💰 LUV Massive INCOME Generation Play - $7.1M Covered Call or Naked Short!

📅 December 16, 2025 | 🔥 Unusual Institutional Income Strategy Detected

🏢 Company Overview

Southwest Airlines Co. (LUV)

- Description: Southwest Airlines Co. is the largest domestic air carrier in the United States by passengers boarded, operating an all-Boeing 737 fleet of nearly 800 aircraft focusing primarily on short-haul leisure routes. The airline uses a point-to-point network and plans cabin modifications in early 2026 to introduce extra legroom rows, assigned seating options, and new fare categories.

- Market Cap: $21.6B

- Sector: Air Transportation, Scheduled

- Total Employees: 72,223

🎯 The Quick Take

Someone just sold $7.1 MILLION worth of call options on Southwest Airlines, collecting massive premium by selling 15,000 calls at the $40 strike expiring March 2026! This trade represents 1.5 million shares worth of exposure - either a massive covered call strategy from someone holding the stock or a bold naked short position betting LUV won't break $40 by March. With the stock at $42.65, they're collecting premium on calls just 6% out of the money.

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (December 16, 2025):

🕐 09:32:01 - MASSIVE CALL SELL:

- Symbol: LUV

- Action: MID SELL CALL

- Expiration: 2026-03-20

- Strike: $40

- Premium: $7.1M 💸

- Volume: 15,000 contracts

- Open Interest: 17,000

- Size: 15,000 contracts

- Spot Price: $42.65

- Option Price: $4.70

Option Symbol: LUV20260320C40 Stock Page: LUV Stock Analysis

🤓 What This Actually Means

Real talk: This is either a MASSIVE covered call income generation strategy or a ballsy naked short bet! 🎯

Translation for us regular folks: Selling 15,000 call options at the $40 strike means controlling 1.5 MILLION shares of exposure. At $4.70 per option, they just collected $7.1 million in premium upfront.

Two scenarios here:

Scenario 1 - The Income Generator (Covered Call): 💰

- They own 1.5M shares of LUV (worth $64M at current price)

- They're willing to sell at $40 (6% below current price)

- They pocket $7.1M in premium no matter what

- If LUV drops below $40 by March, they keep shares AND premium

- If LUV stays below $40, that's 11% return in 3 months just from premium!

Scenario 2 - The Short Bet (Naked Call Sell): 🐻

- They DON'T own the shares

- They're betting LUV won't break above $40 by March 20, 2026

- Unlimited risk if the stock explodes higher

- Maximum profit: $7.1M premium collected

The Z-Score of 9.08 (EXTREMELY UNUSUAL classification) tells us this is about 555x larger than average option activity for LUV - this definitely isn't your neighbor Bob's Robinhood account!

Given Southwest's massive transformation underway and the near-the-money strike, this looks like a sophisticated income generation play from someone who believes Southwest's rally has hit resistance.

📈 Technical Setup / Chart Check-Up

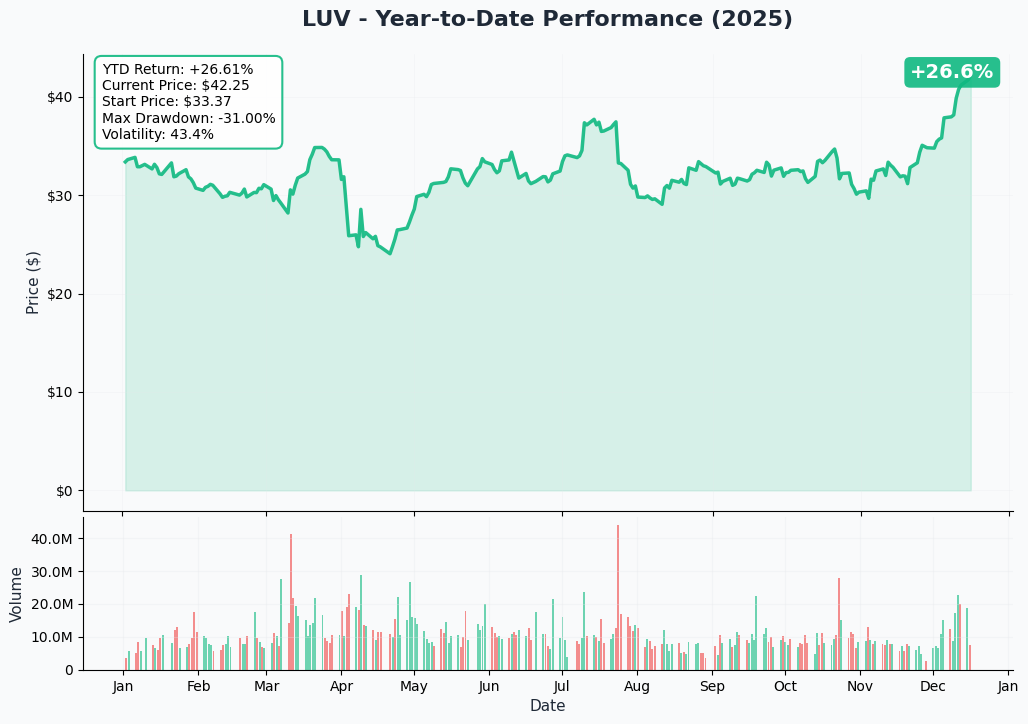

YTD Chart

Southwest has had an explosive year, surging from lows near $24 in early 2025 to the current $42.65 level - that's a 78% rally! The stock jumped significantly in late 2024 following the Elliott Management settlement announcement and transformation plan unveiling. The current price represents the 52-week high zone ($43.53), suggesting the stock may need to consolidate after this massive run.

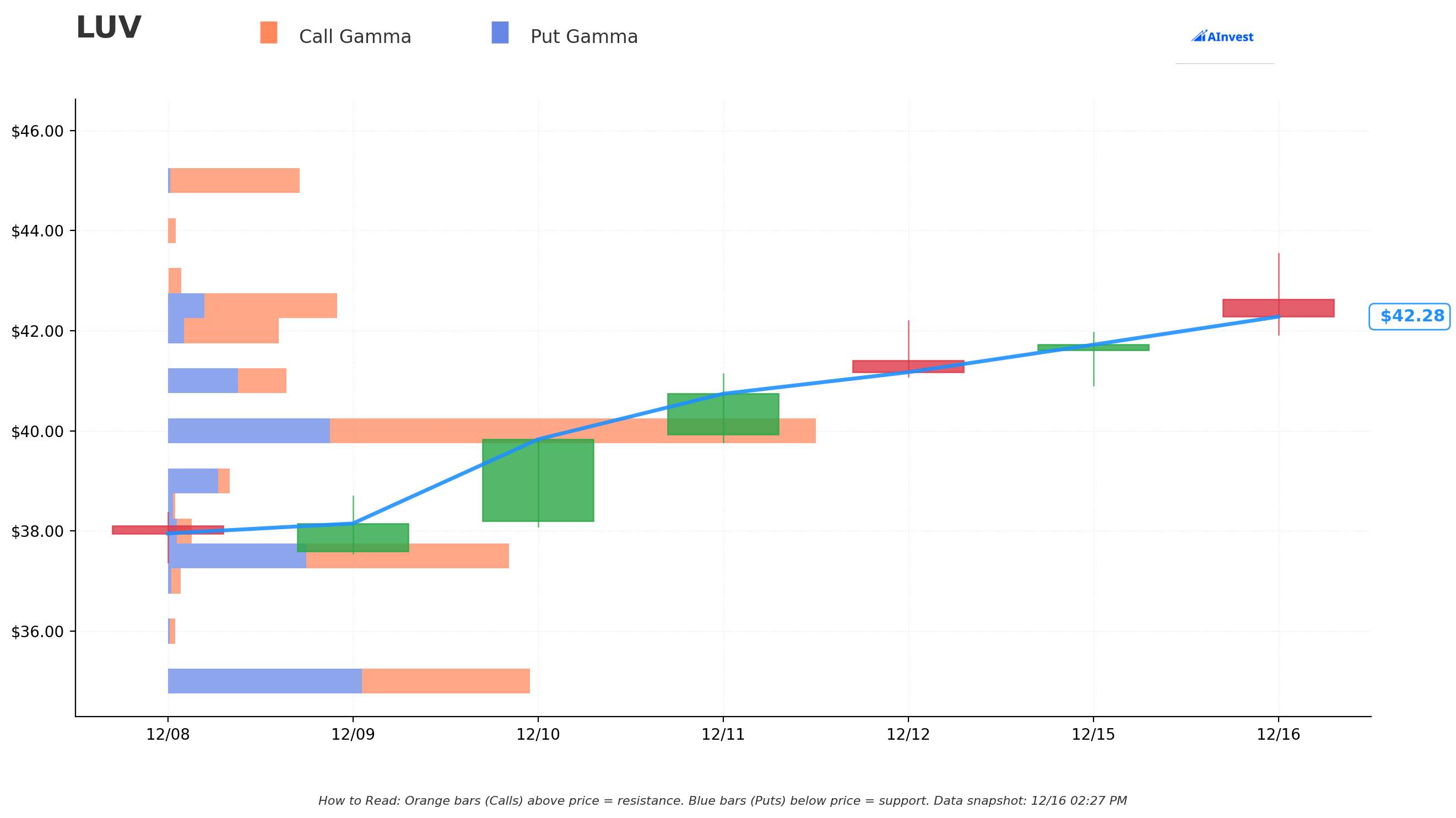

Gamma-Based Support & Resistance Analysis

Current Price: $42.65

The gamma exposure map reveals critical price levels where options activity creates natural support and resistance:

🔵 Support Levels (Put Gamma):

- $42.00 (0.7% below) - Immediate support with 1.92M total GEX, net bullish bias

- $41.00 (3.0% below) - Strong support zone with 2.03M total GEX

- $40.00 (5.4% below) - THE TARGET - massive 11.13M total GEX, the strike with the most activity

- $39.00 (7.7% below) - Secondary support with 1.05M GEX

- $37.50 (11.3% below) - Deep support with 5.81M GEX

- $35.00 (17.2% below) - Major floor with 6.18M GEX

🟠 Resistance Levels (Call Gamma):

- $42.50 (0.5% above) - Immediate resistance with 2.90M GEX

- $45.00 (6.4% above) - Major resistance wall with 2.27M GEX

- $47.50 (12.4% above) - Extended resistance with 1.10M GEX

- $50.00 (18.3% above) - Psychological barrier with 0.80M GEX

Key Insight: The $40 strike has by far the most gamma exposure (11.13M total GEX), suggesting this is where options traders expect the stock to gravitate. With net GEX bias of +5.58M (bullish), market makers are positioned for upside hedging, but the massive call selling at this strike creates a natural ceiling effect.

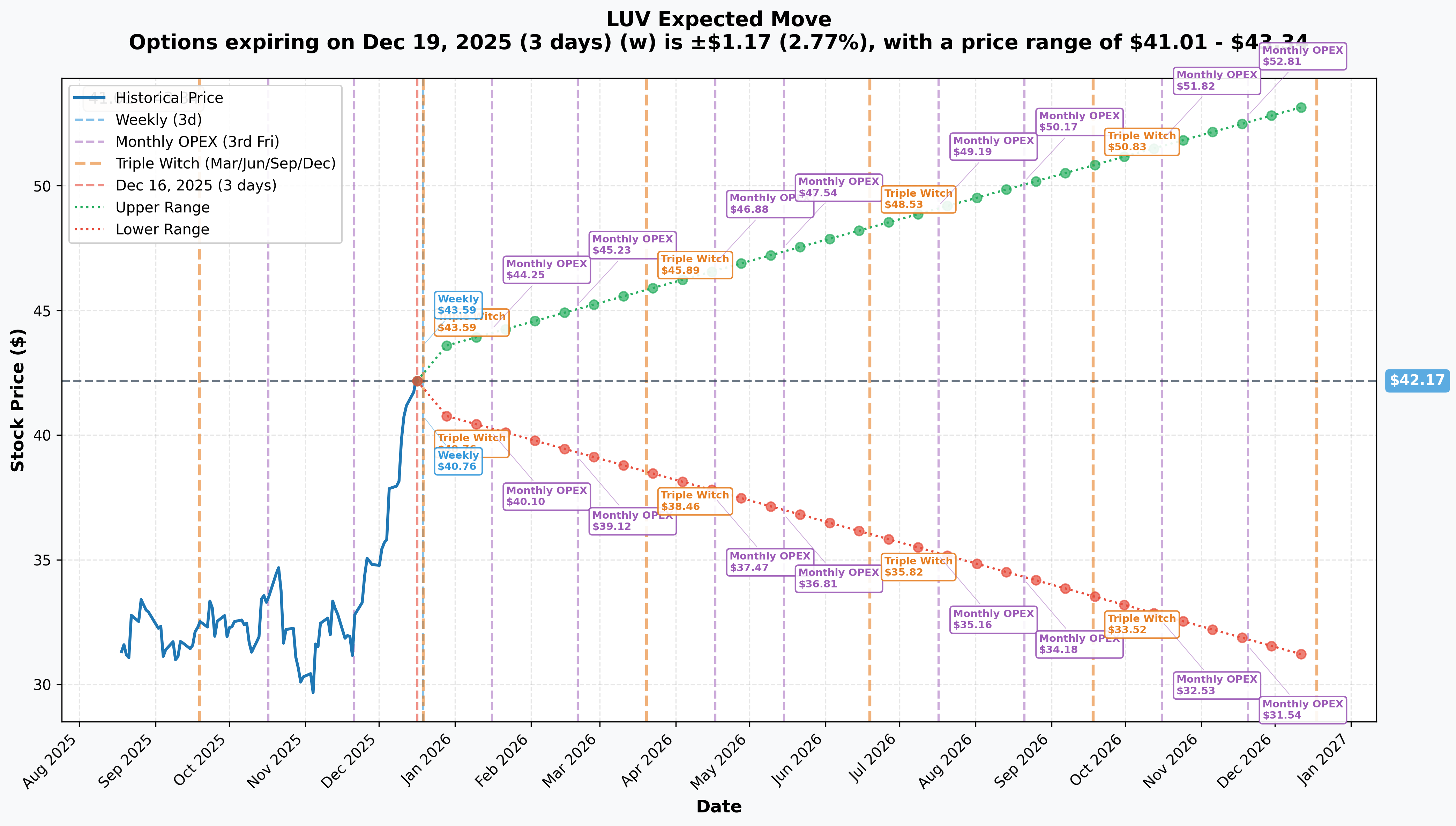

Implied Move Analysis

Weekly Options (December 19, 2025 expiration):

- Implied Move: 2.77% ($1.17)

- Range: $41.01 - $43.34

- Interpretation: Market expects relatively quiet week-end price action

Our Trade Expiration (March 20, 2026):

- Implied Move: ~7.4% based on quarterly timeframe

- Estimated Range: $39.50 - $45.90

- Key Point: The $40 strike sits right at the lower end of the expected range, suggesting the call seller is betting on mean reversion or consolidation after the big rally

LEAPS Context (December 2026):

- Implied Move: 26.45% ($11.16)

- Range: $31.02 - $53.33

- Long-term uncertainty: Southwest's transformation creates significant range expectations over 12+ months

🎪 Catalysts

📅 Upcoming Catalysts

Major Operational Implementation - May 28, 2025

The biggest near-term catalyst is Southwest's "Bags Fly Free" policy termination on May 28, 2025. After 54 years, Southwest will charge $35 for first checked bag and $45 for second bag. This represents a massive revenue opportunity - industry estimates suggest $300-500M in annual incremental revenue.

New fare bundle structure launches the same day with four tiers: Basic, Choice, Choice Preferred, and Choice Extra. This fundamentally changes Southwest's business model and could be a major profit inflection point.

Q2 2025 Earnings - July 24, 2025 (estimated)

Critical test of the transformation thesis. Q1 2025 results (reported April 24) showed the company did NOT reaffirm full-year 2025-2026 EBIT guidance - a major red flag. Q2 guidance projected unit revenue flat to down 4% YoY with weak domestic bookings cited. This earnings report will be crucial for validating whether the transformation is gaining traction.

Assigned Seating Booking Opens - July 29, 2025

Customers can begin selecting seats for flights departing January 27, 2026. This is the first major test of customer acceptance. Southwest's research showed 80% of current passengers and 86% of prospective travelers favor assigned seating, but execution risk remains high given the complexity of the IT systems integration.

Boeing 737 MAX 7 Certification - August 2026 (expected)

Southwest holds nearly 90% of all MAX 7 orders globally (342 aircraft). FAA certification expected August 2026 after years of delays (originally expected 2022). First Southwest flights with MAX 7 won't occur until 2027. These more fuel-efficient aircraft are critical to Southwest's cost reduction and capacity growth plans.

📊 Past Events (Already Happened)

Q4 2024 Earnings Beat (January 30, 2025)

Southwest reported record Q4 revenue of $6.93B with EPS of $0.56 vs $0.46 consensus (22% beat). Full year 2024 revenue hit record $27.5B. The company showed strong execution with RASM up 8.0% YoY in Q4. This strong performance validated early transformation progress.

Elliott Management Settlement (October 24, 2024)

Southwest reached settlement with Elliott Investment Management, which held 11% economic interest (~$1.9B stake). The settlement included six new Elliott-backed directors and a $2.5B share buyback authorization. Executive Chairman Gary Kelly departed November 1, 2024, while CEO Bob Jordan retained his position. This brought fresh oversight and capital discipline.

Technology Infrastructure Upgrades Completed (2024)

Following the catastrophic December 2022 meltdown, Southwest invested $1.3B in maintenance and technology upgrades. The company hired IBM to overhaul IT systems and invested over $112M in real-time crew management tools. Results showed - Southwest ranks third among top U.S. carriers in on-time arrivals in 2025, with completion factors exceeding 99% leading into Thanksgiving.

$750M Accelerated Share Repurchase (January 2025)

Southwest launched its second major buyback tranche of the $2.5B authorization. Combined with the initial $250M ASR completed in October 2024, the company has executed $1B of buybacks with $1.5B remaining. Total 2024 shareholder returns reached $680M through dividends and buybacks.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move dynamics, and catalyst timeline through March 2026 expiration:

🚀 Bull Case (30% chance)

Target: $45-48

- Baggage fees implementation (May 28) exceeds revenue expectations

- Q2 earnings (July 24) show strong pricing power and demand resilience

- Assigned seating rollout generates positive customer response

- Fuel prices remain stable, supporting margin expansion

- Boeing MAX deliveries accelerate (47 MAX 8s expected in 2025)

- Major resistance at $45 (6.4M GEX) and $47.50 (12.4M above current)

- Risk to call seller: Stock assignment above $40, giving up upside above $44.70 breakeven

😐 Base Case (50% chance)

Target: $39-43 range consolidation

- Stock consolidates after 78% YTD rally

- Transformation progress steady but not spectacular

- May baggage fee launch meets expectations but no major surprise

- Q1 weak guidance concern persists but Q2 shows sequential improvement

- $40 strike becomes natural pivot (highest gamma concentration at 11.13M GEX)

- Stock oscillates between $42 support and $42.50 resistance

- Call seller wins: Keeps $7.1M premium, stock not called away

😰 Bear Case (20% chance)

Target: $35-39

- Customer backlash to baggage fees damages brand loyalty

- Q2 earnings disappoint with unit revenue down 4% (worst case guidance)

- Broader economic weakness hits leisure travel demand

- Fuel prices spike without hedging protection (Southwest ending hedging program)

- Execution issues on assigned seating implementation create negative headlines

- Strong support at $40 (11.13M GEX) and $37.50 (11.3% below)

- Call seller crushes it: Keeps stock and $7.1M premium as options expire worthless

💡 Trading Ideas

🛡️ Conservative

"Premium Collection Light" Strategy

- Sell LUV Feb-26 $43 covered calls if you own the stock (1-month duration)

- Premium: ~$1.50-2.00 per contract

- Rationale: Collect income on near-term resistance level while stock consolidates

- Risk: Low - stock already above breakeven, premium reduces cost basis

- Why this works: Shorter timeframe reduces assignment risk while capturing theta decay

⚖️ Balanced

"Bull Put Spread at Support" Approach

- Buy LUV Mar-26 $38 puts / Sell LUV Mar-26 $40 puts (same expiration as the whale trade)

- Max Profit: Premium collected (~$0.80-1.00 per spread)

- Max Risk: $2 width minus premium (net ~$1.00-1.20)

- Breakeven: ~$39.00

- Why this works: Aligns with institutional expectation that $40 holds, defined risk, targets strong gamma support zone

- Key levels: Major gamma support at $40 (11.13M GEX) and $37.50 (5.81M GEX)

🚀 Aggressive

"Fade the Rally" Naked Call Sell ⚠️

- Sell LUV Jan-26 $45 calls (shorter duration than the whale)

- Premium: ~$1.50-2.00 per contract

- Max Profit: Premium collected

- Risk: UNLIMITED if stock explodes higher (uncapped losses above $45)

- Breakeven: $46.50-47.00

- Why this works: Bets on consolidation after 78% YTD run, major resistance at $45 (6.4% above current), shorter timeframe reduces risk window vs March expiration

- WARNING: Only for experienced traders with proper risk management and margin capacity!

⚠️ Risk Factors

What could absolutely wreck this income generation thesis:

🚨 Transformation Exceeds Expectations: Baggage fees and assigned seating drive revenue far above estimates, stock breaks $45+ resistance

🚨 Fuel Collapse: Oil prices crash, giving Southwest massive cost advantage just as they're ending fuel hedging program

🚨 Takeover Speculation: At $42 valuation with $21.6B market cap and strong balance sheet, Southwest could attract acquisition interest from larger carriers

🚨 Economic Boom: Consumer spending surges unexpectedly, leisure travel demand explodes, pricing power accelerates beyond forecasts

🚨 Competitor Failures: If Spirit or Frontier face serious troubles, Southwest gains significant market share in leisure segment

🚨 Boeing Surprise: MAX 7 certification accelerates ahead of August 2026 timeline, unlocking fleet modernization earlier

Remember: This $7.1M trade only makes sense if Southwest stays relatively range-bound or drifts lower toward $40 over the next 3 months. The seller is banking on consolidation after the massive rally, not a continuation higher! 📉

🎯 The Bottom Line

Here's the deal: Someone just collected $7.1 million in premium by selling calls on 1.5 million shares worth of Southwest Airlines exposure. That's either a massive income generation play from a long-term holder willing to cap upside at $40, or a sophisticated short thesis betting the 78% rally has exhausted itself.

Action Plan:

- 💰 If you own LUV stock: Consider covered calls at $43-45 strikes for near-term income while the transformation plays out

- 👀 If you're watching: Monitor the $40 support level (highest gamma concentration) and May 28 baggage fee implementation for direction

- 🐻 If you're bearish: Put spreads at $40/$38 offer defined risk exposure to a pullback, aligning with the institutional flow

- 🚀 If you're bullish: Be cautious - the $45 resistance level (major call gamma wall) and weak Q2 guidance suggest limited near-term upside

Mark your calendar: This trade has until March 20, 2026 to resolve - giving time for two earnings reports (Q1 already disappointed, Q2 July 24 crucial) and the critical May 28 baggage fee launch.

Key dates to watch:

- May 28, 2025: Baggage fees implementation (potential $300-500M annual revenue)

- July 24, 2025: Q2 earnings (must show improvement from weak Q1 guidance)

- July 29, 2025: Assigned seating booking opens (customer acceptance test)

Final thought: When someone sells $7.1M worth of calls at a strike 6% below current price after a 78% rally, they're signaling either strong conviction in range-bound consolidation or outright bearishness. The transformation story is compelling, but execution risk is real. Southwest is abandoning its 53-year brand identity (free bags, open seating) - that's either genius or disaster, and we'll know which by March 2026.

Trade smart, manage your position size, and remember that even covered calls have opportunity cost if the stock rips higher! 💪

⚠️ Disclaimer: Options trading involves significant risk and is not suitable for all investors. Past performance does not guarantee future results. This analysis is for educational purposes only and not financial advice. Always consult with a qualified financial advisor before making investment decisions.