PDD Holdings (PDD) Options Flow Analysis

January 16, 2026 | Unusual Options Activity Report

Executive Summary

A $3.7 million put purchase hit the tape this morning on PDD Holdings, the parent company of Temu and Pinduoduo. This is a significant institutional-sized bet that either represents downside protection for a large equity position or a directional bearish wager. With PDD facing regulatory headwinds in both China and Europe, plus the July 2026 EU tariff implementation looming, this trade deserves close attention.

Key Takeaway: This June 2026 $95 put purchase suggests someone is either hedging significant exposure or betting on a 10%+ decline over the next five months. Given PDD's recent regulatory troubles and the upcoming Q4 earnings, this is smart money positioning you want to track.

Trade Tape

| Field | Value |

|---|---|

| Time | 10:02:25 ET |

| Ticker | PDD |

| Direction | BUY |

| Type | PUT |

| Expiration | 2026-06-18 |

| Strike | $95.00 |

| Option Price | $4.90 |

| Size | 7,600 contracts |

| Premium | $3,724,000 |

| Volume | 7,600 |

| Open Interest | 6,000 |

| Spot Price | $106.50 |

| Moneyness | 10.8% OTM |

| Option Symbol | PDD20260618P95 |

| Classification | Protective Put or Bearish Bet (BTO) |

Unusual Score Analysis

Unusual Score: 6.5/10 - VERY UNUSUAL

[======----] 6.5/10

Why This Trade Stands Out:

- Volume vs Open Interest: 7,600 contracts traded against only 6,000 open interest - this is a 127% V/OI ratio, indicating fresh positioning rather than closing trades

- Premium Size: $3.7M is a large fund allocation, representing institutional-level capital deployment

- Timing: Coming just two months after the unprecedented SAMR regulatory incident and heading into Q4 earnings season

- Strike Selection: The $95 strike sits 10.8% below current price, suggesting the trader expects a meaningful move (not just hedging small volatility)

In Plain English: This is the kind of trade that happens maybe a few times per quarter on PDD. Someone with deep pockets is either protecting a massive long position or making a directional bet on significant downside. Either way, it's worth paying attention to.

Company Overview

PDD Holdings Inc. (NASDAQ: PDD) operates one of the world's largest e-commerce ecosystems, running Pinduoduo in China and Temu internationally.

| Metric | Value |

|---|---|

| Market Cap | ~$152.6 billion |

| Sector | E-commerce / Consumer Discretionary |

| Employees | 23,465 |

| P/E Ratio | 12.24x (Forward: 11.63x) |

| Cash Position | ~$38 billion |

| 52-Week Range | $87.11 - $139.41 |

What They Do: PDD runs a social commerce platform in China (Pinduoduo) with 900+ million users focusing on value-conscious consumers, plus Temu - the international e-commerce app that took the world by storm with ultra-low prices direct from manufacturers. They've pioneered the "C2M" (Consumer-to-Manufacturer) model that cuts out middlemen.

The Bull Case: PDD trades at a significant discount to Alibaba on a P/E basis, holds a fortress balance sheet with $38B in cash, and Temu's European expansion is accelerating (+74% YoY user growth). If they announce a buyback program, the stock could re-rate significantly.

The Bear Case: Revenue growth has decelerated sharply to single digits (+9% YoY in Q3), the December 2025 regulatory incident with SAMR officials was unprecedented, and the July 2026 EU tariff implementation will pressure international margins. Major institutions (FMR, Goldman, Tiger Global) have been reducing exposure.

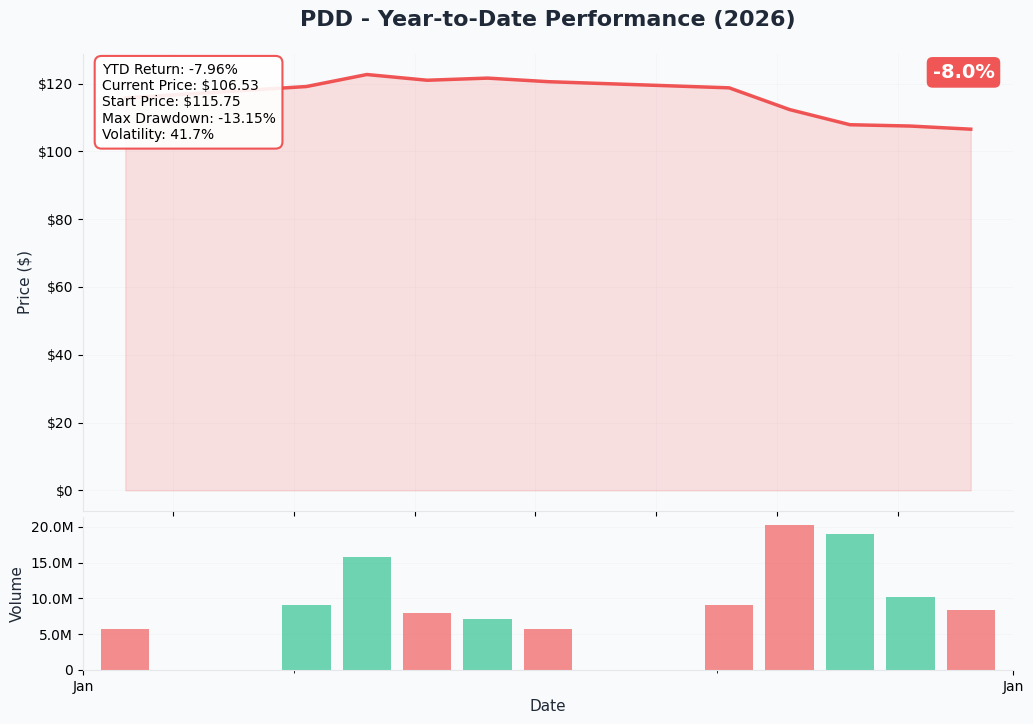

YTD Performance

PDD has been on a roller coaster over the past year, rallying from the April 2025 lows near $87 to peak above $139 in October 2025 before giving back roughly 20% of those gains. The stock currently trades around $106.50, sitting in the middle of its 52-week range.

Trade Thesis: Two Interpretations

This trade can be read two ways, and both are worth considering:

Scenario 1: Protective Put (Hedging)

The Setup: A large fund holding millions of PDD shares is buying downside protection ahead of known risk events.

Why It Makes Sense:

- Q4 2025 earnings expected in March 2026 - management warned of "fluctuating" results due to RMB 100B merchant support program1

- SAMR investigation ongoing following the December 2025 fistfight incident - unprecedented regulatory uncertainty2

- July 2026 EU small parcel duty (EUR 3 per item) will directly impact Temu margins3

- Institutional ownership at just 7.29% - suggesting concentrated holdings among remaining institutions4

Implication: If this is a hedge, the fund likely remains long-term bullish but wants protection through a volatile period. The June expiration captures both Q4 earnings and gives runway toward the EU tariff implementation date.

Scenario 2: Directional Bearish Bet

The Setup: A fund is betting PDD will decline significantly over the next five months.

Why It Makes Sense:

- Revenue growth has collapsed from triple digits to +9% YoY5

- Major institutions have been selling aggressively - MIRAE ASSET removed 39.3M shares (-99.1%), FMR removed 12.7M shares (-45.9%)6

- Multiple analyst downgrades: Arete, Bernstein, and New Street all cut ratings7

- De minimis exemption elimination and 54% tariff rate on small parcels crushing US business8

- Temu US DAU dropped 52% in May 2025 vs March 20259

Implication: If this is a directional bet, the trader sees significant downside risk and believes PDD could revisit the April 2025 lows near $87 or break below.

My Read: Given the timing (heading into Q4 earnings), the strike selection (10.8% OTM), and the June expiration (capturing multiple risk events), this looks more like sophisticated hedging than a pure speculative bet. But make no mistake - whoever bought this protection is clearly concerned about meaningful downside risk.

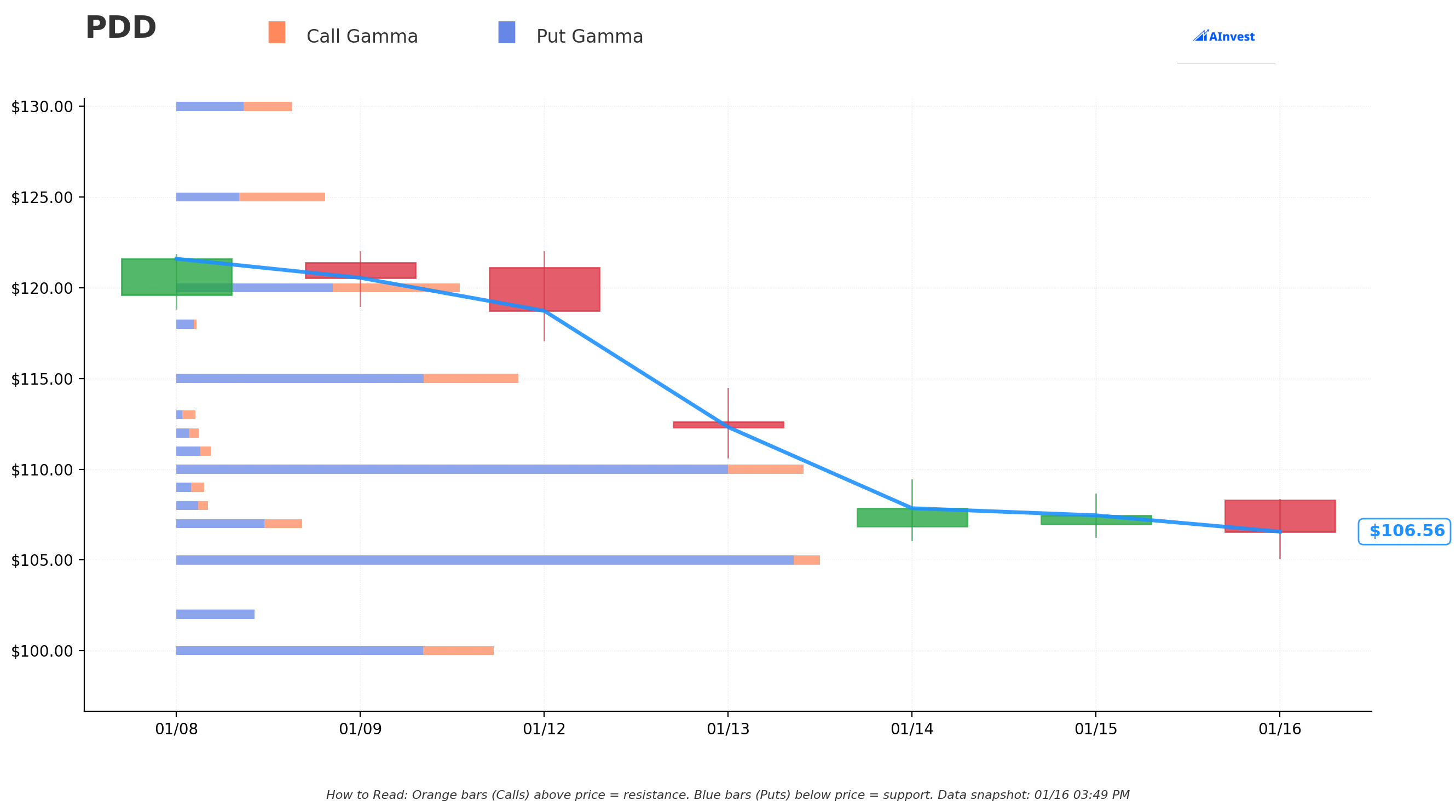

Gamma Support/Resistance Analysis

Dealer gamma positioning shows key levels that could influence price action:

| Level | Type | Significance |

|---|---|---|

| $110 | Resistance | Heavy call open interest, dealer short gamma |

| $105 | Support | Put wall providing downside cushion |

| $100 | Major Support | Psychological level + significant put OI |

| $95 | Strike Target | The put strike from today's trade |

| $90 | Deep Support | Would indicate trend breakdown |

The $95 strike aligns with a notable gamma level, suggesting the trader may be targeting that zone as a potential endpoint for a selloff.

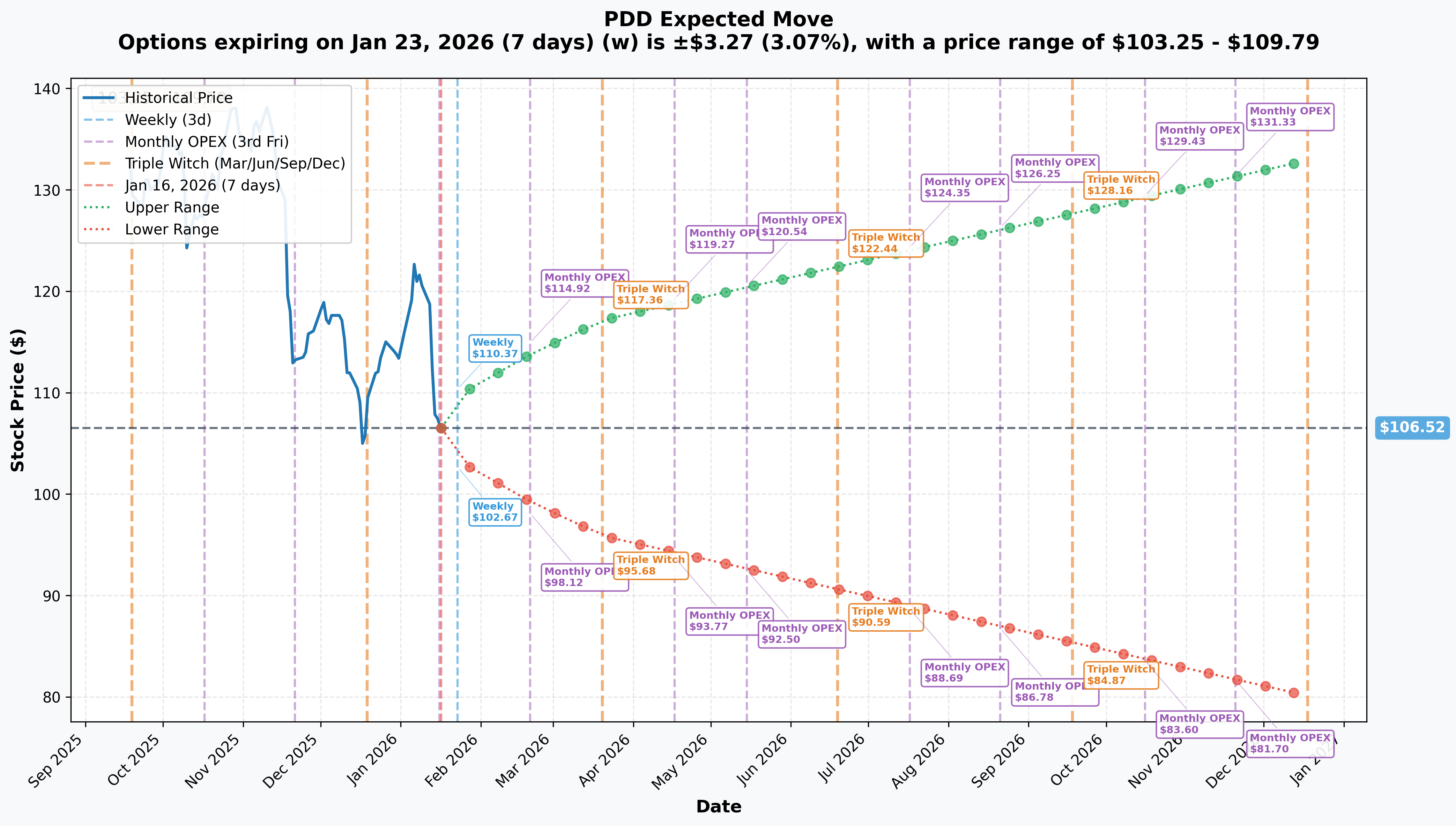

Implied Move Analysis

Options markets are pricing the following expected moves:

| Timeframe | Expiration | Implied Move | Upper Range | Lower Range |

|---|---|---|---|---|

| Weekly | Jan 23, 2026 | +/-3.07% | $109.79 | $103.25 |

| Monthly OPEX | Feb 20, 2026 | +/-6.88% | $113.85 | $99.19 |

| Triple Witch | Mar 20, 2026 | +/-10.01% | $117.19 | $95.85 |

| June Triple Witch | Jun 19, 2026 | +/-14.9%* | $122.44 | $90.59 |

The June implied move range puts the lower bound at $90.59, which is below the $95 strike. This means the options market sees a roughly 30-35% probability of the stock reaching or exceeding this put strike by expiration.

Key Insight: The $95 strike is approximately 1 standard deviation move to the downside based on June expiration implied volatility. This isn't a crazy lottery ticket - it's a reasonable hedge or directional bet that has a real probability of being in the money.

Upcoming Catalysts

| Date | Event | Risk Level | Potential Impact |

|---|---|---|---|

| March 2026 | Q4 2025 Earnings | HIGH | Revenue growth trajectory, margin pressure from RMB 100B program |

| March 2026 | Full Year Guidance | HIGH | First look at 2026 outlook amid tariff headwinds |

| July 1, 2026 | EU Small Parcel Duty | MEDIUM | EUR 3/item on all parcels under EUR 150 |

| Ongoing | SAMR Investigation | HIGH | Regulatory overhang from December 2025 incident |

| Ongoing | US-China Trade Tensions | MEDIUM | Current 54% tariff on small parcels |

The June 2026 expiration strategically captures all of these catalysts except the EU tariff implementation (which hits July 1). This suggests the trader is primarily focused on Q4 earnings and the ongoing regulatory uncertainty.

Price Targets & Probabilities

Based on gamma levels, implied moves, and catalyst analysis:

| Target | Price | Probability | Scenario |

|---|---|---|---|

| Bullish | $120+ | 25% | Q4 beat + buyback announcement + regulatory clarity |

| Base Case | $95-105 | 45% | Continued deceleration but no major negative surprises |

| Bearish | $85-95 | 30% | Q4 miss + SAMR escalation + EU tariff concerns |

The put buyer appears positioned for the bearish outcome or is hedging against it. At $95, they're targeting approximately a 10% decline from current levels.

Trading Strategies

Conservative: Protective Put Spread (Capital Efficient Hedge)

If you're long PDD shares and want downside protection similar to this institutional trade but at lower cost:

- Buy June 2026 $100 Put

- Sell June 2026 $90 Put

- Net Cost: ~$3.50-4.00 per share

- Protection: Covers $100 down to $90 (10-point spread)

- Risk: Loss below $90 not protected; premium paid is max loss if stock stays above $100

Best For: Long-term holders wanting to sleep well through Q4 earnings

Balanced: Short-Term Put Calendar Spread

Capitalize on elevated volatility around earnings while maintaining downside exposure:

- Sell March 2026 $100 Put (collect premium from earnings IV crush)

- Buy June 2026 $100 Put (maintain longer-term protection)

- Net Cost: ~$2.00-2.50 debit

- Thesis: If stock stays above $100 through earnings, March put expires worthless; June put retains value for later catalysts

Best For: Traders who think Q4 won't be catastrophic but want protection for EU tariff period

Aggressive: Follow the Smart Money

Mirror the institutional trade with appropriate position sizing:

- Buy June 2026 $95 Put

- Current Price: ~$4.90

- Max Gain: $95 - stock price at expiration (minus premium)

- Max Loss: $4.90 (100% of premium)

- Break-Even: $90.10 at expiration

Position Sizing: Risk no more than 2-3% of portfolio on this speculative position

Best For: Traders with high conviction on PDD downside

Risk Factors

For Put Buyers (Bearish Positioning):

- PDD could announce a massive buyback program, sending shares higher

- US-China trade relations could improve, reducing tariff pressure

- Q4 earnings could surprise to the upside

- SAMR investigation could conclude without major penalties

- European expansion could offset US weakness

For Put Sellers (Bullish/Neutral Positioning):

- SAMR investigation could escalate to delisting risk concerns

- Q4 revenue could miss significantly as growth continues decelerating

- EU tariff implementation could drive further multiple compression

- Institutional selling could accelerate

- Temu US could continue deteriorating (DAU already down 52%)

General Market Risks:

- Chinese ADRs face ongoing geopolitical uncertainty

- E-commerce sector facing margin compression globally

- Consumer spending in both US and China showing weakness

Bottom Line & Action Plan

What We Know:

- A $3.7 million institutional put purchase hit the tape at 10:02 AM

- Volume exceeded open interest (127% V/OI) indicating fresh positioning

- The June 2026 $95 strike captures Q4 earnings and most near-term catalysts

- PDD faces genuine headwinds: regulatory uncertainty, tariff pressure, growth deceleration

What It Likely Means: This is most likely sophisticated hedging by a fund with significant PDD exposure, though it could also be a directional bet. Either way, someone with deep pockets is concerned enough about the next five months to spend $3.7M on downside protection.

Action Items:

-

If You're Long PDD: Consider adding your own downside protection. A put spread (buy $100 put, sell $90 put) for June offers cost-efficient insurance through the major catalyst window.

-

If You're Considering Going Long: Wait for Q4 earnings clarity in March. The risk/reward improves significantly once we see if revenue stabilization is occurring.

-

If You Want to Follow This Trade: The June $95 put at ~$4.90 offers roughly 2:1 risk/reward to the $85 level. Size appropriately (2-3% of portfolio max).

-

Key Levels to Watch:

- $105: Near-term support - break below would be concerning

- $100: Psychological support - failure here likely triggers accelerated selling

- $95: The institutional target - reaching this level confirms the thesis

Monitor: March 2026 Q4 earnings call for revenue guidance, SAMR investigation updates, and any announcements regarding capital return programs.

References

Analysis generated by OptionLabs | Data as of January 16, 2026

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Options involve risk and are not suitable for all investors. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Footnotes

-

TipRanks, "PDD Holdings Earnings Dates & Reports", January 2026 ↩

-

Bloomberg, "Fistfights Erupt Between China Officials, Temu Owner PDD Staff During Audit", December 11, 2025 ↩

-

EU Council, "Customs: Council agrees to levy customs duty on small parcels as of 1 July 2026", December 12, 2025 ↩

-

WallStreetZen, "PDD Holdings Stock Ownership - Who Owns PDD Holdings in 2026?", January 2026 ↩

-

PDD Holdings Investor Relations, "PDD Holdings Announces Third Quarter 2025 Unaudited Financial Results", November 18, 2025 ↩

-

MarketBeat, "PDD Institutional Ownership", January 2026 ↩

-

TipRanks, "PDD Holdings Stock Forecast, Price Targets and Analysts Predictions", January 2026 ↩

-

SmartAsset, "De Minimis: 2025 Trump Changes and Effects on Consumer Costs", 2025 ↩

-

Axios, "Trump ends de minimis loophole: What consumers, businesses should know", July 30, 2025 ↩