✈️ LUV $4.7M Call Bet - Big Money Bets on Southwest's Turnaround! 🚀

📅 February 12, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $4.7 MILLION on Southwest Airlines calls expiring in June! This is a massive bullish bet on the airline that just ditched its 53-year-old open seating model and is guiding for 330% earnings growth in 2026. With Elliott Investment Management stepping back and the stock up 31% over 12 months, a sophisticated trader is betting this transformation story is just getting started.

📊 Company Overview

Southwest Airlines Co. (LUV) is the largest domestic air carrier in the United States by passengers boarded, operating an all-Boeing 737 fleet of nearly 800 aircraft.

- Market Cap: $25.3B

- Industry: Air Transportation, Scheduled

- Current Price: $54.07 (near 52-week highs)

- Employees: 77,397

- Headquarters: Dallas, Texas

Southwest is in the midst of a historic business model transformation - introducing assigned seating, checked bag fees, and premium fare tiers for the first time in company history. Management is guiding for adjusted EPS of at least $4.00 in 2026 versus $0.93 in 2025 - a 330% increase.

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Option Symbol | Buy/Sell | Type | Expiration | Strike | Volume | Premium | Order Type | Confidence | Vol/OI | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:28:48 | LUV20260618C55 | BUY | CALL | 2026-06-18 | $55 | 15,000 | $4.7M | BTO | LOW | 1.74x | Single Leg CALL |

🤓 What This Actually Means

This is a straight-up bullish bet on Southwest Airlines! Here's the breakdown:

- 💸 Massive premium deployed: $4.7M for 15,000 call contracts

- 🎯 Strike price: $55 (just above current price of $54.07)

- ⏰ Time frame: June 18, 2026 expiration (126 days out)

- 📊 Volume signal: HIGH_ACTIVITY with 1.74x volume to open interest ratio

- 🎰 Strategy: Standalone single leg call - pure directional bullish play

Translation for regular folks:

This trader is betting Southwest will be trading above $55 by mid-June 2026. Given they paid approximately $313 per contract ($4.7M / 15,000), they need LUV above roughly $58.13 at expiration to profit. That's about a 7.5% move higher from current levels.

Why is this interesting?

This isn't your neighbor Bob's Robinhood account! A $4.7M single-ticket options bet on an airline is serious institutional money making a conviction call. The timing is fascinating - coming just two days after Elliott Investment Management announced it's reducing its stake and pulling board members. Someone sees the turnaround working even without the activist pressure.

📈 Technical Setup / Chart Check-Up

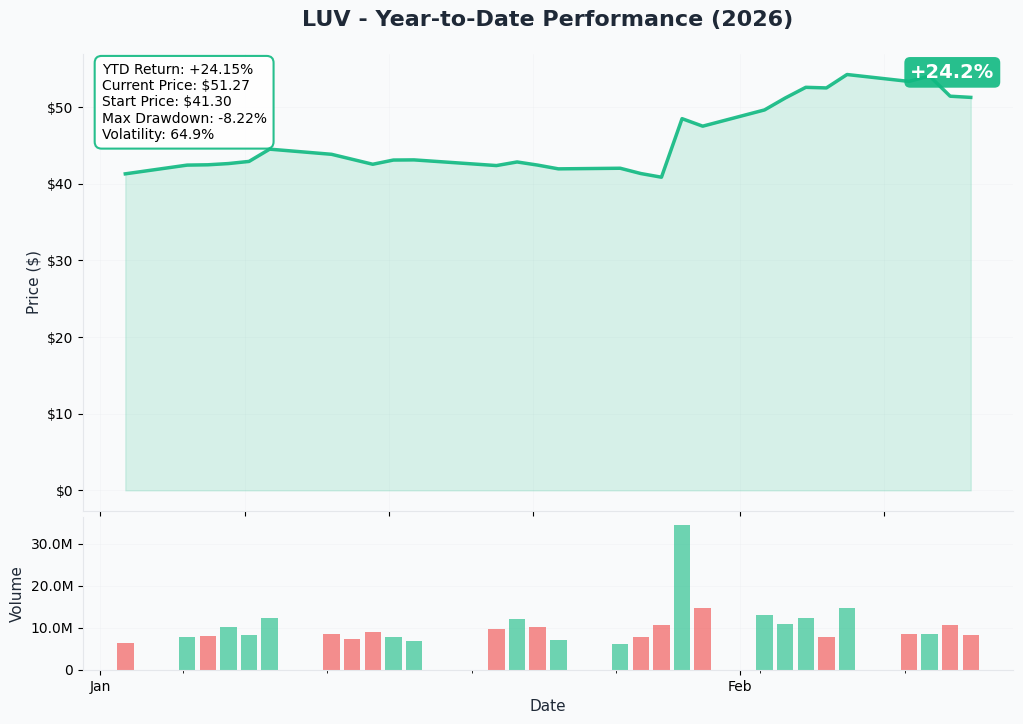

YTD Performance Chart

Southwest has been on a tear! The stock is up 31% over the trailing 12 months and has gained 20% in just the last 30 days following blowout Q4 2025 results. The January 28 earnings report sparked a 17.3% after-hours surge as investors reacted to the aggressive 2026 guidance.

Key observations:

- 📈 Strong momentum: Stock breaking out to multi-month highs

- 💹 Post-earnings breakout: 17.3% after-hours surge on January 28

- 🎢 Volatility: Significant moves on transformation news

- 📊 Volume confirmation: 3.34M shares daily volume with sustained buyer interest

Note: Gamma-based support/resistance and implied move charts are not available for this analysis.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened)

Q4 2025 Earnings Blowout (January 28, 2026):

- 📊 Revenue: $7.4B quarterly record

- 💰 Adjusted EPS: $0.58-$0.61, beating consensus estimates

- 📈 Stock surged 17.3% after-hours on results

Business Model Revolution:

- 🎫 Assigned seating launched February 2026 - ending 54 years of open seating

- 💼 First-ever checked bag fees implemented - early results exceeding expectations

- ✂️ 15% corporate workforce reduction - $300M savings target in 2026

Elliott Investment Exit (February 2026):

- 🚪 Two Elliott-appointed directors stepping down February 23

- 📉 Elliott reduced stake from 16% to ~9%

- ✅ Signals confidence in management execution

🚀 Upcoming Catalysts

Q1 2026 Earnings (April 23-24, 2026):

- 🎯 Guided EPS: At least $0.45 (vs loss of $0.13 in Q1 2025)

- 📊 Guided RASM growth: At least 9.5% YoY

- 📈 First full quarter with new revenue initiatives active

- 💡 This is THE catalyst - will validate or destroy the turnaround thesis

Boeing 737 MAX 7 Certification (August 2026 Target):

- ✈️ CEO expects FAA certification by August 2026

- 📦 342 MAX 7 units on order to replace aging 737-700 fleet

- ⚠️ First deliveries not expected until 2027

Summer 2026 Network Expansion:

- 🌴 New routes to St. Thomas, St. Maarten, Mexico destinations

- 🗺️ Focus on high-demand leisure markets

🎲 Price Targets & Probabilities

Based on the option flow, analyst targets, and catalyst timeline:

📈 Bull Case (35% probability)

Target: $60-$65 by June 2026

How we get there:

- 💪 Q1 2026 earnings crush guidance (EPS significantly above $0.45)

- 🎫 Assigned seating revenue exceeds $1B incremental EBIT projections

- 💼 Bag fee revenue materially beats expectations

- ✈️ Boeing MAX 7 certification timeline advances

- 📈 Analysts upgrade en masse as transformation proves out

Why the trader wins big: At $62, the $55 calls would be worth roughly $7+ intrinsic alone, turning the $4.7M bet into $10M+ (100%+ return).

🎯 Base Case (45% probability)

Target: $52-$58 range through June 2026

Most likely scenario:

- ✅ Q1 earnings meet guidance (confirms transformation on track)

- 📊 Revenue initiatives show progress but no blowout surprises

- 🔄 Stock consolidates around current levels as market digests changes

- ⚖️ Some execution hiccups offset by strong leisure demand

Trader outcome: Modest gain or loss depending on final price. Needs above $58.13 to profit.

📉 Bear Case (20% probability)

Target: $42-$48

What could go wrong:

- 😰 Q1 earnings disappoint - new initiatives underwhelm

- 🎫 Customer backlash to bag fees and assigned seating hurts bookings

- ⛽ Fuel prices spike (no hedging in place)

- ✈️ Boeing delays worsen, constraining growth

- 📉 Broader recession hits leisure travel demand

Trader outcome: Total loss of $4.7M premium.

💡 Trading Ideas

🛡️ Conservative: Wait for Q1 Confirmation

Play: Stay on sidelines until Q1 2026 earnings (April 23-24)

Why this works:

- ⏰ Transformation thesis untested at scale - Q1 is the proof point

- 📊 Stock already up 31% over 12 months - a lot of good news priced in

- 🎯 Better entry likely if results disappoint (pullback to $48-$50)

- ✅ If Q1 crushes, plenty of time to enter for summer catalysts

Action plan:

- 👀 Watch April 23-24 earnings closely for RASM and new revenue metrics

- 🎯 Look for pullback to $48-$50 for stock entry (10% below current)

- ✅ Confirm transformation working before committing capital

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Covered Call on Stock Position

Play: Buy 100 shares LUV + Sell June $60 call

Structure:

- Buy 100 shares @ $54.07 = $5,407

- Sell 1 LUV20260618C60 for premium income

Why this works:

- 📊 Participate in upside to $60 (11% gain)

- 💰 Collect call premium to reduce cost basis

- 🛡️ Downside buffered by premium received

- 🎯 Aligned with base case scenario

Risk management:

- 📉 Max loss if LUV goes to zero (unlikely for major airline)

- ⚠️ Caps upside at $60 strike if turnaround exceeds expectations

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Follow the Whale with Call Spread

Play: Buy June $55/$65 call spread

Structure:

- Buy LUV20260618C55 (same as the whale trade)

- Sell LUV20260618C65 to reduce cost

Why this could work:

- 💸 Significantly cheaper than $4.7M whale position

- 📊 Defined risk with capped upside at $65

- 🎯 Profits if transformation thesis plays out

- 📈 Aligned with bull case target range

Estimated P&L:

- 💰 Cost: ~$200-300 per spread (10 contracts = $2,000-3,000)

- 📈 Max profit: $1,000 per spread if LUV at/above $65 at expiration

- 📉 Max loss: Premium paid (defined and limited)

Risk level: High (could lose entire premium) | Skill level: Intermediate-Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎫 Execution risk on transformation: Southwest is abandoning the differentiated model that built customer loyalty over 54 years. If assigned seating causes operational issues or bag fees alienate loyal customers, the $4.00 EPS guidance could prove wildly optimistic.

-

⛽ Fuel price exposure: Southwest discontinued its fuel hedging program, leaving the company fully exposed to oil price volatility. A spike in jet fuel could devastate margins.

-

✈️ Boeing dependency: Southwest expects 100+ fewer aircraft deliveries than contracted in 2026. MAX 7 certification delays could push fleet modernization into 2028+, constraining growth and increasing maintenance costs.

-

📉 Leisure travel sensitivity: Southwest targets leisure travelers who cut back first in economic downturns. Company previously withdrew guidance amid macroeconomic uncertainty.

-

🎯 Valuation stretched: Stock up 31% over 12 months and 20% in 30 days. Much of the transformation upside may already be priced in. Analyst consensus target of $44.97 suggests limited upside from current $54.07 price.

-

🏛️ Labor costs locked in: All major union contracts settled through 2027-2028 with significant pay raises. New revenue must offset these elevated costs.

-

🤔 LOW confidence signal: The options data shows LOW confidence on this trade, suggesting it may not be a clean institutional signal. Could be portfolio hedging or speculative positioning.

🎯 The Bottom Line

Real talk: A sophisticated trader just bet $4.7 million that Southwest's historic business transformation will drive the stock higher by June. This is a pure conviction play on the turnaround thesis - assigned seating, bag fees, and premium fares turning a 330% EPS growth story from guidance into reality.

What this trade tells us:

- 🎯 Trader expects LUV above $58+ by June 2026 to profit

- 💰 Willing to risk $4.7M on transformation succeeding

- ⏰ Timing aligns with Q1 earnings (April) as validation catalyst

- 📊 Betting Elliott's exit signals "mission accomplished" not "abandon ship"

If you own LUV:

- ✅ Enjoy the ride - you're holding a potential turnaround winner

- 📊 Watch Q1 earnings (April 23-24) for validation of new revenue streams

- 🎯 Consider taking partial profits if stock hits $60+ (11% upside)

- 🛡️ Set mental stop at $48 to protect gains if transformation stumbles

If you're watching from sidelines:

- ⏰ April 23-24 is the moment of truth - first full quarter with new initiatives

- 🎯 Pullback to $48-$50 would be attractive entry point

- 📊 Looking for confirmation of RASM growth exceeding 9.5% guidance

- ✅ Wait for data before following the whale

If you're bearish:

- 🎯 Wait for Q1 disappointment before shorting - momentum is strong

- 📊 First meaningful support around $48-$50 (prior resistance now support)

- ⚠️ Customer backlash to new fees and fuel spikes are your catalysts

- ⏰ Timing is critical - don't fight the tape at 52-week highs

Mark your calendar - Key dates:

- 📅 February 23, 2026 - Elliott board members officially depart

- 📅 April 23-24, 2026 - Q1 2026 earnings report (THE catalyst!)

- 📅 June 18, 2026 - This $4.7M call position expires

- 📅 August 2026 - Target for Boeing MAX 7 certification

Final verdict: This is a high-conviction bet on Southwest's transformation from the airline your parents loved (free bags, no assigned seats) into a more profitable, competitive carrier. The $4.00 EPS guidance (330% growth) is aggressive but not impossible if the new revenue initiatives execute. Q1 earnings in April will either validate this thesis or expose it as overly optimistic. The smart play is to watch, wait for data, and look for better entry points rather than chasing a stock that's already up 31%.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Airlines are inherently cyclical and volatile. Always do your own research and consider consulting a licensed financial advisor before trading.

About Southwest Airlines: Southwest is the largest domestic air carrier in the United States with a $25.3B market cap, operating nearly 800 Boeing 737 aircraft and serving over 100 destinations across the Americas.