💊 NVO $8M Put Close - Big Money Cashes Out Bearish Bet on Novo Nordisk After 58% Collapse!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed out $8 MILLION worth of $NVO $40 puts expiring May 15th -- buying to close an existing bearish position while the stock trades at $36.72, meaning these puts are deep in the money with $3.28 of intrinsic value per share. This is an institutional player locking in profits after riding Novo Nordisk down ~58% from its 2024 highs. With two analyst upgrades/downgrades hitting in the same week and a packed catalyst calendar ahead, the smart money is taking chips off the table on a stock that's already been crushed.

📊 Company Overview

Novo-Nordisk A/S (NVO) is the world's leading provider of diabetes care and obesity treatment products:

- Market Cap: $167.8B

- Industry: Pharmaceutical Preparations (Diabetes & Obesity Therapeutics)

- Exchange: NYSE (ADR)

- Current Price: $36.72 (down ~58% from June 2024 ATH of $142)

- Employees: 69,500

- Headquarters: Denmark

- Primary Business: With roughly one-third of the global branded diabetes treatment market, Novo Nordisk manufactures and markets insulins, GLP-1 therapies (Ozempic, Wegovy), oral antidiabetic agents, and obesity treatments. The company also has a biopharmaceutical segment specializing in protein therapies for hemophilia and other disorders.

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 10:07:00):

| Time | Symbol | Side | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | Z-Score | OI Signal | Spot | Vol/OI | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:07:00 | NVO | BUY | BTC | PUT | 2026-05-15 | $5.1M | $40 | 9,400 | 3.00 | CLOSE | $36.72 | 0.47 | NVO20260515P40 |

| 10:07:00 | NVO | BUY | BTC | PUT | 2026-05-15 | $2.9M | $40 | 14,000 | 4.64 | CLOSE | $36.72 | 0.70 | NVO20260515P40 |

🤓 What This Actually Means

This is a buy-to-close (BTC) on an existing long put position -- classic profit-taking! Here's the breakdown:

- 💸 Total premium paid to exit: ~$8M across two fills (9,400 + 14,000 = 23,400 contracts)

- 🎯 In-the-money by $3.28: $40 strike with NVO trading at $36.72 means each put has $3.28 of intrinsic value

- 📊 Z-Score of 4.64 on the larger fill: This level of activity shows up only a handful of times per year for $NVO. The 3.00 z-score on the other fill is also extremely unusual.

- 📉 Closing, not opening: The "CLOSE" OI signal confirms this trader is exiting a position, not making a new bet

- 🏦 Institutional footprint: Vol/OI ratio of 0.70 on the larger fill indicates high activity relative to existing open interest

What's really happening here:

This institution likely bought these $40 puts when $NVO was trading in the $45-$55 range -- possibly around the time of the 2026 guidance warning on February 4 or before the CagriSema REDEFINE-4 failure on February 23. With the stock now at $36.72, these puts have appreciated significantly. The trader is locking in a huge win.

The timing is telling: Morgan Stanley just upgraded NVO to Equal Weight this morning, suggesting the worst may be priced in. This put-closer seems to agree -- the easy money on the bearish side has already been made.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Novo Nordisk is in freefall territory in 2026. The stock has plunged from ~$47.73 in early December 2025 to $36.72 today -- a roughly 23% decline in just three months and a staggering 58% drop from the June 2024 all-time high of $142. The stock just hit a new 52-week low on March 2 following the Goldman Sachs downgrade.

Key observations:

- 📉 Relentless downtrend: No meaningful bounce since the February 4 earnings-day crash

- 💹 $36.72 = 52-week low territory: The stock just broke below $37 for the first time in over a year

- 🎢 Two catalytic drops: The stock fell ~18% on the 2026 guidance warning and another ~21% after the CagriSema failure

- 📊 Valuation compressed: Trading at just 10.24x trailing P/E, a fraction of its 5-year average of 27.8x

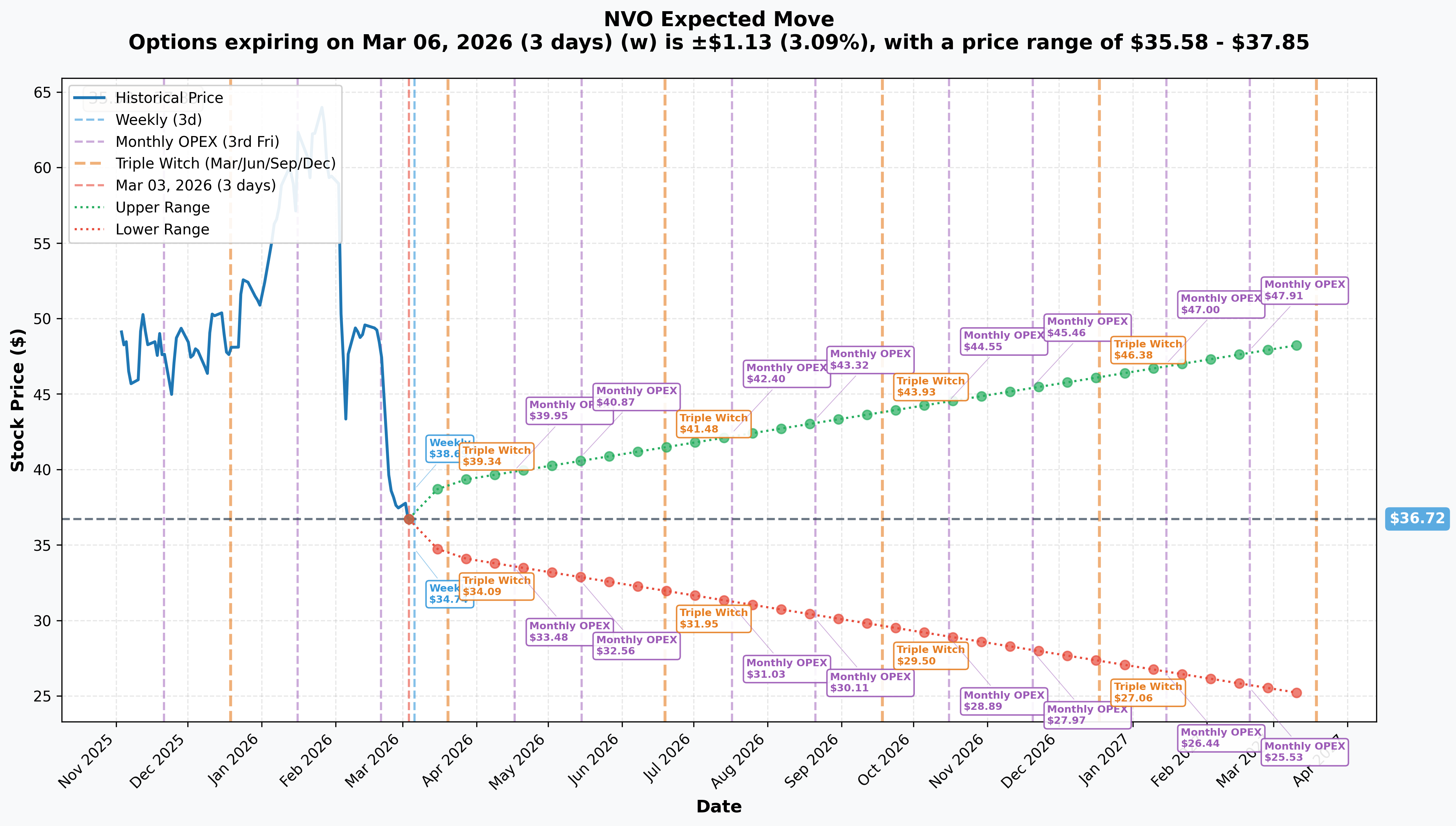

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 3 days): +/-$1.13 (+/-3.09%) --> Range: $35.58 - $37.85

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 17 days): +/-$2.44 (+/-6.66%) --> Range: $34.27 - $39.16

- 📅 May OPEX (May 15 - trade expiry): +/-$4.16 --> Range: $32.56 - $40.87

- 📅 LEAPS (Mar 2027 - 381 days): +/-$11.73 (+/-31.95%) --> Range: $24.99 - $48.45

Translation for regular folks:

Options traders are pricing in a 3.1% move (~$1.13) by Friday and a 6.7% move (~$2.44) by March expiration. That's elevated implied volatility for a pharma stock, reflecting the massive uncertainty around $NVO right now. The implied move through May 15 (this trade's expiration) stretches all the way from $32.56 to $40.87 -- notably, the $40 strike sits right at the upper edge of the expected range, which is why the put-closer decided it was time to cash out.

The LEAPS implied move of 31.95% tells the real story: the market sees $NVO as genuinely uncertain over the next year, with a range of $25 to $48. That's a massive spread for a $168B company.

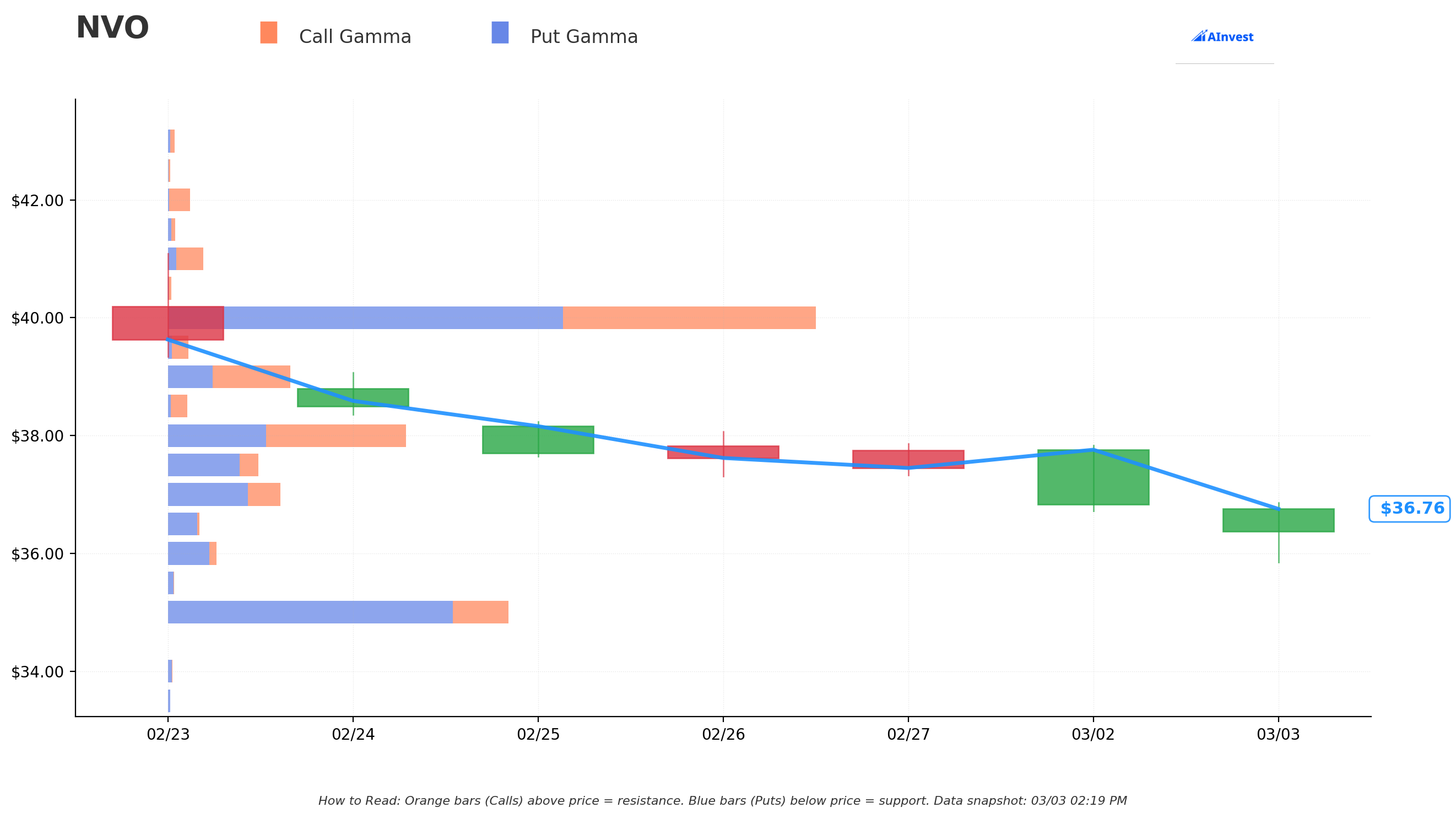

Gamma-Based Support & Resistance Analysis

Key gamma levels based on options positioning:

The gamma profile for $NVO shows concentrated interest at round-number strikes. Here are the levels that matter:

🔵 Support Levels (Put Gamma):

- $35 - Highest gamma concentration below current price; this is the key strike where options market makers have the most exposure. Think of it as a gravitational floor

- $30 - Secondary support; heavy put open interest here represents the next line of defense

- $25 - Deep downside support; LEAPS activity suggests this is where the extreme bear case gets priced

🟠 Resistance Levels (Call Gamma):

- $40 - The strike from today's massive put-close trade; this level carries significant options positioning. It also aligns with the upper end of the May implied move range ($40.87)

- $65-$75 - Higher strike call gamma from pre-decline positioning; would require a major re-rating to reach

- $80-$105 - Legacy call open interest from when $NVO was a $100+ stock; essentially irrelevant at current prices

What this means for traders: The $35-$40 range is the active battleground. The $35 strike acts as the strongest gamma magnet below the current price, while $40 represents significant overhead resistance. A break below $35 opens up a move toward $30, which would be an additional 18% decline. A bounce above $40 would flip the script and trap short sellers -- but that requires a meaningful catalyst shift.

🎪 Catalysts

🔥 Upcoming Catalysts

Eli Lilly Orforglipron FDA Decision - March 28, 2026 (est.) 💊

This is the single biggest near-term risk for $NVO. Eli Lilly expects FDA approval for its oral GLP-1 drug orforglipron by late March. If approved, it launches at just $50/month for Medicare -- undercutting Novo's Wegovy Pill at $149/month by two-thirds. This could disrupt Novo's first-mover advantage in oral GLP-1 and pressure market share immediately.

Q1 2026 Earnings - May 6, 2026 📊

Consensus expects revenue of $11.93B and EPS of $0.91. Key metrics to watch:

- 📊 Wegovy Pill prescription trajectory (can it sustain 130K+ weekly scripts?)

- 💸 MFN pricing impact on realized revenue per patient

- 📉 U.S. Ozempic/Wegovy injectable trends vs. Lilly competition

- 🌍 International operations performance amid patent expirations

CagriSema PDUFA Date Expected - Q2 2026 📋

The FDA will set the review timeline for Novo's December 2025 NDA submission for CagriSema. Standard review would push approval to early-mid 2027; priority review could accelerate to late 2026. Given the REDEFINE-4 failure to beat tirzepatide, the FDA's reception will be closely watched.

Higher-Dose CagriSema Phase 3 Initiation - H2 2026 🧪

Novo plans to start Phase 3 trials for higher-dose CagriSema in the second half of 2026 to address the competitive gap versus tirzepatide. REDEFINE 11 data expected H1 2027.

Amycretin Phase 3 Initiation - Q1 2026 🔬

Novo's next-gen oral obesity candidate enters pivotal trials, though approval isn't expected until Q4 2030 at the earliest.

March 20 - Triple Witch OPEX 📅

Major options expiration could create elevated volatility. The implied move prices a $34.27-$39.16 range through this date.

⏪ Recent Catalysts (Already Happened)

CagriSema REDEFINE-4 Failure (February 23, 2026): CagriSema achieved only 23% weight loss vs. tirzepatide's 25.5%, failing to meet its primary endpoint of non-inferiority. Goldman Sachs slashed CagriSema peak sales from $11.8B to $5B. Stock fell ~21% in the week after.

Q4 2025 Earnings & 2026 Guidance Shock (February 4, 2026): Revenue beat by 4.5% and EPS by 10.9%, but the 2026 guidance of -5% to -13% sales decline sent the stock crashing 18%. New CEO Doustdar warned "it will get worse before it gets better."

Morgan Stanley Upgrade & Goldman Sachs Downgrade (March 2-3, 2026): Goldman downgraded to Neutral with a $41 target (from $63) on March 2. One day later, Morgan Stanley upgraded to Equal Weight with a $40 target, saying risks are now better priced after the sell-off.

Wegovy Pill FDA Approval & Launch (December 2025 - January 2026): FDA approved oral Wegovy on December 22, 2025 -- the first oral GLP-1 for weight management. Strong early uptake with 170K+ patients in 4 weeks. Morgan Stanley raised Wegovy Pill forecasts to $2B in 2026 revenue.

MFN Pricing Agreement (Late 2025): Novo cut Ozempic and Wegovy prices from $1,000-$1,350/month to $350/month for Medicare/Medicaid in exchange for a 3-year tariff exemption. Good for access, painful for margins.

Vivtex Partnership (February 25, 2026): $2.1B deal with MIT-affiliated Vivtex to develop next-gen oral biologic medicines for obesity and diabetes.

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, and the catalyst landscape:

📈 Bull Case (20% probability)

Target: $45-$50 by May 15

How we get there:

- 📊 Wegovy Pill ramp sustains 130K+ weekly prescriptions, driving revenue above expectations

- ❌ Eli Lilly orforglipron receives an FDA Complete Response Letter or delayed approval, removing the competitive threat

- 📈 Q1 earnings on May 6 show the revenue decline is at the mild end (-5%) of guidance, not the severe end (-13%)

- 🤝 CagriSema gets priority review designation, suggesting late 2026 approval

- 💹 Stock re-rates from 10x to 14-15x earnings as sentiment stabilizes

- 🎯 Implied move upper bound through May: $40.87; bull case overshoots to $45-$50 on multiple positive catalysts

Key risk to bulls: Eli Lilly's competitive juggernaut is real. Even with a Wegovy Pill head start, orforglipron at $50/month for Medicare would be a pricing wrecking ball.

🎯 Base Case (50% probability)

Target: $34-$40 range-bound through May

Most likely scenario:

- ✅ Stock consolidates between the $35 gamma support and $40 resistance

- 📊 Orforglipron gets approved on schedule, but launch ramp is gradual and doesn't immediately crater Wegovy share

- 📉 Q1 earnings show revenue decline in the middle of the -5% to -13% guidance range (~-9%)

- ⚖️ Analyst consensus stabilizes around $40-$51 target range

- 🔄 Implied move range through May ($32.56-$40.87) brackets the most likely outcome

This is what the put-closer likely sees: the bearish thesis has played out, $NVO has been cut in half, and the risk/reward of holding short puts into earnings season is no longer favorable. Time to bank the win.

📉 Bear Case (30% probability)

Target: $25-$33

What could go wrong:

- 😰 Orforglipron approved AND launched with aggressive Medicare pricing, directly cannibalizing Wegovy Pill

- 📉 Q1 earnings show revenue decline at the severe end (-13%) or worse, with CEO guiding even lower

- 🌍 Generic semaglutide launches in Canada at 50-80% discounts accelerate, with China and Brazil following later in 2026

- 💊 CagriSema gets standard review timeline, pushing approval to mid-2027 and leaving a competitive vacuum

- 📊 Stock breaks below $35 gamma support, triggering a cascading decline toward the $30 level and eventually the LEAPS implied move lower bound at $25

Impact on the trade: This is exactly the scenario the original put buyer profited from. If you'd held those $40 puts and $NVO drops to $30, the puts would be worth even more. But the put-closer decided the easy money was made -- and that's a reasonable call given how far the stock has already fallen.

💡 Trading Ideas

🛡️ Conservative: The "Wait and Watch" Cash-Secured Put

Play: Sell May 15 $30 puts on $NVO to collect premium while setting your buy target at a 18% discount to today's price

Why this works:

- 💰 $30 strike is below the strong gamma support at $35 AND the monthly implied move lower bound ($32.56)

- 📊 You'd be buying $NVO at roughly 8x earnings -- deep value territory for a $168B pharma company

- ⏰ 73 days of theta decay working in your favor

- 🛡️ Morgan Stanley's upgrade thesis suggests NVO is now fairly valued at ~11x earnings; buying at 8x gives a margin of safety

- 📉 Estimated premium: ~$0.80-$1.20 per contract (~2.7-4% yield on cash secured)

Estimated P&L:

- 💰 Max profit: ~$80-$120 per contract if NVO stays above $30

- 📉 Breakeven: ~$28.80-$29.20 (near the LEAPS implied move lower bound)

- 🎯 Assignment scenario: You own NVO at an effective cost of ~$29 -- excellent entry if you're a long-term believer

Risk level: Low (you're comfortable owning at $29) | Skill level: Beginner-friendly

⚖️ Balanced: The "Bottom Fisher" Bull Put Spread

Play: Sell a put spread below current price to collect premium, betting NVO stabilizes above $35 gamma support

Structure: Sell May 15 $35 puts / Buy May 15 $30 puts

Why this works:

- 🎯 $35 is the highest gamma concentration level below the current price -- options activity creates a natural floor

- 📊 Both strikes are below the March monthly implied move range ($34.27-$39.16)

- ⏰ 73 days of time decay working in your favor

- 💰 Estimated credit: ~$1.50-$2.00 per spread (~30-40% of width)

- 🛡️ Defined risk: Max loss of $5 per spread minus premium collected

- 📈 Current analyst consensus of $51 average price target implies 39% upside from here

Estimated P&L:

- 💰 Max profit: ~$150-$200 per spread if NVO stays above $35 at May expiration

- 📉 Max loss: ~$300-$350 per spread if NVO below $30

- 🎯 Breakeven: ~$33-$33.50

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: The "Contrarian Rebound" Long Call Spread

Play: Buy a call spread for May earnings, betting the put-closer is right that the worst is priced in

Structure: Buy May 15 $37 calls / Sell May 15 $42 calls

Why this works:

- 📈 The $8M put-close signals institutional belief that the downside is mostly exhausted

- 📊 Morgan Stanley's upgrade to Equal Weight with $40 target validates stabilization thesis

- 💊 Wegovy Pill's strong launch with $2B 2026 revenue forecast provides fundamental support

- 🎯 $42 upper strike aligns with Goldman's $41 price target -- a reasonable recovery target

- ⏰ Trade captures Q1 earnings on May 6, which could be a positive re-rating catalyst if guidance improves

- 📉 NVO at 10.24x P/E vs. pharma peer average of 18.9x provides fundamental valuation support

Why this could go wrong:

- 💥 Orforglipron approved March 28 could pressure $NVO further before earnings

- 📉 Q1 earnings could disappoint if MFN pricing impact is worse than expected

- ⚠️ Generic semaglutide launch in Canada could accelerate international revenue declines

Estimated P&L:

- 💰 Net debit: ~$1.80-$2.50 per spread

- 📈 Max profit: ~$2.50-$3.20 per spread if NVO above $42 at expiration (~125% return)

- 📉 Max loss: Premium paid (~$180-$250 per spread) if NVO below $37

- 🎯 Sweet spot: NVO at $40-$42 near Morgan Stanley/Goldman target range

Risk level: High (directional bet on stabilization) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💊 Orforglipron FDA decision on March 28: This is the elephant in the room. Eli Lilly's oral GLP-1 at $50/month for Medicare would undercut Wegovy Pill by 66% and could immediately pressure NVO's prescription volumes. An approval could send $NVO to new lows.

-

📉 CagriSema competitive gap is structural: CagriSema delivered only 23% weight loss vs. tirzepatide's 25.5%. This isn't a dosing issue that's easily fixed -- it's a fundamental efficacy difference. Goldman slashed CagriSema peak sales by ~58% to $5B, and JP Morgan cut longer-term obesity drug forecasts by 40-63%.

-

💸 MFN pricing permanently compresses U.S. margins: Cutting Ozempic/Wegovy prices from $1,000-$1,350 to $350/month is a 65-74% haircut on per-unit revenue. This isn't temporary -- it's the new normal under the MFN agreement.

-

🌍 International patent expirations are starting now: Generic semaglutide is hitting Canada with 50-80% price discounts, and China and Brazil follow in 2026. International operations were supposed to be the growth engine -- that story is fraying.

-

🏛️ Leadership overhaul creates execution risk: A new CEO and entirely new board installed by the Novo Nordisk Foundation during the company's most critical competitive period. New leadership navigating a -5% to -13% revenue decline while battling Eli Lilly is a tough ask.

-

📊 Catching a falling knife risk: Yes, the stock is cheap at 10x earnings. But "cheap" can get cheaper. The 52-week range is $36.72-$91.90 -- the stock has done nothing but go down for 9 months. Momentum is firmly against the bulls.

-

⚖️ Revenue decline guidance may be optimistic: The -5% to -13% 2026 sales decline projection was issued before the CagriSema REDEFINE-4 failure. If the competitive landscape deteriorates further (orforglipron + generics), management may need to revise lower.

🎯 The Bottom Line

Real talk: An institutional player just banked profits on $8M worth of bearish $NVO bets, and the timing tells a story. After riding the stock down 58% from its highs, the smart money is saying: "mission accomplished, time to move on." When the bears start covering, it doesn't necessarily mean the bottom is in -- but it does mean the risk/reward of staying short is shifting.

What this trade tells us:

- 🎯 A large player believes the easy money on the downside has been made

- 💰 Closing $8M in puts suggests the trader's profit target was hit

- ⚖️ With Morgan Stanley upgrading and Goldman's target at $41, the stock is approaching Wall Street's revised fair value estimates

- 📊 The $40 strike acts as a key level -- it's resistance overhead AND the level where institutional positions were concentrated

If you're a long-term believer in $NVO:

- ✅ This is the cheapest the stock has been relative to earnings (10x P/E) in years -- but cheap alone isn't a reason to buy

- 📊 Wait for the March 28 orforglipron FDA decision before making a big commitment -- this is a binary event

- 💊 Wegovy Pill's strong early launch is the best thing NVO has going right now

- 🛡️ Consider selling cash-secured puts at $30-$32 to get paid while you wait for a better entry

- 📈 Average analyst target of $51 implies 39% upside -- but targets are dropping, not rising

If you're watching from the sidelines:

- 🎯 Wait for the orforglipron FDA decision on March 28 -- this single event could move $NVO 10%+ in either direction

- 📊 Q1 earnings on May 6 will be the next fundamental checkpoint

- 💡 The put-closing activity today is a data point, not a buy signal -- institutional profit-taking doesn't mean the bottom is in

- 🤔 The $2.1B Vivtex partnership and amycretin pipeline provide long-term optionality, but these are 2028-2030 stories

If you're bearish:

- 📉 The headwinds are real: MFN pricing, CagriSema failure, orforglipron competition, and international generics

- 🎯 Bear put spreads ($35/$30) offer defined-risk downside plays through May

- ⚠️ Be careful shorting a stock at 10x earnings that just saw $8M in put-closing -- the crowded short trade is getting less crowded

- ⏰ If orforglipron gets approved March 28, that could be the catalyst for the next leg down toward $30

Mark your calendar - Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $35.58-$37.85)

- 📅 March 20 - Triple Witch OPEX (implied range: $34.27-$39.16)

- 📅 March 28 (est.) - Eli Lilly orforglipron FDA decision -- the most important near-term catalyst

- 📅 Q2 2026 - CagriSema PDUFA date announcement expected

- 📅 May 6 - Q1 2026 Earnings (consensus: revenue $11.93B, EPS $0.91)

- 📅 May 15 - Expiration of this $8M put-close trade

Final verdict: This $8M put-close tells us one thing clearly: the institutional bear trade on $NVO has played out. From $142 to $37, the decline has been brutal and the put holders made a fortune. But covering bearish bets is not the same as going long. $NVO faces an absolutely packed catalyst calendar over the next 10 weeks -- orforglipron decision, CagriSema PDUFA timing, and Q1 earnings. Each one could move the stock 10-20%. If you're thinking about getting involved, use defined-risk strategies (put spreads, call spreads) and keep position sizes small. This is a stock where the next 3 months will determine whether 10x earnings is a bargain or a value trap. Don't try to be a hero -- let the catalysts play out and position accordingly.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Scores of 3.00 and 4.64 reflect these specific trades' unusualness relative to recent activity -- they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading.

About Novo-Nordisk A/S: Novo Nordisk is the world's leading diabetes care company with a $167.8B market cap, commanding roughly one-third of the global branded diabetes treatment market. The company manufactures and markets GLP-1 therapies (Ozempic, Wegovy), insulins, and obesity treatments, and is headquartered in Denmark with 69,500 employees worldwide.