💎 PDD $5.1M Mixed Signal - LEAPS Calls Meet Protective Puts! 🎭

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Two massive institutional trades totaling $5.1 MILLION hit PDD today with completely opposite vibes! First, someone dropped $4M on June 2027 LEAPS calls betting big on the Chinese e-commerce giant's recovery, then just an hour later, a second player grabbed $1.1M in May 2026 puts with an EXTREMELY UNUSUAL z-score of 20.72. Translation: Smart money is making long-term bullish bets while simultaneously hedging near-term geopolitical and regulatory risks. This is the ultimate "hope for the best, prepare for the worst" trade setup!

📊 Company Overview

PDD Holdings (PDD) is the powerhouse behind both Pinduoduo (China's innovative social commerce platform) and Temu (the global discount e-commerce disruptor):

- Market Cap: $158.9 Billion (dominant player in global e-commerce)

- Industry: Online Retail & E-commerce Platforms

- Current Price: $112.22 (down from 52-week high of $139.41)

- Primary Business: Operates commerce platforms across 80+ countries, running Pinduoduo in China and Temu worldwide, plus community group purchasing

💰 The Option Flow Breakdown

The Tape (December 23, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Z-Score | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:24:39 | PDD | ASK | BUY | CALL $120 | 2027-06-17 | $4M | $120 | 2,000 | - | 1.95 | LEAPS |

| 12:28:39 | PDD | ASK | BUY | PUT $105 | 2026-05-15 | $1.1M | $105 | 2,000 | - | 20.72 | Long Put |

TOTAL PREMIUM: $5.1M

🤓 What This Actually Means

This is a SPLIT PERSONALITY setup revealing institutional uncertainty! Here's the story:

Trade 1 - The Optimist ($4M LEAPS Calls):

- 💸 Massive long-term bet: $4M premium ($200 per contract × 2,000 contracts) for 541 DAYS to expiration

- 🚀 Bullish strike: $120 is only 6.9% above current $112.22 - not crazy optimistic but solid upside target

- ⏰ Patient capital: June 2027 expiration shows conviction in multi-year recovery story

- 📊 Size matters: 2,000 LEAPS represents $24M+ notional exposure (200,000 shares controlled)

- 🎯 Strategy: This is a leveraged long-term bet on PDD's ability to navigate regulatory challenges, grow Temu globally, and return to growth

Trade 2 - The Pessimist ($1.1M Protective Puts):

- 🛡️ Insurance policy: $1.1M premium ($55 per contract × 2,000 contracts) for DOWNSIDE protection

- 😰 Defensive strike: $105 provides 6.4% cushion below current price - protecting against regulatory/geopolitical shocks

- ⏰ Near-term hedge: 143 days to May 2026 captures Q4 2025 earnings (March 23), regulatory developments, and trade policy evolution

- 🔥 EXTREME unusual score: Z-score of 20.72 means this happens VERY RARELY - maybe a few times per year, signaling serious institutional concern

- 📊 Different player: Almost certainly NOT the same trader as the LEAPS buyer - this is genuine two-sided institutional positioning

What's really happening here: The LEAPS buyer believes PDD's long-term fundamentals (Temu's 1B+ downloads, $59.5B cash fortress, OpenAI-level AI capabilities) will drive stock back toward $120+ by mid-2027 as regulatory overhang fades and international expansion matures. Meanwhile, the put buyer sees significant near-term downside risk from the December 2025 regulatory altercation with Chinese officials, ongoing US-China trade tensions (145% tariffs), and Temu's plunging US market share following de minimis elimination. Both can be right on different time horizons!

Unusual Scores Decoded:

- 🔥 LEAPS Calls: 1.95 z-score = "Above Average" unusual activity (bigger than ~97% of recent trades)

- 💥 Puts: 20.72 z-score = "EXTREMELY UNUSUAL" (bigger than 99.99%+ of trades - this is off-the-charts rare!)

The put trade's extreme unusualness suggests either: (1) A massive institution hedging concentrated long position, (2) Inside knowledge of upcoming regulatory announcement, or (3) Portfolio manager terrified of the SAMR altercation blowing up into full investigation.

📈 Technical Setup / Chart Check-Up

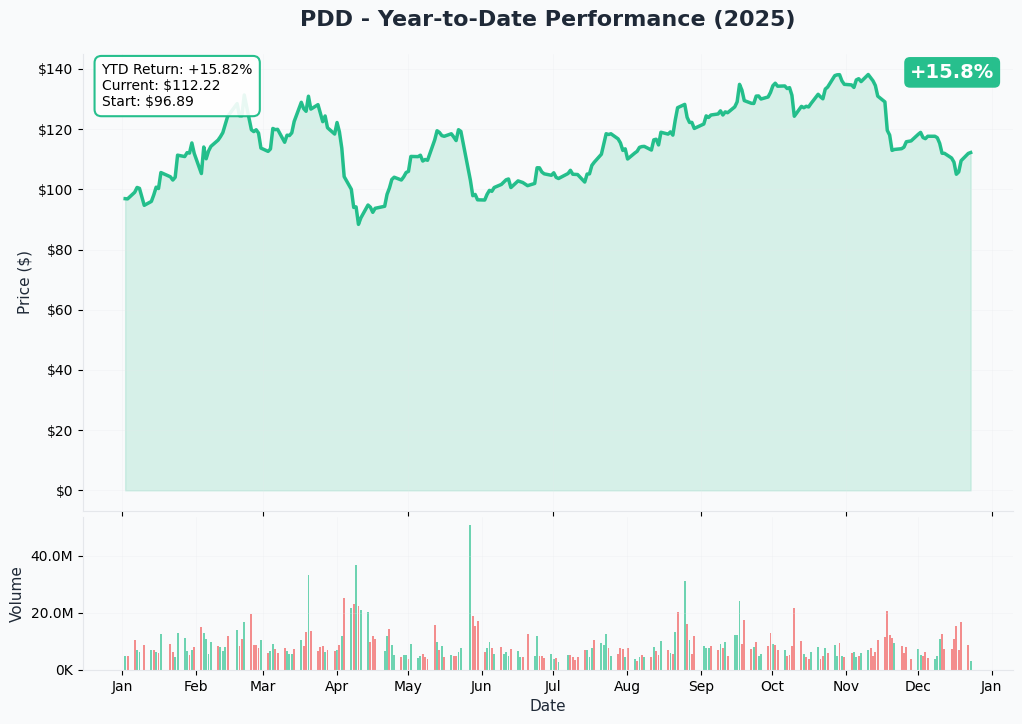

YTD Performance Chart

PDD tells a story of extremes - up 37.9% YTD from $81.35 starting price to current $112.22, but MASSIVELY underperforming Alibaba's +113.6% rally. The chart reveals a brutal journey: the stock rocketed to a 52-week high of $139.41 on strong Temu growth momentum and AI investment optimism, only to crash 19% in the past 3 months on a toxic combination of Q3 earnings miss (revenue growth decelerated to just 9% YoY), the shocking physical altercation with Chinese regulators in December, and mounting European regulatory scrutiny.

Key observations:

- 🎢 High volatility: The stock has swung between $87.11 lows and $139.41 highs (60% range!) - this isn't a stable blue chip

- 📉 Recent weakness: December has been brutal with only 8 green days out of 30 (27% win rate) and 7.56% volatility

- 💪 Still positive YTD: Despite recent selloff, up 37.9% shows underlying fundamental strength from Temu expansion and domestic resilience

- ⚠️ Momentum broken: Failed to hold $120+ level after earnings disappointment - now trading below both moving averages

- 🔄 Consolidation zone: Range-bound between $105-$120 for weeks as market digests bad news and awaits catalysts

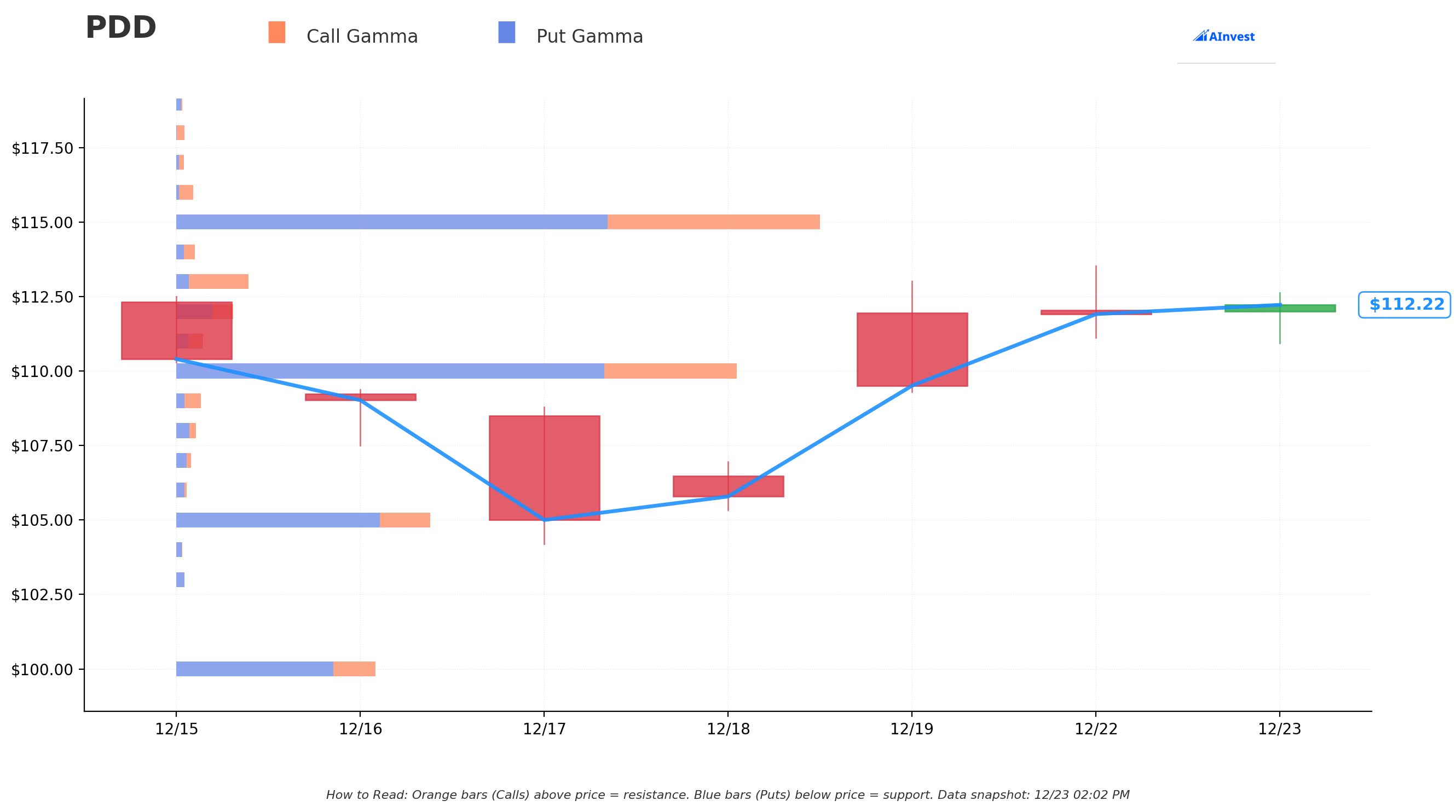

Gamma-Based Support & Resistance Analysis

Current Price: $112.22

The gamma exposure map reveals massive put wall protection below and limited upside resistance - interesting asymmetry:

🔵 Support Levels (Put Gamma Below Price):

- $103 - MASSIVE PUT WALL and HVL (High Volatility Level) with the strongest concentration - this is THE FLOOR dealers will defend aggressively

- $105 - Secondary support zone (EXACTLY where the put buyer struck! Not coincidental) - deep gamma support

- $102 - Third support layer with solid put positioning

- $99 - Extended downside floor

- $98 - Disaster scenario support

🟠 Resistance Levels (Call Gamma Above Price):

- $114 - CALL WALL just above current price - immediate ceiling (only 1.6% overhead!)

- Limited gamma concentration above $114 shows market NOT expecting strong upside breakout near-term

What this means for traders: PDD is trading in a tight range between immediate $114 resistance and strong $103-105 support complex. The gamma data shows HEAVY institutional positioning defending the downside (massive put walls at $103-105) but limited conviction on upside (thin call gamma above $114). This creates a "trapped" setup where the stock wants to consolidate before the next major catalyst.

Notice the put strike? The $105 strike sits EXACTLY at secondary gamma support - the put buyer positioned just above the major $103 floor, expecting that if PDD breaks $105, it could flush quickly to $99-103 on regulatory headlines. Smart defensive positioning.

Net GEX Bias: Bearish - Negative net gamma at ALL key levels suggests market makers are positioned for downside, which typically creates increased volatility on selloffs as dealers sell into weakness rather than stabilize price.

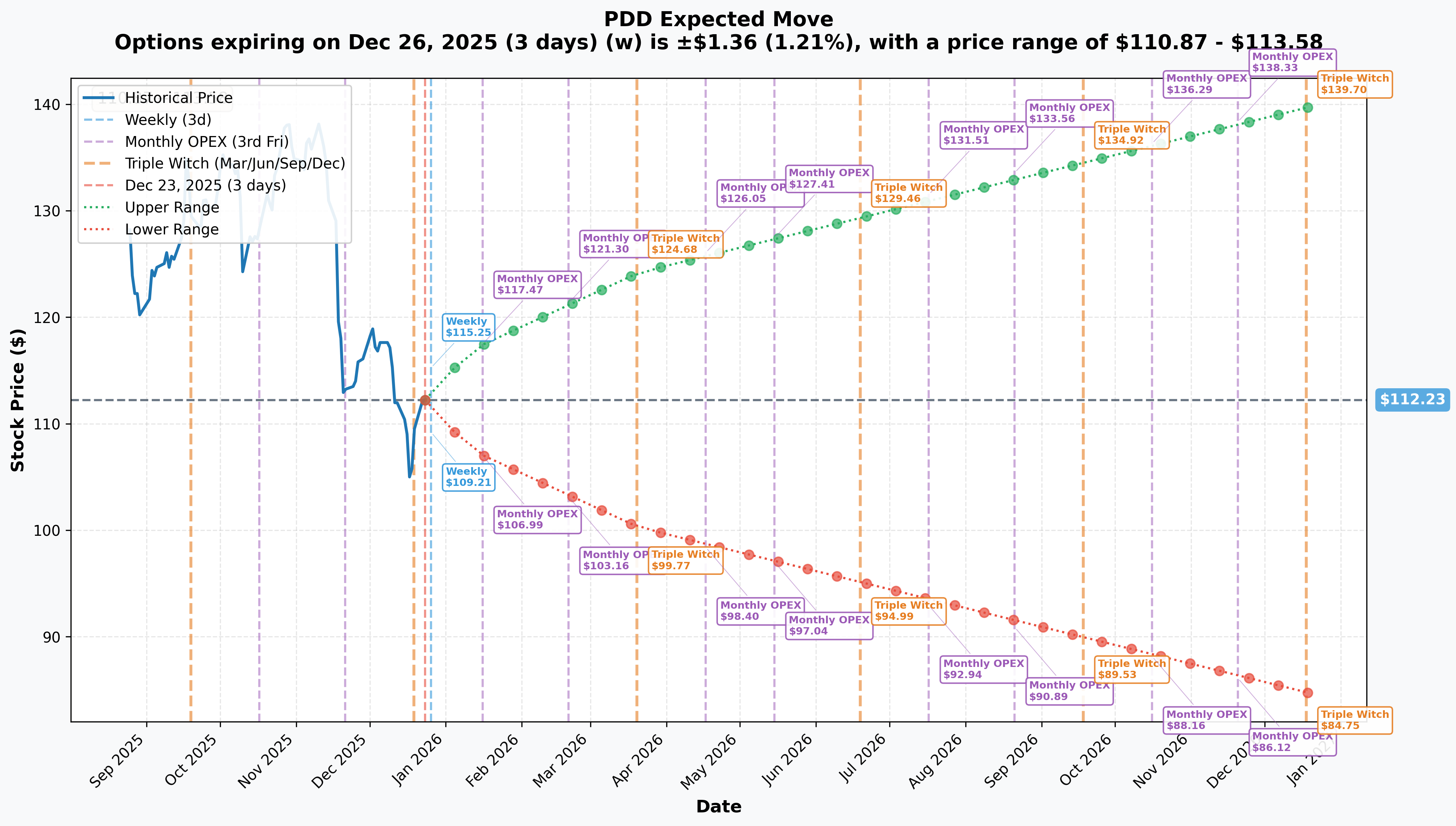

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±$1.36 (±1.21%) → Range: $110.87 - $113.58

- 📅 Monthly OPEX (Jan 16 - 24 days): ±$5.24 (±4.67%) → Range: $106.99 - $117.47

- 📅 Quarterly Triple Witch (Mar 20 - 87 days - NEAR EARNINGS!): ±$11.94 (±10.64%) → Range: $100.28 - $124.17

Translation for regular folks: Options traders are pricing in a tiny 1.2% move ($1.36) through year-end - basically dead money during holiday season. But expectations EXPLODE for the January-March period with a 10.64% implied move ($11.94) through March 20th, which INCLUDES the critical Q4 2025 earnings on March 23, 2026. The market expects FIREWORKS around earnings - a huge swing either direction as PDD reports results showing impact of regulatory troubles and RMB 100B merchant support program.

The $105 put expiring May 15th sits at the lower end of the March quarterly range ($100.28 low), suggesting the put buyer believes there's real risk PDD could test $100-105 if Q4 earnings disappoint or if a formal SAMR investigation gets announced.

Key insight: The low near-term IV (1.2% weekly) with explosive mid-term IV (10.6% quarterly) creates an ideal environment for the $120 LEAPS call buyer - they're paying relatively low premiums during consolidation phase, betting that PDD survives near-term volatility and resumes growth trajectory by 2027.

🎪 Catalysts

🔥 Past Catalysts (Already Happened - Setting The Stage)

Q3 2025 Earnings Disaster - November 18, 2025 💔

PDD's Q3 report was a massive disappointment that triggered the current selloff:

- 📊 Revenue miss: RMB 108.28B ($15.21B) vs consensus RMB 145.2B - came in 25% BELOW estimates!

- 📉 Growth deceleration: Revenue up just 9% YoY vs 44% in Q3 2024 - dramatic slowdown

- 💔 EPS miss: RMB 19.70 ($2.77) vs consensus RMB 23.50

- 📊 Margin compression: Operating margin fell from 27% to 23.1% due to RMB 100B merchant support program

- 🚨 Management warning: No specific guidance provided, warned that Q3 profitability "should not be used as indicator for future quarters"

- 💸 Stock reaction: Down 4.18% in premarket and continued selling through December

Why this matters now: The market is STILL digesting this earnings shock. The growth deceleration from 44% to 9% raises existential questions about whether the RMB 100B merchant investment is destroying value or building long-term moats. This explains why institutions are buying LONG-dated calls (betting on recovery) while hedging with near-term puts (protecting against further deterioration).

Physical Altercation with Chinese Regulators - December 3-17, 2025 🚨

The most explosive negative catalyst of Q4 2025 - PDD employees physically confronted Shanghai market regulators:

- 🥊 The incident: State Administration for Market Regulation (SAMR) officials conducting inspection when situation escalated into FISTFIGHT requiring police intervention

- 💼 Corporate response: PDD dismissed multiple employees including director of compliance, several faced administrative detention

- 📉 Stock impact: Shares fell 6.48% on December 10 amid rumors before official confirmation

- ⚠️ Regulatory risk escalation: This is "highly unlikely to endear PDD to the powerful regulator, which has the ability to instigate sweeping probes into the company's business practices" per Caixin Global

Why this is HUGE: In China's regulatory environment, physically attacking government officials is corporate suicide. SAMR has unlimited authority to launch investigations into PDD's merchant practices, pricing, data handling, VIE structure, etc. The 20.72 z-score on the put trade likely reflects institutional terror about this incident's consequences. When was the last time a major Chinese tech company's employees FOUGHT regulators? This is unprecedented.

Arizona Attorney General Lawsuit - December 1, 2025 ⚖️

Arizona AG Kris Mayes sued Temu for alleged consumer data theft and selling counterfeit brands:

- 📋 First major US state-level legal action against Temu

- 💰 Could result in significant fines and operational restrictions in US

- 🎯 Represents "the biggest fresh overhang on PDD's ADRs in December 2025" per analyst reports

- 🇺🇸 Opens door for other states to file similar lawsuits (copycat risk)

European Regulatory Raids - December 9, 2025 🇪🇺

European competition watchdogs raided Temu's Dublin headquarters amid suspicions of unfair subsidies from Beijing:

- 🔍 Dublin raid: EU investigating potential state aid violations

- 🇩🇪 Germany investigation: Federal Cartel Office launched probe into merchant pricing practices in October 2025

- ⚠️ Consumer protection: EU found several Temu sales tactics breached consumer protection rules

- 💰 Potential impact: Fines could range €10-50M, operational changes could increase costs 5-10%

Elimination of US De Minimis Exemption - February 2025 🇺🇸

Trump's executive orders eliminated duty-free exemption for packages under $800:

- 💔 Temu's US users plummeted: Daily active users dropped 58% in May 2025 following implementation

- 🏭 Business model disruption: Temu's entire competitive advantage (cheap direct-from-China shipping) eliminated overnight

- 📊 Goldman Sachs warning: "PDD's Temu has the highest US exposure amongst China cross-border players" and will "bear a portion of the extra tariff/tax cost burden"

- 🔄 Strategic pivot: Temu announced cessation of direct China shipments, pivoting to local warehouse fulfillment model (higher costs)

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings - March 23, 2026 (90 DAYS!) 📊

The make-or-break catalyst that will determine if PDD is a turnaround story or deteriorating asset:

- 📅 Date: March 23, 2026 after market close

- 💰 Consensus EPS: $2.93

- 🎯 Key metrics to watch:

- Revenue growth trajectory (Q3 was 9% YoY - will it stabilize or continue decelerating?)

- Operating margin performance (Q3 was 23.1% down from 27% - is merchant program paying off yet?)

- Temu international metrics (GMV, user growth in Europe/Latin America post-US struggles)

- Management commentary on SAMR relationship status and investigation risk

- Cash deployment strategy with $59.5B cash fortress

- 2026 profitability expectations and merchant program ROI timeline

Upside surprise potential: If RMB 100B merchant support program shows early success (GMV acceleration, merchant retention), margins could stabilize faster than expected. Temu's pivot to local fulfillment could be progressing ahead of schedule in Europe/Latin America. Any positive commentary on SAMR relationship normalization would be massive relief.

Downside risk factors: Further growth deceleration (revenue growth below 8%), margin compression continuing (below 22%), weak Q1 2026 guidance, formal SAMR investigation announcement, or conservative cash return commentary could trigger 15-25% selloff given damaged sentiment.

This earnings report expires AFTER the $105 put May expiration but WELL BEFORE the $120 LEAPS call June 2027 expiration - showing how the two trades have different time horizons and catalyst dependencies.

Potential SAMR Investigation Announcement - Q1 2026 (High Probability) ⚠️

Following the December fistfight incident, there's elevated risk of formal investigation:

- 🎯 Probability: 60% chance of formal SAMR investigation announcement in Q1-Q2 2026 per analyst estimates

- 📉 Stock impact: Investigation announcement could trigger 15-25% decline as market prices in regulatory uncertainty

- 🔍 Scope risk: SAMR has broad authority over merchant practices, pricing, data handling, VIE structure compliance

- ⏰ Timeline: Chinese regulatory investigations can last 6-18 months with unpredictable outcomes

- 💰 Financial risk: Fines could range from RMB 500M to several billion depending on findings

This is THE catalyst the $105 put buyer is hedging against! If SAMR announces investigation in Q1 2026, stock could gap down 15-20% overnight to the $95-105 range, making those puts massively profitable.

US-China Trade Policy Evolution - Ongoing Through 2026 🇺🇸🇨🇳

Trade tensions remain PDD's biggest external risk:

- 🚨 Current status: US imposed 145% tariffs on Chinese goods; China retaliated with 125% tariffs

- 📊 Temu impact: Already eliminated de minimis exemption causing 58% US user decline

- 🎯 Further escalation risk: Trump administration could impose additional sector-specific penalties on Chinese e-commerce

- 📉 Analyst estimates: Temu's US sales could decline 20-40% if tariff pressures persist without successful mitigation

- 🔄 Mitigation progress: Temu's local warehouse strategy execution will be critical - early signs of success could be positive catalyst

Probability: 90%+ likelihood of continued restrictive trade environment through 2026 regardless of election outcomes. The de minimis ship has sailed - not coming back.

EU Customs Fee Implementation - H1 2026 (70% Probability) 🇪🇺

The EU has proposed flat 2-euro customs fee on small parcels:

- 💰 Impact: Could reduce Temu's gross margins in Europe by 3-5 percentage points

- 📅 Timeline: Likely implementation in H1 2026 (possibly as early as March-April)

- 🌍 Market significance: Europe is Temu's fastest-growing profitable region with $1.7B revenue in 2024 (+171% YoY) and projections to exceed $15B GMV in 2025

- ⚖️ Competitive impact: Levels playing field vs local European retailers, reduces Temu's price advantage

Shopify Partnership Expansion - Ongoing Q1 2026 🤝

Temu launched Shopify app December 19, 2025 enabling merchants to list products directly:

- 🎯 Strategy shift: Moving from direct-from-China model to marketplace aggregator (like Amazon)

- 🌐 Merchant acquisition: Access to Shopify's millions of merchants expands supplier base dramatically

- 💡 Business model evolution: Higher-margin marketplace fees vs low-margin direct shipping

- 📈 Growth catalyst: Could accelerate Temu GMV while improving unit economics

- ⏰ Timeline: Partnership just launched - Q1 2026 metrics will show early traction

This is a MAJOR strategic pivot that could mitigate tariff/customs headwinds. If successful, it validates the $120 LEAPS call thesis that PDD can adapt and thrive despite regulatory challenges.

Temu Market Share Battle vs Shein - Ongoing 2026 🥊

Competitive dynamics could shift significantly:

- 📊 Current position: Temu extended lead over Shein with almost triple observed US sales by late 2025

- 🎯 Market penetration: Children's clothing (Temu 17% vs Shein 20%), Adult clothing (Shein leads with 50%+ share)

- 🚀 Catalyst potential: Continued share gains could offset regulatory headwinds and demonstrate business model resilience

- ⚠️ Risk: Shein fighting back aggressively with dueling lawsuits in London High Court (trial expected late 2026)

💡 Speculative/Rumored Events

Potential Dividend or Buyback Program - H2 2026 (30% Probability) 💰

With $59.5B cash and minimal debt, PDD has massive financial flexibility:

- 💵 Cash fortress: RMB 423.8B ($59.5B) vs RMB 11.3B debt

- 🎯 Catalyst potential: First-ever dividend or substantial buyback could re-rate stock by 10-15%

- ⏰ Probability: Only 30% in 2026 (PDD historically reinvests all cash in growth)

- 🤔 Trigger: If regulatory environment stabilizes and management sees limited M&A opportunities, capital return becomes more likely

Strategic Western Partnership - 2026 (25% Probability) 🤝

Reports suggest PDD exploring alliances with major Western retailers:

- 🎯 Speculation: Potential partnership with Amazon, Walmart, or Target to leverage their logistics networks

- 💡 Strategic logic: De-risks Temu's international expansion by accessing established infrastructure

- 🌐 Geographic targets: Focus on Latin America, Southeast Asia where Temu gaining traction

- 📊 Impact: Could significantly accelerate international GMV while reducing capital intensity

- ⚠️ Barriers: US-China tensions make major partnerships politically risky for American retailers

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timeline, and these two contrasting option trades, here are the scenarios through the different time horizons:

📈 Bull Case - $130-145 by June 2027 (35% probability)

Target for the $120 LEAPS Call trade

How we get there:

- ✅ SAMR investigation avoided or resolved favorably - The December incident doesn't escalate into formal probe, or investigation concludes with manageable fine

- 🚀 RMB 100B merchant program vindicated - Q4 and Q1 2026 earnings show GMV re-acceleration above 15% YoY, proving ecosystem investments are working

- 🌍 International expansion delivers - Temu European GMV exceeds $20B in 2026, Latin America hits $5B+, demonstrating diversification away from China

- 🤝 Shopify partnership succeeds - Merchant marketplace model gains traction, improving margins and reducing regulatory exposure

- 💰 Capital allocation catalyst - Management announces $5-10B buyback program or inaugural dividend, signaling confidence

- 🇺🇸 Trade tensions stabilize - No further tariff escalation, local warehouse strategy proves viable

- 📊 Valuation re-rating - Forward P/E expands from 11.63x toward peer average 15-17x as growth stabilizes at 20%+ and regulatory risks fade

- 🎯 AI capabilities monetization - PDD's $0.50B Q2 2025 R&D investment in AI-powered recommendations and supply chain optimization drives margin expansion

Path to $130-145:

- March 2026 earnings: Beat on revenue ($9B+ vs est), margins stabilize at 24%+, stock rallies to $120-125

- Mid-2026: Positive Shopify partnership metrics, Temu European expansion accelerating, stock consolidates $120-130

- Q3 2026: Revenue growth re-accelerates to 15-18% YoY, regulatory overhang fading, breakout to $135-140

- Early 2027: Potential dividend/buyback announcement, analyst target raises to $150+, stock approaches $140-145

- June 2027: Trading at $130-145 range, LEAPS calls worth $10-25 per contract

LEAPS Call P&L in Bull Case:

- Stock at $130: Calls worth $10.00, profit = $(-190)/share × 2,000 = -$380K loss (breakeven ~$140 due to $200 premium paid)

- Stock at $140: Calls worth $20.00, profit = $(-180)/share × 2,000 = -$360K loss

- Stock at $145: Calls worth $25.00, profit = $(-175)/share × 2,000 = -$350K loss

- Stock at $160+: Calls worth $40+, profit = $(-160)/share × 2,000 = -$320K+ loss turning to PROFIT at $140+

Probability assessment: 35% because it requires MULTIPLE positive catalysts aligning (SAMR situation resolving, merchant program succeeding, international expansion delivering) while avoiding major negative surprises. The $120 strike is reasonable but needs 25-30% appreciation from current $112 over 18 months - achievable but not easy given macro headwinds.

🎯 Base Case - $105-120 Range Through Mid-2026 (40% probability)

Choppy consolidation with both trades expiring near breakeven

Most likely scenario:

- 📊 March 2026 earnings: Meets lowered expectations (revenue $8.5-8.7B, margins 22-23%), guidance cautious, stock stays $110-115

- ⚖️ SAMR situation: No formal investigation announced but relationship remains strained - regulatory overhang persists

- 🌍 International progress mixed: Temu European growth solid (+50% YoY) but decelerating, US recovery slow, Latin America promising but small

- 🇺🇸 Trade policy unchanged: 145% tariffs remain, local warehouse strategy making progress but expensive

- 💰 Margins compressed: RMB 100B merchant program continues pressuring profitability, ROI timeline unclear

- 🎢 Trading range: Oscillates between $105 gamma support floor and $114-120 resistance for months

- 😴 Volatility normalizes: After March earnings, IV compresses from current levels back toward 30-35% range

- 🔄 Waiting for clarity: Market in "show me" mode - needs concrete proof merchant program working before re-rating

Options P&L in Base Case:

- $105 Puts May expiration: Stock at $110-115, puts expire worthless, -$1.1M loss (100% premium paid = insurance cost)

- $120 Calls June 2027: Stock at $110-115 by mid-2026, calls still have time value but underwater, mark-to-market -$1-2M loss (could recover if stock rallies late 2026-2027)

Why 40% probability: This is the path of least resistance - stock neither breaking out nor breaking down dramatically. Fundamentals solid but unspectacular, regulatory issues simmering but not exploding, international growth continuing but not spectacular. Most institutional players adopt wait-and-see stance through 2026. Both option traders would be frustrated but not devastated.

📉 Bear Case - $90-105 Testing Put Strike (25% probability)

Near-term downside scenario where protective puts pay off massively

What could go wrong:

- 🚨 SAMR investigation announced Q1 2026 - Formal probe launched into merchant practices, VIE structure, or data handling following December altercation

- 💔 March earnings disaster - Revenue growth decelerates further (below 7%), margins collapse below 20%, management admits merchant program ROI uncertain

- 🇨🇳 Regulatory crackdown intensifies - Chinese government launches broader platform economy crackdown 2.0, targeting PDD's rapid growth tactics

- 🇺🇸 US entity list addition - Trump administration adds Temu to entity list, severely restricting US operations

- 💸 Temu European collapse - EU customs fees implemented more aggressively than expected (5+ euros), killing business model profitability

- 📊 Institutional exodus accelerates - Following Tiger Global, Mirae Asset, FMR LLC collectively selling $5.9B in Q2 2025, more major holders exit causing selling cascade

- 🥊 Competitive pressure - Alibaba and JD.com deploy massive capital to crush PDD's domestic market share gains

- 💰 Cash deployment concerns - Market loses patience with $59.5B cash sitting idle, demands capital return but management refuses

- 🌍 Macro deterioration - China property crisis worsens, consumer spending collapses, e-commerce TAM shrinks

- 🔨 Break below $105 support triggers cascade - Technical breakdown accelerates selling to $100, then $95 levels

Critical support levels:

- 🛡️ $105: Secondary gamma support + put strike - major battle line (EXACTLY where put positioned!)

- 🛡️ $103: MASSIVE put wall and HVL - strongest floor, must hold or panic ensues

- 🛡️ $99-100: Psychological round number support

- 🛡️ $95: Extended disaster floor

Put P&L in Bear Case:

- Stock at $100 by May 2026: $105 puts worth $5.00, profit = ($5 - $5.50)/share × 2,000 = -$100K loss (still not profitable!)

- Stock at $95 by May 2026: Puts worth $10.00, profit = ($10 - $5.50)/share × 2,000 = +$900K gain (82% ROI!)

- Stock at $90 by May 2026: Puts worth $15.00, profit = ($15 - $5.50)/share × 2,000 = +$1.9M gain (173% ROI!)

- Stock at $85 by May 2026: Puts worth $20.00, profit = ($20 - $5.50)/share × 2,000 = +$2.9M gain (264% ROI!)

LEAPS Call devastation in Bear Case:

- Stock at $95-100: $120 calls deeply out-of-the-money, mark-to-market -$2-3M loss (50-75% of premium), but still 12+ months to recover

Probability assessment: 25% because it requires MULTIPLE major negative catalysts converging (SAMR investigation + earnings miss + trade escalation + EU restrictions). PDD's fundamentals remain strong enough (cash fortress, international diversification, merchant ecosystem) that total collapse is unlikely. BUT, the 20.72 z-score on the put trade suggests the institutional buyer thinks this scenario has HIGHER than 25% probability - they're clearly worried!

💡 Trading Ideas

🛡️ Conservative: Wait for March Earnings Clarity (Cash Gang)

Play: Stay on sidelines until after Q4 2025 earnings on March 23, 2026

Why this works:

- ⏰ Too many unknowns: SAMR investigation risk, merchant program ROI uncertainty, trade policy evolution all create binary event risk

- 📊 Valuation not compelling: At 11.63x forward P/E, PDD isn't screaming cheap given execution risks - needs proof before buying

- 🎢 High volatility environment: Recent 7.56% volatility and gamma positioning suggest continued choppiness

- 💔 Broken momentum: Stock down 19% from highs, failed to hold $120+, technical damage needs time to repair

- 🤔 Smart money conflicted: $4M LEAPS calls vs $1.1M protective puts shows institutions can't agree - why should you pick a side?

- 📅 Better entry coming: Post-earnings clarity + IV crush could offer 10-15% better entry if you're patient

Action plan:

- 👀 Watch March 23 earnings for: Revenue growth trajectory, margin stabilization, SAMR commentary, Temu international metrics

- 🎯 Look for pullback to $100-105 (major gamma support + put strike zone) for stock entry with margin of safety

- ✅ Need to see concrete evidence merchant program ROI improving (GMV acceleration, margin recovery path)

- 📊 Monitor analyst consensus shifting - current $146.39 target seems optimistic given recent news

- ⏰ Re-evaluate Q2 2026 when more data points available on Shopify partnership, EU customs impact, US recovery

Risk level: Minimal (cash position preserves optionality) | Skill level: Beginner-friendly

Expected outcome: Avoid catching falling knife if SAMR investigation announced or earnings disappoint. Get much better entry if stock consolidates or corrects further. Maintain dry powder for higher-conviction opportunities.

⚖️ Balanced: Post-Earnings Defined-Risk Spread (Copy The Pros)

Play: After March earnings settles, sell put spread mirroring institutional hedging zone

Structure: Buy $110 puts, Sell $105 puts (May 15 expiration - SAME as the $1.1M institutional hedge trade)

Why this works:

- 🎢 IV crush opportunity: Buy AFTER March earnings when volatility compresses from current elevated levels (quarterly IV at 10.64%)

- 📊 Defined risk spread: $5 wide = $500 max risk per spread, $500 max profit

- 🎯 Targeting gamma support: $105-110 zone has massive put gamma concentration where institutions clearly positioned

- 🤝 Copying smart money: Essentially replicating the protective put strategy at better post-earnings prices

- ⏰ 52-day window: May 15 expiration gives time for any SAMR announcement or trade policy deterioration to materialize

- 🛡️ Asymmetric setup: Betting on downside while limiting risk - appropriate given elevated uncertainty

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Cost: ~$2.00-2.50 net debit per spread (vs $3-4 now with elevated IV)

- 📈 Max profit: $250-300 if PDD below $105 at May expiration

- 📉 Max loss: $200-250 if PDD above $110 (defined and limited)

- 🎯 Breakeven: ~$107.50-108

- 📊 Risk/Reward: ~1:1 which is acceptable for directional bearish play with institutional validation

Entry criteria:

- ⏰ Wait 2-4 days post-earnings (by March 25-27) for full IV collapse

- 🎯 Only enter if stock trades $112+ after earnings (gives room for spread to work)

- ❌ Skip if stock already below $108 (spread too close to at-the-money, risk/reward unfavorable)

- ✅ Confirm gamma levels haven't shifted dramatically (use updated GEX data post-earnings)

Position sizing: Risk only 2-5% of portfolio (this is hedging/speculation, not core holding)

Risk level: Moderate (defined risk, bearish directional bias) | Skill level: Intermediate

Exit strategy:

- 🎯 Take profit at 50-70% max gain (don't be greedy waiting for full $500)

- ⏰ Close 2 weeks before expiration to avoid gamma risk

- 🚨 Cut loss immediately if stock breaks decisively above $120 (thesis invalidated)

🚀 Aggressive: LEAPS Calendar Spread - Time Arbitrage Play (ADVANCED!)

Play: Sell near-term calls against long-term bullish position to monetize high current IV

Structure:

- Long leg: Buy $120 calls June 2027 (copy the $4M institutional LEAPS)

- Short leg: Sell $115-120 calls March 2026 (capture elevated pre-earnings IV)

Why this could work:

- 💰 IV arbitrage: Current quarterly IV at 10.64% much higher than long-term IV - sell expensive near-term, buy cheaper long-term

- 🎯 Institutional validation: $4M LEAPS buyer with 1.95 z-score believes in long-term recovery - piggyback their thesis

- 📊 Reduce cost basis: Selling March calls generates premium to subsidize June 2027 LEAPS cost

- ⏰ Time decay advantage: Short-dated options decay faster than long-dated - capture theta differential

- 🔄 Rolling strategy: Can roll short leg monthly to continuously harvest premium

- 🚀 Asymmetric upside: If PDD explodes higher mid-2027, long LEAPS capture full move after short calls expire

Why this could blow up (SERIOUS RISKS!):

- 💸 EXPENSIVE initial outlay: June 2027 $120 calls likely cost $25-30 per contract = $2,500-3,000 each

- 📉 Assignment risk: If stock rallies above short strike before March, lose upside and may need to close at loss

- 😱 Bear market devastation: If PDD drops to $90-95, LEAPS could lose 60-80% of value while short calls provide minimal cushion

- 🎢 Complex management: Requires active monitoring and rolling short legs every 30-60 days

- ⚠️ Margin requirements: Selling calls against LEAPS may require margin depending on broker

- 🇨🇳 Regulatory wipeout: SAMR investigation or VIE structure concerns could crater stock 30-40%, destroying entire position

Estimated P&L scenarios (for 10-contract position):

Setup:

- Buy 10x June 2027 $120 calls @ $28 = -$28,000 debit

- Sell 10x March 2026 $115 calls @ $8 = +$8,000 credit

- Net cost: -$20,000 ($2,000 per spread)

Outcome 1 - Bull Case (PDD at $135 by June 2027):

- Short March calls assigned at $115, bought back or rolled 3x for cumulative -$5,000 cost

- Long June 2027 calls worth $15 = +$15,000

- Total P&L: $15,000 - $20,000 - $5,000 = -$10,000 loss (50% loss - NOT GOOD!)

- Need stock above $140+ to profit meaningfully

Outcome 2 - Base Case (PDD at $110-115 range):

- Short March calls expire worthless or rolled for small credit

- Long June 2027 calls worth $0-5 = -$15,000 to -$20,000 loss

- Total P&L: -$10,000 to -$15,000 loss (50-75% loss)

Outcome 3 - Bear Case (PDD at $95):

- Short March calls expire worthless = $0

- Long June 2027 calls essentially worthless = -$28,000

- Collected $8,000 from initial short sale

- Total P&L: -$20,000 loss (100% of net debit)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded calendar spreads extensively and understand assignment/rolling mechanics

- ✅ Can afford to lose ENTIRE $20,000+ net debit (very real possibility!)

- ✅ Have time to actively manage position monthly (rolling short legs)

- ✅ Understand complex tax implications of calendar spreads

- ✅ Believe in PDD's long-term recovery thesis (18+ months) despite near-term pain

- ✅ Can withstand 50-80% drawdowns without panic selling

- ⏰ Have clear plan for managing short calls through earnings (roll BEFORE March 23 or accept assignment risk)

Risk level: EXTREME (can lose 100% of capital) | Skill level: Advanced/Expert only

Probability of profit: ~30% (lower than straight LEAPS due to limited upside from short calls capping gains)

Better alternative for most traders: Just buy 5x June 2027 $120 LEAPS outright for same $10-15K capital, avoid complexity and assignment risk. Simplicity usually beats cleverness in options.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🥊 SAMR investigation time bomb (HIGHEST RISK!): The December 2025 physical altercation with Chinese regulators is unprecedented corporate suicide in China's regulatory environment. SAMR has unlimited authority to launch investigations into merchant practices, pricing algorithms, data handling, VIE structure compliance - everything. 60% probability of formal investigation in Q1-Q2 2026 per analyst estimates. Investigation announcement could gap stock down 15-25% overnight to $85-95 range. This is existential risk that could destroy both option positions - the $105 puts might not provide enough downside protection, and the $120 LEAPS calls would be devastated. The 20.72 z-score extreme unusual activity on the puts screams that sophisticated institutions are TERRIFIED of this outcome.

-

💔 RMB 100B merchant program black hole: PDD's massive ecosystem investment crushed operating margin from 27% to 23.1% in Q3 while revenue growth decelerated to 9%. Management provided ZERO clarity on ROI timeline or success metrics. What if this $14B investment is just burning cash without sustainable GMV gains? Q2 operating profit fell 21% YoY despite revenue growth - that's the WRONG direction! If March earnings show continued margin deterioration below 22% with no path to recovery, market will lose patience. Stock could re-rate from 11.63x P/E to single digits (8-9x), sending it to $80-90 range.

-

🇺🇸 Trade war escalation with no end in sight: Current 145% US tariffs and de minimis elimination already destroyed Temu's US business model - 58% daily user decline in May 2025. Trump administration could go FURTHER: sector-specific penalties on Chinese e-commerce, adding Temu to entity list (restricting operations entirely), or banning transactions with PDD altogether. Goldman Sachs notes PDD has "highest US exposure amongst China cross-border players" making it most vulnerable. Local warehouse pivot is expensive and unproven - burning cash to build infrastructure that may never generate returns. 90%+ probability trade restrictions WORSEN through 2026.

-

🇪🇺 European regulatory vise tightening: Dublin headquarters raided December 9 + Germany anti-trust investigation + EU consumer protection violations + proposed 2-euro customs fee implementation H1 2026. Europe is Temu's CROWN JEWEL with $1.7B 2024 revenue (+171% YoY) projected to exceed $15B GMV in 2025. 70% probability of significant EU regulatory action in 2026 - could include €10-50M fines AND operational restrictions that kill margins. If Europe goes the way of US (regulatory crackdown destroying business model), where's the growth coming from?

-

💸 Institutional exodus accelerating: Tiger Global completely exited removing $462M, Mirae Asset removed $4.12B (-99.1%), FMR LLC removed $1.33B (-45.9%) in Q2 2025. That's $5.9 BILLION in institutional selling in ONE QUARTER! Smart money is running for the exits. Even Li Lu's Himalaya Capital opening $482M position can't offset the wave of redemptions. Q3 2025 showed 262 institutions added shares but 308 decreased - more sellers than buyers. If institutional ownership continues declining, stock becomes orphaned and vulnerable to downside volatility cascades.

-

📊 Valuation trap at 11.63x forward P/E: Looks cheap compared to Alibaba's 19.57x, but PDD deserves discount given: (1) VIE structure regulatory risk, (2) Merchant program destroying margins, (3) Revenue growth collapsing from 44% to 9%, (4) Zero dividend/buyback despite $59.5B cash, (5) Geopolitical crosshairs from both China AND US/EU. The "cheap" valuation is a VALUE TRAP - could easily re-rate to 8-9x P/E (JD.com level at 7.63x) if execution continues deteriorating, sending stock to $75-85 range. Don't confuse low P/E with safety!

-

🥊 Competitive annihilation from Alibaba/JD counterattack: Alibaba and JD.com have deployed massive capital to match PDD's low-cost model, eroding first-mover advantage. These giants have MUCH deeper pockets (Alibaba $240B market cap vs PDD $159B) and can sustain price wars longer. Taobao matching Pinduoduo's gamification, JD leveraging superior logistics network. PDD's domestic GMV growth already plateauing - what happens when Alibaba goes full scorched earth? Could force PDD into permanent margin compression just to defend share.

-

🎢 Extreme volatility (61.9% annualized) creates whipsaw risk: Recent 19% drawdown from $139 highs to $112 happened in just 3 months. December alone saw only 8 green days out of 30 (27% win rate) with 7.56% daily volatility. This stock can gap $8-12 on headlines with no fundamental change. The negative net gamma positioning means market makers SELL into weakness rather than stabilize - creates explosive downside moves. Max drawdown could easily test $90-95 if multiple catalysts align negatively. Are you prepared for 30-40% decline psychologically?

-

📅 March 23 earnings binary event risk: With quarterly implied move at ±10.64% ($11.94), earnings could send stock anywhere from $100 to $124 in one day. Recent track record shows Q3 2025 massive miss triggered 4.18% premarket decline that extended through December. Management has provided NO GUIDANCE, leaving analysts in the dark. Conservative guidance could crush stock even on decent results. This is not a earnings report you want to hold options through unless you LOVE gambling!

-

🌍 China macro deterioration wildcard: Property crisis continuing to dent consumer confidence, GDP growth slowing, government stimulus showing limited effectiveness. PDD's domestic Pinduoduo platform tied to discretionary spending recovery that may never come. If Chinese consumers stay cautious, domestic GMV growth could remain sub-10% for YEARS. International expansion (Temu) can't fully offset domestic weakness AND faces its own regulatory challenges. Dual headwinds with no clear catalyst for reversal.

-

💰 Capital allocation paralysis with $59.5B cash: PDD sitting on $59.5B cash against $1.6B debt - one of the largest cash hoards in e-commerce. Management refuses to return capital via dividend/buyback, preferring to burn it on merchant support program with unclear ROI. Shareholders getting ZERO return on cash while earnings collapse. This is value destruction! If management doesn't announce shareholder-friendly capital allocation by mid-2026, activists could get involved or shareholders revolt. Stock deserves discount for poor capital stewardship.

🎯 The Bottom Line

Real talk: These two trades tell COMPLETELY DIFFERENT stories about PDD's future, and BOTH might be right on different time horizons. The $4M LEAPS call buyer believes in the long-term bull case: Temu's global expansion succeeds, merchant ecosystem investments pay off by 2027, regulatory troubles fade, and PDD returns to double-digit growth. The $1.1M put buyer with EXTREME 20.72 z-score unusualness is terrified of near-term disaster: SAMR investigation announcement, March earnings catastrophe, trade war escalation, or EU regulatory hammer dropping.

What these trades reveal:

The LEAPS Call Bull Case ($4M bet on recovery):

- 🎯 Patient capital betting on 18-month turnaround from current $112 to $120+ by June 2027

- 💰 Believes Temu's 1B+ downloads and global expansion will overcome regulatory headwinds

- 🤝 Shopify partnership validates marketplace evolution reducing tariff exposure

- 🌍 International diversification (Europe $15B+ GMV, Latin America fastest-growing) creates sustainable growth

- 📊 $59.5B cash fortress provides cushion to weather storms and invest in AI/logistics

- ⏰ Regulatory overhang temporary - time heals all wounds in China's business environment

- 🚀 Modest $120 strike (only 6.9% upside needed) shows realistic optimism, not moonshot gambling

The Put Bear Case ($1.1M hedge of doom):

- 🚨 EXTREME 20.72 z-score signals institutional PANIC about near-term catalysts (next 143 days)

- 🥊 December regulatory altercation could trigger formal SAMR investigation announcement Q1 2026

- 💔 March 23 earnings carries ±10.64% implied move risk - could gap to $100-105 on miss

- 🇺🇸🇪🇺 Dual regulatory assault from US (tariffs/lawsuits) and EU (customs fees/investigations) compressing margins

- 📉 RMB 100B merchant program destroying profitability with no end in sight (margins 27% → 23% → ?)

- 💸 Institutional exodus ($5.9B sold in Q2) suggests smart money sees trouble ahead

- 🎯 $105 strike positioned EXACTLY at secondary gamma support - expects flush through $105 floor if bad news hits

Can both be right? ABSOLUTELY! PDD could drop to $95-105 on SAMR investigation or earnings miss in Q1 2026, then recover to $120-130 by mid-2027 as regulatory situation stabilizes and international expansion delivers. The put buyer protects near-term downside, the LEAPS buyer captures long-term recovery. This is sophisticated institutional positioning for a binary, volatile name.

What should YOU do?

If you're bullish on PDD long-term:

- ⏰ Wait for better entry - Don't chase at $112 with March earnings 90 days away creating binary risk

- 🎯 Target $100-105 pullback (put strike zone + major gamma support) for stock accumulation

- 📊 After March earnings, if stock holds $105+ and shows revenue stabilization, consider small LEAPS position (June 2027 $115-120 calls)

- 💰 Never more than 3-5% of portfolio given extreme geopolitical/regulatory risk

- 🛡️ Build position over TIME (3-6 months) rather than all-in bet - dollar-cost-average the volatility

- ✅ Wait for concrete catalyst: SAMR situation clarity, merchant program ROI proof, or shareholder-friendly capital allocation

If you're bearish or neutral:

- 🚫 Don't short outright - borrow costs high, $59.5B cash provides downside cushion, short squeeze risk if news improves

- 📊 Post-March earnings, consider defined-risk put spreads ($110/$105 or $108/$103) to limit exposure

- ⏰ Be PATIENT - let catalysts unfold rather than trying to time exact bottom

- 👀 Watch for institutional positioning changes via 13F filings in Q1 2026

- 🎯 If stock breaks decisively below $103 put wall, could accelerate to $95-100 - but don't chase, wait for stabilization

If you're on the fence (MOST SENSIBLE!):

- 💵 Cash is a position - There are 3,000+ stocks in the market, you don't NEED to own PDD right now

- 📅 March 23 earnings is the moment of truth - wait for that clarity before committing capital

- 🎯 Better opportunities exist with less regulatory/geopolitical risk if you want China exposure (look at Alibaba up 113.6% YTD!)

- 🤔 The fact that sophisticated institutions can't agree (LEAPS vs puts) should tell you something

- ⏰ Let the dust settle for 3-6 months - PDD will still be here, and you'll have much better information

Mark your calendar - Key dates:

- 📅 January 16, 2026 - Monthly OPEX (±4.67% implied move closes)

- 📅 March 20, 2026 - Quarterly triple witch (±10.64% implied move window)

- 📅 March 23, 2026 (CRITICAL!) - Q4 2025 earnings after market close

- 📅 May 15, 2026 - Monthly OPEX, expiration of the $1.1M protective put trade

- 📅 June 17, 2027 - Expiration of the $4M LEAPS call trade

Final verdict: PDD is a BINARY, HIGH-CONVICTION name where you need to pick a side with full awareness of the risks. The long-term bull case (Temu global dominance, merchant ecosystem success, AI capabilities) is compelling at 11.63x forward P/E with $59.5B cash. BUT, the near-term bear case (SAMR investigation risk, merchant program ROI uncertainty, trade war escalation, margin compression) is EQUALLY compelling and could send stock to $90-100 before recovery begins.

The $1.1M put trade with 20.72 z-score is a MASSIVE WARNING SIGNAL that sophisticated money sees serious downside risk in next 143 days. Respect that signal. Don't be a hero trying to catch the falling knife.

Be patient. Wait for March earnings. Let the SAMR situation play out. Look for entry at $100-105 with clear evidence the worst is over. The China e-commerce opportunity will still be massive in 2027, but you don't need to own it at $112 TODAY with a regulatory time bomb ticking.

This is a war of attrition, not a sprint. Protect your capital first. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The 1.95 and 20.72 z-scores reflect these specific trades' sizes relative to recent PDD history - they do not imply the trades will be profitable or that you should follow them. Chinese ADRs carry unique regulatory and geopolitical risks including VIE structure uncertainty, potential delisting, and government intervention. PDD faces multiple binary catalysts (SAMR investigation, earnings, trade policy) that could cause 20-40% moves in either direction. Always do your own research and consider consulting a licensed financial advisor before trading. Past performance doesn't guarantee future results.

About PDD Holdings: PDD Holdings operates commerce platforms across 80+ countries, running Pinduoduo (a social commerce platform in China), Temu (a worldwide e-commerce marketplace), and a community group purchase business in China, with a market cap of $158.9 billion in the Online Retail & E-commerce industry.