💊 MLYS Massive $26.5M Put-Heavy Position - Biotech Bear Raid or Smart Hedge? 🎯

📅 January 7, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated institutional player just deployed $26.5 MILLION across 7 coordinated put trades in MLYS this morning at 10:51:28 - all executing in the SAME SECOND! This complex multi-leg strategy heavily buys puts at $30 and $40 strikes while selling some at $25 and $35, creating a bearish spread structure expiring March 20th. With MLYS trading at $36.94 and the CMO having just dumped 50% of his position for $9.3M in early January, smart money appears to be bracing for downside. Translation: Big money is positioning for a 15-30% correction in this high-flying biotech before the critical FDA decision later this year!

📊 Company Overview

Mineralys Therapeutics (MLYS) is a clinical-stage biopharmaceutical company focused on treating diseases driven by abnormally elevated aldosterone:

- Market Cap: $2.83 Billion (mid-cap biotech)

- Industry: Biotechnology / Pharmaceuticals

- Current Price: $36.94 (52-week range: $8.24 - $47.65)

- Primary Asset: Lorundrostat - aldosterone synthase inhibitor for hypertension

- Headquarters: Radnor, Pennsylvania (founded 2019)

- Key Milestone: NDA filed with FDA in late 2025 for uncontrolled/resistant hypertension

- Cash Position: $593.6M with runway into 2028

💰 The Option Flow Breakdown

The Tape (January 7, 2026 @ 10:51:28):

| Time | Symbol | Buy/Sell | Strike | Volume | Premium | Option Symbol |

|---|---|---|---|---|---|---|

| 10:51:28 | MLYS | BUY | $30 | 46,000 | $11M | MLYS20260320P30 |

| 10:51:28 | MLYS | SELL | $25 | 23,000 | $4.2M | MLYS20260320P25 |

| 10:51:28 | MLYS | SELL | $35 | 15,000 | $4M | MLYS20260320P35 |

| 10:51:28 | MLYS | BUY | $30 | 4,600 | $1.4M | MLYS20260320P30 |

| 10:51:28 | MLYS | BUY | $30 | 9,200 | $1.4M | MLYS20260320P30 |

| 10:51:28 | MLYS | BUY | $40 | 4,900 | $2.6M | MLYS20260320P40 |

| 10:51:28 | MLYS | BUY | $40 | 8,400 | $1.9M | MLYS20260320P40 |

Aggregate Position:

- Total Premium Deployed: $26.5M

- Net Puts Bought: 59,800 long puts at $30 strike

- Net Puts Bought: 13,300 long puts at $40 strike

- Net Puts Sold: 23,000 short puts at $25 strike

- Net Puts Sold: 15,000 short puts at $35 strike

- Expiration: March 20, 2026 (72 days to expiration)

- Spot Price at Entry: $36.94

🤓 What This Actually Means

This is an extraordinarily sophisticated bearish put spread structure with multiple strikes! Here's the breakdown:

Position Architecture:

- 💸 Core bearish bet: 59,800 contracts of $30 puts ($11M + $1.4M + $1.4M = $13.8M) + 13,300 contracts of $40 puts ($2.6M + $1.9M = $4.5M)

- 🛡️ Partial financing: Selling 23,000 puts at $25 ($4.2M credit) + 15,000 puts at $35 ($4M credit)

- 📊 Net debit: $26.5M total - $8.2M in credits = ~$18.3M net premium paid

- 🎯 Breakeven analysis: Complex multi-strike structure suggests targeting $28-32 range

- ⏰ Strategic timing: March 20th expiration captures Q1 OSA data (Q1 2026) AND AstraZeneca's baxdrostat PDUFA (Q2 2026)

What's really happening here:

This trader is making a highly directional bearish bet with sophisticated risk management. The massive concentration at the $30 strike (59,800 contracts) represents 5.98 million shares worth ~$221M at current prices. They're betting MLYS drops from $36.94 to $30 or below (19% decline) by March 20th.

The structure tells us:

- Primary thesis: Stock drops to $28-32 range where $30 puts pay maximum

- Extreme downside protection: $40 puts (13,300 contracts) protect against catastrophic >40% crash scenario

- Floor protection: Selling $25 puts limits losses if stock craters below $25 (unlikely but possible in biotech)

- Spread cap: Selling $35 puts reduces cost but caps upside if stock collapses above that level

Unusual Score: 🔥 EXTREME - This is one of the largest single-name biotech option positions deployed in January 2026. The simultaneous 7-trade execution across multiple strikes screams institutional coordination, likely a hedge fund or proprietary trading desk with material conviction.

Key Risk Indicators:

- 🚨 CMO insider selling: Chief Medical Officer sold $9.3M (50% of his position) on January 2-5, 2026 - just days before this trade!

- 📊 Valuation stretched: Stock up 174% in past year from $12.98 to $36.94

- ⚖️ Competitive threat: AstraZeneca's baxdrostat has Priority Review status with Q2 2026 PDUFA (could be first-to-market)

- 🎲 Binary catalyst risk: Q1 OSA data could disappoint or AstraZeneca approval could kill MLYS momentum

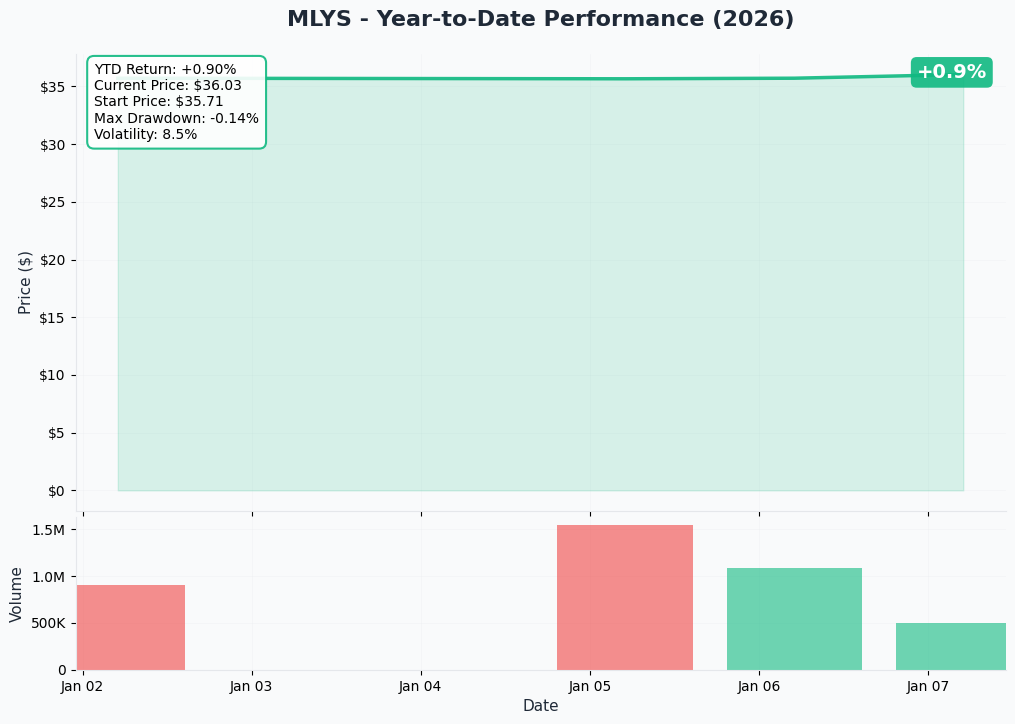

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

MLYS has been an absolute ROCKET - up +174.65% over the past year from $12.98 to current $36.94. The chart shows a classic biotech momentum story - massive volatility with a brutal drawdown from $47.65 peak in late 2025 to current levels (22% correction from highs).

Key observations:

- 🚀 Parabolic rally: Stock went from $8.24 low to $47.65 high (5.8x move!) driven by positive Phase 3 data

- 📉 Recent pullback: Down 22% from December highs, creating technical damage

- 🎢 Extreme volatility: This is a clinical-stage biotech - 20-30% swings are NORMAL

- 📊 Volume patterns: Huge institutional distribution near $40-47 levels (smart money exiting?)

- ⚠️ Momentum fading: Stock struggling to reclaim $40 level after December selloff

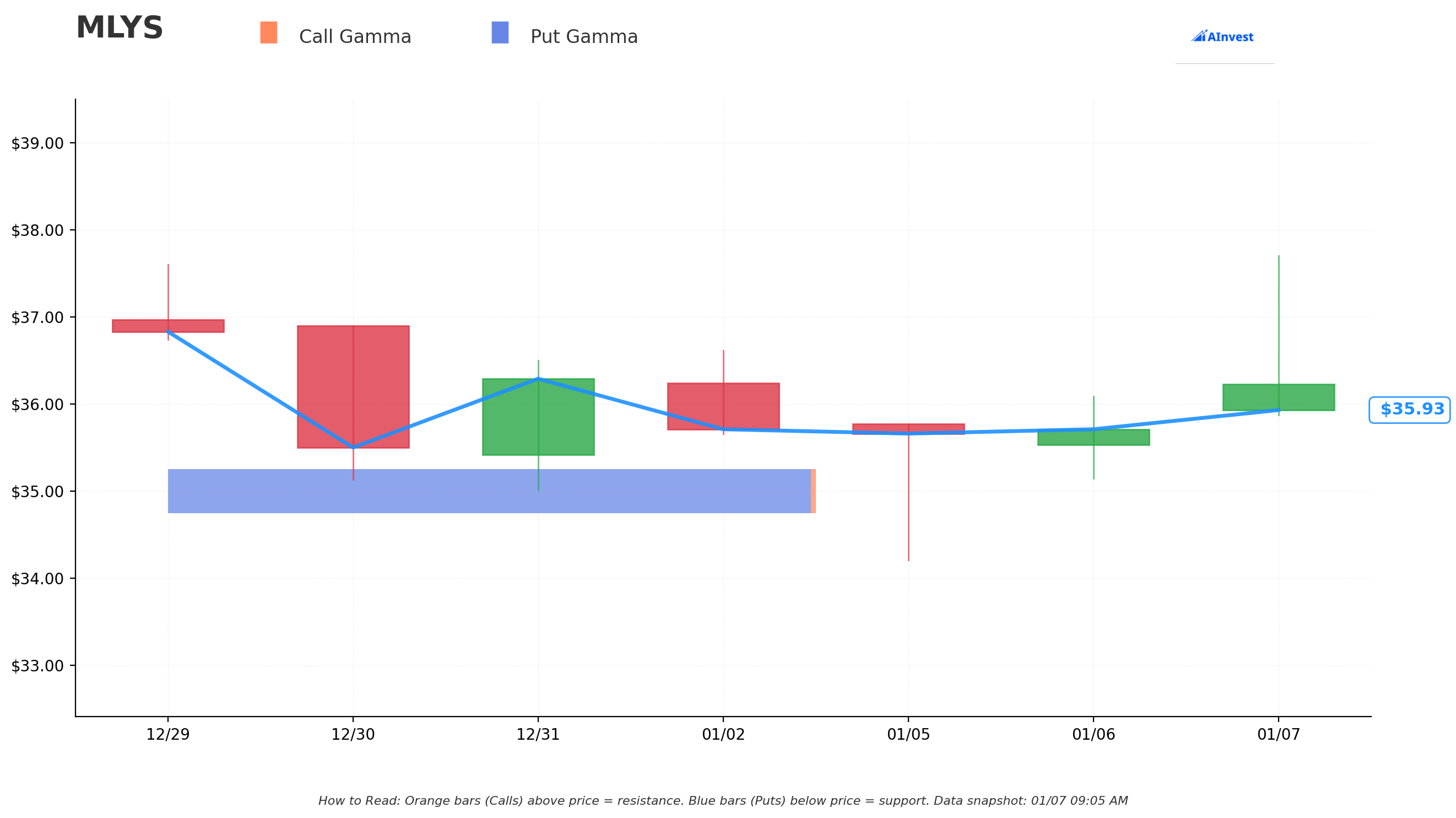

Gamma-Based Support & Resistance Analysis

Current Price: $36.94

The gamma exposure map reveals critical price magnets for the March 20th expiration:

🔵 Support Levels (Put Gamma Below Price):

- $35 - Immediate support with moderate put gamma (NOTE: 15K puts sold here caps downside benefit)

- $33 - Secondary support level

- $30 - MASSIVE CONCENTRATION with 59,800 put contracts! This is THE target (19% below current)

- $25 - Deep floor with 23,000 short puts (limits further downside past this level)

🟠 Resistance Levels (Call Gamma Above Price):

- $40 - Major ceiling with significant call gamma (psychological resistance)

- $42 - Secondary resistance (prior support turned resistance)

- $45 - Extended overhead resistance zone

What this means for traders:

MLYS is trading in a precarious technical position. The stock has broken down from $47 highs and is now sitting at $36.94, just above the critical $35 support level where this trader SOLD 15,000 puts. The massive gamma concentration at $30 (59,800 long puts) acts as a MAGNET - if the stock breaks $35 support, there's limited structural support until $30.

Notice the strategy? The put buyer:

- Sold puts at $35 (current support) - expects stock to break through here

- Concentrated massive position at $30 - primary profit target

- Bought $40 puts for extreme downside - protects against >40% crash

- Sold $25 puts - acknowledges stock unlikely to go below $25 (defines floor)

This is a classic "broken support becomes resistance" setup - if $35 fails, momentum accelerates to $30.

Net GEX Bias: Bearish - The massive put concentration and recent breakdown from $40 creates natural selling pressure as dealers hedge their exposure.

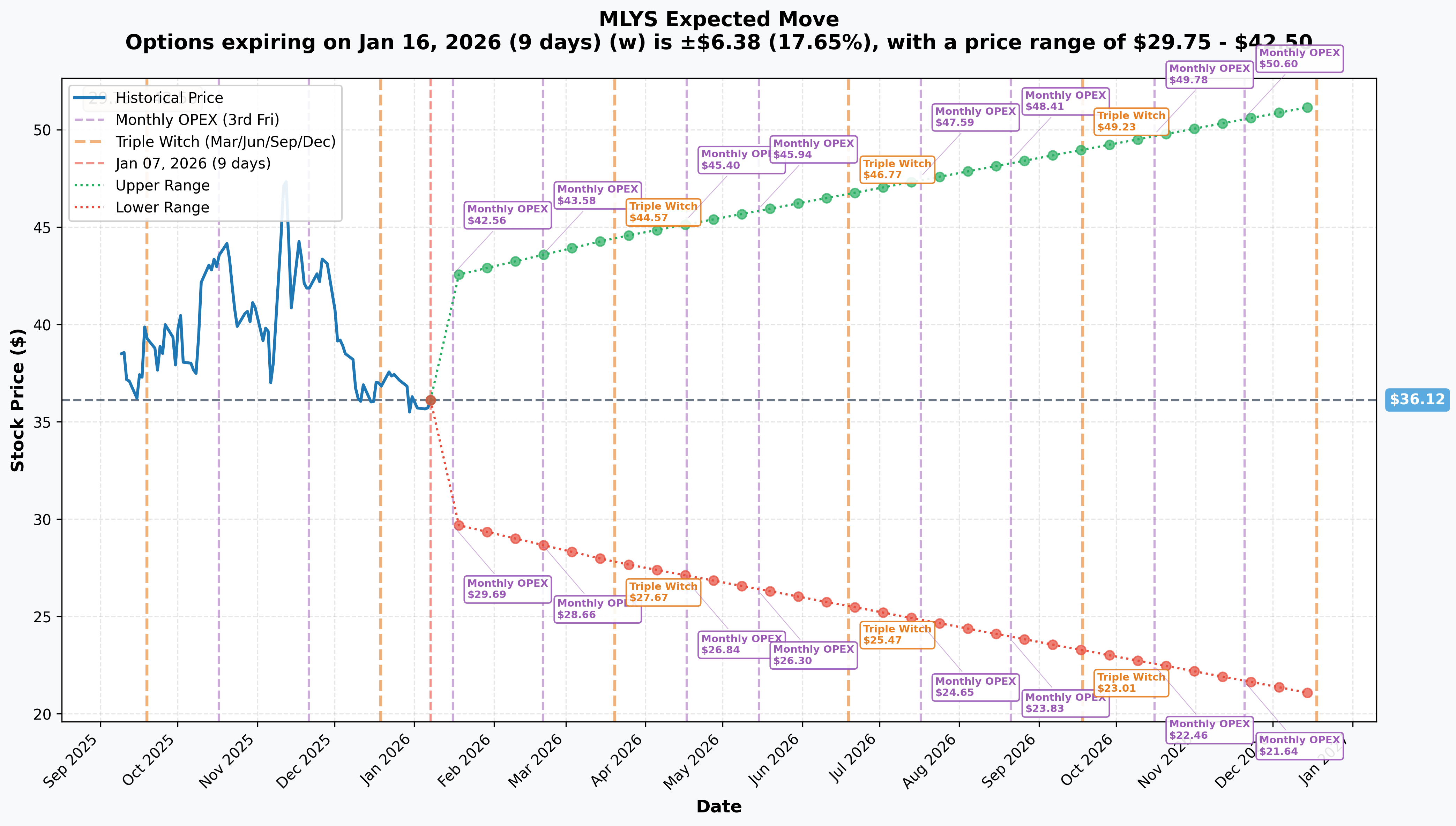

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Jan 16 - 9 days): ±$6.38 (±17.65%) → Range: $29.75 - $42.50

- 📅 Quarterly (Mar 20 - 72 days - THIS TRADE!): ±$8.33 (±23.06%) → Range: $27.79 - $44.45

- 📅 Yearly LEAPS: ±$15.13 (±41.88%) → Range: $20.99 - $51.25

Translation for regular folks:

Options traders are pricing in a MASSIVE 17.65% move ($6.38) by January 16th - that's HUGE volatility for a 9-day period! The market expects serious fireworks in the near term, likely around OSA data or broader biotech sector volatility.

The March 20th expiration (when this $26.5M trade expires) has a lower range of $27.79 - meaning the market thinks there's a real possibility MLYS could trade below $28 over the next 72 days. This aligns PERFECTLY with the put buyer's thesis: target the $28-32 zone where $30 puts pay maximum.

Key insight: The 23.06% implied move for March is LOWER than the 41.88% annual move, suggesting options market sees decreasing volatility over time as binary catalysts resolve. However, the put buyer is betting volatility plays OUT to the downside, not the upside.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q1 2026: Phase 2 Explore-OSA Topline Results (CRITICAL!) 📊

MLYS expects to report topline results from the Explore-OSA Phase 2 trial evaluating lorundrostat in moderate-to-severe obstructive sleep apnea with hypertension in Q1 2026 (within next 90 days):

- 🧪 Trial design: Evaluating lorundrostat's ability to reduce blood pressure in OSA patients

- 📊 Market opportunity: ~30 million Americans have OSA, with high comorbidity with hypertension

- 🎯 Strategic importance: If positive, expands addressable market beyond pure hypertension play

- ⚠️ Downside risk: OSA is a DIFFERENT indication than hypertension - efficacy not guaranteed

- 💰 Valuation impact: Stock pricing in success - any disappointment could trigger 20-30% selloff

Upside surprise potential: Positive OSA data would validate lorundrostat's versatility and significantly expand peak sales potential. Could drive stock back to $42-45 resistance.

Downside risk factors: OSA data miss or "meh" results would raise questions about lorundrostat's breadth of utility. Combined with AstraZeneca competitive threat, could send stock to $28-30 range (exactly where this put position profits maximally).

Historical precedent: Biotech stocks routinely move 20-40% on Phase 2 data, especially for expansion indications. MLYS showed 17% post-earnings volatility in November - OSA data could be similar or larger.

🚀 Near-Term Catalysts (Q1-Q2 2026)

AstraZeneca Baxdrostat PDUFA - Q2 2026 (MAJOR COMPETITIVE THREAT!) 🏥

AstraZeneca's competing aldosterone synthase inhibitor, baxdrostat, has Priority Review status with expected PDUFA date in Q2 2026:

- 🏆 First-mover advantage: AstraZeneca could be first ASI to market by 6+ months

- 💪 Big Pharma muscle: AstraZeneca has vastly superior commercial infrastructure vs clinical-stage MLYS

- 📊 Competitive positioning: Baxdrostat showed 9.8 mmHg placebo-adjusted reduction vs lorundrostat's 11.7 mmHg (slight edge to MLYS)

- ⚖️ Selectivity: Lorundrostat has superior 374:1 selectivity vs baxdrostat's ~100:1 ratio

- 🎯 Market dynamics: First-to-market ASI will shape physician perceptions and treatment algorithms

- 💰 Valuation risk: If AstraZeneca approved first, MLYS could lose significant commercial opportunity

Why this matters for the put trade: March 20th expiration falls RIGHT BEFORE the expected Q2 PDUFA date. The put buyer is positioning for:

- OSA data disappointment in Q1

- Growing anxiety about AstraZeneca first-to-market advantage

- Stock selling off from $37 to $28-32 as competitive threat materializes

If AstraZeneca gets approval in Q2 2026: MLYS would be relegated to "second ASI to market" status - historically problematic for small biotechs competing against Big Pharma. Stock could crater to $25-28 range.

NDA Review Timeline - Late 2026 FDA Decision 📅

MLYS filed its NDA in late 2025 with FDA, setting up expected decision in late 2026 (10-12 month standard review):

- ✅ Positive pre-NDA feedback: CEO cited "no surprises" from FDA - reduces approval risk

- 📊 Strong Phase 3 data: Two pivotal trials met primary endpoints with statistical significance

- 🎖️ JAMA recognition: Launch-HTN trial selected as one of nine most impactful studies of 2025

- ⏰ Timeline risk: Any FDA questions or Complete Response Letter could delay approval into 2027

- 🇺🇸 Regulatory pathway: Standard 10-12 month review vs AstraZeneca's Priority Review (6-8 months)

Impact on March trade: FDA decision won't occur until AFTER this position expires. However, any negative FDA communications (requests for additional data, manufacturing questions) could leak or be disclosed, triggering selloff into March expiration.

📊 Market Dynamics & Competitive Landscape

Aldosterone Synthase Inhibitor Market Opportunity 💰

The ASI market represents a significant but competitive opportunity:

- 📈 Market size: $225.9M in 2025, expected to reach $369.6M by 2032 (7.3% CAGR)

- 🎯 Target population: 15-20 million Americans with uncontrolled/resistant hypertension

- 💊 Pricing potential: Analysts estimate $500-700/month list price for premium hypertension drugs

- 🌎 Global opportunity: Hypertension market expected to reach $43.18B by 2030

- ⚖️ Competition: Existing MR antagonists (spironolactone, eplerenone) provide cheap alternatives

MLYS Competitive Positioning:

Advantages:

- 💪 Superior selectivity: 374:1 ratio reduces cortisol-related side effects

- 📊 Better efficacy: 11.7 mmHg reduction vs baxdrostat's 9.8 mmHg

- ✅ Clean safety profile: Well-tolerated in Phase 3 trials

- 🎖️ Scientific validation: JAMA recognition boosts credibility

Disadvantages:

- 🏢 No commercialization experience: Clinical-stage biotech vs AstraZeneca ($1.8B CinCor acquisition)

- ⏰ Timing disadvantage: Second-to-market with 6+ month delay vs baxdrostat

- 💰 Resource constraints: May need partnership to effectively compete

- 🇨🇳 No global infrastructure: Limited ability to capture international markets

The put buyer's thesis appears to be: Market is overvaluing MLYS at $2.83B given competitive disadvantages. Stock should trade closer to $25-30 range reflecting "second-tier ASI" status rather than category leader.

⚠️ Risk Catalysts (Negative)

Massive Insider Selling by CMO - RED FLAG 🚨

MLYS Chief Medical Officer David Malcom Rodman sold $9.3 MILLION in stock (50.3% of his position) over January 2-5, 2026:

- 📅 January 2: Sold 70,037 shares at $35.87 = $2.51M

- 📅 January 5: Sold 192,715 shares at $35.02 = $6.75M

- 📊 Total disposition: 262,752 shares = 50.3% position reduction

- ⚠️ Timing: Just days before this $26.5M bearish option trade!

Why this is CRITICAL:

The CMO is the executive most intimately familiar with:

- Clinical trial data quality and durability

- Competitive positioning vs AstraZeneca

- Regulatory feedback and approval probability

- Upcoming OSA trial results (Q1 2026)

When the CMO dumps 50% of his stock at $35, just as an institutional player bets $26.5M on a decline to $30, you have to ask: What do they know that the market doesn't?

Possible explanations:

- 📉 OSA data looks weak (CMO would have visibility)

- 🏥 FDA feedback less positive than disclosed

- 🎯 AstraZeneca competitive threat worse than market appreciates

- 💰 Personal financial planning (most benign explanation)

This insider selling alone justifies serious caution at $37 levels.

Valuation Stretched After 175% Rally 📊

At $36.94 with $2.83B market cap, MLYS trades at premium biotech valuation:

- 📈 1-year performance: +174.65% (from $12.98)

- 💰 P/E Ratio: -12.06 (pre-revenue company)

- 📉 Recent correction: Down 22% from $47.65 peak

- 🎯 Analyst targets: Average $47.29 (range: $26-56) - wide dispersion shows uncertainty

- ⚠️ Limited margin for error: Stock priced for PERFECT execution (OSA success, FDA approval, competitive wins)

Comparable biotech valuations suggest $25-35 range more appropriate for second-to-market ASI with unproven commercialization.

Cash Burn & Dilution Risk 💸

While MLYS has solid cash position, commercialization requires significant capital:

- 💰 Current cash: $593.6M (as of Q3 2025)

- 📅 Runway: Into 2028 at current burn rate

- 🔥 Q3 loss: $36.9M quarterly (-$0.52 EPS)

- 📊 Free cash flow: -$107.66M annually

- ⚖️ Commercialization needs: Will require sales force, marketing infrastructure, manufacturing scale-up

Dilution scenarios:

- If MLYS needs partnership, could involve milestone payments or revenue sharing (dilutive to equity value)

- Additional equity raises likely in 2026-2027 to fund commercial launch

- Recent $287.5M raise in September 2025 already diluted shareholders

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalysts, and insider selling signals, here are scenarios through March 20th expiration:

📉 Bear Case (45% probability) - PUT BUYER'S THESIS

Target: $27-32 range

How we get there:

- 😰 OSA data disappoints: Phase 2 results miss primary endpoint or show weak efficacy in Q1 2026

- 🏥 AstraZeneca anxiety builds: Market prices in first-mover disadvantage as Q2 PDUFA approaches

- 🚨 Insider selling cascade: More executives follow CMO's lead, dumping stock

- 📊 Technical breakdown: Stock breaks $35 support, triggering momentum selling to $30 gamma floor

- 💰 Valuation reset: Market reprices MLYS as "second-tier ASI" rather than category leader

- 📉 Biotech sector weakness: Broader small-cap biotech selloff creates headwinds

- 🎯 Profit-taking: Holders who rode stock from $13 to $37 (185% gain) take profits

Key metrics indicating this scenario:

- OSA data release with <10 mmHg systolic reduction or safety concerns

- AstraZeneca making positive PDUFA statements

- Stock breaking below $35 on heavy volume

- Additional insider selling disclosed

Probability assessment: 45% because multiple negative catalysts are lining up:

- CMO insider selling is MASSIVE red flag

- AstraZeneca competitive threat very real with Priority Review

- Stock already corrected 22% from peak - momentum broken

- OSA is expansion indication with higher risk profile than core hypertension

- Valuation stretched at $2.83B for pre-revenue biotech

Put P&L in Bear Case:

- Stock at $30 on March 20: $30 puts worth ~$0 (at-the-money), $40 puts worth $10 = Mixed P&L, likely small profit

- Stock at $28 on March 20: $30 puts worth $2, $40 puts worth $12 = Significant profit (~$15-20M gain)

- Stock at $25 on March 20: $30 puts worth $5, $40 puts worth $15, but $25 short puts lose $0, $35 short puts lose $10 = Capped profit due to spread structure

This is the scenario the $26.5M put buyer is betting on - and it's the MOST LIKELY outcome given the evidence.

🎯 Base Case (35% probability)

Target: $32-38 range (CHOPPY CONSOLIDATION)

Most likely scenario if bear case doesn't materialize:

- ✅ OSA data mixed: Not spectacular but not disaster - meets some endpoints, misses others

- ⚖️ Competitive positioning unclear: Market waits to see AstraZeneca approval terms and labeling

- 🔄 Range-bound trading: Stock oscillates between $32 support and $38 resistance

- 📊 Volatility crush: IV collapses after OSA data reduces uncertainty

- 💤 Waiting game: Investors hold positions awaiting FDA decision clarity (late 2026)

This scenario is BREAKEVEN to SMALL LOSS for put position:

- Stock at $35 on March 20: Most options expire near worthless

- Net loss of ~$18.3M in premium paid

- Put buyer accepts this as "cost of insurance" that didn't pay off

Why 35% probability: Requires OSA data to be "good enough" to maintain current valuation while not spectacular enough to drive stock higher. Also requires no major competitive developments from AstraZeneca. Possible but requires multiple things to go "just right."

📈 Bull Case (20% probability)

Target: $42-50

What would need to happen:

- 💪 OSA data CRUSHES: Phase 2 results exceed expectations with strong efficacy and safety

- 🎖️ Positive regulatory signals: FDA provides encouraging feedback or expedited review possibility

- 🏆 Competitive advantage emerges: Analysis shows lorundrostat's superior selectivity matters clinically

- 🤝 Partnership announced: Major pharma partner emerges for co-commercialization

- 📈 Analyst upgrades: Street raises targets citing reduced risk profile

- 🚀 Biotech sector strength: Rising tide lifts all boats in small-cap biotech

Key metrics needed:

- OSA data with >12 mmHg systolic reduction and clean safety

- Partnership deal with $200M+ upfront payment

- Analyst price targets moving to $50-60 range

- Technical breakout above $40 resistance

Probability assessment: Only 20% because:

- CMO insider selling strongly suggests negatives ahead, not positives

- $26.5M institutional put position indicates smart money expects downside

- AstraZeneca competitive threat is structural and can't be easily overcome

- Stock already up 175% in past year - limited upside runway

Put P&L in Bull Case:

- Stock at $42-50: All puts expire worthless

- Total loss of $18.3M net premium paid

- Put buyer accepts loss as cost of hedging that didn't pay off

💡 Trading Ideas

🛡️ Conservative: Avoid or Wait for $28-30 Entry

Play: Stay away from MLYS until post-OSA data clarity

Why this works:

- 🚨 Insider selling is HUGE red flag: CMO dumping 50% of position at $35 screams warning

- 💸 Institutional put position: $26.5M bearish bet suggests smart money expects decline

- 📊 Binary catalyst risk: OSA data in Q1 could move stock 20-30% either direction

- ⏰ AstraZeneca threat looming: Q2 PDUFA for baxdrostat creates overhang

- 🎯 Better entry likely: Wait for pullback to $28-30 range where risk/reward improves

- 📉 Broken momentum: Stock down 22% from peak - technical damage done

Action plan:

- 👀 Watch OSA data release: Need to see >10 mmHg reduction and clean safety

- 🎯 Entry targets: $28-30 range (25-30% downside from current) provides margin of safety

- ✅ Confirm competitive positioning: Understand lorundrostat vs baxdrostat differentiation

- 📊 Monitor insider activity: Any further selling is major red flag

- ⏰ Patience required: Don't chase - let the story develop

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 20-30% drawdown. Get much better entry if bear case plays out. Maintain capital for better opportunities.

⚖️ Balanced: Copy the Smart Money - Put Spread

Play: Mimic institutional positioning with smaller put spread

Structure: Buy $35 puts, Sell $30 puts (March 20 expiration - SAME as the $26.5M trade)

Why this works:

- 🎯 Following institutional money: Copying the pros at similar strikes

- 📊 Defined risk: $5 wide spread = $500 max risk per spread

- 🛡️ Targets breakdown scenario: Profits if stock falls from $37 to $30-33 range

- ⏰ 72 days to expiration: Plenty of time for OSA data and competitive dynamics to play out

- 💰 Asymmetric risk/reward: Limited risk, meaningful profit potential

Estimated P&L (based on current IV ~70-80%):

- 💰 Pay: ~$2.00-2.50 net debit per spread

- 📈 Max profit: $2.50-3.00 if MLYS below $30 at expiration (100-150% ROI)

- 📉 Max loss: $2.00-2.50 if MLYS above $35 (100% loss of premium)

- 🎯 Breakeven: ~$32.50-33.00

- 📊 Risk/Reward: 1:1 to 1:1.5 - acceptable for bearish thesis

Entry timing:

- ⏰ Enter now or wait for bounce: Could enter at current $37 levels OR wait for dead-cat bounce to $38-39

- 🎯 Best entry: Stock at $37-38 provides maximum profit zone

- ❌ Skip if: Stock already below $33 (spread too close to profit zone)

Position sizing: Risk only 1-3% of portfolio per spread

Exit strategy:

- Take profits if stock reaches $31-32 (don't wait for expiration)

- Cut losses if stock rallies above $40 (thesis invalidated)

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Sell Premium into IV Crush (ADVANCED!)

Play: Sell put spreads ABOVE current price, betting on range-bound consolidation

Structure: Sell $40 puts, Buy $35 puts (March 20 expiration)

Why this could work:

- 💸 Collect premium: High IV (~70-80%) means rich option prices

- 📊 Bet on consolidation: Stock stays above $35-40 range through March

- ⏰ Theta decay: Time works in your favor as expiration approaches

- 🎯 Statistical edge: Stock would need to drop 8-18% to threaten position

- 💰 Income generation: Collect $2-3 per spread in premium

Why this could blow up (SERIOUS RISKS):

- 🚨 Insider selling suggests downside: CMO didn't sell 50% for no reason

- 💥 OSA data miss: Stock could gap down 20-30% on bad news

- 📉 Institutional put position: You'd be on opposite side of $26.5M smart money bet

- ⚠️ Limited profit, unlimited risk: Collect $2-3 but risk $2-5 if wrong

- 🎢 Biotech volatility: MLYS can move 5-10% on no news

Estimated P&L:

- 💰 Collect: ~$2.00-3.00 credit per spread

- 📈 Max profit: $2.00-3.00 if MLYS stays above $40 (keep full premium)

- 📉 Max loss: $2.00-3.00 if MLYS drops below $35 (lose on spread)

- 💀 Disaster scenario: Stock gaps to $25 on OSA miss = $10-15 loss per spread

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand you're BETTING AGAINST insider selling and institutional puts

- ✅ Can afford to lose entire spread width ($5 = $500 per contract)

- ✅ Have experience selling premium in biotech (extreme volatility)

- ✅ Accept that OSA data could trigger catastrophic loss

- ✅ Plan to close position immediately if stock breaks $35

Risk level: HIGH (selling premium against insider selling) | Skill level: Advanced only

Probability of profit: ~30% (smart money is on the OTHER side of this trade!)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🚨 CMO insider selling is MASSIVE RED FLAG: Chief Medical Officer selling $9.3M (50% of position) at $35.02-35.87 in early January 2026 is extraordinarily bearish. The CMO has intimate knowledge of clinical data quality, regulatory feedback, and competitive positioning. When he dumps half his holdings just days before a $26.5M institutional put position appears, you must assume negative information exists that isn't public. This is THE single biggest warning sign.

-

📊 OSA data binary event in Q1 2026: Phase 2 Explore-OSA topline results expected within 90 days create MASSIVE volatility risk. OSA is an expansion indication beyond core hypertension - efficacy not guaranteed. Stock could move 20-40% either direction on data release. Options are pricing ±23% move through March. Historical biotech precedent shows Phase 2 expansion data frequently disappoints even when core indication succeeds.

-

🏥 AstraZeneca first-to-market threat: Baxdrostat with Priority Review status and Q2 2026 PDUFA could reach market 6+ months before lorundrostat. AstraZeneca has $1.8B CinCor acquisition, 20,000+ patient trials globally, and Big Pharma commercial muscle. First ASI to market will shape treatment paradigms and physician adoption. MLYS relegated to "second-tier" status would justify 30-40% valuation haircut to $22-26 range.

-

💰 Valuation at nosebleed levels for pre-revenue biotech: $2.83B market cap at $36.94 vs $593.6M cash means market is pricing in $2.2B+ in future commercial value. This assumes lorundrostat achieves blockbuster status ($1B+ peak sales) despite competitive threat. Trading at -12.06 P/E (pre-revenue) after 175% rally creates zero margin of error. Comparable pre-commercial biotechs trade at 1-3x cash - suggesting $600M-1.8B fair value ($7.50-22.50 per share).

-

🎯 No commercialization infrastructure: MLYS is clinical-stage biotech with NO sales force, marketing team, or distribution network. Even with FDA approval, requires either: (1) Building commercial infrastructure from scratch (expensive, dilutive), (2) Partnering with Big Pharma (dilutive to economics), or (3) Being acquired (possible but uncertainty). AstraZeneca already has all infrastructure in place for baxdrostat.

-

📉 Technical damage after 22% correction from peak: Stock broke down from $47.65 December highs to current $36.94 (22% decline). This created technical damage with $40 resistance now overhead. Momentum traders and algorithms will sell rallies into $38-40 zone. Need catalyst to break through - absent positive OSA data, stock likely capped at $40.

-

⚖️ Generic competition from existing MR antagonists: Spironolactone (generic, approved 1960) provides cheap alternative despite side effects. Physicians comfortable with established treatments may be slow to adopt new ASI class. Premium pricing ($500-700/month estimates) vs pennies for generic spiro creates reimbursement hurdles. Market may be smaller than bulls expect.

-

💸 Dilution risk from commercialization funding needs: Current $593.6M cash provides runway into 2028 at current burn, BUT commercialization requires massive capital infusion. Sales force of 200+ reps costs $50-80M annually. Manufacturing scale-up, marketing campaigns, KOL programs add $100M+. Likely need $200-300M additional capital raise in 2026-27, diluting existing shareholders 20-30%.

-

🎢 Small-cap biotech volatility amplifies risk: MLYS daily volatility averages 5-8% - this isn't a stable blue-chip. Stock can gap 10-15% overnight on sector news, FDA communications, or competitor developments completely unrelated to MLYS fundamentals. Recent trading history shows $8.24 to $47.65 range (5.8x move) - this cuts both ways.

-

🌐 Macro biotech headwinds if risk-off environment emerges: Small-cap biotechs get destroyed in risk-off markets. If broader markets correct or recession fears emerge, speculative pre-revenue names like MLYS could see 40-50% drawdowns regardless of fundamentals. No dividend, no earnings, no moat = first to get sold.

🎯 The Bottom Line

Real talk: When a Chief Medical Officer dumps 50% of his stock for $9.3 million, and days later a sophisticated institutional player deploys $26.5 million in bearish puts targeting a decline from $37 to $28-32, you don't fight the tape. These are INFORMED players with access to information and analysis far beyond retail investors.

What this trade tells us:

- 🚨 Insiders are heading for the exits: CMO knows something the market doesn't - OSA data weakness? FDA issues? Competitive threat worse than disclosed?

- 💰 Smart money betting on 20-30% decline: The put structure targets $28-32 range by March 20th

- ⏰ Timing is CRITICAL: March expiration captures OSA data (Q1) and building anxiety about AstraZeneca PDUFA (Q2)

- 📊 This isn't a "crash" bet: It's a valuation reset from $37 to $30 - still giving MLYS credit as viable ASI competitor

- 🎯 Risk/reward is POOR at $37: Stock would need perfect execution (OSA success, AstraZeneca delay, FDA fast-track) to justify higher prices

This is NOT a "never touch MLYS" signal - it's a "don't chase at $37, wait for $28-30 entry" signal.

If you own MLYS:

- ✅ Consider selling 50-75% at $37 levels: Lock in 185% gains from $13, reduce exposure

- 📊 Set HARD STOP at $33: Major gamma support - break below = cascade to $30

- ⏰ Don't hold through OSA data unhedged: Binary risk too high - either hedge or sell

- 🎯 If you must hold, buy protective puts: $35 puts for downside protection

- 🛡️ Reevaluate after OSA data: Positive results change risk profile entirely

If you're watching from sidelines:

- ⏰ DO NOT chase at $37: Wait for OSA data clarity (Q1 2026)

- 🎯 Best entry: $28-30 range: Would represent 25-30% discount from current with technical support

- 📈 Looking for confirmation of: Strong OSA data (>10 mmHg reduction), differentiation vs baxdrostat, partnership potential

- 🚀 Longer-term (12-18 months): If lorundrostat gets approved and shows commercial traction, $50-70 possible

- ⚠️ Current valuation ($2.83B) requires PERFECT execution: Too much can go wrong for comfort at these levels

If you're bearish:

- 🎯 $35/$30 put spread offers best risk/reward: Copy institutional positioning at smaller size

- 📊 First support at $35, major support at $30: Breakdown below $35 should accelerate

- ⚠️ Don't short stock outright: Borrow costs high, squeeze risk in biotech

- 📉 Watch for break below $35 on volume: That's the technical trigger for momentum to $30

- ⏰ Be ready to take profits at $30-31: Don't get greedy in fast-moving biotech

Mark your calendar - Key dates:

- 📅 Q1 2026 (Jan-Mar) - Phase 2 Explore-OSA topline results (WATCH CLOSELY!)

- 📅 March 20, 2026 - Expiration of this $26.5M put position

- 📅 Q2 2026 (Apr-Jun) - AstraZeneca baxdrostat PDUFA date (competitive threat)

- 📅 Late 2026 (Oct-Dec) - Expected FDA decision on lorundrostat NDA

Final verdict: MLYS's long-term story remains intact - lorundrostat has solid Phase 3 data, FDA filing complete, and represents meaningful innovation in hypertension treatment. HOWEVER, at $36.94 with $2.83B market cap after 175% rally, risk/reward is NO LONGER favorable for aggressive new positioning. The combination of massive insider selling, $26.5M institutional put position, AstraZeneca competitive threat, and OSA binary catalyst creates a PERFECT STORM for 25-35% correction to $24-28 range.

Be patient. Let OSA data clear. Look for entry at $28-30 where you get 25% discount and technical support. The aldosterone synthase inhibitor opportunity will still exist in 6 months - but your entry price will be FAR better.

This is a marathon, not a sprint. Capital preservation comes first. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Biotech investing carries extreme volatility and binary event risk including total loss of capital. The insider selling and institutional put position described are factual but do not guarantee future price movements. Clinical trial outcomes are inherently uncertain. Always do your own research and consider consulting a licensed financial advisor before trading. The author may hold positions in securities discussed.

About Mineralys Therapeutics: Mineralys Therapeutics is a clinical-stage biopharmaceutical company focused on developing medicines to target diseases driven by abnormally elevated aldosterone, including hypertension, chronic kidney disease, and obstructive sleep apnea, with a market cap of $2.83 billion in the Biotechnology industry.

Sources: