💎 META Massive $23M Call Buyback - Short Seller Covers into AI Strength! 🛡️

📅 December 10, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed a HUGE short call position in META this morning at 10:27:58, buying back 3,000 contracts of $600 strike calls for $23 MILLION! This BTC (Buy to Close) trade represents a short seller throwing in the towel - they're buying back their Feb 2026 calls at $75.65 with the stock at $651, taking a beating on this position. With META riding high on AI momentum and sitting 44% above the strike price, this forced buyback suggests capitulation. Translation: Someone bet against META's AI rally and is now paying dearly to exit their position!

📊 Company Overview

Meta Platforms (META) is the world's largest social media empire and an emerging AI powerhouse:

- Market Cap: $1.66 Trillion (4th largest globally)

- Industry: Social Media, Digital Advertising, AI, AR/VR

- Current Price: $651 (down from $796 all-time high in August)

- Primary Business: Facebook, Instagram, WhatsApp, Messenger with 3.48B daily active users monetized through AI-powered advertising

Meta operates the "Family of Apps" reaching nearly half the world's population daily, while simultaneously building massive AI infrastructure ($64-72B capex in 2025) to power Meta AI, Llama 4 models, and future AR glasses. The company beat Q2 2025 earnings with $47.52B revenue (+22% YoY) and $18.34B net profit (+36% YoY), demonstrating advertising strength despite massive AI investments.

💰 The Option Flow Breakdown

The Tape (December 10, 2025 @ 10:27:58):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:27:58 | META | ASK | BUY | CALL $600 | 2026-02-20 | $23M | $600 | 3,000 | 12,000 | 3,000 | $651 | $75.65 |

🤓 What This Actually Means

This is a SHORT CALL BUYBACK - someone is CLOSING an existing short position! Here's the real story:

- 🔴 CLOSING SHORT: BUY TO CLOSE means this trader previously SOLD these calls and is now buying them back to exit

- 💸 Expensive buyback: $23M ($75.65 per contract × 3,000 contracts) - up massively from where they likely sold

- 📉 Underwater position: Stock at $651 vs $600 strike = $51 in-the-money! Calls were likely sold when stock was $580-600

- ⏰ 72 days to expiration: February 20, 2026 expiration - plenty of time left but position deteriorating fast

- 🛡️ Damage control: With stock 8.5% above strike and rising, covering now prevents unlimited upside losses

- 📊 Size matters: 3,000 contracts represents 300,000 shares worth ~$195M in stock exposure

What's really happening here: This trader got CAUGHT SHORT! They likely sold these Feb $600 calls weeks or months ago when META was trading $580-620, collecting premium while betting META wouldn't break $600 by February. But META rallied to $651 (hit $789 in August!), putting these calls deep in-the-money. Now with META showing strength on AI catalysts, they're forced to buy back at $75.65 - a painful exit that could represent a 50-100% loss depending on their original sale price.

Why close now? With 72 days left, the short call is bleeding value daily as META stays elevated. If META continues rallying toward $700+, losses compound exponentially (short calls have UNLIMITED risk). Buying back at $75.65 locks in a massive loss but prevents catastrophic losses if META rips to $750-800.

Unusual Score: 🔥 This is significant institutional repositioning. The open interest of 12,000 contracts shows this strike has heavy activity, and this single 3,000 contract buyback represents 25% of total OI - someone's making a major capitulation move!

📈 Technical Setup / Chart Check-Up

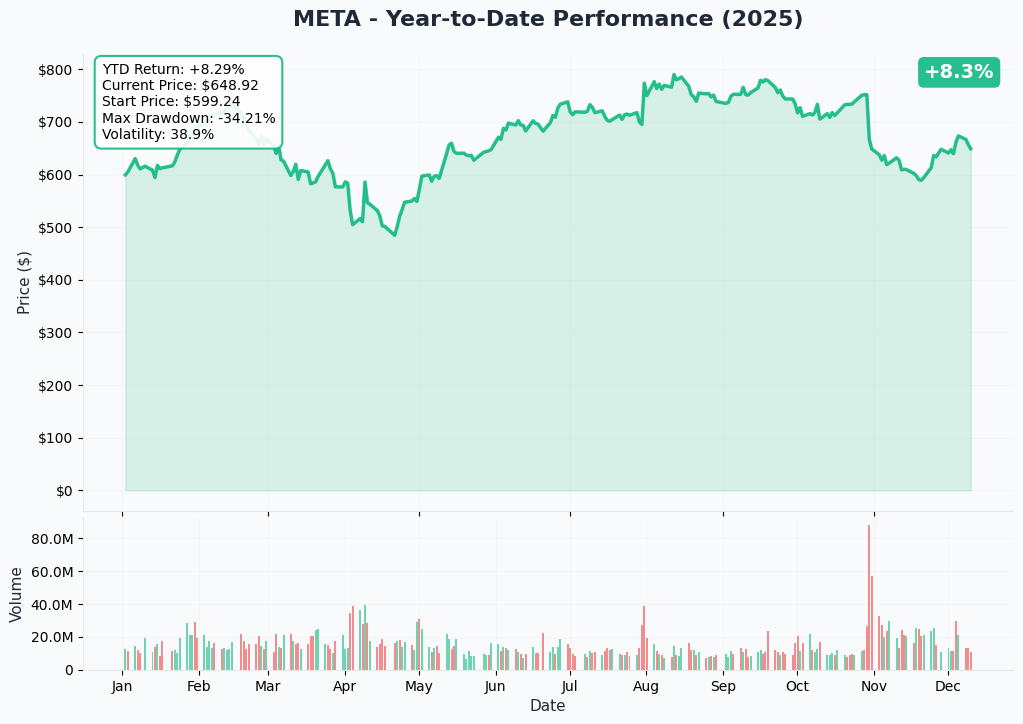

YTD Performance Chart

META has had a wild 2025 - currently at $651 after hitting an all-time high of $796 in August, then pulling back 17.7%. Despite the selloff, META is still up strongly YTD, demonstrating the power of its AI transformation story.

Key observations:

- 🚀 All-time high run: Explosive rally to $796 in August on AI infrastructure announcements and strong earnings

- 📉 Healthy pullback: 17.7% correction from peak provides better entry point while fundamentals remain intact

- 📊 Support holding: Trading above major support levels, consolidating gains before next leg

- 🎯 Range-bound: Currently in $630-670 consolidation zone

- ⚡ Catalyst-driven: Price action closely tied to AI announcements, earnings, and regulatory news

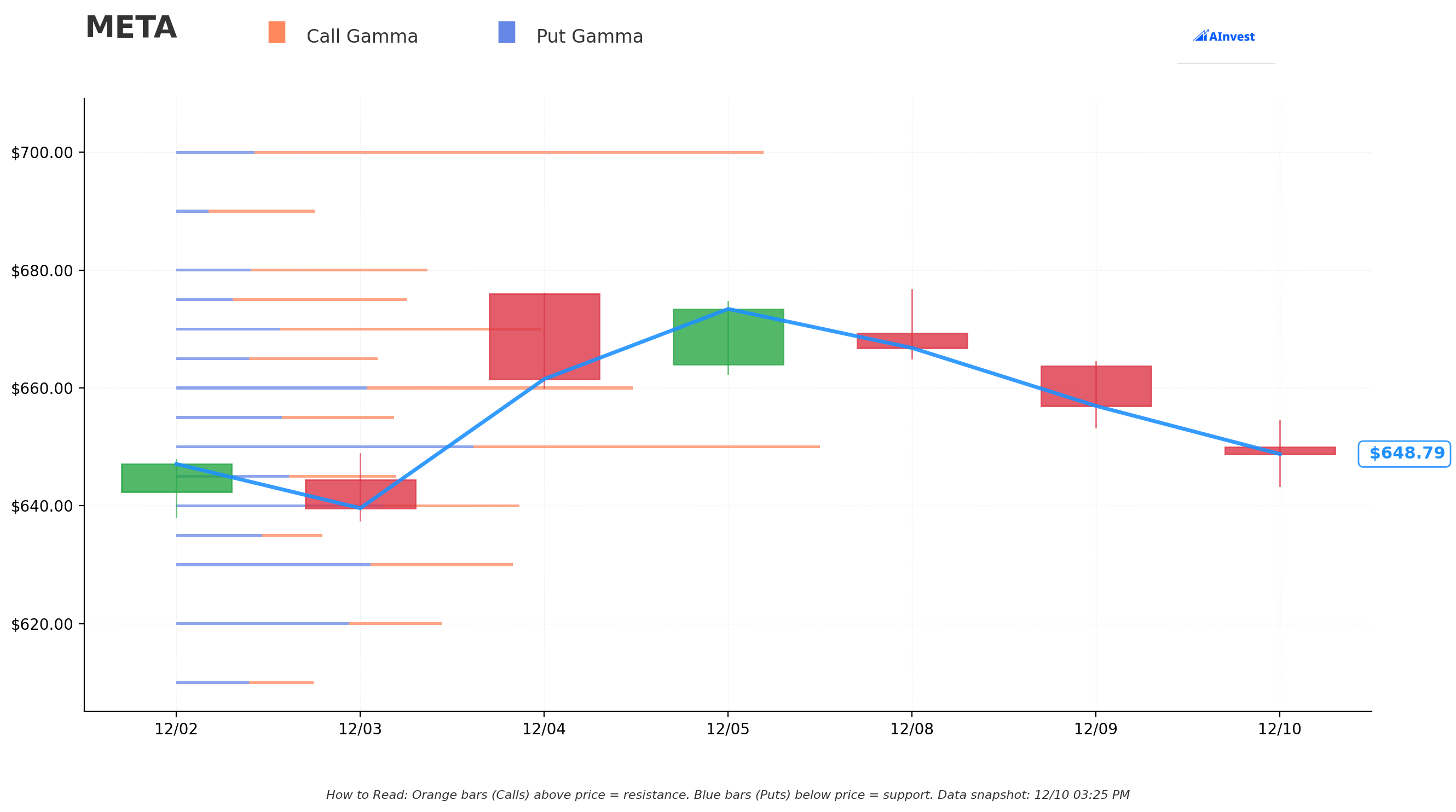

Gamma-Based Support & Resistance Analysis

Current Price: $648.77

The gamma exposure map reveals critical price magnets and barriers governing near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $640 - Immediate support with 23.0B total gamma (strongest nearby floor - 1.4% below)

- $630 - Secondary support at 22.5B gamma (2.9% below)

- $620 - Solid floor with 17.8B gamma (4.4% below)

- $600 - Deep support at 26.5B gamma (7.5% below - THE STRIKE where calls were sold!)

🟠 Resistance Levels (Call Gamma Above Price):

- $650 - Immediate ceiling with 43.2B gamma (STRONGEST RESISTANCE - 0.2% overhead)

- $660 - Secondary resistance at 30.7B gamma (1.7% above)

- $670 - Major barrier with 24.5B gamma (3.3% above)

- $675 - Additional ceiling at 15.5B gamma (4.0% above)

- $680 - Resistance zone with 16.8B gamma (4.8% above)

- $700 - Extended upside target at 39.4B gamma (7.9% above)

What this means for traders: META is pinned just below massive $650 resistance (43.2B gamma - the dominant level). This creates natural selling pressure as price approaches. However, notice the strong call gamma at $700 (39.4B) - if META breaks through $650-670 resistance cluster, it could accelerate toward $700 as dealers hedge their positions.

Notice the $600 level? That's exactly where this short call trade is struck! The 26.5B gamma support there shows it was a logical strike to sell calls against - seemed like a safe ceiling weeks ago. But META powered through and never looked back, crushing the short seller.

Net GEX Bias: Bullish (300.4B call gamma vs 206.1B put gamma) - Massive bullish skew with dealers long puts/short calls creates supportive dynamics for upside moves. The short call buyback actually REMOVES selling pressure (one less dealer hedging short calls).

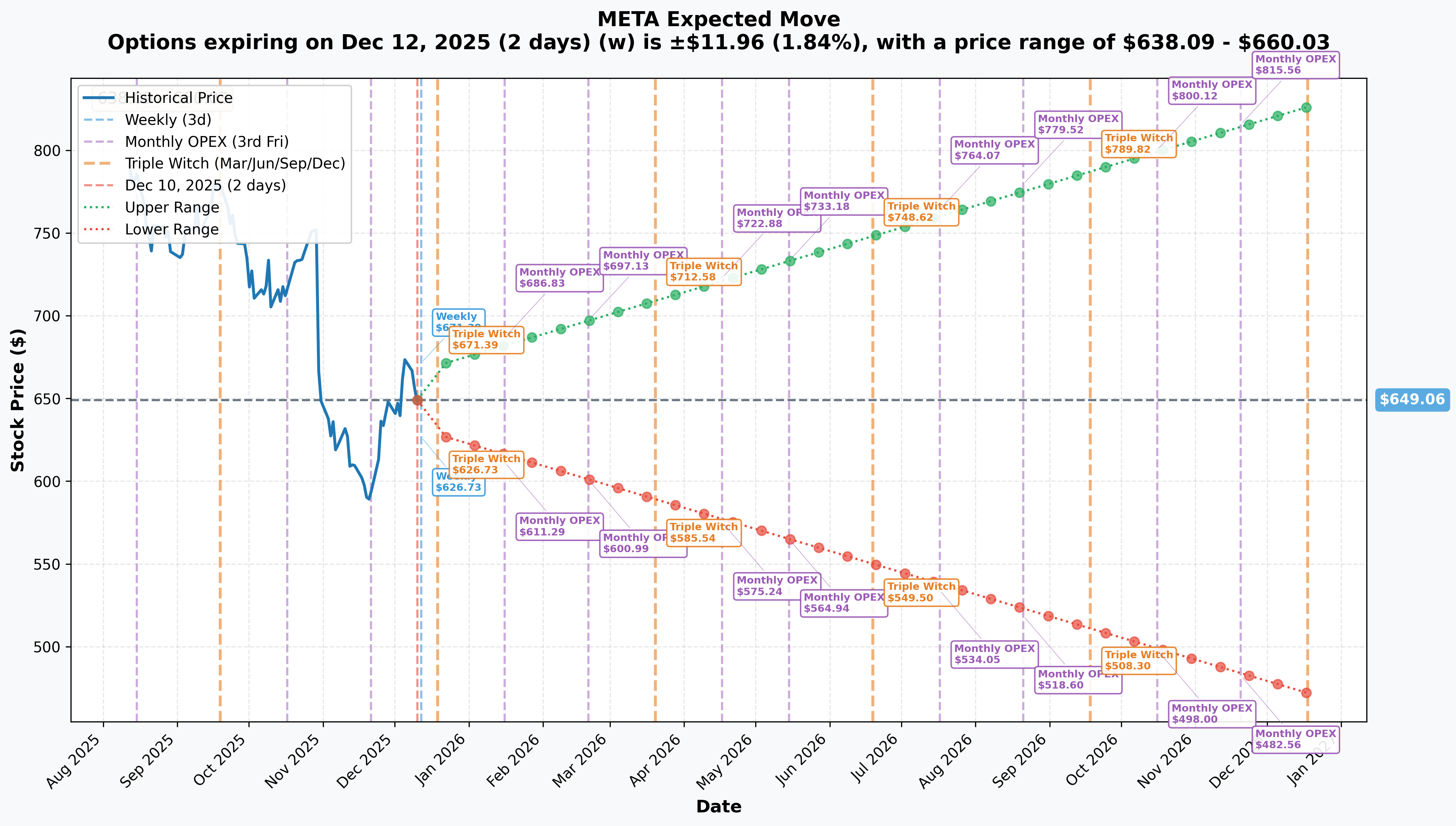

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 2 days): ±$11.96 (±1.84%) → Range: $638-660

- 📅 Monthly OPEX (Dec 19 - 9 days): ±$21.06 (±3.24%) → Range: $628-670

- 📅 Quarterly Triple Witch (Dec 19 - 9 days): ±$21.04 (±3.24%) → Range: $628-670

- 📅 February OPEX (Feb 20 - 72 days - THIS TRADE!): ±$48.06 (±7.4%) → Range: $601-697

Translation for regular folks: Options traders are pricing in a 1.8% move ($12) by Friday for weekly expiration, but a larger 3.2% move ($21) through December OPEX with triple witching volatility. The critical February 20th expiration (when these calls expire) has an implied range of $601-697.

Key insight: The February range bottom of $601 is EXACTLY at the $600 strike! This shows the market originally thought there was a decent chance META trades back to $600 by February. But with META holding $650+ and showing AI strength, the short seller realized staying short was too risky - if META rallies toward the $697 upper range, their losses would be catastrophic (remember: short calls have UNLIMITED loss potential).

🎪 Catalysts

🔥 Recent Catalysts (Last 90 Days)

Q2 2025 Earnings Beat (July 30, 2025) 📊

META crushed Q2 expectations, continuing its streak of earnings dominance:

- 📊 Revenue: $47.52B (up 22% YoY) vs estimates

- 💰 Net Profit: $18.34B (up 36% YoY) - massive margin expansion

- 👥 Daily Active People: 3.48B (up 6% YoY) - still growing at scale!

- 🤖 AI Integration: 4M+ advertisers using generative AI tools (up from 1M six months prior)

- 📈 Q3 Guidance: $47.5-50.5B revenue expected - strong forward outlook

AI Infrastructure Buildout Acceleration 🏭

META is making unprecedented investments in AI infrastructure positioning for long-term dominance:

- 💰 2025 Capex: $64-72B raised from prior $60-65B guidance - 81% growth YoY

- 🏗️ Prometheus (Ohio): 1 gigawatt AI supercluster coming online 2026

- 🌆 Hyperion (Louisiana): Manhattan-sized footprint scaling to 5 gigawatts over several years

- 🎯 Long-term Commitment: $600B+ on U.S. data centers through 2028

This capex surge pressures near-term free cash flow but positions META to lead the AI platform shift - exactly the kind of commitment that forces short sellers to cover!

Llama 4 Model Family Launch (April 2025) 🤖

META released its most advanced AI models, strengthening competitive position against OpenAI and Google:

- 🧠 Llama 4 Scout: 17B active parameters, 16 experts, 10M token context window - "best multimodal model in its class"

- 🚀 Llama 4 Maverick: 17B active parameters, 128 experts - beats GPT-4o and Gemini 2.0 Flash on benchmarks

- 💪 Llama 4 Behemoth: 288B active parameters - outperforms GPT-4.5, Claude Sonnet 3.7, Gemini 2.0 Pro

- 🎁 All models open-sourced for free developer access - unique competitive strategy

Meta AI Hits 1 Billion Users 🎯

Meta AI reached 1B monthly active users in Q1 2025, approaching Zuckerberg's "1 billion users before monetization" threshold:

- 👥 Scale: 1B monthly, 185M weekly, 40M+ daily active users

- 💰 Monetization Timeline: CFO indicated business opportunity "won't show up until after 2025" but approaching inflection point

- 🎯 Revenue Potential: Advantage+ shopping campaigns exceed $20B annual run rate, growing 70% YoY

EU Antitrust Fine (November 2024) ⚖️

European Commission fined META €797.72M ($840M) for Facebook Marketplace antitrust violations:

- 📉 First EU antitrust penalty against META specifically

- 🏛️ META announced appeal - states users "choose whether or not to engage with Marketplace"

- 💸 Cumulative EU fines now exceed $2B+ across GDPR, security breaches, and antitrust matters

While negative, the $840M fine is pocket change for a company generating $47B+ quarterly revenue and sitting on massive cash reserves.

🚀 Upcoming Catalysts (Next 6 Months)

Q3 2025 Earnings - January 28, 2026 (Estimated) 📊

META's next earnings report lands in late January (unconfirmed date):

- 📅 Expected Window: Late January 2026 after market close

- 🎯 Analyst Focus Areas:

- Q4 2025 performance vs $47.5-50.5B guidance

- Full-year 2025 capex execution ($64-72B range)

- Meta AI monetization timeline and user growth trajectory

- Reality Labs losses and Ray-Ban smart glasses momentum

- 2026 outlook and capex guidance

Why this matters for the covered call: Earnings comes 3 weeks BEFORE the Feb 20 expiration! If META beats and rallies to $700+, the short seller just saved themselves from even more catastrophic losses by covering now.

Meta AI Monetization Launch (2026) 💰

With 1B monthly active users achieved, META is approaching monetization:

- 🎯 Threshold Reached: Hit Zuckerberg's stated "1 billion users before monetization" target

- 💵 Revenue Plans: Paid recommendations, premium subscription service for additional compute

- 📊 Ad Integration: Generative AI ad tools now used by 4M+ advertisers (4x growth in 6 months)

- ⏰ Timeline: CFO indicated revenue impact "after 2025" - likely H1 2026 rollout

This is a MASSIVE revenue opportunity - ChatGPT demonstrated AI assistants can generate billions at scale.

Ray-Ban Meta Smart Glasses Acceleration 🕶️

META's AI glasses are seeing explosive adoption:

- 📈 Sales Milestone: 2M+ units sold total, 200%+ Q1 2025 growth YoY

- 🏭 Production Scaling: EssilorLuxottica expanding to 10M+ annual capacity by end 2026

- 🤖 New Features: Live translation (English/Spanish/French/Italian), Shazam integration, continuous AI assistant

- 💰 Revenue Impact: Reality Labs still posting losses but Ray-Ban offsetting Quest weakness

Orion AR Glasses Consumer Launch (2027) 🥽

META's "Artemis" consumer AR glasses represent next major platform:

- 👨💻 Developer Access: Orion prototypes offered to developers in 2026

- 🎯 Consumer Launch: Late 2027 expected (internal timeline)

- 💸 Cost Reduction: Current $10K prototypes targeting $700-1,200 consumer price

- 🌟 Strategic Importance: Transition from smartphone-dependent apps to standalone computing platform

⚠️ Risk Catalysts (Negative)

AI Infrastructure ROI Uncertainty 📉

The massive capex surge creates near-term pressure:

- 💰 Free Cash Flow Pressure: Projected to decline from $52B (2024) to $26B (2026) due to infrastructure spending

- ⏰ Monetization Delayed: Meta AI revenue contribution pushed to post-2025

- 🎯 $600B Commitment: Assumes AI infrastructure delivers commensurate returns through 2028

- 📊 Market Skepticism: Some forecasts project 2026 pullback if AI ROI doesn't materialize on schedule

Reality Labs Continued Losses 🔴

- 💸 Q3 2024 Operating Loss: $4.4B (on just $270M revenue)

- 📈 Increasing Losses: Management guidance that losses "will continue to increase due to ongoing product development"

- 🎮 Quest Sales Weakness: Strong Q4 2024 holiday sales not sustained into 2025

- 🥽 AR Glasses Risk: Over 50% of Reality Labs spending on products not yet launched

Competitive Threats 🥊

- 🤖 Google Gemini 3: November 2025 launch beat ChatGPT on benchmarks, forcing OpenAI "code red"

- 📱 TikTok: 1.59B MAUs eating younger demographic engagement

- 📊 Market Share Erosion: Facebook's global social ad share declining from 89% (2013) to 38.2% (2025)

- 🔍 AI Search Disruption: Google AI Overviews could reduce social referral traffic

Regulatory Overhang 🏛️

- 🇪🇺 EU Fines: €797M antitrust (Nov 2024), $1B+ GDPR (May 2023), $400M+ violations (Jan 2023)

- 📜 Digital Markets Act: New fines possible under 2024 legislation

- 🇺🇸 U.S. Antitrust: FTC scrutiny, Section 230 debate, content moderation pressure

🎲 Trading Ideas

🛡️ Conservative: Sell Cash-Secured Puts at Support

Play: Sell puts at $640 support to get paid while waiting for pullback entry

Structure: Sell Feb 20 $640 puts (same expiration as the covered call!)

Why this works:

- 💰 Collect premium ($8-12 per contract estimated) while waiting to buy META at discount

- 🛡️ $640 is major gamma support (23.0B) - strong floor 1.4% below current price

- ✅ If assigned at $640, you own META at effective cost of $628-632 (strike minus premium) - 3-4% discount

- 📊 If META stays above $640, keep premium and repeat next month

- ⏰ Same Feb 20 expiration as the short call that just covered - ride same time decay

Risk level: Moderate (must have cash to buy 100 shares per contract at $640) | Skill level: Intermediate

⚖️ Balanced: Bull Put Spread Below Support

Play: Sell put spread capitalizing on strong support levels and bullish gamma skew

Structure: Sell $630 puts, Buy $620 puts (February 20 expiration)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Support cluster at $630 (22.5B gamma) and $620 (17.8B gamma)

- 💰 Collect ~$3-4 net credit per spread (30-40% ROI if META stays above $630)

- ✅ Bullish positioning aligned with 300.4B call gamma dominance

- 🛡️ Max loss only occurs if META drops 3-5% below current levels - unlikely given AI momentum

Estimated P&L:

- 💰 Collect: ~$3.50 credit per spread

- 📈 Max profit: $350 if META above $630 at expiration (35% ROI)

- 📉 Max loss: $650 if META below $620 (defined and limited)

- 🎯 Breakeven: ~$626.50

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: Long Call Spread Targeting $700

Play: Buy call spread betting on breakout through resistance toward $700 level

Structure: Buy $660 calls, Sell $700 calls (February 20 expiration)

Why this could work:

- 🚀 Short call buyback REMOVES dealer selling pressure (bullish technical signal)

- 📊 If META breaks $650-670 resistance cluster, path clear to $700 (39.4B gamma magnet)

- 🎯 Earnings in late January could catalyst move - strong Q4 results + AI monetization update

- 💰 Spread caps cost while maintaining 5-6% upside leverage

- 📈 February implied move upper range of $697 aligns with $700 target

Estimated P&L:

- 💸 Cost: ~$18-22 per spread

- 📈 Max profit: $40 if META at/above $700 (80-120% ROI)

- 📉 Max loss: $18-22 (100% of premium if META below $660)

- 🎯 Breakeven: ~$678-682

Why this could blow up:

- ⚠️ Strong resistance: $650 (43.2B gamma) is massive ceiling - may cap upside

- 📉 Earnings risk: Late January earnings could disappoint on AI ROI questions

- 🇪🇺 Regulatory headline risk: EU could announce new fines/restrictions

- 💸 Premium at risk: If META stays range-bound $640-660, lose entire premium

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in ~6 weeks: Q3 results expected late January 2026 create volatility risk. While META has beaten consistently (4 quarters in a row), any disappointment on AI monetization timeline or capex ROI could trigger sharp selloff. Options pricing ±7% move but actual reactions can be larger.

-

💸 Free cash flow pressure from capex: $64-72B annual capex is MASSIVE - 2x historical levels. While strategically sound for AI leadership, this pressures FCF from $52B (2024) to projected $26B (2026). If AI revenue ramp disappoints, market may punish the spending.

-

🇪🇺 EU regulatory overhang: Already took $840M antitrust fine in November. Cumulative EU penalties exceed $2B with ongoing scrutiny under Digital Markets Act. Future fines or operational restrictions possible without warning.

-

📉 Valuation stretched after massive run: While META pulled back 17.7% from August highs, stock still trades at premium valuation requiring successful AI monetization. At 22.5x forward P/E (below tech peers but above historical median), limited margin for error.

-

🔴 Reality Labs burning $4B+ quarterly: VR/AR division showing $17B+ annual losses with Quest sales weakening. While Ray-Ban glasses are bright spot (2M+ units), Orion AR launch not until 2027. Investors may lose patience with losses if timelines slip.

-

🤖 AI competitive intensity: Google Gemini 3 impressed in November launch, OpenAI ChatGPT maintains mind share. While Llama 4 competitive, open-source strategy means META can't directly monetize model itself - must leverage through apps/ads. If Google/OpenAI capture more consumer AI engagement, META's moat weakens.

-

🌐 Social media engagement headwinds: Facebook growth slowing (4.3% YoY), TikTok eating younger demographics (1.59B MAUs). While Family of Apps still 3.48B DAP, engagement time per user may be declining as competition intensifies.

-

🇨🇳 China geopolitical risk: Minimal China exposure limits growth optionality. U.S.-China tensions could impact global tech regulation or supply chains.

-

💰 Advertising cyclicality: 98% of revenue from ads makes META vulnerable to economic slowdown. If recession emerges in 2026, ad budgets cut first - revenue could drop 15-25% in severe scenario.

-

🎯 Meta AI monetization execution risk: Reached 1B users but revenue impact "after 2025" per CFO. If monetization rollout disappoints or adoption lags, the massive AI infrastructure investment ($600B+ through 2028) looks like a waste.

🎯 The Bottom Line

Real talk: Someone just paid $23 MILLION to close a short call position that went badly wrong. They sold $600 calls betting META wouldn't rally, but the stock powered to $651 (and hit $796 in August), leaving them massively underwater. With earnings in ~6 weeks and 72 days to expiration, they cut their losses before it gets worse.

What this trade tells us:

- 🎯 Short seller capitulation = bullish technical signal (removes dealer selling pressure)

- 💪 META's AI momentum too strong for bears - even at $651, shorts can't stomach the risk

- 📈 The $600 strike that seemed safe is now 8.5% in-the-money - META's rally caught skeptics off guard

- ⏰ With late January earnings approaching, short seller didn't want to risk another beat sending META to $700+

- 🛡️ Closing now at $75.65 locks in a painful loss but prevents unlimited upside exposure

This is NOT a bearish signal - it's SHORT COVERING, which is bullish! When shorts throw in the towel, it removes overhead supply and can fuel further rallies.

If you own META:

- ✅ Hold core position - AI infrastructure buildout and monetization trajectory remain compelling

- 📊 Short covering creates bullish technical setup - one less seller in the market

- 🎯 Watch for breakout above $650-670 resistance cluster - could accelerate to $700

- ⏰ Late January earnings critical - need to see AI monetization progress and strong Q4 guidance

- 🛡️ Consider trimming 10-20% if stock reaches $700 to lock in gains before potential volatility

If you're watching from sidelines:

- 📉 Pullback to $630-640 support would offer better entry with 3-5% margin of safety

- 🎯 Short covering + bullish gamma skew (300B calls vs 206B puts) = supportive technical setup

- ⏰ Wait for late January earnings clarity before major commitment

- 💰 Selling cash-secured puts at $640 lets you get paid while waiting for pullback

- 🚀 Longer-term (6-12 months), Meta AI monetization + Ray-Ban acceleration + Llama 4 adoption are legitimate $750-850 catalysts

If you're bearish:

- ⚠️ Don't fight the tape - short covering shows bears getting squeezed

- 📊 Strong support at $640 (23.0B gamma) and $630 (22.5B gamma) makes shorting risky

- 💸 Better to wait for breakdown below $630 before initiating bearish positions

- 🎯 Focus bear case on AI ROI disappointment or Reality Labs losses expanding - those are real risks

Key dates to watch:

- 📅 December 12 (Friday) - Weekly OPEX (±1.8% implied move closes)

- 📅 December 19 (Friday) - Monthly/Quarterly Triple Witch (±3.2% implied move window)

- 📅 Late January 2026 - Q3 FY2025 earnings report (unconfirmed date, likely Jan 28)

- 📅 February 20, 2026 - Monthly OPEX, expiration of these covered calls

- 📅 H1 2026 - Meta AI monetization expected to begin

- 📅 Late 2027 - Orion AR glasses consumer launch

Final verdict: The $23M short call buyback is a BULLISH signal showing bears capitulating into META's AI strength. While the stock faces legitimate risks (AI ROI uncertainty, Reality Labs losses, regulatory headwinds), the fundamental story remains compelling: 3.48B daily users, $47B+ quarterly revenue growing 22%, Meta AI approaching monetization with 1B users, and massive infrastructure positioning for the next computing platform. The short seller who just covered learned an expensive lesson: don't bet against META's AI transformation.

Patience favors buyers here. Look for pullbacks to $630-640 for entry. The AI monetization wave is just beginning, and META is uniquely positioned with scale, engagement, and infrastructure. Let the shorts cover, let the weak hands shake out, then ride the next leg higher. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The short call buyback represents one trader's decision to close their position and does not imply you should follow it. BTC trades indicate position closing, not opening new directional bets. Always do your own research and consider consulting a licensed financial advisor before trading. Short calls carry unlimited risk - this trader learned that lesson the hard way.

About Meta Platforms: Meta Platforms, Inc. operates the world's largest social media enterprise with approximately 4 billion monthly active users across Facebook, Instagram, Messenger, and WhatsApp. The company monetizes through targeted advertising while investing heavily in AI infrastructure and AR/VR technologies, with a market cap of $1.66 trillion.