🔧 LRCX $3.6M Put Buyback - Smart Money Closes Defensive Position! 🛡️

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just bought back $3.6 MILLION worth of LRCX puts this morning at 10:01:35! This massive 5,000 contract buyback of $150 strike puts expiring February 20th signals smart money CLOSING OUT protective positions after the stock bounced from recent lows. With LRCX trading at $166.03 and holding above critical $162.50 gamma support, institutions are taking chips off the table on their downside hedges. Translation: The defensive trade worked - time to lock in gains or cut losses on protection that's no longer needed!

📊 Company Overview

Lam Research Corporation (LRCX) stands as one of the world's largest semiconductor wafer fabrication equipment manufacturers:

- Market Cap: $211.9 Billion (3rd largest in WFE industry)

- Industry: Special Industry Machinery - Semiconductor Equipment

- Current Price: $166.03 (bouncing off recent support)

- Primary Business: Deposition and etch technologies for semiconductor manufacturing - essential equipment for building and patterning chips

- Key Customers: TSMC, Samsung, SK Hynix, Micron (the who's who of global chipmaking)

- Market Position: #1 in etch equipment (largest WFE segment), #2 in deposition technology

Why this matters: Lam Research is THE picks-and-shovels play for the semiconductor boom - when chipmakers build factories, they buy Lam's equipment. The company is particularly exposed to memory chip production (DRAM/NAND) which creates cyclical volatility but massive upside during recovery phases. With AI driving unprecedented demand for High-Bandwidth Memory (HBM), LRCX sits at the center of a multi-year equipment spending cycle.

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 10:01:35):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:01:35 | LRCX | BID | BUY | PUT $150 | 2026-02-20 | $3.6M | $150 | 5,000 | 21,000 | 5,000 | $166.03 | $7.20 |

🤓 What This Actually Means

This is a defensive hedge being CLOSED OUT (Buy-to-Close = BTC)! Here's what went down:

- 💸 Massive buyback: $3.6M spent to buy back puts previously sold or hedged ($7.20 per contract × 5,000 contracts)

- 🛡️ Deep out-of-the-money: $150 strike is 9.7% below current price of $166.03 - protecting against disaster scenario

- ⏰ Extended protection: 70 days to expiration (Feb 20) captures Q3 FY2025 earnings (April 23), memory market updates, China export risks

- 📊 Significant size: 5,000 contracts represents 500,000 shares worth ~$83M

- 🏦 Sophisticated positioning: This trader is closing/adjusting a complex portfolio hedge rather than making a directional bet

- 📈 Order classification: Medium confidence "Close Short Put" - smart money taking off protection that worked

What's really happening here: This trader likely SOLD these $150 puts weeks/months ago when LRCX was lower (perhaps in the $155-160 range during recent weakness). Now with the stock at $166.03 and sitting on gamma support, they're buying back the short puts to:

- Lock in profits - if puts were sold at $10-12 and now worth $7.20, that's a nice gain

- Reduce exposure - close out short volatility risk ahead of earnings

- Free up capital - remove margin requirements tied to the short puts

Think of it like an insurance company buying back a policy they sold - they collected premium upfront, the claim period is running out without incident, so they're closing the book on this risk.

Unusual Score: 🔥 ABOVE AVERAGE (Z-score: 1.44) - This trade is notably larger than typical activity with volume exceeding recent patterns. While not extreme, 5,000 contracts in a single print represents 555x average LRCX option size. The moderate activity classification (Vol/OI ratio: 0.238) suggests this is part of strategic repositioning rather than panic covering.

📈 Technical Setup / Chart Check-Up

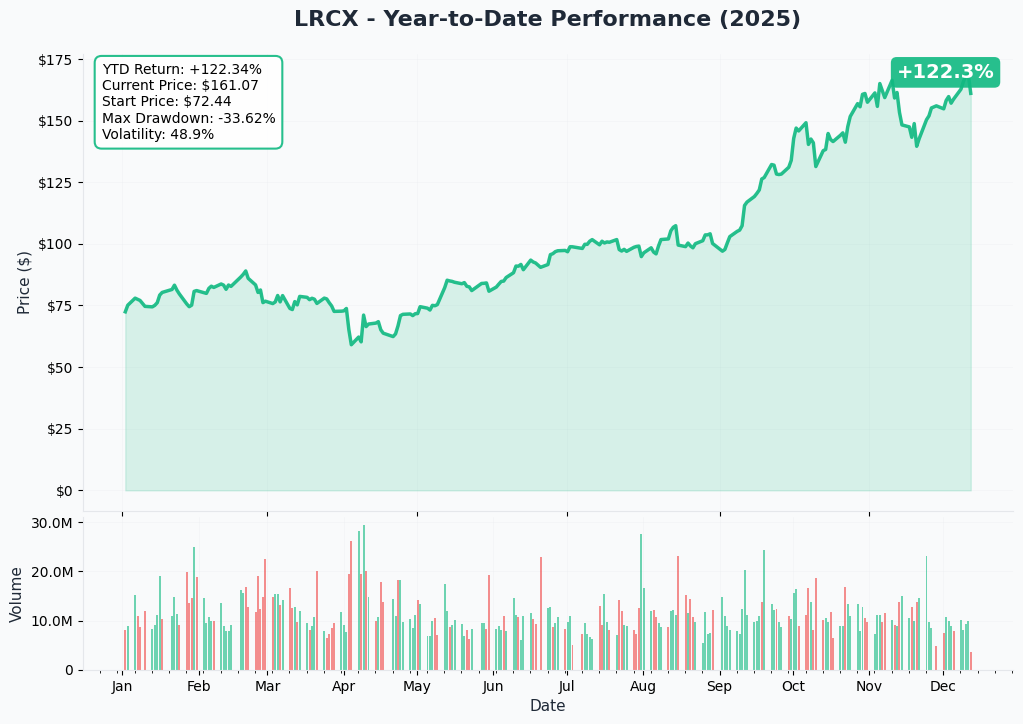

YTD Performance Chart

LRCX is delivering exceptional returns - up +108.96% YTD with current price near $165.54 (started 2024 at ~$70.57 in November 2024, hitting all-time high of $169.69 this year). The chart tells a powerful semiconductor equipment recovery story - after bottoming in late 2024 during the memory market downturn, LRCX has rocketed higher on AI-driven memory demand resurgence.

Key observations:

- 🚀 Relentless rally: Steady climb from $70 lows to near $170 highs throughout 2025

- 📈 All-time high territory: Recent peak of $169.69 represents new records for the stock

- 📊 Consolidation phase: Currently trading in $160-170 range after hitting highs

- 🎢 Moderate pullback: Recent dip from $169 to $160 tested support, now bouncing

- 💪 Strong institutional accumulation: Volume surges during breakouts above key resistance levels

The current price action shows LRCX consolidating gains near all-time highs - a healthy pattern after doubling in 12 months. The put buyback at $166 suggests smart money believes the $160-165 zone provided sufficient support to close downside protection.

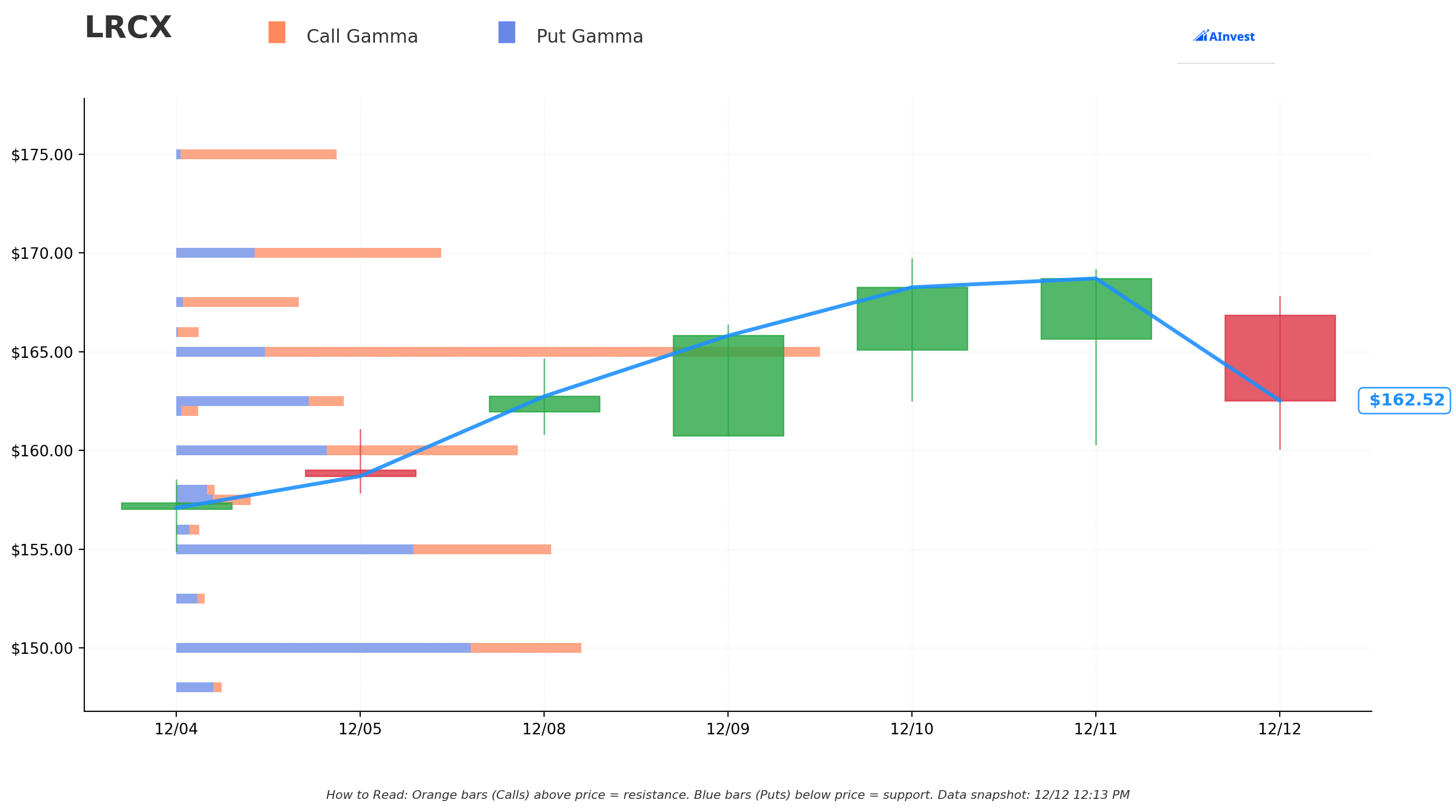

Gamma-Based Support & Resistance Analysis

Current Price: $162.55 (at time of gamma calculation)

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $162.50 - IMMEDIATE SUPPORT with 2.59B total gamma exposure (RIGHT AT CURRENT PRICE! Critical floor)

- $160 - Secondary support at 5.27B gamma (dealers will buy dips aggressively here - only 1.6% below)

- $155 - Major structural floor with 5.76B gamma (strongest nearby support zone)

- $150 - Deep support at 6.20B gamma (HIGHEST PUT GAMMA - exactly where this put trade is struck! THE LINE IN THE SAND)

- $145 - Extended support zone with 1.94B gamma

- $140 - Disaster floor at 2.20B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $165 - IMMEDIATE CEILING with 10.30B gamma (STRONGEST RESISTANCE - massive barrier just 1.5% overhead)

- $167.50 - Secondary resistance at 1.99B gamma (3% above current)

- $170 - Major ceiling zone with 4.19B gamma (recent high area, 4.6% rally required)

- $175 - Extended upside target at 2.53B gamma (7.7% rally needed)

What this means for traders: LRCX is trading RIGHT ON TOP of critical $162.50 support with massive $165 resistance overhead. The gamma data shows market makers holding enormous positions at $165 (10.30B - the single largest level) which creates natural selling pressure as price approaches. This setup screams "consolidation range" between $162-165 before the next big move.

Notice anything? The put buyer closed their position at exactly $150 where there's 6.20B gamma support - the highest put gamma concentration on the entire board! This is THE critical support level where maximum pain occurs for call holders. They're positioning suggested that if LRCX broke below $150, disaster was imminent. With the stock holding $162.50 support firmly, that $150 protection is no longer needed - time to take profits on the hedge.

The $160 level with 5.27B gamma represents a secondary fortress - break below that and momentum could accelerate toward $155, but holding above it keeps the bullish structure intact.

Net GEX Bias: Bullish (37.08B call gamma vs 28.05B put gamma) - Overall positioning remains constructive, with calls outnumbering puts. This suggests dealers will provide support on dips and resistance on rallies, creating range-bound behavior near current levels.

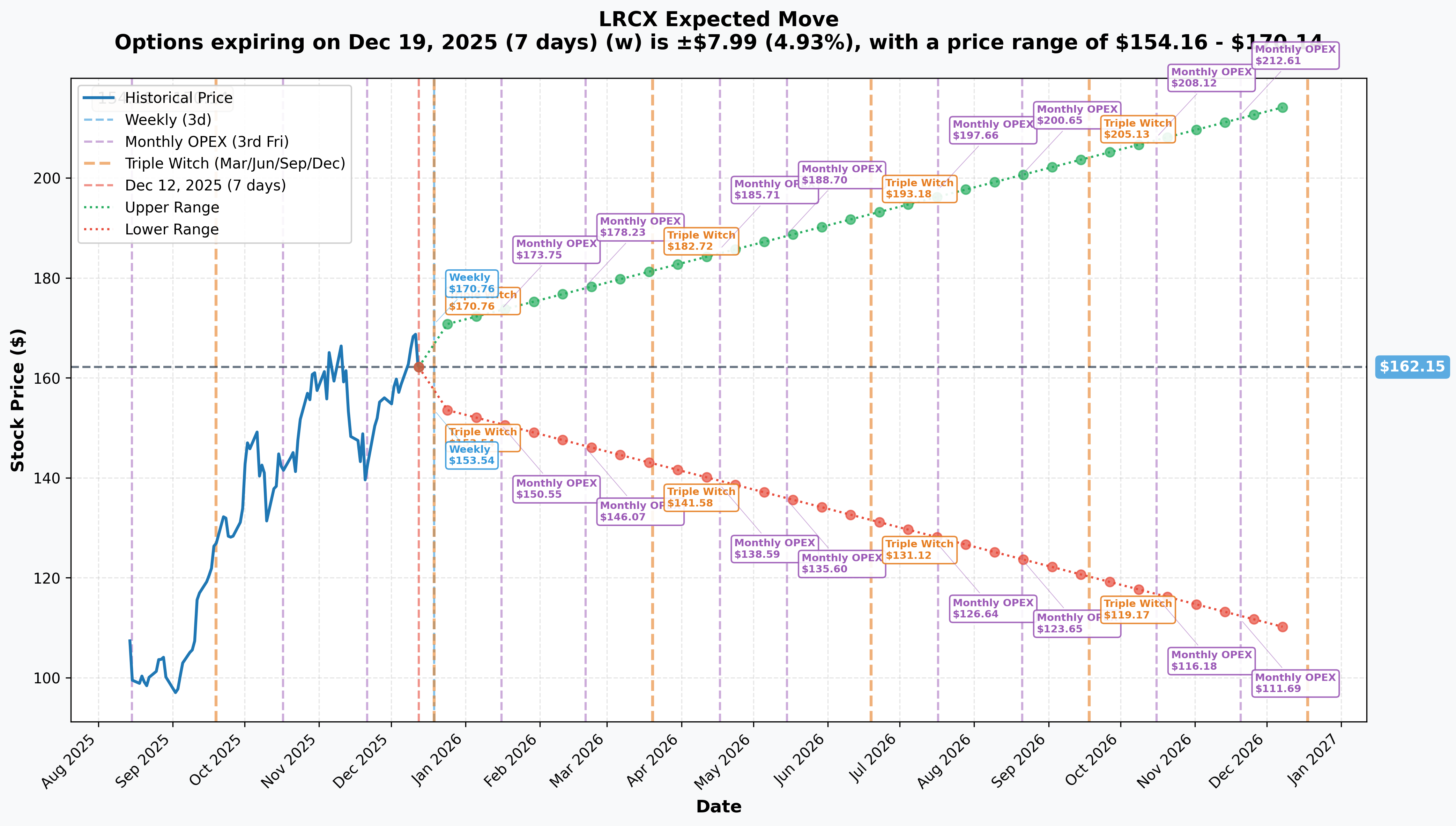

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 7 days): ±$7.99 (±4.93%) → Range: $154.16 - $170.14 (Triple Witch OPEX)

- 📅 Monthly OPEX (Jan 16 - 35 days): ±$11.60 (±7.16%) → Range: $150.55 - $173.75

- 📅 February OPEX (Feb 20 - 70 days - THIS TRADE EXPIRATION!): ±$16.08 (±9.92%) → Range: $146.07 - $178.23

- 📅 Quarterly Triple Witch (Mar 20 - 98 days): ±$20.57 (±12.69%) → Range: $141.58 - $182.72

Translation for regular folks: Options traders are pricing in a 4.9% move ($8) by next Friday for weekly expiration, expanding to a 9.9% move ($16) through February OPEX which includes Q3 earnings on April 23rd. The market expects MODERATE volatility for a $212B mega-cap equipment stock - but the February timeframe captures critical catalysts.

The February 20th expiration (when this $3.6M put trade expires) has a lower range of $146.07 - meaning the market thinks there's a reasonable possibility LRCX could trade as low as $146 over the next 70 days if negative catalysts materialize. This aligns with the put strike at $150 - protecting against that 10-12% downside scenario.

Key insight: The $150 strike sits RIGHT IN THE MIDDLE of the February implied move range ($146-178), suggesting the original put seller was targeting a high-probability strategy - selling protection at strikes they believed would stay out-of-the-money. Now with 70 days left and stock holding well above $150, those puts are decaying rapidly - making it attractive to buy them back and lock in profits.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened)

Q2 FY2025 Earnings Beat - January 29, 2025 ✅

Lam Research crushed expectations with its fourth consecutive quarterly beat, demonstrating operational excellence at a pivotal moment:

- 📊 Revenue: $4.38B (up 5% QoQ) vs guidance midpoint of $4.30B - beat expectations

- 💰 Non-GAAP EPS: $0.91 (up 6% QoQ), beating consensus of $0.87 by 4.6%

- 📈 Gross Margin: 47.5% (non-GAAP), exceeding guidance midpoint

- 🏭 Operating Margin: 30.7% (non-GAAP) - maintaining healthy profitability

- 🌍 Geographic Mix: China (31%), Korea (25%), Taiwan (17%), US (9%), Japan (8%), Southeast Asia (7%), Europe (3%)

Why this matters for the put trade: The strong Q2 beat validated that LRCX fundamentals remain rock-solid despite China headwinds and memory cyclicality. This likely gave the put seller confidence to close protection - if the business is executing well, why pay for downside insurance?

Technology Production Wins - Q4 2024 ✅

Lam secured critical production tool selections that validate its technology leadership:

- 🎯 Aether Dry Resist: Leading memory manufacturer selected Aether dry photoresist as production tool of record for most advanced DRAM processes, achieving 28nm pitch with best-in-class defectivity

- 🔧 Akara Platform: New conductor etch platform selected by leading device manufacturers as production tool of record for multiple advanced planar DRAM and foundry GAA applications

- 💪 GAA & Advanced Packaging: Combined shipments exceeded $3B projected for 2025 from $1B+ each in 2024

These design wins provide multi-year revenue visibility as customers ramp production on next-generation nodes.

Analyst Upgrades - Q4 2024/Q1 2025 ✅

Wall Street enthusiasm surged following strong execution:

- UBS: Raised price target to $175 from $165 (November 2025)

- Citi: Raised price target to $190 from $175

- JPMorgan: Raised price target to $165 from $113

- Current Consensus: Average price target $148.09 (range: $90-$200), 16 Strong Buy ratings, 5 Hold, 0 Sell

China Export Restrictions Absorbed - December 2, 2024 ✅

Lam issued statement on new U.S. semiconductor export controls, with management assessing: "Effect of announced measures on business will be broadly consistent with prior expectations. No plans to update financial guidance for December 2024 quarter."

The market-friendly response - maintaining guidance despite expanded restrictions to 140 companies including Chinese chip equipment makers - removed a major uncertainty overhang. This likely reduced the need for defensive hedging.

🚀 Upcoming Catalysts (Next 6 Months)

Q3 FY2025 Earnings - April 23, 2025 (131 DAYS AWAY!) 📊

This is THE major catalyst that could drive significant price action in either direction:

- 📊 Revenue Estimate: $5.2B ±$300M (guidance) - representing 19% YoY growth

- 💰 EPS Consensus: $1.00 (+28.21% YoY) from $0.78 last year

- 📈 Historical Beat Pattern: Q2 beat by 4.6%, establishing pattern of outperformance

Key metrics to watch:

- Memory vs. foundry/logic revenue mix (memory recovery pace)

- GAA node and advanced packaging shipment momentum (targeting >$3B combined in 2025)

- China revenue percentage given export restrictions (31% in Q2)

- Gross margin trajectory toward 50%+ (Q4 achieved 50.3% record)

- Installed base chamber count growth from 96,000

Why this matters: Earnings falls AFTER the February 20th put expiration, meaning the puts will decay significantly through January-February with no binary event risk. This makes closing the short puts attractive NOW rather than waiting closer to expiration.

Memory Market Recovery Acceleration (2025-2026) 🚀

The memory market resurgence is THE mega-catalyst driving equipment spending:

- 💾 HBM Explosion: High-Bandwidth Memory revenue expected to double from ~$17B in 2024 to ~$34B in 2025, with demand growing 200% in 2024 and forecasted +70% growth in 2025

- 📊 DRAM Market: Global memory revenue hit $170B in 2024 (+78% YoY), led by DRAM at ~$97B, with 2025 forecast exceeding $190B and DRAM reaching $129B

- 🔥 Supply Constraints: LPDDR5X memory lead times extended to 26-39 weeks, indicating tight supply through mid-2026

- 🌊 HBM Market Share: Projected to surge from 18% in 2024 to 50%+ by 2030 (33% CAGR)

This memory tsunami translates directly into equipment orders for Lam Research, particularly for advanced deposition and etch tools required for HBM stacking and DRAM scaling.

2nm Node Production Ramp (2025-2026) 🏭

TSMC, Samsung, and Intel are entering 2nm mass production with GAA transistors in 2025-2026, creating significant WFE demand:

- 🔬 Lam's Aether dry resist qualified for 28nm pitch BEOL logic at 2nm and below, enabling single-patterning cost reduction

- 📈 Leading-edge capacity for 5nm and below projected to grow 17% in 2025

- 💰 Samsung finalizing $44B Texas plant for 2nm output by 2026 with $6.6B CHIPS Act support

- 🎯 TSMC announced $28B investment in new advanced-node fabs across US (Arizona), Taiwan, and Japan

Backside Power Distribution Adoption 🔌

Top three foundries plan backside power delivery at 2nm node, reducing power losses by 30%:

- 🔧 Intel combining PowerVia with RibbonFET (GAA) at 20A node (2nm equivalent)

- ⚙️ Lam's molybdenum ALD deposition technology positioned as tungsten replacement for advanced nodes

Semiconductor Equipment Market Growth 📊

Global WFE sales forecast to reach record $125.5B in 2025 (+7.4% YoY), growing to $138.1B in 2026:

- 🌏 Asia-Pacific accounts for >70% of WFE demand

- 🇨🇳 China maintaining 14% capacity growth to 10.1M wpm in 2025 despite export restrictions

- 🏭 TSMC expanding CoWoS advanced packaging from 330,000 wafers in 2024 to 660,000 in 2025 (+100% YoY)

Management expects to outperform overall WFE market in 2026 according to recent commentary.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20th expiration:

📈 Bull Case (35% probability)

Target: $175-$190

How we get there:

- 💪 Memory market recovery accelerates beyond expectations with HBM revenue doubling to $34B and DRAM spending surge

- 🚀 Additional GAA/advanced packaging design wins announced, pushing 2025 shipments above $3B target

- 📊 Q3 earnings (April) beats with revenue toward $5.5B high-end and gross margins expanding above 50%

- 🇨🇳 China export situation stabilizes or improves - clarity removes uncertainty premium

- 🌐 WFE market tracking toward $125.5B for 2025 with LRCX gaining share

- 📈 Breakout above $170 gamma resistance triggers technical rally toward Citi's $190 price target

- 💰 Margin expansion story gaining traction with path to 50%+ gross margins sustained

Key metrics needed:

- Memory segment revenue growth >25% YoY

- Customer support revenue growing from $1.75B quarterly run rate

- Installed base expanding beyond 96,000 chambers

- Market share stabilizing/improving from recent 11% level

Probability assessment: 35% because fundamentals are exceptionally strong (4 consecutive beats, memory recovery, GAA/backside power tailwinds), but stock already up 109% YTD near all-time highs. Requires continued execution without stumbles. Gamma resistance at $165-170 creates technical hurdles.

🎯 Base Case (50% probability)

Target: $155-$175 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid but unspectacular progress through Q1 2026

- 📱 Memory recovery continues at steady pace, not explosive growth

- ⚖️ Q3 earnings meets/slightly beats consensus without major surprises

- 🤖 GAA and advanced packaging shipments tracking toward $3B+ target but not exceeding dramatically

- 🇨🇳 China remains 25-30% of revenue - neither major positive nor catastrophic negative

- 🔄 Trading within gamma support ($155-162) and resistance ($165-175) bands

- 📊 Market digests massive YTD gains, waits for Q4 earnings and FY2026 outlook

- 💤 Volatility moderates in $160-170 consolidation channel

This is the put buyer's win scenario: Stock holds well above $150, puts decay from $7.20 toward $3-4 by February expiration, position closed profitably. The put buyer collected premium selling these puts originally, now buying back at lower price locks in gains.

Why 50% probability: Stock at healthy consolidation phase after doubling. Fundamentals solid but valuation reasonable (34.4x forward P/E vs historical 25-35x). Most institutional players will hold and accumulate on dips. No major negative catalysts expected near-term.

📉 Bear Case (15% probability)

Target: $140-$155 (TEST SUPPORT ZONE)

What could go wrong:

- 😰 Memory recovery stalls or reverses - NAND remains weak, DRAM pricing softens

- 🚨 New China export restrictions more severe than expected, impacting revenue materially beyond management's "within expectations" guidance

- ⏰ Customer CapEx delays push equipment orders to later quarters

- 🇨🇳 Geopolitical tensions escalate, affecting Taiwan/Korea operations or supply chain

- 💸 Broader tech selloff drags semis lower on recession fears

- 📊 Competitive pressure from Applied Materials or Tokyo Electron

- 🤖 AI memory demand slowdown concerns emerge

- 💰 Margin compression from unfavorable geographic mix or pricing pressure

- 🔨 Break below $160 gamma support triggers cascade to $155, then $150

Critical support levels:

- 🛡️ $162.50: Immediate floor - MUST HOLD or momentum shifts negative

- 🛡️ $160: Secondary support (5.27B gamma) - key psychological level

- 🛡️ $155: Major floor (5.76B gamma) - likely strong buying emerges here

- 🛡️ $150: Deep support (6.20B gamma) + this put strike - disaster scenario

Probability assessment: Only 15% because fundamentals remain robust (4 consecutive beats, memory recovery, technology wins), management absorbed China restrictions without guidance cut, and valuation reasonable. Would require multiple negative catalysts to align. The put buyback itself signals smart money is NOT worried about downside - they're taking profits on protection.

Put value in Bear Case:

- Stock at $145 on Feb 20: Puts worth $5.00, net gain from buyback = -$2.20/share × 5,000 = -$1.1M additional loss

- Stock at $150 on Feb 20: Puts worth $0 (at-the-money), net = -$7.20/share × 5,000 = -$3.6M loss on buyback

- Stock at $155+ on Feb 20: Puts worth $0, original put sale profitable overall

💡 Trading Ideas

🛡️ Conservative: Hold and Monitor Support

Play: If you own LRCX stock, maintain position with tight stops

Why this works:

- ✅ Fundamentals exceptional - 4 consecutive earnings beats, memory recovery accelerating

- 📊 Stock holding critical $162.50 gamma support after recent consolidation

- 💰 Valuation reasonable at 34.4x forward P/E for 20%+ growth story

- 🎯 Multiple catalysts ahead - memory spending, 2nm ramps, Q3 earnings

- 🛡️ Institutional put buyback signals smart money reducing hedges = confidence

- 📈 Analyst consensus $148 average target with 16 Strong Buy ratings (bullish setup)

Action plan:

- 👀 Monitor $160 support level - hold above this keeps bullish structure

- 🎯 Set mental stop at $157-158 (below $155 gamma support = momentum shift)

- ✅ Add on pullbacks to $160-162 range (gamma support buying opportunity)

- 📊 Watch for breakout above $170 resistance for acceleration to $175-180

- ⏰ Hold through Q3 earnings (April 23) expecting continued beat pattern

Risk level: Low to Moderate (core holding) | Skill level: Beginner-friendly

Expected outcome: Stock consolidates $160-175 through Q1, breaks higher into earnings on continued memory strength. Minimal downside below $155 support.

⚖️ Balanced: Covered Call Strategy (Income Generation)

Play: Sell out-of-the-money covered calls against stock holdings

Structure: Sell $170 or $175 calls (February 20 or March 20 expiration)

Why this works:

- 📊 Stock in consolidation mode after big run-up, likely range-bound near-term

- 💰 Generate 2-4% income while waiting for next catalyst

- 🎯 $170-175 strikes above gamma resistance, low probability of assignment

- 🛡️ Reduces cost basis and provides downside cushion

- ⏰ 40-70 days to expiration captures time decay sweet spot

- 📈 If assigned at $170-175, you sell at great prices (10-12% above current)

Estimated P&L:

- 💰 Collect $3-5 premium per call (February $170 calls)

- 💰 Collect $5-7 premium per call (March $175 calls)

- 📊 Effective yield: 2-4% over 40-70 days (annualized 18-35%)

- 🎯 Max profit: Stock assigned at $170-175 + premium collected

- 📉 Downside protection: Premium collected reduces breakeven by $3-7

Entry strategy:

- ⏰ Sell calls on strength when stock approaches $167-169

- 🎯 Target strikes with <30% probability of assignment

- ✅ Roll up and out if stock breaks above strike before expiration

- ❌ Buy back calls and close if stock surges above $175 (preserve upside)

Position sizing: Sell calls against 25-50% of stock holdings (keep some unhedged for upside)

Risk level: Low (you own the stock) | Skill level: Intermediate

Expected outcome: Collect consistent premium income while stock consolidates. If assigned, you sell at attractive levels above current price.

🚀 Aggressive: Bull Put Spread (Copy The Trade)

Play: Sell bull put spread at similar strikes to the institutional position

Structure: Sell $155 puts, Buy $150 puts (February 20 expiration - SAME as the $3.6M trade)

Why this could work:

- 🤝 Essentially copying smart money's original positioning (they likely sold these puts, now closing profitably)

- 📊 Strikes align with major gamma support zones where dealers will defend

- 🎯 $155-150 spread captures 6-9% downside with defined risk

- 🛡️ Stock would need to drop significantly below current $166 level to threaten spread

- ⏰ 70 days to expiration provides time for any volatility to settle

- 💰 High probability of profit if stock stays above $155 (currently 7% margin)

- 📈 Implied volatility relatively low after recent stability

Estimated P&L:

- 💰 Collect $1.50-2.00 net credit per spread

- 📈 Max profit: $150-200 if LRCX stays above $155 at expiration (30-40% ROI)

- 📉 Max loss: $350-500 if LRCX falls below $150 (defined and limited)

- 🎯 Breakeven: ~$153-154 (8% below current price)

- 📊 Probability of profit: ~65-70% (stock needs to stay above $155)

Why this could blow up (SERIOUS RISKS):

- 😱 Memory market reversal: Sudden DRAM/NAND weakness could drop stock 15-20%

- 🇨🇳 China escalation: New export restrictions more severe than expected

- 📊 Broad market selloff: Tech correction drags semis lower regardless of fundamentals

- ⏰ Time risk: 70 days is long enough for multiple negative catalysts to emerge

- 💸 Margin requirement: Short puts require significant buying power/margin

Risk management:

- ✅ Size position at 2-5% of portfolio maximum (this is speculation, not core)

- 🛡️ Close spread if stock breaks below $160 (don't wait for disaster)

- ⏰ Consider closing at 50% profit rather than holding to expiration

- 📊 Monitor earnings date (April 23) falls after expiration - no binary event risk

CRITICAL WARNING:

- ⚠️ You're selling puts on margin - understand margin requirements

- ⚠️ Max loss ($350-500 per spread) is DEFINED but still significant

- ⚠️ Do NOT sell naked puts - always buy protection at lower strike

- ⚠️ Can lose significant capital if wrong on direction

Risk level: MODERATE TO HIGH (defined but substantial risk) | Skill level: Advanced only

Probability of profit: ~65-70% based on current support levels and implied volatility

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🇨🇳 China export restrictions wildcard: Despite management's reassuring comments that December 2024 restrictions are "within expectations", China represents 31% of revenue. Future escalations could materially impact guidance. The U.S. expanded restrictions to 140 companies including Chinese equipment makers, and political tensions remain elevated. Supply chain restructuring to remove Chinese components could pressure costs.

-

💰 Memory market cyclicality remains acute: While DRAM revenue projected to grow from $97B to $129B in 2025, the memory market is notoriously cyclical. NAND spending remained muted through 2024 despite DRAM strength. Customer inventory stocking behavior can reverse quickly as observed in China mid-2024. A sudden CapEx cut by top customers (TSMC, Samsung, SK Hynix, Micron) could crater equipment orders.

-

📊 Market share compression concerns: LRCX market share declined from 15% (2022) to 11% (2023), with etch/clean segment potentially sliding to 18% by Q2 2024 from 27% year earlier. Despite technology wins, competitive pressure from Applied Materials and Tokyo Electron remains intense. Any further share losses would pressure revenue growth assumptions.

-

🎢 2nm GAA and backside power execution risk: These technologies are unproven at high-volume manufacturing. Samsung's 3nm yield issues and Intel's delays highlight potential pitfalls. If TSMC, Samsung, or Intel face production problems at 2nm, equipment purchases could be deferred 6-12+ months. Lam's dry resist and new deposition technologies require successful HVM ramp.

-

💸 Valuation offers limited margin of error: At 34.4x forward P/E following 109% annual gain to near all-time highs, the stock prices in strong execution. Gross margin of 47.5% in Q2 trailing Q4's record 50.3% suggests potential mix/cost headwinds. Any earnings miss or guidance disappointment could trigger 15-20% correction despite solid fundamentals.

-

🏭 Customer concentration risk: Top 4 customers (TSMC, Samsung, SK Hynix, Micron) represent majority of revenue. Single customer CapEx cut materially impacts quarterly results. Loss of Intel from top customer list in FY2024 filing indicates revenue concentration risk is real.

-

📉 AI memory demand sustainability uncertain: The HBM revenue doubling thesis assumes sustained AI infrastructure buildout through 2025-2026. If hyperscaler spending moderates or AI chip demand disappoints, memory equipment orders could decline sharply. PC and smartphone end-markets remain weak, limiting mainstream memory growth.

-

🌐 Macro recession risk: At current valuation, LRCX has zero recession protection. Enterprise IT budgets and fab construction projects get cut first in downturns. If economy weakens in 2025-2026, even strong execution won't prevent 30-40% correction.

-

⚡ Gamma ceiling at $165 creates resistance: The massive 10.30B call gamma at $165 represents natural mechanical selling pressure as market makers hedge their exposure. Breakout above this level requires sustained buying - previous attempts have failed. Stock could remain range-bound $160-170 for extended period.

🎯 The Bottom Line

Real talk: A sophisticated trader just spent $3.6 MILLION buying back puts they likely sold weeks or months ago on LRCX. This isn't a bearish signal - it's smart money locking in profits on a successful hedge after the stock held support and fundamentals stayed strong.

What this trade tells us:

- 🎯 The original put sale (at higher prices) likely collected $10-12+ premium - buying back at $7.20 locks in $3-5/share profit

- 💰 With stock at $166 and puts struck at $150 (9.7% out-of-the-money), protection is no longer needed

- ⚖️ Smart money reducing hedges = confidence in current support levels

- 📊 They're taking risk OFF the table by closing shorts, not adding bearish exposure

- ⏰ With 70 days to expiration and no earnings before Feb 20, time decay favors closing now

This is a BULLISH signal - institutions are becoming LESS defensive, not more worried.

If you own LRCX:

- ✅ Hold your position - fundamentals remain exceptional with 4 consecutive beats and memory recovery accelerating

- 📊 Monitor $160 support - staying above this keeps bullish structure intact

- 🎯 Consider adding on dips to $160-162 where gamma support provides floor

- 💰 Sell covered calls at $170-175 to generate income during consolidation

- ⏰ Position for Q3 earnings (April 23) expecting continued beat-and-raise pattern

If you're watching from sidelines:

- 🎯 Current levels ($165-167) offer reasonable entry with 10-12% upside to $180+ over 6-12 months

- 📈 Wait for dip to $160-162 for better risk/reward if you want margin of safety

- ✅ Memory market recovery, 2nm ramps, and WFE market growth to $125.5B provide multi-year tailwinds

- 🚀 GAA and advanced packaging shipments targeting >$3B in 2025 (from $1B+ each in 2024) validate technology leadership

- ⚠️ Valuation reasonable at 34.4x forward P/E for 20%+ growth, but not cheap

If you're considering puts:

- ❌ Don't fight this tape - institutional money is CLOSING bearish hedges, not adding them

- 📊 Support structure remains intact with $162.50 holding, $160 and $155 below that

- ⏰ No major negative catalysts visible near-term (earnings not until April 23)

- 🛡️ Better to wait for breakdown below $160 before initiating bearish positions

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Weekly/Monthly/Quarterly Triple Witch OPEX (potential volatility)

- 📅 January 16, 2026 (Friday) - Monthly OPEX

- 📅 February 20, 2026 (Friday) - Monthly OPEX, expiration of this $3.6M put trade

- 📅 April 23, 2025 (Wednesday) - Q3 FY2025 earnings report

- 📅 Mid-2025 - Dry resist production expansion and Akara platform scaling

- 📅 2025-2026 - 2nm GAA transistor production ramps at TSMC, Samsung, Intel

Final verdict: LRCX's semiconductor equipment story remains INCREDIBLY compelling - memory market recovering to $190B+ in 2025, HBM revenue doubling, 2nm technology transitions, and WFE market growing to record $125.5B all support multi-year growth. The company's #1 position in etch and technology wins (Aether dry resist, Akara conductor etch) provide competitive moat.

The $3.6M put buyback is a CLEAR signal: smart money is taking OFF hedges as downside fears diminish.

Stay long, stay patient, add on dips. The semiconductor equipment super-cycle is just getting started. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual activity score reflects this specific trade's size relative to recent LRCX history - it does not imply the trade will be profitable or that you should follow it. The put buyer may have complex portfolio hedging needs not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading. Selling puts creates substantial risk including potential assignment and margin calls.

About Lam Research Corporation: Lam Research is one of the largest semiconductor wafer fabrication equipment manufacturers in the world, specializing in deposition and etch technologies. The company holds the #1 market position in etch equipment and #2 in deposition, with a market cap of $211.9 billion serving major chipmakers including TSMC, Samsung, Intel, and Micron.