🦉 OWL $1.3M Put Close - Bearish Bet Unwound as Blue Owl Tests Rock Bottom!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed a $1.3 MILLION bearish put position on Blue Owl Capital, buying back 10,000 contracts at the $10 strike after the stock cratered over 50% from its highs. This is a buy-to-close (BTC) on a long put -- meaning a trader who nailed the OBDC II crisis trade is now cashing out with the stock near $10. When the bears start taking profits, it's worth asking: is the worst already behind $OWL?

📊 Company Overview

Blue Owl Capital Inc. (OWL) is one of the world's largest alternative asset managers:

- Market Cap: ~$7.1B

- Industry: Investment Advice (SIC 6282)

- Exchange: NYSE

- Current Price: ~$9.94 (near 52-week low of $10.07)

- AUM: $307B across Credit, GP Strategic Capital, and Real Assets

- Employees: 1,365 across 20+ offices globally

- Dividend Yield: ~9.3% ($0.92 annual / $0.23 quarterly)

Blue Owl specializes in providing capital solutions to middle-market companies, private equity firms, and real estate owners. They operate three primary platforms: Credit (direct lending), GP Strategic Capital (minority stakes in asset managers), and Real Assets (net lease and digital infrastructure). Their digital infrastructure arm includes a massive $15B data center JV with Crusoe for AI workloads.

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 09:48:39):

| Time | Symbol | Side | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|

| 09:48:39 | OWL | ASK | BUY | PUT | 2026-05-15 | $1.3M | $10 | 10K | OWL20260515P10 |

🤓 What This Actually Means

This is a buy-to-close (BTC) on a long put -- and it's a classic profit-taking move. Here's the breakdown:

- 💸 Premium paid to close: $1.3M ($1.30 per contract x 10,000 contracts)

- 🎯 Strike vs. spot: The $10 put is slightly in-the-money with OWL trading at ~$9.94

- 📊 Massive position: 10,000 contracts = 1,000,000 shares of notional exposure (~$10M)

- 🏦 Vol/OI ratio: 0.476 -- moderate activity relative to existing open interest

- 🔍 Classification: Close Long Put with MEDIUM confidence

What's really happening here:

This trader previously bought these $10 puts -- likely when OWL was trading significantly higher -- betting the stock would fall. And fall it did: OWL has plunged from $20.83 to under $10 over the past year. Now, with the put deep enough in the money, the trader is locking in profits by buying back their position. The May 15 expiration roughly aligns with Q1 2026 earnings, suggesting they may have originally positioned for continued deterioration through the next report but decided to exit early.

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL (Z-Score: 5.31) - This kind of activity shows up only a handful of times per year. A 5.31 z-score means the volume is roughly 5x the standard deviation above average -- this is a significant signal. The fact that it's a closing trade rather than a new position makes it even more interesting: smart money that profited from the sell-off is stepping aside.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Blue Owl is down roughly 30% YTD in 2026, falling from ~$14.20 at year-end 2025 to $9.94 today. The decline has been relentless -- after peaking near $20.83 in March 2025, the stock has been cut in half. The damage accelerated in February when the OBDC II liquidity crisis triggered a ~23% monthly drop, the worst since 2022.

Key observations:

- 📉 Downtrend intact: OWL hit a new 52-week low on February 24 at $10.07

- 💹 $10 psychological support: The stock is dancing right on this critical level

- 🎢 Extreme selling pressure: Bloomberg reported the worst month since 2022

- 📊 Volume elevated: Heavy institutional selling through February on OBDC II fears

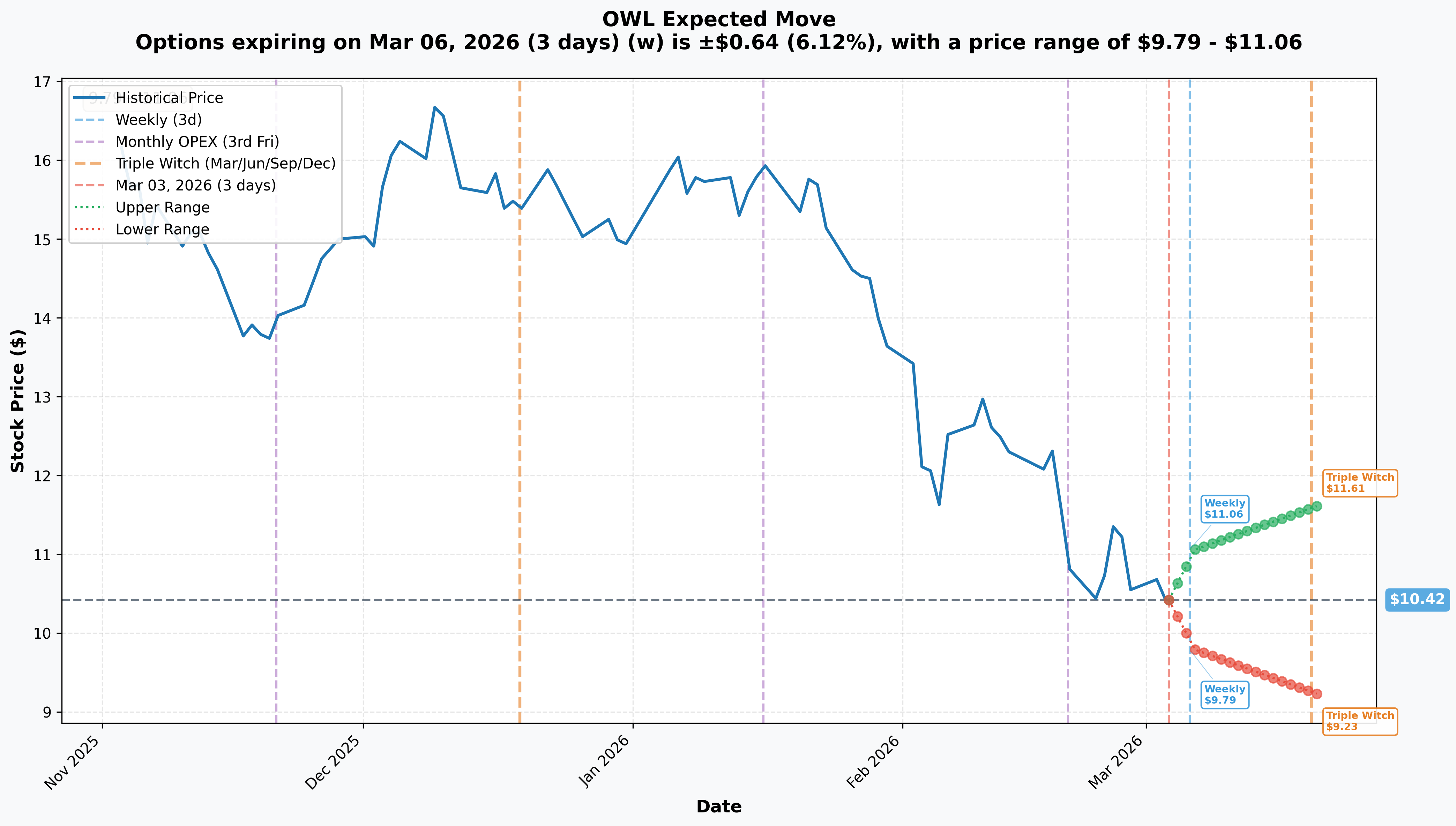

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 3 days): +/-$0.64 (+/-6.12%) --> Range: $9.79 - $11.06

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 17 days): +/-$1.19 (+/-11.42%) --> Range: $9.23 - $11.61

Translation for regular folks:

Options traders are pricing in a 6.12% move (~$0.64) by Friday and a massive 11.42% move (~$1.19) through March expiration. For context, that's a huge implied move for a $10 stock -- the market is saying OWL could easily swing between $9.23 and $11.61 over the next three weeks. This tells you volatility is elevated and the market is genuinely uncertain about whether $10 holds or breaks.

The weekly implied range of $9.79-$11.06 is especially important: if OWL drops below $9.79, it enters uncharted territory below its 52-week low. But if it can hold and bounce above $11, it would be a meaningful technical reversal signal.

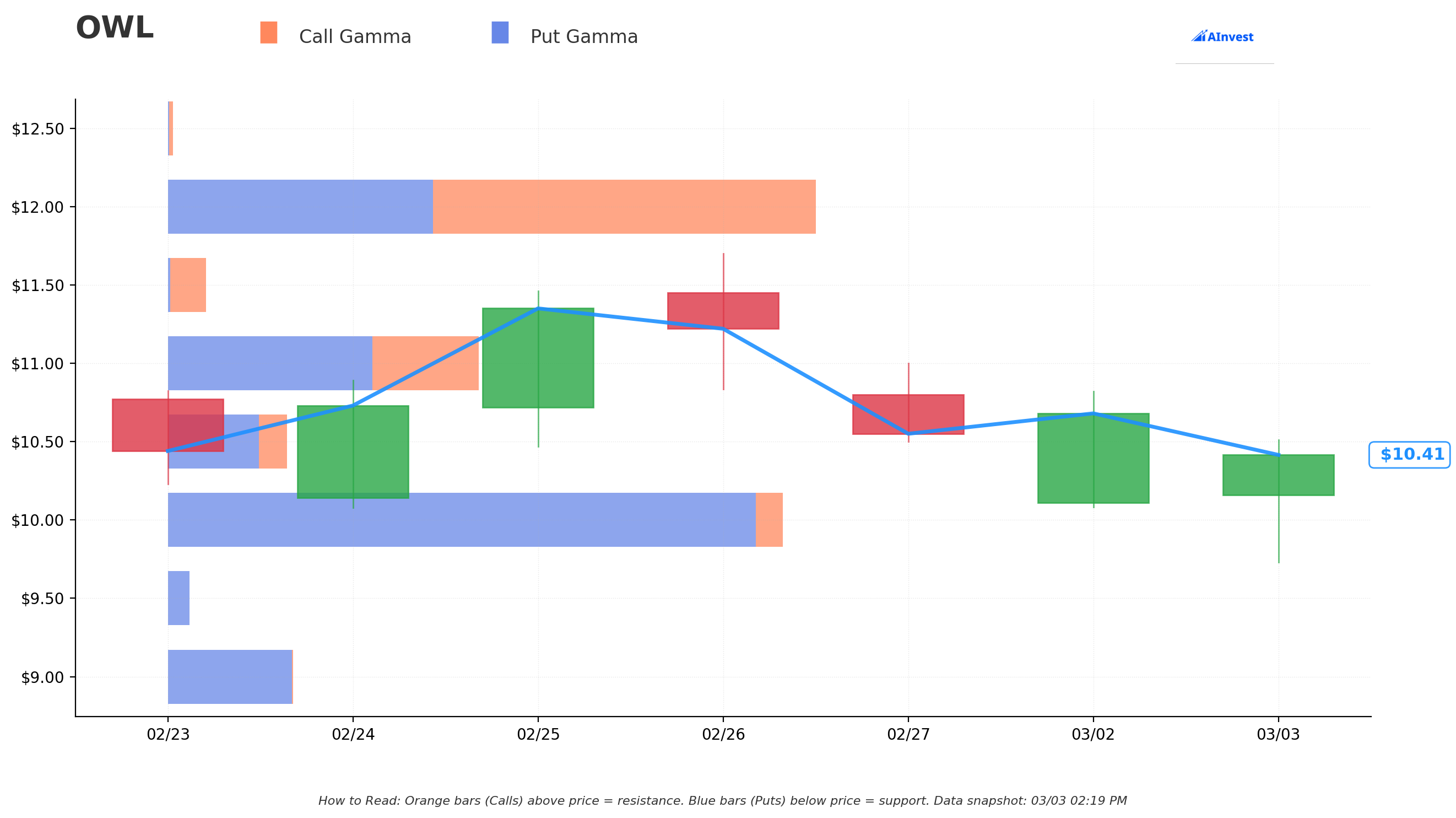

Gamma-Based Support & Resistance Analysis

Key Gamma Levels:

The gamma exposure data shows the $11 strike as the max gamma level, which acts as a magnet for price action and a key resistance zone. Other notable levels include $12, $13 to the upside and $7, $6 to the downside.

🔵 Support Levels (Put Gamma - floors where buyers step in):

- $10 - The put strike from today's trade; massive psychological and technical level

- $9.79 - Weekly implied move lower bound

- $9.23 - Monthly OPEX implied move lower bound; a break here could accelerate selling

🟠 Resistance Levels (Call Gamma - ceilings where sellers emerge):

- $11 - Max gamma strike; strongest resistance level. Aligns almost perfectly with the weekly implied move upper bound ($11.06)

- $11.61 - Monthly OPEX implied move upper bound

- $12-$13 - Higher gamma strikes; if OWL reclaims these levels, the picture changes dramatically

What this means for traders: The $10-$11 zone is the current battlefield. The gamma data tells us there's significant options interest clustering around $11, making it a tough ceiling to crack. Meanwhile, $10 acts as the floor -- if it breaks, the next meaningful gamma support is way down at $7. That's a big gap, which means a breakdown below $10 could get ugly fast. But if $10 holds and OWL recovers toward $11, that gamma wall could actually provide stability as market makers hedge around it.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings - Expected Late April / Early May 2026 📊

Blue Owl's next earnings report will be the critical inflection point. Consensus expects:

- 📊 Revenue: ~$666M

- 💰 Consensus EPS: ~$0.21

- 🔍 Key metrics: net BDC inflows vs. redemptions, FRE margin toward 58.5% target, OBDC II return-of-capital execution, and credit quality (non-accruals, PIK rates)

This is the event that will determine whether the OBDC II crisis was a contained one-off or the start of a broader unraveling. The closing of this put position before earnings suggests the original trader decided not to wait for the verdict.

OBDC II Wind-Down / Capital Return Progress (Q2-Q3 2026) 📉

Blue Owl replaced quarterly redemptions with return-of-capital distributions of up to $2.35/share (~30% of NAV). The pace and pricing of asset dispositions will be scrutinized heavily through mid-year.

Digital Infrastructure Fund IV Launch (2026) 🏗️

Blue Owl's digital infrastructure vertical is a rare bright spot. ODI III closed at $7B (75% above target) in May 2025. A successor fund could raise $8-10B+, and the Phase 2 of the $15B Crusoe JV in Abilene, Texas is expected to energize mid-2026 with $7.1B in construction financing already secured.

BDC Sector Maturity Wall (Throughout 2026) ⚠️

23 of 32 rated BDCs have $12.7B in unsecured debt maturing in 2026, a 73% increase over 2025. This industry-wide headwind keeps pressure on the entire alt-credit space.

Dividend Payments 💰

$0.23/share quarterly dividend confirmed for all of 2026. At current price of ~$9.94, that's a ~9.3% yield -- one of the highest in the alt-manager space.

⏪ Recent Catalysts (Already Happened)

OBDC II Liquidity Crisis (February 19, 2026) -- THE big one:

Blue Owl eliminated quarterly redemptions in its $1.6B retail OBDC II fund, replacing them with return-of-capital distributions. They sold $1.4B in direct lending assets at 99.7% of par to institutional investors. OWL fell ~23% in February, with a ~10% single-day drop on the announcement. Multiple class action lawsuits followed, alleging executives misled investors about redemption pressures.

Q4 2025 Earnings Beat (February 5, 2026):

Revenue of $755.6M beat estimates, AUM crossed $307B with $17B record Q4 fundraising, and FRE margin came in at 58.3%. Solid numbers that were completely overshadowed by the OBDC II fallout two weeks later.

BOSE Secondaries Fund Close (February 11, 2026):

Inaugural Strategic Equity Secondaries fund closed with $3B+ across institutional and private wealth channels, showing Blue Owl can still raise capital in non-BDC strategies.

Moody's Credit Upgrade (January 22, 2026):

OBDC and OCIC upgraded to Baa2 from Baa3 -- an investment grade improvement citing just 27 bps annual net loss rate since 2016. Ironic timing given the OBDC II crisis that followed a month later.

Analyst Downgrades (February-March 2026):

Barclays cut to Equal-Weight from Overweight ($11 target) on March 2, projecting net negative BDC flows for several quarters. Deutsche Bank downgraded to Hold ($10 target) on February 24. On the flip side, Raymond James reiterated Strong Buy at $20 and Bank of America maintained Buy at $24.

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, analyst targets, and the unusual options activity:

📈 Bull Case (25% probability)

Target: $13-$16

How we get there:

- 🏗️ Q1 earnings show OBDC II fallout is contained -- redemptions stabilize, credit quality remains solid

- 💰 Digital infrastructure growth story gains traction: Crusoe JV Phase 2 energizes mid-2026, fund IV launches

- 📊 FRE margins hit or exceed the 58.5% target, validating permanent capital model

- 🤝 BOSE fund success is followed by more product launches in private wealth

- 📈 BofA's $24 target and Raymond James' $20 Strong Buy start pulling price higher from deeply oversold levels

- 💪 Stock breaks above $11 gamma wall, triggering short covering and a relief rally

Key risk to bulls: Barclays projects net BDC flows will turn negative in 2026 and stay pressured for "several quarters." Even good earnings may not be enough to reverse the sentiment.

🎯 Base Case (50% probability)

Target: $9-$11 range-bound

Most likely scenario:

- ✅ OWL consolidates between $9.23 (implied move support) and $11 (max gamma / resistance)

- 📊 Q1 earnings come in roughly in-line; OBDC II wind-down proceeds slowly but orderly

- ⚖️ Analyst sentiment remains split -- bears point to BDC headwinds, bulls to value and yield

- 💰 9.3% dividend yield provides a floor by attracting income-focused buyers

- 🔄 Stock grinds sideways as the market digests the OBDC II fallout and waits for evidence of stabilization

This is the "prove it" zone: OWL needs multiple clean quarters to rebuild trust. The put closer's exit at $10 suggests the easy bearish money has been made, but there's no catalyst to drive a meaningful re-rating near-term.

📉 Bear Case (25% probability)

Target: $7-$9

What could go wrong:

- 😰 Q1 earnings reveal worse-than-expected BDC outflows; OBDC II asset sales below par

- 📉 Private credit "true" default rate approaching 5% sparks broader contagion across the sector

- ⚖️ Securities fraud class actions result in management distractions or settlements

- 💸 UBS warning that AI disruption risk in private credit is "high and not priced in" becomes reality for BDC borrowers

- 📉 $10 support breaks decisively -- next meaningful gamma level is $7, a 30% drop from here

- 🏦 BDC sector maturity wall creates refinancing difficulties, dragging down the entire alt-credit complex

Impact on the trade: If you're the trader who just closed their puts at $10, this is the scenario they decided wasn't worth waiting for. They already captured most of the move from $20 to $10 and didn't want to risk a reversal erasing gains.

💡 Trading Ideas

🛡️ Conservative: The "Collect the 9% Yield" Income Play

Play: Buy OWL shares near $10 and hold for the dividend while the dust settles

Why this works:

- 💰 $0.92 annual dividend ($0.23/quarter) confirmed for all of 2026 -- that's a 9.3% yield at current prices

- 📊 Moody's Baa2 upgrade and the $1.4B asset sale at 99.7% of par validates credit quality

- 🛡️ 67% of analysts still rate Buy or Strong Buy with average target of ~$18.67

- 🏗️ Digital infrastructure growth (Crusoe JV, Stack Infrastructure) provides a long-term secular tailwind independent of BDC drama

- 📈 If stock just holds $10 and you collect 4 quarterly dividends, that's $0.92/share (~9.3% return) even without any price appreciation

Estimated P&L:

- 💰 Dividend income: $0.92/share annually (9.3% yield)

- 📈 Upside to consensus target: ~$18.67 (88% upside)

- 📉 Downside risk: If $10 breaks, next support at $7 (30% downside)

Risk level: Moderate (high yield but stock in downtrend) | Skill level: Beginner-friendly

⚖️ Balanced: The "Support Floor" Put Spread

Play: Sell a put spread below support to collect premium while $10 acts as a floor

Structure: Sell May 15 $9 puts / Buy May 15 $7 puts

Why this works:

- 🎯 $9 is below the weekly implied move lower bound ($9.79) and near the monthly OPEX floor ($9.23)

- 📊 The put-closer's exit suggests downside momentum is fading at $10

- ⏰ 73 days of time decay working in your favor through the Q1 earnings catalyst

- 💰 Collect ~$0.40-0.60 per spread (~20-30% of $2 width)

- 🛡️ Defined risk: max loss $2 per spread minus premium collected

- 💹 The 9.3% dividend yield should attract value/income buyers near $10, providing natural support

Estimated P&L:

- 💰 Max profit: ~$40-60 per spread if OWL stays above $9 at May expiration

- 📉 Max loss: ~$140-160 per spread if OWL below $7

- 🎯 Breakeven: ~$8.40-8.60 (well below current price and implied move support)

Risk level: Moderate (defined risk below support) | Skill level: Intermediate

🚀 Aggressive: The "Bottom Fisher" Call Spread

Play: Buy a call spread targeting the $11 gamma wall as a recovery trade

Structure: Buy May 15 $10 calls / Sell May 15 $12 calls

Why this works:

- 📈 Consensus analyst target of $18.67 implies 88% upside; even a partial recovery to $12 would be a 20% move

- 🤝 The put position being unwound removes 10,000 contracts of bearish open interest from the market

- 📊 Q1 earnings could be the catalyst if OBDC II wind-down proves orderly

- 🏗️ Crusoe JV Phase 2 energization mid-2026 and potential fund IV launch are upcoming positive catalysts

- 💰 Defined risk: you can only lose the net debit paid

Why this could go wrong:

- 💥 If OBDC II fallout spreads to OBDC or other BDCs, OWL could break $10 decisively

- 📉 Barclays' projection of negative BDC flows for "several quarters" could keep the stock pinned

- ⚠️ Class action lawsuit headlines could create negative sentiment spikes

Estimated P&L:

- 💰 Net debit: ~$0.60-0.80 per spread

- 📈 Max profit: ~$1.20-1.40 per spread if OWL above $12 at May expiration

- 📉 Max loss: Net premium paid (~$60-80 per spread) if OWL stays below $10

- 🎯 Sweet spot: OWL rallies to $11-$12 on Q1 earnings relief

Risk level: High (catching a falling knife) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Non-traded BDC contagion: Blue Owl's non-traded BDC funds account for ~20% of fee-related revenue -- the highest concentration among peers. If the OBDC II crisis spreads to the larger OBDC or OCIC funds, the revenue hit could be severe. Barclays projects net BDC flows turning negative for multiple quarters.

-

⚖️ Securities fraud lawsuits: Multiple class action suits name both Co-CEOs and the CFO, alleging they misled investors about redemption pressures throughout 2025. Legal expenses, management distraction, and potential settlements create tail risk that's hard to quantify.

-

💸 Falling interest rates compress BDC income: Blue Owl's BDC portfolios are heavily floating-rate. As rates decline, asset yields are expected to trough at 8.0-8.5% in 2026, directly compressing fund income and potentially pressuring management fees.

-

🏦 $12.7B BDC maturity wall in 2026: The broader BDC sector faces a 73% increase in debt maturities this year. If refinancing conditions tighten or defaults spike, the entire alternative credit complex could come under pressure.

-

🤖 AI disruption risk to private credit borrowers: UBS flagged that private credit's exposure to AI disruption is "high and not priced in", particularly tech/software borrowers comprising ~25% of some BDC portfolios. A wave of borrower distress from AI disruption could hit credit quality.

-

📊 Dividend sustainability questions: While the $0.92/share annual dividend is confirmed for 2026, the 9.3% yield at current prices signals the market doubts its long-term sustainability. If BDC fee revenues decline materially, the dividend could come under review.

🎯 The Bottom Line

Real talk: A trader who crushed it on a bearish OWL bet just walked away from the table with their profits. They bought $10 puts -- probably when the stock was in the teens -- rode the stock down through the OBDC II crisis, and decided $10 is close enough to the bottom to cash out. That's a smart, disciplined exit.

What this trade tells us:

- 🎯 Sophisticated bearish money thinks the easy downside trade is over at $10

- 💰 The unwinding of 10,000 put contracts removes bearish pressure from the market

- ⚖️ At a 9.3% dividend yield and 12.9x earnings, the stock is pricing in a lot of bad news

- 📊 But closing a bearish bet is not the same as going long -- this trader isn't saying "buy OWL," they're saying "the short side is getting crowded at $10"

If you're thinking about buying OWL:

- ✅ The 9.3% dividend yield and 67% Buy ratings with $18.67 average target make a compelling deep-value argument

- 🏗️ The digital infrastructure growth story (Crusoe JV, Stack Infrastructure) is genuinely exciting and uncorrelated to BDC drama

- 🛡️ Moody's Baa2 upgrade and the $1.4B asset sale at 99.7% par validate credit quality

- ⏰ But wait for confirmation: Q1 earnings in late April will be the make-or-break moment

If you're watching from the sidelines:

- 🎯 The $9.23-$9.79 implied move support zone would be a more attractive entry point

- 📊 Watch BDC flow data closely -- if redemptions stabilize, OWL could snap back hard from deeply oversold levels

- 🤝 The $3B BOSE secondaries fund close shows Blue Owl can still raise money outside of troubled BDC channels

- 💡 Consider starting a small position with the yield as your margin of safety and add on Q1 earnings if results are clean

If you're bearish:

- 📉 Deutsche Bank's $10 target and Barclays' $11 suggest limited downside from here even in the bear case

- ⚠️ The smart put trader just exited -- following bears into a crowded trade at the 52-week low is dangerous

- 🎯 If you must short, wait for a bounce to $11+ (gamma resistance) for a better entry rather than pressing at $10

Mark your calendar -- Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $9.79-$11.06)

- 📅 March 20 - Triple Witch OPEX (implied range: $9.23-$11.61)

- 📅 Q1 2026 - Next quarterly dividend payment ($0.23/share)

- 📅 Late April / Early May - Q1 2026 earnings report (THE critical catalyst)

- 📅 May 15 - Expiration of the original put position that was just closed

- 📅 Mid-2026 - Crusoe JV Phase 2 data center energization

Final verdict: This $1.3M put close is a capitulation signal from the bear side -- not a bullish endorsement, but a recognition that the easy downside money has been made. OWL at $10 with a 9.3% yield, $307B AUM, and a legitimate AI infrastructure growth engine is either a deep-value opportunity or a value trap, and Q1 earnings will tell us which. The responsible play is to start small, collect the dividend, and let the next earnings cycle provide clarity. If you chase here without a risk plan, a break below $10 toward the $7 gamma level would be painful. Respect the trend, but recognize that the most profitable bear just left the building.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 5.31 reflects this specific trade's unusualness relative to recent activity -- it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About Blue Owl Capital Inc.: Blue Owl Capital is a ~$7.1B alternative asset manager with $307B in AUM, operating across Credit, GP Strategic Capital, and Real Assets platforms. The firm employs 1,365 people across 20+ global offices and is listed on the NYSE.