🚀 PAR - $658K MEGA BULLISH Call Bet on Burger King Rollout!

📅 December 11, 2025 | 🔥 EXTREMELY UNUSUAL Activity - Z-Score 7,421!

🎯 The Quick Take

Someone just dropped $658,000 on a single bullish call bet on PAR Technology (NYSE: PAR)! This isn't just any trade - with a Z-Score of 7,421, this is 7,421 TIMES the average trade size for PAR! We're talking about one of the most unusual trades we've ever tracked. The buyer scooped up 3,500 April 2026 $50 calls, betting on a massive 31% rally from today's $38 price. The timing? Perfect. PAR is in the middle of rolling out its POS systems to 7,000 Burger King locations through mid-2026, and this trade says "I believe this rollout is going to CRUSH IT." Translation: Someone with serious conviction just made a massive bet that PAR is heading to $50+ as the Burger King partnership accelerates!

📊 Company Overview

PAR Technology Corporation (NYSE: PAR) is the enterprise restaurant tech company transforming how major chains operate:

- Industry: Enterprise Restaurant Technology (POS, Analytics, Engagement Software)

- Market Cap: $1.39 billion (down from $2.7B year ago due to market volatility)

- Current Price: ~$38.04

- 52-Week Range: $31.65 - $81.51 (massive 157% swing!)

- Key Customers: Burger King (7,000 locations), Popeyes, Five Guys, McDonald's (via TASK acquisition), Starbucks (via TASK)

- Revenue Model: Shifting to high-margin subscription SaaS (78% subscription growth in Q1 2025)

- Critical Differentiator: PAR targets enterprise chains with 100+ locations - NOT competing with Toast/Square who focus on mom-and-pop shops

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (December 11, 2025):

| Symbol | Side | Type | Expiration | Premium | Strike | Volume | Spot | Z-Score |

|---|---|---|---|---|---|---|---|---|

| PAR $50 CALL | BUY | CALL | 2026-04-17 | $658K | $50 | 3,500 | $38.04 | 7,421.09 |

Option Symbol: PAR20260417C50

Position Type: BTO (Buy to Open) - Brand new bullish position

🤓 What This Actually Means

This is a long call position - the most straightforward bullish bet you can make! The trader:

- ✅ Paid $658,000 for the right to buy 3,500 contracts (350,000 shares) at $50

- ✅ Betting on a 31% rally from current $38 to $50+ by April 17, 2026

- ✅ Maximum profit: UNLIMITED above $50

- ✅ Maximum loss: $658,000 (the premium paid)

- ✅ Breakeven: ~$51.88 (strike + premium paid per share)

- ✅ Days to expiration: 127 days (roughly 4 months)

Unusual Score: 🚨 EXTREMELY UNUSUAL - Z-Score of 7,421.09!

Let that sink in. This trade is 7,421 TIMES larger than the average PAR options trade. In statistical terms, this is so far outside normal that it happens basically NEVER by chance. This is either:

- A massive institutional bet on the Burger King rollout success

- Inside knowledge (legal) about how installations are progressing

- Conviction that Q2 2025 earnings (August 8) will blow the doors off

The buyer isn't just bullish - they're betting the farm that PAR's transformation story is about to accelerate dramatically. With install velocity expected to peak in Q3-Q4 2025 and the company targeting 20%+ organic ARR growth, someone thinks Wall Street is underestimating this story.

📈 Technical Setup / Chart Analysis

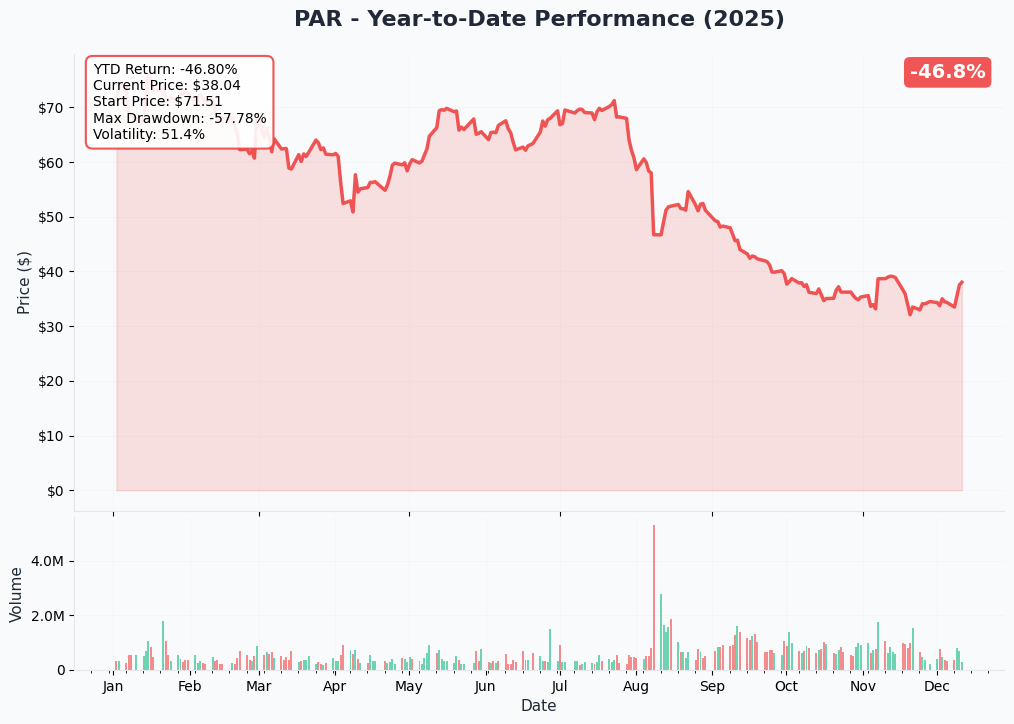

YTD Performance Chart

PAR has been on an absolute rollercoaster ride in 2024-2025! The stock hit a 52-week high of $81.51 in mid-2024 before pulling back to current levels around $38. That's a brutal 53% drawdown from the highs. But here's the thing - the fundamentals have actually IMPROVED during this pullback:

Key observations:

- High volatility: 52-week range of $31.65-$81.51 shows this stock moves BIG

- Technical support: Currently trading near the $38 level with support at $35

- Oversold condition: After a 53% decline, stock is potentially coiled for reversal

- Fundamental divergence: Stock down 49% while ARR grew 52% and subscription revenue up 78%

This is the classic setup where fundamentals improve but the stock gets beaten down. Our $50 call buyer is betting the market finally reconnects price to the improving business reality.

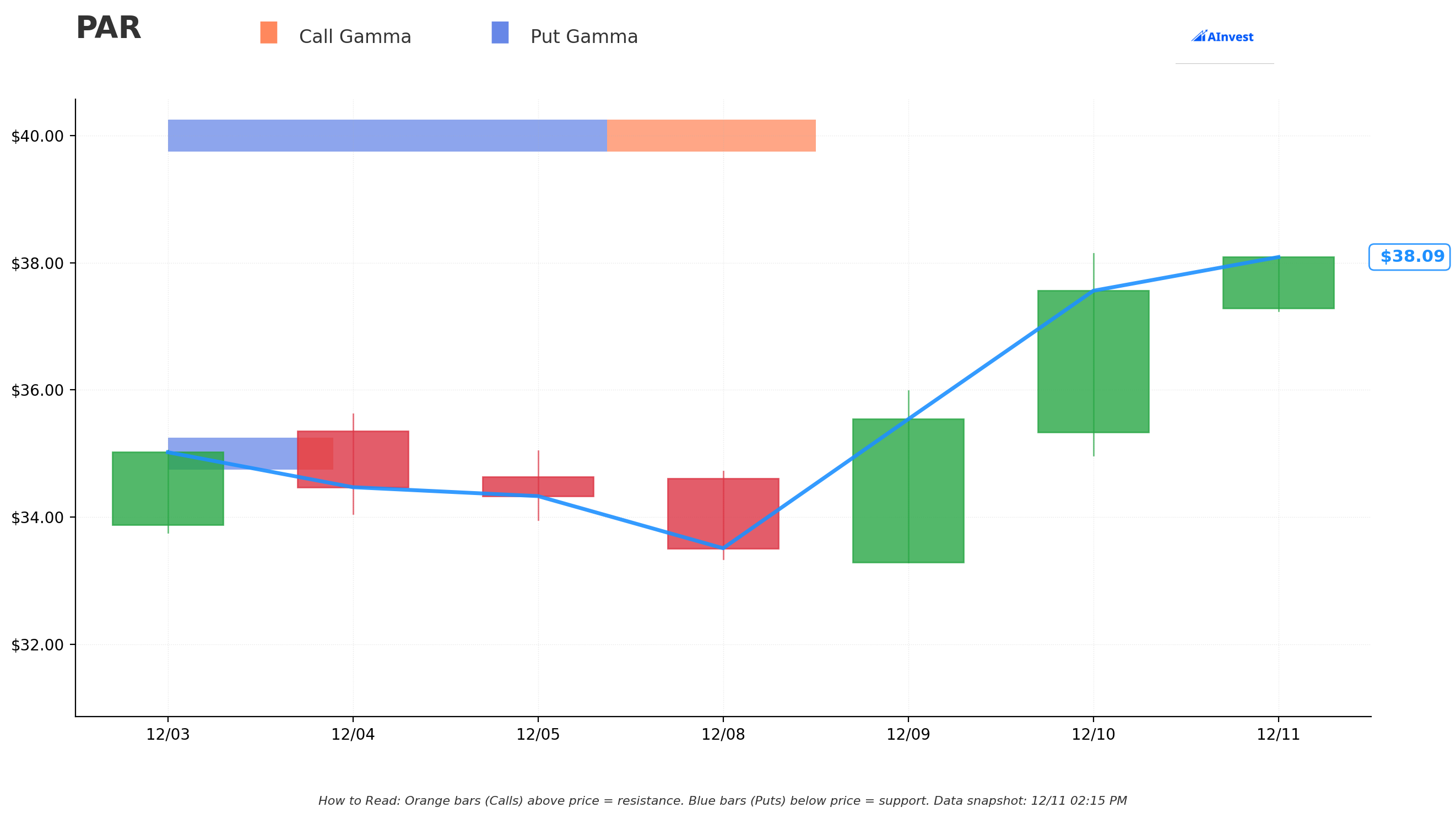

Gamma-Based Support & Resistance Analysis

Current Price: $38.04

The gamma chart reveals the key battleground levels that will determine if this trade wins:

🔵 Support Levels (Put Gamma):

- $35.00: STRONGEST support with 0.15 GEX - this is the floor that's held multiple times

- Distance from current: -8.0% downside

- Put wall here means dealers will buy stock as it falls toward $35, creating natural support

🟠 Resistance Levels (Call Gamma):

- $40.00: MAJOR resistance at 0.58 GEX (HIGHEST on the entire chain!)

- Distance from current: +5.2% upside

- This is the critical level to break - heavy dealer hedging will occur here

- Net GEX: -0.21 (bearish), meaning dealers are net short calls

- $45.00: Secondary resistance at 0.21 GEX

- Distance from current: +18.3% upside

- Breaking $40 opens the door to this level

- $50.00: Our trader's target strike

- Distance from current: +31.4% upside

- This is where maximum pain for dealers occurs

Net GEX Bias: BULLISH (0.83 Call GEX vs 0.54 Put GEX)

What this means: Despite the bearish positioning at $40, the overall options flow is BULLISH with more call gamma than put gamma. This suggests options traders are positioned for upside. The massive $40 resistance is the key - once that cracks, gamma dynamics flip bullish and dealers will be forced to chase the stock higher to hedge their short call exposure. It's a "dam breaking" setup - grind through $40 and momentum accelerates toward $45-50.

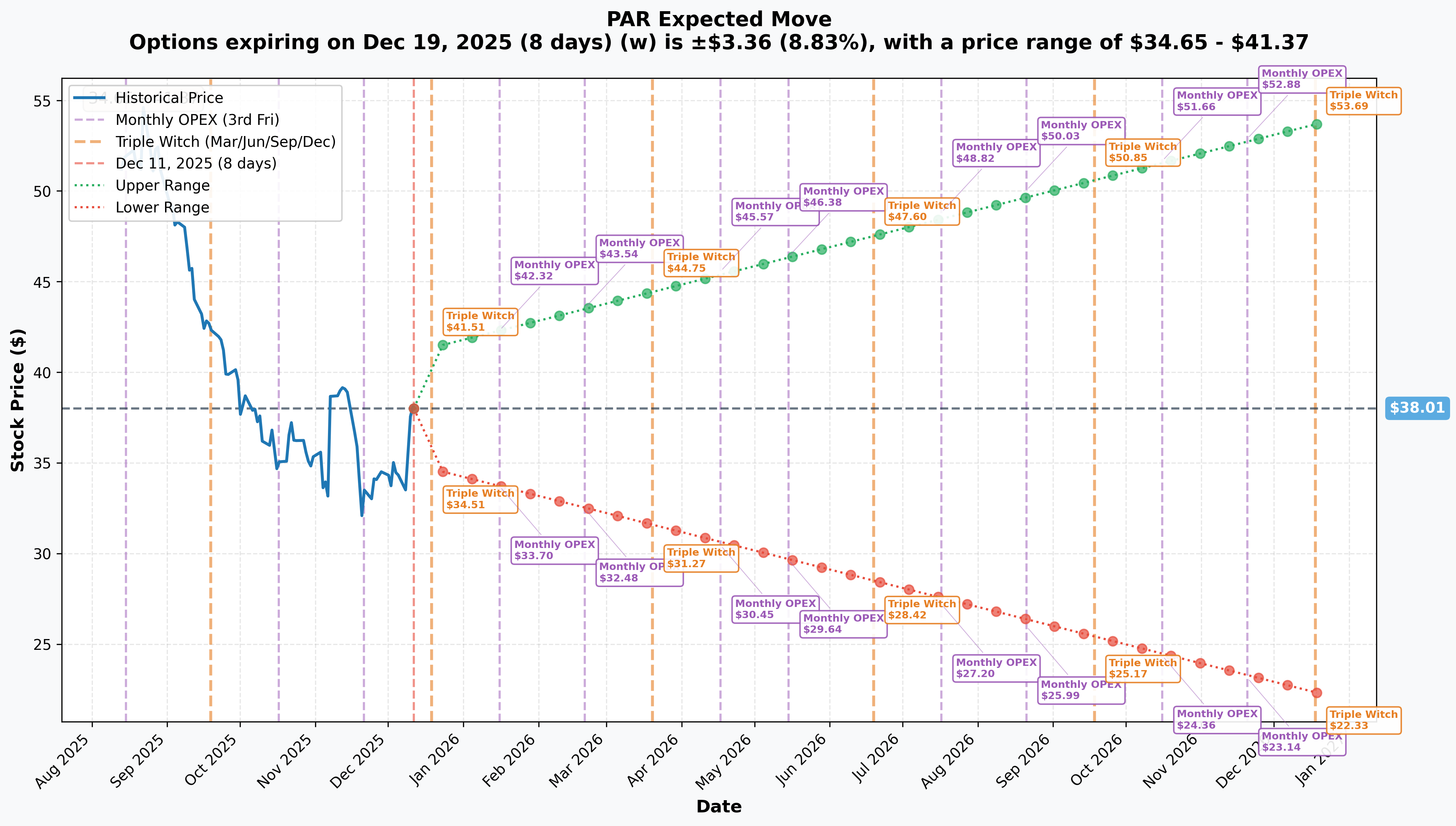

Implied Move Analysis

Current Price: $38.01

Let's look at what options markets are pricing in for volatility:

📅 Monthly OPEX (Dec 19, 2025) - 8 days out:

- Implied Move: ±8.83% ($3.36)

- Range: $34.65 - $41.37

- Reliability: HIGH (near-term expiry)

📅 Yearly LEAPS (Dec 2026) - 372 days out:

- Implied Move: ±41.26% ($15.68)

- Range: $22.33 - $53.69

- Reliability: HIGH

What this tells us: The market is pricing in MASSIVE volatility for PAR over the next year. The yearly LEAPS are pricing $53.69 as the top end - which is ABOVE our trader's $50 strike! This means the market is actually giving this trade decent odds of success. The implied volatility is high (41% annual move) which tells you this stock can swing wildly in either direction.

For our April 2026 $50 call buyer, the implied move suggests the market thinks PAR could reach that level - it's not some crazy out-of-the-money lottery ticket. It's an aggressive but reasonable bet.

🎪 Catalysts

Upcoming Events

Q2 2025 Earnings - August 8, 2025

- Confirmed earnings date after market close

- Why it matters: This is THE catalyst for our call buyer!

- Key metrics to watch:

- Burger King installation progress (rollout continues through mid-2026)

- Organic ARR growth (target: 20%+ for 2025)

- Adjusted EBITDA margin expansion (need to exceed Q1's $4.5M)

- New multiproduct deal signings

- Probability: 100% (confirmed)

- Expected Impact: If installations are ahead of schedule and EBITDA beats, stock could rocket

Burger King Rollout Acceleration - Q1-Q2 2026

- Scale: 7,000 domestic Burger King locations

- Timeline: Rollout started Q2 2024, continues through mid-2026

- Products: Brink POS and MENU Link marketplace order management software

- CEO Quote: "It's hard to express how transformative this new customer will be from both the strategic and the financial aspect of PAR"

- Expected Impact: 20-30% ARR growth in FY24-25

- Why it matters: This is the single biggest driver of PAR's growth story

- Probability: High (contract signed, installations in progress)

Popeyes Implementation Progress - H2 2025 through 2026

- Status: Tier 1 win alongside Burger King

- Timeline: Multi-year contracted rollout expected second half of 2025 through 2026

- Why it matters: Validates PAR's platform with another major QSR brand

- Probability: High (contracted)

Delaget Integration Synergies - Ongoing through 2025

- Deal: $132 million acquisition closed December 31, 2024

- Customer Base: 30,000+ locations across 125+ brands

- Cross-sell Opportunity: Analytics platform to existing PAR POS customers

- Why it matters: Could accelerate ARR growth beyond Burger King

- Probability: Medium (integration risk but signed contracts)

TASK Global Expansion - Ongoing

- Deal: $206 million acquisition closed July 22, 2024

- Global Reach: McDonald's in 65 markets, Starbucks relationships

- Expected Impact: Over $80M of ARR and $20M+ Adjusted EBITDA combined with Stuzo

- Why it matters: International expansion without building from scratch

- Probability: Medium (integration complexity)

Recently Completed

Q1 2025 Earnings Beat - May 9, 2025

- Revenue: $103.86M (48% YoY increase)

- Subscription Revenue: $68.4M, up 78% YoY

- ARR: $282M (52% growth), including 18% organic growth

- Adjusted EBITDA: $4.5M positive (nearly $15M improvement YoY)

- Stock Reaction: +5.8% to $66.02

- Impact: Proved the business model is scaling profitably

Q4 2024 Strong Results - February 28, 2025

- Revenue: $105M, up 50% YoY

- Subscription Revenue: Up 95% YoY, including 25% organic growth

- Adjusted EBITDA: $5.8M (more than doubled from Q3)

- Impact: Second consecutive quarter of positive EBITDA - trend confirmed

Balance Sheet Optimization - November 27, 2024

- Debt Exchange: Exchanged $100M of 2.875% Convertible Notes for 2.4M shares + $336K cash

- CEO Comment: "Provide flexibility to our balance sheet to unlock future accretive investment opportunities"

- Impact: Reduced debt burden, improved financial flexibility

🎲 Price Targets & Probabilities

Using gamma levels, catalyst timing, fundamental trajectory, and analyst consensus:

🚀 Bull Case (35% chance)

Target: $50-60

What needs to happen:

- Q2 earnings (Aug 8) crushes estimates with accelerating Burger King installations

- Install velocity peaks in Q3-Q4 2025 as guided

- Adjusted EBITDA grows sequentially to $6-8M range

- Organic ARR growth exceeds 20% target

- Popeyes rollout accelerates ahead of schedule

- Delaget cross-sell wins announced

- Analyst upgrades with price targets moving to $70-80 range

- Stock breaks through $40 gamma resistance, triggering dealer buying

For this trade:

- Massive profit - If stock hits $55, calls worth ~$5 each = $1.75M value (166% gain)

- At $60, calls worth $10 each = $3.5M value (432% gain!)

Key gamma levels: Breaking $40 (0.58 GEX) opens path to $45 (0.21 GEX), then $50

Market structure supports this: Analyst consensus price targets range $64-$73.60, with high estimate at $90. The bull case is IN RANGE of professional forecasts.

😐 Base Case (45% chance)

Target: $38-45 range

What needs to happen:

- Burger King rollout continues on schedule but doesn't accelerate

- Q2 earnings meet but don't beat expectations

- Adjusted EBITDA stays in $4-6M range (modest growth)

- ARR grows 20% organically as guided (not accelerating)

- TASK/Delaget integrations progress slowly

- Stock grinds higher but gets stuck at $40-45 resistance

- Market cap recovers to ~$1.8-2.0B (still below 2024 highs)

For this trade:

- Modest loss to small gain depending on where stock settles

- At $42: Calls worth ~$0.50-1.00 = $175K-350K value (loss of $300-480K)

- At $45: Calls worth ~$2.00 = $700K value (breakeven to small gain)

- Needs $51.88 to breakeven on premium paid

Key gamma levels: Stock gets capped at $40 resistance (0.58 GEX), grinds sideways

This is the "show me" scenario - market wants proof of execution before re-rating the stock higher. Not bearish, just skeptical.

😰 Bear Case (20% chance)

Target: $30-35

What needs to happen:

- Burger King rollout hits delays or technical issues

- Q2 earnings disappoint with slowing installation velocity

- Adjusted EBITDA declines sequentially (like Q1's $4.5M vs Q4's $5.8M)

- TASK/Delaget integrations prove harder than expected

- Competition from NCR Aloha (100,000 restaurants) or Oracle Simphony intensifies

- Restaurant technology spending slows if economy weakens

- Stock breaks below $35 support level

- Insider selling accelerates (currently low insider ownership at 3.7%)

For this trade:

- Total loss of $658,000 - calls expire worthless

Key gamma levels: Breaking $35 support (0.15 GEX) opens air pocket to $30

Risk factors supporting this:

- Stock already down 49% YoY despite strong fundamentals

- GAAP profitability still not achieved

- Three major acquisitions ($338M total) create integration risk

- Execution risk on 7,000-location rollout

💡 How To Play This

Our $50 call buyer has massive conviction, but you don't need to bet $658K to play this setup. Here are three ways to position based on your risk tolerance:

🛡️ Conservative: Bull Put Spread ($35/$40)

Strategy: Sell $40 puts, buy $35 puts (January 2026 expiry) Cost: Net credit received (income trade) Max Profit: Premium collected if PAR stays above $40 Max Loss: $5 per spread if PAR crashes below $35 Rationale: Gamma shows strong support at $35 and resistance at $40. Collect premium betting PAR stays in this range, similar to selling insurance. Works even if stock goes sideways.

Best for: Income-focused traders who think PAR won't crater but aren't sure about huge upside

⚖️ Balanced: Call Debit Spread ($40/$50)

Strategy: Buy $40 calls, sell $50 calls (April 2026 expiry) Cost: Net debit (lower than naked calls) Max Profit: $10 per spread if PAR hits $50+ Max Loss: Premium paid Rationale: Leverages the same $50 target as our whale trader but reduces cost by selling the $50 calls. Gives you exposure to the Burger King catalyst without risking as much capital.

Best for: Bullish traders who want defined risk and lower capital outlay

🚀 Aggressive: Long Calls ($45 or $50)

Strategy: Buy April 2026 $45 or $50 calls outright Cost: Full premium (higher theta decay) Max Profit: Unlimited above strike Max Loss: 100% of premium Rationale: Mimic the whale's trade with smaller size. You get pure upside leverage if the Burger King rollout accelerates and earnings blow out. This is the "I believe" trade.

Best for: Risk-tolerant traders with strong conviction in the Burger King catalyst

Position sizing advice: PAR's 52-week range of $31.65-$81.51 (157% swing!) tells you this stock is VOLATILE. Don't bet money you can't afford to lose. Even if you love the story, keep position size to 1-3% of portfolio max.

⚠️ Key Risks To Watch

Let's be brutally honest about what could go wrong:

Execution Risk on Burger King Rollout

Rolling out 7,000 locations over 2+ years is complex. Any delays, technical glitches, or service failures could tank the stock. PAR's entire bull thesis hinges on flawless execution.

Integration Complexity

PAR acquired TASK ($206M), Delaget ($132M), and Stuzo in 2024 - that's $338M+ deployed on M&A. Integrating three companies simultaneously while rolling out Burger King is a LOT of moving parts. Management must achieve $80M+ ARR and $20M+ Adjusted EBITDA targets or these deals become value destroyers.

Profitability Still Distant

Only three quarters of positive Adjusted EBITDA (Q3-Q4 2024, Q1 2025), and Q1's $4.5M was DOWN from Q4's $5.8M. GAAP profitability is still nowhere in sight. If EBITDA margins don't expand, market patience could run out.

Competition & Market Risk

NCR Aloha has 100,000 restaurants, Oracle Simphony has Starbucks/Dunkin'. These are entrenched, well-funded competitors. PAR also faces rapid AI adoption risk in restaurant tech (43% annual growth forecasted) - if they fall behind on AI integration, they lose competitive edge.

Valuation Disconnect

Stock is down 49% YoY while fundamentals improved. Why? Either:

- Market knows something we don't (bearish)

- Market is wrong and will correct higher (bullish)

- Forward multiples were too high even with growth (neutral)

Current price near $38 is actually BELOW some analyst targets of $64-$73.60, suggesting potential upside. But it also means Wall Street isn't unanimously bullish.

Insider Selling

Only 3.7% insider ownership, with insiders selling stock without offsetting purchases. This raises questions about management conviction. If they believed $50+ was coming, why aren't they buying?

Illinois BIPA Lawsuit

Alleged violations related to fingerprint scan data collection on POS systems. Legal proceedings are "costly, time consuming, distracting" and pose reputational risk with customers.

🎬 The Bottom Line

This $658K call trade is one of the most unusual we've ever tracked - Z-Score of 7,421 means someone is making a MASSIVE bullish statement. The thesis is clear:

The Bull Thesis: PAR is executing a transformational rollout with Burger King (7,000 locations through mid-2026), achieved first consecutive positive EBITDA quarters, subscription revenue growing 78% YoY with 69%+ gross margins, and strategic acquisitions (TASK/Delaget) position them as a consolidator in the $19.97B restaurant tech market growing at 16.4% CAGR. Stock down 49% YoY despite fundamentals improving = mispricing opportunity. Q2 earnings on August 8 could be the catalyst that finally reconnects price to value.

The Bear Thesis: Execution risk is MASSIVE. 7,000-location rollout + three major acquisitions ($338M deployed) = lots of things that can go wrong. GAAP profitability still absent, sequential EBITDA decline in Q1, low insider ownership (3.7%), and intense competition from NCR/Oracle all create risk. 52-week range of $31.65-$81.51 shows this stock can CRATER just as fast as it rallies.

Our Take: The trade makes sense IF you believe in the Burger King rollout story. The timing is right - install velocity peaks in Q3-Q4 2025, Q2 earnings in August will show progress, and gamma resistance at $40 (once broken) could trigger momentum to $45-50. But this is absolutely a HIGH RISK, HIGH REWARD play. The $658K buyer has deep pockets and can afford to be wrong. Most retail traders should use spreads to define risk.

Watch these key signals:

- Q2 Earnings (Aug 8) - Installation velocity, EBITDA growth, ARR acceleration

- $40 level - Breaking this gamma resistance opens the door to $45-50

- Insider buying - If management starts buying, bullish signal strengthens

- Competitive wins - Any new Tier 1 brand signings validate the platform

If PAR executes flawlessly on Burger King and the integrations, $50 is absolutely achievable. If they stumble, this trade goes to zero. That's the setup.

Trade carefully, size positions appropriately, and don't bet the farm unless you have conviction like our $658K whale! 🐋

⚠️ Disclaimer

This analysis is for informational and educational purposes only and should not be considered financial advice. Options trading involves substantial risk and is not suitable for all investors. Past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions.