🛡️ PG: Defensive Giant Gets a $1.1M Bullish Wake-Up Call!

📅 March 12, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.1 MILLION on PG call options this morning, betting Procter & Gamble's stock climbs 4.7% to $160 by April 17th — the same day as Q3 FY2026 earnings. This isn't accident timing: with 7,900 contracts bought against just 6,000 open interest, this is a brand-new opening position from someone who is very much not your neighbor Bob. Translation: A big player is making a specific bullish bet on a defensive consumer staples mega-cap right into earnings — and the $160 strike punches through a key gamma resistance wall.

📊 Company Overview

Procter & Gamble (PG) — founded in 1837 — is the world's largest consumer packaged goods company. You've used their products today. Probably multiple times.

- Market Cap: ~$356 Billion

- Industry: Soap, Detergents, Cleaning Preparations, Perfumes, Cosmetics (FMCG)

- CEO: Shailesh Jejurikar (new, effective January 1, 2026 — first full quarter underway)

- Annual Revenue: ~$85 billion across 180+ countries

- Iconic Brands: Tide, Pampers, Gillette, Head & Shoulders, Crest, Oral-B, Olay, Febreze, Swiffer, Always

- Dividend King: 69 consecutive years of dividend increases — the Mount Rushmore of boring-but-reliable stocks

This is the ultimate defensive play — people buy Tide laundry detergent and Pampers diapers whether the market is up 20% or down 20%. So when someone drops $1.1M in calls on PG... you pay attention.

💰 The Option Flow Breakdown

📊 The Tape — March 12, 2026 @ 11:02:27

| Field | Detail |

|---|---|

| Date / Time | 2026-03-12 / 11:02:27 |

| Symbol | PG |

| Side | MID |

| Buy / Sell | BUY |

| Type | CALL $160 |

| Expiration | 2026-04-17 |

| Premium | $1.1M |

| Strike | $160 |

| Volume | 7,900 |

| Open Interest | 6,000 |

| Size | 5,443 |

| Spot Price | $152.81 |

| Option Price | $2.04 |

| Strategy | Long Call (BTO — Buy to Open) |

| Vol/OI Ratio | 1.32x (new opening position) |

| Unusualness | EXTREMELY UNUSUAL relative to history |

🤓 What This Actually Means

Let's break this down in plain English:

- 💸 $1.1M laid out: At $2.04 per contract × 5,443 contracts × 100 shares = $1.11 million in premium, paid upfront

- 🎯 The bet: PG needs to trade above $162.04 ($160 strike + $2.04 premium) for this position to profit at expiration — that's a 6.1% move from $152.81

- 📊 New money, new position: Volume of 7,900 vs open interest of only 6,000 means this is almost certainly a fresh Buy to Open — someone just loaded up from scratch, they're not closing an existing short

- 🏦 Why it's unusual: This is a large, single-ticket call purchase on one of the most sedate, dividend-focused stocks in the S&P 500. PG doesn't normally attract aggressive bullish option bets — it's known for covered call income strategies and institutional accumulation. Seeing EXTREMELY UNUSUAL flow here means someone has a very specific, high-conviction thesis

- ⏰ April 17 expiration is NOT random: That is the exact date of P&G's Q3 FY2026 earnings report (before market open). This is a pre-earnings directional bet — the call buyer is wagering PG either beats estimates or pre-announces something bullish

What's really happening here:

The buyer needs PG to rally ~$7 from $152.81 to $160 — and not just reach it, but close above the $162 breakeven. That's a 4.7% move to the strike, which in ordinary times would take PG weeks. But the context is critical: Q3 earnings are April 17, a new CEO (Shailesh Jejurikar) is in his first full quarter at the helm, and analyst consensus sits at Buy with an average price target of $170.86. The $160 strike also happens to punch right through the $160 gamma resistance level (more on this below). If that wall breaks, market dynamics could accelerate the move higher.

This could also be a rotation story: in a turbulent market environment, big money sometimes pours into consumer staples as a defensive shelter — and buying calls instead of stock gives upside leverage with limited downside (you can only lose the $1.1M premium, not the full stock position).

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

PG has been drifting in consolidation territory year-to-date, trading between roughly $147 and $165. The stock recovered from restructuring-driven lows in mid-2025 and has traded sideways-to-lower more recently — down approximately 4.4% over the trailing 12 months. The stock dropped about 2.3% on March 4 following news of significant insider selling by Executive Chairman Jon Moeller, which added to near-term headwinds. Currently trading around $151-153, PG sits in a tug-of-war between defensive rotation buyers and investors concerned about flat organic volume growth.

Key observations from the YTD chart:

- 📉 Lower from January highs: Stock peaked near $165 in January and has gradually pulled back to current $152 range — creating a potential mean-reversion setup if catalysts emerge

- 🎯 Support holding: Multiple tests of the $149-150 zone have found buyers — consistent with the gamma picture below

- 📊 Tight consolidation: Low-volatility consumer staples behavior — the stock doesn't make dramatic moves, which is exactly why this $1.1M call purchase stands out so sharply

🔵🟠 Gamma-Based Support & Resistance Analysis

The gamma exposure map shows where market makers are heavily positioned — these are the price levels that act as magnets or walls for near-term price action:

Current Price: $151.22 (as of analysis time)

🔵 Support Levels (Put Gamma — Dealers Buy Dips Here):

- $150.00 — STRONGEST FLOOR with 19.64 total GEX — this is a massive put gamma wall. Think of it as a trampoline: dealers have to buy stock aggressively here to hedge their exposure. This is the line in the sand.

🟠 Resistance Levels (Call Gamma — Dealers Sell Rallies Here):

- $152.50 — Immediate resistance at 5.98 GEX — minor speed bump

- $155.00 — Solid resistance at 15.93 GEX — meaningful ceiling that needs to be cleared

- $157.50 — Lighter resistance at 3.65 GEX — easier to push through

- $160.00 — 11.93 GEX — THIS IS THE CALL BUYER'S TARGET STRIKE. Not coincidental. Smart money strikes at key gamma levels.

- $165.00 — Extended resistance at 9.62 GEX — well beyond current price

Overall GEX Bias: Bullish (call GEX 52.80 > put GEX 49.77) — the market's options positioning tilts modestly bullish overall.

What this tells us:

PG is sitting right above the dominant $150 support floor, with a staircase of gamma resistance levels between here and the $160 target. The $155 level (15.93 GEX) is the first major hurdle — that's where dealers will sell into any rally. Get through $155, and $157.50 is light. Then comes $160 with 11.93 GEX — that's a real wall, but it's also the target. Here's the interesting part: if a bullish earnings catalyst or major news drives buying through $160, the gamma dynamics can flip and become self-reinforcing — dealers who were short calls suddenly have to buy stock to hedge, which pushes the stock higher. That's the squeeze scenario the call buyer may be betting on.

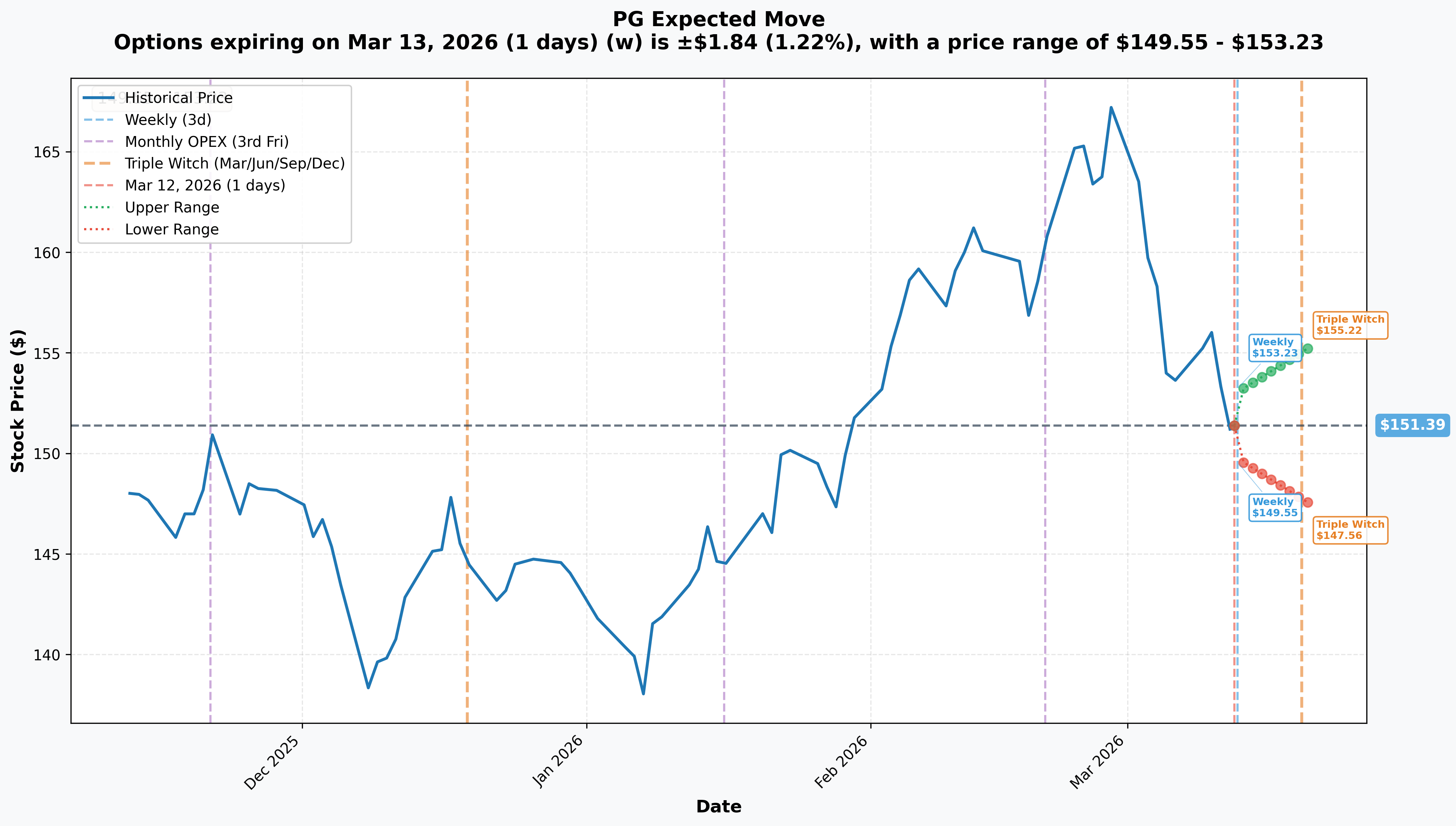

📅 Implied Move Analysis

The options market is telling us precisely how much PG is expected to move over upcoming expirations:

- 📅 Weekly (March 13): ±1.22% = ±$1.84 → Range: $149.55 — $153.23

- 📅 Monthly OPEX (March 20 — Triple Witch): ±2.53% = ±$3.83 → Range: $147.56 — $155.22

- 📅 April OPEX (April 17 — THIS TRADE): The options market is currently pricing in a move toward approximately $155-$156 for April expiration under a neutral/base-case scenario

Translation for regular folks:

The options market alone doesn't think PG gets to $160 by April 17 — the neutral implied range tops out around $155-156. So the call buyer is betting on an above-consensus outcome: a strong Q3 earnings beat, a catalyst surprise, or a macro rotation into defensives that pushes PG well beyond what the market currently implies. That's what makes this trade interesting and inherently speculative — this buyer is fighting the market's own probability estimate, which means they either know something or have very strong conviction on a catalyst.

🎪 Catalysts

🔥 Upcoming Catalysts (The Big Ones)

Q3 FY2026 Earnings — April 17, 2026 (Before Market Open) 🚨 THIS IS THE TRADE CATALYST

P&G reports fiscal Q3 results on April 17, 2026 — the same day this call expires. Wall Street expectations:

- 📊 Consensus Revenue: ~$20.63 billion

- 💰 Consensus Core EPS: ~$1.57

- 📈 Full-Year FY2026 Core EPS Range: $6.83–$7.09 (maintained guidance)

- 🎯 Critical watch items: Organic sales volume trend (Q1: +2%, Q2: flat — Q3 is the tie-breaker), tariff cost absorption, Tide evo consumer adoption data, and new CEO Jejurikar's first full quarter of strategic commentary

- 💰 Annual Dividend Increase: P&G has raised its dividend for 69 consecutive years — the annual increase is typically declared alongside Q3 earnings in April. A 70th consecutive increase announcement would extend the Dividend King streak and attract institutional income buyers

Tide evo Nationwide Rollout — Ongoing (February 2026 Launch)

P&G launched Tide evo — a revolutionary waterless detergent tile — for nationwide U.S. distribution in February 2026. The product took 10 years to develop and is priced at $19.99 for 42 tiles (a 54% premium to Tide Pods). Q3 earnings will be the first real data point on early consumer adoption velocity. Tide Pods grew into a $2 billion annual business after its 2012 launch — if Tide evo shows any similar early traction, it changes the organic growth narrative significantly.

CAGNY 2026 Conference — February 19, 2026 (Already Happened)

New CEO Jejurikar presented P&G's "integrated growth strategy" at CAGNY alongside CFO Schulten, highlighting Tide evo, Swiffer PowerMop, and SK-II Greater China recovery as innovation proof points. The April earnings call will be his first opportunity to show Q3 execution against that strategy.

📋 Already Happened (Recent Context)

Q2 FY2026 Results — January 22, 2026

P&G's Q2 showed mixed results: Core EPS of $1.88 beat consensus by $0.01 — but organic sales were flat (0% growth) with a -1% volume decline. Net sales of $22.2B grew 1% YoY. Shareholder returns remained strong at $4.8B ($2.5B dividends + $2.3B buybacks). The flat organic growth is the bear case worry — if Q3 continues the trend, full-year 0%–4% guidance gets squeezed.

CEO Transition — January 1, 2026

Shailesh Jejurikar became P&G's CEO on January 1, 2026, succeeding Jon Moeller (now Executive Chairman). Jejurikar spent 36+ years at P&G building the Fabric & Home Care segment (Tide, Ariel, Downy, Febreze — approximately one-third of total company revenue). April 17 will be his second earnings call as CEO — investors will be scrutinizing his tone and any strategic pivots closely.

Insider Selling — February 11–12, 2026

Executive Chairman Jon Moeller sold approximately $28.1 million in PG shares over two days — 11,036 shares at $160 on February 11 and 162,232 shares at $162.45 on February 12. Additional executive Gary Coombe sold ~$5.86 million in the same window. The stock fell 2.3% on March 4 after broader awareness of these transactions. Worth noting: Moeller himself sold shares at $160 — the exact strike of today's call trade. That's an interesting coincidence (or not).

Analyst Activity — Recent

Erste Group upgraded PG to Buy on February 18 citing attractive valuation and EPS durability. BofA raised its target to $171, UBS to $170, Citi maintained Buy at $181. Average analyst target: $170.86 — that's 11.8% above current price. Capital International Investors also increased their PG holdings by 53,506 shares (+0.9%) to a $933M total position just yesterday (March 11). Institutional accumulation is happening even as retail stays nervous.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the April 17 catalyst framework:

📈 Bull Case (20% probability)

Target: $160–$165 by April 17

How we get there:

- 💪 Q3 FY2026 earnings (April 17) beat consensus with organic volume turning positive — reversing the Q2 flat-line trend

- 🚀 Tide evo consumer adoption data surprises upside on the earnings call — early sell-through data shows strong momentum

- 💰 70th consecutive dividend increase announced alongside Q3 — income buyers rotate in aggressively

- 🌍 Macro risk-off environment drives broad rotation into consumer staples defensives — PG benefits as a safe harbor

- 📊 Stock clears $155 GEX resistance, then $157.50 — momentum builds toward the $160 gamma wall

- 🔥 Breaking $160 gamma resistance triggers dealer hedging (short gamma squeeze dynamics) — stock can accelerate above the level

This is the call buyer's thesis: ~$7 gain from $152.81 to $160 = +4.7% move to strike, or +6.1% to $162 breakeven. For PG, this is aggressive but achievable on a strong earnings catalyst.

🎯 Base Case (55% probability)

Target: $152–$156 range through April OPEX

Most likely scenario:

- ✅ Q3 earnings in-line with consensus (~$1.57 EPS, ~$20.6B revenue) — not a blowout, but no disaster either

- 📊 Organic sales modestly positive (+1%) — a slight improvement from Q2's flat but not a V-shape reversal

- ⚖️ Guidance maintained at 0%–4% organic sales growth — management stays cautious on tariffs

- 💤 Stock drifts between the $150 gamma floor and the $155 GEX resistance, finding no catalyst to break either way

- 🔄 Implied move for April OPEX points to $155-156 as the options market's fair value — stock settles near there

- 💔 The $1.1M call expires worthless or near-worthless — buyer loses most of the premium

The base case is that PG is a slow-moving defensive stock that doesn't cover 4.7% in 36 days without a specific catalyst. The call buyer loses here, but with a defined loss: just the $1.1M premium.

📉 Bear Case (25% probability)

Target: $147–$150 (test the $150 floor)

What could go wrong:

- 😰 Q3 earnings disappoint with Q3 organic volume declining further — guidance narrowed toward the bottom of the 0%–4% range

- 🏪 Consumer trade-down to private label accelerates as mid-single-digit price hikes from August 2025 erode P&G's volume base

- 🌍 Broader macro deterioration hits consumer staples multiples — tariff escalation exceeds the $1B pretax headwind already in guidance

- 📉 Insider selling overhang (Moeller's $28M exit) weighs on sentiment heading into earnings

- 💥 Stock breaks below $150 gamma support — the trampoline gives way and downside accelerates toward $147-148

Critical level: The $150 put gamma wall (19.64 GEX — strongest support in the chart) is the key line. As long as that holds, the call buyer's bet is still theoretically alive. If $150 breaks convincingly, this becomes a painful ride.

💡 Trading Ideas

🛡️ Conservative: "The Dividend Shield" — Buy PG Stock + Sell Near-Term Calls

Play: Buy 100 shares of PG around $152.50 and sell the April 17 $155 covered call for approximately $3.50

Why this works:

- 🎯 You own the defensive dividend champion outright — 3.1% yield plus 70th consecutive increase likely in April

- 💰 The $3.50 call premium reduces your cost basis to ~$149 — already at/near the $150 gamma support floor

- 📊 If stock stays flat or rallies to $155, you pocket the premium (2.3% in 36 days). If it rips to $160+, you still profit $5.50/share from entry to $155 + the $3.50 premium = $8.50 total gain (5.6% in 36 days)

- 🛡️ Defined downside cushion: even if PG dips to $147, your effective cost is $149 from the premium offset — gamma support at $150 limits the damage

- 📅 Mark your calendar: April 17 — decision point on whether to roll the covered call or take assignment

Estimated P&L:

- 📈 Stock at $155+: +$5.50 (stock) + $3.50 (premium) = +$8.50/share, +5.6% ROI in 36 days

- 🎯 Stock flat at $152.50: +$3.50 premium = +2.3% income return

- 📉 Stock at $147: Net cost $149, position down $2 = -1.3% — very manageable

Risk level: Low | Skill level: Beginner-friendly

⚖️ Balanced: "The Earnings Strangle" — Copy the Call Trade Concept, But Defined Risk

Play: Buy a PG April 17 $155/$160 call spread — buy the $155 call, sell the $160 call

Why this works:

- 💸 Cost: Approximately $1.50-2.00 net debit (versus paying $2.04 for the naked $160 call alone)

- 🎯 Max profit: $3.00-3.50 if PG trades at or above $160 on April 17 — that's a 150-175% return on the debit paid

- 📊 Breakeven: PG at approximately $156.50-157 — the stock only needs a 2.9% rally from current levels, versus the 4.7% needed for the naked $160 call

- ⚡ You benefit from any move above $155 through the $160 resistance zone — a zone that aligns perfectly with gamma resistance AND the options market's own implied move upper range for April

- 🎪 The April 17 earnings catalyst is the setup — a single-penny EPS beat and positive Tide evo commentary could push PG from $152 to $156-158 quickly

Entry timing: Consider entering now or on a dip toward $150 gamma support. Wait for a day the stock is near the floor — your spread gets cheaper and your risk/reward improves.

Estimated P&L:

- 📈 PG at $160+ on April 17: +$3.00-3.50 per spread (~150-175% gain)

- 🎯 PG at $157: +$1.50-2.00 (breakeven territory — slight gain)

- 📉 PG below $155 at expiration: Lose the ~$1.50-2.00 debit (100% loss on the spread)

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: "Follow the Whale" — The $160 Long Call (Like the Big Trade)

Play: Buy the PG April 17 $160 call outright at approximately $2.04 (same as the institutional trade — smaller size, obviously)

Why this could work:

- 💥 You're aligned with a $1.1M institutional conviction bet — someone who presumably did serious research decided this was worth 7-figures

- 🚀 Analyst consensus is Buy at $170.86 average target — Citi has a $181 target. The street sees significant upside and the call buyer is expressing the same view

- 🎰 Q3 earnings on April 17 create binary event upside: a beat + dividend hike + positive Tide evo data could gap PG 4-6% in one day

- 📊 Maximum leverage: $2.04 in premium controls $16,000 of stock. A 6% move in PG turns into a 3-4x gain on the option

- 🔥 If PG breaks $160 gamma resistance and the squeeze kicks in (dealers forced to buy), the stock can overshoot quickly to $162-165

Why this could blow up (serious risks):

- ⏰ Time is working against you immediately — theta decay burns approximately $0.04-0.05/day on this option, every single day PG doesn't move

- 💸 The options market itself is only pricing PG at ~$155-156 for April — you're fighting the implied probability

- 😱 Earnings are binary — a weak Q3 with continued flat organic growth and this call goes to zero

- 📉 At $152.81, PG needs to gain 4.7% to reach the strike and 6.1% to break even — that's a big ask for a defensive consumer staples stock in 36 days without a major catalyst

Estimated P&L:

- 📈 PG at $165 on April 17: Call worth ~$5 = +$2.96/contract (+145% gain)

- 🎯 PG at $162: Call worth ~$2.00 = ~breakeven

- 📉 PG at $158: Call worth ~$0.20 = -$1.84/contract (-90% loss)

- 💀 PG below $160 at expiration: Total loss of $2.04 premium (100%)

CRITICAL: Size this aggressively small — 1-3% of portfolio maximum. The naked long call has a high probability of expiring worthless (the market is only pricing a ~25-30% chance PG hits $160 by April 17). You're betting on a specific catalyst outcome, not a high-probability statistical trade.

Risk level: HIGH — options can and do expire worthless | Skill level: Advanced

⚠️ Risk Factors

Don't get caught flat-footed by these landmines:

-

📉 Flat organic growth could continue: Q2 FY2026 showed zero organic sales growth with -1% volume decline. If Q3 continues the trend, full-year guidance gets pressure and the stock rerates lower. At a ~24x P/E, PG has limited margin for error if organic growth disappoints for two consecutive quarters.

-

🏪 Price hike backlash risk: P&G raised prices mid-single-digit on 25% of U.S. products in August 2025 to cover a $1 billion pretax tariff burden. Consumers are already shifting to value-size packages. If trade-down to private label (Walmart's Equate, Target's Up & Up) accelerates in Q3, volume numbers could disappoint badly.

-

🌍 Tariff / trade policy escalation: The $400M after-tax tariff headwind is already baked into guidance. But consumer staples companies broadly are under tariff pressure as of early 2026. Any escalation in U.S.-China trade tensions could increase this headwind beyond what management has already quantified.

-

👔 New CEO uncertainty: Shailesh Jejurikar has been CEO for only 10 weeks as of today. April 17 is only his second earnings call. Any strategic pivot, guidance revision, or unexpected commentary from new leadership will be scrutinized under a microscope. Execution risk is elevated in CEO transition years.

-

🏦 Insider selling at $160 creates psychological resistance: Jon Moeller sold 162,232 shares at $162.45 and 11,036 shares at exactly $160.00 in February. That creates an overhead supply zone at the very strike this call is targeting. His $28.1M sale plus Gary Coombe's $5.86M sale in the same window is a significant amount of insider distribution — not a reason to panic, but worth acknowledging.

-

🌏 China / emerging market exposure: P&G generates approximately 57% of revenue outside North America. SK-II, the premium China skincare brand, suffered double-digit declines due to anti-Japanese consumer sentiment — though Q1-Q2 FY2026 showed early signs of Beauty volume recovery. Any reversal of that recovery or renewed China macro slowdown would weigh on international organic sales.

-

🛍️ Tide evo premium pricing risk: Tide evo is priced at a 54% premium to Tide Pods ($19.99 vs $12.97 for 42 units). Consumer adoption at this premium price point amid budget pressure is unproven. If Q3 earnings commentary on Tide evo sell-through is disappointing, it undermines P&G's core innovation narrative heading into FY2027.

-

⏰ Time decay works against call buyers: At $2.04, this call loses approximately $0.04-0.05 per day in theta decay. With 36 days to expiration, a stock that goes nowhere bleeds the entire premium. PG is famous for being a slow mover — that's the enemy of long calls.

🎯 The Bottom Line

Real talk: Someone just laid $1.1 million on a consumer staples stock that your mom probably thinks is too boring to talk about. That alone tells you this is worth paying close attention to.

Here's the deal: The $160 April 17 call is a very specific, very calculated bet. The buyer needs PG to rally 4.7% to the strike — and needs it to happen by Q3 earnings day. The trade is essentially saying: "I think Q3 earnings will be a positive surprise, Tide evo will show early traction, the new CEO will say the right things, and institutional rotation into defensives will push this stock through the $160 gamma wall."

That's a lot of dominoes to fall. But consider the bull case context: analysts have an average price target of $170.86, institutional capital is quietly accumulating, the company has returned $14-15 billion to shareholders annually, and a 70th consecutive dividend increase is almost certainly coming on April 17. In a choppy, macro-uncertain market, defensive consumer staples can become the go-to destination for institutional money that doesn't want tech volatility. When that rotation happens, even boring stocks like PG can move fast.

If you already own PG:

- ✅ Stay long — the $150 gamma floor is rock-solid support and the 3.1% dividend yield cushions downside

- 📊 Consider selling the April 17 $155 covered call to generate $3-3.50 in extra income while you wait for earnings

- 🎯 Mark April 17 as your key date — that's when the story either confirms or falls apart

- 💰 Resist the urge to buy the $160 calls unless you can afford to lose the entire premium

If you're watching from the sidelines:

- ⏰ A dip toward $149-150 gamma support is a compelling risk/reward entry for the stock itself

- 🎲 The balanced call spread ($155/$160) gives you earnings upside with 36 days of runway and defined risk

- 📅 April 17 before market open — Q3 earnings are the moment of truth

If you're skeptical:

- 🛡️ PG at $150 with a 3.1% dividend yield and Buy-rated by most analysts is an unusually attractive defensive entry — the bear case here is more "rangebound" than "crash"

- 📊 The $150 put gamma wall is 19.64 GEX — the single strongest support level in the chart. Shorting PG here means fighting that wall directly

Final verdict: PG is a $356B Dividend King getting an unusual $1.1M bullish call bet right into its Q3 earnings. The options market says it probably won't reach $160 — but one big buyer disagrees. With a new CEO, Tide evo launch momentum, institutional accumulation on March 11, and analyst targets averaging $170, there are real reasons to be bullish here even if $160 by April 17 is a stretch. The $150 support is fortress-level. The upside catalyst is binary (earnings beat or miss). Your job is to decide how much conviction you have — and size accordingly.

Don't bet the farm. But don't ignore the whale. 👀

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. The unusual options activity described reflects a single trade and does not guarantee any future price movement. Past performance of options strategies does not guarantee future results. The $160 April 17 call has a high probability of expiring worthless if PG does not reach $160 by expiration — you can lose 100% of any premium paid. Always do your own research, understand your personal risk tolerance, and consider consulting a licensed financial advisor before making any investment decisions. Options are not suitable for all investors due to the speculative nature and risk of loss.