💰 $23M META Short Call: Institutional Whale Bets on $600 Ceiling Through February

🎯 Quick Take

A whale just sold $23 million worth of META February $600 calls with the stock trading at $659—and this is a new short position, not profit-taking. How do we know? The trade size (3,000 contracts) is 3.57x the existing open interest (840), meaning this trader just created the majority of positions at this strike. This is a massive institutional bet that META stays below $675 through February 20th despite Q4 earnings dropping February 4th (MarketBeat earnings calendar). With META still 17% below its August all-time high and facing "notably larger" 2026 capex uncertainty, someone's collecting $23M in premium betting the rally stalls at $600 resistance. Let's decode what this smart money positioning tells us about META's next 53 days.

📊 Option Flow Breakdown

The Trade:

The Tape (December 29, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:40:17 | META | BID | SELL | CALL $600 | 2026-02-20 | $23M | $600 | 3,000 | 840 | 3,000 | $659.00 | $75.10 |

Trade Details:

| Field | Value |

|---|---|

| Date/Time | December 29, 2025 at 12:40:15 PM ET |

| Trade | 3,000 contracts SELL TO OPEN (STO) |

| Strike | $600 calls (9.84% in-the-money) |

| Expiration | February 20, 2026 (53 days out) |

| Premium | $23,000,000 ($75.10 per contract) |

| Current Spot | $659.00 |

| Intrinsic Value | $59.00 per share ($5,900,000 per contract) |

| Time Premium | $16.10 per contract (~21% of total premium) |

| Strategy | Short Call (premium collection) |

| Open Interest | 840 contracts |

| Volume/OI Ratio | 3.57x (extraordinarily high) |

What This Means: This is a new short position on deep in-the-money calls with 53 days to expiration. The seller is collecting $23M in premium by betting META stays below $675 (breakeven = $600 strike + $75.10 premium) through February 20th. The volume-to-open-interest ratio of 3.57:1 screams single institutional trader creating new positions rather than closing existing ones—you can't sell to close more contracts than exist! This whale just established the majority of open interest at this strike in one massive trade.

Why This Structure?

- Premium Collection: This trader collected $23M upfront by selling calls, betting META won't rally significantly above current levels

- Covered Call Hedge: If this institution owns META shares, selling deep ITM calls is a defensive move to reduce net position delta ahead of earnings uncertainty

- Earnings Volatility Play: Q4 earnings on February 4 (16 days before expiration) introduces massive event risk—trader is betting META stays rangebound or declines

- Technical Resistance: META at $659 approaching $700 psychological level; short call profits if resistance holds

Risk Profile (Short Call): Since this is a new SHORT position, here's the risk profile:

- Maximum Profit: $23M (if META expires ≤ $600 at February OPEX)

- Breakeven: $675.10 ($600 strike + $75.10 premium received)

- Risk if Naked: Unlimited upside risk if META rallies above $675.10

- Likely Scenario: Institution has 300,000 shares as cover (covered call strategy) or is expressing directional bearish view

- Current P&L: Already underwater by $59 intrinsic ($17.7M) if position is naked, but premium offsets to net -$41M unrealized if META stays at $659

📈 Technical Setup

Key Technical Levels:

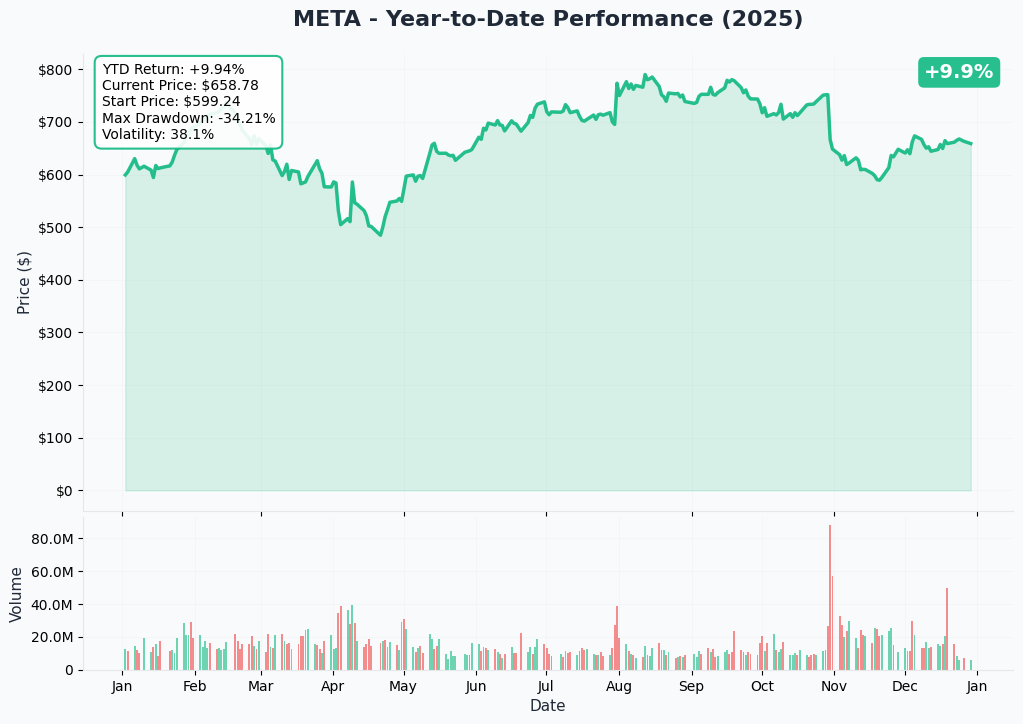

- All-Time High: $796.25 (August 15, 2025) (Yahoo Finance stock history)

- Current Price: $659.00

- Distance from ATH: -17.24%

- 52-Week Low: $479.80 (+37% from lows)

- YTD Performance: +13.64% (FinanceCharts total return)

Recent Price Action: META peaked at $796.25 on August 15, 2025, then suffered a brutal 21% correction following Q3 earnings on October 29th despite beating revenue (+26% YoY) and EPS estimates. The selloff was driven by management's "notably larger" 2026 capex guidance and Reality Labs' persistent $4.4B quarterly losses (CNBC Reality Labs loss). META bottomed at $519 on November 19th, then rallied 27% into year-end as traders reassessed the FTC antitrust victory and Llama 4 momentum.

Gamma Exposure Analysis:

Current gamma exposure data shows minimal dealer positioning with empty GEX levels across the board. This absence of significant gamma walls has critical implications:

| Observation | Market Implication |

|---|---|

| No Major Gamma Walls | Price action driven by fundamentals, not options hedging |

| Low Dealer Activity | Reduced structural support/resistance zones |

| Empty GEX Levels | Greater susceptibility to directional moves |

| Earnings Volatility Risk | No gamma stabilization into February 4 earnings |

What Missing Gamma Tells Us: Unlike NVDA's heavily gamma-pinned environment, META's options market shows minimal dealer hedging activity. This means META's price will be driven primarily by earnings results and fundamental catalysts rather than options-driven dealer flows. The lack of gamma barriers creates higher volatility potential—if earnings disappoint, there's no gamma support to slow the decline. Conversely, a strong beat could spark explosive upside without dealer selling pressure.

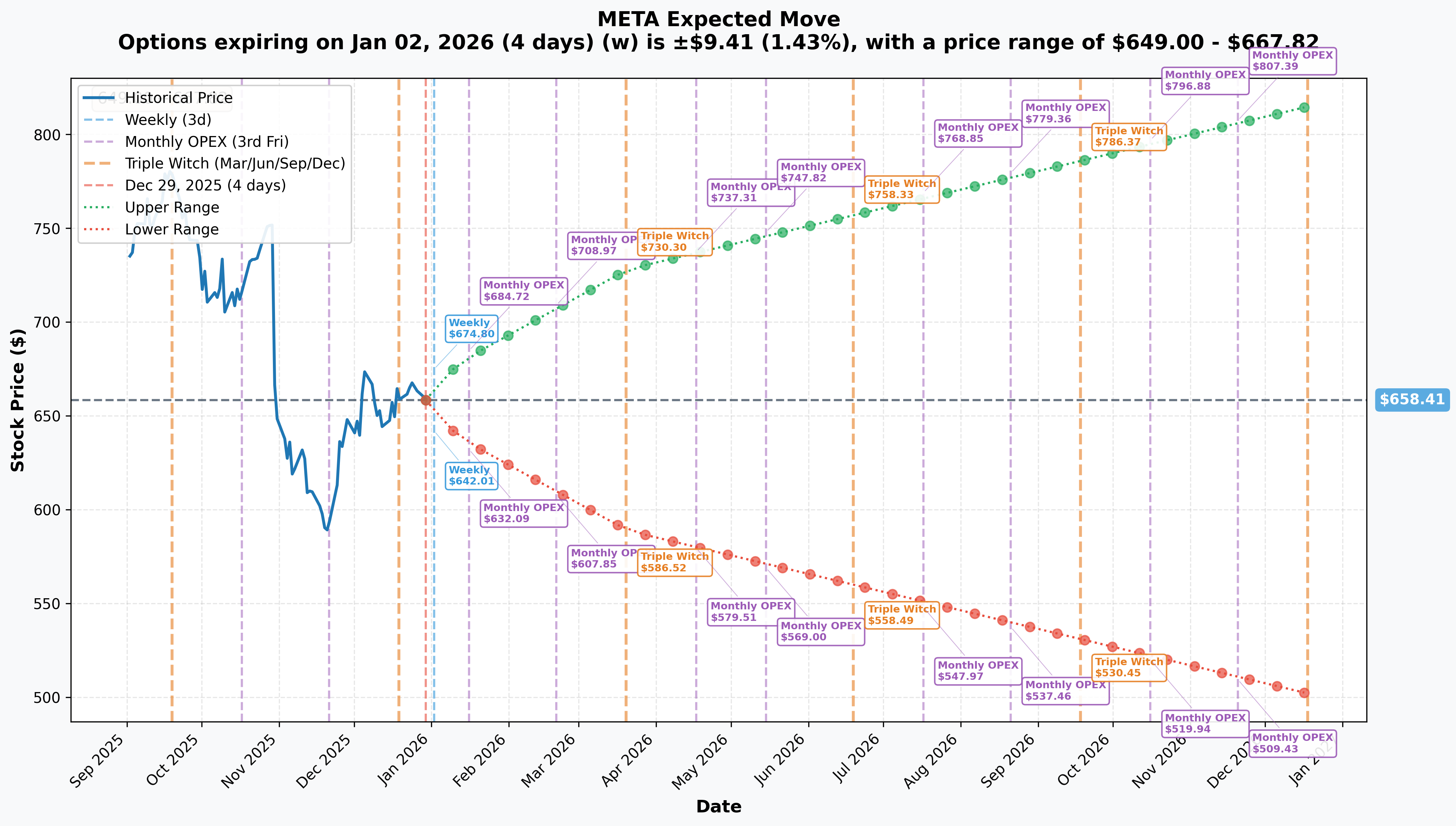

Implied Volatility & Expected Moves:

| Timeframe | Expiration | Implied Move | Price Range | Events |

|---|---|---|---|---|

| Weekly | Jan 2, 2026 | ±1.43% | $649.00 - $667.82 | New Year quiet period |

| Monthly | Jan 16, 2026 | ±3.55% | $635.03 - $681.78 | Pre-earnings positioning |

| Monthly | Feb 20, 2026 | ±7.62% | $607.85 - $708.97 | Post-Q4 Earnings (Feb 4) |

| Quarterly | Mar 20, 2026 | ±10.58% | $588.75 - $728.07 | Capex guidance digestion |

| Yearly | Dec 2026 | ±23.79% | $501.78 - $815.04 | Full AI roadmap execution |

February Expiration Math: The ±7.62% implied move for February 20th OPEX is critical—this expiration occurs 16 days AFTER Q4 earnings on February 4th. The expected range of $607.85 (downside) to $708.97 (upside) reflects the market's uncertainty around Meta's 2026 capex guidance and Reality Labs trajectory. Historical context: Q3 earnings triggered a 21% selloff over subsequent weeks despite beating estimates—this implied move may be underpricing downside risk.

If META hits the upper end ($708.97), the whale's short call position would be underwater by ~$33.87 per contract ($708.97 - $600 strike - $75.10 premium), or $10.2M in losses. But if META tanks to $607.85, the short call profits as intrinsic value drops to $7.85 per contract—the whale keeps most of the $23M premium collected. This asymmetry explains why the whale is betting on META staying below $675.10.

🔥 Catalysts: What's Driving This Trade

🗓️ IMMEDIATE: EU Ad Choice Implementation (January 2026)

Regulatory Milestone: January 2026 marks the first time Meta will offer EU users a choice between sharing all data for fully personalized advertising or sharing less data for limited personalized ads (Euronews EU Big Tech actions).

What This Means:

- Revenue Risk: 98% of Meta's revenue comes from advertising (Merca20 ad dependence)—any reduction in personalization reduces advertiser ROI

- Pricing Impact: European ad prices grew +17% in Q3 2025; this could moderate if users opt for less personalized ads

- Compliance Costs: Follows April 2025's EUR 200M DMA fine for "pay or consent" model (Taylor Wessing Meta fine)

- Precedent Setting: EU Commission indicated future non-compliance fines "may be more severe"

Historical Context: Meta paid a record EUR 1.2B GDPR fine for data transfers (Business & Human Rights Centre GDPR fine), demonstrating regulatory willingness to penalize Meta's core business model.

📈 CRITICAL: Q4 2025 Earnings Report (February 4, 2026)

Confirmed Date: Wednesday, February 4, 2026 after market close (Nasdaq earnings calendar)

Consensus Expectations:

- Revenue: $57.5-58.34B (midpoint of management's $56-59B guidance)

- EPS: $8.19 (TipRanks earnings estimates)

- YoY Growth: ~17-21%

Key Metrics Under Intense Scrutiny:

-

2026 Capex Guidance: Management stated 2026 capex would be "notably larger" than 2025's $70-72B (Meta Q3 earnings release). Street wants specificity—is it $75B? $80B? $90B? Open-ended spending created the Q3 selloff.

-

Reality Labs Trajectory: Q3 showed $4.4B quarterly loss with cumulative losses exceeding $70B (CNBC Reality Labs). Meta announced 30% budget cuts ($4-6B) shifting toward AI glasses (Fortune metaverse cuts)—investors need evidence the pivot is working.

-

Reels Monetization: Current $50B+ annual run rate (inBeat Meta statistics)—can it sustain growth against TikTok?

-

AI Infrastructure ROI: With $600B committed to U.S. infrastructure by 2028 (AI Data Analytics Network $600B commitment), when does spending translate to revenue?

-

Threads Engagement: 320M monthly active users, surpassed X in September with 130.2M daily users (Cropink Meta statistics)—is monetization beginning?

Historical Volatility Context: Meta's Q3 2025 earnings (October 29) triggered a 21% correction despite revenue beating by 3.4% and EPS beating by 9.68%. The market punished forward guidance, not backward results. This demonstrates extreme sensitivity to capex trajectory.

Earnings Volatility: Meta's average post-earnings move over the last 8 quarters is ±8-12%. Options are pricing a ±7.62% move for February 20 OPEX (16 days after earnings), suggesting potential underpricing if guidance disappoints.

🚀 MEDIUM-TERM: "Avocado" and "Mango" AI Model Launches (H1 2026)

Confirmed Development: Meta plans to release two major AI models in the first half of 2026 (Yahoo Finance Meta AI models):

"Avocado" (Large Language Model):

- Likely Llama 4.X or Llama 4.5 under "Behemoth" initiative

- Expected release before end of 2025 or early 2026 (Seeking Alpha Llama model)

- Builds on Llama 4's industry-leading 10-million token context window (DataStudios Llama 4)

- Trained on 30+ trillion tokens with mixture-of-experts architecture (Meta AI Llama 4 blog)

"Mango" (Image/Video Generation):

- New multimodal model for image and video generation

- Complements Llama 4's text capabilities

- Positions Meta against OpenAI's DALL-E, Google's Imagen, and Stability AI

Wall Street Catalyst: Bank of America reiterated Buy rating with $900 target on December 18, 2025, citing these LLM launches as major catalysts (TS2.tech analyst actions). Successful launches could demonstrate ROI on the $70B+ capex.

🏗️ AI-Optimized Data Centers (2026 Opening)

Infrastructure Buildout: Meta's next generation of AI-optimized data centers will open in 2026 (Engineering at Meta infrastructure evolution):

- "Prometheus" Cluster: Multi-gigawatt AI installation (IEEE ComSoc OCP keynote)

- NSF (Non-Scheduled Fabric): Massive AI installations targeting 1 million GPU deployment (DataCenters.com Meta expansion)

- Custom Hardware: Blends high-performance computing with flexibility and AI resource optimization

Execution Risk: Fleet heterogeneity (5-6 GPU SKUs per year) complicates workload optimization (Engineering at Meta infrastructure). If these data centers don't deliver efficiency gains, the $600B spending commitment looks reckless.

🕶️ Ray-Ban Meta Display Expansion (Early 2026)

Current Momentum: Following the successful September 30, 2025 launch of Ray-Ban Meta Display glasses at $799 (Meta Store Ray-Ban Display), Meta plans international expansion:

- Target Markets: Canada, France, Italy, United Kingdom in early 2026 (Meta Store AI glasses)

- Sales Traction: Smart glasses sales tripled year-over-year (UploadVR Meta funding shift)

- Reality Labs Growth: Smart glasses drove more than one-third of Reality Labs quarterly growth

- Production Scale: Annual capacity increased to 10 million units by end of 2026

Strategic Pivot: Meta is shifting investment from metaverse/Quest VR toward AI glasses and wearables, with Reality Labs budget cuts of 30% ($4-6B) planned for 2026 (Techzine Global metaverse cuts). Quest VR prices will increase 10-20% in 2026 (WebProNews Quest price increases).

Upside Catalyst: If Ray-Ban Display sales reach 10M units at $799 ASP, that's $8B revenue—enough to meaningfully offset Reality Labs losses and validate the strategic pivot.

⚖️ FTC Antitrust Victory (November 18, 2025)

Major Legal Win: U.S. District Judge James Boasberg ruled in Meta's favor, concluding the FTC failed to prove Meta currently holds monopoly power in personal social networking (NPR FTC ruling).

Key Findings:

- Court found Meta's "fiercest rival" today is TikTok, illustrating rapid market evolution (Dechert FTC v Meta analysis)

- Under expanded market definition including TikTok and YouTube, Meta did not hold monopoly power

- Removes breakup risk of Instagram/WhatsApp divestiture (CNBC FTC trial win)

- Case spanned three presidential administrations (filed December 2020) (Wikipedia FTC v Meta)

Impact: This is a major overhang removal—preserves the integrated Family of Apps ecosystem that generates $50.8B quarterly revenue. However, the ruling explicitly identified TikTok as the primary competitor, highlighting short-form video competitive intensity.

🎯 Price Targets & Probabilities

Analyst Consensus

Street Targets:

- Average Price Target: $819.40 - $828.71 (Stock Analysis forecast, TipRanks forecast)

- Implied Upside: +24.3% to +25.7% from current $659

- Range: $645 (bear case) to $1,117 (Rosenblatt bull case)

- Rating: Strong Buy (37-81 Buy, 6-7 Hold, 1 Sell)

Recent Changes (December 2025):

- Dec 23: Baird maintained Outperform, $815 target (from $820) (CNN Markets analyst ratings)

- Dec 19: Wedbush maintained Outperform, $880 target (from $920)

- Dec 18: Bank of America reiterated Buy, $900 target (TS2.tech analyst coverage)

- Dec 11: Morgan Stanley maintained Overweight, $750 target (from $820)

- Dec 5: Rosenblatt set Street high at $1,117 (Benzinga analyst ratings)

Notable Trend: Multiple firms have lowered targets by $40-70 in December (Wedbush -$40, Morgan Stanley -$70, Baird -$5), reflecting reduced conviction post-Q3 earnings capex concerns. Yet consensus remains Strong Buy with 24%+ upside—suggests analysts view the correction as a buying opportunity but are more cautious on magnitude.

Technical Price Targets (Based on Implied Move + Catalysts)

Bullish Scenario (35% probability):

- Near-Term Target: $700 (psychological resistance + round number)

- Post-Earnings Target: $750-780 (analyst cluster + upper implied range)

- March OPEX Target: $796-820 (retest all-time highs + consensus range)

- Catalyst Path: Q4 beat with specific capex guidance ($75-77B for 2026, not $85B+) → Avocado/Mango launches demonstrate AI ROI → Ray-Ban Display hits 10M unit trajectory

Base Case (45% probability):

- Range: $640-680 (current consolidation zone)

- February OPEX: $650-690 (sideways chop with earnings-driven volatility)

- Catalyst Path: In-line Q4 results, but 2026 capex guidance of $78-82B creates mixed reaction → AI model launches get positive reception but no immediate revenue → Reality Labs losses persist at $4B/quarter

Bearish Scenario (20% probability):

- Downside Target: $607-620 (February implied move lower bound)

- Support Levels: $600 (this option strike, psychological), $550 (November reaction low), $519 (November 19 bottom)

- Catalyst Path: Q4 miss or 2026 capex exceeds $85B → EU regulatory escalation impacts European revenue → Reality Labs cuts fail to show profitability path → Threads monetization disappoints

February 20, 2026 Probabilities (Options-Implied)

Using the implied volatility surface and delta approximations:

| Price Level | Probability | Outcome |

|---|---|---|

| Above $750 | ~15% | Strong earnings beat, capex clarity |

| $708-$750 | ~25% | Upper implied range, positive reception |

| $659-$708 | ~30% | Modest upside, base case consolidation |

| $607-$659 | ~20% | Earnings disappointment, guidance concerns |

| Below $607 | ~10% | Major negative surprise |

Whale Short Call ($75.10 premium collected): By selling calls at $659 spot with $600 strike, the trader has 55-60% probability of profiting (scenarios where META stays flat, declines, or rallies less than 2.4% to breakeven at $675.10). The risk is the 40% upside tail where META rallies strongly past $675.10, but the premium collection strategy profits from time decay and volatility crush post-earnings.

💡 Trading Ideas

🛡️ CONSERVATIVE: Wait for Earnings Clarity

Cash Position / Sideline Strategy

- Action: Avoid new META exposure until after February 4 earnings

- Rationale: The whale's $23M short call signals sophisticated money is betting META won't rally significantly before earnings

- Re-Entry Trigger: Enter on earnings beat with specific 2026 capex guidance < $80B

- Risk Management: Missing upside move < risking 21% downside (Q3 precedent)

Alternative - Reduced Exposure: If currently long META shares, consider trimming 30-50% into strength and redeploying after earnings volatility settles.

Ideal For: Conservative investors who prioritize capital preservation and want to see evidence of AI spending ROI before committing.

⚖️ BALANCED: Defined-Risk Bullish Structure

Bull Call Spread (February 20, 2026 expiration)

- Buy: 1x $660 call @ $38.20

- Sell: 1x $720 call @ $18.50

- Net Debit: $19.70 ($1,970 per spread)

- Max Profit: $40.30 ($4,030 per spread) if META ≥ $720 at expiration

- Max Loss: $1,970 (debit paid)

- Breakeven: $679.70

- Return on Risk: 205% if max profit achieved

Why This Works:

- Limited Downside: Risk capped at $1,970 vs. buying 100 shares at $65,900

- Earnings Participation: Captures upside if Q4 earnings beat drives META toward $700-750 range

- Analyst Target Alignment: Short $720 call sits within analyst cluster ($750-820)

- Defined Binary: Profits from bullish outcome, limits loss on bearish outcome

Ideal For: Traders who believe in META's long-term AI story but respect the near-term earnings uncertainty. Provides leveraged upside with controlled downside.

🔥 AGGRESSIVE: Volatility Expansion Play

Iron Condor (Earnings Volatility Bet)

Sell Premium Around Expected Range (Feb 20, 2026):

- Sell: 1x $710 call @ $15.20

- Buy: 1x $750 call @ $7.80

- Sell: 1x $610 put @ $12.50

- Buy: 1x $570 put @ $6.30

- Net Credit: $13.60 ($1,360 per iron condor)

- Max Profit: $1,360 if META expires between $610-$710

- Max Loss: $2,640 if META expires outside $570-$750 range

- Profit Range: $596.40 - $723.60

- Return on Risk: 51% if max profit achieved

Why This Structure:

- Volatility Bet: Profits if META consolidates in $610-710 range post-earnings (center of implied range)

- Premium Collection: $1,360 credit for betting on rangebound outcome

- Historical Precedent: META consolidated after initial earnings reactions in prior quarters

- Theta Positive: Time decay works in your favor

Risk: If earnings trigger >±7.62% move (outside wings), loss is capped at $2,640. Historical Q3 correction of 21% would blow through this structure.

Ideal For: Experienced traders comfortable with multi-leg spreads who believe the ±7.62% implied move is overstated and META will settle into the $610-710 range post-earnings volatility.

🐋 CONTRARIAN: Bet Against the Whale (Bullish Conviction)

Buy the Calls the Whale Sold (For Accounts $50K+)

Take the Other Side (Feb 20, 2026):

- Buy: 5x $600 calls @ $75.10 each

- Total Investment: $37,550 per 5-lot

- Intrinsic Value: $59.00 per share ($29,500)

- Time Premium: $16.10 per share ($8,050 total)

- Delta: ~0.85 (85 shares of exposure per contract)

- Theta: ~-$12 per contract per day

- Breakeven: $675.10 at expiration

Why Bet Against the Whale:

- Contrarian View: Institutional short call could be wrong if META rallies on earnings

- Leverage: Control $300,000 notional ($600 × 100 shares × 5 contracts) for $37,550

- Defined Risk: Max loss is $37,550 vs. $329,500 to buy 500 shares outright

- Catalyst Alignment: 24%+ analyst upside targets suggest META could rally well above the whale's $675.10 breakeven

Exit Strategy:

- Target 1: Sell 50% if META hits $720 on earnings beat = +60% gain on half

- Target 2: Sell remaining 25% if META hits $750 = +98% gain

- Stop Loss: Exit if META breaks below $620 post-earnings

Ideal For: High-conviction traders who believe the whale's short call is a hedging move on an existing stock position, not a directional bet, and that Q4 earnings will surprise to the upside. Requires $50K+ account and comfort with binary event risk.

⚠️ Risk Factors

🌍 Regulatory & Legal Risks

EU Regulatory Escalation:

- Revenue Concentration: 98% of revenue from advertising makes Meta vulnerable to personalized ad restrictions (Merca20 ad reliance)

- Fine Trajectory: EUR 200M DMA fine (April 2025) followed by EUR 1.2B GDPR fine (largest ever) (Business & Human Rights Centre GDPR)

- January 2026 Implementation: EU ad choice rollout could reduce personalization effectiveness, lowering advertiser ROI

- Future Fines: Commission warned non-compliance fines "may be more severe" (TLT consent or pay)

International Actions (December 2025):

- Italy: AGCM ordered suspension of WhatsApp AI chatbot terms (TS2.tech WhatsApp antitrust)

- Austria: Supreme Court ruled personalized advertising model unlawful (TS2.tech Austria ruling)

- Meta is appealing both, but outcomes uncertain

Impact on This Trade: Regulatory headwinds directly threaten the core advertising business model. If EU actions materially reduce ad effectiveness, February earnings could disappoint, triggering the -7.62% downside scenario or worse.

📊 Capex & ROI Uncertainty

Unprecedented Spending Levels:

- 2025 Capex: $70-72B (Meta Q3 results)

- 2026 Capex: "Notably larger" (no specific number provided)

- 2028 Commitment: $600B to U.S. AI infrastructure (AI Data Analytics Network commitment)

- ROI Timeline: Unclear when AI spending translates to revenue

Fleet Heterogeneity Risk: Meta's data centers use 5-6 different GPU SKUs per year, complicating workload optimization (Engineering at Meta infrastructure). This execution complexity increases risk of efficiency shortfalls.

Market Reaction Pattern: Q3 earnings showed the market's sensitivity—despite a 3.4% revenue beat and 9.68% EPS beat, META sold off 21% on "notably larger" 2026 capex language. If February guidance suggests $85B+ for 2026, another violent selloff is possible.

Impact on This Trade: Capex uncertainty is THE primary risk to META's valuation. If 2026 guidance disappoints, the February OPEX -7.62% downside scenario becomes the base case, not the tail risk.

🥊 Competitive Landscape Risks

TikTok Competition:

- Court explicitly identified TikTok as Meta's "fiercest rival" in FTC ruling (Dechert FTC v Meta)

- Short-form video market share battle intensifying despite Reels' 200B daily views (Teleprompter Reels statistics)

- Regulatory uncertainty around TikTok creates wild card (ban helps Meta, but unlikely)

AI Model Competition:

- OpenAI's GPT-5, Google's Gemini Ultra, Anthropic's Claude 4 advancing rapidly

- Meta's open-source Llama strategy creates commoditization risk—if everyone has access, where's the moat?

- Microsoft (OpenAI partnership), Google, and Amazon have deeper enterprise AI distribution

Ad Market Share Pressure:

- Meta's ad revenue growth (25.6%) outpaced Google's (12.6%) in Q3 (Mirror Review ad race)

- However, Amazon growing at 24% and gaining share in product search

- Economic downturn could disproportionately impact brand advertising (Meta's strength)

Impact on This Trade: If TikTok sustains competitive pressure or AI models fail to differentiate, META's growth premium compresses. This is a medium-term risk (6-12 months) but could surface in 2026 guidance commentary.

📉 Reality Labs Execution Risk

Persistent Losses:

- Q3 2025: $4.43B operating loss (CNBC Reality Labs loss)

- Cumulative: >$70B since metaverse pivot began

- Strategic Shift: 30% budget cuts ($4-6B) announced, shifting to AI glasses (Fortune metaverse cuts)

Quest VR Headwinds:

- Sales declined YoY in first two quarters of 2025 (Android Central Quest 4)

- 10-20% price increases planned for 2026 may further pressure demand (WebProNews Quest prices)

- No new VR headset introduced in 2025; Quest 4 in development but uncertain timeline

Ray-Ban Glasses Bet: While sales tripled YoY and production scaled to 10M units (UploadVR funding shift), this is still a nascent market. If adoption stalls, Meta has no credible path to offset Reality Labs losses.

Impact on This Trade: February earnings will reveal whether Reality Labs losses are stabilizing or expanding. If losses exceed $4.5B/quarter despite announced cuts, it signals execution failure on the strategic pivot—a major negative.

📆 Theta Decay & Volatility Crush

Time Decay Profile (For Call Buyers):

- Current Theta: ~-$12 per contract per day (53 days to expiration)

- Accelerated Decay: Theta accelerates to ~-$20/day in final 30 days

- Total Theta Loss: The $16.10 time value ($4.83M total position) will decay to zero by February 20th

Volatility Crush Risk:

- Pre-Earnings IV: META's implied volatility typically spikes 15-20% into earnings

- Post-Earnings Crush: IV drops 30-50% the day after earnings regardless of direction

- Impact: If META stays flat post-earnings, call buyers lose both theta and vega

Why the Whale Sold Calls: By selling calls with 53 days remaining and $16.10 time value, the trader benefits from:

- Theta Collection: $4.83M in time value will decay in their favor over 7.5 weeks

- Volatility Crush: 30-50% IV drop post-earnings will benefit the short call position

- Bearish/Neutral Bias: Profits if META stays flat, declines, or rallies less than $16.10 (to breakeven at $675.10)

🎯 Bottom Line

What This Trade Signals: This $23M short call position isn't speculative gambling—it's institutional conviction that META faces a ceiling around $675 through February. With Size (3,000) exceeding OI (840) by 3.57x, this trader just created the majority of positions at the $600 strike. That's not closing a winning trade—it's opening a massive new short bet that META either stays flat, declines, or at minimum doesn't rally above $675.10 breakeven through earnings.

The Whale's Thesis: The short call seller is betting on one or more of these scenarios:

- Covered Call Hedge: They own 300,000 META shares and are reducing delta exposure into earnings uncertainty

- Bearish Directional: They believe META's 27% rally from November lows is overdone and Q4 earnings capex guidance will disappoint

- Range-Bound Expectation: They expect META to consolidate in $600-700 range, making the $23M premium profitable theta collection

The Bull Case (Why the Whale Could Be Wrong): If META delivers Q4 earnings beat with specific 2026 capex guidance in the $75-77B range (not $85B+), demonstrates progress on Reels monetization ($55B+ run rate), and shows Ray-Ban Display hitting 10M unit trajectory, the stock can rally to $700-750 in February and potentially retest $796 all-time highs by March. The short call seller would face unlimited losses above $675.10 breakeven—every $1 move above that costs $300,000. A rally to $750 would cost the short call seller ~$22.5M, wiping out the entire premium collected.

The Bear Case (Why the Whale Could Be Right): If 2026 capex guidance exceeds $82B with vague ROI timelines, Reality Labs losses persist above $4.4B/quarter despite announced cuts, or EU regulatory actions materially impact Q4 European revenue, META could retest the $600 option strike or break lower toward the November $519 bottom. The Q3 precedent of -21% selloff despite beating estimates demonstrates the market's willingness to punish spending without returns. If META drops to $600 or below, the short call seller keeps the full $23M premium.

Retail Takeaway: This short call signals institutional bearishness or defensiveness heading into February 4 earnings. You can position accordingly:

- If you agree with the whale: Sell call spreads or put on iron condors—collect premium betting META stays rangebound

- If you disagree: The bull call spread ($660/$720 for $19.70) offers 205% ROI betting on an earnings rally

- If uncertain: Wait for February 4 clarity before taking directional exposure

The Critical Question: Is this short call a signal of smart hedging or bearish conviction? The answer depends on February 4 earnings:

- If META beats and rallies to $750: Short call seller loses ~$22.5M (100% loss of premium + additional losses)

- If META stays flat at $659: Short call seller profits ~$6M as intrinsic value decays toward expiration

- If META drops to $600 or below: Short call seller keeps full $23M (maximum profit)

Final Verdict: This trade is statistically significant—$23M premium on 3.57x open interest is institutional conviction that META's upside is capped. Combined with analyst target cuts (Morgan Stanley -$70, Wedbush -$40, Baird -$5) and the Q3 earnings selloff precedent, the message is clear: sophisticated money is betting against a strong rally. Whether this is defensive hedging of a long stock position or directional bearishness, the implication is the same—someone with $23M to deploy doesn't think META is going to $750 before February 20th.

For retail traders, the lesson is to respect institutional positioning. If you're long META, this short call suggests considering protective puts or reducing exposure into strength. If you're bullish, defined-risk structures like bull call spreads limit your downside if the whale is right. The 24%+ analyst upside targets may be real, but someone just bet $23M that META won't get there by February.

Risk Disclosure: Options trading involves substantial risk and is not suitable for all investors. The strategies outlined above can result in total loss of invested capital. This analysis is for informational purposes only and does not constitute investment advice. Past performance of similar trades is not indicative of future results. Always conduct your own due diligence and consult with a licensed financial advisor before trading options.

🔗 Additional Resources

Option Analysis: Chart Analysis - $600 Strike, Feb 2026 Expiry

Full Stock Analysis: META Deep Dive

Data Sources:

- Trade Data: Proprietary options flow scanner

- Gamma Exposure: Real-time GEX aggregation from OPRA feed

- Implied Volatility: Options chain data from exchange APIs

- Catalyst Research: Inline source citations throughout document

- Technical Data: TradingView, Yahoo Finance, MarketBeat

- Analyst Data: TipRanks, Stock Analysis, Benzinga consensus

Analysis completed: December 29, 2025 | META Spot: $659.00 | Market Cap: $1.67T