🛡️ PRAX Massive $13.3M Put Hedge - Smart Money Buying Insurance Before Dual NDA Submissions!

📅 February 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $13.3 MILLION on PRAX puts this morning in three separate trades! This institutional-grade hedge bought a total of 2,340 contracts across $310 and $320 strikes expiring December 18, 2026 - protecting a massive position just days before Praxis files TWO NDAs (ulixacaltamide and relutrigine) expected by mid-February. With PRAX up +278.6% YTD at $304.66 and riding one of biotech's hottest pipelines, smart money is locking in downside protection at the peak. Translation: Big players are buying expensive insurance before the FDA lottery begins!

📊 Company Overview

Praxis Precision Medicines (PRAX) is a clinical-stage biopharmaceutical company focused on developing therapies for central nervous system disorders:

- Market Cap: $8.41 Billion

- Industry: Pharmaceutical Preparations

- Current Price: $304.66 (near 52-week high of $326.91)

- 52-Week Low: $26.70 (up 1,041% from low!)

- Pro Forma Cash: ~$1.5 billion (runway through 2028)

- Primary Business: Translating genetic insights into therapies for CNS disorders characterized by neuronal excitation-inhibition imbalance

Key Product Candidates:

- Ulixacaltamide - Essential tremor (NDA expected mid-February 2026, Breakthrough Therapy Designation)

- Relutrigine - SCN2A/8A developmental and epileptic encephalopathies (NDA expected mid-February 2026, Breakthrough Therapy Designation)

- Vormatrigine - Focal onset seizures (Phase 2/3 POWER1 results expected H1 2026)

- Elsunersen - Early-onset SCN2A-DEE (EMBRAVE3 Part A results expected H1 2026)

💰 The Option Flow Breakdown

📊 What Just Happened

The Tape (February 5, 2026 @ 10:28:03):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Chart |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:28:03 | PRAX | BUY | PUT | 2026-12-18 | $6.9M | $320 | 900 | 0 | 720 | $304.66 | $95.52 | PUT $320 |

| 10:28:03 | PRAX | BUY | PUT | 2026-12-18 | $3.2M | $310 | 540 | 0 | 360 | $304.66 | $89.47 | PUT $310 |

| 10:28:03 | PRAX | BUY | PUT | 2026-12-18 | $3.2M | $310 | 900 | 0 | 360 | $304.66 | $89.47 | PUT $310 |

Total Premium: $13.3 Million across 2,340 contracts

Strategy Classification: Long Put (all three trades classified as standalone Long Put positions - outright bearish/hedge play)

🤓 What This Actually Means

This is a massive defensive hedge on a substantial long position! Here's what went down:

- 💸 Huge premium paid: $13.3M total ($6.9M on $320 puts + $6.4M on $310 puts)

- 🛡️ Protection strikes: $310-$320 provides 0-5% downside cushion below current price

- ⏰ Strategic timing: December 2026 expiration captures both NDA submissions, PDUFA dates (expected Q4 2026/Q1 2027), and multiple pivotal trial readouts

- 📊 Size matters: 2,340 contracts represents 234,000 shares worth ~$71M of underlying exposure

- 🏦 Institutional insurance: All three trades executed at the SAME timestamp (10:28:03) - coordinated institutional hedging, not a bearish bet

- 📈 Zero prior OI: These are brand new positions opening, not rolling existing hedges

What's really happening here: This trader likely holds a MASSIVE long position in PRAX accumulated during the 278% YTD rally from $79.52 to $304.66. Now, with two potentially transformational NDA submissions imminent and stock near all-time highs, they're paying a whopping $95.52 per share for $320 puts and $89.47 per share for $310 puts for insurance through year-end. Think of it like buying a $13.3M homeowner's policy when you live in a mansion worth hundreds of millions - this is EXPENSIVE protection, but the downside risk justifies the cost.

Why December 2026 expiration? This timeframe covers:

- ✅ Mid-February NDA submissions (ulixacaltamide + relutrigine)

- ✅ FDA acceptance decisions (~60 days after submission)

- ✅ Potential PDUFA dates (Q4 2026 - Q1 2027)

- ✅ POWER1 vormatrigine Phase 2/3 results (H1 2026)

- ✅ EMBRAVE3 elsunersen Part A results (H1 2026)

- ✅ Q4 2025 and Q1-Q3 2026 earnings reports

Unusual Score: 🔥 HIGH - Three coordinated trades totaling $13.3M in premium on a stock with 0 prior open interest at these strikes. This is significant institutional activity - not your average retail hedge.

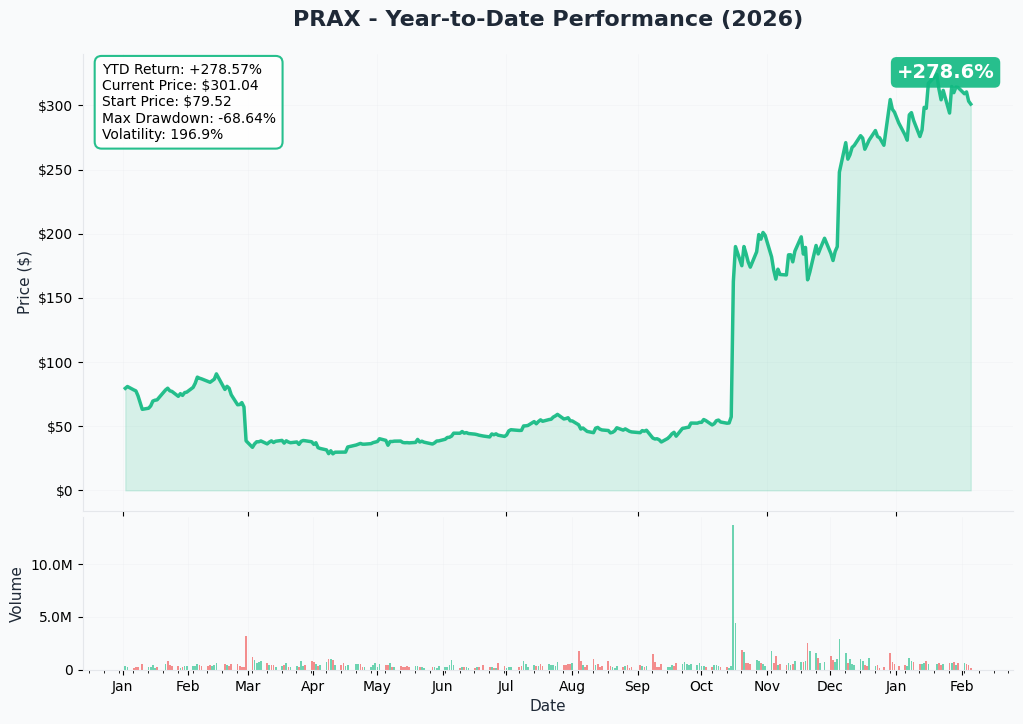

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

PRAX has been on an INCREDIBLE run - up +278.6% YTD from $79.52 to $301.04. But the chart tells a story of extreme volatility and binary events:

Key observations:

- 🚀 Parabolic rally: Stock exploded from ~$50 in October to $300+ in January on positive Phase 3 results

- 📈 Breakthrough moment: October surge from ~$60 to $190+ on Essential3 Phase 3 wins for ulixacaltamide

- 💥 January acceleration: Climbed from $190 to $300+ on BTD designation and $575M capital raise

- 🎢 Extreme volatility: 196.9% annualized vol - this is NOT a stable stock

- 📉 Max drawdown: -68.64% at one point - showing how fast biotech can turn

- ⚠️ Volume spike: Massive trading volume in October during Phase 3 results announcement

The March 2025 scare: Remember, PRAX suffered a Phase 3 futility finding in February/March 2025 that sent shares crashing 40%. The company continued with Study 2 which ultimately succeeded, but this demonstrates the binary risk inherent in biotech investing.

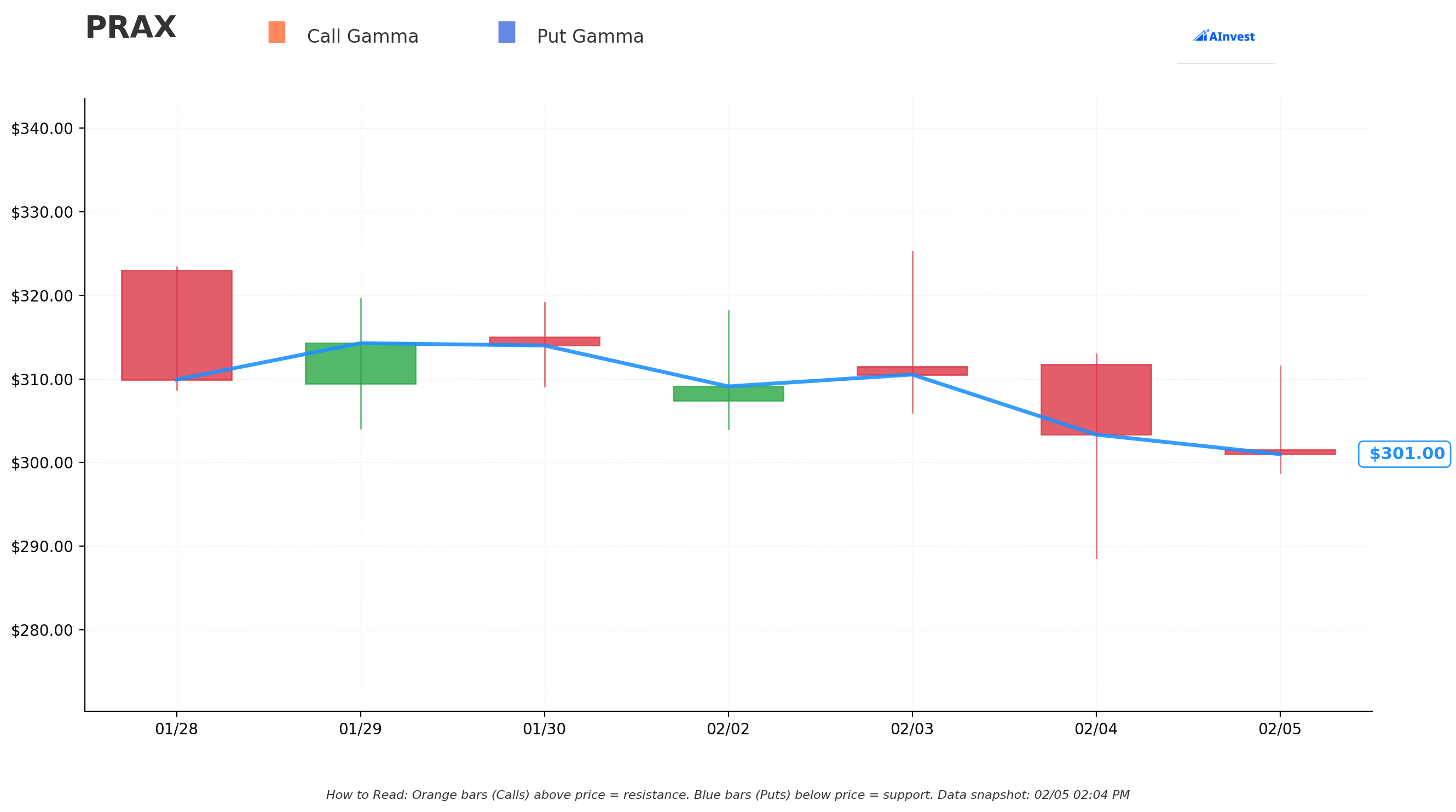

Gamma-Based Support & Resistance Analysis

Current Price: $301.00

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🟠 Resistance Levels (Call Gamma Above Price):

- $310 - First resistance with significant call gamma (1.5% above current) - aligns with put strike!

- $320 - Major resistance zone (6.3% above current) - matches the $320 put strike

- $330 - Secondary resistance (9.6% above current)

- $340 - Extended upside target (13% above current)

🔵 Support Levels (Put Gamma Below Price):

- $300 - Immediate support with 0.036 total gamma (STRONGEST nearby floor!)

- $290 - Secondary support at 0.026 gamma (3.6% below current)

- $280 - Deeper support at 0.008 gamma (7% below current)

- $270 - Major structural floor with 0.029 gamma (10.3% below current)

- $260 - Strong support at 0.032 gamma (13.6% below current) - January offering price!

What this means for traders: PRAX is trading right at the $300 gamma support level - a critical technical floor. The put buyer struck at $310 and $320, positioning just above current price - this is INSURANCE, not speculation. They're protecting against a scenario where FDA issues concerns on the NDAs and stock drops 20-40% to the $200-250 range.

Net GEX Bias: Bullish (0.189 total call gamma vs 0.142 total put gamma) - Overall positioning remains bullish, but the put buyer clearly sees significant downside risk through year-end.

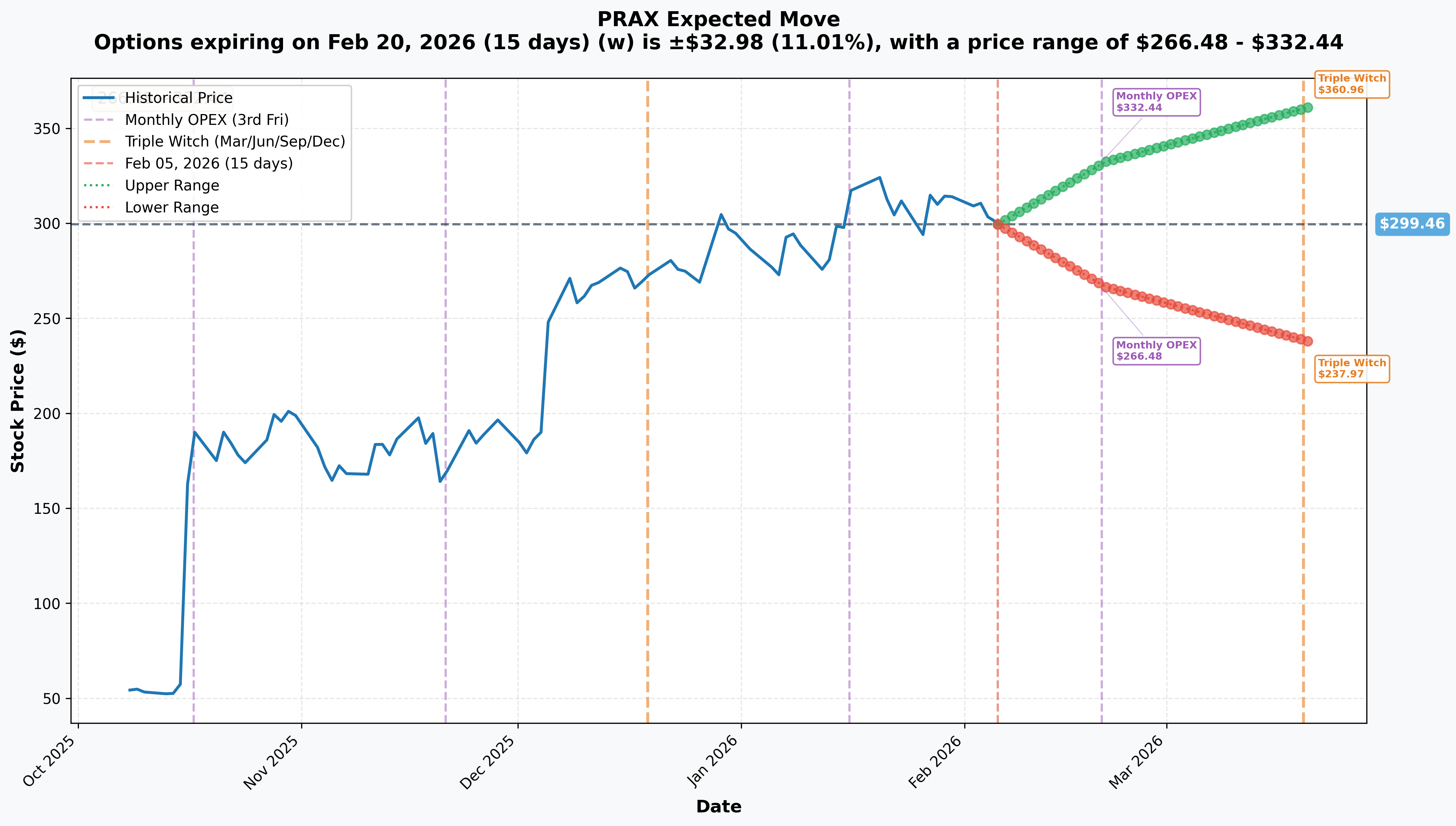

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX (Feb 20 - 15 days): ±$32.98 (±11.01%) → Range: $266.48 - $332.44

- 📅 Quarterly Triple Witch (Mar 20 - 43 days): ±$61.50 (±20.54%) → Range: $237.97 - $360.96

Translation for regular folks: Options traders are pricing in a MASSIVE 11% move ($33) through February OPEX and an even larger 20.5% move ($61.50) through March Triple Witch. This tells you the market expects FIREWORKS around the NDA submissions - for a biotech stock, this is actually reasonable given binary FDA risk.

Key insight: The implied move range of $266.48 - $332.44 for February perfectly brackets the $310 and $320 put strikes. The put buyer is positioning for a scenario where negative news sends PRAX toward the LOW END of implied range ($266.48) or below.

Why the December puts make sense: By extending to December 2026, the put buyer captures not just NDA submissions but the actual PDUFA decisions. If FDA accepts the NDAs in April (60 days after submission) and grants standard 6-month review with BTD, potential PDUFA dates would fall in Q4 2026 - exactly when these puts expire.

🎪 Catalysts

🔥 Immediate Catalysts (Next 2 Weeks)

Dual NDA Submissions - Expected by Mid-February 2026:

Per Praxis's January 12, 2026 press release, the company expects to file TWO NDAs by mid-February 2026:

| Drug | Indication | Patient Population | Designation | Peak Sales Est. |

|---|---|---|---|---|

| Ulixacaltamide | Essential Tremor | ~7 million in U.S. | Breakthrough Therapy | >$2.5B |

| Relutrigine | SCN2A/8A-DEEs | ~5,000 patients | Breakthrough Therapy | ~$650M |

Why this is HUGE:

- 🎯 Both drugs have FDA Breakthrough Therapy Designation - enables expedited review

- 📊 Successful pre-NDA meeting with FDA for ulixacaltamide confirms FDA alignment on submission

- 💊 Relutrigine showed 53% placebo-adjusted seizure reduction in EMBOLD study

- ⏰ With BTD, standard review period is 6 months from acceptance

Q4 2025 Earnings Report - March 4, 2026:

Per TipRanks, PRAX reports Q4 2025 results before market open on March 4, 2026. Key metrics to watch:

- Cash runway update (currently ~$1.5B, should last through 2028)

- NDA submission confirmations

- Clinical program updates on POWER1, EMBRAVE3

🚀 Near-Term Catalysts (Q1-Q2 2026)

POWER1 Study Topline Results - Vormatrigine (H1 2026):

Per Praxis's Q3 2025 corporate update, POWER1 Phase 2/3 study in focal onset seizures is expected to deliver topline results in H1 2026:

- 📊 Enrollment exceeded original plans due to strong clinician/patient interest

- 💊 Previous RADIANT study showed 56.3% median seizure reduction

- 🎯 22% of patients achieved 100% seizure reduction in Phase 2

- 💰 Large addressable market: millions of epilepsy patients

EMBRAVE3 Part A Results - Elsunersen (H1 2026):

FDA aligned on simplified, accelerated registrational pathway for elsunersen:

- 📋 Single-arm, baseline-controlled study design

- 🏥 Ensures all children receive active treatment from day one

- 🎯 First disease-modifying therapy potential for SCN2A-DEE

- 💊 Orphan Drug and Rare Pediatric Disease Designations

📅 Catalyst Calendar Summary

| Timeframe | Catalyst | Asset | Impact |

|---|---|---|---|

| Mid-Feb 2026 | NDA Submission | Ulixacaltamide (ET) | Very High |

| Mid-Feb 2026 | NDA Submission | Relutrigine (SCN2A/8A-DEEs) | Very High |

| Mar 4, 2026 | Q4 2025 Earnings | Corporate | Medium |

| H1 2026 | POWER1 Topline Results | Vormatrigine (FOS) | High |

| H1 2026 | EMBRAVE3 Part A Results | Elsunersen (SCN2A-DEE) | Medium-High |

| H2 2026 | POWER2 Full Enrollment | Vormatrigine (FOS) | Medium |

| Q4 2026/Q1 2027 | Potential PDUFA Dates | Ulixacaltamide/Relutrigine | Very High |

✅ Recent Catalysts (Already Happened)

December 2025 - January 2026:

- ✅ FDA granted Breakthrough Therapy Designation for ulixacaltamide (December 29, 2025)

- ✅ Successful pre-NDA meeting with FDA (December 4, 2025)

- ✅ Relutrigine NDA plans announced (December 11, 2025)

- ✅ Elsunersen FDA alignment on accelerated pathway (December 9, 2025)

- ✅ $575 million public offering priced at $260 (January 6, 2026)

- ✅ Key executive and board appointments (January 8, 2026)

October 2025:

- ✅ Essential3 Phase 3 positive topline results - stock exploded from ~$60 to $190+

- ✅ EMBOLD registrational cohort positive results - 53% seizure reduction

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through December 2026 expiration:

📈 Bull Case (30% probability)

Target: $400-$500

How we get there:

- 💪 Both NDAs accepted by FDA with no information requests

- 🚀 POWER1 vormatrigine results show best-in-disease efficacy, similar to Phase 2

- 🤖 EMBRAVE3 elsunersen demonstrates disease-modifying potential

- 📈 Analyst upgrades flow in - average price target already $374-$470 with high of $843

- 💊 PDUFA dates set for Q4 2026 with Breakthrough Therapy expedited review

- 🎯 Market assigns acquisition premium as big pharma circles for CNS assets

- 📊 Combined peak revenue estimates of $20+ billion drive multiple expansion

Key metrics needed:

- Clean NDA acceptance letters (no Refuse to File)

- POWER1/EMBRAVE3 results meeting or exceeding expectations

- No safety signals emerging from long-term extension data

- Continued strong cash position ($1.5B runway)

Probability assessment: 30% because biotech execution is inherently uncertain, but PRAX has delivered repeatedly (Essential3 Study 2 succeeded after Study 1 futility, EMBOLD exceeded expectations).

🎯 Base Case (45% probability)

Target: $280-$340 range (VOLATILE CONSOLIDATION)

Most likely scenario:

- ✅ NDAs submitted on time, accepted by FDA after standard 60-day review

- 📋 Typical FDA questions/requests during review process create uncertainty

- ⚖️ POWER1 results solid but not spectacular - market already expects success

- 📊 PDUFA dates set for Q4 2026/Q1 2027 - stock trades sideways waiting

- 🤔 Competition concerns emerge (Jazz Pharmaceuticals' suvecaltamide in development)

- 💤 Volatility compression after initial catalyst frenzy

This is the put buyer's target scenario: Stock consolidates in $280-340 range through year-end. Puts provide peace of mind but expire with limited value. The $13.3M is the "sleep well at night" premium for protecting a massive winning position.

Why 45% probability: NDA submissions are high probability but commercial success uncertain. Ulixacaltamide's high discontinuation rates due to adverse events could limit market penetration.

📉 Bear Case (25% probability)

Target: $150-$250 (PUTS PAY OFF!)

What could go wrong:

- 😰 FDA issues Refuse to File letter on one or both NDAs

- 🚨 Safety concerns emerge requiring additional clinical data

- ⏰ POWER1 vormatrigine fails to replicate Phase 2 results (remember: Phase 3 Study 1 failed before Study 2 succeeded)

- 💸 Commercial concerns: ulixacaltamide relegated to second/third-line treatment behind established therapies

- 🔬 Competitive threat: Jazz Pharmaceuticals' suvecaltamide shows superior safety profile

- 📉 Broader biotech selloff drags PRAX lower (sector funding dropped 57% in 2024-2025)

- 💰 Insider selling continues - General Counsel sold $4.85M, Adage Capital sold $33.2M

- 🔨 Break below $260 (January offering price) triggers cascade to $200-220

Critical support levels:

- 🛡️ $300: Current gamma floor - MUST HOLD or momentum shifts

- 🛡️ $260: January offering price - major psychological support

- 🛡️ $200: Extended floor if FDA disaster scenario

Put P&L in Bear Case:

- Stock at $250 on Dec 18: $320 puts worth $70, profit = -$25.52/contract (loss on premium)

- Stock at $200 on Dec 18: $320 puts worth $120, profit = +$24.48/contract ($2.4M gain on 720 contracts)

- Stock at $150 on Dec 18: $320 puts worth $170, profit = +$74.48/contract ($5.4M gain on 720 contracts)

💡 Trading Ideas

🛡️ Conservative: Wait for NDA Acceptance Clarity

Play: Stay on sidelines until FDA acceptance letters received (expected ~60 days after submission)

Why this works:

- ⏰ NDA submissions imminent but acceptance NOT guaranteed - binary risk too high

- 💸 Options EXTREMELY expensive with 197% volatility - terrible risk/reward pre-catalyst

- 📊 Stock at all-time highs after 278% YTD gain - zero margin of safety

- 🎯 Better entry likely post-NDA acceptance if stock dips on "sell the news" or FDA questions

- 📉 Historical precedent: PRAX dropped 40% on Phase 3 futility finding - binary risk is REAL

Action plan:

- 👀 Watch for NDA submission press releases (expected mid-February)

- 🎯 Look for pullback to $260-280 support zone for stock entry

- ✅ Need to see FDA acceptance letters before committing capital

- 📊 Monitor POWER1 and EMBRAVE3 readout timing for additional catalysts

- ⏰ Revisit after April when FDA acceptance status is clear

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Post-NDA Put Spread (Copy The Pros)

Play: After NDA submissions confirmed, sell put spread similar to institutional positioning

Structure: Buy $300 puts, Sell $260 puts (December 2026 expiration)

Why this works:

- 🎯 Targets support zone at $260-$300 where institutions are positioning

- 🤝 "Copies" smart money positioning at lower capital outlay

- 📊 Defined risk spread ($40 wide = $4,000 max risk per spread)

- ⏰ December expiration captures PDUFA decision timing

- 🛡️ Protects against FDA rejection or commercial disappointment scenario

Estimated P&L:

- 💰 Pay ~$15-20 net debit per spread (adjust based on timing)

- 📈 Max profit: $2,000-2,500 if PRAX below $260 at December expiration

- 📉 Max loss: $1,500-2,000 if PRAX above $300 (defined and limited)

- 🎯 Breakeven: ~$280-285

Entry timing:

- ⏰ Wait for NDA submission confirmation (by mid-February)

- 🎯 Only enter if stock trades $290+ (gives room to work)

- ❌ Skip if stock already below $270 (spread too close to at-the-money)

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Long Stock with Collar (ADVANCED ONLY!)

Play: Buy shares, sell upside calls, buy downside puts to create a protected position

Structure:

- Buy 100 shares at ~$305

- Sell 1 June $380 call (collect premium)

- Buy 1 June $260 put (protection)

Why this could work:

- 💪 Participate in bull case upside to $380 (25% gain)

- 🛡️ Protected below $260 (15% downside max)

- 💰 Call premium partially offsets put cost

- ⏰ June expiration captures NDA acceptance and early POWER1 data

- 📊 Analyst targets range $374-$470 suggest further upside possible

Risks:

- ⚠️ Stock could gap below $260 on bad FDA news before put protection kicks in

- 📉 Upside capped at $380 - if PRAX rips to $500, you miss gains above collar

- 💸 Net debit required (call premium may not fully cover put cost)

- 🎢 Extreme volatility (197%) creates execution risk

Risk level: High (levered exposure) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Binary NDA submission risk: FDA could issue Refuse to File letter if submissions incomplete or insufficient data. PRAX already experienced Phase 3 futility finding in February 2025 - execution risk is REAL. Even with Breakthrough Therapy Designation, approval is not guaranteed.

-

💊 Ulixacaltamide safety concerns: High discontinuation rates due to adverse events (dizziness, brain fog) could limit market penetration and relegate drug to second/third-line treatment. Most common TEAEs: dizziness (14.3%), constipation (9.9%), headache (8.8%), fatigue (8.8%).

-

⚖️ Jazz Pharmaceuticals competition: Suvecaltamide (JZP385) targets same T-type calcium channel mechanism. If Jazz shows better safety profile, ulixacaltamide's addressable market shrinks significantly.

-

📊 Valuation at nosebleed levels: Trading near $305 after 278% YTD gain with $8.4B market cap - stock is priced for PERFECT execution on multiple programs. Combined peak revenue estimates of $20B+ require all four drugs to succeed. Zero margin of safety at current levels.

-

📉 Historical volatility is EXTREME: 196.9% annualized volatility and -68.64% max drawdown show how fast sentiment can shift. This is a biotech rollercoaster - not a stable dividend stock. Prepare for 20-40% swings on binary news.

-

💰 Insider selling: General Counsel Alex Nemiroff sold 25,130 shares for ~$4.85M; Adage Capital sold 313,910 shares for ~$33.2M over last 6 months. While this could be tax/diversification, insider selling at all-time highs warrants monitoring.

-

🐋 Smart money buying $13.3M insurance: This institutional put purchase signals sophisticated players are WORRIED about downside despite bullish fundamentals. When funds managing hundreds of millions pay $13.3M for protection at all-time highs, it's a MAJOR caution flag.

-

🏭 Clinical pipeline risk: POWER1 and EMBRAVE3 studies still reading out in H1 2026. If vormatrigine fails to replicate Phase 2 results (56.3% seizure reduction), stock could crash 30-50%. Remember: Phase 3 failure rates in biotech are 40-50%.

-

💸 Funding environment: Biotech sector funding dropped 57% from 2024 to 2025. While PRAX has $1.5B cash, broader sector headwinds could pressure valuation multiples.

🎯 The Bottom Line

Real talk: Someone just spent $13.3 MILLION on PRAX puts protecting a massive position days before two potentially transformational NDA submissions. This isn't bearish on PRAX's long-term story - it's smart risk management by institutions who've made HUGE money on the 278% YTD rally and don't want to give it back on an FDA surprise.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY through December 2026 (not necessarily crash, but protecting against 15-30% downside scenario)

- 💰 They're worried enough about $305→$260 move to pay $89-95/share for insurance (30% of stock price!)

- ⚖️ The timing (days pre-NDA submission) shows they see binary risk - FDA could go either way with massive implications

- 📊 They structured at $310/$320 strikes (at/above current price) - this is PURE insurance, not speculation

- ⏰ December 2026 expiration captures both NDA submissions AND potential PDUFA decisions

This is NOT a "sell everything" signal - it's a "the rally has been incredible, protect your gains" signal.

If you own PRAX:

- ✅ Consider trimming 25-40% at $300-310 levels (lock in 278% YTD gains!)

- 📊 If holding through NDA submissions, set MENTAL STOP at $260 (January offering price)

- ⏰ Don't get greedy - you've already won! Up 278% YTD is EXCEPTIONAL. Protecting profits is smart.

- 🎯 If NDAs accepted AND POWER1 delivers, stock could reach $400+ - but that's 2-3 catalysts away

- 🛡️ Consider buying 1-2 protective puts per 100 shares (copy this trade's structure but smaller size)

If you're watching from sidelines:

- ⏰ Mid-February is NDA submission deadline - DO NOT enter before submissions confirmed!

- 🎯 Post-submission pullback to $260-280 would be EXCELLENT entry (15-20% off highs)

- 📈 Looking for: Clean NDA acceptance letters, POWER1 setup for H1 readout, continued $1.5B cash position

- 🚀 Longer-term (12+ months), combined $20B peak revenue potential justifies higher valuation IF execution delivers

- ⚠️ Current 197% volatility means this is a TRADER'S stock, not a buy-and-hold

If you're bearish:

- 🎯 Wait for NDA submission news before initiating shorts - fighting 278% momentum at all-time highs is dangerous

- 📊 First support at $300 (gamma), major support at $260 (offering price), deeper support at $200

- ⚠️ Post-submission put spreads offer defined-risk way to play downside

- 📉 Watch for FDA Refuse to File letter or safety signal emergence - those are the crash triggers

- ⏰ December puts like the institutional trade capture all major catalysts

Mark your calendar - Key dates:

- 📅 Mid-February 2026 - NDA submissions expected (ulixacaltamide + relutrigine)

- 📅 February 20 - Monthly OPEX (±11% implied move window)

- 📅 March 4, 2026 - Q4 2025 earnings report

- 📅 March 20 - Quarterly triple witch (±20.5% implied move!)

- 📅 April 2026 - FDA acceptance decisions expected (~60 days after submission)

- 📅 H1 2026 - POWER1 vormatrigine topline results

- 📅 H1 2026 - EMBRAVE3 elsunersen Part A results

- 📅 Q4 2026/Q1 2027 - Potential PDUFA dates for ulixacaltamide/relutrigine

- 📅 December 18, 2026 - This $13.3M put trade expires

Final verdict: PRAX's story remains INCREDIBLY compelling - dual NDA submissions with Breakthrough Therapy Designation, four late-stage assets with $20B+ peak revenue potential, and $1.5B cash runway through 2028. BUT, at $305 after 278% YTD gain with binary FDA events approaching, the risk/reward is NO LONGER favorable for aggressive new positioning. The $13.3M institutional put buy is a CLEAR signal: smart money is de-risking at the peak.

Be patient. Let NDA submissions clear. Look for better entry points $260-280. The CNS revolution will still be here after FDA acceptance letters arrive, and you'll sleep better at night paying $270 instead of $305.

This is biotech - the most binary sector in the market. Protect your capital first. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Biotech investing involves binary event risk with potential for 30-50% gaps in either direction on FDA decisions. The put buyer may have complex portfolio hedging needs not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading.

About Praxis Precision Medicines: Praxis Precision Medicines, Inc. is a clinical-stage biopharmaceutical company focused on translating genetic insights into the development of therapies for patients affected by central nervous system disorders characterized by a neuronal excitation-inhibition imbalance, with a market cap of $8.41 billion in the Pharmaceutical Preparations industry.