💰 PPLT: Someone Just Cashed Out $1.1M from Platinum's Epic Rally!

📅 December 24, 2024 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A trader just locked in $1.1 million in profits from PPLT's massive platinum rally, selling to close 571 contracts of March 2026 $210 calls! This wasn't a bearish bet - this was pure profit-taking after platinum surged over 78% year-to-date. The Z-score of 3.31 tells us this is extremely unusual activity, happening only a few times per year.

💰 The Option Flow Breakdown

📊 What Just Happened

Trade Details:

| Parameter | Value |

|---|---|

| Ticker | PPLT (abrdn Physical Platinum Shares ETF) |

| Time | 12:04:53 ET |

| Action | SELL TO CLOSE (Profit Taking) |

| Option Type | CALL - March 2026 $210 |

| Strike | $210 (3.4% above current price) |

| Premium | $1.1 Million |

| Contracts | 571 (Size 2,200 vs OI 1,400) |

| Option Price | $18.50 per share |

| Spot Price | $203.10 |

| Expiration | 2026-03-20 (Triple Witch) |

| Vol/OI Ratio | 1.57x (157% of open interest traded) |

| Unusualness | Z-Score 3.31 (Extremely Unusual) |

🤓 What This Actually Means

Translation for us regular folks:

This is a victory lap trade. Someone bought these calls when platinum was much cheaper, rode the massive 78%+ rally, and is now taking chips off the table. Let me break down why this matters:

🎯 Sell to Close = Profit Taking: The "sell to close" marker tells us the trader is exiting an existing long position, not making a new bearish bet. They're banking profits after an incredible run.

💵 $1.1M Premium: At $18.50 per share across 571 contracts (57,100 shares), this trader walked away with over a million dollars. If they bought these when platinum was around $115-130 earlier in the year, they potentially doubled or tripled their money.

📊 Volume Crushes Open Interest: With 2,200 contracts trading against just 1,400 in open interest, we're seeing 157% of the outstanding positions trade hands. That's massive turnover suggesting smart money is repositioning.

🗓️ March 2026 Timing: The March 2026 expiration (Triple Witch) gives clues about their original thesis. They expected the platinum supply deficit to persist through 2025-2026, which it did - but maybe they think the easy money has been made.

🏢 What is PPLT?

About the ETF:

PPLT is the abrdn Physical Platinum Shares ETF, one of the largest pure-play platinum investments available to retail traders. Here's what you need to know:

📦 Physical Backing: Unlike futures-based commodity ETFs, PPLT holds actual physical platinum bullion stored in JPMorgan vaults in London and Zurich. You're getting direct exposure to platinum prices without contango risk.

💰 Size & Scale:

- Net Asset Value (NAV): $200.58

- Assets Under Management: $2.89 billion

- Expense Ratio: 0.60%

- YTD Performance: +78% to +130% (sources vary)

- Premium to NAV: Currently trading at +3.72% premium

📈 2024 Performance: PPLT has been an absolute monster in 2024. Platinum surged more than 90% from Q2 2024, passing $1,900 per ounce and briefly approaching the $2,250 all-time high set back in 2008.

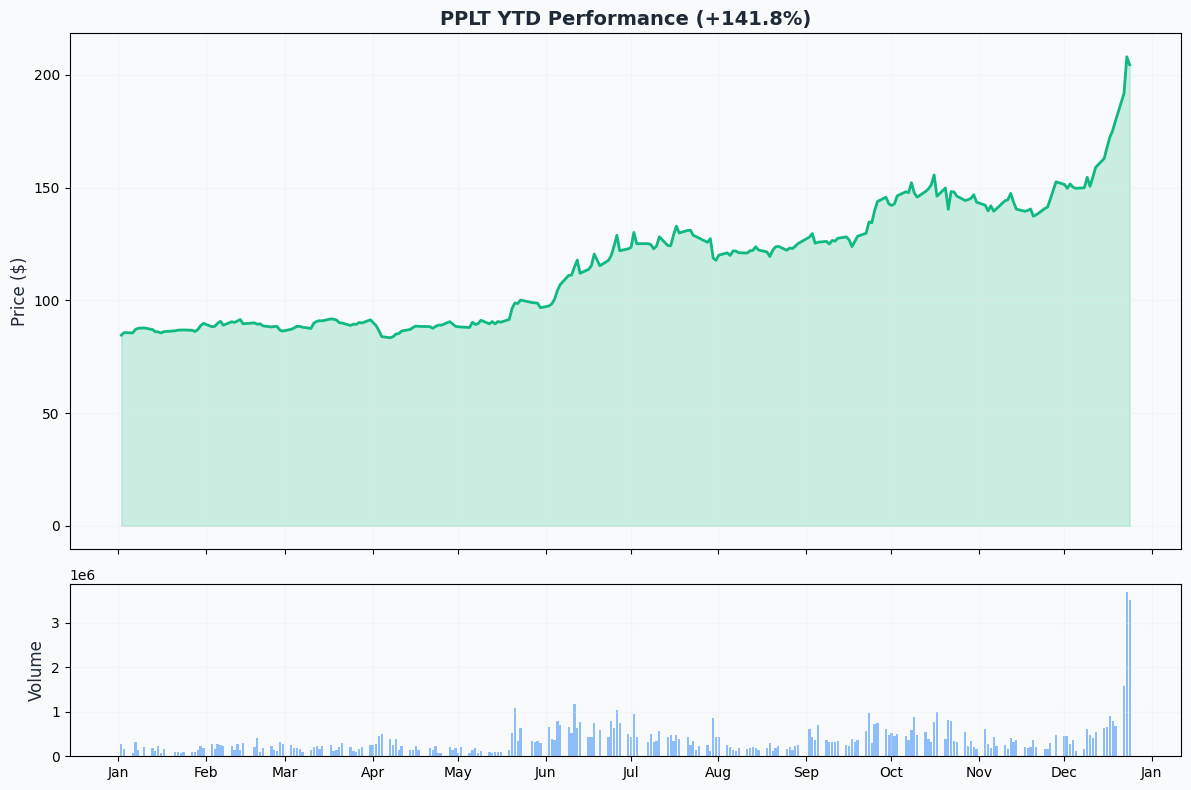

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Chart Analysis:

Look at that rocket ship! PPLT has gone from around $110 in early 2024 to over $200 by December - that's a 78-130% gain depending on your entry point. The chart shows a powerful uptrend with multiple breakouts:

✅ Early 2024 Breakout: Platinum broke above $130 resistance as supply deficit news emerged

✅ Mid-Year Acceleration: The rally intensified when China reclassified platinum as a "strategic critical mineral" in 2024, creating structural demand

✅ Q4 Explosion: Platinum passed $1,900/oz as the 995,000-ounce supply deficit (46% higher than forecast) was confirmed

✅ Recent Consolidation: After the massive rally, PPLT is consolidating around $200-204, which is perfectly normal after such a strong move

Key Observation: Despite the rally, PPLT saw $64 million in outflows in 2025, suggesting some investors (like our trader) are taking profits. Smart money is asking: "Has platinum run too far, too fast?"

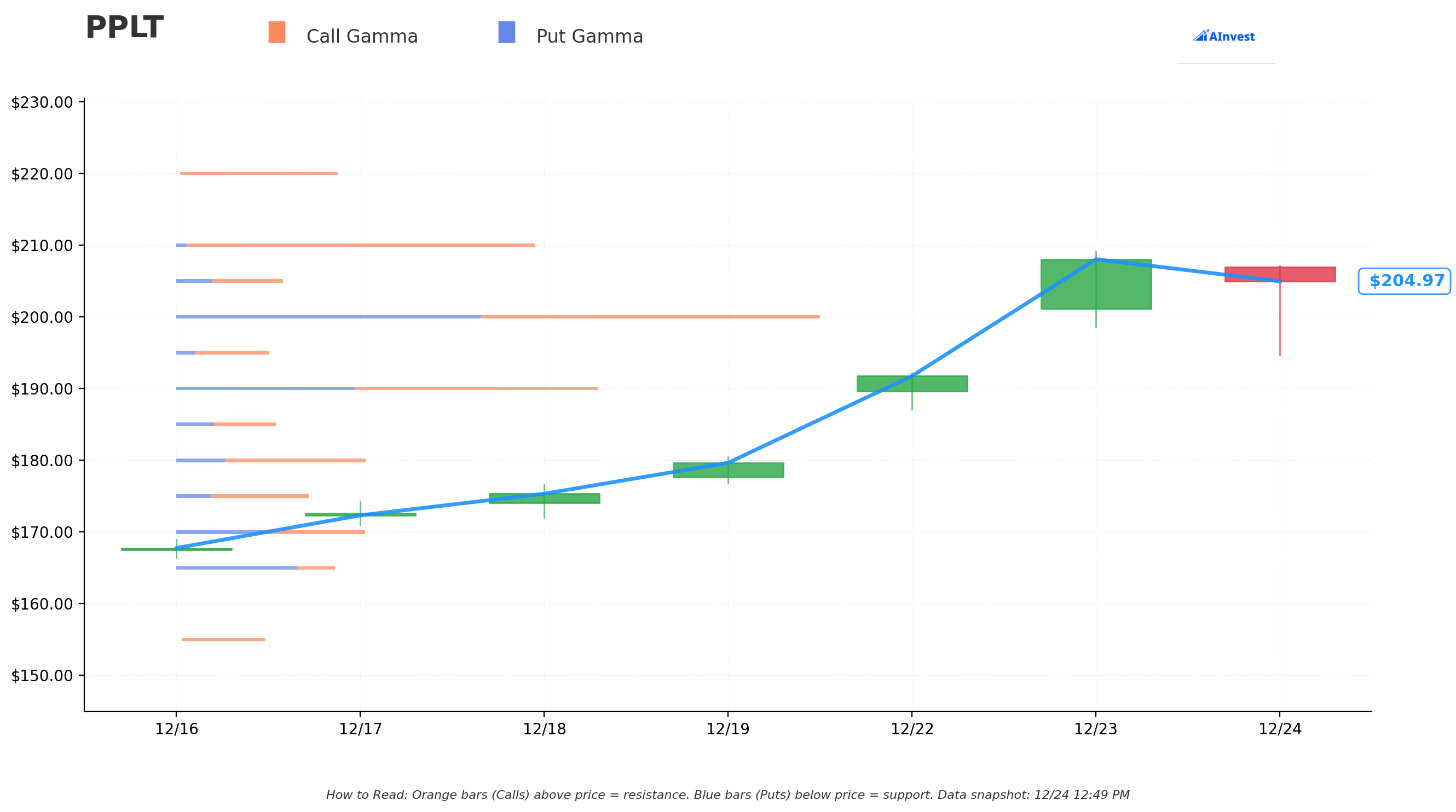

Gamma-Based Support & Resistance Analysis

Gamma Levels Breakdown:

The gamma exposure map shows where options market makers have the most risk - and therefore where price might find support or resistance. Think of these as "gravitational pull" zones created by options activity.

🔵 Support Levels (Put Gamma - Below Current Price):

1️⃣ $200 - Strongest Support (Total GEX: 0.856): This is the critical floor. With heavy call gamma (0.450) and put gamma (0.407) clustered here, market makers will fight to defend this level. If we break below $200, watch out for a flush to the next level.

2️⃣ $190 - Secondary Support (Total GEX: 0.558): A solid backstop about 7% below current price. This aligns with the recent consolidation low from November.

3️⃣ $180 - Major Support (Total GEX: 0.250): This represents the "don't panic" level - still 11.9% below current price but within the noise of a commodity ETF.

4️⃣ $170-175 Range - Deep Support: If we're testing these levels (14-17% down), the bullish thesis is breaking and profit-taking has turned into selling pressure.

🟠 Resistance Levels (Call Gamma - Above Current Price):

1️⃣ $205 - Immediate Resistance (Total GEX: 0.141): Just 0.3% above current price, this is the near-term ceiling. Options sellers are positioned here expecting consolidation.

2️⃣ $210 - Major Resistance (Total GEX: 0.475): THE big level - and notice this is exactly where our trader sold their calls! With massive call gamma (0.461), this is where market makers have the most short exposure. Breaking above $210 would trigger hedging flows that could propel PPLT to $220.

3️⃣ $220 - Extended Resistance (Total GEX: 0.216): The next major barrier at 7.6% above current price. This would represent a new all-time high for PPLT in the modern era.

Key Insight: The net GEX is bullish (total call GEX 2.94 vs put GEX 1.33), meaning more traders are positioned for upside than downside. But the concentration at $210 explains why our trader took profits there - it's a known barrier.

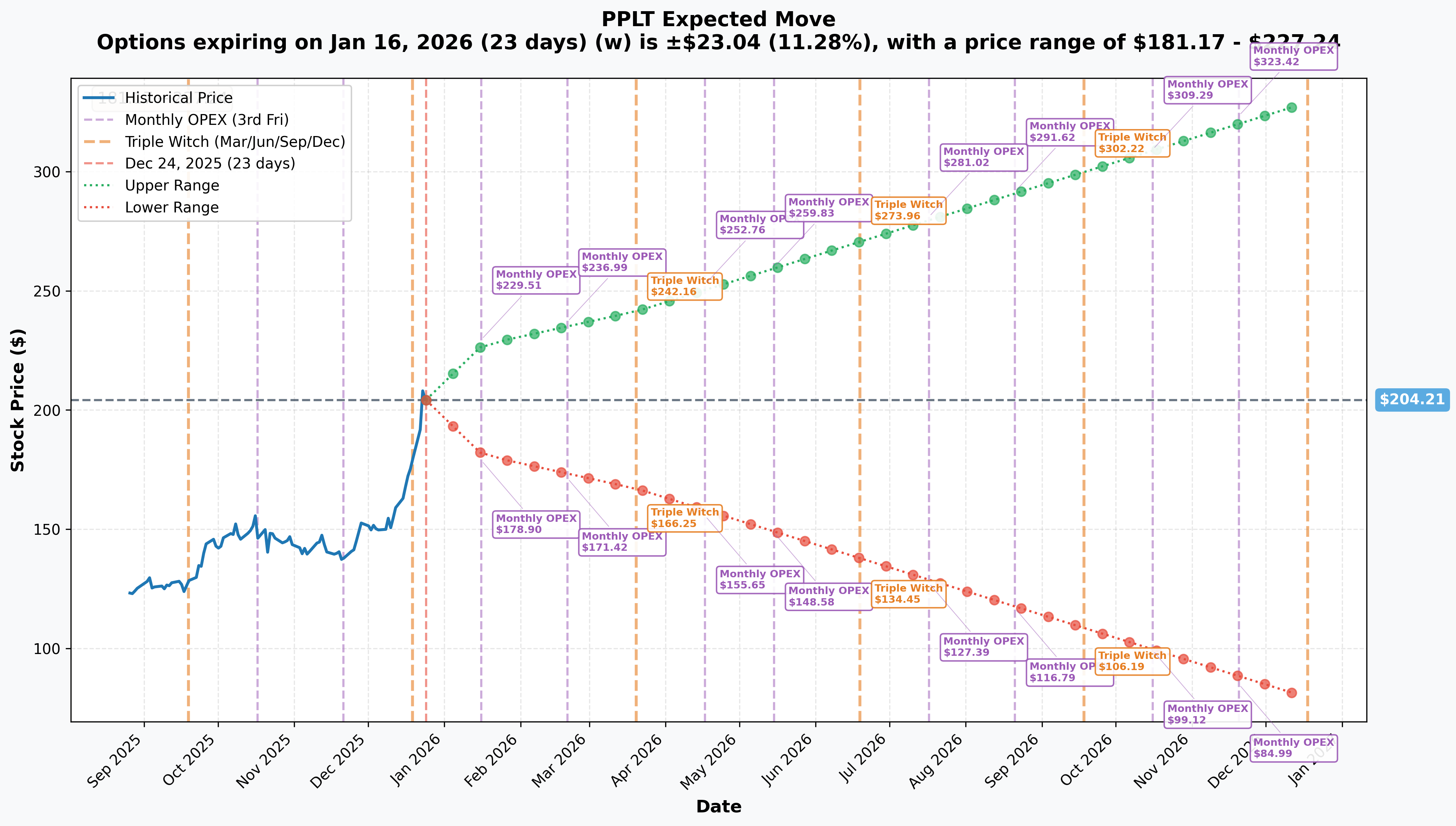

Implied Move-Based Support & Resistance

Implied Volatility Expectations:

Options market is pricing in significant moves across different timeframes. Here's what the implied volatility curve tells us:

📅 Monthly OPEX (January 16, 2026 - 23 days out):

- Implied Move: ±11.28% (±$23.04)

- Upper Range: $227.24

- Lower Range: $181.17

- Reliability: ✅ High

The market expects PPLT to trade between $181-227 over the next month. That's a $46 range on a $204 ETF - wild volatility reflecting commodity market uncertainty.

📅 Quarterly Triple Witch (March 20, 2026 - 86 days out):

- Implied Move: ±18.27% (±$37.31)

- Upper Range: $241.52

- Lower Range: $166.89

- Reliability: ✅ High

This is the expiration of our trader's calls! The market is pricing an 18% move in either direction by March. That means:

💚 Bull Case: PPLT could hit $241 (19% upside from today) 💔 Bear Case: PPLT could fall to $167 (18% downside from today)

Our trader sold $210 calls when the upper range is $241? That suggests they think the probability of breaking $210 cleanly is low, or they're happy to cap upside and bank profits.

📅 Yearly LEAPS (December 18, 2026 - 359 days out):

- Implied Move: ±61.21% (±$125)

- Upper Range: $329.20

- Lower Range: $79.21

- Reliability: ✅ High

The one-year outlook is incredibly wide - from $79 to $329. This reflects the binary nature of the platinum thesis: either the supply deficit through 2029 drives prices to new all-time highs, or global recession/EV adoption crushes demand.

Trading Implication: With such wide expected ranges, PPLT is more suitable for directional bets than premium selling strategies. Iron condors would need enormous width to be safe.

🎪 Catalysts

✅ Recent Catalysts (Already Happened - Past 3 Months)

1. Supply Deficit Confirmation (Major Bullish)

The biggest catalyst was the WPIC confirmation in March 2025 that the platinum market recorded a deficit of 995,000 ounces in 2024 - 46% higher than previously forecast. Translation: There was way more demand than supply, and everyone underestimated it.

Key details:

- Total demand exceeded 8 million ounces for first time since 2019

- Supply was only 7,293,000 ounces

- This is the third consecutive year of deficit

- Recycling at 10-year lows with limited recovery expected

2. Platinum Price Rally (Major Bullish)

Platinum surged more than 90% from Q2 2024, passing $1,900 per ounce in December. This was the second-best performing precious metal after silver, crushing gold's "mere" 58% gains.

Investment demand surged 77% year-over-year to 702,000 ounces, with platinum ETF holdings rising by 142,000 ounces in Q4 2024 alone (largely driven by US-based funds like PPLT).

3. China Strategic Mineral Classification (Structural Bullish)

China's reclassification of platinum as a "strategic critical mineral" in 2024 was a game-changer. This reflects:

- China's >95% import dependency on platinum

- Their intensifying energy transition needs

- China accounts for 29% of global platinum demand

- China became the largest market for platinum bar/coin investment globally (64% of total at 226,000 ounces)

This creates a structurally higher floor for long-term platinum demand. When the world's second-largest economy says "we need to stockpile this," you pay attention.

4. Mining Sector Restructuring (Bullish - Supply Side)

Major South African platinum miners are cutting production due to unprofitability at previous lower prices:

- Anglo American Platinum: Reduced 2024 PGM production guidance to 3.3-3.7 million ounces, down from 3.8 million, with parent company planning to demerge the platinum unit by June 2025

- Impala Platinum: Announced potential 3,900 job cuts as part of South African restructuring

- Sibanye Stillwater: Plans to cut 4,000 jobs and reduce US platinum/palladium production by ~200,000 ounces from 2025

These cuts were made when platinum was cheaper - now that prices are higher, they can't easily reverse course. Mine development takes years, creating a supply lag.

5. Automotive Demand Strength (Bullish - Demand Side)

Automotive platinum demand reached a seven-year high in 2024, growing 1% to 3,237,000 ounces despite global vehicle production being revised downward.

The driver? Platinum-for-palladium substitution reached approximately 700,000 ounces in 2024, up from 540,000 ounces in 2023. Once automakers switch a vehicle platform to platinum catalysts, that increased demand continues for the platform's entire lifespan (typically 7 years), regardless of whether palladium gets cheaper again.

🔮 Upcoming Catalysts (Next 6 Months)

1. Continued Supply Deficit Through 2025-2029 (Major Bullish)

WPIC forecasts the third consecutive year of deficit at 848,000-850,000 ounces in 2025, with deficits expected to persist through 2029.

Key projections:

- Total demand: 7.82 million ounces in 2025 (down 5% YoY but still exceeding supply)

- Total supply: 7.44 million ounces (down 4% YoY)

- Mine supply forecast to shrink 5% in 2025

- South African production constrained by electricity shortages and regulatory pressures

This is the bull thesis in a nutshell: More demand than supply for the next 4+ years.

2. Investment Demand Growth (Bullish)

Investment demand expected to grow 6% to 742,000 ounces in 2025, driven by:

- Bar and coin demand projected to increase 47% to 522,000 ounces (China alone: 418,000 ounces)

- Platinum ETF holdings forecast to rise by 70,000 ounces

- Improved sentiment following recent price breakout

The catch? We're already seeing $64 million in PPLT outflows in 2025 despite the rally. Some investors are skeptical about sustainability.

3. Automotive Sector Evolution (Mixed)

Bullish side:

- WPIC projects automotive demand will reach eight-year high of 3,245,000 ounces in 2025 (+2% from 2024)

- US policy shifts under Trump administration expected to slow BEV adoption, supporting ICE vehicle production

- Each 1% reduction in BEV market share increases PGM demand by 25,000 ounces annually

- Hybrid vehicles gaining market share, requiring higher platinum loadings due to temperature variability

Bearish side:

- 2026 automotive demand forecast to decline 3% to 2,915,000 ounces due to EV transition

- Long-term structural headwind from BEV adoption (EVs don't need PGM catalysts)

4. Hydrogen Economy Acceleration (Long-term Bullish)

This is the next-decade bull case for platinum:

- WPIC projects China's hydrogen-linked platinum demand will approach 1 million ounces per annum by late 2030s

- China aims for 1 million hydrogen vehicles and 1,000 refueling stations by 2030 (currently 28,000 vehicles, 400+ stations)

- Global hydrogen uptake forecast to increase to 875,000-900,000 ounces by 2030

- Government support across Europe, Japan, South Korea for hydrogen infrastructure

Reality check: Hydrogen adoption has been "5 years away" for the past 15 years. But China's strategic mineral classification suggests they're serious this time.

5. Industrial Demand Dynamics (Mixed - Short-term Bearish, Long-term Bullish)

Near-term headwind:

- Industrial demand forecast to fall 22% in 2025 to 1,902,000 ounces, largely due to cyclical reduction in glass demand

- Glass sector demand expected to plunge 74% to 177,000 ounces from record 2024 levels

Medium-term recovery:

- Industrial demand projected to return to growth in 2026, rising 9% to 2,076,000 ounces

- Recovery driven by chemical demand rebound and new glass capacity expansion

6. Jewelry Demand Growth (Bullish)

Jewelry demand projected to rise 7% in 2025 to 2,157,000 ounces - highest level since 2018. Drivers:

- Platinum taking market share from gold jewelry based on price discount

- China's platinum jewelry demand surged 300% year-over-year in Q1 2025

- Strong fabrication growth in India

7. Price Target Upgrades (Bullish Sentiment)

Analyst consensus is getting more bullish:

- Most analysts predict platinum will reach $1,770/oz by end of 2025 (from current ~$970/oz spot = ~$1,940 implied PPLT price)

- Bullish forecasts see $2,340/oz by 2026 (would be new all-time high)

- Conservative estimates: $1,710-$1,748 range

Note: Spot platinum is currently around $970/oz, while PPLT is $204. PPLT roughly tracks 1/5th of platinum spot price due to its structure.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move analysis, and fundamental catalysts, here are the realistic scenarios:

🐂 Bull Case - Breakout Scenario (30% Probability)

Target: $220-241 (8-18% upside)

Path: PPLT breaks and holds above $210 resistance, triggering market maker hedging flows. The March 2026 implied move upper range of $241 becomes achievable if:

✅ Supply deficit data for Q1 2025 confirms the 850,000-ounce annual deficit forecast ✅ China announces strategic stockpiling program ✅ Palladium prices surge, making platinum substitution even more attractive ✅ Hydrogen infrastructure announcements from major economies

Profit Potential: 8-18% over 3 months on shares, or 2-4x on at-the-money calls

Why it could happen: The fundamental supply/demand imbalance is real. If industrial demand recovers faster than expected and investment flows continue, platinum could make another leg higher.

Risk: Current price already reflects much of the bullish thesis. Breaking $220 would require new catalysts, not just confirmation of existing trends.

⚖️ Base Case - Consolidation with Upside Bias (50% Probability)

Target: $200-210 range (0-3% from current)

Path: PPLT grinds between gamma support at $200 and resistance at $210, consolidating the massive 78%+ YTD gain. This is healthy price action after such a strong rally.

✅ Supply deficit continues but doesn't surprise to upside ✅ Automotive demand holds steady with platinum-for-palladium substitution ✅ Investment flows moderate but remain positive ✅ Industrial demand weakness in glass sector offset by other sectors

Profit Potential: Limited on shares (0-3%), but theta decay makes this tough for option holders. Better to sell premium (covered calls, cash-secured puts) in this scenario.

Why it's most likely: After a 78%+ rally, consolidation is normal. The trader selling $1.1M of calls suggests smart money expects choppy trading near current levels. The concentration of gamma at $210 creates a natural ceiling.

Trading Strategy: Sell covered calls at $210-220 strikes to collect premium while holding shares. Or wait for a dip toward $200 support to add shares.

🐻 Bear Case - Profit-Taking Cascade (20% Probability)

Target: $180-190 (-7% to -12% downside)

Path: PPLT breaks below $200 gamma support, triggering stop-losses and momentum selling. The consolidation turns into a correction as traders who bought the rally panic.

❌ Global recession fears spike, crushing industrial demand ❌ Electric vehicle adoption accelerates faster than expected ❌ South African power supply improves, increasing mine production ❌ Palladium prices collapse, reversing platinum substitution incentive ❌ China pauses strategic mineral stockpiling ❌ Technical breakdown: Loss of $200 support leads to test of $180-190

Downside Risk: 7-12% over 1-2 months on shares. Long calls would likely see 50-100% losses as both delta and vega work against you.

Why it could happen: The $64 million in ETF outflows despite the rally is a red flag. PPLT approaching the 2008 all-time high of $2,250 (spot platinum) creates psychological resistance. Commodities can correct violently when momentum breaks.

Opportunity: If PPLT dips to $180-185 (gamma support zone), that could be a high-probability entry for patient bulls. The fundamental thesis remains intact even if we see a 10% correction.

💡 Trading Ideas

🛡️ Conservative - "Steady Eddie" Cash-Secured Puts

Strategy: Sell March 2026 $190-195 cash-secured puts

Cost/Margin: $19,000-19,500 per contract (cash secured)

Income: Approximately $8-12 per share ($800-$1,200 per contract) in premium

Rationale: You're getting paid to set a buy order 5-7% below current price at the secondary gamma support level. If PPLT dips to $190, you'd be buying at a reasonable entry with gamma support below at $185 and $180.

Why this works:

- You only get assigned if PPLT drops 7%+ - and at that point, you're buying with strong support

- Even if assigned, your effective cost basis is $190 minus premium collected ($182-187)

- If PPLT stays above $190, you keep the premium and can repeat next month

Risk Management:

- Set aside the full cash amount ($19,000-$19,500)

- Don't sell more contracts than you're comfortable owning shares

- If assigned, immediately sell covered calls at $200-210 to collect more premium

Who this is for: Investors who want to own PPLT but don't want to chase current prices. You're being patient and getting paid to wait.

Sleep Factor: 😴😴😴 You'll sleep fine. Worst case? You own platinum with 7% downside protection.

⚖️ Balanced - "Follow the Smart Money" Debit Spread

Strategy: Buy February 2026 $200 calls / Sell $210 calls (debit spread)

Cost: Approximately $4-5 per share ($400-500 per contract)

Max Profit: $5-6 per share ($500-600 per contract) = 100-150% return

Rationale: You're making the same bet as the trader who just took profits - that PPLT can reach $210 by early 2026. But instead of paying for expensive long calls, you're capping upside at $210 (where our trader sold) to reduce cost.

Why this works:

- Breakeven: $204-205 (within 1% of current price)

- Max profit at $210 resistance (exactly where gamma peaks)

- Risk/reward: Risking $4-5 to make $5-6

- February expiration gives you 2 months for the move

Scenario Analysis:

- PPLT at $205 by February: +20% to +25% profit

- PPLT at $210 by February: +100% to +150% profit (max gain)

- PPLT at $220 by February: Still +100-150% (capped at $210)

- PPLT below $200: Lose 50-100% of premium

Risk Management:

- Only risk 1-2% of portfolio on this trade

- Consider taking profits at 50-75% max gain rather than waiting for $210

- If PPLT breaks below $200, exit to avoid theta decay

Who this is for: Traders who are cautiously bullish and want defined risk. You're betting platinum can grind 3% higher to $210 but not betting on a massive breakout.

Sleep Factor: 😴😴 You'll sleep okay. Your max loss is capped at premium paid.

🚀 Aggressive - "Hydrogen Economy Believer" LEAPs Call

Strategy: Buy December 2026 $220 or $240 LEAP calls

Cost: Approximately $12-18 per share ($1,200-$1,800 per contract) for $220 strike

Max Profit: Unlimited (but realistically 2-5x if platinum reaches $2,340 target)

Rationale: You're making a long-term bet on the hydrogen economy thesis. If China, Europe, and Japan seriously build out hydrogen infrastructure in 2025-2026, platinum demand could surge beyond current forecasts. The one-year implied move of ±61% suggests the market sees potential for explosive moves.

Why this works:

- Full year to be right about the hydrogen catalyst

- If platinum reaches analyst targets of $2,340/oz by 2026, PPLT could hit $250-280

- At $250, your $220 calls would be worth at least $30 (150% gain from $12 entry)

- At $280, your $220 calls would be worth $60 (400% gain)

Why this is aggressive:

- Theta decay: You're paying for 12 months of time value

- Needs a 8-18% move just to break even

- If platinum consolidates at current levels, you could lose 50-80% due to theta decay

- Requires strong conviction in long-term platinum bull thesis

Scenario Analysis:

- Best case: China hydrogen economy accelerates, platinum supply deficit widens, PPLT hits $260+ = 300-500% gain

- Good case: Steady supply deficit, modest gains to $230-240 = 50-150% gain

- Base case: PPLT trades $200-210 range all year = 40-80% loss due to theta

- Worst case: Recession/EV adoption crushes demand, PPLT falls to $170-180 = 80-100% loss

Risk Management:

- Only allocate 2-5% of portfolio (this is a lottery ticket with better odds)

- Consider scaling in: Buy half position now, half on any dip to $195

- Take partial profits (50%) if PPLT hits $230, let the rest ride for $250+

- Set a stop-loss at 50% of initial investment if platinum thesis breaks

Who this is for: Aggressive traders with strong conviction in the platinum supply deficit and hydrogen economy. You're willing to risk losing most of your investment for a chance at 3-5x returns.

Sleep Factor: 😰😰 You'll be checking platinum prices daily. This is a high-risk, high-reward play.

⚠️ Risk Factors

Let's be real about what could go wrong:

1. The Rally May Be Exhausted 💔

PPLT has seen $64 million in outflows in 2025 despite surging 144% - that's a red flag. When prices are going up but smart money is selling, it often means the easy gains are behind us.

Risk Level: 🔴 HIGH

What to watch: If PPLT breaks below $200 gamma support on heavy volume, the rally may be over.

2. Electric Vehicle Adoption Could Accelerate 🚗⚡

While 2025 automotive demand is expected to hit an eight-year high, the 2026 forecast shows a 3% decline to 2,915,000 ounces due to EV transition.

EVs don't use PGM catalysts. If BEV adoption accelerates (better batteries, charging infrastructure, government incentives), it could crater 40%+ of current platinum demand.

Risk Level: 🟡 MEDIUM (short-term), 🔴 HIGH (5+ years)

What to watch: BEV market share reports, Tesla/BYD production numbers, charging infrastructure buildout.

3. Supply Could Recover Faster Than Expected ⛏️

GlobalData forecasts 3.6% production growth in 2025 linked to ongoing expansion at Two Rivers mine and commencement of Mareesburg project.

If South Africa's electricity crisis eases or higher prices incentivize new production, the supply deficit could narrow quickly.

Risk Level: 🟡 MEDIUM

What to watch: South African power supply improvements, new mine developments, recycling rate increases.

4. Industrial Demand Weakness 🏭

Industrial demand is forecast to fall 22% in 2025, largely due to glass sector normalization (down 74% from record 2024 levels).

If global recession hits, industrial demand could fall even further than projected.

Risk Level: 🟡 MEDIUM

What to watch: PMI data, manufacturing indices, chemical sector demand.

5. Palladium Substitution Reversal 🔄

Platinum-for-palladium substitution is already moderating as prices approach parity. If palladium prices collapse (possible if Russian supply normalizes), automakers could reverse course after 2026.

Risk Level: 🟡 MEDIUM (post-2026)

What to watch: Palladium prices, automaker catalyst specifications.

6. Hydrogen Economy Delays 🎭

Hydrogen adoption has been "just around the corner" for 15+ years. While China aims for 1 million hydrogen vehicles by 2030, they currently have just 28,000.

If hydrogen infrastructure buildout disappoints, the long-term bull case weakens.

Risk Level: 🟢 LOW (short-term), 🟡 MEDIUM (long-term)

What to watch: China hydrogen policy, infrastructure investment announcements.

7. Commodity Price Volatility 🎢

PPLT's one-year implied move of ±61% tells you everything - this is a volatile commodity. Even if the long-term thesis is correct, you could see 20-30% drawdowns along the way.

Risk Level: 🔴 HIGH (for short-term traders)

What to watch: VIX, commodity sector correlation, geopolitical events.

8. Geopolitical & Currency Risks 🌍

- South Africa political instability: 70%+ of global production comes from one country facing electricity crisis, labor unrest, regulatory uncertainty

- Russian sanctions: 10-12% of supply faces increasing restrictions

- Strong US Dollar: Platinum is dollar-denominated; if USD surges, commodity prices typically fall

- China economic slowdown: 29% of demand comes from China; if their economy stumbles, demand craters

Risk Level: 🟡 MEDIUM

What to watch: DXY (dollar index), South Africa news, China GDP reports.

🎯 The Bottom Line

Real talk: This $1.1 million option trade tells a clear story - smart money is banking profits after an incredible 78%+ rally, not making new bullish bets.

The trader who sold these March 2026 $210 calls likely made 100-300% on their position and decided that the risk/reward no longer justified holding. They looked at the same data we did:

✅ Bullish factors: Structural supply deficit through 2029, China strategic stockpiling, automotive demand at 7-year highs, hydrogen economy potential

❌ Bearish factors: Already up 78% YTD, $64M in ETF outflows, approaching 2008 all-time highs, 22% industrial demand decline expected in 2025, long-term EV headwinds

Their conclusion? Take the money and run.

📋 Here's Your Action Plan:

If You Already Own PPLT:

🎯 Trim on strength: Consider selling 25-50% of your position if you're up big. You can always buy back on a dip.

📞 Sell covered calls: Collect premium at $210-220 strikes. If called away, you bank profits at reasonable levels.

🛡️ Set stops: Protect profits with a stop-loss at $195-198 (just below $200 gamma support).

If You're Watching from the Sidelines:

⏳ Be patient: Don't chase a 78% rally. Wait for a dip to $190-195 (secondary gamma support) before entering.

💵 Sell cash-secured puts: Get paid to set your buy order 5-7% lower.

📊 Monitor catalysts: Watch for Q1 2025 supply deficit data, China stockpiling announcements, hydrogen infrastructure news.

If You're Bullish on Long-term Thesis:

🚀 Scale into LEAPs: Buy December 2026 calls at $220-240 strikes, but only allocate 2-5% of portfolio.

📅 Mark your calendar: March 20, 2026 (Triple Witch) - this is when our trader's calls expire. Monitor PPLT behavior leading up to this date.

🌐 Watch hydrogen economy: China's goal of 1M hydrogen vehicles by 2030 could drive next decade of demand.

If You're Bearish or Risk-Averse:

❌ Stay in cash: After a 78% rally, there's no shame in waiting for a better entry.

🎪 Short-term trades only: If you must play, use tight stops and small position sizes.

📉 Watch for breakdown: If PPLT breaks $200 on volume, the correction could be sharp to $180-185.

🎓 The Key Lesson

Markets don't go up forever, even with great fundamentals. The supply deficit through 2029 is real. China's strategic mineral classification is bullish. The hydrogen economy could add 1M ounces of annual demand by the late 2030s.

But timing matters. Our trader recognized that after a 78% run, it was time to de-risk. That doesn't mean the bull thesis is broken - it means the easy money has been made.

The question for you: Are you early (getting in on a multi-year supply deficit story), or are you late (buying the top of a parabolic move)?

My take: PPLT is a HOLD if you own it, WAIT for a dip if you don't. The gamma resistance at $210, combined with $64M in ETF outflows and approaching all-time highs, suggests we need consolidation before the next leg higher.

If platinum is truly in a structural bull market due to supply deficits, you'll get another chance to buy at better prices. Be patient. Protect profits. Don't chase.

⚠️ Disclaimer: Options trading involves significant risk and is not suitable for all investors. This analysis is for educational purposes only and should not be considered financial advice. The platinum market is highly volatile, and you could lose your entire investment. Past performance (like PPLT's 78% gain) does not guarantee future results. Always do your own research and consider your risk tolerance before trading. The writer may or may not hold positions in PPLT or related securities.

🔗 Helpful Links:

- PPLT ETF Page on Ainvest

- PPLT Option Chain Analysis

- WPIC: Platinum Market in Structural Deficit

- Why Structural Deficit and Hydrogen Could Boost Platinum

- China's Strategic Critical Mineral Classification

Last Updated: December 24, 2024 Data Source: ThetaData, WPIC, CME Group, ETF.com