🐻 PLUG — Someone Just Sold $2.2M in LEAP Calls, Betting This Stock Goes Nowhere for 11 Months!

📅 February 26, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A major player just dumped $2.2M in LEAP call options on PLUG, selling 50,000 contracts at the $2.50 strike expiring January 2027 — and they did it below the bid, meaning they wanted out fast. This is a covered call write on approximately 5 million shares, and it screams one thing: whoever owns this stock does not expect it to go above $2.50 for almost a year. With Q4 earnings dropping March 2, a suspended $1.66B DOE loan, and $800M+ in annual cash burn, this trade fits the bearish narrative like a glove.

💰 The Option Flow Breakdown

📊 What Just Happened

| Detail | Value |

|---|---|

| 📅 Date & Time | February 26, 2026 at 12:16:23 ET |

| 🏷️ Ticker | PLUG (Plug Power Inc.) |

| 📌 Direction | SELL CALL |

| 💵 Strike | $2.50 |

| 📆 Expiration | 2027-01-15 (LEAP — ~11 months out) |

| 💰 Total Premium | $2.2M |

| 📦 Size | 48,010 contracts (representing ~4.8M shares) |

| 📊 Volume vs OI | 50,000 volume vs. 7,700 OI — that is 6.5x the open interest |

| 🏷️ Option Price | $0.46 per contract |

| 📍 Spot Price | $1.88 |

| 🔴 Execution | BELOW BID (aggressive sell) |

| 🏷️ Classification | Short Call (STO) — Covered Call on ~5M shares |

🤓 What This Actually Means

Let me break this down in plain English.

Someone holding roughly 5 million shares of PLUG (worth about $9.4M at current prices) just sold call options against their position. They collected $2.2M in premium — basically agreeing to sell their shares at $2.50 if the stock ever gets there before January 2027.

Here is why this matters:

🔴 They sold BELOW the bid. That means they were not even waiting for a buyer to meet their price — they took whatever was offered. That is urgency. That is conviction.

🔴 Volume was 6.5x the open interest. This was not some regular rotation. This was a brand-new, massive position being established in a single shot.

🔴 The $2.50 strike is 33% above the current $1.88 price. Even with that buffer, they are willing to cap their upside there. Translation: they do not see PLUG going meaningfully higher for nearly a year.

🔴 $0.46 premium on a $1.88 stock means they are collecting about 24.5% in income over 11 months. That is the kind of yield you chase when you think the stock is dead money — or worse.

Real talk: this is a classic "I own this stock, it is going nowhere, let me at least get paid while I wait" play. And with PLUG's fundamentals, it is hard to argue with them.

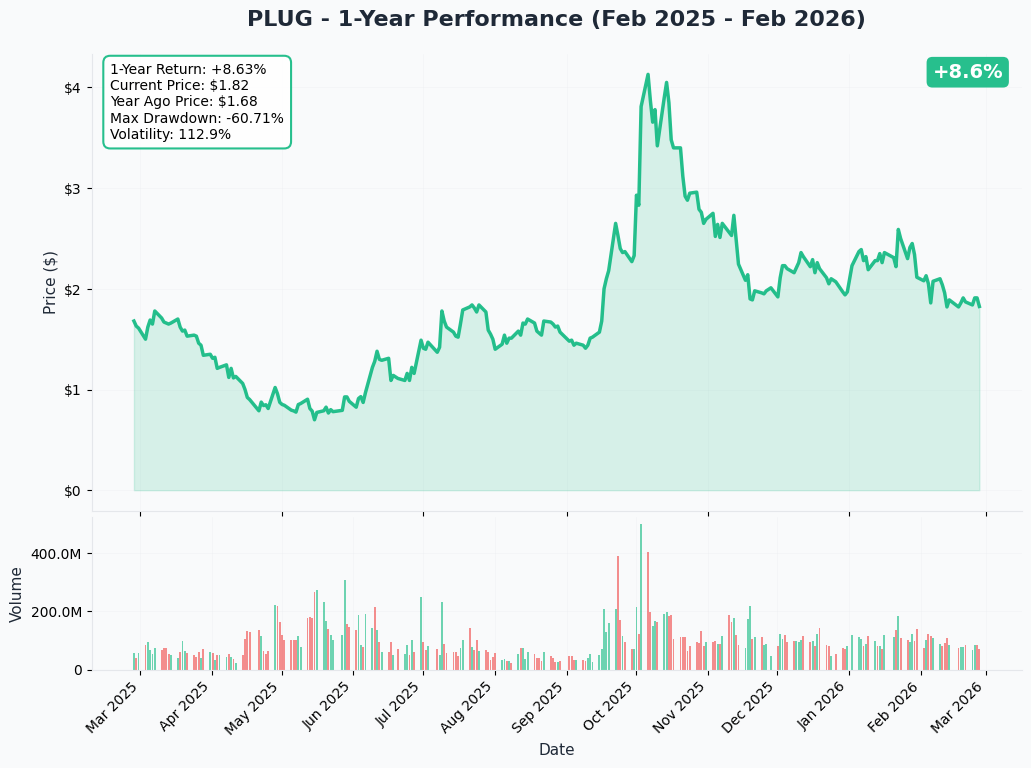

📈 Technical Setup / Chart Check-Up

YTD Chart

PLUG has been in a slow bleed since the start of 2026. The stock peaked near $2.50 in early January and has been grinding lower ever since, with each bounce getting weaker. We are now sitting at $1.83, well below the 50-day moving average, and the trend is decisively down.

The YTD picture tells a story of persistent selling pressure. Every rally attempt gets sold into, and the stock keeps making lower highs. That is not the kind of chart where you want to be buying calls.

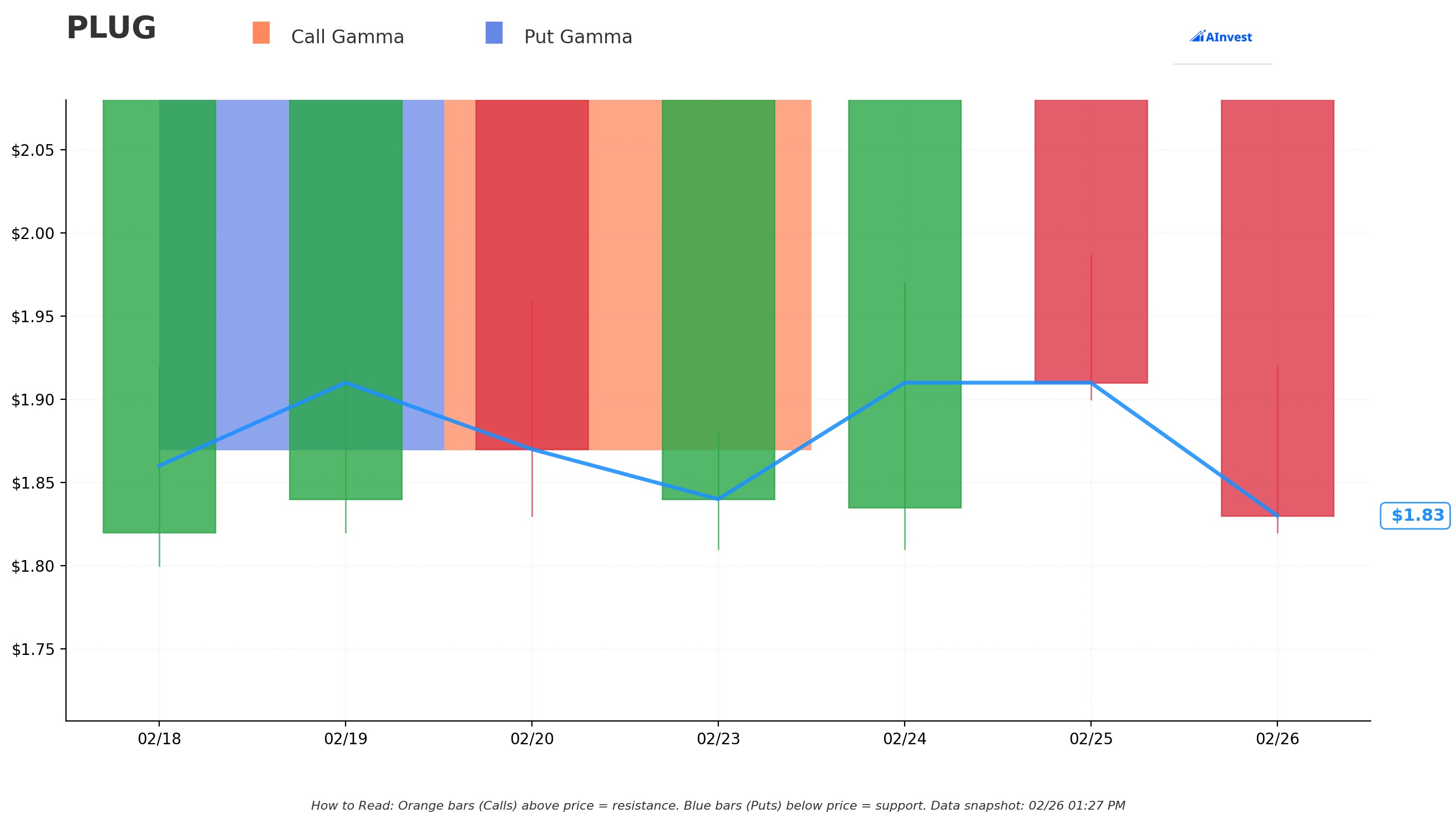

🔵🟠 Gamma-Based Support & Resistance Analysis

What the options market is telling us about key price levels:

Here is where the big options positioning sits — these levels act like magnets and walls for the stock price:

🟠 Resistance at $2.00 — This is the strongest level above the current price. The total gamma exposure here is 12.14, with call gamma of 6.84 dominating. The $2.00 strike is about 9.3% above the current $1.83 price. Think of it like a ceiling — there is a lot of options activity pinning the stock below this level. Market makers hedging here will naturally push back against rallies.

🔵 Support at $1.50 — The only real support level below, sitting about 18% lower. Put gamma of 2.66 provides some floor here, but honestly, it is thin. If PLUG breaks below $1.50, there is not much options-based support to catch it.

👀 Net GEX Bias: Bullish — Now, this sounds contradictory given everything else, but here is the nuance. The "bullish" gamma bias just means there is more call gamma than put gamma overall ($26.05 call vs. $10.13 put). This is mostly because of the sheer volume of covered call selling at higher strikes — like the exact $2.2M trade we are analyzing. It does not mean the stock is going up. It means market makers are positioned in a way that could dampen big moves in either direction.

The key takeaway: PLUG is trapped in a $1.50 to $2.00 range based on options positioning, with very thin liquidity on both sides. That is a sparse options chain for a $2.66B market cap company, and it tells you how little institutional interest there is.

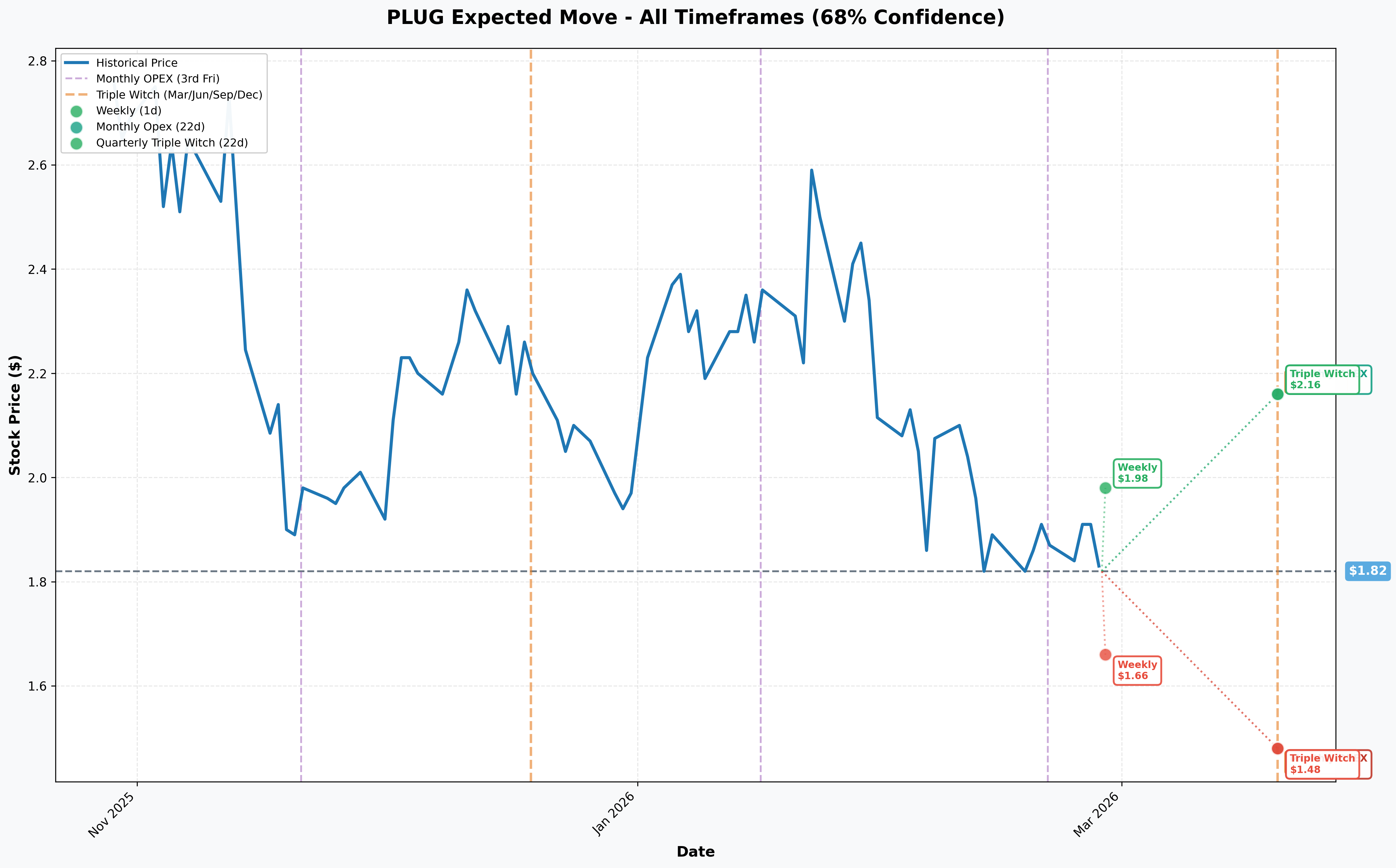

📊 Implied Move Analysis

The options market is pricing in some meaningful volatility, especially with Q4 earnings just days away:

📅 Weekly (by February 27): ±8.9% move → Range: $1.66 to $1.98 📅 Monthly OPEX (by March 20): ±18.5% move → Range: $1.48 to $2.16 📅 Triple Witch (March 20): Same range — $1.48 to $2.16

The monthly implied move reaching $2.16 on the upside still falls short of the $2.50 covered call strike. Even in the options market's best-case scenario over the next month, the stock does not reach where this seller capped their upside. That tells you how comfortable this trade is — the seller has a massive cushion.

On the downside, $1.48 is dangerously close to the only gamma support at $1.50. If earnings disappoint on March 2, a move to $1.50 or below is very much on the table.

🎪 Catalysts

⏰ Upcoming (Mark Your Calendar)

📅 Q4 2025 / Full-Year Earnings — March 2, 2026 [CRITICAL] This is the big one. Nasdaq's preview shows consensus at ~$220.7M revenue (15.3% YoY growth) and -$0.10 EPS. While Zacks gives a +41.93% Earnings ESP suggesting a possible beat, the real numbers to watch are cash burn trajectory and any going concern language in the audit opinion. With $336M cash against $991M in debt and $800M+ annual burn, the math is terrifying.

📅 CEO Transition — March 2, 2026 Andy Marsh steps down and Jose Luis Crespo formally takes over as CEO upon the 10-K filing. New CEO, new strategy — but also new uncertainty.

📅 Class Action Lead Plaintiff Deadline — April 3, 2026 Multiple law firms have filed securities fraud class actions. This deadline could escalate legal overhang.

📅 Data Center Monetization Closing — Q1/Q2 2026 (speculative) The non-binding LOI for $275M+ in liquidity from selling electricity rights was expected to close in Q1 2026. If it happens, it is a lifeline. If it does not, look out below.

📅 Q1 2026 Earnings — May/June 2026 First full quarter under CEO Crespo. Market will want proof the ship is turning.

✅ Already Happened (Recent)

📉 DOE Loan Suspension (November 10, 2025) — Plug voluntarily suspended all activities under the $1.66B DOE loan guarantee. Stock tanked 17%.

📉 Share Authorization Doubled (February 12, 2026) — After two failed votes, shareholders approved expanding authorized shares from 1.5B to 3.0B. That is massive dilution capacity with only 1.39B shares outstanding.

📉 45V Tax Credit Phase-Out Accelerated — The "One Big Beautiful Act" moved the 45V clean hydrogen tax credit phase-out to end of 2027 (originally 2033). This guts Plug's long-term hydrogen production economics.

📉 TD Cowen Downgrade (January 9, 2026) — Cut from Buy to Hold, slashed target from $4.00 to $2.00, calling 2026 a "year of reckoning for the hydrogen sector."

📉 Securities Fraud Class Actions Filed (February 2026) — Pomerantz, BFA Law, and Schall Law Firm filed suits alleging misstatements about DOE loan access.

Catalyst Score: 3/10 — High catalyst density but almost entirely negative. The Q4 earnings and data center monetization deal are the only potential positives in a sea of headwinds.

🏢 Company Overview

Plug Power Inc. (NASDAQ: PLUG) is building an end-to-end green hydrogen ecosystem — from production (electrolyzers) to storage, delivery, and energy generation (fuel cells). They are classified under Electrical Industrial Apparatus (SIC), with a current market cap of approximately $2.66B on about 1.39 billion shares outstanding.

The company has major partnerships with Walmart, Amazon, Home Depot, BMW, and BP, and recently secured a NASA liquid hydrogen supply contract. Their GenEco electrolyzer business grew 46% quarter-over-quarter in Q3 2025 to ~$65M in revenue.

But here is the problem: Plug burns through $800-900M in cash per year, has $336M in cash versus $991M in debt, and profitability is not expected until 2028 at the earliest. They raised $399M in late 2025 through convertible notes and warrant exercises just to keep the lights on. The 52-week range of $0.69 to $4.58 tells you everything about the volatility and uncertainty here.

With 30.23% short interest according to Fintel, nearly a third of the float is being bet against this company. That is not just bearish — that is one of the highest short interest readings in the market.

🎲 Price Targets & Probabilities

Based on the gamma levels, implied move ranges, and the massive catalyst calendar, here is how we see the scenarios playing out:

🐻 Bear Case — $1.00 to $1.50 (35% probability)

Target: $1.50 (gamma support) with risk of $1.00 or lower

This is the scenario where things break. If Q4 earnings on March 2 show continued massive cash burn, any going concern language from auditors, or if the $275M data center deal falls through, PLUG could easily test the $1.50 gamma support. Below that, there is essentially no options floor until much lower levels. Remember, the 52-week low is $0.69 — this stock has traded under a dollar before.

Key triggers: ❌ Disappointing Q4 earnings or raised going concern risk ❌ Data center monetization deal collapses ❌ Additional dilutive equity raise announced ❌ 45V tax credit fully repealed

⚖️ Base Case — $1.50 to $2.00 (45% probability)

Target: $1.75-$1.85 range (current area)

This is the "dead money" scenario — and it is exactly what the covered call seller is betting on. PLUG drifts sideways in the $1.50 to $2.00 range, trapped below the $2.00 gamma resistance and above the $1.50 gamma support. Earnings come and go without a disaster but also without a miracle. The covered call seller collects their 24.5% premium, the stock goes nowhere, and everyone moves on.

The implied move data supports this: the monthly range caps out at $2.16 on the upside and $1.48 on the downside, both very close to our gamma boundaries.

🐂 Bull Case — $2.00 to $2.50 (15% probability)

Target: $2.00 (gamma resistance) with a stretch to $2.16 (implied move upper)

For PLUG to rally meaningfully, you need multiple things to go right simultaneously: ✅ Q4 earnings beat with significantly improved burn rate ✅ $275M data center monetization deal closes ✅ New CEO Crespo delivers a credible turnaround plan ✅ Short squeeze ignites on the 30% short interest

Even in this scenario, the $2.00 gamma resistance is a tough wall, and the implied move only puts the upside at $2.16 by March OPEX. Getting to $2.50 (where the covered call caps out) would require a genuine paradigm shift that is not visible in the current fundamentals.

🚀 Squeeze Case — $2.50+ (5% probability)

With 30% short interest, a true short squeeze is technically possible but would need an extraordinary catalyst — think a surprise acquisition offer or a major government policy reversal on hydrogen subsidies. This is a tail-risk event, not a base case.

💡 Trading Ideas

🛡️ Conservative — "The Income Collector" (Mirroring the Whale)

Strategy: Sell March 20, 2026 $2.00 covered calls (if you already own shares) or sell $2.00 cash-secured puts

If you are already stuck holding PLUG, follow the smart money. Sell calls against your position at the $2.00 resistance level heading into earnings. You collect premium, and the $2.00 strike aligns perfectly with the gamma resistance.

Why this works: You are getting paid to wait while the stock chops around. If the stock pops on earnings, you sell at $2.00 (a ~9% gain from $1.83). If it stays flat or drops, the premium cushions your loss.

⚠️ Risk: If PLUG somehow rips past $2.00, you miss the upside. But given the fundamentals, that is a risk most people would happily take.

⚖️ Balanced — "The Earnings Straddle Sell"

Strategy: Sell March 20, 2026 $2.00 straddle (sell the $2.00 call and $2.00 put simultaneously)

With implied volatility jacked up ahead of March 2 earnings, options premiums are fat. The implied move is ±18.5% by March OPEX, which is steep for a stock trading at $1.83. If PLUG stays in its $1.50-$2.16 implied range, both sides decay in your favor.

Why this works: You are betting PLUG stays in its range — exactly what the gamma positioning and the $2.2M covered call trade suggest. You profit from the volatility crush after earnings.

⚠️ Risk: Naked put selling on PLUG means you are committed to buying a stock with serious fundamental problems if it tanks. Only do this with capital you can afford to lose. The short put side has unlimited risk to the downside.

🚀 Aggressive — "The Fade" (Bearish Directional)

Strategy: Buy March 20, 2026 $1.50 puts

If you believe the bear case — Q4 earnings disappoint, cash burn scares the market, and the stock tests its gamma support at $1.50 — cheap puts let you profit from the move. With the implied move suggesting $1.48 is within range by March OPEX, this is not a crazy bet.

Why this works: You are aligned with the institutional flow (massive covered call selling = bearish view), the fundamental picture ($800M+ cash burn, DOE loan suspended, tax credits evaporating), and the technical setup (lower highs, persistent selling pressure).

⚠️ Risk: The 30% short interest creates squeeze risk. Any positive earnings surprise or deal announcement could cause a violent short-term rally. Put premiums are elevated due to earnings, so you are paying up for the trade. If PLUG just drifts sideways, your puts expire worthless.

⚠️ Risk Factors

Let us be honest about everything that could go wrong — in both directions:

For Bears (what could cause a rally): ❗ Short squeeze potential — 30% short interest is a powder keg. Any positive surprise could trigger violent covering. ❗ Data center deal closes — If the $275M monetization actually happens, it changes the liquidity narrative overnight. ❗ Earnings beat — Zacks' Earnings ESP of +41.93% suggests a possible EPS beat. If accompanied by better-than-expected guidance, the stock could pop. ❗ Incoming CEO surprise — Crespo could announce a credible turnaround plan that the market latches onto. ❗ CFO was buying at $0.72-$1.03 — CFO Paul Middleton bought 1M shares in mid-2025. Insiders buying at lower prices does mean something.

For Bulls (what could cause further decline): ❗ Cash burn continues — At $800-900M annually with only $336M in unrestricted cash, the runway is measured in months, not years. ❗ Dilution incoming — With 3.0B authorized shares and only 1.39B outstanding, the company has room to issue another 1.6 billion shares. That is not a typo. ❗ DOE loan termination — The voluntary suspension could become permanent termination, removing PLUG's cheapest capital source. ❗ 45V tax credit gone by 2028 — The accelerated phase-out destroys the economic foundation for green hydrogen production. ❗ Class action lawsuit overhang — Securities fraud litigation adds legal costs and management distraction. ❗ "Year of reckoning" — TD Cowen and Wood Mackenzie both flagged 2026 as a make-or-break year for the entire hydrogen sector. ❗ Incoming CEO sold stock — Crespo sold 37,300 shares at $1.32 before his appointment. Not exactly a vote of confidence.

🎯 The Bottom Line

Real talk: this $2.2M covered call LEAP trade is one of the most fundamentally aligned unusual options trades we have seen in a while. It is not some speculative gamble — it is a calculated play by someone who owns 5 million shares of a stock they believe is dead money for the next 11 months. And looking at the numbers, it is really hard to disagree with them.

Here is the deal:

📌 If you own PLUG: Follow the smart money. Sell calls against your position to generate income while you wait. The $2.00 strike at gamma resistance is your natural level. Collect premium, reduce your cost basis, and protect yourself heading into a volatile earnings report on March 2.

📌 If you are watching from the sidelines: Keep watching. The risk/reward here is brutal for new longs. You have $800M+ annual cash burn, a suspended $1.66B government loan, accelerating tax credit phase-outs, potential massive dilution from 1.6B authorized-but-unissued shares, active fraud lawsuits, and a CEO transition — all for a stock trading at $1.83 with a 52-week low of $0.69.

📌 If you are bearish: The institutional money agrees with you. That said, respect the 30% short interest. Squeeze risk is real, even if the fundamentals are terrible. Size your positions accordingly and use defined-risk strategies.

📅 Mark your calendar: March 2 earnings is the next inflection point. That report will tell us whether PLUG has stabilized its cash burn or is heading toward more desperate capital raises.

The covered call seller is collecting 24.5% in premium over 11 months and betting the upside is capped at $2.50. In an environment where Wood Mackenzie calls 2026 a "year of reckoning" for hydrogen, that is a bet we would not want to be on the other side of.

⚠️ Disclaimer: This analysis is for educational purposes only and is not financial advice. Options trading involves significant risk of loss. The unusual options activity discussed represents institutional positioning and does not guarantee future price movement. Always do your own research and consider your risk tolerance before making any trading decisions. Past performance does not guarantee future results.