🐋 MLYS $2.3M Speculative Call Bet - Someone Is Loading Up Ahead of Imminent Clinical Data!

📅 February 27, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just bought $2.3 MILLION in MLYS April $45 calls - nearly 23,000 contracts on a clinical-stage biotech trading at $28.66. The $45 strike is 57% out-of-the-money, making this one of the most aggressively speculative single-leg call buys we've seen this week. The timing is notable: Mineralys has EXPLORE-OSA Phase 2 topline data expected any day now (Q1 2026 guidance), Q4 earnings on March 18, and FDA NDA acceptance for lorundrostat pending in H1 2026. With today's call volume running 319% above normal, this is a significant directional bet on a major catalyst-driven move higher.

📊 Company Overview

Mineralys Therapeutics (MLYS) is a clinical-stage biopharmaceutical company developing lorundrostat, an oral aldosterone synthase inhibitor (ASI) for hypertension:

- 💊 What they do: Developing lorundrostat, a first-in-class oral drug that blocks aldosterone production to treat uncontrolled and resistant hypertension

- 💰 Market Cap: $2.3B

- 🏢 Sector: Pharmaceutical Preparations (clinical-stage biopharma)

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$28.66

- 🔬 Key Story: NDA filed with FDA in Q4 2025 after two positive Phase 3 trials; PDUFA date expected in 2026. Launch-HTN results recognized by JAMA as "Research of the Year". Also exploring lorundrostat in obstructive sleep apnea (OSA) and chronic kidney disease (CKD).

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:07:36 | MLYS | MID | BUY | CALL $45 | 2026-04-17 | $2.3M | $45 | 23K | 14K | 22,984 | $28.66 | $1.00 | MLYS20260417C45 |

🤓 What This Actually Means

Let me break this down in plain English:

- 💸 $2.3 million spent: 22,984 contracts at $1.00 each ($1.00 x 100 shares x 22,984 = ~$2.3M)

- 📈 Strike $45 is 57% above current price - this is deeply out-of-the-money and requires a huge move to pay off

- ⏰ 49 days to expiration (April 17, 2026) - less than two months for the thesis to play out

- 📊 Volume vs OI: 23K volume vs 14K OI - volume is 1.64x open interest, indicating this is likely opening a new position (Buy-to-Open), not closing existing contracts

- 🤝 MID fill - executed at the midpoint of the bid-ask spread, consistent with institutional-style negotiated execution rather than a retail market order

- 🎯 Breakeven at expiration: $46.00 ($45 strike + $1.00 premium paid) = needs a +60.5% rally from current levels by April 17

What's the thesis here?

At $1.00 per contract, this is a relatively cheap lottery ticket on a massive move. For $2.3 million, the trader controls exposure on nearly 2.3 million shares of MLYS (roughly 2.9% of the total shares outstanding). The asymmetry is the point: if MLYS were to reach $55 on a major catalyst, these calls would be worth $10 each - a 10x return. If the stock stays below $45, the entire $2.3M is lost.

The most logical explanation is that this trader is positioning ahead of one or more of the following: (1) the imminent EXPLORE-OSA Phase 2 data readout, which could open a massive new market in sleep apnea; (2) FDA NDA acceptance and PDUFA date announcement that would de-risk the regulatory timeline; or (3) speculative M&A interest, given that AstraZeneca paid $1.3B to acquire CinCor's competing ASI (baxdrostat) in 2023, and lorundrostat has arguably stronger clinical data.

Why $45? The 52-week high is $47.65. The consensus analyst price target is $47.29, with a high target of $56. A $45 strike essentially bets that MLYS reclaims its recent highs - which would only take a single major positive catalyst in a biotech with this kind of event density.

Why this volume matters: MLYS typically trades ~5,500 call contracts per day. Today's 23,000+ contracts represent a 319% increase over normal volume. In a $2.3B market cap biotech, this kind of activity stands out.

📈 Technical Setup / Chart Check-Up

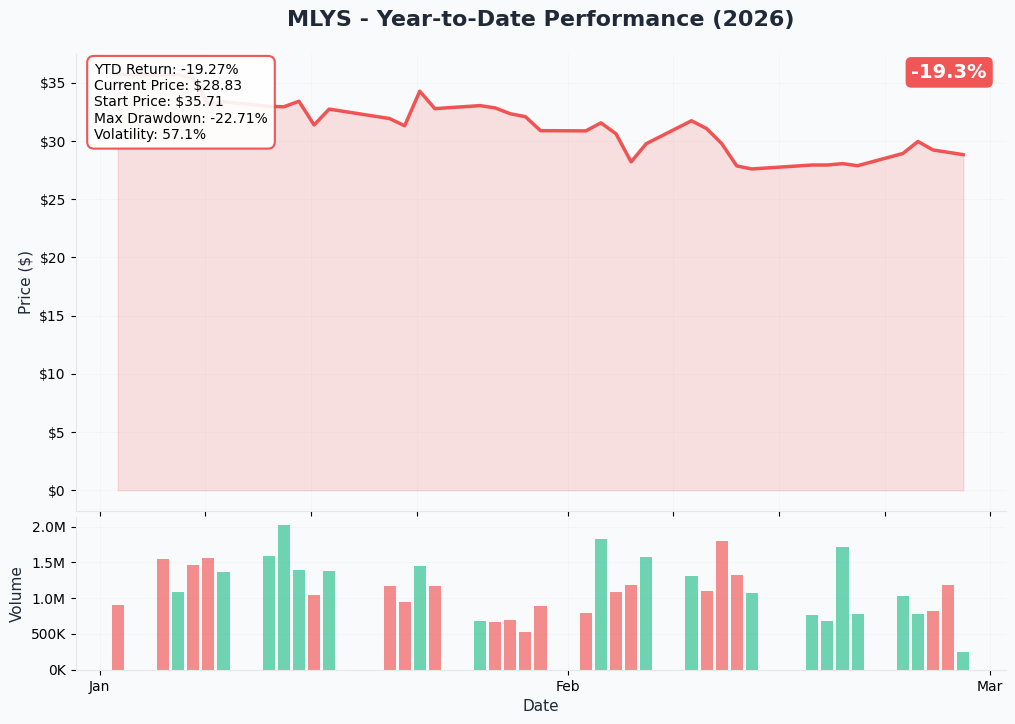

YTD Performance

MLYS has had a turbulent ride over the past year, currently trading at ~$28.66:

- 📈 1-Year Performance: +228.73% - the stock was under $9 a year ago, so the long-term trajectory has been strongly positive

- 📉 Down ~39% from 52-week high of $47.65 - the stock peaked in November 2025 around the time of positive clinical data and analyst upgrades, then pulled back on heavy insider selling ($70.9M in the last 90 days)

- 📊 1-Month: -10.83% | 1-Week: +4.96% - recent weakness but showing signs of stabilization with a bounce this week

- 💰 September 2025 offering at $25.50 provides a natural floor - the stock is currently trading above its last capital raise price, which is a positive sign

Key takeaway: MLYS is trading in a post-peak consolidation phase, roughly 40% below highs but still well above the offering price. The catalyst calendar ahead is dense enough to either re-ignite the rally toward $45+ or, if data disappoints, push the stock back toward the low $20s.

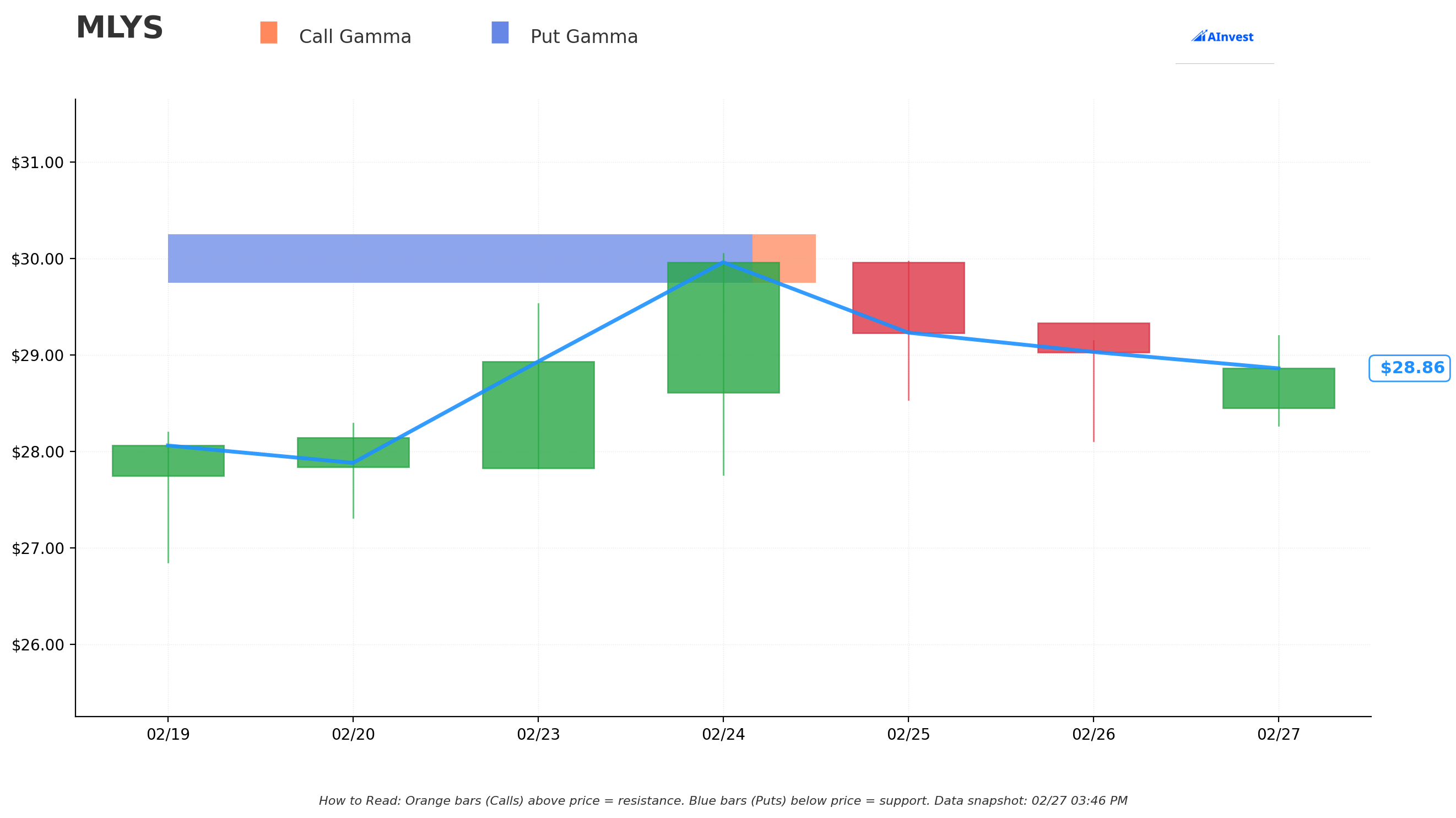

Gamma-Based Support & Resistance Analysis

Current Price: $28.89

The gamma exposure (GEX) map shows where options market makers have concentrated hedging positions:

🔵 Support Level (Put Gamma Below Price):

- $25.00 - Strongest support with 0.72 total gamma exposure (13.4% below current price). This is the LINE IN THE SAND. The September 2025 offering was priced at $25.50, and the $25 strike has the most put gamma concentration. A break below $25 would be technically significant.

🟠 Resistance Level (Call Gamma Above Price):

- $30.00 - Strongest resistance with 1.16 total gamma exposure (just 3.9% overhead). This is the near-term ceiling. A breakout above $30 would clear the most concentrated gamma resistance and could trigger accelerated dealer hedging flows to the upside.

What this means for traders: The current gamma picture is straightforward: $25 support, $30 resistance, stock at $29. The $30 level is the critical near-term hurdle. If MLYS breaks above $30 on a catalyst, there is limited gamma resistance above, meaning moves could accelerate quickly. The $45 strike on the call trade sits well above all current gamma concentration, reinforcing that this is a catalyst-dependent play, not a technical setup.

Net GEX Bias: Bearish (2.44B total call gamma vs 4.01B total put gamma) - put gamma exceeds call gamma, suggesting dealers are net short delta. In isolation, this creates downward hedging pressure. However, in a biotech with binary catalysts, gamma profiles can shift rapidly.

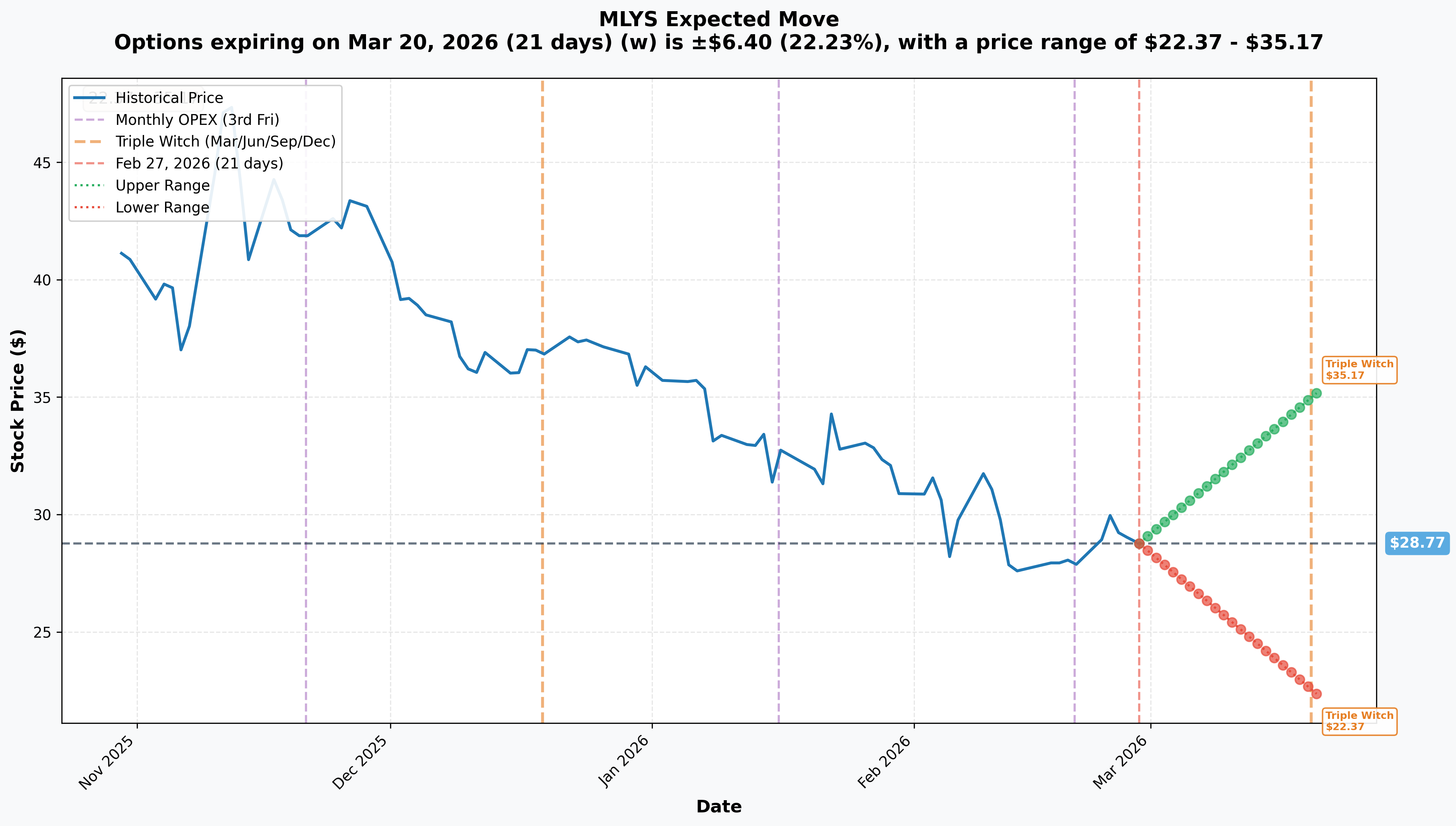

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 21 days): ±$6.40 (±22.23%) --> Range: $22.37 - $35.17

- 📅 April 17 OPEX (THIS TRADE!): Not priced separately, but the monthly move of ±22% in 21 days implies the April expiration (49 days out) likely prices a ±30-35% move, roughly $20 - $38+

Translation: The options market is pricing a potential 22% move in either direction by March 20 OPEX alone. That is an enormous implied move for a stock at $29, reflecting the binary nature of the upcoming catalysts (clinical data, earnings, FDA decisions). The $45 strike requires a move beyond even the upper end of the March implied range - it needs roughly +57% - which underscores how speculative this trade is. This is not a "the options market expects $45" trade. It is a "if the right catalyst hits, the payout is massive" trade.

Key insight: A 22% implied move on a $29 stock means the market is pricing in potential swings of $6+ by March OPEX. For reference, that would put the stock anywhere from $22 to $35. A positive EXPLORE-OSA readout combined with NDA acceptance could feasibly push the stock to $35-40, but reaching $45 likely requires a transformative event like M&A interest or a combination of multiple positive catalysts hitting simultaneously.

🎪 Catalysts

🔥 Upcoming Catalysts

EXPLORE-OSA Phase 2 Topline Data - Q1 2026 (IMMINENT - days to weeks) 🧬

This is the catalyst most likely driving today's unusual options flow. Mineralys completed enrollment in the Phase 2 EXPLORE-OSA trial evaluating lorundrostat in overweight/obese adults with moderate-to-severe obstructive sleep apnea and hypertension. Topline results are expected in Q1 2026, meaning they could drop any day.

- 🎯 Why it matters: ~54 million Americans have OSA, and the overlap with hypertension is substantial. Positive data here would open a major new indication that competitor baxdrostat is NOT pursuing

- 📈 If positive: Could re-rate the stock toward the $35-45 range as the market assigns value to a second large indication

- 📉 If negative: Limited damage to the core hypertension NDA (this is exploratory Phase 2), but the stock likely drops 10-20% on a narrowing of the perceived opportunity

- 🔢 Probability of positive outcome: ~55-65% (strong mechanistic rationale - lorundrostat's bedtime dosing targets aldosterone during sleep - but OSA is a novel indication for this drug class)

Q4 2025 / Full-Year 2025 Earnings - March 18, 2026 📊

Confirmed earnings date, after market close. As a pre-revenue biotech, the financials themselves are secondary, but the conference call is critical.

- 📊 Key items to watch: updated cash runway guidance (currently funded into 2028 with $593.6M on hand), NDA review progress, EXPLORE-OSA data status, pre-commercialization spending updates

- 💡 Q3 2025 EPS came in at ($0.52) vs. consensus of ($0.96) - a significant beat driven by declining R&D costs as pivotal trials completed

- 📈 Potential positive surprise: If management provides color on NDA acceptance timing or hints at EXPLORE-OSA results during the call

FDA NDA Acceptance & PDUFA Date - Expected H1 2026 📋

The FDA typically takes 60 days to review an NDA filing for acceptance. Given the Q4 2025 filing, an acceptance decision is expected in Q1-Q2 2026. Acceptance would come with a PDUFA action date, providing the market with a definitive regulatory timeline.

- ✅ Probability of acceptance: ~85-90% based on the robust clinical package (two positive pivotal trials + supportive Phase 2 data, pre-NDA FDA feedback incorporated)

- 📈 Impact of acceptance with PDUFA date: Strong positive - removes the largest single regulatory uncertainty

- 📉 Impact of Complete Response Letter (CRL): Devastating - stock could decline 40-60%

AstraZeneca Baxdrostat PDUFA Decision - Q2 2026 ⚔️

The competitive elephant in the room. AstraZeneca's baxdrostat NDA was accepted under FDA Priority Review with a Q2 2026 PDUFA target. If approved, baxdrostat would be the first-in-class ASI to reach the market.

- ⚖️ Silver lining for MLYS: First-in-class approval validates the aldosterone synthase inhibitor mechanism, potentially de-risking lorundrostat's own regulatory path

- ⚠️ Competitive risk: AstraZeneca's commercial machine ($220B+ market cap) vs. Mineralys as a standalone $2.3B biotech creates a meaningful first-mover disadvantage

- 📊 Efficacy comparison favors MLYS: Launch-HTN showed 11.7 mmHg placebo-adjusted SBP reduction vs. baxdrostat's 9.8 mmHg in BaxHTN - potentially supporting "best-in-class" positioning

✅ Recent Catalysts (Already Happened)

NDA Filing for Lorundrostat - Q4 2025 📋

Mineralys filed its NDA with the FDA for lorundrostat in uncontrolled and resistant hypertension, supported by three positive clinical trials:

- Launch-HTN (Phase 3): 1,083 patients; lorundrostat 50mg reduced SBP by 19.0 mmHg; placebo-adjusted -11.7 mmHg (P <.0001)

- Advance-HTN (Phase 2 pivotal): Lorundrostat 50mg reduced 24-hour ambulatory SBP by 15.4 mmHg (7.9 mmHg placebo-adjusted)

- Explore-CKD (Phase 2): SBP reduction -9.3 mmHg; UACR (albuminuria) reduction -25.6% (both statistically significant)

JAMA "Research of the Year" - December 12, 2025 🏆

The Launch-HTN trial was selected in JAMA's inaugural "Research of the Year Roundup", chosen by JAMA's top editors as one of the most impactful studies of the year. This recognition reinforces the scientific credibility of the clinical program.

September 2025 Equity Offering - $287.5M 💰

Mineralys closed an upsized $287.5M public offering at $25.50/share, pushing total cash to $593.6M and eliminating near-term dilution risk through 2028.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, the analyst target range, and the dense catalyst calendar, here are the scenarios through the April 17, 2026 expiration:

📈 Bull Case (20% probability)

Target: $42-$56

How we get there:

- 🧬 EXPLORE-OSA Phase 2 delivers positive topline data (stock rallies 15-25% on the news)

- 📋 FDA accepts lorundrostat NDA with a PDUFA date (additional 10-15% upside)

- 🤝 M&A speculation intensifies - AstraZeneca's $1.3B CinCor acquisition sets a precedent, and lorundrostat's potentially superior data could attract interest from large pharma

- 📊 Combination of catalysts pushes stock toward the analyst consensus target of $47.29 (high target: $56)

- 📈 Stock breaks through $30 gamma resistance with momentum, and thin gamma above $30 allows rapid price appreciation

Call trade P&L at $50: Calls worth $5/share, profit = $4.00/share x 22,984 contracts = $9.2M gain (400% ROI) Call trade P&L at $55: Calls worth $10/share, profit = $9.00/share x 22,984 contracts = $20.7M gain (900% ROI)

This is the lottery-ticket scenario. Multiple catalysts stack in a compressed timeframe, driving a re-rating toward the 52-week high of $47.65 and beyond. The asymmetric payout is exactly what makes this trade attractive despite its low probability.

🎯 Base Case (50% probability)

Target: $25-$35 range

Most likely scenario:

- 📊 EXPLORE-OSA data is mixed or modestly positive - stock moves 5-10% in either direction

- 📋 Q4 earnings on March 18 provide no major surprises; cash position confirmed as strong

- ⏳ NDA acceptance comes but with standard review timeline (PDUFA in late 2026 or early 2027)

- ⚔️ Baxdrostat PDUFA approaches in Q2, creating competitive uncertainty

- 🔄 Stock trades within the implied move range of $22-$35

Call trade P&L at $35: Calls still out-of-the-money by $10, expire worthless, loss = -$2.3M (-100%) Call trade P&L at $30: Calls deeply OTM, expire worthless, loss = -$2.3M (-100%)

In the base case, the stock stays well below the $45 strike and the calls expire worthless. However, the trader could potentially sell the calls before expiration if a catalyst drives a sharp move toward $35-40, recovering some premium through increased implied volatility and delta appreciation - even without reaching $45.

📉 Bear Case (30% probability)

Target: $18-$25

What could go wrong:

- 🧬 EXPLORE-OSA Phase 2 fails - stock drops 10-20% as the market narrows lorundrostat's addressable opportunity

- ⚠️ FDA issues a Refuse to File (RTF) or requests additional data for the NDA - stock drops 40-60%

- 📉 Heavy insider selling continues ($70.9M in the last 90 days, including CEO and CMO sales), further undermining sentiment

- ⚔️ AstraZeneca's baxdrostat receives positive FDA advisory committee feedback ahead of its PDUFA, reinforcing competitive first-mover advantage

- 📊 Break below $25 gamma support triggers accelerated selling toward the low $20s or teens

- 🏥 Broader biotech sector rotation or risk-off macro environment

Call trade P&L: Calls expire worthless, loss = -$2.3M (-100%)

The $25 level with concentrated put gamma is the critical support. Below $25.50 (the September offering price), there is limited structural support and the stock could re-test levels not seen since mid-2025.

💡 Trading Ideas

🛡️ Conservative: "Defined-Risk Catalyst Play" - Debit Call Spread

Play: Buy the MLYS April 17 $30 calls, sell the April 17 $40 calls

Structure: $30/$40 bull call spread, 49 days to expiration

Why this works:

- 📊 Captures the same directional thesis (positive catalyst + rally) at a much lower cost than the $45 calls

- 🛡️ Defined risk: you can only lose the net debit paid (roughly $2.50-$3.50 per spread depending on fill)

- 💰 Max profit: $10 per spread minus debit paid (~$6.50-$7.50 gain) if MLYS above $40 at expiry

- 📈 The $30 strike is only 4.7% above current price - achievable on moderate good news

- 🎯 Profits fully at $40, which is below the 52-week high and within the analyst target range

- ⏰ April expiration captures EXPLORE-OSA data, Q4 earnings (March 18), and potential NDA acceptance

Position sizing: Risk no more than 2-3% of portfolio given the binary catalyst risk. 20 spreads at ~$3 each = ~$6,000 risk for ~$14,000 max profit.

Risk level: Moderate (defined risk, binary catalyst exposure) | Skill level: Intermediate

⚖️ Balanced: "Straddle the Data" - April Long Straddle

Play: Buy the MLYS April 17 $30 call AND buy the April 17 $30 put

Why this works:

- 🎯 You do NOT need to predict the direction - you profit from a big move in either direction

- 📊 With the options market pricing a ±22% move by March OPEX alone, a straddle captures volatility regardless of whether EXPLORE-OSA data is positive or negative

- 🧬 Binary biotech catalysts are ideal for straddles - the stock will likely move sharply one way or the other

- 💰 Breakeven roughly $23 on the downside and $37 on the upside (depending on straddle cost)

- 🔬 You are effectively betting that the implied volatility is underpricing the actual move - a reasonable assumption ahead of clinical data in a small-cap biotech

Position sizing: 10-20 contracts per leg at roughly $5-6 combined per straddle = $5,000-$12,000 risk. You need a ~20%+ move to profit.

Risk level: Moderate-High (can lose full premium if stock doesn't move enough) | Skill level: Intermediate-Advanced

🚀 Aggressive: "Follow the Whale" - April $40 Calls

Play: Buy MLYS April 17 $40 calls outright

Why this works (and why it's risky):

- 💥 Lower strike ($40 vs $45) means higher delta and a more achievable target

- 📊 $40 is within the analyst target range and below the 52-week high of $47.65

- ⏰ Same April expiration captures all the near-term catalysts

- 🎯 If MLYS hits $50 on a combination of positive catalysts, these calls would be worth ~$10, potentially a 5-8x return on a likely ~$1.50-2.50 entry

- 🐋 Directionally aligned with the institutional flow but at a more reasonable strike

Why it could blow up:

- 📈 Still needs a +39% rally to reach the $40 strike from $28.66

- ⏰ Only 49 days of time - short fuse for such a large move

- 🧬 If EXPLORE-OSA data disappoints, these expire worthless

- 💸 100% loss of premium is the most likely individual outcome

Position sizing: Risk ONLY what you can afford to lose completely. 50 contracts at ~$2 each = ~$10,000 at risk.

Risk level: HIGH (can lose 100% of premium, binary catalyst bet) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Strike is 57% OTM with 49 days to expiration: The $45 strike requires MLYS to rally from $28.66 to $45+ in under two months. That's the kind of move that typically only happens on a transformative catalyst - FDA approval, M&A, or a combination of multiple positive events in rapid succession. The probability of these calls finishing in-the-money at expiration is low.

-

🧬 Binary clinical data risk: EXPLORE-OSA is a Phase 2 proof-of-concept trial in a novel indication for the ASI drug class. Phase 2 trials fail roughly 35-45% of the time. A negative readout would not destroy the core lorundrostat thesis, but it would dampen the bull case and likely push the stock toward $24-26.

-

📊 Heavy insider selling is a red flag: MLYS insiders sold $70.9 million in stock over the past 90 days, including CEO Jon Congleton ($9.6M), CMO David Rodman ($570K), and Director Brian Slingsby ($1M stake). While some of this may be pre-planned 10b5-1 selling, the magnitude - especially the CEO selling at $45 and again at $32 - warrants attention.

-

⚔️ AstraZeneca's baxdrostat has a regulatory head start: Baxdrostat received FDA Priority Review with a Q2 2026 PDUFA target. If approved first, AstraZeneca's $220B+ commercial machine could lock up formulary positioning, specialty pharmacy relationships, and physician prescribing habits before lorundrostat even reaches the market. Being second-to-market in a same-mechanism class is a meaningful disadvantage.

-

💊 Pre-revenue biotech with no commercial infrastructure: MLYS has $0 in revenue and has never brought a drug to market. Building a sales force, securing payer coverage, and competing against AstraZeneca's established commercial network requires flawless execution. The $593.6M cash position helps, but money alone doesn't guarantee a successful launch.

-

📉 Stock already down 39% from highs - could this be "catching a falling knife"? MLYS peaked at $47.65 in November 2025 and has steadily declined since. The decline isn't purely technical - it reflects insider selling, competitive concerns, and the natural post-NDA-filing "now what?" uncertainty that many biotechs experience. The unusual call buying today could represent informed positioning, or it could be speculative retail driven by the imminent catalyst.

-

⏰ Time decay on cheap OTM options is deceptive: At $1.00 per contract, this may feel cheap, but OTM options with 49 days to expiration lose value rapidly. If MLYS doesn't move meaningfully toward $45 within the next 2-3 weeks, theta decay will erode the position aggressively - even if the stock modestly rallies.

🎯 The Bottom Line

Here's the deal: Someone spent $2.3 million buying 23,000 MLYS April $45 calls at $1.00 each. This is not a hedge. This is not a covered call roll. This is a pure, speculative, catalyst-driven bet that Mineralys Therapeutics will make a dramatic move higher in the next 49 days.

What this trade tells us:

- 🎯 Someone believes a major positive catalyst is imminent - most likely EXPLORE-OSA Phase 2 data or FDA NDA acceptance

- 💰 At $1.00 per contract, the risk/reward is highly asymmetric: $2.3M at risk for potentially $20M+ if the stock reaches $55

- 📊 The 319% increase in call volume over normal levels is notable, especially on a day with no public news

- ⏰ The April 17 expiration is calibrated to capture the Q1 catalyst window: EXPLORE-OSA data (any day), Q4 earnings (March 18), and potential NDA acceptance (Q1-Q2)

This IS a bullish signal, but context matters: The $45 strike is 57% away. These calls have roughly a 10-15% probability of finishing in-the-money at expiration based on current implied volatility. The trader knows this - they are buying lottery tickets with favorable asymmetry, not making a high-probability bet. This type of flow is common in clinical-stage biotechs ahead of binary catalysts, and it does NOT guarantee the outcome.

If you're bullish on MLYS:

- ✅ Use defined-risk strategies (call spreads) rather than naked OTM calls - the $30/$40 call spread gives you catalyst exposure with much better odds

- 📊 Watch the $30 gamma resistance level - a breakout above $30 is your first confirmation signal

- 📅 Mark March 18 (Q4 earnings) as the first scheduled catalyst checkpoint

- 🧬 Monitor EXPLORE-OSA data announcements daily - this is the trigger

If you're watching from the sidelines:

- 📊 Wait for the EXPLORE-OSA data readout before committing capital - there is no edge in guessing Phase 2 results

- 🎯 The analyst consensus target of $47.29 with a high of $56 from HC Wainwright shows meaningful Street optimism, but that's predicated on successful NDA approval and commercial execution

- 💰 The $593.6M cash position (funded into 2028) eliminates near-term dilution risk, which is a genuine positive for the equity story

- ⚖️ A straddle or strangle strategy lets you profit from the expected volatility without betting on direction

If you're cautious:

- ⚠️ The insider selling pattern is concerning - CEO selling at $45 and again at $32 is not a confidence-inspiring signal

- ⚔️ AstraZeneca's baxdrostat has a clear regulatory lead and massive commercial advantages as the likely first-to-market ASI

- 📉 The bearish GEX bias and 39% drawdown from highs suggest the path of least resistance may still be sideways-to-lower absent a catalyst

- 🛡️ If you own shares, consider buying April puts as insurance ahead of the data readout

Key dates to mark:

- 📅 Any day now - EXPLORE-OSA Phase 2 topline data (Q1 2026 guidance, could drop any time)

- 📅 March 18, 2026 - Q4 2025 / FY2025 earnings (after market close)

- 📅 Q1-Q2 2026 - FDA NDA acceptance decision / PDUFA date

- 📅 Q2 2026 - AstraZeneca baxdrostat PDUFA decision (competitive read-through)

- 📅 April 17, 2026 - THIS TRADE EXPIRES - moment of truth for the $2.3M bet

Final verdict: This is a textbook biotech lottery-ticket trade. The trader spent $2.3M on deeply OTM calls ahead of a dense catalyst window, betting on a transformative outcome. The asymmetric payout profile - limited downside ($2.3M) with multi-bagger upside potential - is the core logic. For retail traders, the key lesson is this: you do not need to replicate the $45 strike. A $30/$40 call spread or a $30 straddle gives you catalyst exposure at a fraction of the cost and with far better probability. Let the whale take the aggressive bet - you can ride the same wave with smarter risk management.

The EXPLORE-OSA data readout is THE event to watch. Until it drops, this is all positioning and speculation. After it drops, the picture becomes much clearer. 💊

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Clinical-stage biotech options carry extreme binary risk - Phase 2 trials can fail, NDA filings can be rejected, and stock prices can decline 50%+ on negative catalysts. Always do your own research and consider consulting a licensed financial advisor before trading.

About Mineralys Therapeutics: Mineralys Therapeutics is a clinical-stage biopharmaceutical company focused on developing lorundrostat, an oral aldosterone synthase inhibitor for the treatment of hypertension, with a market cap of $2.3B in the Pharmaceutical Preparations industry. The company has filed an NDA with the FDA and is actively exploring additional indications including obstructive sleep apnea and chronic kidney disease.