🛢️ PBR Options Flow: $1.5M LEAPS Call SELL -- Premium Harvesting on Brazil's Oil Giant

📅 March 9, 2026 (2026-03-09) | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just sold $1.5 million worth of PBR LEAPS calls at the $22 strike expiring March 2027 -- a full year out. With PBR trading around $18.18, this $22 strike sits 21% above current price, making this a textbook covered call or premium collection play. The volume-to-open interest ratio of 30.4x screams unusual activity. This trade says: "I'm happy to collect fat premiums and dividends, and if PBR runs to $22 over the next year, I'll take that too." In a market roiled by the Iran oil shock, this is a sophisticated income strategy on one of the world's cheapest mega-cap oil stocks.

🏢 Company Overview

Petroleo Brasileiro S.A. - Petrobras (PBR) is Brazil's state-controlled oil and gas giant and one of the largest oil producers on the planet. The company dominates deepwater offshore production in Brazil's pre-salt fields, where lifting costs run as low as $5-7 per barrel -- among the cheapest anywhere in the world.

Key Stats:

- 💰 Market Cap: $113.4 billion

- 🛢️ Production: 3.0 million boed in 2025 (record, up 11% YoY)

- 💵 Dividend Yield: ~6-7.6% (one of the fattest yields in energy)

- 📊 Forward P/E: ~5.5x (absurdly cheap for a company this profitable)

- 🌊 Pre-Salt Dominance: 82% of total output from ultra-low-cost deepwater fields

- 🏛️ State Ownership: Brazilian government controls ~64% of voting shares

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the trade that triggered our unusual activity alert:

| Time | Symbol | Buy/Sell | C/P | Expiration | Strike | Volume | OI | Premium | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:29:59 | PBR | SELL | CALL | 2027-03-19 | $22 | 11,000 | 362 | $1,500,000 | $18.33 | $1.36 | PBR20270319C22 |

Total Premium Collected: $1,500,000 across 1 trade

🤓 What This Actually Means

Let's unpack why this trade is notable:

- 🐋 Big Premium Harvest: $1.5M in premium income collected in a single transaction

- 📅 LEAPS Expiration: March 19, 2027 = 375 days out. This trader is taking a year-long position

- 🎯 21% Out-of-the-Money: At $22 strike vs. $18.18 spot, the stock needs to rally 21% before the seller loses money beyond the premium

- 📊 Vol/OI Ratio: 30.4x: Volume was 11,000 contracts against only 362 open interest. That is 30x more volume than existing positions -- a massive spike

- 🏷️ Classification: Sell-to-Open (STO) Short Call -- this is a new position being established

- ⚡ Z-Score: 0 -- While the z-score reads flat (likely due to thin LEAPS data), the Vol/OI ratio tells the real story

Real Talk: This is almost certainly a covered call strategy. Here's why: selling naked calls on a stock that just surged 41% YTD with oil above $100/bbl would be reckless. More likely, this trader owns roughly 1.1 million shares of PBR (11,000 contracts x 100 shares) and is selling calls against the position to collect $1.5M in premium income on top of PBR's juicy 6-7% dividend yield. They're saying: "I'll cap my upside at $22 (still a 21% gain from here) in exchange for guaranteed income today."

The breakeven for the call seller is $23.36 ($22 strike + $1.36 premium). PBR would need to rally 28% over the next year before this trade actually loses money.

📈 Chart Check-Up

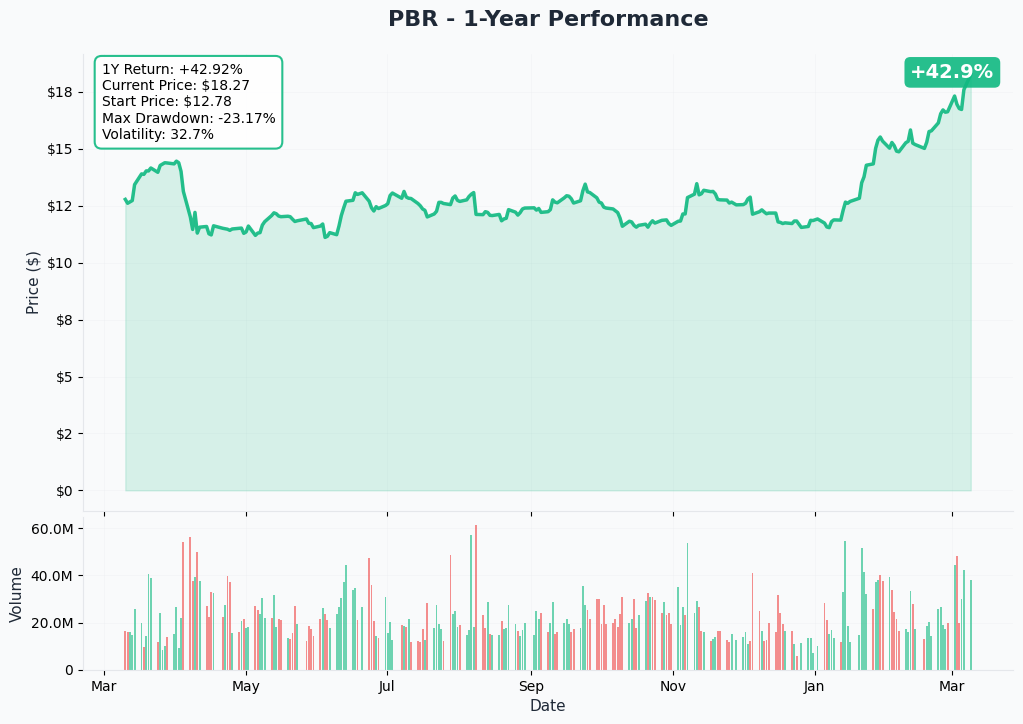

YTD Performance Analysis

PBR has been on a tear in 2025-2026, surging +41% YTD through early March as oil prices spiked and Q4 earnings crushed expectations. The stock is trading near its 52-week high of $17.82 and recently posted a +5.20% single-day move on March 6 following the earnings release.

Key Observations:

- Powerful uptrend accelerated by the Iran/Hormuz oil supply crisis

- Stock sitting near all-time highs with momentum firmly bullish

- The 41% YTD rally makes the covered call logic even more appealing -- locking in gains while collecting premium

- Short-term MA above long-term MA = general buy signal with a 3-month MACD also on a buy

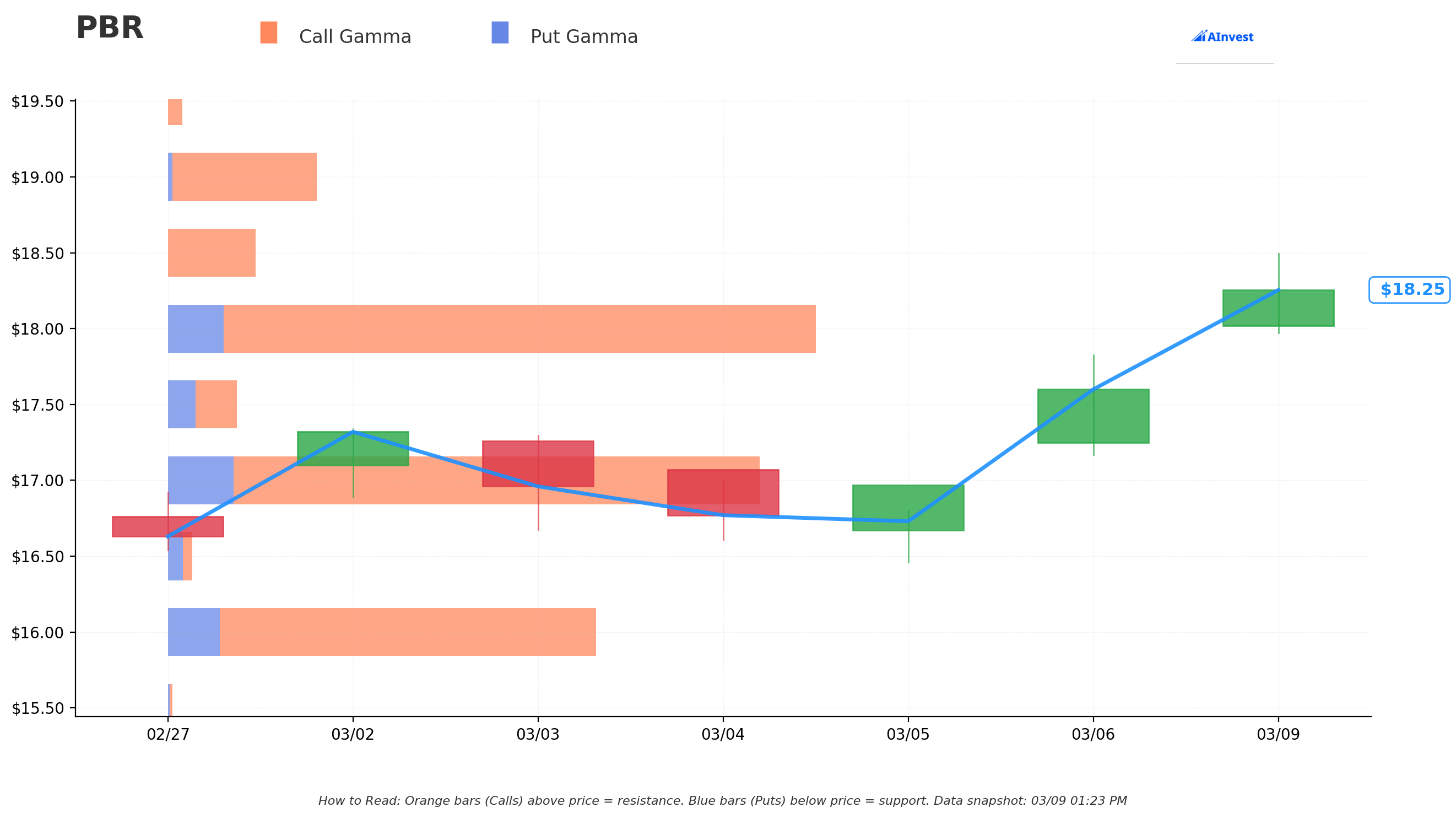

🎯 Gamma-Based Support & Resistance Analysis

What The Gamma Levels Tell Us:

The gamma exposure (GEX) data reveals natural price floors and ceilings created by options market maker hedging activity:

Key Support Levels (Where Dealers Buy Dips):

- 🔵 $18.00 -- Strongest support with 23.0B total GEX (only 1.0% below current price). This is a wall.

- 🔵 $17.00 -- Massive secondary support with 21.1B total GEX (6.5% below). A fortress if the first level breaks.

- 🔵 $16.00 -- Deep support at 15.1B GEX (12.0% below)

- 🔵 $15.00 -- Last line of defense with 20.1B total GEX (17.5% below)

Key Resistance Levels (Where Upside Gets Sticky):

- 🟠 $18.50 -- Immediate resistance with 3.1B net call gamma (1.7% above). This is the first hurdle.

- 🟠 $19.00 -- Moderate resistance at 5.2B total GEX (4.5% above)

- 🟠 $20.00 -- Major resistance with 23.1B total GEX (10.0% above). Morgan Stanley's new price target sits right here.

- 🟠 $21.00 -- Light resistance at 1.1B GEX (15.5% above)

Translation for regular folks: The $18 level is built like a bunker -- enormous call gamma means dealers will be buying the stock aggressively on any dip to that level. Meanwhile, $20 is the big resistance magnet, which happens to align perfectly with Morgan Stanley's freshly raised $20 price target.

Net GEX Bias: BULLISH -- Total call GEX of 115.6B vs. put GEX of 29.3B. Dealers are positioned for upside, and any move higher will trigger additional buying pressure from delta-hedging.

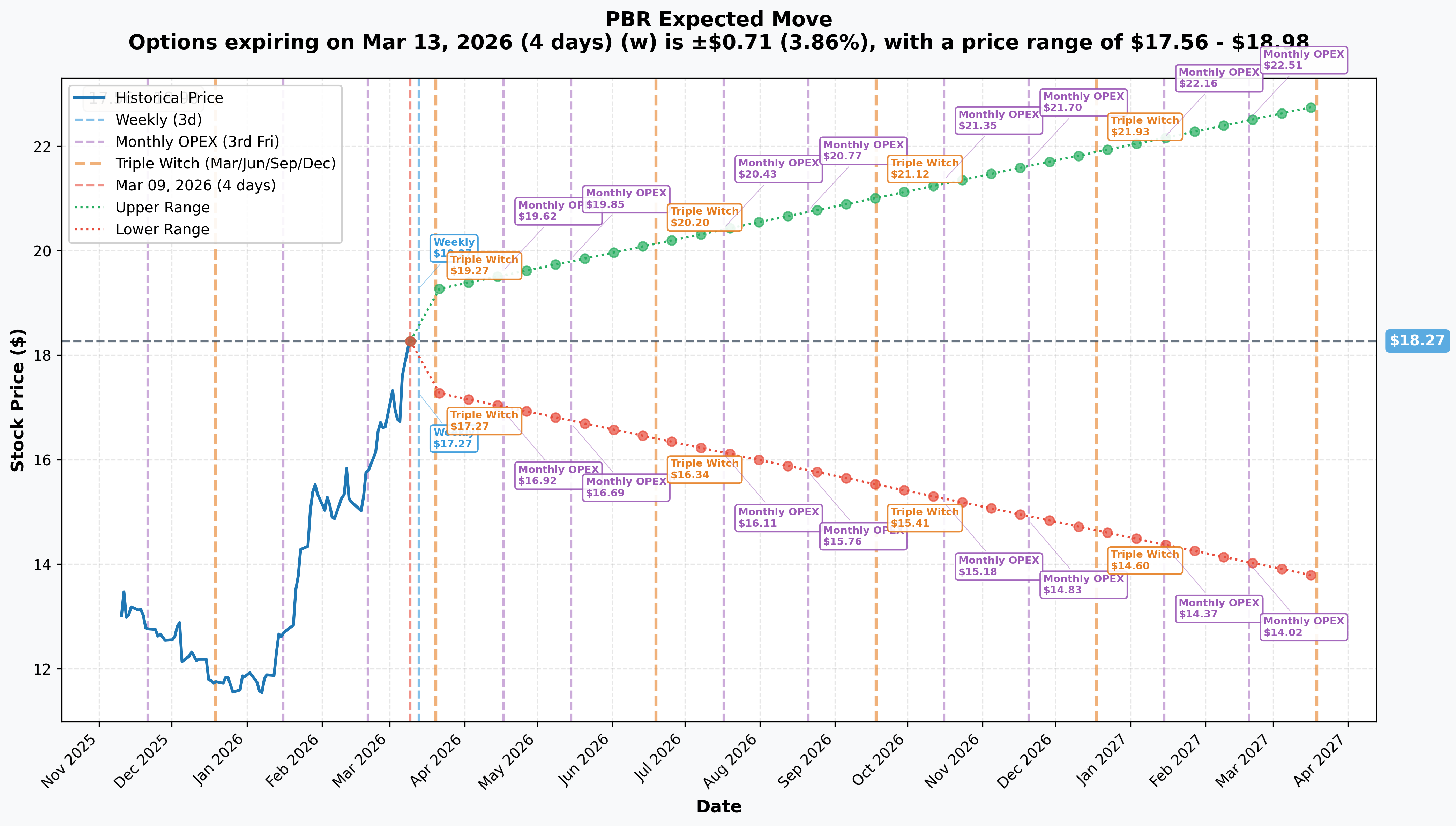

📊 Implied Move Analysis

What Options Are Pricing In:

| Timeframe | Expiry | Days Out | Implied Move | Dollar Range | Price Range |

|---|---|---|---|---|---|

| Weekly | Mar 13 | 4 | ±3.86% | ±$0.71 | $17.56 - $18.98 |

| Monthly OPEX | Mar 20 | 11 | ±5.44% | ±$0.99 | $17.28 - $19.26 |

| Triple Witch | Mar 20 | 11 | ±5.44% | ±$0.99 | $17.28 - $19.26 |

| Yearly LEAPS | Mar 19, 2027 | 375 | ±24.66% | ±$4.50 | $13.76 - $22.77 |

The Critical Insight: Look at that yearly LEAPS implied move -- the market is pricing PBR's upper range at $22.77 over the next year. The $22 call that was sold sits just barely inside that upper bound. This means the options market gives roughly a 15-20% probability that PBR reaches $22 by March 2027. The seller is betting on the more likely outcome -- that PBR stays below $22 -- and pocketing $1.5M for that bet.

Near-term: The weekly implied move of ±3.86% ($17.56-$18.98) reflects elevated volatility from the Iran/Hormuz oil supply crisis. PBR is swinging with crude oil right now, and crude is swinging on war headlines.

🎪 Catalysts

🔥 Why PBR Is in Play Right Now

1. Q4 2025 Earnings Blowout (March 5, 2026)

Petrobras just crushed Q4 expectations across the board:

- Revenue: $23.61B vs. $22.22B consensus (6.26% beat)

- Net income tripled to R$15.6B ($2.96B) vs. Q4 2024

- Adjusted EBITDA: R$59.9B, up 46.3% YoY

- Free Cash Flow: R$19.3B ($3.7B) in Q4 alone

- Q4 Dividend: R$8.1B declared

The kicker: These results were achieved with Brent averaging $69/bbl in 2025. Now oil is above $100. Let that sink in.

2. Iran/Hormuz Oil Supply Crisis -- The Game Changer

This is the single biggest near-term catalyst in all of energy:

- Brent crude surged past $100/bbl, hitting an intraday high of $119.50

- WTI trading at $101.56 -- first time above $100 since Russia's Ukraine invasion in 2022

- Approximately 20% of global crude and natural gas supply suspended

- Iraq cut output by 60%, from ~4.3M bpd to 1.7-1.8M bpd

Why PBR Specifically Benefits: Petrobras has zero exposure to Middle East supply disruptions. As a non-OPEC producer operating exclusively in the Western Hemisphere, every dollar of the Brent spike flows straight to the bottom line. At $100+ Brent vs. the $69 average in 2025, Petrobras could see a 40-50%+ uplift in revenue per barrel if prices sustain.

3. Record Pre-Salt Production

- Total oil and gas production hit 3.0 million boed in 2025, up 11% YoY

- Buzios field broke 1 million bpd on October 29, 2025

- Tupi/Iracema field hit 1 million bpd on January 9, 2026

- New FPSO P-78 (180,000 bpd capacity) started production December 31, 2025

- P-79 in final commissioning for H1 2026

4. Dividend Machine

Petrobras is one of the highest-yielding large-cap stocks globally:

- 6.1-7.6% dividend yield

- R$41.2B total shareholder payout proposed for 2025

- Q4 2025 dividend payment date: March 27, 2026

- Next ex-dividend date expected: April 22, 2026

This is exactly why someone would sell covered calls on PBR: collect the option premium ($1.5M) PLUS the dividends (~7% yield on 1.1M shares = ~$1.4M/year), giving you a double income stream while maintaining equity exposure up to $22.

📅 Upcoming Catalyst Calendar

| Date | Event | Why It Matters |

|---|---|---|

| Mar 18, 2026 | Brazil Central Bank Selic Rate Decision | BRL impact; 25-50 bps cut expected |

| Mar 27, 2026 | Q4 2025 Dividend Payment | Cash hits accounts |

| Apr 16, 2026 | Annual General Meeting | Board elections, R$41.2B payout vote |

| Apr 22, 2026 | Next Dividend Ex-Date (expected) | Eligibility cutoff |

| H1 2026 | FPSO P-79 Commissioning | +180,000 bpd capacity |

| May/Jun 2026 | Q1 2026 Earnings | First quarter with $100+ oil -- massive beat potential |

| Oct 4, 2026 | Brazil Presidential Election | Lula vs. Bolsonaro -- potential regime change |

🎲 Price Targets & Probabilities

Bull Case: $20-$22 (10-21% upside)

Path to Get There:

- ✅ Brent sustains above $90-100/bbl through 2026

- ✅ Q1 2026 earnings massively beat the $0.35 EPS consensus on elevated oil prices

- ✅ FPSO P-79 commissioning adds production ahead of schedule

- ✅ Bolsonaro wins October election, triggering a governance re-rating

Supporting Evidence:

- Morgan Stanley just raised its price target to $20 from $17.50

- Gamma resistance at $20 (23.1B GEX) acts as a magnet, not a ceiling, if momentum sustains

- LEAPS implied upper range of $22.77 includes this target

- At $100+ Brent, PBR could see $5-7B in additional annual revenue

Probability: 35% -- Requires oil to stay elevated and/or political tailwinds

Base Case: $17-$19 (current range, ±5%)

What Keeps Us Here:

- Oil pulls back modestly to $80-90 as Iran tensions partially de-escalate

- PBR captures some but not all of the oil price benefit due to fuel pricing below international parity

- Strong earnings but political uncertainty caps the multiple

- Dividend yield supports the floor

Supporting Evidence:

- Massive gamma support at $18 (23.0B GEX) and $17 (21.1B GEX)

- Monthly OPEX implied range of $17.28-$19.26 centers on current price

- Analyst consensus average of $15.61 (before Morgan Stanley's upgrade) suggests current price already reflects good news

- Net bullish GEX bias means dips get bought aggressively

Probability: 45% -- The most likely outcome if oil normalizes somewhat

Bear Case: $14-$16 (12-23% downside)

Path to Get There:

- ❌ Iran conflict de-escalation crashes oil back to $58-70 range

- ❌ Lula administration increases fuel subsidies or redirects capital to political projects

- ❌ Brazil election uncertainty creates governance concerns

- ❌ Global recession depresses oil demand

- ❌ BRL weakness hurts ADR valuation

Supporting Evidence:

- Gamma support at $16 (15.1B GEX) and $15 (20.1B GEX) provides natural floors

- BTG Pactual and Goldman Sachs targets of $15 suggest downside risk if oil reverts

- The stock rallied 41% YTD largely on the oil spike -- if that unwinds, so does PBR

- Gross debt of $69.8B becomes a concern if cash flows compress

Probability: 20% -- Oil price reversal is the main trigger

💡 Trading Ideas

🛡️ Conservative: Mirror the Whale -- Covered Call Income Strategy

Setup:

- Own 100 shares of PBR at $18.18 ($1,818 investment)

- Sell 1 Mar 19, 2027 $22 Call for ~$1.36 credit ($136 per contract)

- Dividend Income: ~$1.27/share over the next year (~7% yield) = $127

- Total Income: $136 (premium) + $127 (dividends) = $263 per contract

- Income Yield on Position: 14.5% annualized

- Upside Cap: $22 (21% gain) + $2.63 premium/dividends = 35.5% total return potential

- Downside Protection: Premium + dividends reduce cost basis to $15.55 (14.5% cushion)

Why This Works:

- This is exactly what the $1.5M trader appears to be doing, scaled up 110x

- PBR's 6-7% dividend provides a baseline income stream

- The 21% OTM strike gives plenty of room for price appreciation before assignment

- Even if PBR drops to $16, you still pocket premium + dividends, reducing your loss

- The $18 and $17 gamma support levels provide strong natural floors

Risk Management:

- If PBR rallies past $22, you get called away but still earn 35.5% total return -- that's a great outcome

- If oil crashes and PBR drops below $15, the premium/dividends offset some pain but won't save you

- Consider rolling the call if PBR hits $20 and you want to extend the trade

Ideal For: Income-focused investors who want exposure to emerging market energy with enhanced yield

⚖️ Balanced: The "Iran Premium Fade" Put Spread

Setup:

- Buy 1 Jun 19, 2026 $17 Put for ~$1.20

- Sell 1 Jun 19, 2026 $14 Put for ~$0.40

- Net Debit: $0.80 per share ($80 per contract)

- Max Profit: $2.20 per share ($220 per contract) = 275% return

- Max Loss: $0.80 per share ($80 per contract)

- Breakeven: $16.20 (10.9% below current price)

Why This Works:

- If the Iran/Hormuz crisis de-escalates (ceasefire, diplomatic breakthrough), oil could drop 20-30% quickly

- Pre-war EIA forecast was $58/bbl for 2026 -- a massive gap from current $100+ levels

- PBR rallied 41% largely on the oil spike; a reversion could easily take it back to $14-16

- June expiration covers the Q1 earnings report and multiple geopolitical inflection points

- The $17 put strike aligns with the $17 gamma support -- if that level breaks, the selloff accelerates

Risk Management:

- Max loss capped at $80 per contract -- well-defined risk

- This is a hedge or a contrarian bet, not a core position

- If oil stays above $90, this trade expires worthless

- Consider sizing to 2-3% of portfolio max

Ideal For: Traders who think the oil spike is overdone and want a defined-risk way to play the reversal

🚀 Aggressive: The "Q1 Earnings Moonshot" Bull Call Spread

Setup:

- Buy 1 Jun 19, 2026 $19 Call for ~$1.50

- Sell 1 Jun 19, 2026 $22 Call for ~$0.60

- Net Debit: $0.90 per share ($90 per contract)

- Max Profit: $2.10 per share ($210 per contract) = 233% return

- Max Loss: $0.90 per share ($90 per contract)

- Breakeven: $19.90 (9.5% above current price)

Why This Works:

- Q1 2026 earnings (May/June) will be Petrobras's first full quarter with $100+ oil

- Consensus EPS of $0.35 was set when Brent was at $69 -- the actual number could be dramatically higher

- Every $10/bbl increase in Brent translates to approximately $5-7B in additional annual revenue

- Morgan Stanley's $20 target sits right in the profit zone

- Gamma analysis shows $20 as a major magnet with 23.1B GEX

Profit Scenarios:

- At $19.90: Break even

- At $20.50: Spread worth $1.50, profit $60 (67% return)

- At $22+: Spread worth $3.00, profit $210 (233% return)

Risk Management:

- Max loss capped at $90 per contract

- If oil drops below $80, close the position early to salvage remaining value

- Consider entering half the position now and adding if PBR clears $18.50 resistance

Ideal For: Bullish traders who believe $100+ oil will supercharge Q1 earnings beyond what the market expects

⚠️ Risk Factors

🛢️ Oil Price Reversal -- The Elephant in the Room

The single biggest risk to PBR right now: what if the Iran conflict ends?

- Pre-war Brent forecasts were $58-84/bbl for 2026. Current prices of $100+ include a massive geopolitical premium.

- Any ceasefire, diplomatic deal, or conflict de-escalation could send oil tumbling 20-30% in days.

- PBR's 41% YTD rally is heavily correlated to the oil spike. If oil reverts, so does PBR.

- The covered call seller may be hedging exactly this risk -- collecting $1.5M in premium as insurance against an oil price reversal.

Severity: HIGH. This is the dominant risk factor. Size your positions accordingly.

🏛️ Brazilian Political Risk

Petrobras is not a normal oil company. It is a tool of the Brazilian state.

- Government controls 64% of voting shares and uses Petrobras for national policy goals

- Fuel prices are set below international parity: diesel 64% cheaper, gasoline 27% cheaper than international benchmarks. This means Petrobras cannot fully capture the $100+ oil windfall domestically.

- New chairman Bruno Moretti is a Lula administration ally with limited energy operational expertise

- The $109B 5-year capex plan includes $13B in energy transition spending that may not generate competitive returns

- October 2026 presidential election: Lula vs. Flavio Bolsonaro is now a dead heat. Campaign season will inject volatility starting mid-year.

Silver Lining: A Bolsonaro victory could drive a 15-25% re-rating as markets price in more shareholder-friendly governance, fuel price parity, and higher dividends.

💱 Currency Risk (BRL/USD)

- BRL weakened past 5.26/USD in early March 2026

- Central Bank expected to cut Selic rate by 25-50 bps on March 18, potentially weakening the real further

- Petrobras earns revenue in USD-linked oil prices but reports in BRL and pays dividends in both currencies

- A weaker BRL actually benefits ADR holders short-term (more BRL per dollar of oil revenue) but creates translation uncertainty

🏭 Execution & Operational Risks

- FPSO P-79 commissioning delays could push back 2026 production targets

- Namibia Block 2613 regulatory approval uncertain after government procedural objections

- Refinery utilization target of 95% is ambitious

- Gross debt of $69.8B (62% leasing) could become a concern if oil reverts and cash flows compress

🎯 The Bottom Line

The Big Picture: This $1.5M LEAPS call sale is a textbook institutional income play on one of the cheapest, highest-yielding mega-cap energy stocks in the world. The trader is saying: "PBR at 5.5x forward P/E with a 7% dividend? I'll own the stock, sell calls 21% above current price, and collect premium + dividends for a combined 14-15% annualized income stream. If oil stays high and PBR runs to $22, I'll take my 35% total return and move on. If oil pulls back, the premium and dividends cushion the blow."

What We Know:

- PBR just posted record Q4 earnings with oil averaging $69. Now oil is above $100.

- Production hit 3.0M boed in 2025, up 11% YoY, with two more FPSOs coming online in 2026

- The stock trades at 5.5x forward P/E -- that is ludicrously cheap for this level of cash generation

- Morgan Stanley just raised its target to $20 (10% upside)

- Gamma analysis is decisively bullish with massive support at $18 and $17

The Catch:

- PBR is a state-controlled company. The government takes its cut through fuel subsidies, political capex, and governance influence.

- The oil spike could be temporary. If Iran de-escalates, the geopolitical premium evaporates.

- Brazil's presidential election in October adds significant uncertainty to the second half of the year.

The Play-by-Play:

If You Like Income: ✅ The covered call strategy is the star here. Own shares, sell $22 LEAPS calls, collect dividends. Total income potential of 14-15% annualized with 21% upside buffer before you get called away. The $18 gamma wall protects your downside. This is a sophisticated, risk-aware income play that works in most scenarios.

If You're Bullish on Oil: 📈 Q1 2026 earnings will be the next major catalyst. If Brent stays above $90, the $0.35 EPS consensus is laughably low. A bull call spread from $19 to $22 gives you 233% max return with defined risk.

If You're Cautious: ⚡ The 41% YTD rally and $100+ oil have pulled forward a lot of good news. A put spread from $17 to $14 is cheap insurance against an oil reversal, costing just $80 per contract.

Key Levels to Watch:

- $18.00 -- Gamma wall support. If this breaks, $17 is next.

- $18.50 -- Immediate resistance. Clearing this opens $19-20.

- $20.00 -- Morgan Stanley target and major gamma resistance. The prize for bulls.

- $22.00 -- The call strike. If PBR reaches this, the covered call trade caps out. Still a 35% total return.

⚖️ Disclaimer

This analysis is for educational and informational purposes only and should not be considered financial advice. Options trading carries substantial risk and is not suitable for all investors. The risk of loss in trading options can be significant, and you should carefully consider whether options trading is appropriate for your financial situation. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Specific Risks for PBR:

- Brazilian state-controlled company subject to political interference in pricing, capex, and dividends

- Oil price reversal from Iran conflict de-escalation could trigger sharp declines

- Emerging market currency risk (BRL/USD) adds an additional volatility layer

- Options strategies presented have defined risks but can result in total loss of premium paid

- LEAPS options carry additional risks including lower liquidity and wider bid-ask spreads

Data Sources: Trade data from proprietary options flow analysis. Company information from public filings and financial news sources. Gamma exposure calculated from aggregated options positioning data. Implied moves derived from at-the-money straddle pricing.

Analysis Date: March 9, 2026 PBR Stock Price: $18.18 Market Cap: $113.4 Billion Brent Crude: ~$108.75/bbl

Remember: This is a premium collection trade on an emerging market energy stock during a geopolitical oil shock. The math works in most scenarios, but "most" is not "all." Size your positions based on your risk tolerance, diversify across uncorrelated strategies, and always have an exit plan. 💪