🚨 LRCX $6.6M Option Position Closed Before Weekly Expiration!

📅 January 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just paid $6.6 MILLION to close out a short call position on Lam Research with just 3 days until expiration! This massive Buy-to-Close (BTC) trade suggests a sophisticated trader is taking profits or removing risk on a bet that went wrong as LRCX sits $23+ above the $180 strike. With a z-score of 3.52, this trade size is exceptionally unusual - happening only a few times per year for LRCX options.

💰 The Option Flow Breakdown

📊 What Just Happened

| Field | Value |

|---|---|

| Date/Time | January 6, 2026 at 09:54:09 ET |

| Symbol | LRCX |

| Option | LRCX20260109C180 |

| Strike | $180.00 |

| Expiration | January 9, 2026 (3 days!) |

| Type | CALL |

| Trade | BUY to Close |

| Size | 2,760 contracts |

| Price | $23.87 per contract |

| Premium | $6,600,000 |

| Spot Price | $203.65 |

| Open Interest | 3,400 contracts |

| Volume | 2,800 contracts |

| Z-Score | 3.52 (EXTREMELY UNUSUAL) |

🤓 What This Actually Means

Real talk: This is someone closing out a massive short call position they had on Lam Research. When you see "Buy to Close," it means they previously sold these calls (probably when LRCX was lower) and now they're buying them back to exit the trade.

Why this matters:

- 🎯 Deep in the money: The $180 calls are trading $23.65 in-the-money with LRCX at $203.65

- 💰 Expensive exit: At $23.87 per contract, they're paying almost pure intrinsic value to close

- ⏰ Time pressure: With only 3 days to expiration, this could be forced covering before assignment

- 📊 Huge size: 2,760 contracts represents 276,000 shares of exposure - this isn't retail

Translation for us regular folks: Someone bet LRCX wouldn't go above $180 (by selling calls), but the stock blasted through that level and they're now cutting their losses or locking in profits before things get worse. This is like betting against Michael Jordan in the playoffs - sometimes you just gotta admit defeat and move on! 😅

🏢 Company Overview

Lam Research Corporation is a $259.9B semiconductor equipment manufacturer that dominates the etch and deposition technology space. They're the picks-and-shovels play for the AI chip boom, with a commanding 45% market share in etch equipment and 80%+ dominance at sub-5nm nodes.

What they do: Lam makes the ultra-sophisticated machines that chipmakers like TSMC, Samsung, Intel, and Micron use to manufacture cutting-edge semiconductors. Think of them as building the factories that build AI chips.

Industry: Special Industry Machinery, NEC (Semiconductor Equipment)

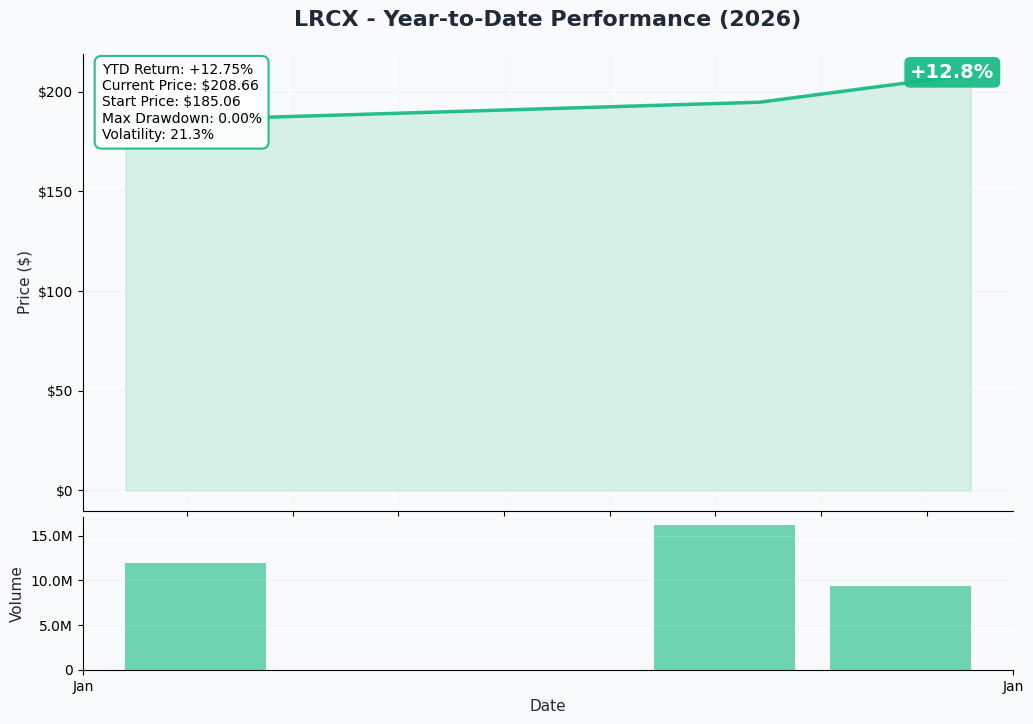

📈 Chart Check-Up

YTD Performance

Holy moly! 🚀 LRCX has been on an absolute tear, currently trading near $208-209 after explosive 2025 performance. The stock is up 143% in 2025, fueled by AI-driven semiconductor equipment demand. The recent consolidation around the $200 level shows some profit-taking, but the broader trend remains incredibly bullish.

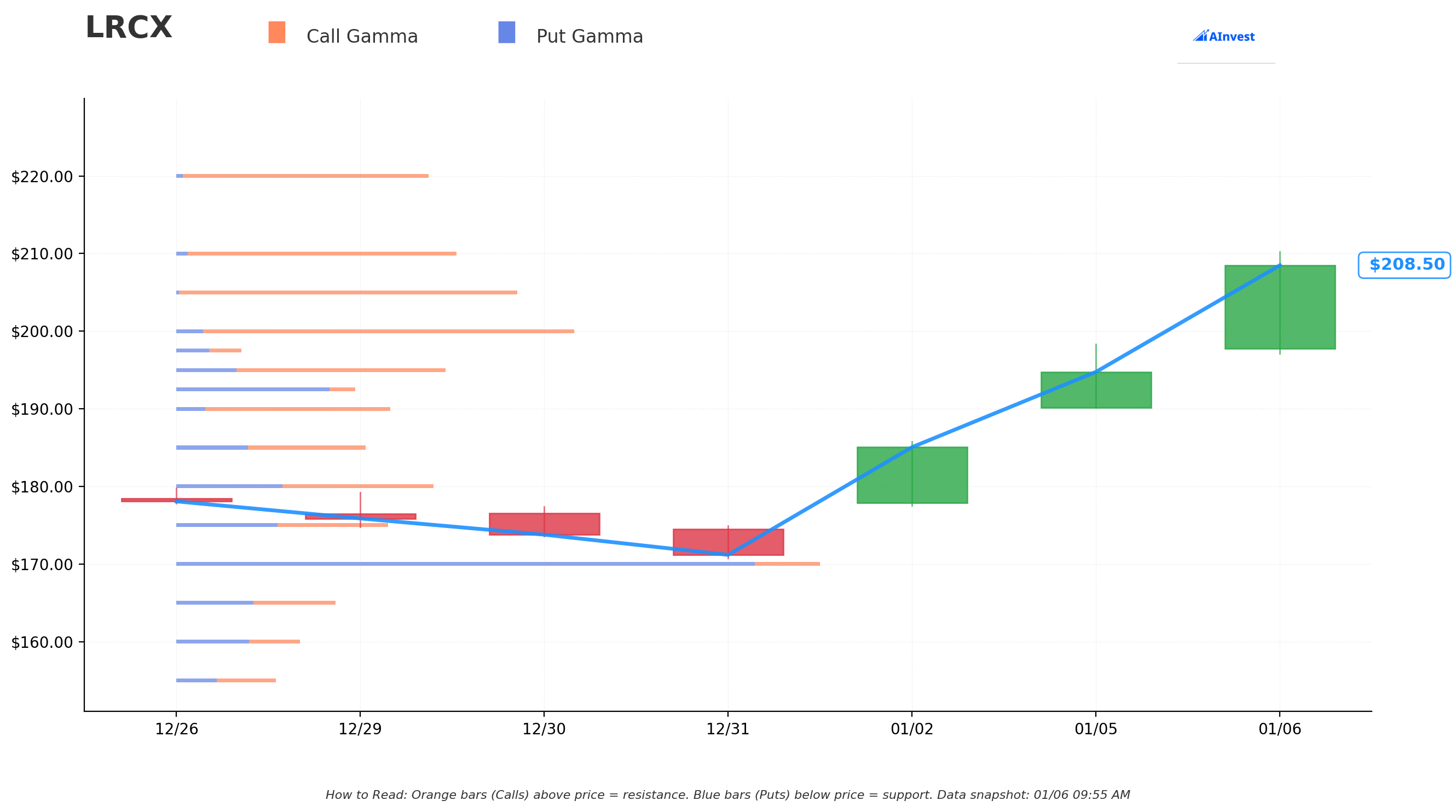

🔷 Gamma-Based Support & Resistance Analysis

Current Price: $208.45

The gamma wall shows where options traders have placed their bets, and these levels often act as magnets or barriers for price action:

🟢 Major Support Levels (Put Gamma):

- $205.00 - The fortress! 2.7B in total gamma makes this the strongest nearby support

- $200.00 - Psychological level with 3.1B gamma - big money defending this round number

- $195.00 - Secondary support at 2.1B gamma

- $180.00 - Where today's trade is centered! 2.0B gamma (this is the closed strike)

🔴 Resistance Levels (Call Gamma):

- $210.00 - Immediate ceiling with 2.2B gamma - needs volume to break through

- $220.00 - Major resistance at 2.0B gamma - would be a significant breakout level

Net GEX Bias: Bullish - Market makers are net short gamma, which means they'll buy into weakness and sell into strength, providing a stabilizing effect but with bullish undertone.

What this means: LRCX has strong support in the $200-205 zone where massive amounts of put options create a floor. The $210 level is the next battleground for bulls.

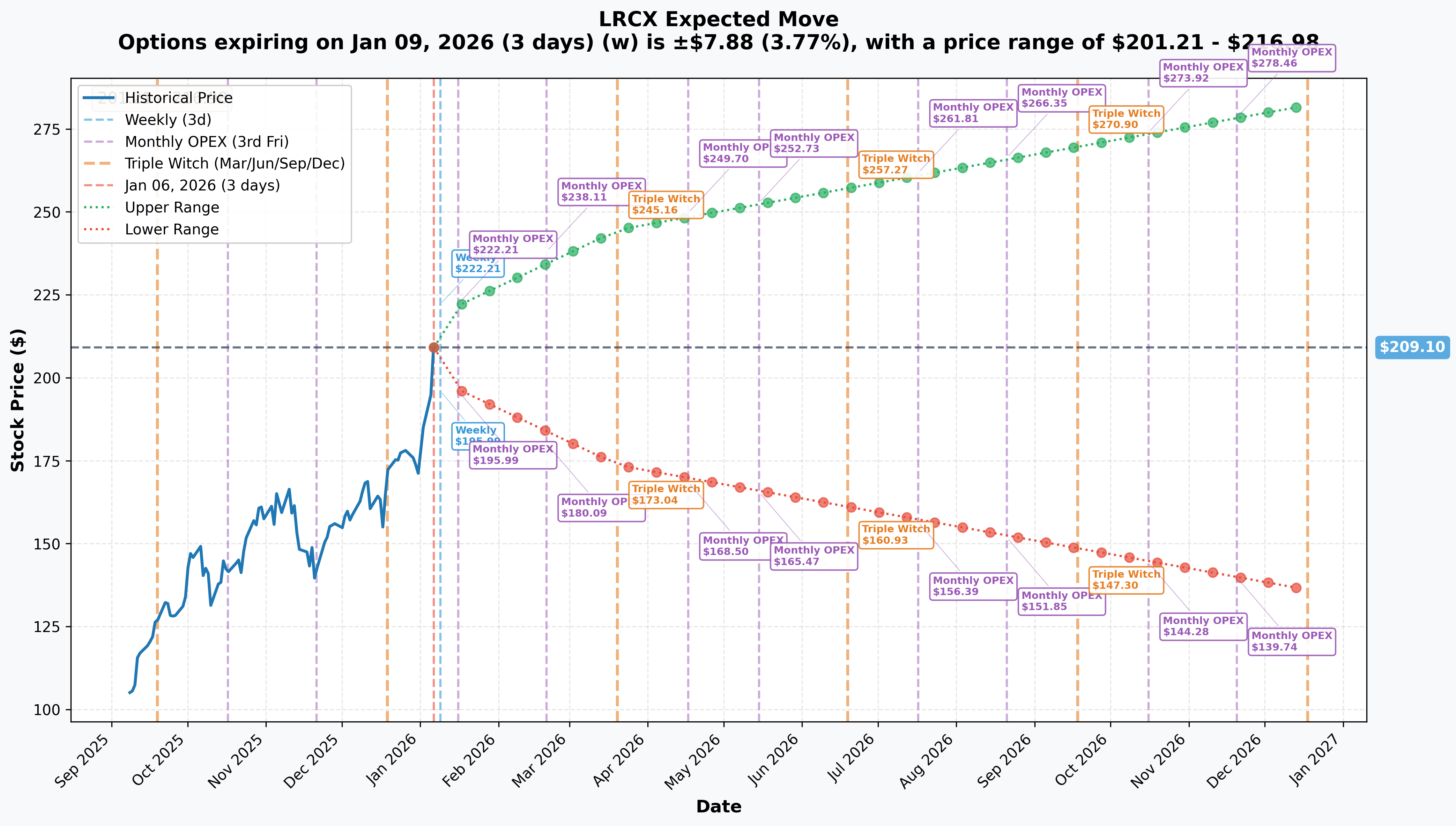

📊 Implied Move Analysis

Current Price: $209.10

The options market is pricing in these expected moves:

-

📅 Weekly (Jan 9 - THIS expiration!): ±3.77% → Range: $201.21 - $216.98

- Translation: Options are pricing a $8-9 move in either direction by Friday

- Our $180 strike is WAY outside this range (hence the BTC trade!)

-

📅 Monthly OPEX (Jan 16): ±6.1% → Range: $196.35 - $221.85

- Wider range heading into potential volatility

-

📅 Quarterly Triple Witch (Mar 20): ±16.98% → Range: $173.59 - $244.61

- Massive expected range for Q1 - market pricing in significant uncertainty

Key insight: The January 9th expiration (our trade's expiration!) expects LRCX to stay between $201-217. The person who sold $180 calls is so far in-the-money that they're guaranteed to be assigned unless they buy to close (which is exactly what this $6.6M trade is doing!).

🎪 Catalysts

🔥 Upcoming (Next 6 Months)

📊 Q2 FY2026 Earnings - January 28, 2026 1

- Expected Revenue: $5.2B (+/- $300M)

- Expected EPS: $1.15-1.17

- Key Metrics to Watch:

- China revenue percentage (expected decline to ~35% from 43%)

- Memory segment demand commentary (HBM boom!)

- 2026 WFE outlook update

- Export control impact quantification ($600M headwind)

💵 Dividend Payment - January 7, 2026 (Tomorrow!) $0.26 per share to holders of record December 3, 2025 2

📈 Memory Customer CapEx Explosions: According to AInvest's analysis, Lam's major customers are going on a spending spree in 2026:

- Micron: $20B CapEx (+45% YoY) - massive HBM capacity build-out

- Samsung: +50% HBM capacity expansion for AI demand

- SK Hynix: Accelerated HBM production timeline

🌐 Wafer Fab Equipment (WFE) Market Growth:

- 2026 WFE projected at $131B (+10% YoY)

- 2027 WFE expected to hit $150B (+14% YoY) per Bank of America

- SEMI forecasts $126.2B in 2026 (+9% YoY)

📚 Recent Past Events (Already Happened)

✅ Q1 FY2026 Earnings Beat - October 22, 2025 Lam crushed expectations according to Nasdaq's earnings report:

- Revenue: $5.32B (beat by $100M)

- Non-GAAP EPS: $1.26 (beat by $0.04)

- Record 50.6% gross margin

- Record 35.0% operating margin

🏢 Silicon Forest Expansion - November 21, 2025 Opened new $65M office building in Tualatin, Oregon with 700 workspaces

⚠️ Export Control Update - December 2, 2024 U.S. government announced new restrictions impacting China sales:

- $200M revenue reduction in December 2025 quarter

- $600M total revenue impact expected in calendar 2026

- China revenue expected to drop from 43% to <30% of total

📊 Analyst Upgrades - Q4 2025

- UBS maintained Buy with $200 target (December 23)

- Cantor Fitzgerald raised to $210 target (December 16) - record high!

- Consensus rating: 50% Strong Buy, 33% Buy per MarketBeat

🎲 Price Targets & Probabilities

Based on the gamma levels, implied move data, and upcoming catalysts, here's how I see LRCX setting up:

🚀 Bull Case: $220-225 (20% probability)

What needs to happen:

- January 28 earnings blow past expectations with strong 2026 guidance

- Memory CapEx announcements exceed current expectations

- China export control impact proves less severe than feared

- Breaks through $210 resistance with conviction

Gamma target: The $220 level has 2.0B in gamma resistance - if bulls can crack through $210, this becomes the next magnet.

Implied move support: The monthly range tops out at $221.85, making $220-225 the upper boundary of reasonable expectations.

📊 Base Case: $200-210 (50% probability)

What needs to happen:

- Earnings meet expectations without major surprises

- Stock consolidates in the strong gamma support zone

- Market digests valuation (31-36x forward P/E vs 23.7x historical average)

Gamma sweet spot: The $200-210 range has the highest gamma concentration, creating a natural consolidation zone. The $205 level (2.7B gamma) is the strongest support.

Catalyst timing: With earnings on January 28, expect choppy trading in this range until we get clarity on 2026 outlook.

😰 Bear Case: $180-195 (30% probability)

What needs to happen:

- Earnings disappoint or guidance gets cut

- China export controls prove more damaging than expected

- Memory customers pull back CapEx plans

- Broader market correction pulls down high-valuation semis

Gamma floor: The $195 level (2.1B gamma) and $180 level (2.0B gamma - our BTC strike!) provide significant support. Breaking below $195 would be concerning.

Valuation reality check: Some analysts see 20% downside risk given the 143% run in 2025 and stretched multiples.

💡 Trading Ideas

🛡️ Conservative: Put Credit Spread (Income Play)

Strategy: Sell the Feb 21 $190 put / Buy the Feb 21 $180 put Credit Received: ~$3.00 per spread ($300 per contract) Max Risk: $700 per spread (width minus credit) Breakeven: $187

Why this works:

- You're collecting premium betting LRCX stays above $190

- Strong gamma support at $200 and $195 provides cushion

- 7 weeks until expiration gives earnings time to pass

- Max gain if LRCX stays above $190 (58% probability)

- The $180 level (our BTC strike!) has 2.0B gamma support as your safety net

Best for: Neutral to slightly bullish traders who think LRCX holds $190+

⚖️ Balanced: February Straddle (Earnings Play)

Strategy: Buy Feb 21 $205 call + Feb 21 $205 put

Cost: $18-20 per straddle ($1,800-2,000 per contract)

Breakeven: $185 or $225

Target: Earnings volatility on Jan 28

Why this works:

- Captures the January 28 earnings event with 3+ weeks of time value

- The $205 strike sits right at the strongest gamma support level

- Monthly implied move suggests ±6.1% range ($196-222) - you profit if we break outside $185-225

- Eliminates directional risk - you win if LRCX makes a big move either way

- High IV means expensive, but earnings could deliver the juice

Best for: Traders who expect fireworks from earnings but aren't sure of direction

🚀 Aggressive: January 16 $215 Calls (Lottery Tickets)

Strategy: Buy Jan 16 $215 calls Cost: ~$2.50-3.50 per contract ($250-350 each) Max Risk: Premium paid Target: Quick 2-3x on momentum into earnings

Why this works (or doesn't!):

- Super cheap way to bet on continued momentum

- 10 days until expiration = pure gamma play

- Need LRCX to break $210 resistance and run toward $220

- If analyst upgrades continue or positive news drops, these explode

- Warning: These are basically scratch-off tickets - high risk of total loss

Best for: YOLO traders with money they can afford to lose who think LRCX rips higher into earnings season

⚠️ Risk Factors

Let's keep it real - here's what could wreck these trades:

🇨🇳 China Export Controls: The $600M revenue hit in 2026 is priced in, but what if it's worse? China was 43% of revenue in Q1. If restrictions tighten further, this could significantly impact 2026 estimates. Source

📊 Valuation Stretched: Forward P/E of 31-36x is way above the historical average of 23.7x. After a 143% run in 2025, some analysts see 20% downside risk. If growth disappoints, multiple compression could be painful.

📉 Memory Cycle Risk: Memory spending is historically cyclical and volatile. If AI demand moderates or customers get disciplined with CapEx, the memory equipment boom could stall quickly. Remember, this sector can turn on a dime! 🎢

🎰 Options Are Expensive: With implied volatility elevated ahead of earnings, option premiums are pricey. You're paying up for protection/speculation, which means you need bigger moves to profit.

⏰ Short-Dated Trade Risk: That $6.6M BTC trade shows how quickly positions can go against you near expiration. Don't sell naked calls on LRCX unless you really know what you're doing!

🏢 Insider Sales: CEO Tim Archer sold 50,000 shares at $163.86 in December under a 10b5-1 plan. While planned sales, insiders have been taking chips off the table.

📉 Broader Market Risk: High-beta stock (beta: 1.78) means if the broader market tanks, LRCX goes down 1.78x harder. With January seasonality often weak, watch macro conditions.

🎯 The Bottom Line

Here's the deal: This $6.6M Buy-to-Close trade tells us someone had a bearish/neutral bet on LRCX that went horribly wrong (or wonderfully right if they're locking in profits). They sold $180 calls expecting LRCX to stay below that level, but the stock blasted through and is now trading $23+ higher with only 3 days until expiration.

What this means for you:

📈 If you're bullish on LRCX: This BTC trade removes 2,760 contracts of overhead supply at $180, which is already deep support. The gamma data shows fortress-level support at $200-205, and the memory equipment boom is just getting started with Micron's +45% CapEx increase and HBM demand exploding. Mark your calendar for January 28 earnings - that's the big catalyst that determines if we break $210 or pull back to $200.

👀 If you're on the sidelines: Wait for earnings clarity on January 28. The valuation is stretched (31-36x forward P/E), and China risks are real. If LRCX dips back to $195-200 on any earnings wobble, that becomes a high-probability entry with 2.1B+ gamma support underneath you.

😰 If you're bearish: Good luck fighting this freight train! The short-seller who just spent $6.6M covering calls learned this lesson the hard way. That said, after a 143% run in 2025, some mean reversion is possible. If earnings disappoint on January 28, a move back to $195 wouldn't shock me. But trying to short this ahead of earnings with bullish momentum is like stepping in front of a speeding truck.

The real lesson from this trade: Don't sell naked calls on high-momentum stocks before major catalysts! This trader either:

- Lost a fortune as LRCX ripped from $180 to $208, or

- Made money elsewhere and is cutting risk before potential assignment

Either way, that's a $6.6M bill to get out of a position that's 3 days from expiration. Learn from their pain! 💸

My take: LRCX has legitimate tailwinds from AI/memory equipment boom, but after 143% gains, risk/reward is balanced. The $200-210 range is the battleground into earnings. Trade accordingly based on your risk tolerance, and never sell naked calls unless you can afford to get steamrolled!

⚠️ Risk Disclaimer: Options trading involves substantial risk and is not suitable for all investors. The strategies discussed can result in total loss of premium paid or unlimited losses in the case of naked short positions. Past performance does not guarantee future results. This analysis is for educational purposes only and not financial advice. Always do your own research and consider consulting a licensed financial advisor before making investment decisions.