. The bullish trader is betting these levels break as positive catalysts materialize throughout 2026.

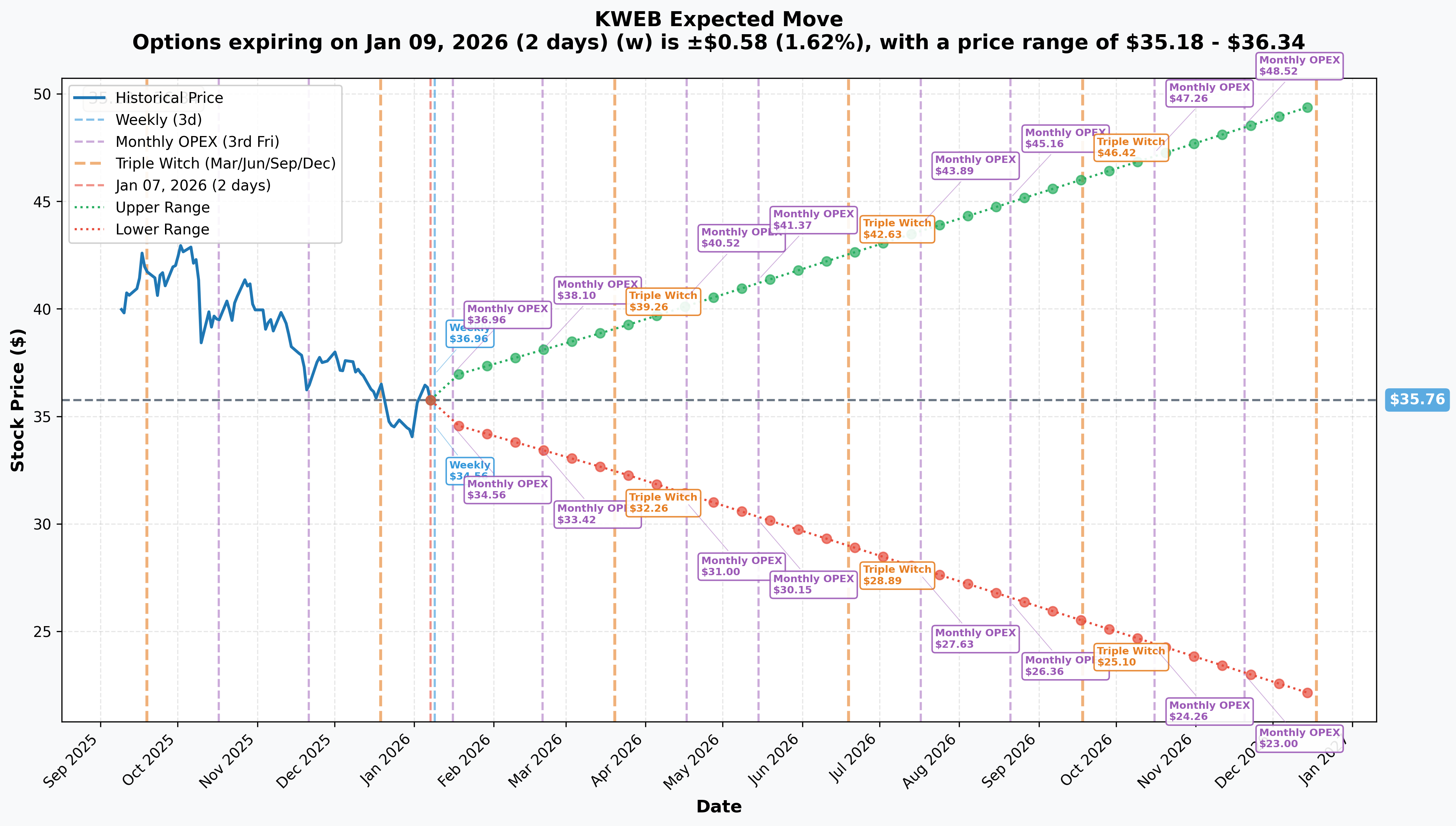

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 9 - 2 days): +/-1.62% ($0.58) - Range: $35.18 - $36.34

- Monthly OPEX (Jan 16 - 9 days): +/-3.17% ($1.13) - Range: $34.63 - $36.89

- Quarterly Triple Witch (Mar 20 - 72 days): +/-9.27% ($3.31) - Range: $32.45 - $39.07

- September Triple Witch (Sep 18 - THIS TRADE!): Upper range: $46.42, Lower range: $25.10

Translation for regular folks: The options market is pricing a wide range for September 2026 - anywhere from $25.10 on the downside to $46.42 on the upside. The $41 strike sits within the upper implied move range, meaning the market DOES think this level is achievable, but it's not a slam dunk. The trader needs the bullish scenario to play out.

Key insight: The September implied move upper bound of $46.42 exceeds the $41 strike, suggesting the market sees this as within the realm of possibility. The analyst average price target of $46.62 aligns almost perfectly with this level.

Catalysts

Upcoming Catalysts (Next 8 Months)

Q4 2025 Earnings Season (January-March 2026)

The big guns report soon - these results will set the tone for the year:

-

Alibaba FY Q3 (December quarter): Expected late January/early February 2026

- Consensus revenue ~$42B, key metrics: AI Cloud growth trajectory (up 34% last quarter)

- $52 billion AI/cloud infrastructure commitment - China's largest private computing project

-

Tencent Q4 2025: Expected March 2026

- Key metrics: Gaming revenue (43% international growth last quarter), WeChat monetization, AI integration

- Bernstein ranks Tencent as top pick for 2026

-

JD.com Q4 2025: Expected March 2026

- Total revenue up 14.9% YoY last quarter, watching margin expansion

-

PDD Holdings Q4 2025: Expected March 2026

- Revenue RMB 108.27B ($15.21B) last quarter, watching Temu profitability

China's "Two Sessions" (March 2026)

Annual legislative meetings - historically significant for Chinese equities:

- 2026 GDP growth target announcement (likely 4.5-5%)

- Fiscal stimulus details

- Technology self-sufficiency initiatives

- Consumer spending support measures

AI IPO Activity (H1 2026)

- MiniMax & Zhipu AI: Hong Kong IPOs targeted for January 2026

- Both backed by Alibaba and Tencent, could boost AI sector sentiment

- DeepSeek's breakthrough already prompting re-rating of Chinese tech stocks

Policy Support Catalysts

- China shifted to "moderately loose" monetary policy - first time since 2010

- $51 billion consumer stimulus announced for 2026

- Goldman Sachs raised 2026 GDP forecast to 4.8%

- Tariff rate reduced from 41% to 31% with 178 exclusions extended

Trade Agreement Extension (November 2026)

- Current tariff exclusions expire November 10, 2026

- Semiconductor tariffs delayed until June 2027

- Positive developments could boost sentiment into September expiration

Recent Catalysts (Already Happened)

Strong Q3 2025 Earnings (November 2025)

- Tencent: Revenue RMB 192.9B (+15% YoY), international gaming +43%, 32% dividend increase

- Alibaba: $38.38B revenue (+8% YoY), cloud +34%, EPS beat by $0.067

- JD.com: Total revenue +14.9% YoY, margin expansion continuing

- PDD: RMB 108.27B revenue (+9% YoY), Non-GAAP EPS beat by 34%

- Baidu: AI Cloud up 33% YoY, Apollo Go 3.1M driverless rides (+212%)

Institutional Accumulation (Q2-Q3 2025)

- Soros Fund increased KWEB stake 30.2% - now 293,404 shares ($10.07M)

- Mirae Asset grew position 83.1%

- Smart money positioning for 2026 rally

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through September 18, 2026 expiration:

Bull Case (35% probability)

Target: $45-$50+

How we get there:

- Q4 earnings show continued acceleration in AI revenue across Alibaba and Tencent

- Goldman's 20% upside forecast materializes as corporate profits grow 14%

- "Two Sessions" announces aggressive stimulus exceeding market expectations

- Trade tensions ease further with tariff exclusions expanded

- AI IPOs (MiniMax, Zhipu) drive sector re-rating

- Alibaba's $52B AI infrastructure deployment shows early results

- Property sector stabilizes, consumer confidence rebounds

- KWEB breaks above $38 resistance and momentum accelerates toward $46.62 analyst target

Call P&L in Bull Case:

- KWEB at $45: Calls worth $4.00, gain = $1.59/share x 4,250 = $675K (67% ROI)

- KWEB at $50: Calls worth $9.00, gain = $6.59/share x 4,250 = $2.8M (280% ROI!)

- KWEB at $55 (analyst high): Calls worth $14.00, gain = $11.59/share x 4,250 = $4.9M (490% ROI!)

Base Case (40% probability)

Target: $38-$44 range (MODEST RALLY)

Most likely scenario:

- Earnings meet expectations but don't dramatically exceed

- Policy support is incremental rather than transformative

- AI investments continue but monetization timeline remains long (3+ years to profitability per Bloomberg)

- Trade agreement renewed without major changes

- E-commerce price wars moderate but don't fully end

- KWEB rallies into $38-$44 range, approaching but not exceeding $41 strike

- Implied volatility compresses as macro uncertainty resolves

Call P&L in Base Case:

- KWEB at $38: Calls worth ~$0.50, loss = -$1.91/share x 4,250 = -$812K (81% loss)

- KWEB at $41: Calls worth ~$1.50, loss = -$0.91/share x 4,250 = -$387K (39% loss)

- KWEB at $44: Calls worth $3.00, gain = $0.59/share x 4,250 = $251K (25% ROI)

Bear Case (25% probability)

Target: $28-$34 (TEST LOWS)

What could go wrong:

- China's deflationary spiral deepens as Eurasia Group warns

- Property crisis enters fifth year, more developers default

- Trade tensions escalate after November 2026 expiration deadline

- ADR delisting risk materializes - SEC accelerates timeline

- E-commerce price wars (Meituan posted first loss since 2022) intensify further

- Consumer weakness persists despite stimulus

- Global risk-off drives capital out of emerging markets

- Break below $35, then $34, then $33 gamma support triggers cascade

Call P&L in Bear Case:

- KWEB at $32: Calls worth $0, loss = -$2.41/share x 4,250 = -$1M (100% loss)

- KWEB at $28: Calls worth $0, loss = -$2.41/share x 4,250 = -$1M (100% loss)

Why only 25% bear probability: Despite real risks, multiple tailwinds are aligning - monetary policy easing, fiscal stimulus, improving earnings, AI investment cycle, and reasonable valuations (17.86x P/E). The market has already priced in significant pessimism at current levels.

Trading Ideas

Conservative: Wait for Dip to Add Long Exposure

Play: Buy KWEB shares on pullback to $34-35 support zone

Why this works:

- Gamma support at $34-35 provides natural floor

- P/E of 17.86x offers value vs US tech (30x+)

- Dividend yield of 2.74% pays you to wait

- Multiple earnings catalysts coming (Q4 results Jan-Mar)

- Goldman's 20% upside forecast provides institutional backing

- Analyst target of $46.62 implies 31% upside from $35.57

Entry plan:

- Scale in: 1/3 at $35, 1/3 at $34, 1/3 at $33

- Stop loss: Below $32 (10% risk)

- Target: $42-45 (18-26% upside)

- Time horizon: 6-12 months

Risk level: Moderate (long ETF, diversified exposure) | Skill level: Beginner-friendly

Balanced: Follow the Smart Money - Sell Put Spread

Play: Sell bull put spread below current price to collect premium

Structure: Sell $34 puts / Buy $32 puts (March 2026 expiration)

Why this works:

- Collects premium while betting KWEB stays above $34 support

- Gamma support at $33-35 provides backstop

- Q4 earnings catalysts should support prices

- Defined risk ($200 max loss per spread)

- Takes advantage of elevated implied volatility

Estimated P&L:

- Collect: ~$0.60-0.80 net credit per spread ($60-80)

- Max profit: $60-80 if KWEB above $34 at March expiration

- Max loss: $140-120 if KWEB below $32

- Breakeven: ~$33.20-33.40

Position sizing: 5-10 spreads = $600-800 premium collected, $1,200-1,400 max risk

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Replicate the Whale Trade (Smaller Size)

Play: Buy September 2026 $41 calls - same trade as the $1M buyer!

Structure: Buy KWEB Sep 18 2026 $41 Calls

Why this could work:

- Aligns with Goldman's 20% upside forecast

- Analyst target of $46.62 well above $41 strike

- Multiple catalysts through September (earnings, Two Sessions, AI IPOs)

- 8+ months gives time for thesis to play out

- Institutional buyer clearly sees value at this level

Why this could blow up (SERIOUS RISKS):

- 15.3% out-of-the-money requires significant rally to profit

- Breakeven at $43.41 (22% above current) is aggressive

- China deflation and property risks remain elevated

- ADR delisting could accelerate unexpectedly

- Time decay burns premium over 8 months

- Can lose 100% of premium if KWEB below $41 at expiration

Estimated P&L:

- Cost: ~$2.41 per contract ($241 per contract, $2,410 for 10 contracts)

- KWEB at $45: Worth $4.00, gain = 66% ROI

- KWEB at $50: Worth $9.00, gain = 273% ROI

- KWEB at $38: Worth $0, loss = 100%

Position sizing: Risk only 2-5% of portfolio. If you have $50K portfolio, risk $1,000-2,500 max = 4-10 contracts.

Risk level: HIGH (can lose entire premium) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

China's deflationary spiral is a top 2026 risk: Eurasia Group ranks China's deflation trap as #7 global risk. Xi Jinping prioritizing political control over consumption stimulus ahead of 2027 Party Congress. State-driven investment creating overcapacity. "Involution" dynamic compressing margins across e-commerce and food delivery.

-

Property crisis in fourth year with no end in sight: Evergrande delisted with $300B+ debt. Country Garden ($205B debt) undergoing liquidation analysis. Vanke ($50B liabilities) narrowly avoided default with deadline extended to January 28, 2026. $130B in developer defaults already. Property weakness crushes consumer confidence.

-

ADR delisting risk remains real: SEC Chairman indicated continued scrutiny. "Delisting could come faster than you think." Goldman Sachs estimates $800B at risk in extreme scenario. Mitigation: 69% of KWEB in Hong Kong listings, but PDD and others not dual-listed.

-

Trade agreement is a tactical truce, not strategic shift: Tariff exclusions expire November 10, 2026. Semiconductor and rare earth disputes unresolved. Any escalation could hammer Chinese internet stocks.

-

E-commerce price wars compressing margins: Meituan posted first loss since 2022 from competition with Alibaba and JD.com. PDD/Temu facing tariff headwinds. "Anti-involution" policy not expected to reduce competition until Q3 2026.

-

AI investments won't be profitable for 3+ years: Tencent and Alibaba AI ventures expected to remain unprofitable through 2028. Massive capex with uncertain returns. DeepSeek disruption could commoditize AI infrastructure.

-

Long-dated calls face significant time decay: 8 months of theta burn. Even if thesis is correct, early timing could result in losses. Need patience and strong conviction to hold through volatility.

-

Regulatory surprises always possible: New Cybersecurity Law amendments effective January 2026 increase compliance burden. Human-like AI regulation draft could create uncertainty. Antitrust cases ongoing at Supreme People's Court.

The Bottom Line

Here's the deal: A sophisticated trader just bet $1 MILLION that China's internet sector rallies 15%+ by September 2026. This isn't blind optimism - it's a calculated bet backed by multiple converging catalysts:

Why the bull case is compelling:

- Goldman Sachs forecasts 20% upside for Chinese equities in 2026, driven by 14% corporate profit growth

- Top holdings showing strong momentum: Tencent +43% international gaming, Alibaba +34% cloud

- Valuation at 17.86x P/E is CHEAP vs US tech (30x+)

- Analyst target of $46.62 implies 31% upside

- Smart money (Soros) increasing positions

- Policy support shifting to "moderately loose" - first time since 2010

- $51B consumer stimulus and tariff reductions providing tailwinds

Why you should be cautious:

- China deflation and property crisis are real structural headwinds

- ADR delisting risk could accelerate

- E-commerce price wars crushing margins

- This is a leveraged bet that can lose 100%

If you're bullish on China:

- Consider smaller position in the same $41 September calls (2-5% of portfolio max)

- Or buy KWEB shares on dips to $34-35 support for lower-risk exposure

- Set mental stop if thesis invalidated (break below $32)

If you're on the sidelines:

- Watch Q4 earnings (Jan-Mar) for evidence of continued momentum

- "Two Sessions" (March 2026) could be major catalyst

- Better entry may come on pullback to $33-34 support

If you're bearish:

- Respect that smart money is positioned bullish

- Deflationary/property risks are legitimate concerns

- Consider defined-risk bear spreads rather than outright short

Mark your calendar - Key dates:

- January 28, 2026: China Vanke bond deadline - property sector indicator

- Late January/Early February 2026: Alibaba Q4 FY earnings

- March 2026: China "Two Sessions," Tencent Q4 earnings

- September 18, 2026: This call option expiration (Triple Witch)

- November 10, 2026: Tariff exclusions expire

Final verdict: This $1M call buy signals institutional conviction in China's internet sector turnaround. The thesis is supported by Goldman's 20% upside forecast, improving fundamentals at Tencent and Alibaba, and attractive valuations. However, real risks remain from deflation, property crisis, and geopolitics. This is a high-conviction, high-risk trade that requires patience and strong stomach for volatility.

The smart money has spoken. Now it's your turn to decide.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual activity highlighted reflects this specific trade's characteristics - it does not imply the trade will be profitable or that you should follow it. Chinese equities carry unique risks including regulatory, geopolitical, and currency exposure. Always do your own research and consider consulting a licensed financial advisor before trading. You can lose 100% of premium paid for options.

About KraneShares CSI China Internet ETF: KWEB tracks China's largest internet companies including Tencent, Alibaba, PDD, Meituan, and JD.com, providing diversified exposure to the China internet sector with $8.99 billion in assets under management.