🥈 PAAS $3.4M Short Call LEAPS - Someone Betting Silver Won't Hit $70 For 2 Years!

📅 January 21, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just SOLD $3.4 MILLION worth of January 2028 $70 strike calls on Pan American Silver this morning! In two separate trades at 09:44, a total of 3,900 contracts were written at the money with 2 full years until expiration. With PAAS trading at all-time highs near $57.58 after a +149% rally in 2025, this institutional player is collecting massive premium betting the silver rally runs out of steam before $70. Translation: Smart money thinks the easy gains are behind us and is willing to bet 2 years of premium income that PAAS doesn't break $70!

📊 Company Overview

Pan American Silver Corp. (PAAS) is the world's largest diversified silver producer with exposure to the precious metals boom:

| Metric | Value |

|---|---|

| Market Cap | $24.74 Billion |

| Industry | Silver & Gold Mining (Precious Metals) |

| Current Price | $57.58 (near all-time high of $58.30) |

| 52-Week Range | $20.55 - $58.30 |

| 1-Year Return | +149.33% |

| P/E Ratio | 31.91 |

| Employees | 9,000 |

Primary Business: Pan American operates 10 mines across Latin America producing silver, gold, zinc, lead, and copper. Key operations include La Colorada, Dolores, Huaron, Morococha, Shahuindo, La Arena, and facilities in Canada. Following the $2.1B acquisition of MAG Silver in September 2025, they now own 44% of the high-grade Juanicipio mine, which is driving significant production growth.

💰 The Option Flow Breakdown

📊 The Tape (January 21, 2026)

| Time | Symbol | Side | Type | Strike | Expiration | Volume | Premium | Order Type | Strategy | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:44:42 | PAAS | SELL | CALL | $70 | 2028-01-21 | 1,600 | $2.4M | STO | Short Call | 108.86 | EXTREMELY UNUSUAL |

| 09:44:47 | PAAS | SELL | CALL | $70 | 2028-01-21 | 2,300 | $999K | STO | Short Call | 156.89 | EXTREMELY UNUSUAL |

Total Premium Collected: $3.399 Million (combined both trades) Total Contracts Sold: 3,900 contracts = 390,000 shares worth of exposure Option Symbol: PAAS20280121C70

🤓 What This Actually Means

This is a premium collection strategy by someone with a neutral-to-bearish view on PAAS reaching $70! Here's the breakdown:

- 💰 Massive premium collected: $3.4M in premium income collected upfront

- 🎯 Strike well above current price: $70 strike is 21.5% above current price of $57.58

- ⏰ Extreme duration: 2 full years (730 days) until January 21, 2028 expiration - this is a LEAPS trade!

- 📊 Size matters: 3,900 contracts in 5 seconds shows institutional execution, not retail clicking around

- 🏦 Thesis: Seller believes either PAAS won't reach $70 OR they're selling covered calls against a massive long position

What's really happening here:

Two scenarios explain this activity:

Scenario 1 - Covered Call Writing (Most Likely): An institution holding 390,000+ shares of PAAS is selling calls against their position to generate income. With PAAS up 149% in 2025, they're happy to cap their upside at $70 (another 21.5% gain) in exchange for $3.4M in immediate premium. If PAAS hits $70 by January 2028, they sell their shares at $70 and keep the premium - total return would be ~31.5% on top of current price. Not bad for taking chips off the table!

Scenario 2 - Naked Short Calls (More Aggressive): The seller believes silver's parabolic rally is overdone and PAAS won't sustain above $70 for the next 2 years. They're betting that the 147% silver rally in 2025 will mean-revert, commodity cycles will normalize, or geopolitical tailwinds will fade. If PAAS stays below $70, they keep the entire $3.4M premium.

Unusual Score: 🔥 EXTREME (Z-Scores of 108.86 and 156.89) - These scores indicate this activity is roughly 100-150 standard deviations above normal volume patterns. We're talking about trades that occur only a few times per year in terms of size and unusual characteristics.

📈 Technical Setup / Chart Check-Up

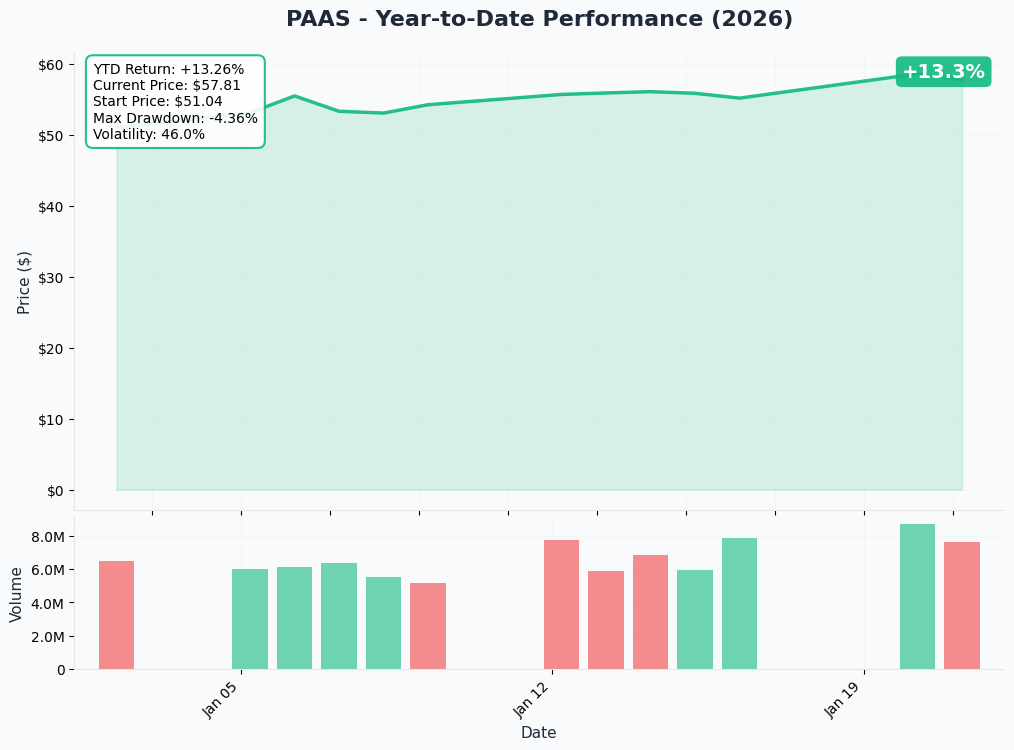

YTD Performance Chart

PAAS has been on an absolute tear - up +149% over the past 12 months riding the silver and gold bull market. The chart tells a story of precious metals mania driven by the MAG Silver acquisition and silver prices surging from ~$30/oz to ~$70/oz in 2025.

Key observations:

- 🚀 Parabolic rally: Stock more than doubled from $23 area to nearly $58 in 12 months

- 📈 All-time high territory: Just hit $58.30 on January 20, 2026 - uncharted waters

- 🎢 Extended move: After such a powerful rally, some consolidation or pullback is healthy

- 📊 Volume confirmation: Institutional accumulation visible throughout 2025

- ⚠️ Overbought signals: RSI likely in extreme territory after sustained rally

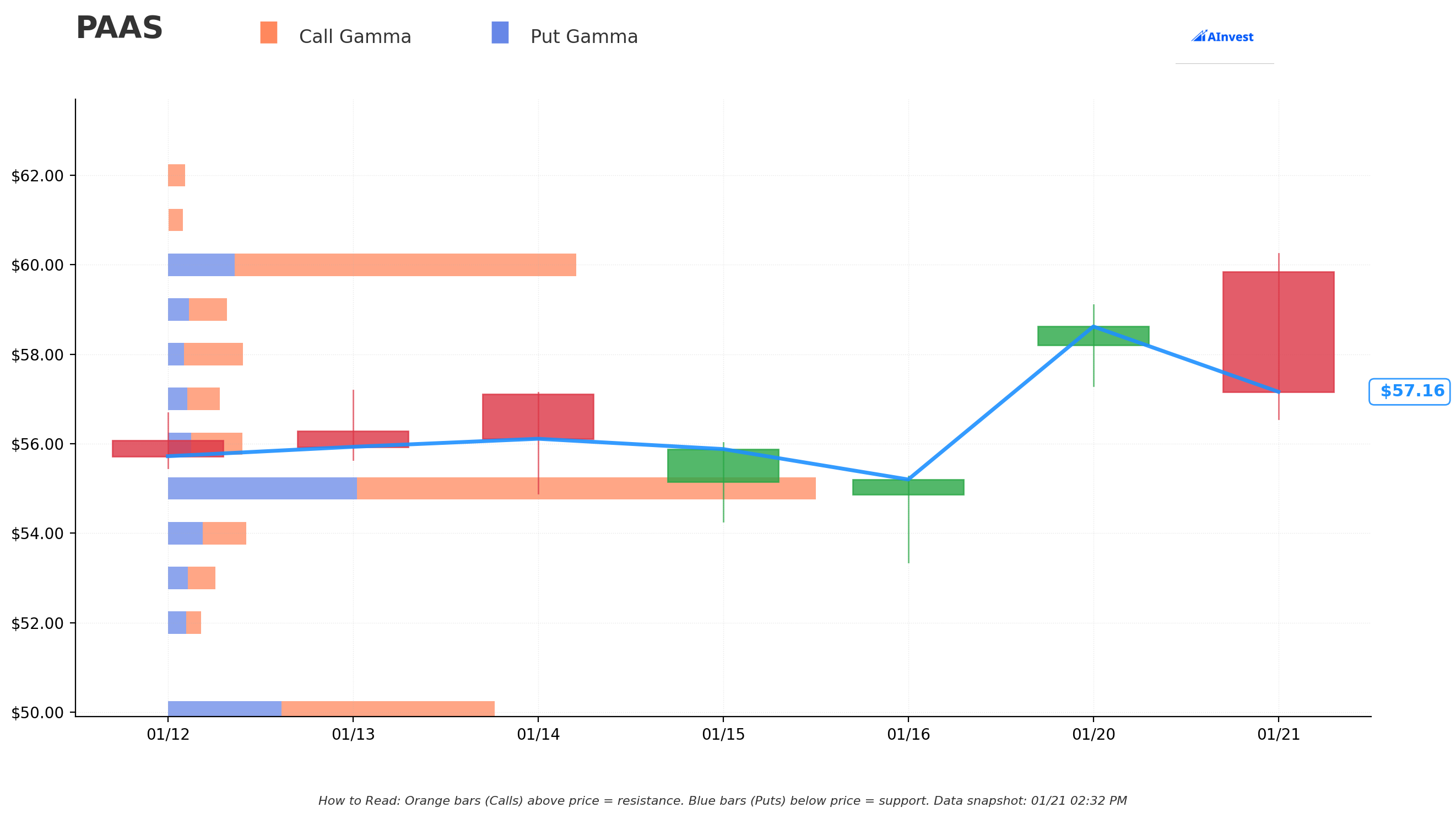

🔵 Gamma-Based Support & Resistance Analysis

Current Price: $57.38

The gamma exposure map reveals where market makers have significant options exposure, creating natural support and resistance zones:

🔵 Support Levels (Put Gamma Below Price):

- $57 - Immediate support (0.66% below) with 0.47B total gamma - first line of defense

- $56 - Secondary support (2.4% below) with 0.66B gamma

- $55 - Major structural support (4.1% below) with 5.85B gamma - STRONGEST SUPPORT LEVEL!

- $54 - Additional cushion (5.9% below) with 0.69B gamma

- $50 - Deep support (12.9% below) with 2.94B gamma - psychological round number

- $49 - Extended floor (14.6% below) with 1.73B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $58 - Immediate resistance (1.1% above) with 0.69B gamma

- $59 - Secondary resistance (2.8% above) with 0.54B gamma

- $60 - Major ceiling (4.6% above) with 3.70B gamma - Key resistance zone!

- $65 - Extended resistance (13.3% above) with 1.30B gamma

What this means for traders:

The gamma data shows $55 is THE critical support level with massive 5.85B total gamma exposure. Market makers will aggressively buy dips at this level to maintain their hedges. On the upside, $60 is the major resistance with 3.70B gamma creating natural selling pressure. The $57-$60 range is the immediate battleground.

Notice the call strike: The $70 strike where this trade was executed is well above all measured gamma levels - the call seller positioned at a strike that currently has minimal market maker positioning, meaning they're betting on a price level the market doesn't expect to reach.

Net GEX Bias: Bullish (21.2B call gamma vs 7.1B put gamma) - Overall dealer positioning remains bullish, but current price action is constrained by overhead resistance.

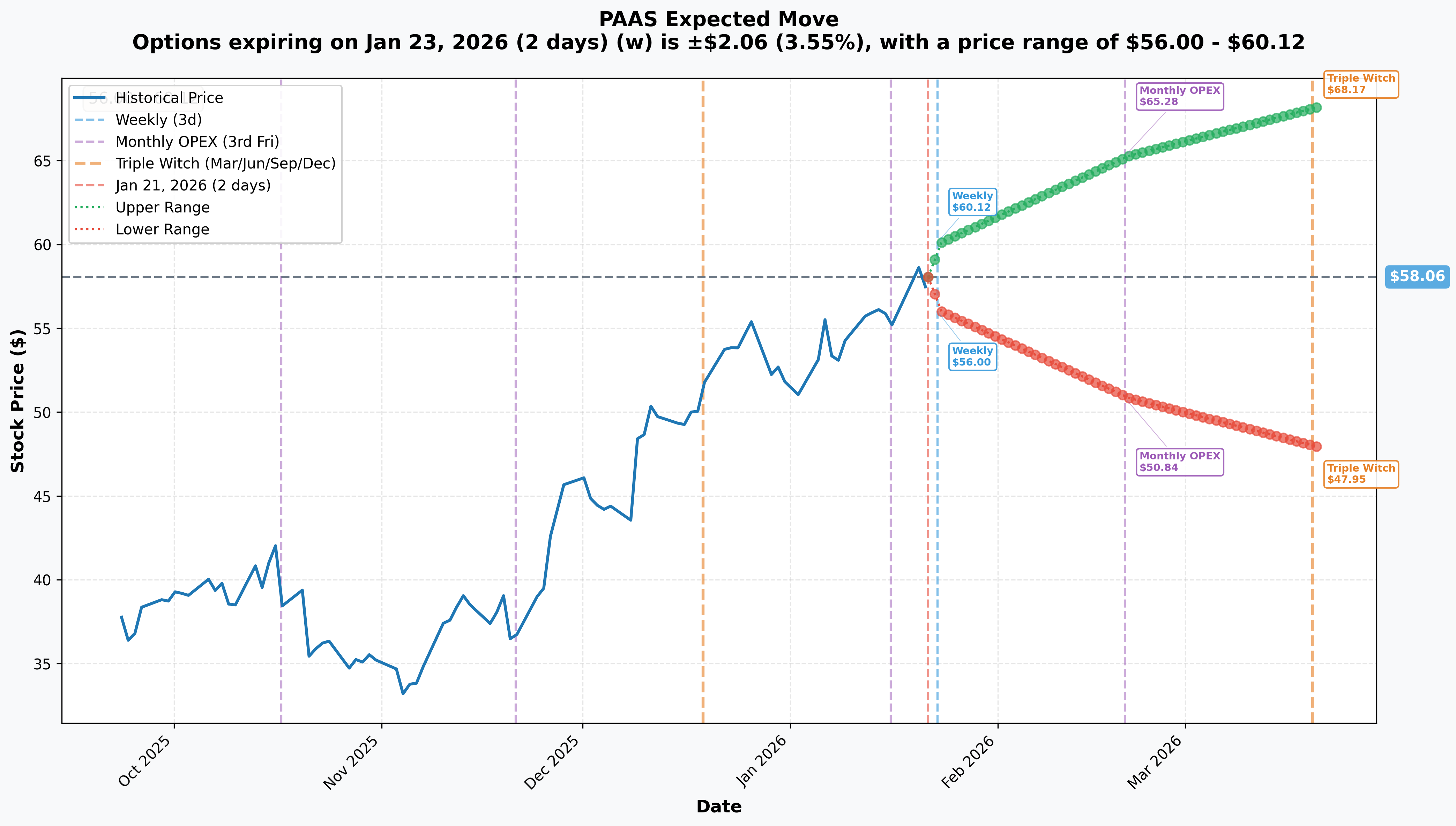

📊 Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry | Days Out | Implied Move % | Implied Move $ | Range |

|---|---|---|---|---|---|

| 📅 Weekly | Jan 23 | 2 days | ±3.55% | ±$2.06 | $56.00 - $60.12 |

| 📅 Monthly OPEX | Feb 20 | 30 days | ±12.44% | ±$7.22 | $50.84 - $65.28 |

| 📅 Triple Witch | Mar 20 | 58 days | ±17.42% | ±$10.12 | $47.95 - $68.17 |

Translation for regular folks:

Options traders expect PAAS to stay in a tight $56-$60 range this week (3.5% either way). But looking out to February OPEX, the market is pricing in a 12.4% potential swing - that's $7+ either direction! By March quarterly expiration, the implied range stretches from ~$48 to ~$68.

Key insight for the call sale: The March Triple Witch implied move caps out at $68.17 - still below the $70 strike where these calls were sold. This tells us the market does NOT expect PAAS to trade meaningfully above $68 even three months out. The call seller at $70 is positioned above where even volatile scenarios reach.

What about 2 years out? While we don't have specific 2028 implied move data, extrapolating the vol term structure suggests a wide range is possible - but the seller is clearly betting that even with 730 days of volatility, $70 is a stretch target.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

Q4 2025 / Full Year 2025 Earnings - February 18, 2026

According to Pan American Silver's press release, the company reports Q4 and full year 2025 results after market close on February 18th:

- 📊 Full-year silver production: 22.8 million oz (already announced - exceeded guidance of 22.0-22.5M oz!)

- 💰 Full-year gold production: 742.2 thousand oz (within guidance)

- 🏦 Year-end cash position: Estimated $1.319 billion (up $408M from Q3)

- 💎 Juanicipio contribution: First full contribution from acquired asset

- 📈 Q3 highlights to build on: Record $251.7M free cash flow, $169.2M net earnings

La Colorada Skarn Updated PEA - Q2 2026

Per Pan American Silver guidance, an updated Preliminary Economic Assessment for La Colorada Skarn is expected in Q2 2026:

- 🏭 Potential: Annual silver production averaging 17.2 million ounces during first 10 years

- 💵 Capital requirements: Part of planned 2026 capex of $515-$550 million

- 🎯 Significance: This is a major growth project that could significantly expand PAAS production profile

2026 Production Guidance (Already Released)

According to Business Wire, 2026 guidance shows strong growth:

| Metric | 2026 Guidance | 2025 Actual | Change |

|---|---|---|---|

| Silver Production | 25-27M oz | 22.8M oz | +10-18% |

| Gold Production | 700-750K oz | 742.2K oz | Flat |

| Silver AISC | $15.75-18.25/oz | Lower | - |

| Capex | $515-550M | - | - |

✅ Past Catalysts (Already Happened)

MAG Silver Acquisition Completed - September 4, 2025

Per Mining.com, the transformational $2.1B acquisition closed:

- 💰 Deal structure: US$500M cash + ~60.2M Pan American shares

- 🏭 Key asset: 44% JV interest in Juanicipio mine (Fresnillo operates with 56%)

- 📊 Resource addition: +58M oz silver to proven & probable reserves

- 🎯 Initial contribution: 2.5M oz silver + $44M dividend in December 2025

Record Q4 2025 Production

As reported by Pan American Silver:

- 🥈 Silver production: 7.3 million oz (record quarterly production!)

- 🥇 Gold production: 197.8 thousand oz

- ✅ Exceeded annual guidance ranges

Silver Price Surge - 2025

According to GoldSilver:

- 📈 Silver surged from ~$30/oz (January 2025) to ~$70/oz (December 2025) - up 147%!

- 🏆 All-time high of $54.47/oz broke the 1980 record on October 17, 2025

- 💰 Gold broke above $4,000/oz for first time in October 2025

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, upcoming catalysts, and the short call positioning, here are the scenarios through January 2028:

📈 Bull Case (20% probability)

Target: $70+ (call seller loses)

How we get there:

- 💎 Silver continues bull run to $100/oz as BNP Paribas forecasts

- 🏭 La Colorada Skarn PEA shows even better economics than expected

- 📈 Production ramp exceeds 27M oz guidance, margins expand significantly

- 🌍 Central bank gold/silver buying accelerates, driving sustained precious metals demand

- 💰 PAAS P/E multiple expands from 32x to 40x+ on growth acceleration

- 🚀 Stock breaks $60 gamma resistance, momentum carries to $65, then $70+

Call seller P&L if PAAS at $75 in January 2028:

- Calls worth $5 intrinsic value

- Loss = ($5.00 - premium received) x 390,000 shares

- Premium received averaged ~$8.70/contract, so still profitable unless above ~$78.70

Probability assessment: Only 20% because reaching $70 requires another 21.5% gain from already-extended levels, plus sustained silver prices at historically elevated levels for 2 more years.

🎯 Base Case (55% probability)

Target: $50-$65 range (call seller wins)

Most likely scenario:

- ⚖️ Silver prices consolidate in $55-70/oz range after massive 2025 rally

- 📊 Production growth delivers as guided (25-27M oz) but already priced in

- 🏦 Q4 earnings solid but no major surprises - $0.45-0.55 EPS range

- 📉 Some profit-taking after 149% rally, healthy pullback to $50-55 area

- 🔄 Stock trades in wide $50-65 range for 12-18 months digesting gains

- 🌍 Precious metals cycle matures, base case gold $4,500-5,000, silver $55-65

Call seller P&L in base case:

- Calls expire worthless or minimal value

- Full $3.4M premium retained

- ROI: 100% on premium collected

Why 55% probability: After 149% rally, stocks typically need time to consolidate. Silver at $70/oz is already at historical extremes. While fundamentals remain strong, valuation and momentum suggest a breather is more likely than continued parabolic moves.

📉 Bear Case (25% probability)

Target: $35-$50 (call seller big winner)

What could go wrong:

- 😰 Silver prices correct sharply to $45-50/oz as 2025 rally mean-reverts

- 🇲🇽 Mexico regulatory risks materialize - royalty hikes halt mining investments per EY Mining Report

- 💸 Operating cost inflation continues - Peru costs +84%, Mexico +58% per EY data

- 🌍 Federal Reserve raises rates, strengthening dollar and crushing precious metals

- 📉 Broader commodity selloff as recession fears emerge

- 🏭 La Colorada Skarn PEA disappoints on economics or timeline

Key support levels if selling intensifies:

- 🛡️ $55: Major gamma support (5.85B) - first major defense

- 🛡️ $50: Psychological round number with 2.94B gamma

- 🛡️ $45: Extended bear case floor

Call seller P&L in bear case:

- Calls expire completely worthless

- Full $3.4M premium retained

- Meanwhile, if covered call, underlying shares down significantly (offset by premium)

Probability assessment: 25% because precious metals rarely maintain parabolic moves indefinitely. The regulatory and cost headwinds in Latin America are real, and silver's 147% rally in 2025 created stretched conditions.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put Writing at Support

Play: Sell cash-secured puts at gamma support to potentially buy PAAS at a discount

Structure: Sell PAAS $50 puts expiring March 20, 2026 (58 days)

Why this works:

- 💰 Collect premium while waiting for pullback (estimated $1.50-2.00/contract based on current IV)

- 🎯 $50 strike sits at major gamma support (2.94B) with 12.9% downside cushion

- ⏰ If assigned, effective purchase price ~$48 vs current $57.58 - 17% discount!

- 📊 Implied move data shows $47.95 as lower range for March - just below put strike

- 🏦 Uses 149% rally patience - why chase when you can get paid to wait for pullback?

Estimated P&L:

- 💵 Premium collected: ~$150-200 per contract ($1,500-2,000 per 100 shares)

- ✅ If PAAS stays above $50: Keep entire premium (8-10% return on collateral in 58 days)

- 📉 If assigned at $50: Own PAAS at ~$48 effective cost basis - attractive entry after pullback

Position sizing: Only write puts on shares you'd actually want to own. One contract = $5,000 collateral required.

Risk level: Moderate (defined risk to downside, requires capital) | Skill level: Intermediate

⚖️ Balanced: Call Spread Premium Collection (Mini Version of This Trade)

Play: Sell call spread capturing premium decay in extended stock

Structure: Sell PAAS $65/$70 call spread expiring June 2026

Why this works:

- 🎯 Mimics the institutional trade but with defined risk and smaller capital requirement

- 📊 $65 strike sits at gamma resistance (1.30B), $70 is where big money is betting against

- ⏰ 5-month duration captures potential consolidation phase

- 💰 Collect premium as time decay works in your favor

- 🛡️ Defined risk: max loss is $5 spread width minus premium collected

Estimated P&L:

- 💵 Premium collected: ~$1.50-2.00 per spread

- 📈 Max profit: $150-200 per spread if PAAS below $65 at June expiration

- 📉 Max loss: $300-350 per spread if PAAS above $70

- 🎯 Breakeven: ~$66.50-67

When to enter:

- ✅ Wait for any rally toward $60 gamma resistance for better entry

- ⏰ Consider after Q4 earnings (Feb 18) if stock spikes on results

Risk level: Moderate (defined risk, bearish-neutral directional) | Skill level: Intermediate

🚀 Aggressive: Post-Earnings Volatility Play

Play: Buy straddle before Q4 earnings to capture potential big move

Structure: Buy PAAS $57.50 straddle expiring February 20, 2026 (enters around Feb 10)

Why this could work:

- 📊 Q4 earnings on Feb 18 is major catalyst - record production already announced but details matter

- 🎢 Implied volatility will spike pre-earnings, creating potential for both directions

- 💎 If La Colorada Skarn update comes early or production surprises, could move 15%+

- 📉 If commodity correction begins or costs disappoint, could drop 10-15%

- ⏰ Earnings IV typically underprices actual moves in commodity stocks

Risks (SERIOUS):

- 💸 EXPENSIVE: Straddles in elevated IV environment are costly

- ⏰ IV CRUSH: Even with 10% move, IV collapse post-earnings could hurt both legs

- 📊 Stock could move 5% and you still lose on time decay

- 🎢 Need 12%+ move to profit after IV crush

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Extended valuation after 149% rally: PAAS trades at 31.9x P/E after more than doubling in a year. According to Yahoo Finance, the stock hit all-time highs of $58.30 on January 20, 2026. Much of the good news (MAG acquisition, production growth, silver rally) is already reflected in the price. Limited margin of safety at current levels.

-

🥈 Silver price volatility is extreme: Silver surged 147% in 2025 per GoldSilver, creating stretched conditions. If Fed raises rates or dollar strengthens, silver could correct 20-30% rapidly. Support at $69-70 per Forex.com analysis, but "after such a powerful rally, the outlook is no longer one-sided."

-

🇲🇽 Latin American regulatory risks: Per EY Mining Report, Mexico has proposed royalty hikes that could halt ~$6.9B in mining investments. Peru mining costs have increased 84% since 2019. Mexico costs up 58%. PAAS has significant exposure to both countries plus Bolivia, Argentina, and Guatemala.

-

💸 Analysts trading BELOW current price: Average analyst price target is $44-50 according to Stock Analysis and TipRanks. Even the most bullish target from BofA at $68 is below the $70 call strike. When stock trades 20%+ above average analyst targets, caution is warranted.

-

🏭 Execution risk on growth projects: La Colorada Skarn requires significant capital ($515-550M total capex in 2026 per company guidance). Large mining projects frequently face delays, cost overruns, and permitting challenges. Any disappointment on PEA economics could pressure stock.

-

🌍 Currency exposure across 6 countries: PAAS has exposure to PEN, MXN, ARS, BOB, GTQ, CAD, CLP, and BRL per company filings. Volatile EM currencies can swing operating costs significantly quarter to quarter.

-

📊 Short call seller positioned for flat/down: A $3.4M institutional trade betting against $70 is a signal that sophisticated players see limited upside. When institutions sell premium at these sizes, they typically have strong conviction. This doesn't mean they're right, but it's worth noting.

-

⏰ 2-year LEAPS duration means lots can change: Between now and January 2028, we could see: Fed policy shifts, global recession, commodity supercycle end, new regulations, management changes, operational issues. The long duration creates uncertainty in both directions.

🎯 The Bottom Line

Real talk: Someone just collected $3.4 MILLION selling January 2028 $70 calls on Pan American Silver - betting that even with 2 full years of potential upside, PAAS won't sustainably trade above $70. After the stock's incredible 149% rally in 2025, smart money is saying "the easy money has been made."

What this trade tells us:

- 🎯 Institutional view: PAAS likely caps out somewhere between current $57.58 and $70 over the next 2 years

- 💰 They're comfortable giving up potential gains above $70 in exchange for $3.4M in immediate income

- ⚖️ The trade structure (selling calls 21.5% above current price) shows confidence but not outright bearishness

- 📊 If this is a covered call, they're happy to sell at $70 if it gets there - still 21%+ more upside

- ⏰ The 2-year duration shows conviction that silver's parabolic rally won't sustain at these levels

This is NOT a "PAAS is crashing" signal - it's a "the rally is getting long in the tooth" signal.

If you own PAAS:

- ✅ Consider selling covered calls at $65-70 strikes to generate income while you hold

- 📊 Your cost basis matters - if you bought under $30, protecting 100%+ gains makes sense

- 🎯 Set trailing stops around $50-52 (gamma support area) to protect against deeper pullback

- ⏰ Q4 earnings on February 18 is next major catalyst - assess position before/after

If you're watching from sidelines:

- ⏰ Patience pays - stock is at all-time highs with analysts targeting 15-25% lower

- 🎯 Better entry opportunities likely come on pullbacks to $50-55 gamma support zone

- 📈 If you want exposure, sell cash-secured puts at $50 to get paid to wait

- 🏦 Watch Q4 earnings reaction on Feb 18 for sentiment shift signals

If you're bullish long-term:

- 💎 Silver supercycle thesis remains intact with forecasts ranging to $100/oz per BNP Paribas

- 🏭 Production growth (25-27M oz 2026) and Juanicipio economics are legitimate catalysts

- 📊 If silver sustains $65-70/oz, PAAS earnings power could exceed current estimates

- ⏰ But even bulls should respect the parabolic nature of the rally and manage position sizes

Mark your calendar - Key dates:

- 📅 January 23, 2026 - Weekly options expiration (±3.55% implied move)

- 📅 February 18, 2026 - Q4/FY 2025 earnings after market close

- 📅 February 20, 2026 - Monthly OPEX (±12.44% implied move)

- 📅 March 20, 2026 - Triple Witch quarterly expiration

- 📅 Q2 2026 - La Colorada Skarn Updated PEA expected

- 📅 January 21, 2028 - These short calls expire (730 days away!)

Final verdict: Pan American Silver's long-term fundamentals remain compelling - diversified production, strong balance sheet ($2B+ liquidity), and precious metals tailwinds. BUT, at 31.9x P/E after a 149% rally with the stock trading above every analyst target, the risk/reward isn't as favorable as it was 12 months ago. The $3.4M short call trade is a signal that sophisticated players are capping their expectations and monetizing elevated volatility.

The call seller's playbook is worth considering: In extended markets, sometimes the smartest money to make is the premium you collect, not the breakout you chase.

If you're long, protect gains. If you're flat, be patient for better entry. If you're a premium seller, these elevated volatility levels are your friend.

Silver may or may not hit $100/oz - but $3.4M says $70 PAAS is a stretch. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores of 108-157 indicate this trade's extreme unusualness relative to recent PAAS options history - this happens only a few times per year. LEAPS options carry extended duration risk including time decay and potential for significant underlying price changes. Covered call writing limits upside potential. Always do your own research and consider consulting a licensed financial advisor before trading.

About Pan American Silver Corp. (PAAS): Pan American Silver Corp. is a silver and gold mining company operating 10 mines across Latin America and Canada, producing silver, gold, zinc, lead, and copper, with a market cap of $24.74 billion in the Precious Metals Mining industry. The company employs approximately 9,000 people and is listed on both NYSE and TSX.