💳 PYPL Massive $5.8M LEAP Accumulation - Turnaround Bulls Betting Big on $80! 🚀

📅 November 6, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Institutional money just loaded up $5.8 MILLION worth of PayPal call LEAPs targeting $80 (19% above current $67), betting on CEO Alex Chriss's turnaround thesis through January 2027. These aren't short-term flips - someone's positioning for PayPal's transformation from stagnant payments dinosaur to profitable growth machine, with eyes on Fastlane acceleration, BigCommerce partnership launch in 2026, and aggressive $15B buyback program supporting 15-16% EPS growth targets. Translation: Smart money believes the turnaround is real and $80+ is achievable over the next 14 months!

📊 Company Overview

PayPal Holdings, Inc. (PYPL) was spun off from eBay in 2015 and provides electronic payment solutions to merchants and consumers, with a focus on online transactions:

- Market Cap: $63.68 Billion

- Industry: Services-Business Services

- Current Price: $67.00 (at time of trades)

- Primary Business: 434M active accounts, 36M merchants, Venmo, PYUSD stablecoin

💰 The Option Flow Breakdown

The Tape (November 6, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:51:08 | PYPL | MID | BUY | CALL | 2027-01-15 | $1.7M | $80 | 2.2K | 5.6K | 2,000 | $66.73 | $8.59 |

| 10:55:40 | PYPL | MID | BUY | CALL | 2027-01-15 | $2.1M | $80 | 4.7K | 5.6K | 2,500 | $66.83 | $8.59 |

| 11:59:30 | PYPL | MID | BUY | PUT | 2027-01-15 | $2.0M | $135 | 299 | 300 | 299 | $66.31 | $68.18 |

🤓 What This Actually Means

This is aggressive bullish accumulation on long-dated call options! Here's what went down:

- 💸 Total call premium deployed: $3.8M ($8.59 per contract × 4,500 contracts across two trades)

- 🎯 Deep out-of-the-money: $80 strike with PYPL at $67 = 19.4% upside needed

- ⏰ Extended time horizon: 434 days to January 2027 expiration - this is a LEAP position

- 📊 Substantial size: 4,500 contracts represents 450,000 shares worth ~$30M

- 🏦 Institutional conviction: This is hedge fund/family office scale positioning

- 🛡️ Potential hedge: The $135 put purchase ($2M) could be portfolio protection, not related to PYPL thesis

What's really happening here:

Someone is making a multi-year bet on PayPal's turnaround under CEO Alex Chriss who took over in late 2023. After years of stagnation (stock basically flat 2021-2024), PYPL surged 39% in 2024 as the turnaround gained traction, but still trades at just 13x P/E (vs 23x 3-year average). The $80 strike represents a reasonable multiple expansion scenario if PayPal executes on its strategic initiatives: Fastlane checkout scaling (40% faster than traditional checkout), BigCommerce partnership launching in 2026, PYUSD stablecoin expanding to 20M merchants, and $15B buyback program supporting EPS growth.

Unusual Score: 🔥 EXTREME (1,507x average size) - This happens maybe once a year! The trade size is comparable to a hedge fund initiating a material position. With 14 similar-sized trades over the lookback period occurring every ~2 days, this represents concentrated institutional accumulation.

📈 Technical Setup / Chart Check-Up

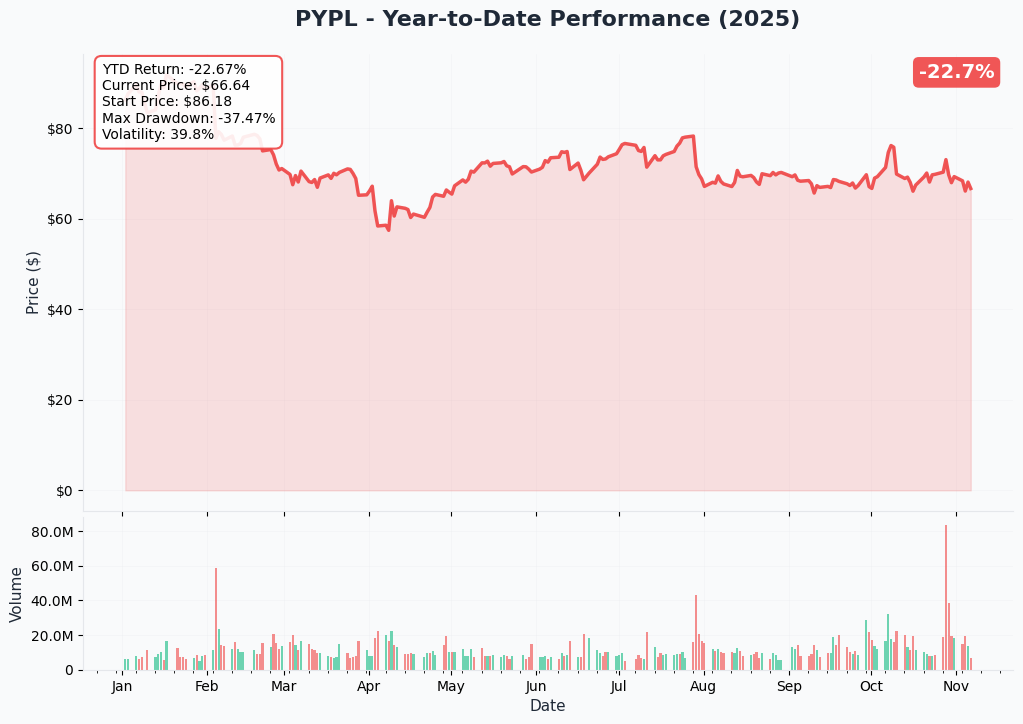

YTD Performance Chart

PayPal is showing strong recovery momentum after years of stagnation. The turnaround under CEO Alex Chriss is gaining credibility with the market.

Key observations:

- 📈 Strong 2024 performance: Up 39% in 2024, outperforming S&P 500 for first time in 3 years

- 💹 Recent consolidation: Trading around $67 after a strong run from mid-$50s in Q3 2024

- 🎢 Volatility normalizing: Stock finding support after initial surge off turnaround announcement

- 📊 Volume patterns: Institutional accumulation visible in options market aligns with stock stability

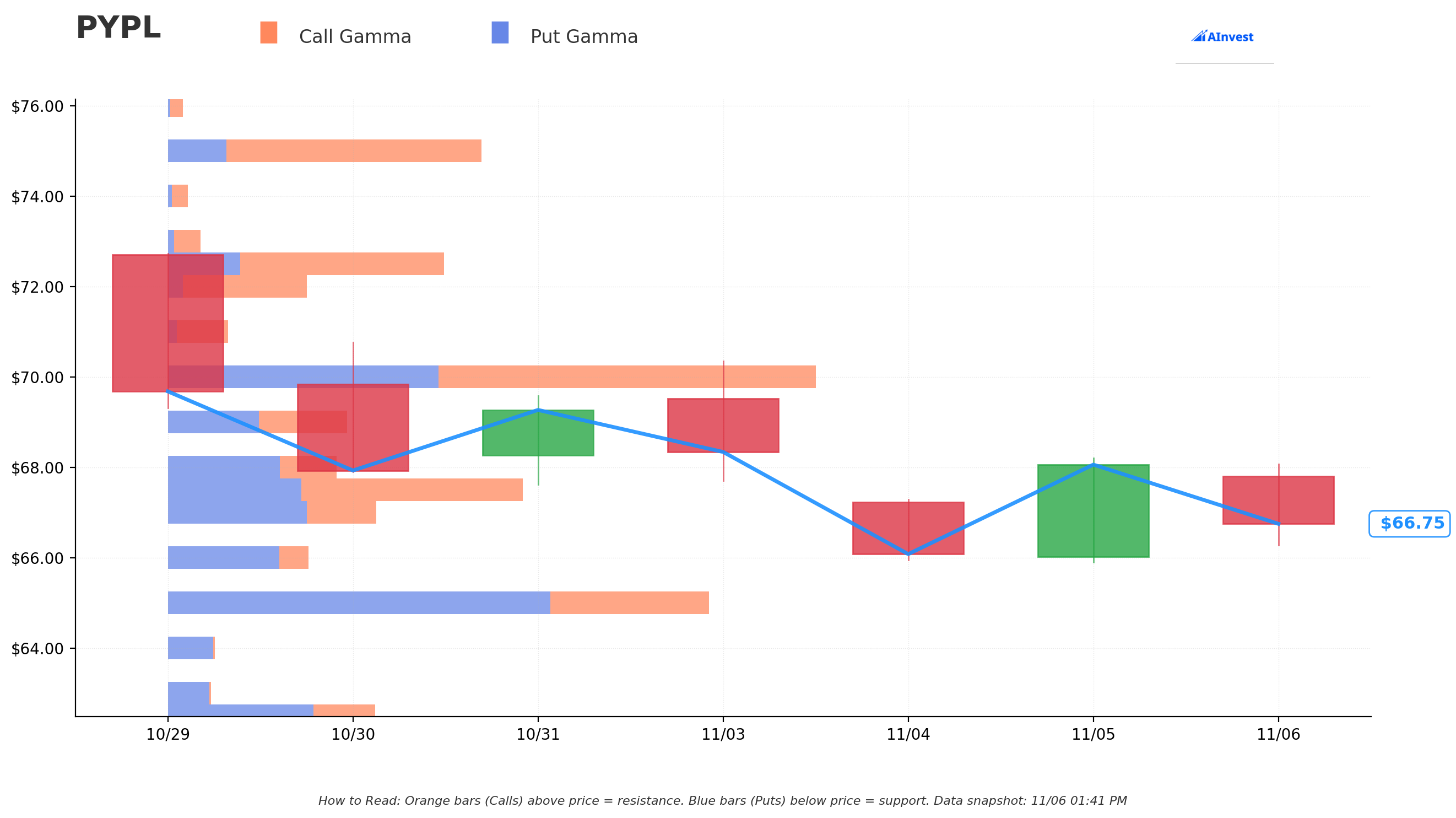

Gamma-Based Support & Resistance Analysis

Current Price: $66.79

The gamma exposure map reveals critical price magnets and walls around current levels:

🔵 Support Levels (Put Gamma Below Price):

- $65 - Strongest nearby support with 32.2B total gamma exposure (largest put wall)

- $62.5 - Secondary support at 12.4B gamma

- $60 - Deep support with 15.2B gamma (major psychological level)

- $66 - Minor support at 8.3B gamma (just below current price)

🟠 Resistance Levels (Call Gamma Above Price):

- $70 - Immediate resistance with 40.0B gamma (STRONGEST level!)

- $67.5 - Minor resistance at 21.4B gamma (just above current)

- $72.5 - Secondary ceiling at 16.7B gamma

- $75 - Major resistance zone with 18.9B gamma

- $80 - Extended target with 19.0B gamma (where the big bets are!)

What this means for traders:

PYPL is trading in a tight range between strong support at $65 and massive resistance at $70. The gamma data shows the $70 level is the KEY battleground - market makers hedging these positions will sell stock as price approaches $70, creating natural resistance. However, if PYPL breaks cleanly through $70 on strong catalyst (earnings beat, partnership announcements), next stops are $72.5, $75, and eventually the $80 target where these LEAPs are positioned. The strong put support at $65 means dealers will buy dips, creating a floor and suggesting downside is limited barring fundamental deterioration.

Net GEX Bias: Bullish (178.4B call gamma vs 134.5B put gamma) - Overall positioning leans constructive, but immediate overhead resistance at $70 needs to be cleared.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened)

Q4 2024 Earnings Beat - February 4, 2025 📊

PayPal reported strong Q4 2024 results that exceeded expectations across key metrics:

- 📊 Revenue: $8.4B (up 4% YoY, beating $8.26B consensus)

- 💰 Adjusted EPS: $1.19 (vs $1.11 consensus), beating by 7%

- 📈 Full Year 2024: Non-GAAP EPS surged 21% to $4.65 (vs $4.57 expected)

- 💵 Transaction Margin Dollars: Increased 7% to $14.7B, the most important metric showing improving profitability

- 📊 Operating Margin: Expanded 116 basis points to 18.4%, demonstrating operational leverage

What mattered: After years of margin pressure, PayPal finally showed transaction margin dollar growth acceleration under new CEO, validating the turnaround thesis.

PayPal 2.0 Investor Day - February 25, 2025 🚀

PayPal unveiled its strategic vision and medium-term targets at Investor Day in New York:

- 🎯 2027 Targets: High single-digit transaction margin dollar growth, low-teens+ EPS growth

- 🔮 Longer-term ambitions: 10%+ transaction margin dollar growth, 20%+ adjusted EPS growth

- 🛠️ PayPal Open Platform: New merchant offering enabling easy discovery and integration of commerce tools

What mattered: Management laid out clear roadmap to accelerating profitable growth, giving institutional investors confidence to make long-term bets like these $80 calls.

Q1 2025 Earnings Beat - April 29, 2025 💪

PayPal continued execution with another strong quarterly beat:

- 💰 Adjusted EPS: $1.33 (vs $1.16 consensus), beating by 15%

- 📊 Revenue: $7.79B (slight miss vs $7.85B consensus), but revenue less important than margin trends

- 💵 Transaction Margin Dollars: Grew 7% YoY to $3.72B, continuing strong trajectory

- 📈 EPS acceleration: Up 23% despite modest revenue growth, showing operational leverage

What mattered: Second consecutive quarter of solid execution, margin expansion, and EPS beats. The pattern is becoming credible.

Fastlane by PayPal General Availability - August 2024 ⚡

PayPal's Fastlane became available to all U.S. businesses in August 2024, addressing the friction in guest checkout:

- 🚀 Recognition rate: Fastlane recognizes 70% of guests

- ⚡ Speed improvement: Accelerates checkout by nearly 40% vs traditional guest checkout

- 🌍 International expansion: Partnership with J.P. Morgan Payments to offer Fastlane in UK and Europe

What mattered: Fastlane represents PayPal's answer to Stripe's superior checkout experience. Early BigCommerce data showing 70% recognition and 40% speed boost is compelling for merchant adoption.

Amazon Buy with Prime Integration - September 2024 🛒

PayPal integrated as payment option for Amazon's Buy with Prime feature:

- 🤝 Partnership details: Beginning 2025, Prime members can link Amazon accounts to PayPal

- 📈 Buy with Prime growth: Orders increased 50%, merchants seeing 16% average revenue increase

What mattered: This validates PayPal's relevance - Amazon doesn't partner with declining players. Access to Amazon's merchant ecosystem represents material upside opportunity.

PYUSD Stablecoin Expansion Progress 💎

PayPal's stablecoin PYUSD expanded to Solana blockchain in May 2024 for faster, cheaper transactions:

- 💰 Market cap: Peaked at $1.012B in August 2024, currently eighth-largest USD stablecoin at ~$630M

- 🏢 Corporate adoption: First corporate payment to Ernst & Young using PYUSD completed October 3, 2024

- 💵 Rewards program: Offering 4% yields on PYUSD holdings

What mattered: First major payments company to launch regulated stablecoin. While still small, corporate payment to EY validates real-world utility beyond speculation.

🚀 Upcoming Catalysts (Next 12-18 Months)

Q4 2025 Earnings - February 2026 📅

PayPal will report Q4 2025 (full year) results in early February 2026:

- 📊 Guidance reaffirmed: Transaction margin dollars of $15.45-15.55B (5-6% growth), non-GAAP EPS of $5.35-5.39 (15-16% growth)

- 💰 Consensus 2025 EPS: $5.01 (up 7.7% from 2024's $4.65)

- 🎯 What to watch: Whether PayPal beats guidance midpoint ($5.37 EPS) and provides strong 2026 outlook

Probability: High (80%) - PayPal has beaten earnings for 4 consecutive quarters under Chriss, establishing credible execution pattern.

BigCommerce Payments Launch - Early 2026 🤝

BigCommerce Payments powered by PayPal scheduled for U.S. launch in 2026, with international expansion to follow:

- 💼 Partnership scope: Embedded payments with advanced capabilities, simplified account management, Pay Later BNPL

- 🎯 Merchant value: Dedicated "Money" dashboard within BigCommerce Control Panel

- 💰 Revenue potential: Access to BigCommerce's SMB merchant base with embedded payment processing, competing directly with Stripe and Square

Probability: Very High (90%) - Partnership already announced, technology integration underway. Launch timing is the only uncertainty.

PYUSD Merchant Rollout - Throughout 2025-2026 💎

PayPal plans to roll out PYUSD to 20M business customers in 2025:

- 💰 Revenue potential: Stablecoin transaction fees, merchant adoption incentives

- 🎯 Market opportunity: Expanding into crypto payments market with regulated stablecoin gives competitive edge

- 📊 Current scale: ~$630M market cap, eighth-largest USD stablecoin

Probability: Medium (60%) - Technology proven (EY payment successful), but merchant adoption pace uncertain given crypto market volatility and regulatory uncertainties.

Venmo $2B Revenue Target - By 2027 🎯

Venmo targeting $2B in revenue by 2027, nearly doubling from current levels:

- 📈 Q4 2024 progress: Venmo monetized monthly active users increased 24%, Pay with Venmo TPV surged 50% YoY

- 💳 Growth drivers: Venmo debit card TPV projected to rise at 20%+ CAGR through 2027, Pay With Venmo expanding at double that rate

- 🎯 Strategic importance: Venmo is PayPal's youth brand and U.S. P2P leader

Probability: High (75%) - Early trajectory strong with 24% user growth and 50% TPV surge. Path to $2B appears credible if momentum sustains.

Share Buyback Acceleration - Ongoing Through 2027 💰

New $15B authorization announced February 2025 (in addition to $4.86B remaining from 2022 program):

- 💵 2025 plan: ~$6B in buybacks (vs $6.047B completed in 2024)

- 📊 Free cash flow support: $6.8B generated in 2024, $6B guidance for 2025

- 🎯 CFO guidance: 70-80% of free cash flow allocated to buybacks

- 💡 EPS impact: With 1B shares outstanding and $6B annual buyback at $67/share, potential to retire ~9% of float over 2 years, providing 4-5% annual EPS tailwind

Probability: Guaranteed (100%) - Already authorized and funded by free cash flow. This is happening.

⚠️ Risk Catalysts (Negative)

Competition Intensification 🥊

PayPal faces intensifying competitive pressures from multiple directions:

- 🍎 Apple Pay dominance: Growing 3-4x faster in in-app payments, ecosystem lock-in advantage

- 💳 Stripe developer capture: 27.5% revenue growth vs PayPal's 10%, winning enterprise/developer segments

- 🛒 Amazon competition: Amazon Pay expansion, potential for Buy with Prime to internalize payment processing

- 📊 Market share dynamics: PayPal at 43.4% U.S. share vs Stripe at 20.8%, but Stripe growing faster

Transaction Loss Rate Spike 💸

Recent quarters showed concerning fraud/loss trends:

- 📈 Loss rate surge: Spiked 37.5% YoY (from 0.08% to 0.11% of TPV)

- 💔 Margin impact: Core transaction margin dropped 0.6% to 46.0%

- ⚠️ Take rate compression: Blended take rate declined to 1.86% from 1.91% YoY in Q3 2024

Regulatory Headwinds ⚖️

CFPB oversight expansion in November 2024 treating digital wallets like banks creates compliance costs and operational constraints.

Active Account Growth Slowdown 📉

Only 2.1% growth in 2024, well below historical rates. Difficulty attracting younger users vs Apple Pay and even Venmo represents long-term concern.

🎲 Price Targets & Probabilities

Using gamma levels, turnaround execution metrics, and upcoming catalysts, here are the scenarios:

📈 Bull Case (35% probability)

Target: $80-$92

How we get there:

- 💪 Q4 2025 earnings beat with transaction margin dollars hitting $15.5B+ (high end of guidance)

- 🚀 BigCommerce Payments launches successfully in Q1 2026 with strong merchant adoption

- 📱 Fastlane adoption accelerates as more merchants see 70% recognition rate and 40% speed boost

- 💰 $6B+ buyback execution reduces share count materially, driving EPS above $5.50 for 2025

- 💎 PYUSD reaches 5M+ merchants, generating incremental revenue

- 📊 Multiple expansion from 13x to 16-17x P/E as market re-rates turnaround: 16x × $5.37 EPS = $86, or 16x × $5.79 (2026E) = $93

Key catalyst: Successful BigCommerce launch in Q1 2026 combined with Fastlane momentum creates narrative of "PayPal winning back relevance" that justifies multiple expansion. Buyback-driven EPS beats every quarter reinforce execution credibility.

Breakout levels: Need to clear gamma resistance at $70 (40B), then $75 (18.9B), to reach $80 target (19.0B). Would require sustained buying pressure and positive catalyst chain.

🎯 Base Case (45% probability)

Target: $70-$78 range

Most likely scenario:

- ✅ Solid Q4 2025 earnings meeting guidance midpoint (EPS $5.35-5.39)

- 🤝 BigCommerce partnership launches but adoption pace moderate in early quarters

- ⚡ Fastlane continues scaling but doesn't become game-changer in 2025-2026 timeframe

- 💰 Buyback program proceeds as planned ($6B annually), providing steady EPS support

- 💎 PYUSD makes progress but stays niche (1-2M merchants by end 2026)

- 📊 Multiple expansion to 14-15x P/E from current 13x as execution continues: 14.5x × $5.37 = $78

- 🔄 Trading between strong gamma support at $65 and resistance at $70-75 range

This is the realistic scenario: Turnaround is real, but pace is gradual rather than explosive. PayPal executes on initiatives, margin expansion continues, buybacks support EPS growth, but competitive headwinds prevent dramatic re-rating. Stock grinds higher to $70-78 range by Jan 2027, making these $80 calls finish near-the-money or slightly in-the-money.

📉 Bear Case (20% probability)

Target: $55-$65

What could go wrong:

- 😰 Q4 2025 earnings miss or weak 2026 guidance disappoints at current valuation

- 🥊 Competitive pressures intensify: Apple Pay continues 3-4x growth, Stripe takes more enterprise share

- 💸 Transaction loss rates remain elevated, pressuring margins below guidance

- 🐌 Active account growth stays anemic at 2%, raising concerns about long-term relevance

- ⚖️ CFPB regulatory compliance creates unexpected costs

- 🤝 BigCommerce integration delays or merchant adoption disappoints

- 📉 Broader fintech/payments sector selloff drags all names lower

- 🛡️ Key support: Strong put gamma at $60-65 should limit downside unless fundamentals deteriorate significantly

Important note: Even in bear case, these $80 calls have 14 months to expiration. If PayPal trades $55-65 through most of 2025 but executes well, could still rally to $75-80 in late 2026 on multiple expansion. Time is on the buyer's side.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put Strategy

Play: Sell cash-secured puts to get paid while waiting for better stock entry

Structure: Sell $65 puts, 60-90 day expirations (Dec 2025, Jan 2026, Feb 2026)

Why this works:

- 💰 Collect premium from elevated volatility around earnings and catalysts

- 🎯 $65 strike aligns with strongest gamma support (32.2B gamma) - high probability of staying above

- 📊 If assigned, buying at $65 represents good entry (3% below current, 23% below $80 target)

- ⏰ Can repeat 3-4 times before Jan 2027 expiration, accumulating income while waiting

- 🛡️ Downside protection: Only take assignment if willing to own PYPL for turnaround

Estimated P&L (current market conditions):

- 💰 Collect ~$2-3 premium per contract per cycle ($200-300)

- 📈 Max profit: Keep all premium if PYPL stays above $65 at expiration

- 📉 Assignment risk: Buy 100 shares at $65 if stock drops (must have $6,500 cash per contract)

- 🎯 Effective entry: $65 - $2.50 premium = $62.50 basis if assigned

Risk level: Moderate (capital required) | Skill level: Intermediate

⚖️ Balanced: Bull Call Spread (Lower Cost Than Naked Calls)

Play: Buy bull call spread targeting $75-80 range through mid-2026

Structure: Buy $70 calls, Sell $80 calls (June 2026 expiration)

Why this works:

- 📊 Defined risk spread ($10 wide = $1,000 max loss per spread)

- 🎯 Targets clearing $70 resistance (40B gamma) and reaching $80 where big money positioned

- ⏰ 7 months to expiration captures Q4 2025 earnings, BigCommerce launch, multiple quarterly updates

- 💰 Much cheaper than buying naked calls ($3-4 debit vs $8.59 for 2027 LEAPs)

- 📈 Captures most of the upside move ($70→$80) without paying for deep out-of-the-money time premium

Estimated P&L (adjust based on current prices):

- 💰 Net debit: ~$3-4 per spread (pay $7-8 for $70 calls, collect $4 for $80 calls)

- 📈 Max profit: $600-700 if PYPL at/above $80 at June 2026 expiration (175-233% return)

- 📉 Max loss: $300-400 if PYPL below $70 (defined and limited)

- 🎯 Breakeven: ~$73-74 (need ~8% move from current levels)

Entry timing: Now or on pullbacks to $65-66 support levels

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Follow The Smart Money - Long Dated Calls (HIGH RISK!)

Play: Replicate the institutional trade with smaller position

Structure: Buy $80 calls (Jan 2027 expiration)

Why this could work:

- 🐋 Following footsteps of sophisticated institutional buyer who just deployed $3.8M

- ⏰ 14 months provides multiple chances for thesis to play out: Q4 2025, full 2025, Q4 2025 earnings cycles

- 📊 Captures all major catalysts: BigCommerce launch, Venmo scaling to $2B, $15B buyback execution, PYUSD expansion

- 💰 At 13x P/E (vs 23x 3-year average), multiple expansion to 16x on $5.37 EPS = $86 target

- 🎯 Analyst consensus $93.62 average target suggests $80 is reasonable intermediate goal

- ⚡ Theta decay manageable with 14 months - only loses ~$0.20/month initially

Why this could blow up (SERIOUS RISKS):

- 💥 Total loss possible if PYPL stays below $80 through Jan 2027 expiration

- 🥊 Competitive pressures from Apple Pay and Stripe could prevent multiple expansion

- 💸 Transaction loss rates spiked 37.5% - if this continues, margins suffer

- 📉 Active account growth only 2.1% raises long-term relevance questions

- ⚖️ Regulatory headwinds from CFPB oversight expansion

- 🐌 Turnaround could take longer than expected - 14 months might not be enough time

- 💰 Current $8.59 option price = $859 per contract at risk

Estimated P&L:

- 💰 Cost: $8.59 per contract ($859 per contract)

- 📈 Max profit: UNLIMITED above $80 (every $1 move = $100 profit per contract)

- 📉 Max loss: $859 per contract if PYPL below $80 at Jan 2027 expiration (100% loss)

- 🎯 Breakeven: $88.59 (need 32% move from current $67)

- 💡 Profit zones: $80-88 = partial profit, $90+ = excellent returns (2-3x), $100+ = home run (4-5x)

Position sizing: Risk only 1-2% of portfolio (e.g., $1,000-2,000 max = 1-2 contracts)

Risk level: EXTREME (100% loss possible) | Skill level: Advanced only

⚠️ WARNING: DO NOT attempt this trade unless you:

- Can afford to lose 100% of the premium paid

- Understand turnaround thesis could take years, not months

- Have conviction in PayPal's strategic initiatives and management execution

- Won't panic sell on short-term volatility

- View this as high-conviction speculation, not core portfolio holding

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🥊 Competition intensifying from all directions: Apple Pay growing 3-4x faster in in-app payments with ecosystem lock-in advantage. Stripe growing 27.5% vs PayPal's 10% and winning enterprise/developer segments. Amazon could internalize Buy with Prime payments. One bad quarter showing market share loss could reset stock lower.

-

💸 Transaction loss rate spike threatening margins: Spiked 37.5% YoY (from 0.08% to 0.11% of TPV), contributing to 0.6% drop in core transaction margin to 46.0%. If fraud/loss trends continue, could pressure transaction margin dollar growth below guidance, undermining entire turnaround thesis.

-

📉 Active account growth anemic: Only 2.1% growth in 2024, well below historical rates. Difficulty attracting younger users vs Apple Pay raises existential questions about long-term relevance in evolving payments landscape. Network effects weaken if user growth stalls.

-

⚖️ Regulatory compliance costs rising: CFPB oversight expansion in November 2024 treating digital wallets like banks creates unexpected compliance costs and operational constraints. Could pressure margins and slow innovation.

-

🐌 Turnaround execution risks: BigCommerce integration complexity could delay 2026 launch or limit merchant adoption. PYUSD merchant rollout to 20M targets faces crypto market volatility and merchant hesitation. Fastlane adoption competing with Stripe, Shopify solutions. Any stumble on major initiatives resets timeline.

-

💰 Valuation trap risk: Just because PYPL trades at 13x P/E (vs 23x 3-year average) doesn't guarantee multiple expansion. Market might be correctly pricing in structural growth challenges. Could stay at 13-14x if execution doesn't improve. Would need to reach $6+ EPS just to hit $80 at current multiple.

-

📊 Time decay on long-dated options: While these Jan 2027 LEAPs have 14 months, theta decay accelerates in final 6 months. If stock is still at $67-70 by July 2026, option value could drop 30-40% even with time remaining. Need meaningful upside move in first 6-9 months.

-

🎢 Earnings volatility creates whipsaw risk: PayPal can move 5-10% on quarterly results. If you're long options, one disappointing quarter could wipe out 20-30% of position value overnight. Need stomach for volatility and conviction to hold through temporary setbacks.

🎯 The Bottom Line

Real talk: Someone just bet nearly $4 million that PayPal's turnaround under CEO Alex Chriss is real and the stock can hit $80+ by January 2027. This isn't a short-term flip - it's a conviction bet on the company's multi-year transformation from stagnant payments dinosaur to profitable growth machine.

What this trade tells us:

- 🎯 Sophisticated institutional player believes PayPal can achieve high single-digit transaction margin dollar growth and low-teens EPS growth through 2027

- 💰 The $80 strike represents reasonable 16x P/E on $5.00 EPS, below historical 23x average but fair given execution risks

- ⚖️ Risk/reward favorable at 13x current P/E with 4 consecutive quarters of beats, improving margins, and $15B buyback tailwind

- 📊 14-month timeline captures major catalysts: Q4 2025 earnings, BigCommerce launch, Venmo scaling, PYUSD expansion

If you own PYPL:

- ✅ Hold your position if you bought sub-$60 - turnaround thesis gaining traction

- 📊 Consider trimming 25-30% if cost basis above $70 to reduce exposure

- ⏰ Key test coming with Q4 2025 earnings in February 2026 - will guide for full year 2025

- 🎯 If earnings beat with transaction margin dollars above $15.5B and strong 2026 outlook, $75-80 becomes realistic near-term target

- 🛡️ Set mental stop at $60 (major gamma support at $60-65) if fundamentals deteriorate

If you're watching from sidelines:

- 💡 Current $67 level is reasonable entry for patient, long-term investors

- 🎯 Better opportunistic entry on pullback to $62-65 gamma support zone (strong 32B put wall at $65)

- ⏰ Wait for Q4 2025 earnings in February 2026 to confirm execution trajectory before committing large capital

- 📈 Looking for confirmation that BigCommerce partnership launches smoothly, Fastlane adoption accelerating, and transaction margin trends sustaining

- ⚠️ Turnaround theses take time - be prepared to hold 12-24 months minimum

If you want options exposure:

- 🛡️ Conservative players: Sell cash-secured $65 puts, collect premium while waiting for better stock entry

- ⚖️ Balanced approach: Buy $70/$80 bull call spreads (June 2026) for defined-risk exposure to upside

- 🚀 Aggressive speculators: Small position in $80 Jan 2027 calls (1-2% of portfolio max) following institutional footsteps

- ⚠️ Size appropriately: Options can go to zero - only risk capital you can afford to lose completely

Mark your calendar - Key dates:

- 📅 February 11, 2026 - Q4 2025 (full year) earnings report

- 📅 Early 2026 - BigCommerce Payments powered by PayPal U.S. launch

- 📅 Throughout 2025 - PYUSD rollout to 20M business customers

- 📅 By End 2027 - Venmo targeting $2B revenue milestone

- 📅 January 15, 2027 - Expiration date for these $3.8M call LEAPs

Final verdict: This is a high-conviction turnaround bet on PayPal's ability to reignite profitable growth under new leadership. After 39% gains in 2024, the easy money has been made, but the stock still trades at just 13x P/E with multiple catalysts ahead. The $80 target is achievable if execution continues on trajectory, but competition from Apple Pay and Stripe remains formidable. This is a "show me" story - management needs to deliver on BigCommerce, Fastlane, and Venmo monetization to justify higher valuation. Patient investors with 12-24 month horizon could be rewarded, but this isn't a get-rich-quick trade.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 1,507x unusual score reflects this specific trade's size relative to recent history - it does not imply the trade will be profitable or that you should follow it. Turnaround stories can take years to play out and face significant execution risks. Always do your own research and consider consulting a licensed financial advisor before trading.

About PayPal Holdings, Inc.: PayPal was spun off from eBay in 2015 and provides electronic payment solutions to merchants and consumers with a $63.68 billion market cap, operating 434 million active accounts and owning Venmo, a peer-to-peer payment app, in the Services-Business Services industry.