⚡ PCG $2.5M Call Buy - Big Money Betting on Utility Comeback!

📅 February 12, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up on $2.5 MILLION worth of PG&E calls at the $20 strike! This is a major bullish bet on California's largest utility - trading at $17.53 today but down 20% since the January LA wildfires spooked investors. With PG&E just reporting solid Q4 earnings this morning (fourth straight year of double-digit EPS growth) and analysts pointing to 40%+ upside, smart money sees value in this beaten-down utility play.

📊 Company Overview

PG&E Corporation (PCG) is California's largest combined electric and gas utility serving Northern and Central California:

- 🏢 Market Cap: $37.58 Billion

- ⚡ Industry: Electric & Other Services Combined (Utilities)

- 💰 Current Price: $17.53

- 🏠 Headquarters: Oakland, California

- 👥 Customers Served: 5.3M electricity + 4.6M gas customers across 47 counties

- 📍 Exchange: NYSE

PG&E emerged from bankruptcy in 2020 following devastating wildfires in 2017-2018. Today, the company is executing a $73 billion infrastructure investment plan to modernize the grid and capture surging AI/data center electricity demand in its service territory.

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (February 12, 2026 @ 10:54:35):

| Option Symbol | Time | Side | Buy/Sell | Type | Expiration | Strike | Volume | Premium | OI Change | Z-Score | Vol/OI | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PCG20261218C20 | 10:54:35 | BTO | BUY | CALL | 2026-12-18 | $20 | 20,000 | $2.5M | - | 0 | 0.95 | Single Leg CALL |

🤓 What This Actually Means

This is a straightforward bullish bet on PG&E stock rallying to $20+ by December! Here's the breakdown:

- 💸 Massive premium paid: $2.5M for 20,000 call contracts

- 🎯 Strike price: $20 (14% above current $17.53 price)

- ⏰ Time to expiration: 10 months (December 18, 2026)

- 📊 Average cost per contract: ~$1.25 ($125 per contract)

- 🎰 Breakeven at expiration: $21.25 (21% upside required)

- 📈 HIGH_ACTIVITY signal: Volume/OI ratio of 0.95 shows aggressive new positioning

Translation for regular folks: This trader is betting that PG&E will climb from $17.53 to at least $20 (14% gain) by year-end. With analysts targeting $20.82-$21.45 and some seeing the stock as high as $26, this bet aligns with Wall Street's bullish consensus. The 10-month timeframe gives plenty of runway for wildfire fund reform legislation and data center growth to play out.

Why this matters: The timing is notable - this trade came on earnings day after PG&E reported solid results and raised 2026 guidance. Someone's not waiting for the dust to settle; they're loading up while the stock is still down 20% from January highs.

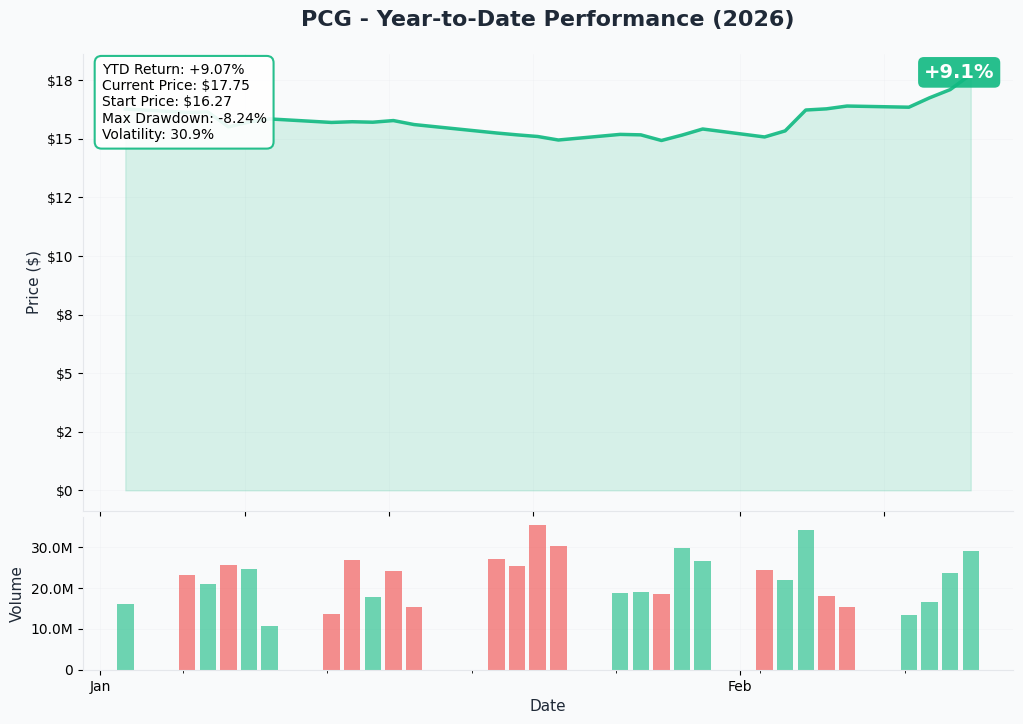

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

PG&E is trading at $17.53, down approximately 20-22% YTD since the Los Angeles wildfires erupted on January 7, 2026. Despite no direct exposure to the LA fires (PG&E serves Northern California, not Southern California), the stock sold off hard on fears about the shared $21 billion California wildfire insurance fund.

Key observations:

- 📉 Sell-off overdone? Stock punished for fires in competitor's territory

- 💹 52-week range: $12.97 - $17.95 (trading near upper end)

- 📊 1-year performance: Still up +6.67% vs year ago

- 🎯 Valuation gap: Trading below 10x 2026 earnings vs 15x+ for peer utilities

Note: Gamma exposure and implied move charts are not available for this analysis.

🎪 Catalysts

🔥 Just Happened Today!

Q4 2025 Earnings Released (February 12, 2026)

PG&E reported results this morning - the same day as this massive call buy:

- 📊 Q4 EPS: $0.36 vs $0.37 expected (slightly below consensus)

- 💰 Q4 Revenue: $6.8B vs $7.1B expected

- 📈 Full-year 2025 Core EPS: $1.50 - up 10% YoY and fourth consecutive year of double-digit growth

- 🎯 2026 Guidance RAISED: Core EPS now $1.64-$1.66 (10% growth expected)

- ✅ Wildfire ignitions down 43% in 2025 - three years without major equipment-caused fire

- 💸 Fourth rate reduction in two years - bundled residential rates 11% below January 2024

🚀 Upcoming Catalysts (Next 6 Months)

$73 Billion Infrastructure Plan

- Largest capital commitment in company history

- Supports up to 10 GW of new data center load anticipated over next decade

- 307 miles of powerline undergrounding in high-risk areas by 2027

- Infrastructure for 3 million EVs by 2030

Data Center Demand Pipeline

- 10 GW total pipeline - up from 5.5 GW in February 2025

- 17 data center projects (1.5 GW) in final engineering phase

- First connections projected 2026-2030

- For every 1 GW of new demand, PG&E customers may save 1-2% on monthly bills

Wildfire Fund Reform - THE KEY CATALYST

- SB 254 established $18B Wildfire Fund Continuation Account

- PG&E's contribution share reduced from 64% to 47.85% under new legislation

- Wide-ranging wildfire policy reform expected in 2026 legislative session

- Resolution of AB 1054 reform is the single most material catalyst for rerating

Q1 2026 Earnings

- Expected late April/early May 2026

- Watch for data center connection progress and wildfire mitigation spend

2027 General Rate Case

- Filed May 2025, CPUC decision expected late 2026/early 2027

- Rate changes effective January 2027 at earliest

Dividend Growth

- Current: $0.20 annually ($0.05/quarter)

- Target: 20% payout ratio by 2028 (up from 7% in 2025)

- Projected 2028 annual dividend: ~$0.328/share

🎲 Price Targets & Probabilities

📈 Bull Case (35% probability)

Target: $22-$26

How we get there:

- 🏛️ California legislature passes comprehensive wildfire fund reform in 2026

- ⚡ Data center demand materializes faster than expected (AI boom continues)

- 📊 PG&E executes on $73B infrastructure plan without major hiccups

- 🔥 Another year without major equipment-caused fire validates safety improvements

- 📈 Multiple expands from below 10x to 12-13x earnings (still discount to peers)

- 🎯 Analyst high target of $26 from TipRanks becomes realistic

What the option buyer needs: Stock at $20+ by December 2026 to profit. If PCG hits analyst consensus of $21+, this trade makes ~$1.50-$2.50/contract profit ($3M-$5M total).

🎯 Base Case (45% probability)

Target: $18-$21

Most likely scenario:

- ✅ Solid earnings execution continues (9%+ annual EPS growth maintained)

- ⏳ Wildfire fund reform progresses but takes time (legislative process is slow)

- 📊 Data center connections begin ramping in late 2026

- 🔄 Valuation gap narrows modestly as wildfire fears fade

- 💹 Stock grinds higher to analyst consensus range of $20.82-$21.45

This is the sweet spot for the trade: At $20-$21, the calls are in-the-money and the trader profits nicely. At $18-$19, they're underwater but still have time value.

📉 Bear Case (20% probability)

Target: $14-$17

What could go wrong:

- 🔥 Major California wildfire (anywhere in state) triggers fund concerns

- 📉 CPUC reduces allowed return on equity (already proposed 35 basis point cut)

- ⚖️ 2026-2028 Wildfire Mitigation Plan fails to resolve 12 critical issues

- 💸 Interest rates stay higher for longer, increasing infrastructure financing costs

- 🤖 Data center demand growth slows on AI hype cooldown

- 📊 Stock retests $15 support from earlier in 52-week range

Max loss for option buyer: $2.5M (full premium) if stock stays below $20 at December expiration.

💡 Trading Ideas

🛡️ Conservative: Wait for Pullback Entry

Play: Buy PCG stock on any pullback to $16-$17 range

Why this works:

- 📊 Current price ($17.53) already reflects significant pessimism

- 🎯 Analyst consensus of $21+ implies 20%+ upside

- 💰 Dividend provides income while waiting (1.1% yield, growing)

- ⚡ Exposure to AI/data center electricity demand theme

- 🛡️ Regulated utility provides defensive characteristics

Entry: $16-$17 on pullback Stop-loss: $14.50 (52-week low area) Target: $20-$22 over 12 months Position size: Small (2-3% of portfolio given regulatory/wildfire risks)

Risk level: Low-Moderate | Skill level: Beginner-friendly

⚖️ Balanced: Covered Call Strategy

Play: Buy 100 shares PCG + Sell June 2026 $20 call

Structure:

- Buy 100 shares at $17.53 = $1,753

- Sell PCG June 2026 $20 Call for ~$0.50-$0.70 credit

Why this works:

- 💰 Collect premium while waiting for stock to appreciate

- 🎯 Cap your gains at $20 but that's still 14%+ profit

- 🛡️ Premium reduces cost basis by 3-4%

- ⏰ 4-month holding period aligns with Q1 earnings catalyst

Estimated P&L:

- 📈 Stock at $20+: ~$3.00-$3.20 profit ($250-$320 per 100 shares)

- 🎯 Stock at $18-$19: ~$0.50-$2.00 profit (premium + modest appreciation)

- 📉 Stock at $16-$17: ~breakeven to small loss (premium offsets decline)

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Follow the Flow (Leap Calls)

Play: Buy December 2026 $20 calls similar to the institutional trade

Structure: Buy PCG December 18, 2026 $20 Calls

Why this works:

- 🐋 Following $2.5M institutional flow - smart money sees value

- ⏰ 10 months for wildfire reform catalyst to play out

- 📈 Leverage gains if stock rallies to analyst targets

- 💰 Defined risk (can only lose premium paid)

Estimated cost: ~$1.00-$1.50 per contract ($100-$150 for 1 contract)

Scenarios:

- 📈 PCG at $22: ~$1.00 profit per contract (100% gain)

- 🎯 PCG at $20: Breakeven to small loss

- 📉 PCG below $20: Lose premium paid

Risk level: High | Skill level: Intermediate-Advanced

⚠️ Important: Options can expire worthless. Only risk capital you can afford to lose.

⚠️ Risk Factors

Don't ignore these potential landmines:

-

🔥 Wildfire fund uncertainty remains: The $21 billion California wildfire fund lacks replenishment mechanism. If Southern California Edison faces major Eaton fire liability, it could strain the shared fund and impact all California utilities including PG&E.

-

📉 Stock down 20% on contagion fears: PG&E had no exposure to the January LA fires (wrong service territory), but investors sold first and asked questions later. This sentiment-driven selling could continue if wildfire headlines persist.

-

⚖️ Regulatory pressure on returns: CPUC proposed 35 basis point reduction in allowed return on equity. Regulatory environment described as "volatile" which creates uncertainty for long-term earnings power.

-

💸 $73B capital plan execution risk: This is the largest capital commitment in company history and represents significant credit and execution risk. Data center demand projections may not fully materialize.

-

🌡️ Climate change intensifies wildfire risk: 45% increase in climate-related risk noted in 2025 Wildfire Mitigation Plan. Despite improved prevention (43% ignition reduction), climate trends work against the company.

-

📜 Bankruptcy history: PG&E emerged from bankruptcy in 2020 after $30 billion in wildfire liabilities from 2017-2018 fires. While operational improvements are real, the ghost of past failures looms.

-

💰 Option premium at risk: This $2.5M call position needs PCG above $21.25 at December expiration to profit. If stock stays flat or declines, the entire premium is lost.

🎯 The Bottom Line

Real talk: A $2.5M bet on PG&E calls landed today - right on earnings day. This isn't your neighbor Bob's Robinhood account; this is institutional money making a calculated bet that California's largest utility is oversold after the LA wildfire scare.

The bull thesis is straightforward:

- 📉 Stock down 20% on fears about fires in someone else's service territory

- 💰 Trading below 10x earnings vs 15x+ for peer utilities

- 🎯 Analyst consensus of $21+ implies 40%+ upside

- ⚡ Positioned to capture AI/data center electricity demand boom

- 📈 Fourth straight year of double-digit EPS growth, guidance raised again today

The bear thesis is legitimate:

- 🔥 California wildfire risk never goes away

- 📜 Regulatory environment remains challenging

- 💸 $73B capital plan is execution-heavy

- ⚖️ Wildfire fund reform is political, timing uncertain

Who should consider PCG:

- ✅ Value investors looking for beaten-down utilities at discount valuations

- ✅ Income seekers (dividend growing toward 20% payout ratio by 2028)

- ✅ AI theme players wanting electricity demand exposure without mega-cap tech valuations

- ❌ Risk-averse investors who can't stomach headline volatility from California wildfires

Key dates to mark:

- 📅 Late April/May 2026 - Q1 2026 earnings

- 📅 Throughout 2026 - California legislative session (wildfire fund reform)

- 📅 Late 2026 - 2027 General Rate Case decision expected

- 📅 December 18, 2026 - Expiration date for this $2.5M call trade

Bottom line: PG&E is a value play on California utility reform and AI-driven electricity demand. The 20% selloff created an opportunity that institutional money is now betting on. At below 10x earnings with 40%+ analyst upside targets, the risk/reward looks favorable - but you need conviction that wildfire headlines won't derail the thesis. This $2.5M call buy is a vote of confidence that the worst is behind PG&E.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. PG&E has significant regulatory and wildfire-related risks that could result in material losses. Always do your own research and consider consulting a licensed financial advisor before trading.

About PG&E Corporation: PG&E is California's largest combined electric and gas utility with a $37.58 billion market cap, serving approximately 5.3 million electricity customers and 4.6 million gas customers across 47 counties in Northern and Central California.