💎 META $10M Put Protection - Smart Money Hedging At Record Highs! 🛡️

📅 December 18, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $10 MILLION on META puts this morning at 10:42:04! This substantial hedge bought 6,100 contracts of $670 strike puts expiring January 23rd - protecting a major position while META trades near record highs at $668.70. With META up massively on AI-powered advertising and 700M Meta AI users, smart money is locking in downside protection at the peak. Translation: Institutional investors are buying insurance on their gains after an incredible rally!

📊 Company Overview

Meta Platforms (META) is the largest social media company in the world, boasting close to 4 billion monthly active users:

- Market Cap: $1.64 Trillion (6th largest in tech globally)

- Industry: Computer Programming, Data Processing & Services

- Current Price: $668.70 (near record highs of $675+)

- Primary Business: Facebook, Instagram, Messenger, WhatsApp - monetizing through targeted advertising, plus Reality Labs (AR/VR innovation)

💰 The Option Flow Breakdown

The Tape (December 18, 2025 @ 10:42:04):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:42:04 | META | ASK | BUY | PUT $670 | 2026-01-23 | $10M | $670 | 6,100 | 394 | 4,945 | $668.7 | $21.00 |

🤓 What This Actually Means

This is a defensive hedge on a significant long position! Here's what went down:

- 💸 Substantial premium paid: $10M ($21.00 per contract × 6,100 contracts × 100 shares)

- 🛡️ Protection strike: $670 provides very tight 0.2% downside cushion - basically at-the-money protection

- ⏰ Strategic timing: 36 days to expiration captures Q4 2024 earnings aftermath, Q1 2025 earnings prep (April 30), and antitrust trial developments

- 📊 Size matters: 6,100 contracts represents 610,000 shares worth ~$408M at current prices

- 🏦 Institutional insurance: This is sophisticated portfolio hedging by someone sitting on major gains

What's really happening here: This trader likely holds a MASSIVE long position in META stock or calls accumulated during the rally. Now, with META trading near all-time highs and facing multiple near-term catalysts (earnings, antitrust trial), they're paying $21 per share for the Jan 23 $670 puts for insurance. If META drops below $670 by January 23rd, these puts pay off dollar-for-dollar. Think of it like buying a $10M insurance policy when you own a mansion that's appreciated massively.

Unusual Score: 🔥 EXTREMELY UNUSUAL (69.56x Z-score) - This happens just a few times a year! We're talking about protection for a position worth over $400M. The classification as "EXTREMELY_UNUSUAL" with HIGH_ACTIVITY signals means this is literally off-the-charts unusual - only a handful of larger trades in recent history.

📈 Technical Setup / Chart Check-Up

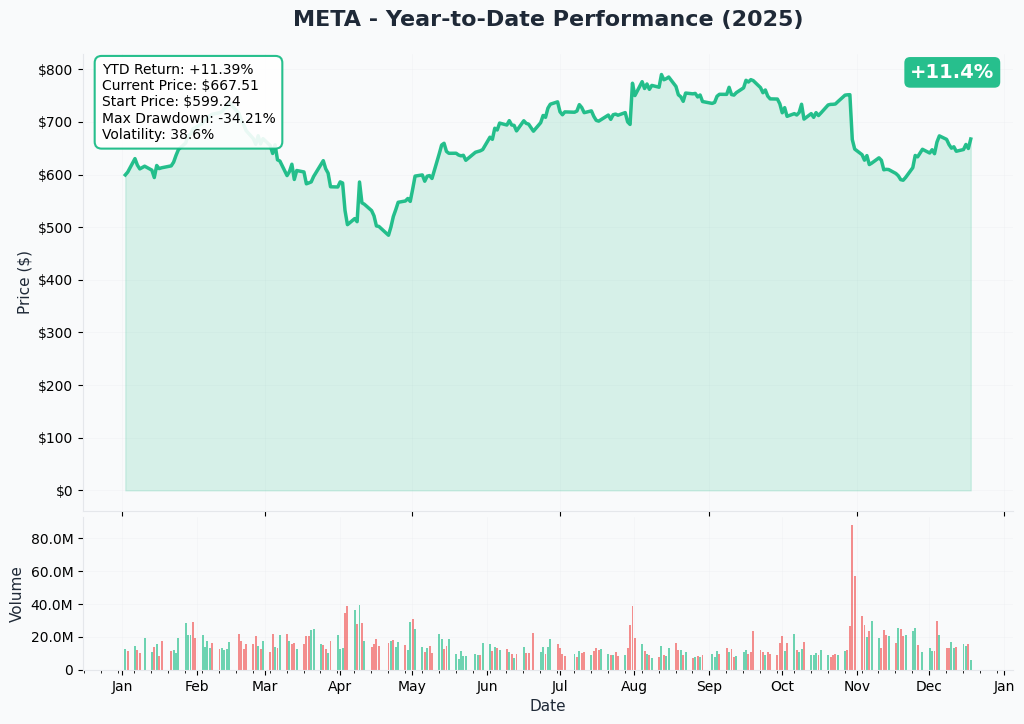

YTD Performance Chart

META has had an absolutely stellar year - the chart shows a powerful uptrend from the start of 2025, climbing from around $500 levels to current highs near $670. The price action has been consistently strong throughout the year with relatively shallow pullbacks.

Key observations:

- 🚀 Steady institutional accumulation: Consistent uptrend shows institutional buying throughout 2025

- 📈 Breakout momentum: Multiple resistance levels conquered on path from $500s to $670s

- 📊 Volume confirmation: Strong volume supporting rallies indicates healthy buying interest

- 🎯 Near record highs: Trading within striking distance of all-time highs - elevated risk/reward

- ⚠️ Extension risk: After such a strong run, near-term consolidation or pullback increasingly likely

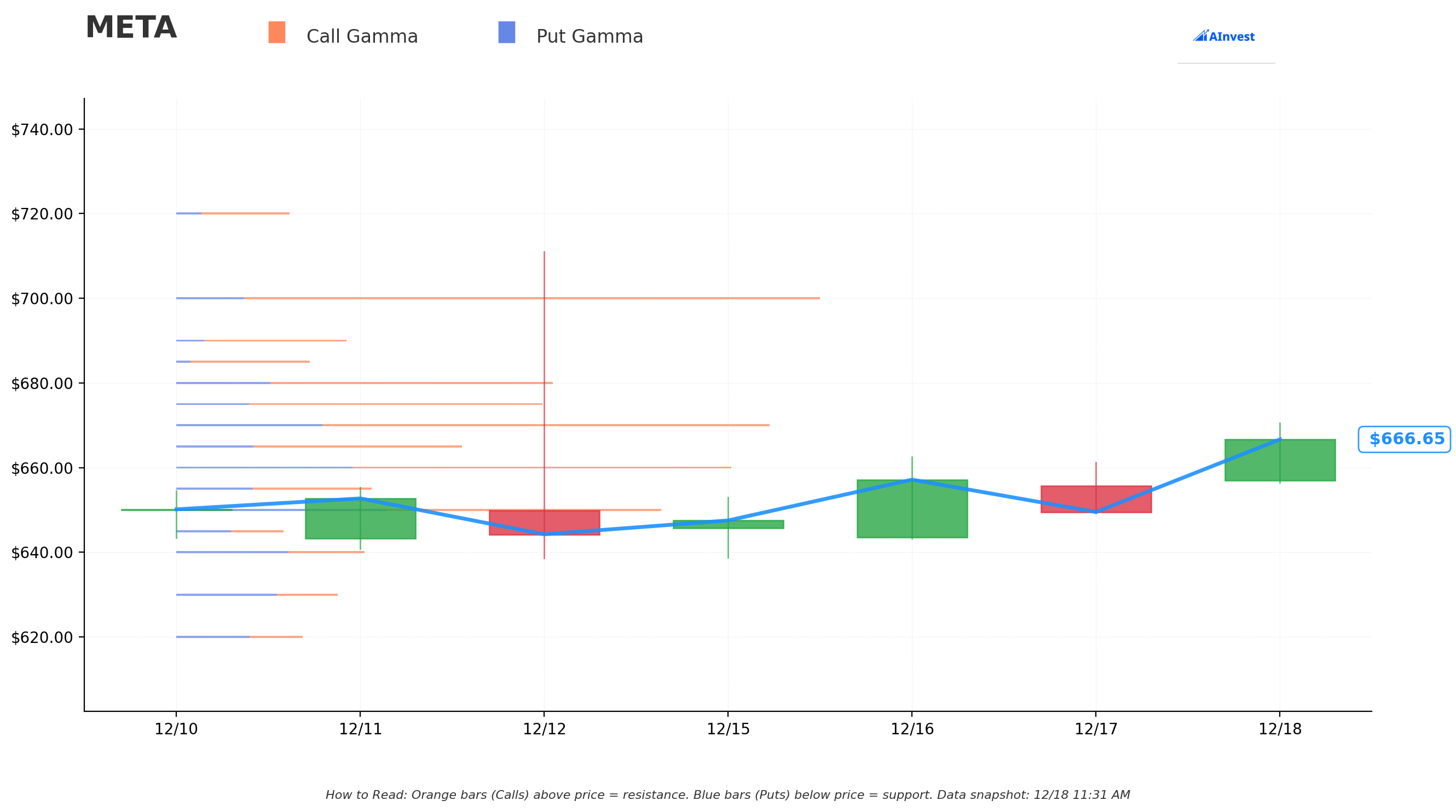

Gamma-Based Support & Resistance Analysis

Current Price: $667.25

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $665 - Immediate support with 22.6B total gamma exposure (strongest nearby floor!)

- $660 - Strong secondary support at 44.2B gamma (dealers will buy dips aggressively here)

- $655 - Tertiary support at 15.6B gamma

- $650 - Major structural floor with 38.9B gamma (important psychological level)

- $640 - Deep support at 15.1B gamma (bearish scenario floor)

- $600 - Extended disaster scenario at 16.8B gamma (10% correction)

🟠 Resistance Levels (Call Gamma Above Price):

- $670 - Immediate ceiling with 46.9B gamma (STRONGEST RESISTANCE - dealers will sell into rallies)

- $675 - Secondary resistance at 28.9B gamma (1.2% overhead)

- $680 - Additional ceiling zone with 29.6B gamma (2% above current)

- $700 - Major upside target at 51.0B gamma (5% rally required - highest call gamma level)

What this means for traders: META is trading in a TIGHT range between strong $665 support and massive $670 resistance. The gamma data shows market makers holding enormous positions at $670 (46.9B - matching exactly where this put trade is struck!) which creates natural selling pressure as price approaches. This setup screams "consolidation range" before the next big move. The $660 level with 44.2B gamma is extremely important - break below that and momentum could accelerate toward $650.

Notice anything? The put buyer struck EXACTLY at $670 where there's 46.9B gamma resistance - the single strongest resistance level on the board. They're positioning for protection if META can't break through this ceiling and instead rolls over. Smart positioning.

Net GEX Bias: Bullish (379.2B call gamma vs 168.4B put gamma) - Overall positioning remains constructive, but immediate price action constrained by overhead resistance at $670-$680.

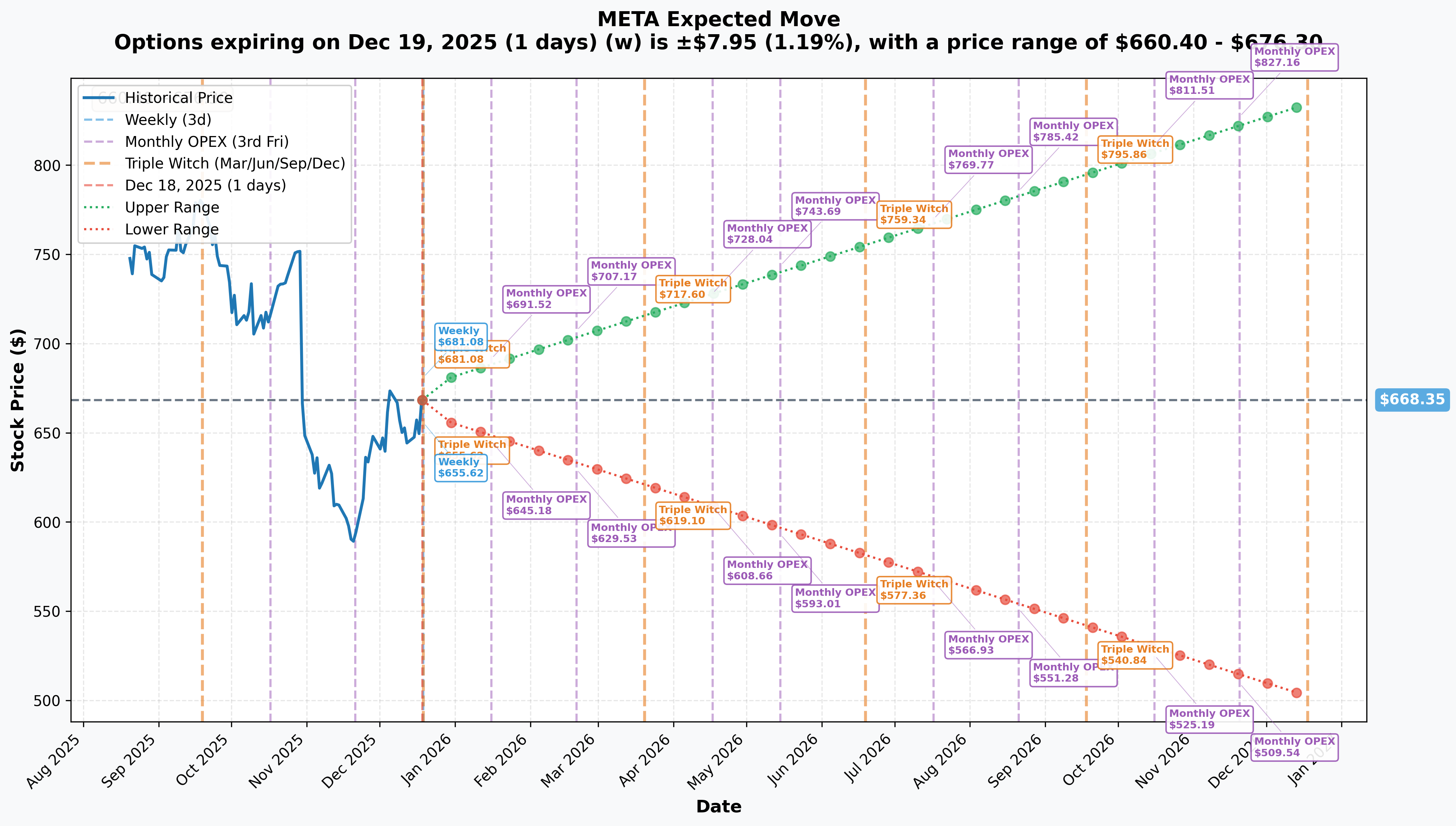

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly/Monthly/Triple Witch (Dec 19 - 1 day): ±$7.95 (±1.19%) → Range: $660.40 - $676.30

- 📅 Monthly OPEX (Jan 16 - 29 days): ±$23.17 (±3.47%) → Range: $645.18 - $691.52

- 📅 January 23 OPEX (36 days - THIS TRADE!): ~±$26 (±3.9%) → Range: ~$642 - $694

- 📅 Triple Witch (Mar 20 - 92 days): ±$49.25 (±7.36%) → Range: $619.10 - $717.60

- 📅 Yearly LEAPS (Dec 18, 2026 - 365 days): ±$166.20 (±24.87%) → Range: $502.15 - $834.55

Translation for regular folks: Options traders are pricing in a 1.2% move ($8) by tomorrow for weekly expiration, but a larger 3.5% move ($23) through January 16th which captures near-term volatility. The January 23rd expiration (when this $10M trade expires) has an expected range of roughly $642-$694, meaning the market thinks there's a reasonable possibility META could trade anywhere in that 8% band over the next 36 days.

Key insight: The put strike at $670 sits right in the middle of the expected range, suggesting this isn't a "crash protection" bet but rather intelligent hedging against normal volatility. The trader is protecting against a move down to $650-$660 levels (3-5% pullback), which is well within the implied move range.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Tomorrow: December 19, 2025 - Triple Witching OPEX 📊

Tomorrow is quarterly triple witching options expiration - one of the four times per year when stock options, stock index futures, and stock index options all expire simultaneously. This creates elevated volatility potential as dealers rebalance massive positions.

- ⚡ Expected move: ±1.2% ($8) implies range of $660-$676 for settlement

- 📊 Volume surge: Expect significantly higher trading volume as positions roll forward

- 🎢 Volatility spike: Intraday swings often amplified on triple witch days

- 🎯 Key levels: $670 resistance and $665 support will be critical battle zones

Historical precedent: Tech mega-caps often see exaggerated moves on triple witch as algorithmic hedging creates feedback loops.

Impact on the put trade: With expiration tomorrow, the $670 puts won't expire but could see increased volatility as underlying stock moves on triple witch dynamics.

🚀 Near-Term Catalysts (Q1 2026)

Q1 2025 Earnings - April 30, 2025 (CONFIRMED) 📊

Meta already reported Q1 2025 earnings with stellar results, but the stock's reaction and forward guidance will impact near-term sentiment:

Key Q1 2025 Results:

- 📊 Revenue: $42.3B (+16% YoY or +19% constant currency)

- 💰 Operating Income: $17.6B (41% margin)

- 💵 Net Income: $16.6B ($6.43 EPS)

- 👥 Headcount: 76,800 employees (+4% QoQ despite 5% layoffs announced)

What matters for the put timeframe: Since the January 23 puts expire well before Q1 2025 earnings, the focus is on how recent earnings momentum continues and any surprises in business trends that emerge between now and late January.

FTC Antitrust Trial - April 14, 2025 (HIGH RISK CATALYST!) ⚖️

The most significant binary risk event on the horizon is Meta's antitrust trial beginning April 14, 2025:

- 🚨 Issue: FTC alleges Instagram (2012) and WhatsApp (2014) acquisitions violated antitrust laws by maintaining monopoly in personal social networking

- ⚖️ Status: Judge Boasberg denied Meta's motion for summary judgment in November 2024, allowing trial to proceed

- 🎯 FTC's Position: Judge noted FTC presents "substantial evidence" of anticompetitive harm

- ⚠️ Potential Remedies: Could include forced divestiture of Instagram/WhatsApp, structural changes to platform integration, or behavioral restrictions

- 📅 Timeline: Trial in April 2025, but the $670 puts expire January 23rd - BEFORE trial begins

Why this matters: While the trial itself happens after these puts expire, any pre-trial developments, settlement discussions, or legal briefings in late December through January could move the stock. Markets often price in legal risk ahead of major trials.

5% Workforce Reduction - Notifications by February 10, 2025 👥

Meta announced January 14, 2025 plans to cut 5% of workforce (~3,600 employees from 72,000+ total):

- 📅 Notification Timeline: Affected employees to be notified by February 10, 2025

- 🎯 Strategy: Targeting low performers, will hire replacements later in 2025

- 💬 Zuckerberg Quote: Described 2025 as "an intense year"

- 📊 Market Reaction: Generally positive as seen in Q1 results showing efficiency gains

Impact window: Falls squarely within the put expiration timeframe. While markets typically view cost cutting favorably, execution hiccups or employee morale issues could create near-term headwinds.

📊 Strategic Developments (Ongoing)

AI Monetization: The $20B+ Growth Engine 🤖

Meta's AI initiatives are already generating massive revenue, not just hypothetical future gains:

- 💰 Advantage+ Shopping Campaigns: Exceeded $20B annual run rate in Q4 2024 (up 70% YoY) - this is AI monetization IN REAL TIME

- 🖥️ Andromeda ML System: New partnership with Nvidia enabled 10,000x increase in model complexity for ad retrieval, driving 8% improvement in ad quality

- 📱 Meta AI Assistant: 700M monthly active users (up from 600M in December), available in 43 countries and 12 languages - approaching 1B user milestone

- 📊 Reels Revenue: $50B annual run rate as of Q4 2024 - demonstrating AI-driven content recommendation success

Why this supports higher valuations: Unlike competitors spending billions on AI with uncertain returns, Meta is ALREADY generating tens of billions in incremental revenue from AI applications. The Advantage+ platform proves AI ROI is immediate, not hypothetical.

Llama 4 AI Platform Evolution 🚀

Meta's open-source AI strategy is positioning Llama as the Android of AI:

- 📥 Llama Downloads: 650M total (averaging 1M downloads/day) - massive developer adoption

- 🆕 Llama 4 Released April 5, 2025: Scout (17B active params, 109B total) and Maverick (17B active, 400B total) models now available

- 🎯 Performance: Maverick beats GPT-4o and Gemini 2.0 Flash on benchmarks - competitive with closed models

- 🔬 In Development: Llama 4 Behemoth (288B active parameters, ~2T total) coming later in 2025

- 🌍 Multimodal: Text/image input, text output across 12 languages

Strategic value: By giving away leading AI models, Meta creates ecosystem lock-in (developers build on Llama) and ensures they have best-in-class AI for their own advertising/products without being dependent on OpenAI, Google, or Anthropic.

Ray-Ban Meta Smart Glasses: Hardware Success 👓

Unlike Reality Labs' VR struggles, smart glasses are a clear winner:

- 📊 Sales: 1M+ units sold in 2024 (vs 300K for previous version), 2M+ total since late 2023 launch

- 📈 Market Growth: Global smart glasses shipments surged 210% YoY in 2024, with Ray-Ban Meta accounting for majority share

- 🎯 2025 Target: 2-5M units (analysts' estimates), with EssilorLuxottica expanding production capacity to 10M+ pairs/year by end of 2026

- 🔮 Orion AR Prototype: Consumer version "Artemis" targeted for 2027 at $700-$1,200 (vs Apple Vision Pro at $3,499)

Revenue impact: While currently small relative to $48B+ quarterly ad revenue, smart glasses represent new hardware revenue stream with high margins and strategic positioning for future AR/VR market.

WhatsApp Business Messaging: Multi-Billion Dollar Opportunity 💬

WhatsApp is transitioning from cost center to significant revenue driver:

- 💰 2024 Revenue: $1.7B (up from $1.3B in 2023)

- 📈 Growth Rate: Paid messaging crossed $1B+ annual run rate by late 2024, doubled since early 2023

- 🎯 Management Guidance: Described as "multi-billion-dollar annual run-rate" business with double-digit growth

- 🤑 Click-to-WhatsApp Ads: $10B annualized run rate by end of 2024 (+40% QoQ)

- 📊 External Estimates: Analysts project $6-7B revenue from WhatsApp in 2025

Why this matters: WhatsApp's 2B+ users were previously unmonetized. Business API becoming WhatsApp's largest revenue stream opens massive TAM in enterprise messaging. This is pure incremental revenue on existing user base.

Instagram Dominance: Will Exceed 50% of Meta's US Revenue 📸

Instagram is becoming Meta's crown jewel:

- 💰 2025 Revenue Projection: $32.03B US ad revenue (+24.4% vs 2024)

- 🎯 Milestone: Will represent 50.3% of Meta's US revenue for first time in 2025

- 📊 Reels Success: Instagram Reels at $50B run rate globally

- 🆕 New Features: Meta-verified users can now add clickable links to Reels (December 2024 launch)

- 📈 Threads Growth: Continued rollout of business tools and creator monetization features

Competitive moat: Instagram holds 68% social ad spend share in US, far ahead of TikTok, Snapchat, and other platforms. Reels' $50B run rate shows successful competition with TikTok short-form video.

⚠️ Risk Catalysts (Negative)

AI Infrastructure Costs Ballooning 💸

The elephant in the room - massive capex spending with uncertain long-term ROI:

- 💰 2025 Capex Guidance: $66-72B (narrowed from $64-72B), up ~$30B YoY at midpoint

- 📈 Updated Guidance: Raised to $70-72B range during 2025 (Q3 2024: $19.37B spent, nine-month total ~$51B)

- 🏗️ Major Projects: Prometheus cluster (Ohio) at 1 gigawatt capacity coming online 2026; Hyperion cluster (Louisiana) scalable to 5 gigawatts

- ⚠️ 2026 Outlook: Management indicated capex growth will be "notably larger" than 2025, with analysts modeling $80B+

The concern: While Advantage+ and other AI tools are generating revenue NOW, the $66-72B annual capex (potentially $80B+ in 2026) is massive relative to $16.6B Q1 net income. If AI advertising growth plateaus or competition intensifies, these infrastructure investments might not generate expected returns. This is why smart money is hedging with the $670 puts.

Reality Labs Continues Burning Cash 🔥

The metaverse/VR bet remains a massive cash drain:

- 📉 Q4 2024 Losses: Record quarterly loss of $4.97B (revenue $1.083B, costs $6.05B)

- 💸 Full Year 2024: $17.73B total Reality Labs deficit

- 🔄 Strategic Pivot: Up to 30% budget cut for VR/metaverse teams, shifting toward AI glasses and wearables

- ⚖️ Critical Year: CTO Andrew Bosworth's memo described 2025 as "most critical year in my 8 years at Reality Labs," determining if projects are "work of visionaries or a legendary misadventure"

The reality: Reality Labs has lost $50B+ since 2019 with no clear path to profitability. The 30% budget cuts and "critical year" language suggest even Meta management is losing patience. Further writedowns or strategic pivots could impact stock sentiment.

European Regulatory Fines Accelerating 🇪🇺

Europe continues to be a regulatory headache:

- 💰 DMA Fine: €200M imposed for "consent or pay" model violation (March-November 2024)

- 🔄 Model Changes: November 12, 2024 introduced third option of less intrusive advertising and lower subscription prices, but EU flagged this could face future investigation

- 📊 DSA Compliance: EU preliminary findings show Facebook/Instagram breach obligations for illegal content reporting and researcher data access

- ⚠️ Future Risk: DMA violations carry up to 10% global revenue penalties vs 4% for GDPR - stakes are much higher

Why this matters: €200M is pocket change for Meta, but the precedent of European regulators aggressively enforcing DMA/DSA creates ongoing uncertainty. 10% of global revenue would be ~$18B - a material risk if violations continue.

TikTok Competitive Threat Remains 🎯

Despite Instagram Reels' success, TikTok still dominates short-form video:

- 📊 Market Share: TikTok holds 40% of short-form video market vs 20% for Instagram Reels and 20% for YouTube Shorts

- 💔 Engagement Gap: TikTok leads with 2.50% avg engagement rate vs Instagram overall 0.50% (though Reels specifically shows 1.48% engagement)

- 👥 User Base: TikTok's cultural relevance with Gen Z remains unmatched despite Instagram's larger total user base

- ⚖️ Regulatory Wild Card: If US TikTok ban is enforced, Instagram could capture 20%+ of reallocated ad dollars, but ban timing uncertain

The threat: While Instagram has more users, TikTok's superior engagement means advertisers get better ROI per dollar spent on TikTok. If TikTok solves its regulatory issues and remains in US market, it continues to be formidable competition for Meta's short-form video strategy.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 23rd expiration:

📈 Bull Case (30% probability)

Target: $690-$710

How we get there:

- 🚀 Breakout above $670-$680 gamma resistance on positive momentum and year-end buying

- 💪 Further AI monetization announcements or major Advantage+ customer wins drive narrative

- 📊 Early whispers of better-than-expected Q4 2024 performance (earnings reported after puts expire)

- 🎯 Meta AI crosses 1B monthly active users milestone, reinforcing platform ecosystem strength

- 🇪🇺 Positive developments on European regulatory front or settlement discussions

- 📈 Broad market strength in mega-cap tech as investors rotate into "AI winners with proven revenue"

- 🤖 Llama 4 Behemoth release or major enterprise adoption announcements

Key metrics needed:

- Sustained buying pressure to overcome $670 (46.9B gamma) and $700 (51.0B gamma) resistance

- Reaccelerating ad impression growth (family of apps engagement metrics)

- WhatsApp monetization update showing faster-than-expected progress toward $6-7B run rate

- Ray-Ban smart glasses demand exceeding 2025 targets

Probability assessment: Only 30% because it requires breakout above major gamma resistance at $670 with stock already near all-time highs. Would need significant positive catalyst to overcome dealer hedging pressure at these levels. The $670 put buyer clearly doesn't see this as the most likely scenario.

Put P&L in Bull Case:

- Stock at $690 on Jan 23: Puts worth $0 (expire worthless), loss = -$21/share × 6,100 = -$12.8M (100% loss - but underlying position gained $21+ per share, so net outcome still positive)

- Stock at $710 on Jan 23: Puts worth $0, same outcome - hedge cost is "insurance premium paid" for peace of mind

🎯 Base Case (50% probability)

Target: $650-$675 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ⚖️ Trading within gamma support ($650-$665) and resistance ($670-$680) bands for next 5 weeks

- 📊 December holiday season typically sees lighter volume and range-bound price action

- 🎢 Triple witch tomorrow (Dec 19) creates near-term volatility but doesn't break the range

- 📅 Workforce reduction notifications by Feb 10 proceed smoothly without major disruption

- 🤖 AI initiatives continue delivering but no major surprises - steady as she goes

- ⚖️ Antitrust trial preparation proceeds but no bombshells in pre-trial briefings

- 💤 Market digests YTD gains, waits for Q4 2024 earnings in late January for next catalyst

- 📉 Minor pullback to $650-$660 support tests the range but buyers step in (strong gamma floor)

This is the put buyer's ideal scenario: Stock consolidates in $650-$670 range, puts expire with minimal value or worthless, but downside protection served its purpose during uncertain period. The $10M is simply the "insurance premium" they're willing to pay to sleep well at night while holding a $400M+ position.

Put P&L in Base Case:

- Stock at $670 on Jan 23: Puts at-the-money, worth ~$8-10, loss = -$11-13/share × 6,100 = -$6.7M to -$7.9M (55-65% loss)

- Stock at $655 on Jan 23: Puts worth ~$15, loss = -$6/share × 6,100 = -$3.7M (29% loss - but hedge provided protection on $9M unrealized loss in underlying)

- Stock at $665 on Jan 23: Puts worth ~$5, loss = -$16/share × 6,100 = -$9.8M (76% loss)

Why 50% probability: Stock at technical inflection near major resistance after strong YTD run. No immediate major catalysts in next 36 days to force breakout. Fundamentals solid but already priced in. Most likely outcome is consolidation/digestion of gains with volatility from triple witch and workforce changes but no directional breakthrough.

📉 Bear Case (20% probability)

Target: $620-$650 (TEST THE SUPPORT LEVELS!)

What could go wrong:

- 😰 Broad tech selloff as year-end tax loss harvesting or profit-taking accelerates

- 🚨 Unexpected negative development in antitrust case (unfavorable pre-trial ruling or evidence disclosure)

- 📉 Ad market weakness signals emerge - December ad spending data disappoints

- 💸 Investor concern about $70-72B 2025 capex intensifies, with questions about ROI timeline

- 🇪🇺 Additional European regulatory action or fines announced

- 📊 Workforce reduction (5% layoffs) creates more disruption than expected - execution concerns

- 🤖 AI competitor (OpenAI, Google, Anthropic) announces breakthrough that threatens Meta's AI positioning

- 💰 Major institutional investor announces position reduction or downgrade from prominent analyst

- 🔨 Break below $665 immediate support triggers cascade through $660 to test $650 major floor

Critical support levels:

- 🛡️ $665: Immediate gamma floor (22.6B) - losing this opens door to further weakness

- 🛡️ $660: Strong secondary support (44.2B gamma) - MUST HOLD or momentum shifts bearish

- 🛡️ $650: Major psychological and gamma support (38.9B) - this is the LINE IN THE SAND

- 🛡️ $640: Deep bear scenario (15.1B gamma) - would represent meaningful correction

Probability assessment: Only 20% because Meta's fundamentals remain exceptionally strong (AI monetization proven, WhatsApp growing, Instagram dominant), market cap provides downside cushion (institutional support), and multiple gamma support levels below current price. Would require multiple negative catalysts to align or broader market correction to drag META down significantly.

However: The $10M institutional put buyer clearly thinks downside risk is meaningful enough to pay $21/share for protection. When smart money spends this much on insurance, they've done the math on tail risks.

Put P&L in Bear Case:

- Stock at $650 on Jan 23: Puts worth $20.00, loss = -$1/share × 6,100 = -$610K (only 5% loss - excellent hedge outcome!)

- Stock at $630 on Jan 23: Puts worth $40.00, profit = +$19/share × 6,100 = +$11.6M (90% gain - hedge more than pays for itself!)

- Stock at $620 on Jan 23: Puts worth $50.00, profit = +$29/share × 6,100 = +$17.7M (138% gain - massive windfall on disaster scenario)

💡 Trading Ideas

🛡️ Conservative: Trim and Protect (Wise Money Management)

Play: If you own META shares after big YTD gains, consider taking some profits and using puts for downside protection on remaining position

Why this works:

- 📈 META has had an incredible run - locking in some gains makes sense after such strong performance

- 🎯 Stock at major resistance ($670-$680 gamma barrier) with limited near-term catalysts to drive breakout

- ⏰ December seasonality typically favors consolidation, not explosive moves higher

- ⚖️ Antitrust trial risk (April 2025) and capex concerns ($70-72B) create uncertainty

- 🛡️ Small put position (1-2 contracts per 200 shares) provides peace of mind through January

- 💰 You've won! Protecting profits is smart money management, not bearish

Action plan:

- ✅ Sell 25-40% of META position at $665-670 levels (lock in gains, reduce risk exposure)

- 🛡️ Consider buying Jan 23 $665 or $670 puts for remaining shares (1-2 contracts per 200 shares held)

- 📊 Set mental stop at $660 (major gamma support) - if this breaks, trim further or add put protection

- 👀 Watch for buying opportunity on any pullback to $650-655 support zone to reenter trimmed position

- ⏰ Revisit in late January after puts expire and ahead of Q4 2024 earnings for repositioning

Risk level: Minimal (profit protection) | Skill level: Beginner-friendly

Expected outcome: Reduce portfolio volatility, lock in some gains, sleep better through holidays knowing downside protected. If stock consolidates or dips, you've made smart move. If it breaks out, you still have 60-75% exposure.

⚖️ Balanced: Bull Put Spread (Define Your Risk)

Play: Sell put spread targeting gamma support levels for income in consolidation scenario

Structure: Sell $665 puts, Buy $655 puts (January 23 expiration)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets strong gamma support zone at $655-$665 where dealers will defend

- 💰 Collect premium betting stock stays above $665 (strongest nearby support)

- ⏰ 36 days to expiration gives time cushion for minor pullbacks

- 📈 Base case 50% probability favors consolidation above $655-$660 support

- 🛡️ Maximum loss defined and limited if wrong about support levels

Estimated P&L:

- 💰 Collect ~$3-4 credit per spread (premium received)

- 📈 Max profit: $300-400 per spread if META stays above $665 at expiry (keep full premium)

- 📉 Max loss: $600-700 per spread if META below $655 at expiry

- 🎯 Breakeven: ~$661-662

- 📊 Risk/Reward: ~1.5:1 to 2:1 (favorable for defined-risk credit spread)

Entry timing:

- ⏰ Best to enter after tomorrow's triple witch volatility settles (Dec 20-23)

- 🎯 Enter if META trades $667-672 (at or above current levels)

- ❌ Skip if stock already testing $665 support (spread too close to short strike)

Position sizing: Risk only 3-5% of portfolio per spread. Can scale with multiple spreads if confident in support.

Management:

- 🎯 Take profit at 50-60% of max gain if reached quickly (don't be greedy)

- ⚠️ Consider closing if stock breaks below $660 with momentum (cut losses early)

- ⏰ Let expire worthless if META stays above $665 through January 23

Risk level: Moderate (defined risk, selling premium) | Skill level: Intermediate

🚀 Aggressive: Calendar Spread - Play the Consolidation (ADVANCED ONLY!)

Play: Profit from time decay and consolidation by selling near-term premium and buying longer-dated protection

Structure: Sell Dec 19 $670 calls/puts (tomorrow expiry), Buy Jan 23 $670 calls/puts (same strike)

Why this could work:

- 📉 Theta decay advantage: Dec 19 options (1 day) decay MUCH faster than Jan 23 options (36 days)

- 🎯 Consolidation play: Maximum profit if stock stays near $670 through tomorrow's expiry

- 📊 Vega advantage: If volatility drops after triple witch, helps position

- ⏰ Roll opportunity: If profitable, can roll forward the short leg week by week

- 💰 Lower cost: Calendar spreads cheaper than outright directional bets

Why this could blow up (SERIOUS RISKS):

- 🎢 Triple witch chaos: Tomorrow's expiry is quarterly triple witch - can see wild intraday swings

- 📈 Gap risk: If META gaps significantly up or down tomorrow, both legs move against you

- 💸 Assignment risk: Could be assigned on short leg if moves deep ITM before expiry

- ⚠️ Complexity: Managing a calendar through triple witch requires experience and attention

- 🕐 Time intensive: Need to actively monitor position through tomorrow's session

Estimated P&L:

- 💰 Net debit: ~$5-8 per calendar spread (difference between long and short premium)

- 📈 Max profit: $3-5 per spread if stock right at $670 tomorrow at close (short expires worthless, long retains most value)

- 📉 Max loss: ~$5-8 if stock moves far from $670 (both legs decline in value)

- 🎯 Breakeven: Stock needs to stay roughly $665-675 range for profit

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded calendar spreads before and understand time decay mechanics

- ✅ Can actively monitor position during trading hours tomorrow (triple witch requires attention!)

- ✅ Understand assignment risk on short leg if it goes ITM

- ✅ Have plan for adjusting or closing if position moves against you

- ✅ Accept that triple witch can create wild swings that blow past normal technical levels

- ⏰ Are prepared to close both legs if price action gets choppy

Risk level: EXTREME (complex strategy during high-volatility event) | Skill level: Advanced only

Probability of profit: ~45% (requires precision - stock must stay near $670 through tomorrow)

Alternative aggressive play: For those wanting directional bet, selling short-dated $680-$685 call credit spreads captures premium betting on resistance holding. But again, triple witch makes this dangerous for inexperienced traders.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Triple Witch Tomorrow (Dec 19): Quarterly options expiration creates MASSIVE volatility potential. Stock could gap $10-15 either direction based on dealer hedging flows as trillions in notional exposure expires. META could easily test $680 resistance or $655 support intraday with wild swings. Don't try to be a hero trading through triple witch unless you're very experienced.

-

💸 $70-72B Capex Concerns Growing: Meta is spending MORE on AI infrastructure than most companies' entire revenue. While Advantage+ demonstrates current AI ROI, the $70-72B 2025 capex (potentially $80B+ in 2026) is staggering - over 4x annual net income at Q1 run rate. If ad market softens or AI competition intensifies, these investments might not generate expected returns. This is THE bear case - and why institutional money is buying $10M worth of puts.

-

⚖️ Antitrust Trial in April 2025: Judge Boasberg allowed FTC case to proceed, citing "substantial evidence" of anticompetitive harm. While trial is after these puts expire, any pre-trial developments (unfavorable rulings, damaging evidence disclosure, settlement discussions) in late December or January could move stock. Potential remedies include Instagram/WhatsApp divestiture - which would be catastrophic for Meta's business model integration. This is binary legal risk that's hard to quantify.

-

🔥 Reality Labs Burning $17.73B Annually: The metaverse/VR bet has consumed $50B+ since 2019 with no profitability in sight. CTO memo calling 2025 "most critical year" determining if projects are "work of visionaries or legendary misadventure" is brutally honest about existential questions. The 30% budget cuts indicate even Meta leadership questions this strategy. Further writedowns or strategic pivots could impact sentiment.

-

🇪🇺 European Regulatory Escalation: €200M DMA fine is first under new framework with penalties up to 10% global revenue (vs 4% for GDPR). That's potentially $18B+ if violations continue. Europe showing increasing willingness to aggressively enforce Digital Markets Act and Digital Services Act. Each quarter brings new regulatory risk.

-

🐋 Smart Money Buying $10M Insurance at Peak: This institutional put purchase with 69.56x Z-score (EXTREMELY UNUSUAL) signals sophisticated players are WORRIED about near-term downside despite bullish fundamentals. When funds managing hundreds of millions pay $10M for protection at-the-money rather than staying fully long, it's a major caution flag. They're not betting on a crash - they're protecting gains against 5-10% pullback scenario.

-

📊 Resistance at $670 is MASSIVE: The 46.9B call gamma at $670 (exactly where put is struck!) is the strongest single resistance level. Market makers will systematically SELL into rallies to hedge exposure. This creates mechanical selling pressure making breakout difficult. Current price ($667-668) sitting right under this ceiling. Would need sustained institutional FOMO buying to overcome.

-

💰 Workforce Reduction Could Get Messy: 5% layoffs (~3,600 employees) with notifications by Feb 10 falls squarely in put expiration window. While markets typically like cost cutting, execution matters. Zuckerberg calling 2025 "an intense year" suggests internal pressure. Employee morale issues, key talent departures, or operational hiccups could create near-term headwinds.

-

🎯 TikTok Still Dominates Engagement: Despite Instagram Reels' $50B run rate success, TikTok holds 40% short-form video market share vs 20% for Reels with 2.50% engagement vs Instagram's 0.50% overall (Reels at 1.48%). If TikTok survives regulatory challenges, it remains formidable competition. US ban scenario is double-edged - benefits Meta but also indicates aggressive regulatory environment that could turn on Meta next.

-

📉 Year-End Positioning Risks: December historically sees reduced liquidity as funds close books for year. With META near all-time highs after strong YTD performance, tax loss harvesting in other positions or general profit-taking could create downward pressure. January effect (reinvestment) might help, but late December can get choppy.

-

🌐 Macro Headwinds if Economy Weakens: Meta derives 96%+ of revenue from advertising - highly cyclical to economic conditions. While Q1 2025 showed strong +16% YoY growth, any signs of ad market weakness in December or early January could hit stock disproportionately. Advantage+ AI tools help efficiency but don't eliminate macro sensitivity.

🎯 The Bottom Line

Real talk: Someone just spent $10 MILLION on at-the-money protection for META with the stock trading near record highs. This isn't bearish on Meta's long-term AI story or dominant social media position - it's smart risk management by institutions who've made HUGE money on the rally and want to protect those gains through a volatile period.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY through January (not crash, but protecting against normal 5-8% consolidation scenario)

- 💰 They're worried enough about $668→$650 move to pay $21/share for insurance (3.1% of stock price!)

- ⚖️ The timing (day before triple witch, 36 days to expiry) captures near-term event risk - triple witch volatility, workforce reduction notifications, antitrust developments

- 📊 They structured at-the-money at $670 - right at major gamma resistance - expecting if stock can't break through, it consolidates or pulls back

- ⏰ January 23rd expiration is BEFORE April antitrust trial but captures all near-term uncertainty

This is NOT a "sell everything" signal - it's a "protect your gains and manage risk intelligently" signal.

If you own META:

- ✅ Consider trimming 25-40% at $665-670 levels if you have large gains (lock in profits, reduce exposure)

- 📊 If holding through January, set MENTAL STOP at $660 (major gamma support) to protect remaining position

- ⏰ Don't get greedy after such a strong run - protecting capital is smart, not weak

- 🎯 If stock consolidates to $650-655 support zone, that's excellent re-entry for trimmed shares

- 🛡️ Consider buying 1-2 protective puts per 300-500 shares if holding concentrated position (copy this trade's structure but smaller size)

If you're watching from sidelines:

- ⏰ Tomorrow (Dec 19) is triple witch - expect elevated volatility but probably not ideal entry

- 🎯 Waiting for pullback to $650-660 support zone provides better risk/reward (7-10% off highs with strong gamma support)

- 📈 Looking for confirmation of: Continued AI monetization (Advantage+, Meta AI), WhatsApp business growth, Instagram maintaining 50%+ revenue share

- 🚀 Longer-term (6-12 months), Llama 4 platform adoption, Ray-Ban glasses scaling to 5M units, and WhatsApp hitting $6-7B revenue run rate are legitimate catalysts for continued upside

- ⚠️ Near-term (next 36 days), risk/reward less favorable at $667 vs $655 - patience pays

If you're bearish:

- 🎯 Don't fight the trend - META fundamentals remain strong with proven AI monetization

- 📊 First support at $665 (gamma), major support at $660 (44.2B gamma wall), deeper support at $650

- ⚠️ Put spreads ($665/$655 or $660/$650) offer defined-risk way to play consolidation/pullback scenario

- 📉 Watch for break below $660 - that's the trigger for potential cascade toward $650, then $640

- ⏰ Timing matters: Fighting into year-end and triple witch is dangerous; better to wait for technical setup

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - TOMORROW! - Quarterly Triple Witch options expiration

- 📅 December 20-31 - Holiday season reduced liquidity, tax loss harvesting period

- 📅 January 23, 2026 - Monthly OPEX, expiration of this $10M put trade

- 📅 February 10, 2025 - Deadline for 5% workforce reduction notifications

- 📅 April 14, 2025 - FTC antitrust trial begins

- 📅 April 30, 2025 - Q1 2025 earnings results (already reported with strong performance)

- 📅 Late 2025 - Llama 4 Behemoth release expected

- 📅 2027 - Orion AR glasses consumer version launch target

Final verdict: Meta's AI monetization story is REAL - $20B+ Advantage+ run rate, 700M Meta AI users, $50B Reels run rate - this isn't vaporware, it's happening NOW. BUT, at $668 near all-time highs with $670 resistance, triple witch tomorrow, $70-72B annual capex concerns, and April antitrust trial looming, the near-term risk/reward is NO LONGER heavily skewed to upside. The $10M institutional put buy with 69.56x Z-score is a CLEAR signal: smart money is derisking at the peak.

Be patient. Let triple witch clear. Look for better entry points at $650-660 if you're buying. Protect gains if you're holding. The AI advertising revolution will still be generating billions in revenue in February - and you'll sleep better buying at $655 instead of $670.

This is about capital preservation after a great run, not abandoning the thesis. Play smart. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 69.56x Z-score reflects this specific trade's size relative to recent META history - it does not imply the trade will be profitable or that you should follow it. Triple witch expiration creates elevated volatility and gap risk. The put buyer may have complex portfolio hedging needs not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading.

About Meta Platforms: Meta Platforms, Inc. is the largest social media company in the world, boasting close to 4 billion monthly active users worldwide across Facebook, Instagram, Messenger, and WhatsApp. The company monetizes through targeted advertising and is investing heavily in AI and Reality Labs (AR/VR technologies), with a market cap of $1.64 trillion in the Computer Programming, Data Processing & Services industry.