🐋 MBLY: $1.4M Call Bet on Mobileye Near All-Time Lows -- Someone Sees a Double From Here!

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.4 million on 10,000 Mobileye August $8 calls -- buying right at the ask, at-the-money, with a z-score of 53.8 (about 54 standard deviations above average trade size). With volume 36x the existing open interest, this is a brand new position opening on a stock trading near its all-time low. With analysts seeing 97%+ upside to $15-$17, this trader is betting Mobileye's "transition year" narrative flips bullish well before August.

🏢 Company Snapshot

Mobileye Global Inc. (NASDAQ: MBLY) -- The company behind the eyes of self-driving cars:

- 🚗 What they do: Develops and deploys Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies -- the cameras, chips, and software that let cars see the road

- 💰 Market Cap: $6.83B

- 🏢 Sector: Prepackaged Software / Autonomous Driving / ADAS

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$8.01

- 👥 Employees: 4,200

- 🔑 Key Story: Near all-time lows despite massive new OEM wins (19M+ EyeQ6H systems), a Mahindra partnership for 6+ models, a $900M Mentee Robotics acquisition expanding into Physical AI, and Volkswagen robotaxi deployments planned for 2026. Analysts see 97%+ upside -- the market just hasn't caught on yet.

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:46:16 | MBLY | ASK | BUY | CALL $8 | 2026-08-21 | $1.4M | $8 | 10,000 | 275 | 10,000 | $8.01 | $1.35 | MBLY20260821C8 |

🤓 What This Actually Means

Let me break this down in plain English.

Someone walked up to the options market at 10:46 AM and bought 10,000 call contracts on Mobileye in a single clip. At $1.35 per contract (times 100 shares each), that is a $1.4M bet that MBLY trades above $9.35 by August 21.

A few things make this trade absolutely stand out:

✅ Z-Score of 53.8 -- This trade is roughly 54 standard deviations above the average trade size for MBLY options. You might see a trade this outsized a handful of times per year across the entire options market. This is serious institutional money moving.

✅ Volume/OI ratio of 36.4x -- There were only 275 contracts of open interest before this trade. The buyer just added 10,000 contracts on top of that. This is not rolling, not hedging, not closing -- this is a brand new position being opened from scratch.

✅ Bought at the ASK -- The buyer lifted the offer, meaning they were willing to pay up to get filled immediately. No patience, no negotiating at mid. They wanted IN and wanted it NOW.

✅ ATM strike -- The $8 strike with the stock at $8.01 is essentially at-the-money. This gives the trade maximum delta exposure (about 0.55-0.60 delta), meaning the position moves roughly dollar-for-dollar with the stock from here. This is a pure directional conviction bet, not a lottery ticket on some far OTM strike.

✅ 5.5 months to expiration (August 21, 2026) -- Plenty of runway to capture Q1 earnings (April 23), the Loop Capital conference (March 10), Mentee Robotics acquisition closing, and EyeQ6H ramp updates.

✅ Notional exposure -- At 10,000 contracts x 100 shares x $8.01, this trade controls about $8M in MBLY stock. The buyer chose to risk $1.4M to control $8M of upside -- roughly 5.7x leverage.

What's the thesis here?

This trader is betting that Mobileye at ~$8 is a gift. With a consensus analyst target of $16-$17 (roughly 100% upside), the stock sitting near its all-time low, and a loaded catalyst calendar over the next 5 months, this trade is a bet that the market eventually wakes up to the disconnect between where MBLY trades and where the business is heading. At $1.35 per share of premium, the breakeven is just $9.35 -- only a 16.7% move from current levels. If MBLY simply gets back to $15 (the low end of analyst targets), these calls would be worth $7 each, turning $1.4M into roughly $7M -- a 5x return.

📈 Technical Setup / Chart Check-Up

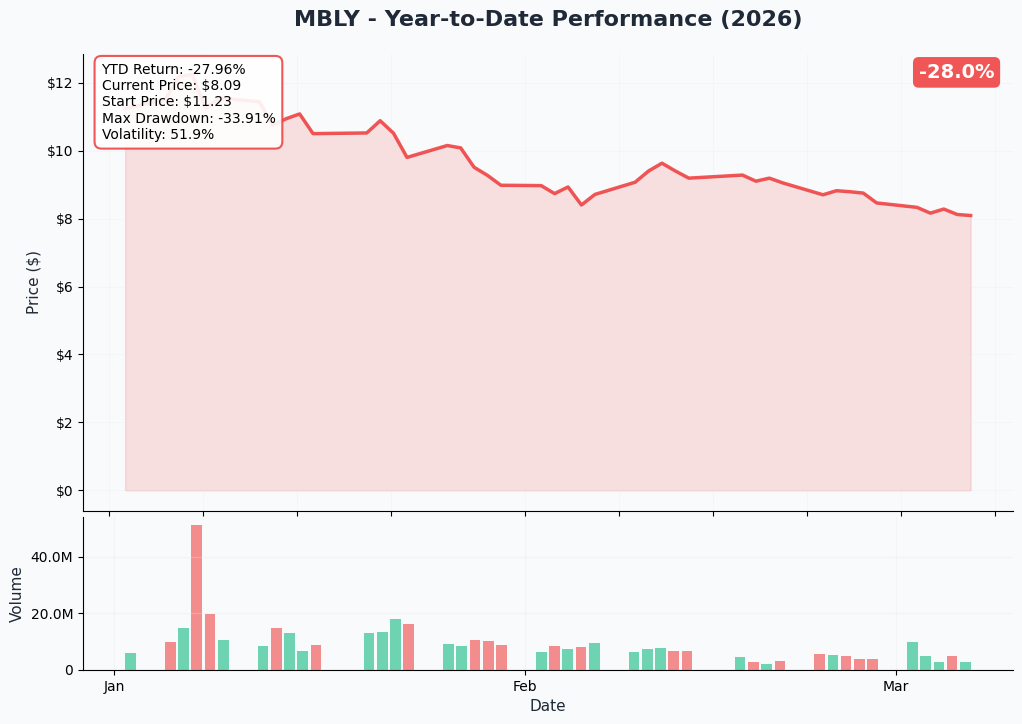

YTD Performance

MBLY has been in a brutal downtrend, trading near its all-time low:

- 📉 Near all-time low: Stock hit $8.32 on February 5, 2026 -- current levels around $8 are essentially at the floor

- 📊 Market cap ~$6.8B -- down massively from the $50+ IPO euphoria in late 2022

- 💀 Sentiment washed out: Everyone who wanted to sell has likely already sold. The easy money on the short side is gone.

- 📈 Revenue growing: Despite the stock action, the company posted 15% YoY revenue growth in 2025 and 51% growth in operating cash flow

- 🔄 Potential bottoming pattern: The stock has been consolidating in the $8-$10 range -- a base for a reversal if catalysts deliver

Key takeaway: MBLY is a "fallen angel" trading at the bottom of its range. The business fundamentals (revenue growth, OEM wins, cash generation) are far better than the stock price suggests. This is exactly the kind of setup where a catalyst can spark a sharp re-rating higher.

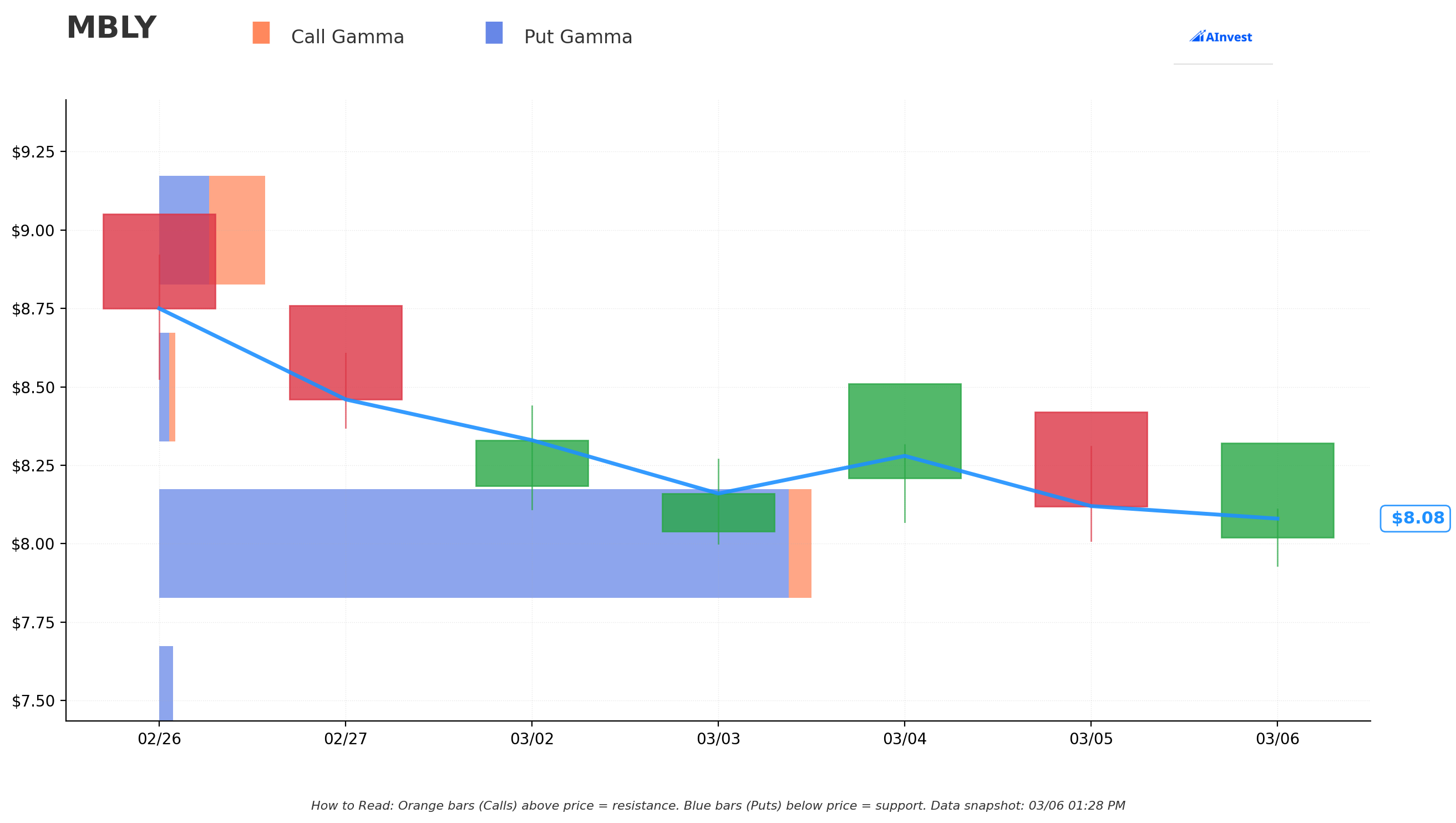

🔵🟠 Gamma-Based Support & Resistance

How to read this chart: The blue bars (put gamma) below the current price act as support floors -- heavy options activity that tends to slow down declines. The orange bars (call gamma) above the current price act as resistance ceilings -- strikes where hedging activity can cap rallies. Bigger bars mean stronger levels.

Current Price: $8.09

🔵 Support Levels (Put Gamma Below Price):

- $8.00 -- Strongest support with 16.5 total gamma exposure (just 1.1% below current price). This is the LINE IN THE SAND -- heavy put gamma at the round $8 level creates a natural floor. The whale's $8 strike sits right here.

- $7.50 -- Secondary support (7.2% below) with modest gamma

- $7.00 -- Deep support (13.4% below) -- if MBLY breaks here, the thesis is in real trouble

🟠 Resistance Levels (Call Gamma Above Price):

- $8.50 -- First resistance (5.1% above) with 0.41 total gamma. Relatively thin, meaning the stock can push through without much friction.

- $9.00 -- Significant resistance with 2.68 total gamma (11.3% above). This is the first real hurdle -- clearing $9 would be a major technical breakout signal.

- $9.50 -- Extended resistance (17.5% above) with lighter gamma

What this means for traders:

The gamma map tells a clear story: MBLY has a strong floor at $8 and relatively thin resistance above it. The path of least resistance is actually higher. The $8 put gamma wall acts as a support cushion, while the call gamma above is spread thin -- there is no massive overhead barrier until $9. If any catalyst drives buying, the stock could move quickly through the $8.50 and $9 levels before encountering meaningful resistance.

Net GEX Bias: Bearish (9.5 total call gamma vs 22.4 total put gamma) -- the put-heavy gamma means dealers are positioned for downside protection, which paradoxically creates a floor. If the stock starts rallying, dealers would need to buy shares to stay hedged, potentially accelerating the move up.

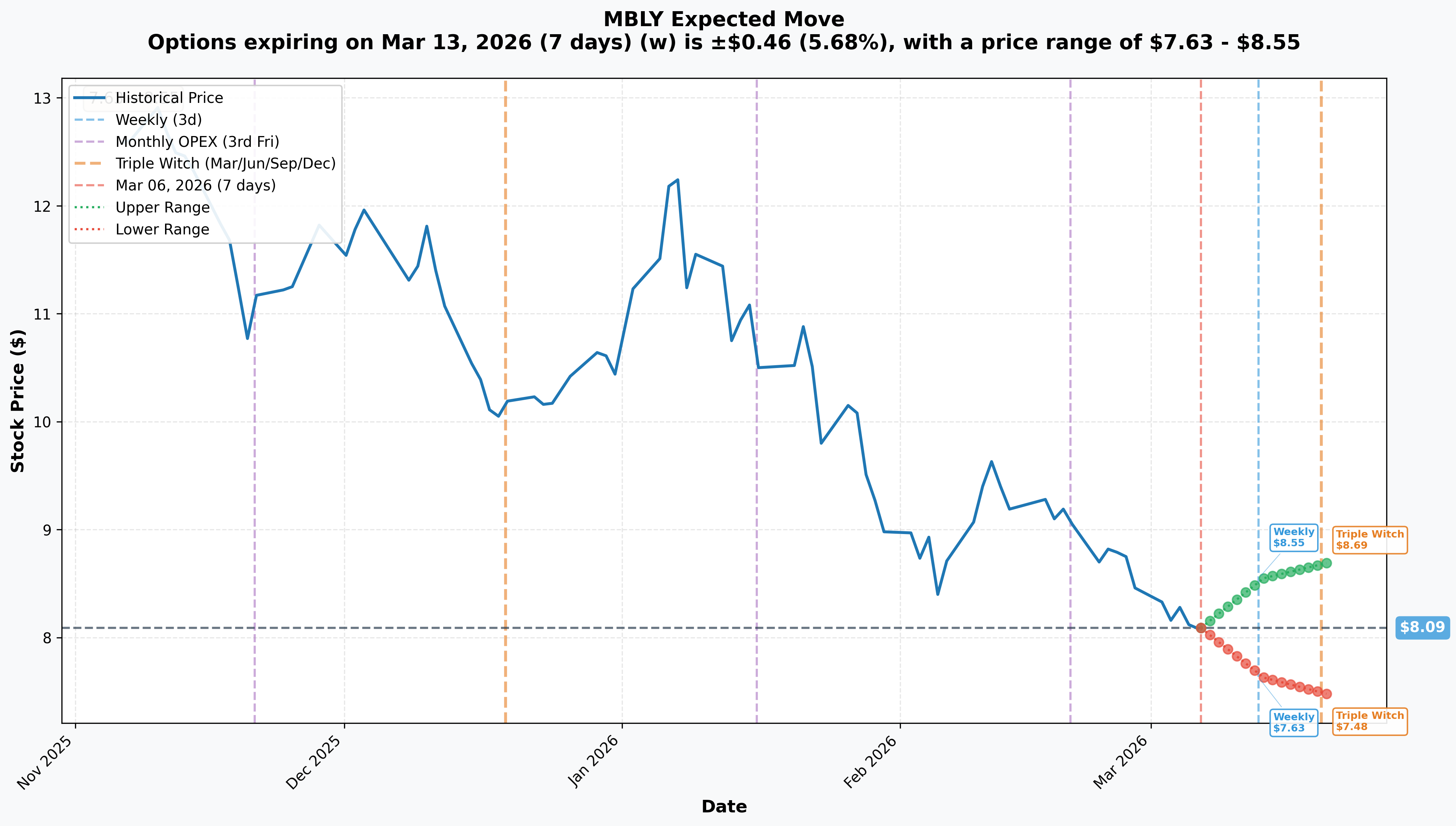

📐 Implied Move Analysis

The options market is pricing in the following expected ranges based on implied volatility:

| Timeframe | Expiration | Expected Range | Move % |

|---|---|---|---|

| 📅 Weekly | 2026-03-13 | $7.63 - $8.55 | +/- 5.7% |

| 📅 Monthly OPEX / Triple Witch | 2026-03-20 | $7.48 - $8.69 | +/- 7.5% |

Translation:

The weekly implied move of +/- 5.7% is elevated for a stock at this price -- the market expects volatility. The Triple Witch expiration on March 20 prices in a range of $7.48 to $8.69, which aligns well with the $7.50 support and $8.50 resistance from the gamma analysis.

For the August 21 expiration (the whale's trade), implied volatility is pricing in a much wider range. At ~55-60% annualized IV (typical for MBLY), the implied move over 5.5 months is roughly +/- 35-40%, putting the expected range at approximately $5.20 to $10.80. The trader's breakeven at $9.35 is well within the upper half of this distribution.

Key insight: The weekly 5.7% implied move reflects the upcoming Loop Capital conference on March 10. The broader August range validates this trader's thesis -- the market acknowledges that MBLY can move substantially in either direction. The whale is betting on the upside tail.

🎪 Catalysts

🔥 Upcoming Catalysts

Loop Capital Investor Conference -- March 10, 2026 📊

Mobileye is presenting at this conference just 4 days from now. Management updates at investor conferences often provide fresh color on OEM pipeline progress, EyeQ6H ramp timelines, and demand trends. This could be a near-term sentiment catalyst.

Mentee Robotics Acquisition Closing -- Expected Q1 2026 🤖

The $900M acquisition of Mentee Robotics is expected to close this quarter. This expands Mobileye into Physical AI / humanoid robotics -- a red-hot sector. First proof-of-concept deployments with customers are expected in 2026, with commercial production targeted for 2028. If the market starts valuing MBLY as an AI + robotics play, the re-rating could be significant.

Q1 2026 Earnings -- April 23, 2026 📊

This is THE major checkpoint before the August expiration. Consensus expects ~19% YoY revenue growth in Q1. Key things to watch:

- 📊 EyeQ shipment volumes (targeting 37M+ for full year 2026)

- 🤖 SuperVision adoption updates with new OEM partners

- 🚕 VW robotaxi deployment timeline progress

- 💰 Any upward revision to the conservative "flat to 5% growth" full-year guidance

VW Robotaxi U.S. Deployments -- 2026 🚕

Volkswagen is planning to deploy Mobileye Drive-enabled ID.Buzz robotaxis on the Uber network in Los Angeles starting in 2026. Any concrete deployment timeline announcement would be a massive sentiment driver.

EyeQ6H Ramp with New U.S. Automaker 🚗

A major top-10 U.S. automaker selected EyeQ6H-powered Surround ADAS as standard equipment. Production timelines and initial shipment volumes will be critical updates over the coming months.

✅ Recent Catalysts (Already Happened)

Q4 2025 Results -- January 22, 2026 📊

Mobileye reported full-year 2025 revenue of $1,894M, up 15% YoY. EPS of $0.06 beat the $0.03 consensus estimate. Cash from operations surged 51% to $602M. However, the stock dropped ~6% on the "transition year" guidance of flat to 5% revenue growth for 2026. Management deliberately set a low bar.

Mahindra Partnership -- February 10, 2026 🇮🇳

Mahindra selected Mobileye's SuperVision and Surround ADAS for 6+ upcoming models, with production starting in 2027. This opens the massive Indian automotive market.

Major U.S. OEM Win -- January 2026 🇺🇸

A top-10 U.S. automaker selected EyeQ6H-powered Surround ADAS -- an estimated 9M vehicles from this single OEM, contributing to 19M+ EyeQ6H systems expected worldwide.

Mentee Robotics Acquisition Announced -- January 6, 2026 🤖

Mobileye agreed to acquire Mentee Robotics for $900M ($612M cash + 26.2M shares), expanding into humanoid robotics and Physical AI.

Investor Conference Circuit -- February-March 2026 🎤

Mobileye has been actively presenting at Wolfe Research (Feb 11), Morgan Stanley TMT (Mar 4), and Loop Capital (Mar 10) conferences -- a sign that management is proactively getting in front of investors at depressed levels.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, analyst targets, and the catalyst calendar through the August 21, 2026 expiration:

📈 Bull Case (30% probability)

Target: $13-$17

How we get there:

- 🚀 Q1 earnings on April 23 beat expectations with 19%+ revenue growth and raised full-year guidance

- 🤖 Mentee Robotics acquisition closes and first PoC deployments generate excitement around Physical AI narrative

- 🚕 VW announces concrete robotaxi deployment dates in Los Angeles on the Uber network

- 📊 Analysts upgrade from the current $16-$17 consensus target as confidence in execution builds

- 📈 Stock breaks through $9 gamma resistance and runs through thin overhead supply

- 🔄 Intel overhang eases as the market digests prior share sales

Call trade P&L at $15: Calls worth $7/share, profit = $5.65/share x 10,000 contracts = $5.65M gain (404% ROI) Call trade P&L at $17: Calls worth $9/share, profit = $7.65/share x 10,000 contracts = $7.65M gain (546% ROI)

This is the scenario where the "transition year" turns out to be the bottom, and the stock re-rates toward analyst consensus. The average target of $16.17 from 18 analysts represents nearly 100% upside, and Oppenheimer has a target as high as $28.

🎯 Base Case (45% probability)

Target: $9-$12

Most likely scenario:

- ✅ Q1 earnings come in roughly in line with expectations -- no fireworks, but no disaster

- 📊 Management reaffirms conservative 2026 guidance, maintaining the "transition year" stance

- 🔄 EyeQ6H ramp progresses on track but revenue recognition is back-half weighted

- 📈 Stock grinds higher from $8 through the $8.50 and $9 gamma levels over months

- ⚖️ Intel overhang remains a periodic headwind but is better understood by the market

Call trade P&L at $11: Calls worth $3/share, profit = $1.65/share x 10,000 contracts = $1.65M gain (118% ROI) Call trade P&L at $9.50: Calls worth $1.50/share, profit = $0.15/share x 10,000 contracts = $150K gain (11% ROI)

Even in the base case, this trade likely makes money. The $9.35 breakeven is only 16.7% above current levels, and with 5.5 months of runway and multiple catalysts ahead, a grind to $10-$11 is very achievable. The trader could also sell the calls before expiration if the stock hits $10-$11 and capture meaningful remaining time value.

📉 Bear Case (25% probability)

Target: $6-$8

What could go wrong:

- 😰 Q1 earnings disappoint -- OEM program delays push EyeQ6H ramp into 2027

- 📉 Intel sells another large block of shares, pressuring the stock with additional supply

- 🚗 Autonomous driving competition intensifies -- Tesla FSD, Waymo, and Chinese rivals capture OEM attention

- 💸 Mentee Robotics acquisition adds $100M+ in annual operating expenses with no near-term revenue

- 📊 Auto industry cyclical downturn reduces OEM spending on ADAS technology

- 📉 Break below $8 gamma support triggers a slide toward $7.50 and then $7.00

Call trade P&L: Calls expire worthless or near-worthless, loss = up to -$1.4M (-100%)

The $8 gamma support is the critical floor. A sustained break below would undermine both the technical setup and the whale's thesis. The trader's maximum loss is capped at the $1.4M premium paid.

💡 Trading Ideas

🛡️ Conservative: "The Cheap Seat" -- Bull Call Spread

Play: Buy the MBLY August $8 call / Sell the MBLY August $12 call

Why this works:

- 📊 Mirrors the whale's directional thesis but caps your cost significantly

- 🛡️ Defined risk: you can only lose the net debit paid (roughly $1.00-$1.20 per spread)

- 💰 Max profit: $4 per spread minus debit (~$2.80-$3.00 gain) if MBLY above $12 at expiry

- ⏰ Same August 21 expiration captures all the same catalysts

- 📈 The $8 strike is ATM -- you start profiting almost immediately on any rally

- 🎯 The $12 short strike aligns with the lower end of analyst targets

Position sizing: 10 spreads at ~$1.10 each = ~$1,100 risk for ~$2,900 max profit. Risk no more than 2-3% of portfolio.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

⚖️ Balanced: "The Turnaround Play" -- August $9 Calls

Play: Buy MBLY August 21, 2026 $9 calls

Why this works:

- 💸 Cheaper than the ATM $8 calls -- likely around $0.75-$0.85 per contract

- 📈 Only needs MBLY at $9.85 to break even -- a 23% move with 5.5 months of runway

- 🎯 If MBLY hits analyst consensus at $15, these calls would be worth $6 each -- roughly a 7x return

- ⏰ Captures all upcoming catalysts: Loop Capital (Mar 10), Q1 earnings (Apr 23), VW robotaxi updates

- 📊 The $9 strike sits right at the strongest gamma resistance level, meaning a break above it signals a technical breakout

Why it could hurt:

- 📉 Slightly out-of-the-money means more of the premium is time value

- ⏰ If MBLY stays stuck below $9 for months, time decay accelerates in the final weeks

Position sizing: 20 contracts at ~$0.80 each = ~$1,600 at risk. Only risk what you can afford to lose.

Risk level: Moderate-High (can lose 100% of premium) | Skill level: Intermediate

🚀 Aggressive: "Ride the Whale" -- Long August $8 Calls

Play: Buy MBLY August 21, 2026 $8 calls -- the same trade as the whale

Why this works (and why it's risky):

- 💥 Identical strike, same expiration -- you're riding alongside $1.4M of institutional conviction

- 📊 ATM strike means maximum delta -- the position moves nearly dollar-for-dollar with the stock

- 🚀 If MBLY hits $15, these calls would be worth $7 each -- a 5x return from $1.35 entry

- 📈 Breakeven at $9.35 is only 16.7% above current price -- achievable with one solid earnings beat

- 🤝 With 10,275 contracts of open interest after this trade, the strike has meaningful liquidity

Why it could blow up:

- 💸 $1.35 per contract is not cheap for an $8 stock -- you're paying 16.9% of the stock price for 5.5 months

- ⏰ If MBLY stays flat, time decay erodes $0.20-$0.25 per month

- 📉 Intel share sales could create periodic selling pressure

- 🚗 Autonomous driving is a "show me" sector -- promises do not always translate to revenue

Position sizing: Risk ONLY what you can afford to lose completely. 10 contracts = ~$1,350 at risk.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Intel ownership overhang: Intel still owns ~80% of MBLY and has been systematically selling shares to raise cash as it restructures. They have already dumped over $1B worth of MBLY shares. Each new block sale creates selling pressure and signals that Intel -- the entity with the most inside knowledge -- is a willing seller at these prices. More sales could come without warning.

-

🚗 "Transition year" could mean "disappointment year": Management labeled 2026 a transition year with flat to 5% revenue growth. While this could be sandbagging, it could also be a genuine warning that the big OEM ramp takes longer than bulls expect. New auto programs notoriously slip timelines.

-

⚔️ Autonomous driving is a knife fight: Tesla FSD is improving rapidly. Waymo has a growing robotaxi network. Chinese ADAS competitors are aggressive on price. If OEMs decide to use cheaper Chinese alternatives or build in-house, Mobileye's moat narrows.

-

💸 Mentee Robotics is a dilutive bet: The $900M acquisition adds ~$100M+ in annual R&D expenses and 26.2M shares of dilution -- all for a business that will not generate meaningful revenue until 2028. If the humanoid robotics hype fades, this becomes an expensive distraction.

-

📊 Low liquidity options: Before this trade, there were only 275 contracts of open interest at the $8 August strike. Even after adding 10,000 contracts, MBLY options are relatively illiquid compared to mega-cap names. Wider bid-ask spreads and slippage are real costs for retail traders.

-

🌍 Auto industry cyclicality: If the global economy slows or tariffs hit the auto sector, OEMs pull back on technology spending first. ADAS adoption is a luxury in a downturn, not a necessity. Macro risk and consumer slowdowns could delay the entire thesis.

-

⏰ Time decay on a 5.5-month $1.35 premium: The trader is paying roughly $0.25/month in time decay. If MBLY does not make meaningful progress toward $9-$10 by early summer, the calls could lose 40-50% of value even if the stock is flat.

🎯 The Bottom Line

Here's the deal: Someone with serious conviction just put $1.4M on the table betting Mobileye rallies from near its all-time low over the next 5.5 months. This is not a hedge. It is not a roll. With a z-score of 53.8 and volume 36x the open interest, this is a brand new directional bet that MBLY's "transition year" is actually its turning point.

What this trade tells us:

- 🎯 Institutional money sees MBLY as deeply undervalued at $8, trading at a massive discount to the $16-$17 analyst consensus

- 💰 They are willing to risk $1.4M on this thesis, and they paid at the ask to get filled -- urgency, not hesitation

- ⏰ The August expiration strategically captures Loop Capital (Mar 10), Q1 earnings (Apr 23), potential VW robotaxi updates, and EyeQ6H ramp milestones

- 📊 The ATM $8 strike says they expect the stock to move substantially -- not just a small bounce, but a re-rating

If you are bullish on MBLY:

- ✅ Consider defined-risk strategies (call spreads) rather than naked calls to limit downside

- 📊 The $8 gamma support is your floor -- set alerts if MBLY breaks below $7.50

- ⏰ Mark April 23 (Q1 earnings) as your first major checkpoint for thesis validation

- 💡 Watch the Loop Capital conference on March 10 for near-term sentiment clues

If you are on the sidelines:

- 🎯 Wait for Q1 earnings confirmation before committing capital -- the "transition year" narrative needs to be validated with actual numbers

- 📊 A confirmed close above $9 (breaking the key gamma resistance level) would be a meaningful technical signal worth watching for

- 📈 The analyst consensus target of $16.17 (97% upside) with a high of $28 from Oppenheimer shows the Street sees massive upside -- the question is timing

If you are bearish:

- ⚠️ The Intel overhang is real -- watch for SEC filings indicating new block sales

- 📉 A break below the $8 gamma support level changes the picture and opens the path to $7.50 and $7.00

- 🛡️ If you are short, the $9 level is your stop -- a breakout above $9 with volume means the bulls have won the near-term battle

Key dates to mark:

- 📅 March 10, 2026 -- Loop Capital investor conference (management commentary)

- 📅 Q1 2026 -- Mentee Robotics acquisition expected to close

- 📅 April 23, 2026 -- Q1 2026 earnings (19% revenue growth expected -- THE make-or-break moment)

- 📅 H1 2026 -- VW/Uber robotaxi deployment updates in Los Angeles

- 📅 August 21, 2026 -- THIS TRADE EXPIRES -- moment of truth for the $1.4M bet

Final verdict: MBLY at $8 is the kind of setup that makes contrarian investors lean forward. The stock is near its all-time low, but the business is winning new OEM deals, generating growing cash flow, expanding into robotics, and trading at a massive discount to analyst targets. The $1.4M whale trade reflects a clear thesis: the "transition year" label is sandbagging, and the stock is coiled for a snapback. The breakeven at $9.35 is achievable with a single positive catalyst, and the risk/reward skews heavily toward the upside at these levels. If you want to play along, defined-risk call spreads are the smartest way to ride with the whale without risking your entire account. Just remember -- Intel owns 80% of this company and has been a willing seller. That overhang does not disappear overnight.

Be patient. Let the earnings tell the story. And remember: at $8, even a modest re-rating delivers outsized returns.

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Options trading involves significant risk of loss and is not suitable for all investors. Always do your own research and consider your risk tolerance before entering any trade. Past unusual options activity is not a reliable predictor of future stock price movement.

About Mobileye Global Inc.: Mobileye Global Inc. develops and deploys advanced driver assistance systems (ADAS) and autonomous driving technologies, building comprehensive software and hardware solutions for self-driving vehicles. With a market cap of $6.83B, 4,200 employees, and headquarters in Jerusalem, the company is a leader in computer vision and AI for automotive safety, listed on NASDAQ.