📉 Southwest Airlines (LUV) $1.9M Put Purchase - Smart Money Hedges Transformation Risk! 🛡️

📅 December 5, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.9 MILLION on Southwest Airlines puts this morning at 11:47:22! This defensive bet bought 23,000 contracts of $35 strike puts expiring January 16th - protecting against downside just as Southwest executes its most radical transformation in 53 years. With the airline ditching its iconic free bags and open seating policies to chase $1.5B in new revenue, smart money is buying insurance against execution risk. Translation: Big money sees 2026 as make-or-break for Southwest's reinvention!

📊 Company Overview

Southwest Airlines (LUV) is the largest domestic air carrier in the United States by passengers boarded:

- Market Cap: $18.52 Billion (4th largest U.S. carrier)

- Industry: Air Transportation, Scheduled

- Current Price: $37.45 (near 52-week high of $37.96)

- Primary Business: All-Boeing 737 fleet operating point-to-point short-haul leisure routes, undergoing massive transformation to assigned seating and premium cabins by January 2026

💰 The Option Flow Breakdown

The Tape (December 5, 2025 @ 11:47:22):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:47:22 | LUV | ASK | BUY | PUT $35 | 2026-01-16 | $1.9M | $35 | 23K | 5.4K | 22,000 | $37.45 | $0.85 |

🤓 What This Actually Means

This is a bearish directional bet with defensive hedging characteristics! Here's the breakdown:

- 💸 Significant premium paid: $1.9M ($0.85 per contract × 22,000 contracts)

- 📉 Downside strike: $35 provides 6.5% cushion below current price of $37.45

- ⏰ Strategic timing: 42 days to expiration captures critical transformation milestones through early January 2026

- 📊 Unusual size: 23,000 volume vs 5,400 open interest (4.26x ratio) - massive fresh positioning

- 🚨 Extremely unusual: Z-score of 18.03 classifies this as EXTREMELY_UNUSUAL - happens a few times a year

- 🏦 Institutional hedge: This represents 2.2 million shares worth ~$82M of downside protection

What's really happening here: This trader is positioning for potential turbulence as Southwest executes its transformation. With assigned seating sales starting July 29, 2025 and first flights January 27, 2026, the next 42 days represent a critical window. The $35 strike at $0.85 suggests they're protecting against:

- Customer backlash to bag fees ($35 first bag, $45 second) starting May 2025

- Technology glitches during assigned seating rollout (December 2022 meltdown still fresh)

- Disappointing early booking data for premium seats

- Government shutdown impact on Q4 earnings (already cut guidance to $500M EBIT from $600-800M)

Unusual Score: 🔥 EXTREMELY UNUSUAL (18.03 Z-score) - This is about 18 standard deviations above normal activity! The 4.26x volume-to-OI ratio shows this is fresh positioning opening new bearish exposure, not closing existing positions.

📈 Technical Setup / Chart Check-Up

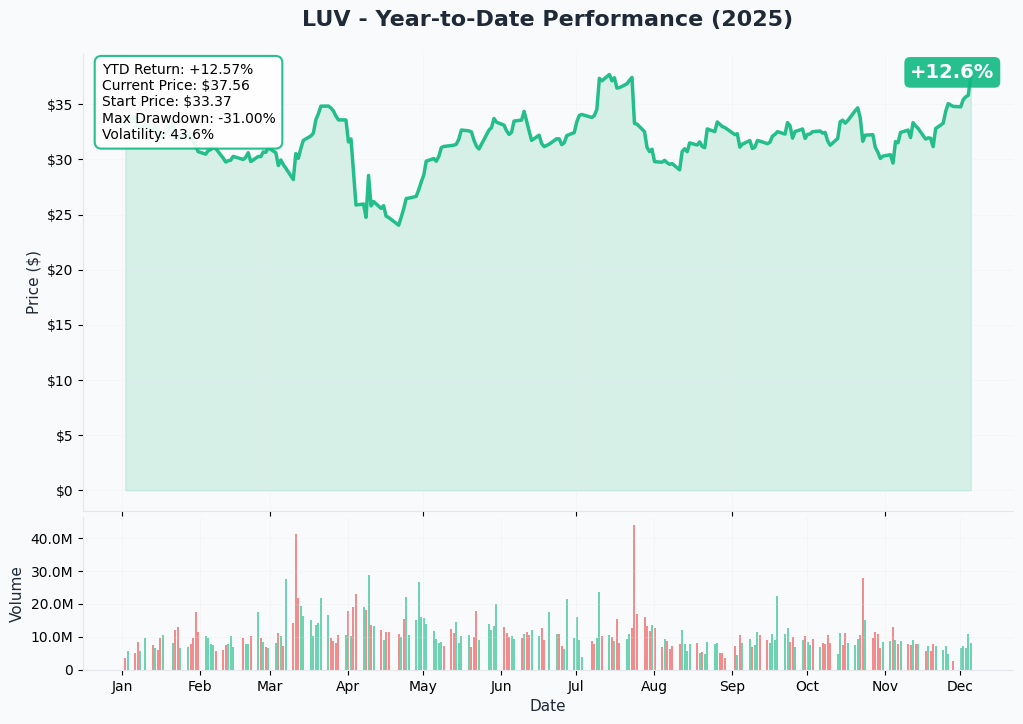

YTD Performance Chart

Southwest has had a volatile transformation year - currently trading at $37.45 after a dramatic recovery from $23.82 lows in early September. The stock surged +55% in just 3 months following the Elliott Management settlement in October 2024 and announcement of sweeping policy changes.

Key observations:

- 🚀 Major rally: Explosive move from $24 in September to $37.96 all-time high on transformation optimism

- 📈 Positive YTD: Up approximately +35% year-to-date

- 📊 Elliott catalyst: Board overhaul and strategic validation drove sharp re-rating

- ⚠️ Recent pressure: December guidance cut due to government shutdown and fuel costs

- 📉 Trading volume: Current 5M vs 9M average suggests consolidation phase

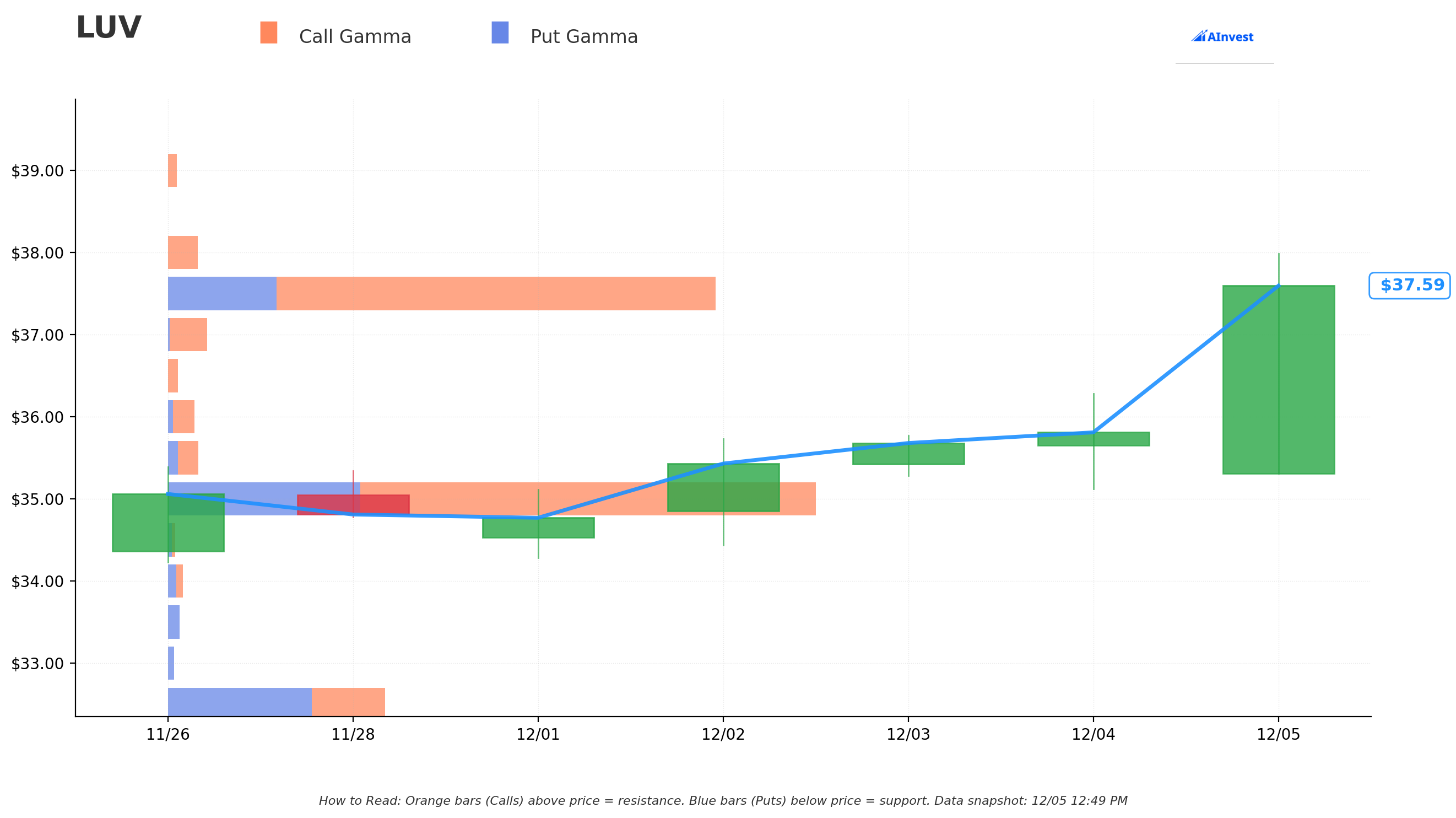

Gamma-Based Support & Resistance Analysis

Current Price: $37.635

The gamma exposure map reveals critical price levels that will govern near-term trading action:

🔵 Support Levels (Put Gamma Below Price):

- $37.50 - Immediate support with 10.1B total gamma (0.36% below current - VERY CLOSE!)

- $37.00 - Secondary floor at 0.7B gamma (1.69% down)

- $36.00 - Tertiary support with 0.48B gamma (4.34% drop)

- $35.50 - Extended support at 0.54B gamma (5.67% decline)

- $35.00 - MAJOR FLOOR with 11.85B gamma (exactly where this put is struck! 7.00% down)

- $32.50 - Deep support at 4.10B gamma (13.64% crash scenario)

🟠 Resistance Levels (Call Gamma Above Price):

- $38.00 - Immediate ceiling with 0.56B gamma (0.97% overhead)

- $40.00 - Major resistance at 5.81B gamma (6.28% rally required)

- $42.50 - Extended ceiling with 0.97B gamma (12.93% upside)

- $45.00 - Distant target at 0.67B gamma (19.57% rally)

What this means for traders: Southwest is trading precariously close to $37.50 support (just 14 cents away!). The gamma data reveals a MASSIVE wall at $35.00 with 11.85B in total gamma exposure - the second strongest level on the entire board after $37.50. This is NOT coincidental - the put buyer struck EXACTLY at this major gamma support level.

Critical insight: The stock is essentially trapped between $37.50 support and $38.00 resistance in a tight 1.3% range. A break below $37.50 could trigger momentum selling toward $37.00, then accelerate to the $35.00 mega-support where the puts become at-the-money. The unusual put positioning suggests smart money expects this $37.50 level to fail.

Net GEX Bias: Bullish (28.68B call gamma vs 13.15B put gamma) - Overall positioning remains constructive with 2.2x more call exposure, but the immediate price action is constrained by proximity to support.

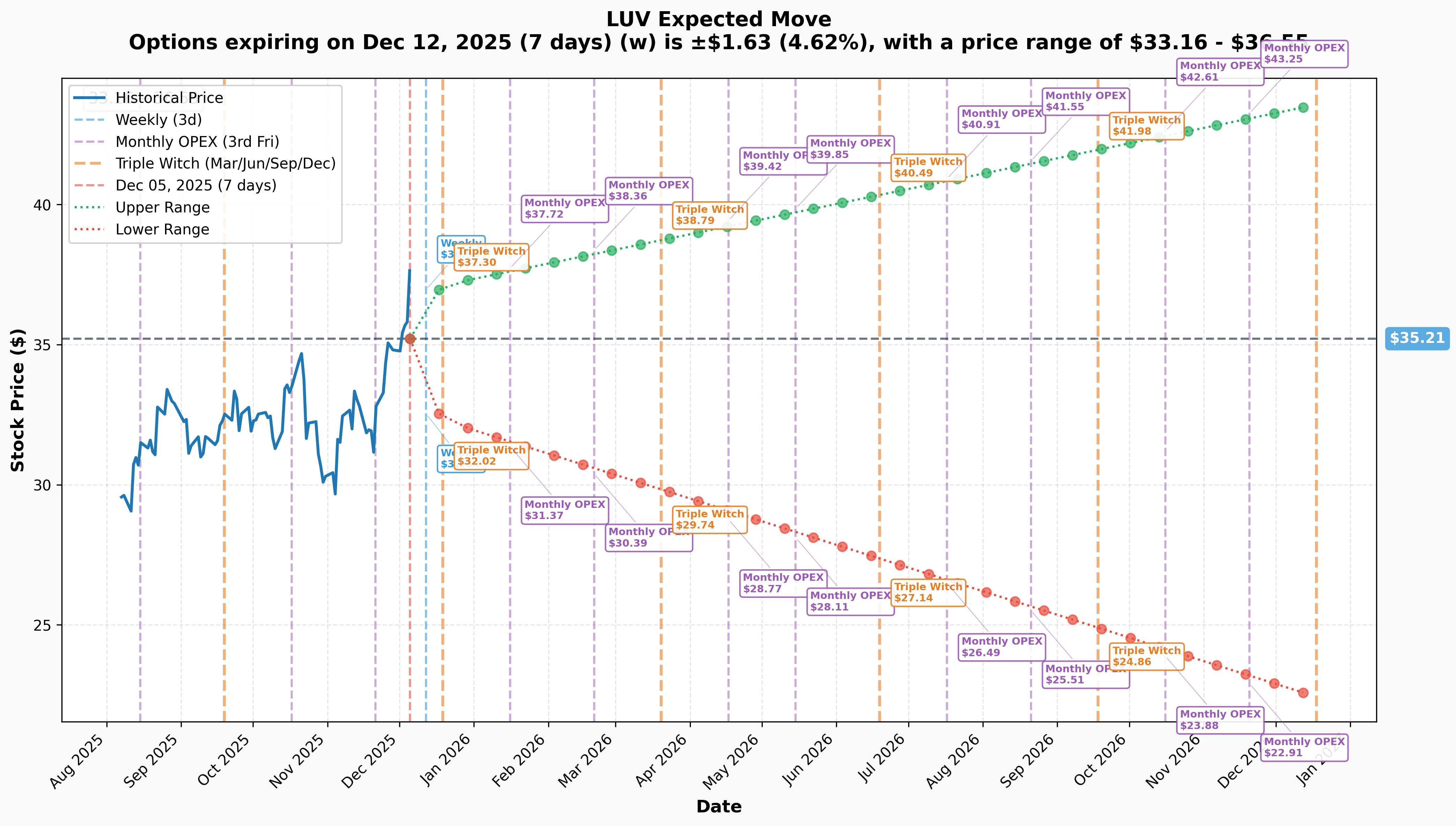

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 7 days): ±$1.63 (±4.62%) → Range: $33.16 - $36.55

- 📅 Monthly OPEX (Dec 19 - 14 days): ±$2.24 (±6.36%) → Range: $32.29 - $37.12

- 📅 Quarterly Triple Witch (Dec 19 - same): ±$2.24 (±6.36%) → Range: $32.29 - $37.12

- 📅 January OPEX (Jan 16 - 42 days - THIS TRADE!): ±$6.35 (±18.0%) → Range: $31.37 - $37.72

Translation for regular folks: The options market is pricing in a 4.6% move ($1.63) by December 12, expanding to a 6.4% swing ($2.24) through December 19 triple witch expiration. However, the real action is expected through January 16th with an implied 18% move that takes the lower range to $31.37 - well below the $35 put strike.

Key insight: The dramatic increase from 4.6% (weekly) to 18% (January) reflects MASSIVE uncertainty around Southwest's transformation execution. The market thinks there's a real possibility LUV trades as low as $31 by mid-January if:

- Assigned seating sales (starting July 29) show weak early booking data

- Technology issues emerge during preparation phase

- Government shutdown impact worse than disclosed

- Customer revolt against bag fees materializes

The $35 put buyer is positioned right in the middle of this implied range - not catastrophic downside betting, but protection against a 6-7% correction over next 42 days.

🎪 Catalysts

✅ Recent Catalysts (Already Happened)

Elliott Management Settlement (October 2024)

Southwest reached a landmark settlement with activist investor Elliott Management, ending a months-long proxy battle:

- Elliott's Stake: 14.8% economic exposure ($1.34 billion invested)

- Board Overhaul: Six new directors appointed, representing the largest board change Elliott has driven in a U.S. fight

- Leadership: CEO Bob Jordan retained position, avoiding Elliott's initial demand for removal

- Strategic Impact: Settlement validated Elliott's critique that leadership was "too entrenched" and accelerated transformation timeline

Q3 2024 Earnings (October 24, 2024)

Southwest reported record third quarter revenue of $6.87 billion (up 5.3% YoY, beating consensus):

- Net Income: $67 million ($0.11 per diluted share)

- Adjusted EPS: $0.15 (beating consensus of $0.05 but down 60.5% YoY)

- Load Factor: 81.2% (up 0.5 percentage points YoY)

- Revenue Passenger Miles: 36.73 billion (up 3.1% YoY)

Q4 2024 Results (January 2025)

Full-year results released showing transformation momentum:

- Q4 Net Income: $261 million ($0.42 per diluted share)

- Q4 Adjusted EPS: $0.56 (up 47% YoY)

- Full-Year Net Income: $465 million ($0.76 per diluted share)

- Full-Year Adjusted EPS: $0.96

Q1 2025 Earnings (April 24, 2025)

First quarter results beat expectations despite seasonal weakness:

- Adjusted EPS: Loss of $0.13 vs consensus loss of $0.18 (beat)

- Revenue: $6.43 billion vs $6.40 billion expected (beat)

- Operating Revenue: Record quarterly $6.4 billion

- Stock Reaction: +1.89% to $25.52

Strategic Policy Changes (September-October 2024)

Southwest announced sweeping operational changes breaking from 53-year traditions:

1. End of Open Seating (Effective January 27, 2026)

- Assigned seating goes on sale July 29, 2025 for travel starting January 27, 2026

- New seat categories: Standard, Preferred (near front), Extra Legroom (33-35 inches)

- Expected financial impact: $1+ billion incremental EBIT in 2026, $1.5 billion run rate in 2027

2. End of "Bags Fly Free" (Effective May 2025)

- First checked bag: $35; Second bag: $45

- Free bags retained for highest fare tier and A-List Preferred members

3. Premium Cabin Retrofit

- Over 400 aircraft already retrofitted with extra legroom seating as of Q3 2025

- Full fleet retrofit target by January 2026 launch

🔥 Upcoming Catalysts (Next 6 Months)

⚠️ IMMEDIATE RISK: Revised 2025 Guidance Cut (December 5, 2025 - TODAY!)

Southwest lowered 2025 earnings expectations on December 5, 2025 due to government shutdown and fuel pressures:

- 2025 EBIT Guidance: ~$500 million (down from prior $600-800 million range)

- Cause: Reduced demand during FAA shutdown, flight cancellations at 40+ major airports, higher fuel prices

- Capacity Adjustment: Full-year 2025 capacity growth reduced to ~1%

- Initiative Targets Reaffirmed: $1.8 billion incremental EBIT for 2025, $4.3 billion for 2026

This guidance cut happened THE SAME DAY as this $1.9M put purchase - suggesting the trade was either:

- Positioned ahead of the announcement (insider knowledge)

- Placed immediately after announcement betting on further deterioration

- Protecting existing long position against cascading bad news

Assigned Seating Launch (July 29, 2025 - Sales Begin in 7.5 months)

Critical Revenue Catalyst:

- Sales Start: July 29, 2025

- First Flights: January 27, 2026

- Expected Revenue Impact: $1+ billion incremental EBIT in 2026, $1.5 billion annual run rate by 2027

- Customer Research: 80% of Southwest customers and 86% of other airline passengers prefer assigned seats

- Fleet Status: Over 400 aircraft retrofitted as of Q3 2025, on track for full fleet by January 2026

Why this matters for the put trade: The January 16 expiration expires BEFORE assigned seating sales begin (July 29) but captures any negative pre-announcement data leaks, technology concerns, or early investor skepticism about execution. If the market senses problems with the rollout in December/January, the stock could sell off hard.

New Cabin Interiors (October 2025 - Ongoing)

Fleet Modernization:

- First MAX 8 with New Cabin: Entered service October 2025

- Features: RECARO R2 seats with multi-adjustable headrests, device holders, USB-A and USB-C power ports

- Fleet Size: 810 aircraft (5th largest commercial fleet globally, largest 737 operator)

- 2025 Delivery Expectations: Up to 47 Boeing 737 MAX 8 aircraft (down from original 136 due to Boeing delays)

Global Airline Partnerships (2025-2026)

Network Expansion:

- Icelandair Partnership: Launched 2025 through Baltimore-Washington International (BWI)

- Condor Partnership: Announced December 2025 for additional Atlantic routes

- China Airlines Partnership: First trans-Pacific carrier agreement

- EVA Air Partnership: Additional trans-Pacific service

- Total Partners: Five international airline partners (significant for historically domestic-focused carrier)

Boeing 737 MAX 7 Certification (Expected Late 2026)

Fleet Modernization Risk/Catalyst:

- Order Book: 342 Boeing 737 MAX 7 aircraft on order

- Current Status: Certification delayed, not expected until late 2026

- Impact: 27 MAX 7s originally scheduled for 2024 pushed to 2025, now further delayed

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th expiration:

📈 Bull Case (20% probability)

Target: $40-$42

How we get there:

- ✅ Government shutdown impact proves temporary - air traffic returns to normal by late December

- 📈 Early booking data for assigned seating (internal metrics) leaks positive - strong customer acceptance

- 🛡️ Credit agencies maintain investment-grade ratings despite guidance cut

- 💪 Fuel prices stabilize or decline, allowing EBIT guidance raise back toward $600M

- 🚀 Boeing delivers closer to 47 MAX 8s than feared, supporting capacity growth

- 📊 Q4 2025 revenue tracking better than feared despite shutdown

- 🔄 Breakout above $38 gamma resistance triggers technical rally to $40

Key metrics needed:

- January capacity utilization >80% (proving demand resilience)

- No further guidance cuts or negative pre-announcements

- Technology systems testing for assigned seating progressing smoothly

- Analyst upgrades as transformation de-risks

Probability assessment: Only 20% because it requires PERFECT execution after today's guidance cut damaged credibility. The stock faces massive resistance at $38-$40 with limited catalysts to drive breakout before January 16.

🎯 Base Case (50% probability)

Target: $35-$38 range (CONSOLIDATION)

Most likely scenario:

- ⚖️ Stock digests today's guidance cut over next 2-3 weeks

- 📊 Trading range-bound between $37.50 support and $38.00 resistance

- 🤷 No major positive or negative news on transformation execution

- ⏰ Market waits for July 29 assigned seating sales launch for real data

- 💤 Implied volatility gradually declines from current elevated levels

- 🔄 Modest drift toward $35-$36 on profit-taking and risk reduction

- 📉 Put buyer's $35 strike finishes near-the-money or slightly profitable if stock drifts to $35-$36

This is the put buyer's expected scenario: Stock consolidates weakly, potentially testing $35 support as investors reduce exposure ahead of transformation risks. The $1.9M premium is insurance against worse outcomes, but breakeven is around $34.15 ($35 strike - $0.85 paid).

Why 50% probability: Stock lacks near-term catalysts to drive higher, but fundamentals not broken enough to collapse. Most likely outcome is range-bound chop with slight bearish bias.

📉 Bear Case (30% probability)

Target: $31-$35 (PUT PAYS OFF!)

What could go wrong:

- 😰 Further guidance cuts as government shutdown impact lingers longer than expected

- 🚨 Technology issues surface during assigned seating preparation - December 2022 meltdown PTSD

- 📉 Customer backlash to bag fees intensifies - negative social media trends, boycott threats

- 💸 Credit rating downgrade from BBB/Baa1 as profitability deteriorates

- ⚠️ Boeing delivery delays worsen - receives <30 aircraft instead of 47

- 🇨🇳 Domestic demand weakens further - consumer confidence at multi-year lows

- 🔨 Break below $37.50 gamma support triggers cascade to $37, then $35

- 📊 Analyst downgrades citing execution risk and stretched timeline

Critical support levels:

- 🛡️ $37.50: Must hold or momentum shifts bearish (ALREADY THREATENED!)

- 🛡️ $37.00: Secondary floor - break here accelerates to $35

- 🛡️ $35.00: MAJOR GAMMA FLOOR (11.85B) + this put strike - hard floor

Probability assessment: 30% because Southwest faces EXTREME execution risk over next 6 weeks. Today's guidance cut proves near-term visibility is poor. Any additional negative news could break $37.50 support and trigger selling to $35 put strike.

Put P&L in Bear Case:

- Stock at $33 on Jan 16: Puts worth $2.00, profit = $1.15/share × 22,000 = $253K gain (135% ROI)

- Stock at $31 on Jan 16: Puts worth $4.00, profit = $3.15/share × 22,000 = $693K gain (371% ROI!)

- Stock at $35 on Jan 16: Puts worth $0 (at-the-money), loss = -$0.85/share × 22,000 = -$187K (100% loss)

- Stock at $37+ on Jan 16: Puts expire worthless, total loss = -$1.9M

💡 Trading Ideas

🛡️ Conservative: Avoid Until Transformation Proves Out

Play: Stay on sidelines until assigned seating sales data (July 29, 2025) provides real validation

Why this works:

- ⏰ Transformation execution risk is EXTREME - Southwest changing 53-year business model

- 📉 Today's guidance cut shows near-term visibility is terrible (cut from $600-800M to $500M)

- 🎯 No meaningful catalysts between now and January 16 expiration to drive upside

- 💸 Better entry likely at $32-$35 if execution concerns materialize

- 📊 Credit rating agencies have negative outlooks (S&P BBB, Moody's Baa1) - downgrade risk

- 🤔 The $1.9M institutional put buy signals smart money is worried

Action plan:

- 👀 Monitor assigned seating preparation progress through airline industry publications

- 🎯 Look for pullback to $32-$34 for stock entry with meaningful margin of safety

- ✅ Need to see July 29 booking data showing strong customer acceptance before committing

- 📊 Watch for credit rating actions - downgrade would be major negative

- ⏰ Revisit mid-2026 after assigned seating rollout complete and initial results known

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 15-20% drawdown if transformation stumbles. Get better entry if stock corrects. Maintain capital preservation.

⚖️ Balanced: Small Put Spread Hedging Transformation Risk

Play: Define risk put spread mirroring institutional positioning

Structure: Buy $37 puts, Sell $35 puts (January 16 expiration - SAME as the $1.9M trade)

Why this works:

- 📊 Defined risk spread ($2 wide = $200 max risk per spread)

- 🎯 Targets consolidation range $35-$38 where stock likely trades

- 🤝 Essentially "copying" the smart money bearish positioning

- ⏰ 42 days to expiration captures government shutdown fallout and any pre-announcement leaks

- 🛡️ Protects against execution risk without betting on catastrophic failure

- 💰 Limited capital at risk - can position size appropriately

Estimated P&L:

- 💸 Pay ~$0.60-0.70 net debit per spread (current pricing)

- 📈 Max profit: $130-140 if LUV below $35 at January expiration

- 📉 Max loss: $60-70 if LUV above $37 (defined and limited)

- 🎯 Breakeven: ~$36.30-36.40

- 📊 Risk/Reward: ~2:1 which is acceptable for bearish speculation

Entry timing:

- ⏰ Enter now or wait 1-2 days for any volatility spike

- 🎯 Only enter if stock trading $37-38 (gives room to work)

- ❌ Skip if stock already below $36 (spread too close to at-the-money)

Position sizing: Risk only 2-5% of portfolio (directional speculation, not core holding)

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Outright Put Purchase (FOLLOW THE WHALE!)

Play: Buy puts betting on transformation execution failure

Structure: Buy $35 puts or $34 puts (January 16 expiration)

Why this could work:

- 🐋 Following $1.9M institutional positioning - they clearly see significant downside risk

- 📉 Stock trading at $37.45, just 14 cents above $37.50 gamma support - vulnerable!

- 💥 Today's guidance cut could be first of multiple negative announcements

- 🎰 Transformation has massive execution risk - December 2022 operational meltdown precedent

- 📊 Boeing delivery delays constraining growth (only 20-47 vs 85+ planned)

- ⚡ Customer backlash to bag fees could be more severe than management expects

- 🚨 Break below $37.50 triggers cascade to $35, potentially $32.50

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Puts cost $0.85-1.10 depending on strike ($85-110 per contract)

- ⏰ TIME DECAY: Theta burns value daily - need move to happen soon

- 📈 Reversal risk: Any positive news on transformation sends stock to $40+, puts lose 50-80%

- 😱 Binary execution: Either works big or loses most of premium

- 🎢 Stock could consolidate $36-38 and puts finish near worthless

- ⚠️ No earnings catalyst before expiration - relying on negative pre-announcements

Estimated P&L ($35 puts at $0.85):

- 💰 Cost: $85 per put contract

- 📈 Profit scenario: Stock at $33 = put worth $2.00, gain = $115 (135% ROI)

- 🚀 Home run: Stock at $31 = put worth $4.00, gain = $315 (371% ROI)

- 📉 Loss scenario: Stock at $36-37 = put worth $0-0.50, loss = $35-85 (40-100% loss)

- 💀 Total loss: Stock above $37 = lose entire $85 (100% loss)

Breakeven point: $34.15 (need 9% decline from current $37.45)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand you're betting on near-term execution failure

- ✅ Accept that stock could stay $36-38 and you lose money despite being "right" directionally

- ✅ Will take profits at 50-100% gains rather than holding for home run

- ⏰ Plan to manage position actively - this isn't buy-and-forget

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Probability of profit: ~35-40% (need significant negative catalyst)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🚨 Transformation execution risk is EXTREME: Southwest is attempting its most radical operational change in 53-year history - assigned seating starting January 27, 2026, bag fees starting May 2025, premium cabins, four-tier fare structure. Technology systems must support seat assignments, pricing tiers, and partnerships. December 2022 operational meltdown (17,000+ cancellations) shows what happens when Southwest's systems fail. Customer backlash if loyal base rejects changes could damage brand permanently.

-

💸 Today's guidance cut damages credibility: 2025 EBIT guidance slashed to $500M from $600-800M due to government shutdown and fuel costs. This proves management has poor near-term visibility. If they were wrong by $100-300M on 2025, how confident should investors be in $1.5B premium seating revenue target for 2027?

-

🛫 Boeing dependency creates growth constraint: All-Boeing 737 fleet creates single-supplier risk. Only receiving 20-47 aircraft in 2025 vs 85+ originally planned due to Boeing quality issues. MAX 7 certification delayed to late 2026, eliminating 27+ aircraft from 2025 plans. Can't grow capacity without aircraft deliveries, limiting revenue upside.

-

💰 Labor costs inflated with no offset yet: $12 billion pilot contract with ~50% cumulative pay increases through 2028, 22% flight attendant raises in April 2024. All 12 unions covering 83% of employees have new contracts through ~2028. Costs up massively, but revenue initiatives (assigned seating, bag fees) don't launch until 2026. Margin squeeze continues through 2025.

-

📉 Domestic demand weakening: U.S. domestic travel spending down 3% YoY in Q2 2025, consumer confidence at multi-year lows. Southwest's core customer (price-sensitive leisure traveler) most affected by economic headwinds. Shorter booking windows reducing revenue visibility. Corporate travel demand lower than expected.

-

⚖️ Credit rating at risk: S&P BBB rating with negative outlook (July 2024), Moody's Baa1 rating with negative outlook (October 2024). Both agencies concerned about financial trajectory. Investment-grade status maintained but at risk if transformation fails. Downgrade would increase borrowing costs and damage customer confidence.

-

🎯 Unproven revenue assumptions: $1.5 billion annual premium seating target is ambitious and untested. Assumes customer willingness to pay for assignments and extra legroom. Risk that loyal Southwest customers trade down to Basic fares, offsetting gains from premium seats. No airline has successfully transitioned from open to assigned seating at this scale.

-

🏪 Competitive pressure intensifying: Ultra-low-cost carriers (Spirit, Frontier) adding pressure on leisure routes. Premium carriers (Delta, United) improving products and winning share. Southwest losing unique positioning - adding bag fees eliminates "Bags Fly Free" differentiation, but can't compete on premium product with legacy carriers (no lie-flat seats, limited international service).

-

📊 Stock near 52-week highs with limited upside catalysts: Trading at $37.45 vs 52-week high of $37.96 after 55% rally in 3 months. Valuation reflects successful transformation, but execution hasn't happened yet! Limited margin of safety. Next 6 months lack positive catalysts (assigned seating sales July 29 is beyond January 16 put expiration).

-

🎢 Gamma levels show vulnerability: Stock trading just 14 cents above $37.50 support with massive 10.1B gamma. Break below triggers selling to $37, then potentially cascade to $35 mega-support (11.85B gamma). Technical setup favors downside over next few weeks.

🎯 The Bottom Line

Real talk: Someone just spent $1.9 MILLION betting that Southwest's transformation story has significant downside risk over the next 42 days. This isn't a bet against Southwest long-term - it's a bet that execution between now and January 16 could stumble badly.

What this trade tells us:

- 🎯 Smart money sees material risk to the $35-$37 price level (6-9% downside)

- 💰 They're worried enough to pay $0.85/share for protection expiring in just 6 weeks

- ⚖️ The timing (same day as guidance cut) shows they expect near-term deterioration

- 📊 The $35 strike sits exactly at major gamma support - they expect this level to be tested

- ⏰ January 16 expiration captures government shutdown fallout, technology preparation issues, and any negative pre-announcements

This is NOT a "Southwest is going bankrupt" signal - it's a "transformation risk is underpriced" signal.

If you own Southwest:

- ✅ Consider trimming 30-50% at $37-38 levels to lock in gains from September rally

- 📊 Set MENTAL STOP at $37.00 (major support) to protect remaining position

- ⏰ Don't get greedy - you're up 55% in 3 months! Taking some profit is prudent.

- 🎯 If stock holds $37 through January, can re-evaluate on assigned seating sales data (July 29)

- 🛡️ Consider buying 1-2 protective puts per 200 shares if holding large position through transformation

If you're watching from sidelines:

- ⏰ Avoid new long positions until transformation execution de-risks (post July 29 sales data)

- 🎯 Better entry likely at $32-$35 if execution concerns materialize

- 📈 Need confirmation of: assigned seating customer acceptance, technology readiness, no further guidance cuts

- 🚀 Longer-term (12+ months), if transformation delivers $1.5B revenue, stock could reach $42-$45

- ⚠️ Current risk/reward unfavorable - downside to $32 (-15%) more likely than upside to $42 (+12%)

If you're bearish:

- 🎯 First support at $37.50 (must break), major support at $37.00, target support at $35.00

- 📊 Put spreads ($37/$35 or $36/$34) offer defined-risk way to play downside

- ⚠️ Watch for break below $37.50 - that's the trigger for cascade to $35

- 📉 Outright puts risky without catalyst, but following the $1.9M whale has logic

- ⏰ Manage position actively - take profits at 50-100% gains

Mark your calendar - Key dates:

- 📅 December 12 - Weekly implied move window closes (±4.6% = $33.16-$36.55 range)

- 📅 December 19 - Monthly OPEX / Triple Witch (±6.4% = $32.29-$37.12 range)

- 📅 January 16, 2026 - Expiration of this $1.9M put trade

- 📅 January 27, 2026 - First assigned seating flights begin!

- 📅 May 2025 - Bag fees go into effect ($35/$45)

- 📅 July 29, 2025 - Assigned seating sales begin (CRITICAL DATA POINT!)

- 📅 Late 2026 - Boeing 737 MAX 7 expected certification

Final verdict: Southwest's long-term transformation story could work brilliantly - $4.3B incremental EBIT by 2026 from assigned seating, premium cabins, and international partnerships is a massive prize IF execution delivers. BUT, near-term risk/reward is TERRIBLE at $37.45 after today's guidance cut. The $1.9M put purchase is a CLEAR warning: smart money is derisking before potential turbulence.

Wait for better prices. Let transformation prove out. The opportunity will still be there at $32-$35 with 20% less risk.

Be patient. Protect your capital. This is a show-me story now. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 18.03 Z-score unusual classification reflects this trade's size relative to recent LUV activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Southwest's transformation involves significant execution risk with potential for material stock price volatility in either direction.

About Southwest Airlines: Southwest Airlines operates as the largest domestic air carrier in the United States by passengers boarded, maintaining an all-Boeing 737 fleet of approximately 800 aircraft focused on short-haul leisure routes, with a market cap of $18.52 billion in the Air Transportation industry.