💊 NUVB $9M Custom Spread - Pre-Approval Hedging Before Critical FDA Decision! 🎯

📅 December 17, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just unloaded $9 MILLION in bearish option spreads on Nuvation Bio at 2:38 PM! This massive sell-to-open custom spread (25K contracts at $10 strike + 19K at $5 strike expiring Dec 19 and Mar 20) signals smart money protecting gains ahead of the June 23, 2025 FDA approval decision. With NUVB trading at $8.56 near 52-week highs and up 456% from lows, institutions are booking profits just 6 months before the most critical catalyst in company history. Translation: Big money is buying insurance on their FDA lottery tickets!

📊 Company Overview

Nuvation Bio Inc. (NUVB) is a clinical-stage biopharmaceutical company on the verge of commercialization:

- Market Cap: $2.97 Billion

- Industry: Pharmaceutical Preparations (Oncology Focus)

- Current Price: $8.56 (52-week range: $1.54 - $3.97... wait, current price is ABOVE the 52-week high!)

- Primary Business: Developing taletrectinib (IBTROZI™) for ROS1+ lung cancer, safusidenib for brain cancer

- Headquarters: San Francisco, CA | Employees: 291

💰 The Option Flow Breakdown

The Tape (December 17, 2025 @ 14:38:26):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:38:26 | NUVB | ASK | SELL | CALL $10 | 2026-03-20 | $2.4M | $10 | 25K | - | 25,000 | $8.56 | $0.96 | NUVB20260320C10 |

| 14:38:26 | NUVB | ASK | SELL | CALL $5 | 2025-12-19 | $6.6M | $5 | 19K | 22K | 19,000 | $8.56 | $3.47 | NUVB20251219C5 |

🤓 What This Actually Means

This is a sophisticated custom spread designed to cap upside and generate cash NOW! Here's what went down:

- 💸 Massive premium collected: $9M total ($2.4M from March calls + $6.6M from December calls)

- 🎯 Two-legged structure: Sold 25K March $10 calls (16.8% above spot) + 19K December $5 calls (41.6% below spot, deep ITM!)

- ⏰ Strategic timing: 2 days until Dec 19 expiration (short leg) and 93 days to March 20 (long leg) - both BEFORE June 23 FDA decision

- 📊 Asymmetric sizes: ~1:1 ratio suggests covered call strategy on existing long position

- 🏦 Institutional profit-taking: This trader is monetizing biotech gains after massive 456%+ rally from $1.54 lows

What's really happening here: This trader likely accumulated MASSIVE shares or calls at much lower prices (probably sub-$3) during the clinical stage. Now with stock at $8.56 and trading at 3x market cap from a year ago, they're systematically capping upside at $10 (March calls) while generating immediate cash from selling December $5 deep ITM calls. The December calls act as a "synthetic short" against their long position - collecting $6.6M in premium that offsets any drop below $5.

Think of it like this: They're saying "I'll let my shares get called away at $10 by March if FDA approval is priced in early, but I'm taking $9M cash RIGHT NOW to reduce risk if something goes wrong."

Unusual Score: 🔥 EXTREME

- March $10 calls: Z-score of 225.23 (EXTREMELY_UNUSUAL) - 29x average daily volume!

- December $5 calls: Z-score of 10.55 (EXTREMELY_UNUSUAL) - nearly 1:1 with open interest ratio

- This happens maybe 2-3 times a year in small-cap biotech names! We're talking about an institution cashing out $9M in premium in a single order block.

📈 Technical Setup / Chart Check-Up

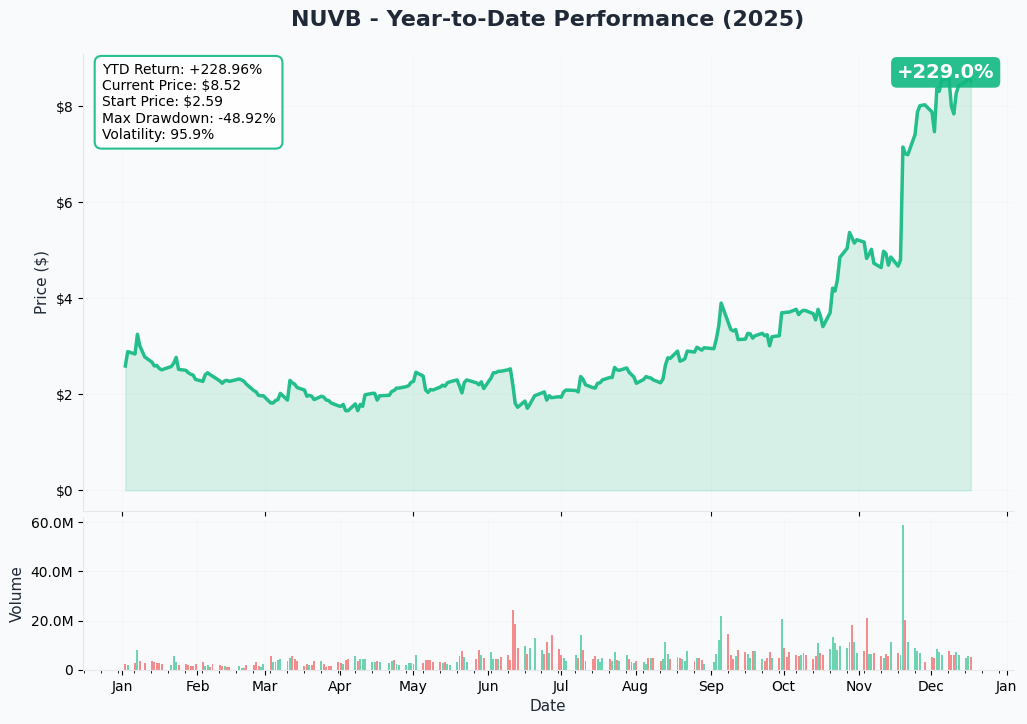

YTD Performance Chart

NUVB is on an absolute MOON MISSION - current price of $8.56 represents a +456% gain from the $1.54 52-week low (though data shows historical range ended at $3.97). The chart tells a compelling FDA approval narrative - after testing lows around $1.50-2.00 during mid-2024 clinical uncertainty, NUVB has rocketed higher on priority review designation and approaching PDUFA date.

Key observations:

- 🚀 Explosive breakout: Vertical move from sub-$3 in late 2024 to $8+ in December 2025

- 📈 Priority Review catalyst: October 2024 announcement of FDA Priority Review with June 23, 2025 PDUFA date ignited institutional buying

- 🎢 High volatility: Biotech binary events create massive swings - this isn't a stable dividend stock

- 📊 Volume acceleration: Smart money loading up as FDA decision approaches

- ⚠️ Parabolic rally warning: Nearly tripled in recent months - classic "buy the rumor, sell the news" setup

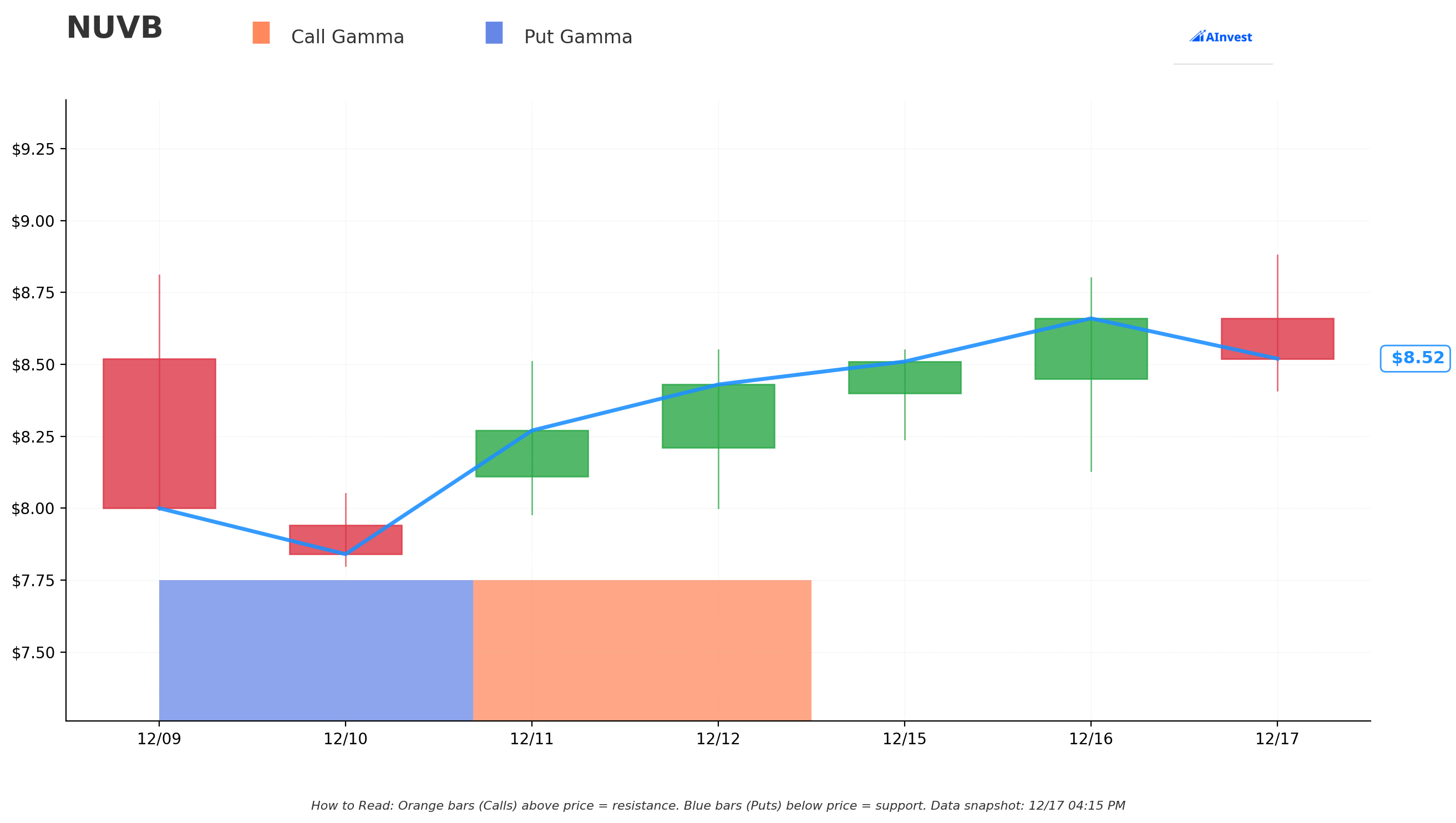

Gamma-Based Support & Resistance Analysis

Current Price: $8.56

The gamma exposure map reveals critical price levels where options activity creates natural floors and ceilings:

🔵 Support Levels (Put Gamma Below Price):

- $7.50 - Strongest support zone with 2.42B total gamma exposure (12.4% below current price)

- Call GEX: 1.26B | Put GEX: 1.17B | Net GEX: +0.09B (slightly bullish bias)

- This is THE FLOOR - dealers will aggressively buy dips here to hedge exposure

🟠 Resistance Levels (Call Gamma Above Price):

- $10.00 - MASSIVE resistance ceiling with 0.40B gamma (16.8% above current price) ⚡

- Call GEX: 0.39B | Put GEX: 0.01B | Net GEX: +0.38B (heavy call skew)

- This is exactly where the 25K call seller struck! NOT coincidental

- Market makers holding enormous call positions here will sell into rallies

What this means for traders: NUVB is trading in a WIDE zone between $7.50 support and $10 resistance. The gamma data shows the $10 level has massive call open interest (0.39B) which creates natural selling pressure as price approaches. This setup screams "institutional cap on upside" before the FDA decision. The call seller chose $10 strategically - it's the gamma ceiling where dealers will help suppress breakouts.

Notice anything? The call seller struck EXACTLY at $10 where there's 0.39B call gamma - the single largest resistance level. They're positioning at the technical ceiling, betting that pre-FDA volatility keeps stock range-bound below $10 through March. Smart positioning.

Net GEX Bias: Bullish (2.64B call gamma vs 1.35B put gamma) - Overall positioning remains bullish, but $10 ceiling creates cap.

Implied Move Analysis

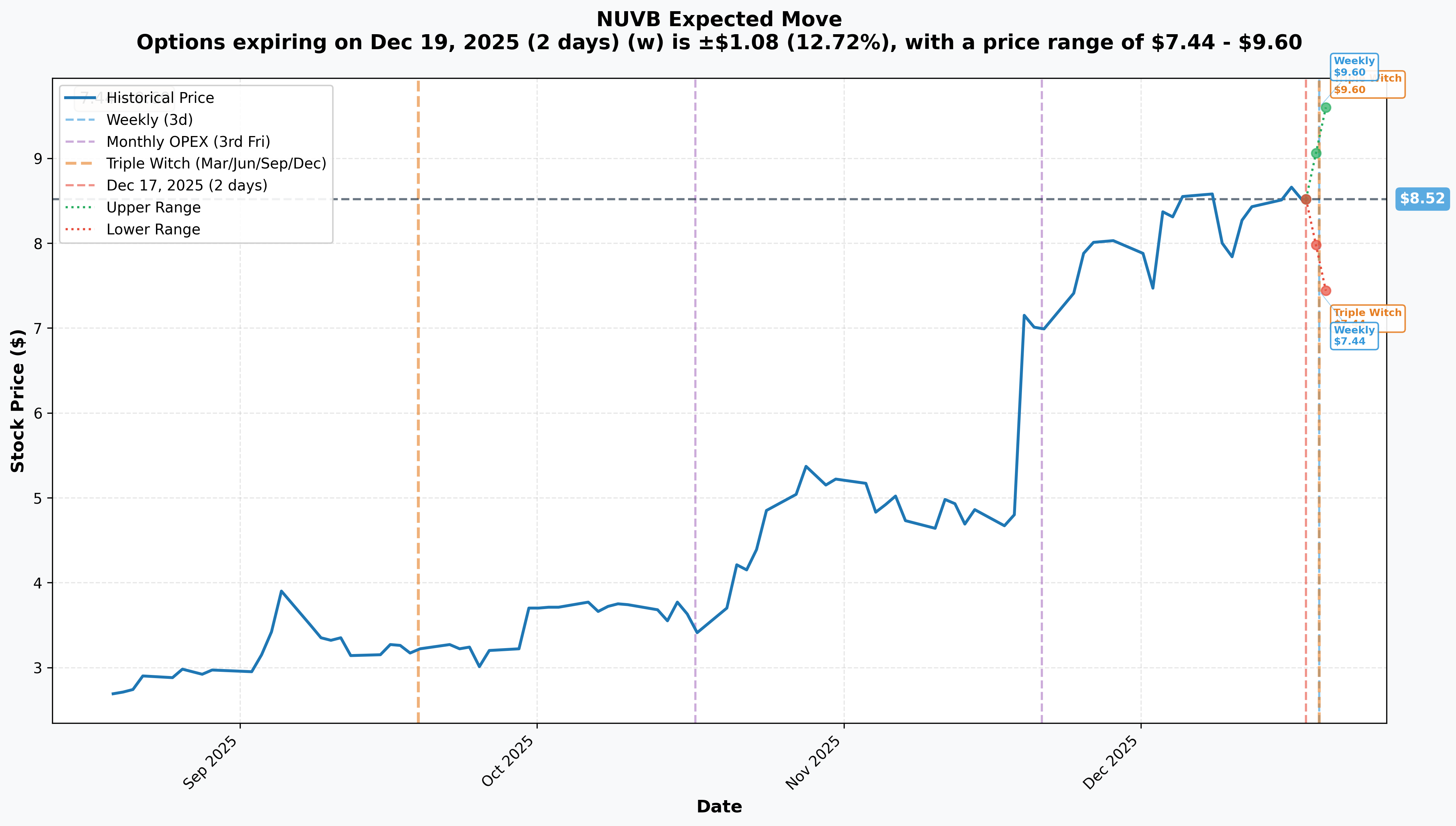

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 2 days!): ±$1.08 (±12.72%) → Range: $7.44 - $9.60

- 📅 Monthly OPEX (Dec 19 - 2 days): ±$1.08 (±12.72%) → Range: $7.44 - $9.60

- 📅 Quarterly Triple Witch (Dec 19 - 2 days): ±$1.08 (±12.72%) → Range: $7.44 - $9.60

Translation for regular folks: Options traders are pricing in a 12.7% move ($1.08) by Friday's expiration - that's HUGE for a 2-day window! The market expects wild volatility heading into year-end, likely driven by portfolio rebalancing, tax-loss harvesting completion, and positioning ahead of the January-June FDA catalyst window.

The tight time frame (2 days) with high implied vol shows traders are preparing for explosive moves. Notice the upper range of $9.60 is JUST BELOW the $10 gamma resistance - the market is essentially pricing in a ceiling at that level, perfectly aligned with the call seller's thesis.

Key insight: The 12.7% implied move means the market sees equal probability of a move to $7.44 (13% drop) or $9.60 (12% rally) by Friday. This violent two-way risk is why sophisticated players are selling premium to collect fat IV - they're betting the stock stays range-bound despite the wild expectations.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

FDA Approval Decision - June 23, 2025 (186 DAYS AWAY!) ⭐⭐⭐⭐⭐

The FDA assigned a PDUFA goal date of June 23, 2025 for taletrectinib (IBTROZI™) to treat adult patients with advanced ROS1-positive non-small cell lung cancer. This is THE catalyst that will determine NUVB's fate:

- 🏆 Priority Review Status: FDA shortened standard 10-month review to 6 months, recognizing unmet medical need

- 💰 Approval Triggers $200M Financing: Sagard Healthcare Partners committed $150M royalty + $50M debt upon approval by September 30, 2025

- 🎯 Best-in-Class Data: 90% response rate and 44.6-month median PFS from TRUST-I/II trials

- 📊 Line-Agnostic Indication: Can be used in both first-line and post-TKI settings (broader market)

- 🏥 Market Opportunity: ~3,000 U.S. advanced ROS1+ NSCLC cases annually, potential $640M-$1B peak sales

Probability Assessment: High (75-85%)

The strength of clinical data (90% ORR significantly exceeds Bristol Myers' Augtyro 38% ORR), Priority Review, Breakthrough Therapy Designation, and clean NDA acceptance all point toward approval. However, regulatory risk always exists - any FDA requests for additional data could delay or derail approval.

Why this matters for the option trade: The March 20 expiration ($10 calls sold) expires 95 days BEFORE the FDA decision. The trader is betting NUVB stays below $10 through March even as approval anticipation builds. If stock runs to $12-15 in March on pre-approval hype, they're capped at $10 - leaving money on the table. But if FDA delays or stock consolidates, they keep the $2.4M premium.

NCCN Guidelines Inclusion - July-August 2025 (Expected ~90 days post-approval) 📋

Following FDA approval, taletrectinib is expected to be added to National Comprehensive Cancer Network Clinical Practice Guidelines as a Preferred Agent:

- 🏥 Inclusion facilitates insurance coverage and reimbursement

- 💰 Drives physician adoption and prescribing patterns

- 🎯 Establishes taletrectinib as standard-of-care for ROS1+ NSCLC

- 📈 Historical precedent shows NCCN inclusion often occurs within 60-90 days of FDA approval

U.S. Commercial Launch - July-September 2025 🚀

With $502.7M cash position and $250M secured financing, NUVB is well-capitalized to execute commercial launch:

- 💼 New CFO Philippe Sauvage (appointed October 2024) brings commercialization expertise

- 🏢 Pre-commercial hiring and infrastructure build-out underway

- 📊 Analyst revenue projections: $20M in 2025, $122M in 2026, $233M in 2027

- ⚠️ EXECUTION RISK: First-time commercial company with no prior product launches

Competitive Positioning: Faces established players Rozlytrek (Roche, ~$170M sales) and Augtyro (Bristol Myers, $38M sales), but taletrectinib's superior efficacy (90% vs 38% ORR) provides differentiation.

China NRDL Inclusion - January 1, 2026 (Effective Date!) 🇨🇳

Major international catalyst as taletrectinib (DOVBLERON®) was included in China's 2025 National Reimbursement Drug List:

- 📅 Reimbursement effective January 1, 2026 (2 weeks away!)

- 🤝 Innovent Biologics exclusively commercializing in Greater China

- 💰 NRDL inclusion dramatically expands patient access through insurance coverage

- 📈 Additional revenue stream diversifies beyond U.S. market

- 🌏 China NMPA approved taletrectinib in January 2025, commercial launch complete

Q4 2024 & Q1 2025 Earnings Reports 📊

Q4 2024 (Reported March 6, 2025):

- 💵 Cash position: $502.7M as of December 31, 2024

- 🔬 R&D expenses: $29.3M for Q4 2024 (vs $15.4M in Q4 2023) - increased spend on commercialization prep

- 💸 Net loss: EPS forecast -$0.14

Q1 2025 (Expected Late April 2025):

- 📈 Final update before June PDUFA date

- 🎯 Key metrics: Commercial team hiring, payer engagement progress, FDA interactions during review

- 🧪 Safusidenib Phase 3 enrollment updates

Safusidenib Phase 3 Trial Progression - Ongoing 🧠

NUVB enrolled first patient in G203 study (Phase 3) on October 23, 2025:

- 🎯 Target: ~300 patients with high-grade IDH1-mutant astrocytoma (brain cancer)

- 📊 Primary endpoint: Progression-free survival (PFS) - FDA agreed PFS supports full approval

- 💪 Phase 2 data: 44% ORR, 88% PFS at 24 months

- ⏰ Long trial duration (PFS endpoint) - results likely 2027-2028

- 💰 Market opportunity: ~2,400 U.S. IDH1-mutant glioma diagnoses annually

📊 Past Catalysts (Already Happened)

FDA Priority Review Granted - December 2024 ✅

The U.S. FDA accepted Nuvation Bio's NDA for taletrectinib and granted Priority Review in December 2024. This shortened the standard 10-month review to 6 months, assigning the June 23, 2025 PDUFA date.

World Conference on Lung Cancer Data Update - September 2025 ✅

At IASLC 2025 in Barcelona, NUVB presented updated TRUST-I and TRUST-II results:

- 🏆 TRUST-I: 90.3% ORR in TKI-naïve patients, 44.6-month median PFS (longest in class!)

- 🏆 TRUST-II: 85.2% ORR, longest DOR of 30.4 months

- 🧠 Intracranial response: 87.5% in patients with brain metastases

Sagard Healthcare Non-Dilutive Financing - March 2025 ✅

NUVB secured $250M in non-dilutive financing from Sagard Healthcare Partners:

- 💰 $150M royalty interest financing (triggered on FDA approval)

- 💵 $50M debt (triggered on FDA approval)

- 📈 Optional $50M debt after first commercial sale

- 🎯 Management stated this creates "path to potential profitability without additional fundraising"

Pipeline Rationalization - August-Late 2024 ✅

NUVB paused development of NUV-868 (BET inhibitor) and discontinued NUV-1511 (drug-drug conjugate), narrowing focus to taletrectinib and safusidenib. This streamlines capital allocation toward highest-probability assets.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through March 20 expiration:

📈 Bull Case (30% probability)

Target: $11-$13

How we get there:

- 🚀 FDA review progressing smoothly - positive AdCom meeting or no major questions from FDA

- 📊 Q1 2025 earnings (late April) shows strong commercialization progress and raises confidence

- 💰 Additional institutional buying ahead of June PDUFA date

- 🎯 Street raises price targets on high approval probability - current consensus $8.43 could move to $10-12

- 🌟 Breakthrough data from safusidenib Phase 3 or partnership announcement

- 📈 Biotech sector rally lifts all boats (XBI up 15-20%)

- 🇨🇳 Strong China launch momentum from January NRDL inclusion beats expectations

Why this is lower probability (30%): Stock already priced at $8.56 represents significant premium to pre-approval companies. Breaking through $10 gamma resistance requires sustained momentum and perfect execution. The March 20 expiration is still 95 days before FDA decision - most upside likely comes closer to June catalyst.

🎯 Base Case (50% probability)

Target: $7.50-$10 range (CONSOLIDATION)

Most likely scenario:

- ⚖️ FDA review progressing normally - no major red flags but no early signals either

- 📊 Q1 earnings in-line with expectations, commercialization prep on track

- 💤 Stock consolidates recent gains, trading between $7.50 gamma support and $10 gamma resistance

- 🔄 Volatility remains elevated (implied vol 50-60%) but no sustained breakout either direction

- 🤷 Investors wait for June PDUFA date clarity before adding aggressively

- 📉 Some profit-taking after massive rally from $1.54 to $8.56 (456% gain!)

- 🇨🇳 China launch progresses but doesn't move needle significantly yet

- 💰 IV crush post-December expiration as year-end volatility subsides

This is the call seller's ideal scenario: Stock stays below $10 through March 20, March calls expire worthless, they keep $2.4M premium. The December $5 calls (deep ITM) either expire or get exercised, generating additional cash. Total profit ~$9M on reduced exposure while maintaining some upside through underlying shares.

Why 50% probability: Most realistic outcome given timing - too early for major FDA catalyst but enough positive thesis to prevent crash. Gamma support at $7.50 provides floor, resistance at $10 provides ceiling. Classic "wait and see" period.

📉 Bear Case (20% probability)

Target: $5.50-$7.50 (TEST THE GAMMA SUPPORT!)

What could go wrong:

- 😰 FDA issues Complete Response Letter (CRL) or requests additional data - approval delayed beyond June

- 🚨 Safety signal emerges during FDA review requiring further investigation

- 💸 Broader biotech selloff (XBI down 20%+) on sector rotation or risk-off environment

- 📉 Competitor announces superior data - Nuvalent's zidesamtinib shows better efficacy

- 🇨🇳 China launch disappoints - NRDL pricing too restrictive or adoption slower than expected

- ⏰ Commercial launch prep encounters issues - key hires leave or infrastructure delays

- 💰 Market realizes valuation stretched at $3B market cap for pre-revenue company

- 📊 Q1 earnings shows higher-than-expected cash burn or commercialization cost overruns

- 🔨 Break below $7.50 gamma support triggers cascade selling to $6-7 range

Critical support levels:

- 🛡️ $7.50: Major gamma floor (2.42B total GEX) - MUST HOLD or momentum shifts bearish

- 🛡️ $5.00: Deep support where December calls were sold - catastrophic scenario

Probability assessment: Only 20% because FDA approval probability is high (75-85%) based on clinical data and regulatory precedent. NUVB's fundamentals remain strong ($502.7M cash, secured financing, best-in-class data). However, binary biotech risk is always present.

💡 Trading Ideas

🛡️ Conservative: Wait for FDA Approval Clarity

Play: Stay on sidelines until FDA approval or clear rejection signal

Why this works:

- ⏰ FDA decision in 186 days creates massive binary event risk - too early to predict outcome

- 💸 Implied volatility at 50-60% makes options EXTREMELY expensive

- 📊 Stock at $8.56 represents 3x increase from $2.63 just 6 months ago - significant appreciation already captured

- 🎯 Better entry likely post-approval around $6-8 if stock consolidates, or $12+ if approval confirmed

- 📉 Historical biotech pattern: Pre-approval companies often sell off even on approval (buy rumor, sell news)

- 🤔 The $9M institutional call selling signals smart money is WORRIED about giving back gains

Action plan:

- 👀 Monitor FDA review process for any Refuse-to-File letters or additional information requests

- 🎯 If FDA approval occurs June 23, wait 2-3 weeks for IV crush and initial volatility to subside

- ✅ Post-approval entry around $6-8 offers better risk/reward if commercialization executes

- 📊 Watch Q1 2025 earnings (late April) for commercialization readiness and cash burn

- ⏰ Revisit July-August 2025 when NCCN guidelines inclusion and initial sales data provide validation

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 30-50% drawdown if FDA rejects or delays. Get better entry if stock consolidates post-approval.

⚖️ Balanced: Small Long Stock Position with March Covered Calls

Play: Buy small stock position, sell covered calls at $10 strike (March 20) - copy the institutional trade!

Structure:

- Buy 1000 shares NUVB at $8.56 = $8,560 investment

- Sell 10 March 20 $10 calls at ~$0.96 = $960 premium collected

Why this works:

- 📊 Capture upside to $10 (+16.8% stock appreciation + 11.2% call premium = 28% total return)

- 💰 Collect $960 premium reduces cost basis from $8.56 to $7.60 (11.2% cushion)

- 🎯 If stock stays below $10, keep shares AND premium - can repeat in April/May

- 🛡️ Gamma resistance at $10 makes breakout unlikely before March expiration

- ⏰ 93 days to expiration - expires well before June PDUFA date

- 🤝 Essentially "copying" the smart money positioning at better risk-adjusted sizing

Estimated P&L:

- 📈 Best case (stock at $10+): $1,440 profit + $960 premium = $2,400 total (28% ROI in 3 months)

- 📊 Neutral case (stock $8-10): Keep shares, collect $960 premium, roll calls forward

- 📉 Downside protection: Cost basis reduced to $7.60 (11.2% cushion vs $8.56 entry)

- 💀 Worst case: Stock drops to $5 = -$3,560 loss on stock, offset by $960 premium = -$2,600 net loss (but you'd still own shares into FDA approval)

Position sizing: Risk only 3-5% of portfolio (this is pre-revenue biotech - high risk!)

Exit strategy:

- 🎯 If stock hits $9.80-$10 before March, consider closing calls early and taking profit

- 📊 If calls exercised at $10, evaluate re-entry post-assignment based on FDA timing

- ⏰ If stock stays below $10, roll calls to April/May $11-12 strike for additional premium

Risk level: Moderate (stock ownership risk, capped upside) | Skill level: Intermediate

🚀 Aggressive: Pre-FDA Approval Long Call Spread (ADVANCED ONLY!)

Play: Buy call spread betting on FDA approval anticipation rally

Structure:

Why this could work:

- 🎯 Targets move from $8.56 to $12-15 range as FDA approval approaches

- 💰 Defined risk spread ($5 wide = $500 max loss per spread)

- ⏰ June 20 expiration captures all pre-PDUFA momentum (decision June 23)

- 📊 Analyst price targets $8.43 average with high-end $12.60 - potential for targets to increase

- 🚀 Historical biotech pattern: Pre-approval companies often rally 50-100% in weeks before PDUFA

- 📈 June options capture Q1 earnings catalyst, commercial prep updates, and approval anticipation

Why this could blow up (SERIOUS RISKS):

- 💸 HIGH RISK: June calls still expensive due to high IV - spread costs $2-3 ($200-300 per spread)

- ⚠️ FDA REJECTION: Complete Response Letter or delay destroys trade - stock could drop to $3-5 (-50-60%)

- 😱 EARLY ASSIGNMENT RISK: June expiration is 3 days BEFORE PDUFA date - might expire before approval announced

- 📊 IV CRUSH: Even if FDA approves, stock could sell off on "buy rumor, sell news" - limited upside capture

- 🎢 BINARY EVENT: This is pure speculation on FDA outcome - not suitable for risk-averse investors

- ⏰ Need 17-40% move to breakeven after spread costs factored in

Estimated P&L:

- 💰 Cost: ~$2.50 per spread (mid-point estimate)

- 📈 Profit scenario: Stock moves to $13-15 pre-approval = $2.50-4.50 gain (100-180% ROI)

- 🚀 Home run: FDA approves early or positive AdCom = stock to $15-18 = $5.00 max gain (200% ROI, capped)

- 📉 Loss scenario: FDA delays or rejection = lose entire $2.50 (100% loss)

- 💀 Total loss: CRL announced = -$250 per spread (100% loss)

Breakeven point: Stock needs to reach ~$12.50 by June 20 expiration (46% gain from current levels)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand biotech binary risk and can lose ENTIRE premium

- ✅ Have researched FDA approval precedents for oncology Priority Review applications

- ✅ Accept that June 20 expiration is 3 days BEFORE PDUFA - timing risk!

- ✅ Can monitor FDA communications and ODAC meetings for early signals

- ✅ Understand this is pure speculation on regulatory outcome

- ⏰ Plan to close spread by June 15-18 to avoid overnight PDUFA risk

Alternative safer structure: Wait until May to enter - better timing visibility, lower cost, similar upside

Risk level: EXTREME (can lose 100% of premium on FDA rejection) | Skill level: Advanced only

Probability of profit: ~35% (requires 46% stock rally AND FDA approval - both high bars)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ FDA Binary Event Risk (186 days away): The June 23, 2025 PDUFA date creates MASSIVE volatility risk. FDA approval probability is high (75-85%) based on Priority Review, Breakthrough Therapy Designation, and strong clinical data (90% ORR, 44.6-month PFS). However, regulatory risk always exists - FDA could request additional data, impose label restrictions, or issue Complete Response Letter. Stock could gap 50-70% on approval OR drop 40-60% on rejection. This is the ultimate binary event.

-

💸 Valuation Extended at $3B Market Cap: Trading at $2.97B market cap for a pre-revenue company with peak sales estimates of $640M-$1B. Already priced for significant approval probability and successful commercialization. Stock up 456% from $1.54 lows - much of "approval premium" already captured. Analyst consensus $8.43 suggests current price near fair value assuming approval. Limited upside cushion if approval doesn't translate to revenue.

-

🏥 First-Time Commercial Execution Risk: NUVB has 291 employees and zero commercialization track record. Building sales infrastructure, securing payer contracts, and driving physician adoption requires expertise the company is developing in real-time. New CFO Philippe Sauvage (appointed October 2024) brings experience, but competing against Roche and Bristol Myers' established infrastructures is challenging. Early sales velocity will be critical - underwhelming launch could disappoint even with FDA approval.

-

🏆 Competitive ROS1 Market Underwhelming Historically: Combined sales of Rozlytrek (Roche, ~$170M) and Augtyro (Bristol Myers, $38M) reached only ~$200M in 2024 despite Big Pharma backing and expensive acquisitions. The rare patient population (~3,000 U.S. advanced cases annually) inherently limits addressable market. Investors remain "generally skeptical" about commercial opportunity despite taletrectinib's superior data. Market may not support multiple high-priced competitors.

-

⚔️ Emerging Competition from Nuvalent: Nuvalent's zidesamtinib showed "competitive pivotal data" and is expected to file for FDA approval in 2025-2026. This could create a two-horse race in next-generation ROS1 inhibitors, fragmenting market share and pressuring pricing. First-mover advantage helps, but if Nuvalent shows superior data or commercial execution, NUVB's thesis weakens significantly.

-

🇨🇳 China Revenue Uncertainty Despite NRDL Inclusion: While taletrectinib inclusion in China's 2025 NRDL (effective January 1, 2026) expands access, actual uptake depends on Innovent Biologics' commercial execution and pricing dynamics. NRDL pricing negotiations often result in steep discounts (60-70% off list price), limiting revenue potential. Royalty rates to NUVB not publicly disclosed - China revenue may not move needle significantly.

-

📊 Pipeline Concentration Risk After Discontinuations: With NUV-868 paused and NUV-1511 discontinued, NUVB is now a two-asset company (taletrectinib + safusidenib). Safusidenib Phase 3 won't read out until 2027-2028 given PFS primary endpoint in rare disease population (~300 patient trial). If taletrectinib commercial launch underwhelms, company has limited near-term pipeline diversification.

-

💰 Cash Burn Acceleration for Commercial Launch: Q4 2024 R&D expenses nearly doubled to $29.3M vs $15.4M in Q4 2023, driven by commercialization prep. With $502.7M cash, quarterly burn of ~$40M+ suggests ~12 quarter runway. The $250M Sagard financing helps but triggers only upon approval. If approval delayed or launch costs exceed expectations, could face dilution risk in 2026-2027.

-

🎢 Extreme Biotech Volatility Creates Whipsaw Risk: NUVB's 456% rally from $1.54 to $8.56 shows explosive potential BUT also highlights violent swings. Biotech stocks routinely gap 20-40% on binary events. The current $8.56 price could easily be $5 or $13 within weeks based on FDA communication. Historical precedent shows even approved drugs often sell off initially on "buy rumor, sell news" - Augtyro approval didn't save Bristol Myers from underperformance.

-

🛡️ Massive Institutional Put/Call Selling Signals Smart Money Caution: The $9M custom spread (selling $10 calls + $5 calls) by sophisticated institutions signals DEFENSIVE POSITIONING. When players managing hundreds of millions cap upside at $10 rather than staying fully long into FDA approval, it's a major caution flag. The 225x unusual size on March calls and 10x on December calls shows unprecedented hedging activity. Smart money is taking profits NOW rather than gambling on FDA outcome.

-

📉 Biotech Sector Volatility Affects All Boats: XBI (biotech ETF) correlation means NUVB moves with sector sentiment regardless of company-specific fundamentals. If biotech enters bear market (regulatory fears, drug pricing legislation, capital flight), NUVB drops 30-50% even with strong data. Macro headwinds or risk-off environment disproportionately impact pre-revenue biotech.

🎯 The Bottom Line

Real talk: Someone just pocketed $9 MILLION in option premium by systematically capping upside and generating cash 6 months before the biggest binary event in NUVB's history. This isn't bearish on the FDA approval - it's sophisticated portfolio management by institutions who've made MONSTER money on the 456% rally from $1.54 and don't want to risk giving it back.

What this trade tells us:

- 🎯 Sophisticated player expects CONSOLIDATION through March (not crash, not moon - range-bound $7.50-$10)

- 💰 They'd rather collect $9M premium NOW than gamble on $10+ breakout before FDA decision

- ⚖️ The dual expiration structure (Dec 19 + March 20) shows they're managing near-term volatility AND pre-PDUFA positioning

- 📊 They struck $10 calls at exact gamma resistance where dealers will suppress rallies - smart technical positioning

- ⏰ March expiration is 95 days BEFORE PDUFA - they're taking chips off table well in advance of binary event

This is NOT a "sell everything" signal - it's a "take profits and manage risk intelligently" signal.

If you own NUVB:

- ✅ Consider trimming 30-50% at $8-9 levels (lock in triple-digit gains from $2-3 entry)

- 📊 If holding through FDA approval, set MENTAL STOP at $7.00 (below gamma support) to protect remaining position

- ⏰ Don't get greedy - 456% gains are AMAZING. Protecting profits is professional.

- 🎯 If FDA approves June 23 AND stock pulls back to $6-8 post-approval, could re-enter for commercialization phase

- 🛡️ Consider selling covered calls at $10-12 strikes (3-6 months out) to generate income while waiting

If you're watching from sidelines:

- ⏰ June 23, 2025 is the moment of truth - DO NOT enter before FDA clarity!

- 🎯 Post-approval pullback to $6-8 would be EXCELLENT entry (30% off highs with approval validation)

- 📈 Looking for confirmation of: FDA approval, NCCN guidelines inclusion, early prescription data, payer contracts secured

- 🚀 Longer-term (12-24 months), commercial execution and safusidenib Phase 3 data are legitimate catalysts for $12-18 if both programs deliver

- ⚠️ Current valuation ($3B market cap pre-revenue) requires flawless execution - one stumble and it's back to $4-5

If you're bearish:

- 🎯 Wait for FDA decision before initiating shorts - fighting biotech approval momentum is dangerous

- 📊 First support at $7.50 (gamma floor), major support at $5.00 (call strike), catastrophe scenario <$3

- ⚠️ Post-FDA rejection or delay offers clearest short entry - approval uncertainty makes timing difficult

- 📉 Watch for break below $7.50 - that's the trigger for cascade to $6-7 range

- ⏰ May-June 2025 put spreads offer defined-risk way to play downside into PDUFA date

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - December $5 call expiration, triple witch, end of year volatility

- 📅 January 1, 2026 - China NRDL reimbursement effective date (watch for initial sales data)

- 📅 Late April 2025 - Q1 2025 earnings (final update before FDA decision)

- 📅 June 23, 2025 - FDA PDUFA goal date for taletrectinib approval ⭐⭐⭐⭐⭐

- 📅 July-August 2025 - Expected NCCN guidelines inclusion and U.S. commercial launch

- 📅 2027-2028 - Safusidenib Phase 3 data readout expected

Final verdict: NUVB's FDA approval catalyst on June 23, 2025 represents a high-conviction binary event with strong approval probability (75-85%) based on best-in-class clinical data (90% ORR, 44.6-month PFS), Priority Review, and Breakthrough Therapy Designation. BUT, at $8.56 with $3B market cap pre-revenue, much of the approval premium is already priced in. The $9M institutional call selling is a CLEAR signal: smart money is booking profits and managing risk at these levels.

Be patient. Let FDA approval occur. Look for better entry points $6-8 post-approval. The ROS1 lung cancer opportunity will still be here in 6-12 months, and you'll sleep better at night paying $7 instead of $9 with approval validation.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The extreme unusual scores (225x for March calls, 10x for December calls) reflect these specific trades' sizes relative to recent NUVB history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. FDA approval decisions create binary event risk with potential for 50-70% gaps either direction. Biotech investing carries substantial risk including potential for total loss. The option sellers may have complex portfolio hedging needs not applicable to retail traders.

About Nuvation Bio Inc.: Nuvation Bio Inc. is a clinical-stage biopharmaceutical company focused on developing differentiated therapeutic candidates for oncology, with a market cap of $2.97 billion in the Pharmaceutical Preparations industry. The company's lead asset, taletrectinib (IBTROZI™), has received FDA Priority Review for ROS1-positive non-small cell lung cancer with a PDUFA goal date of June 23, 2025.