💼 PYPL Massive $2.2M Bullish Call Bet - Smart Money Loading Up Pre-Earnings! 🚀

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.2 MILLION on PYPL calls this morning at 10:42:27! This aggressive bet bought 3,200 contracts of $57.50 strike calls expiring May 15th - a massive bullish position just weeks before PayPal's critical Q4 2025 earnings. With PYPL down approximately 35% year-over-year despite five consecutive quarters of profitable growth, smart money is betting on a major reversal. Translation: Institutional investors see the recent analyst downgrades as an overreaction and are positioning for a comeback!

📊 Company Overview

PayPal Holdings (PYPL) is a digital payments giant navigating a pivotal turnaround under CEO Alex Chriss:

- Market Cap: $54.4 Billion

- Sector: Business Services / Digital Payments

- Current Price: $59.66 (as of January 5, 2026)

- Primary Business: Electronic payment solutions to merchants and consumers, operating 438 million active accounts globally, including Venmo peer-to-peer payments

- Headquarters: San Jose, California

- Employees: 24,400

PayPal was spun off from eBay in 2015 and has become one of the world's largest digital payment processors, competing with Apple Pay, Stripe, and traditional payment networks.

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 10:42:27):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Option_Strategy | Confidence | Z_Score | Z_Classification | Vol_OI_Ratio | Vol_OI_Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 10:42:27 | PYPL | BUY | CALL $57.50 | 2026-05-15 | $57.50 | 3,200 | $2.2M | BTO | Long Call | MEDIUM | 174.04 | EXTREMELY_UNUSUAL | 21.622 | HIGH_ACTIVITY |

🤓 What This Actually Means

This is a massive bullish bet on PayPal's turnaround! Here's what went down:

- 💸 Huge premium paid: $2.2M ($687.50 per contract × 3,200 contracts)

- 🎯 Strategic strike: $57.50 is slightly in-the-money (stock at $59.66), providing built-in value with room to run

- ⏰ Perfect timing: 130 days to expiration captures Q4 2025 earnings (expected early-to-mid February), potential bank charter news, and Q1 2026 earnings

- 📊 Massive size: 3,200 contracts represents 320,000 shares worth ~$19M

- 🏦 Institutional conviction: This is sophisticated positioning, not retail speculation

What's really happening here: This trader is betting BIG that PYPL recovers from the December analyst downgrades that sent the stock from ~$89 in early October to current levels around $60. The May 15 $57.50 calls give them leverage to profit from any rally back toward the $78 average analyst price target. With the stock already slightly above the strike price, they're positioned to benefit from any positive earnings surprise, bank charter approval news, or reversal in branded checkout growth trends.

Unusual Score: 🔥 EXTREMELY UNUSUAL (174.04x Z-score) - This activity is several times larger than typical PYPL option flow! The volume-to-open-interest ratio of 21.6x signals massive new positioning, not existing trades being closed. When you see this kind of size and conviction, institutions are making a statement.

📈 Technical Setup / Chart Check-Up

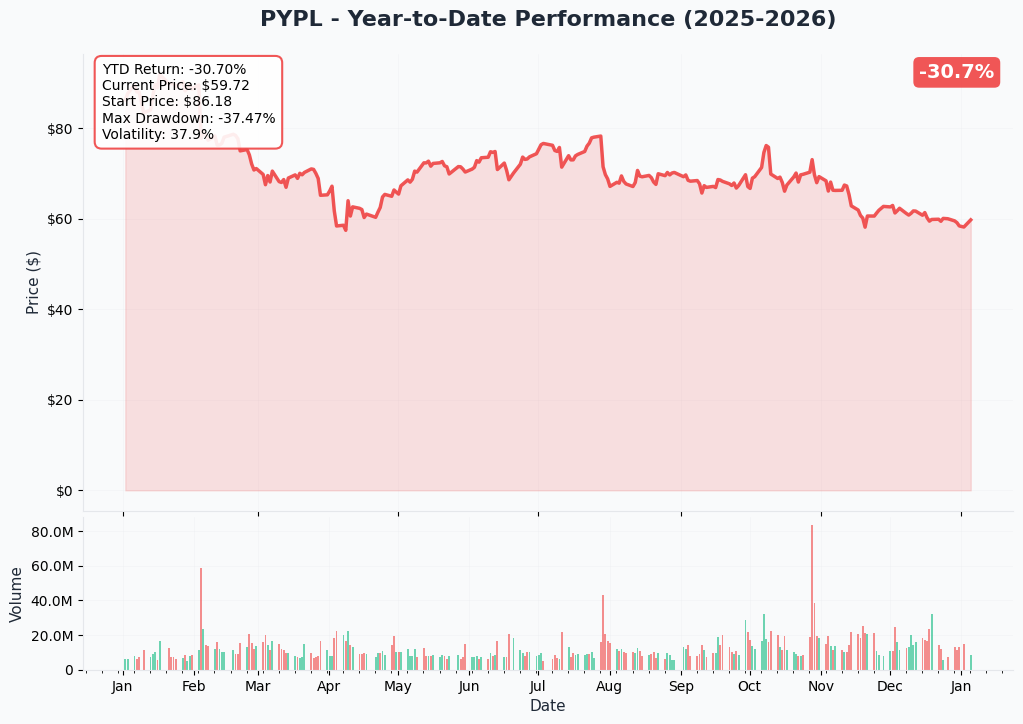

YTD Performance Chart

PayPal is having a rough year - down approximately 35% from early 2025 highs with current price of $59.66. The chart tells a painful story of optimism turning to disappointment:

Key observations:

- 📉 Brutal selloff: Crashed from ~$89.55 in early October 2025 to ~$60.89 by early December on analyst downgrades

- ⚠️ Post-earnings drop: Despite Q3 beat on October 28, stock fell 9% as guidance disappointed

- 🎢 High volatility: Stock trading in wide range throughout 2025

- 📊 Recent stabilization: Found support in the high-$50s to low-$60s range

- 💔 Broken promises: Management's retreat from "linear path" of margin expansion hurt credibility

- 🛡️ Silver lining: Stock holding above $55.85 (52-week low), showing some institutional support

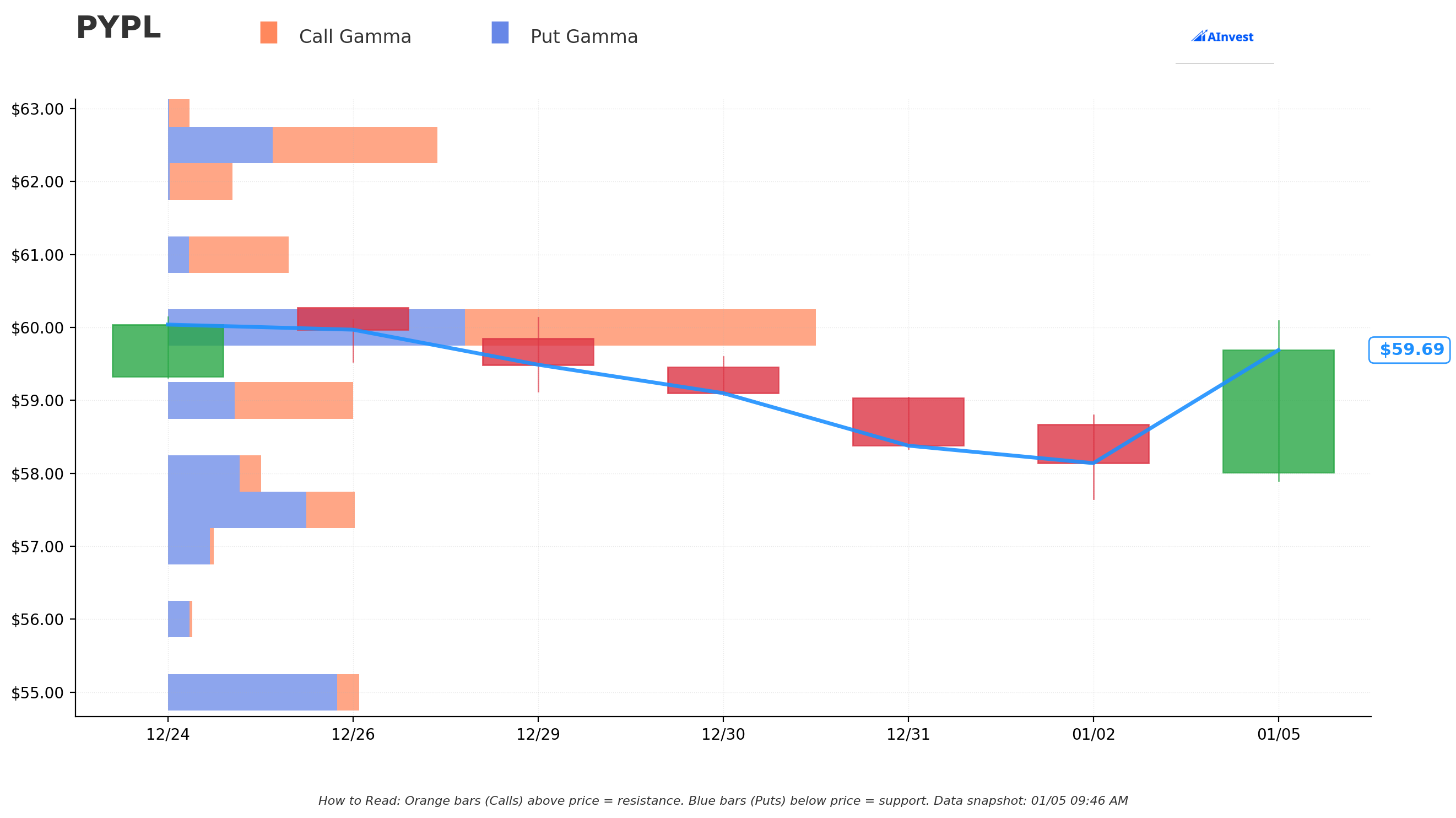

Gamma-Based Support & Resistance Analysis

Current Price: $59.66

The gamma exposure map reveals critical price magnets and barriers for near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $59.00 - Immediate support with 13.9B total gamma (strongest nearby floor!) - just 1.1% below current price

- $58.00 - Secondary support at 7.0B gamma - 2.8% drop would test this level

- $57.50 - CRITICAL support at 14.0B gamma (exactly where this call trade is struck! Not coincidental) - 3.6% below current

- $55.00 - Major structural floor with 14.4B gamma - 7.8% drop would be disaster scenario

🟠 Resistance Levels (Call Gamma Above Price):

- $60.00 - Immediate ceiling with 48.5B gamma (STRONGEST RESISTANCE - dealers will sell into rallies!) - only 0.6% overhead

- $61.00 - Secondary resistance at 8.9B gamma - 2.2% rally target

- $62.50 - Major ceiling zone with 20.1B gamma - 4.8% above current

- $65.00 - Extended upside target at 30.8B gamma - 8.9% rally required

- $67.50 - Stretch goal at 10.1B gamma - 13.1% rally

- $70.00 - Home run scenario at 14.9B gamma - 17.3% rally

What this means for traders: PYPL is trading in a critical zone right between massive $59 support (13.9B) and crushing $60 resistance (48.5B - the single largest gamma level). The enormous gamma at $60 (nearly 50B) creates natural selling pressure as price approaches - this is the LINE IN THE SAND that bulls need to break. The call buyer struck at $57.50 where there's 14.0B gamma, positioning just below major support at $59. Smart strategy - they get downside protection from gamma support while maintaining upside to $65-70 resistance levels.

Notice anything? The call buyer positioned EXACTLY at $57.50 where there's 14.0B total gamma - this provides a solid floor if the stock dips temporarily. If PYPL can break through the massive $60 resistance (48.5B gamma), the next resistance isn't until $62.50, creating room for a quick 5% rally.

Net GEX Bias: Bullish (150.7B call gamma vs 106.1B put gamma) - Overall positioning leans bullish, suggesting market makers would need to buy stock on dips to hedge their short call positions. This creates mechanical support.

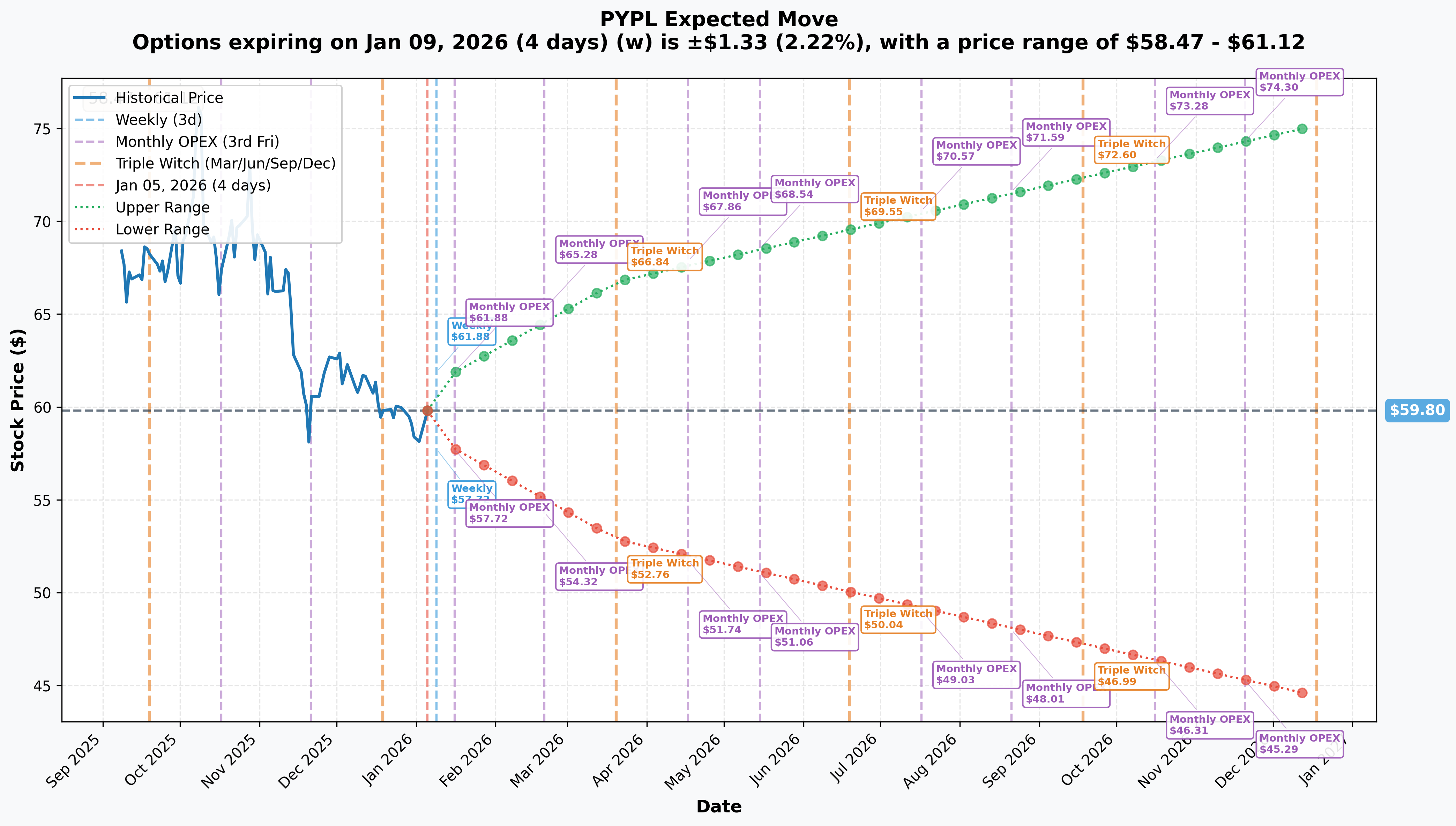

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$1.33 (±2.22%) → Range: $58.47 - $61.12

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$2.08 (±3.48%) → Range: $57.72 - $61.88

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$6.95 (±11.62%) → Range: $52.85 - $66.75

- 📅 May OPEX (May 15 - 130 days - THIS TRADE!): Estimated ±$9.50 (±15.9%) → Range: $50.30 - $69.30

Translation for regular folks: Options traders are pricing in a 2.2% move ($1.33) by this Friday for weekly expiration, but a much larger 11.6% move ($6.95) through March quarterly expiration which likely includes Q4 earnings. The market expects some volatility around earnings, but the relatively modest implied moves (compared to high-growth tech stocks) reflect PYPL's maturity as a large-cap fintech.

The May 15th expiration (when this $2.2M trade expires) has an upper range around $69.30 - meaning the market thinks there's a reasonable possibility PYPL could rally back toward analyst price targets of $76-78 over the next 130 days. The $57.50 call buyer starts profiting at breakeven around $65 (assuming $7.50 premium paid), which sits comfortably within the implied move range.

Key insight: The relatively low implied volatility compared to late 2025 suggests the market has calmed down after the December analyst downgrades. This makes options cheaper to buy - smart money is taking advantage of reduced premiums to load up before the next catalyst.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings Release - Expected February 3-11, 2026 📊

PayPal is expected to report fiscal Q4 2025 results in early-to-mid February 2026 (exact date unconfirmed, but historical pattern suggests first or second week). This is THE catalyst that could validate or destroy the bull thesis:

Wall Street expectations:

- 📊 Revenue: Consensus $8.83B (historical pattern of Q4 being strongest quarter)

- 💰 EPS: Consensus $1.29 (fitting into full-year guidance of $5.35-$5.39)

- 🛡️ Q4 Guidance from October: Non-GAAP EPS $1.27-$1.31 (+7-10% YoY)

Key metrics to watch:

- 🔍 Branded checkout growth: CFO warned it "may grow slower than Q3" - any stabilization would be HUGE positive surprise

- 💵 Venmo revenue trajectory: Targeting $2B by 2027, looking for 20%+ growth continuation

- 🛍️ BNPL volume: Approaching $40B TPV with 68% U.S. market penetration

- 📈 Transaction margin dollars: Market watching for evidence that 2026 won't be as bad as feared

- 🎯 2026 Guidance: This is the BIG ONE - any positive surprise on transaction margin dollar growth would crush the bear thesis

Upside surprise potential: According to management's February 2025 Investor Day targets, PayPal is targeting high single-digit transaction margin dollar growth by 2027 with low-teens EPS growth. If 2026 guidance shows a path back to this trajectory faster than expected, stock could rally 15-20%.

Downside risk: Management explicitly stated 2026 is an "investment year" with headwinds from BNPL rewards and agentic commerce investments. Some analysts project transaction margin dollar growth below 3% in 2026, well below the "linear path" promised earlier. Another disappointing guide could send stock to $50 support.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Bank Charter Application Decision - 12-18 Month Timeline 🏦

PayPal submitted applications on December 15, 2025 to the Utah Department of Financial Institutions and FDIC to establish PayPal Bank, a Utah-chartered industrial loan company (ILC):

Why this matters:

- 💰 Margin improvement: Reduce reliance on partner banks, potentially improving margins by 30-50 bps

- 🎯 Strategic optionality: Pursue direct card network membership, expand lending capabilities

- 🏢 Competitive positioning: Block (Square) already secured ILC charter in 2025

- 💼 Small business lending: PayPal has extended $30B in loans to date, charter enables expansion

- 🏛️ Regulatory environment: Trump administration's deregulatory stance increases approval probability

Timeline: Typical FDIC/state review takes 12-18 months. Decision could come as early as mid-2026 (best case) or Q1 2027 (more realistic). Any positive news about application progress would be stock-positive.

Risk: Approval not guaranteed. Regulatory scrutiny on fintech remains elevated despite political environment.

Next Dividend Payment - Expected March 11, 2026 💵

PayPal initiated its first-ever dividend in October 2025:

- 💰 Quarterly Dividend: $0.14 per share ($0.56 annualized)

- 📊 Dividend Yield: ~0.24% (at current prices)

- 🎯 Payout Ratio Target: 10% of adjusted net income

- 📅 Expected Ex-Date: March 2026

- 📅 Expected Payment: March 11, 2026

While the yield is modest, the dividend signals management confidence and attracts income-focused institutional investors. First payment was December 10, 2025.

📊 Strategic Product Catalysts (2026)

Venmo Monetization Acceleration - Path to $2B Revenue 💙

PayPal's Venmo peer-to-peer payment app is targeting $2B in revenue by 2027, up from ~$900M in 2021:

2026 key drivers:

- 💳 Debit card growth: +40% monthly active users YoY

- 🛍️ Pay with Venmo: Expected 35% TPV growth in 2026

- 🏪 In-store rollout: Full capabilities throughout 2026, accessing $4.2T U.S. retail payments market

- 📊 Merchant integration: Expanding beyond P2P into commerce

Why this matters for the call trade: Venmo revenue growing 20%+ becomes a larger portion of overall PayPal revenue, helping offset branded checkout deceleration concerns. Any announcements of major merchant partnerships or accelerated monetization would boost stock.

Fastlane Checkout Expansion - International Growth 🚀

PayPal's Fastlane guest checkout solution is showing strong metrics:

- 📊 Current reach: 171M+ eligible accounts, 264M+ eligible cards in U.S.

- 🌍 UK launch: Available in 2025

- 🎯 Performance: 50% higher conversion rate, 35% faster checkout vs. standard flows

- 🗺️ International expansion: Additional markets expected throughout 2026

Competitive context: Fastlane competes directly with Stripe Link and Shop Pay. Success in international markets would validate the technology and create new revenue streams.

PayPal World Platform Expansion - Global Interoperability 🌐

Launched in September 2025, PayPal World connects major payment systems globally:

- 🤝 Launch Partners: Mercado Pago, NPCI International (UPI), Tenpay Global, PayPal, Venmo

- 👥 Combined Reach: Nearly 2 billion users globally

- 💡 Features: Cross-border P2P transfers, AI agent commerce compatibility, stablecoin readiness

- 🎯 Merchant benefit: Automatic access to new payment methods without integration work

2026 expansion: Additional wallet partners expected to join platform. This is PayPal's "differentiated moat" - creating a global wallet interoperability layer that competitors can't easily replicate.

BNPL (Buy Now Pay Later) Expansion - $40B TPV Market 🛒

PayPal's BNPL business is approaching $40B in TPV for 2025:

- 🏆 Market leadership: 68% of U.S. online shoppers have used PayPal BNPL, #1 BNPL app with 57% usage

- 🌍 Geographic footprint: Currently in 9 global markets, additional rollouts planned

- 💰 Blue Owl partnership: $7B receivables purchase agreement de-risks balance sheet

- 📊 Order value impact: BNPL orders generate 80%+ higher average order value

2026 catalyst potential: New geographic markets, improved credit risk management through Blue Owl partnership, and potential regulatory clarity could drive BNPL growth acceleration.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in ~30 days: Q4 results expected early-to-mid February create massive volatility risk. Management has explicitly warned that branded checkout "may grow slower than Q3" and that 2026 is an "investment year" creating headwinds. Even a solid earnings beat could disappoint if 2026 guidance doesn't show improvement. The December analyst downgrades (Morgan Stanley to $51, BofA to $68) set a very negative tone.

-

💸 2026 "Investment Year" Headwinds: CEO Alex Chriss explicitly stated investments in BNPL rewards and agentic commerce create "headwind of transaction margin dollar growth in '26". Management walked back the "linear path" of margin expansion outlined at Investor Day. Analysts project reported transaction margin dollar growth likely below 3% in 2026, not recovering to ~6% until 2027. This creates near-term earnings pressure.

-

🛍️ Branded Checkout Deceleration Risk: PayPal's core branded checkout business (PayPal button on merchant sites) showed mid-Q3 consumer slowdown that "persisted into Q4" per CFO comments. This is the legacy business that still drives majority of revenue. If deceleration continues or worsens in 2026, it would be extremely difficult for Venmo/BNPL/Fastlane to offset the headwind given their smaller size.

-

🍎 Intense Competition from Apple Pay, Stripe, Zelle: PayPal faces mounting pressure from multiple angles:

- Apple Pay: 65.6M U.S. users, processing ~$10T annually, deep device-level integration advantage

- Stripe: Growing TPV +12.3% vs PayPal's +6.1%, winning among tech companies (80.1% integration rate vs PayPal's 74.3%)

- Zelle: Bank-integrated P2P taking share from Venmo

- Take rate pressure from competition could compress margins further

-

🏦 Bank Charter Uncertainty: ILC approval not guaranteed despite December 15, 2025 application. Typical 12-18 month review process means no clarity until mid-2026 at earliest. Block already has ILC charter, giving them competitive advantage. Regulatory environment could shift. Any denial would be stock-negative.

-

🌍 Macroeconomic Consumer Spending Slowdown: PayPal management noted consumer spending slowdown mid-Q3 that persisted into Q4. As a payments processor, PayPal is directly exposed to consumer health. Any recession or prolonged spending weakness would hit volumes hard. E-commerce growth normalizing post-pandemic also creates headwind.

-

📊 Valuation Still Not Cheap: Trading at 10x forward earnings sounds cheap, but that's based on aggressive EPS growth assumptions. If 2026 transaction margin dollars grow only 2-3% (vs. 5-6% needed for target), EPS could disappoint. The 35% YTD decline has helped valuation, but execution risk remains elevated.

-

📉 Morgan Stanley $51 Price Target Overhang: The December 18, 2025 downgrade to Underweight with $51 target (from $74) represents 15% downside from current levels. Morgan Stanley is a highly influential Wall Street firm - their bearish stance could pressure the stock until fundamentals inflect. Other downgrades from BofA (to $68) and Baird add to negative sentiment.

-

🎯 Execution Risk on Multiple Fronts: PayPal is simultaneously trying to: fix branded checkout deceleration, monetize Venmo, scale BNPL profitably, launch Fastlane internationally, build PayPal World platform, obtain bank charter, manage China headwinds, invest in AI/agentic commerce. That's a LOT of moving parts for a company in turnaround mode. Any stumble on execution could reignite concerns.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through May 15th expiration:

📈 Bull Case (35% probability)

Target: $70-$78

How we get there:

- 💪 Q4 earnings BEAT with revenue approaching $9B and EPS toward high-end of $1.31 guidance

- 🎯 The key: 2026 guidance surprises positively - transaction margin dollar growth guided to 4-5% (vs. feared 2-3%), signaling branded checkout stabilization

- 🚀 Venmo revenue growth accelerates to 25%+ with new merchant partnerships announced

- 💳 Fastlane international expansion showing strong traction in UK and additional markets

- 🏦 Bank charter application progressing well, potential approval timeline communicated (even if not final approval yet)

- 📊 BNPL reaching profitability inflection point with Blue Owl partnership derisking balance sheet

- 🤖 PayPal World adding major new wallet partners (e.g., major Asian payment platforms)

- 💰 Analyst upgrades from BofA, Morgan Stanley reconsidering bearish stance after better-than-feared guidance

- 📈 Breakout above $60 gamma resistance (48.5B) triggers technical rally through $65 to $70

- 🎁 Possible accelerated share buyback announcement ($6B program for 2025 continues into 2026)

Key metrics needed:

- Q4 transaction margin dollar growth showing sequential improvement

- Branded checkout growth NOT decelerating further (stable or improving)

- 2026 EPS guidance of $5.50+ (vs. feared $5.20-5.40)

- Venmo monetization metrics beating internal targets

Path to $78 (consensus price target): If execution delivers on multiple fronts and 2026 guidance dispels the "investment year headwind" fears, stock could re-rate from 10x to 12-13x forward earnings. At $5.50 EPS and 13x multiple = $71.50. With momentum and bank charter optimism, $75-78 is achievable.

Probability assessment: 35% because it requires PayPal to exceed current low expectations on multiple dimensions. The December downgrades set a very negative baseline - any "not as bad as feared" outcome could trigger short covering and momentum. But execution risk is real and branded checkout trend is genuine headwind.

🎯 Base Case (45% probability)

Target: $58-$68 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings roughly meeting consensus (~$8.8B revenue, $1.28-1.30 EPS)

- ⚖️ 2026 guidance slightly disappointing but not catastrophic - transaction margin dollar growth 3-4%, EPS $5.30-5.40

- 📱 Venmo growing 20%+ but not accelerating dramatically - steady progress toward $2B 2027 target

- 🛍️ Branded checkout stabilizes but doesn't improve - "good enough" to stop hemorrhaging but not exciting

- 🏦 Bank charter no major updates (still in review process, 12-18 month timeline confirmed)

- 🤝 Fastlane and PayPal World making progress but not major announcements

- 🔄 Trading within gamma support ($57.50-$59) and resistance ($60-$65) for weeks/months

- 📊 Market digests the 35% YTD decline, waits for clearer 2026 visibility

- 💤 Analyst ratings stay mixed - no major upgrades or additional downgrades

- 📉 Stock grinds sideways as "show me" story - needs multiple quarters of proof before re-rating

This is a neutral scenario for the call buyer: Stock stays range-bound $58-68, the $57.50 calls maintain some intrinsic value but don't explode higher. Modest profit possible if stock ends around $65-68 by May, but not the home run they're positioned for.

Why 45% probability: This is the "muddle through" scenario where PayPal neither crashes nor rips. Fundamentals remain decent (profitable growth, new initiatives making progress) but not exciting enough to drive major re-rating. Stock at technical inflection - neither confirming breakdown nor breakout. Most likely outcome is patience required.

📉 Bear Case (20% probability)

Target: $48-$55 (TEST MORGAN STANLEY'S $51 TARGET)

What could go wrong:

- 😰 Q4 earnings miss or guidance deeply disappoints - 2026 transaction margin dollar growth guided to only 2% with EPS $5.10-5.20

- 🚨 Branded checkout deceleration worsens - CFO warns of further slowdown in Q1 2026

- ⏰ Management walks back Investor Day targets even further - admits "linear path" not achievable until 2027+

- 💸 Consumer spending weakness intensifies - macro recession fears hit payment volumes

- 🍎 Competition intensifies - Apple Pay or Stripe announcing major merchant wins at PayPal's expense

- 🏦 Bank charter application delayed or early signs of regulatory pushback

- 💰 Margin compression from aggressive pricing to defend market share

- 📊 Analyst downgrades continue - Jefferies or other bulls capitulate, joining Morgan Stanley's bearish view

- 🔨 Break below $59 support triggers cascade to $57.50, then $55

- 🇨🇳 Potential international headwinds or regulatory issues in key markets

Critical support levels:

- 🛡️ $59.00: Immediate gamma floor (13.9B) - first line of defense

- 🛡️ $57.50: Major support (14.0B gamma) + this call strike - MUST HOLD or trade breaks down

- 🛡️ $55.00: Deep support (14.4B gamma) - disaster scenario approaching 52-week low of $55.85

Probability assessment: Only 20% because it requires multiple negative catalysts compounding. PayPal's fundamentals aren't broken - still profitable, growing, with $6-7B annual free cash flow and aggressive buybacks. The 35% decline has already priced in significant negativity. For stock to break $55, we'd need earnings disaster AND macro deterioration AND competitive losses. Possible but not base case.

Call P&L in Bear Case:

- Stock at $55 by May 15: Calls worth ~$0 (out-of-money above $57.50 strike), loss approaching -$2.2M (100% loss)

- Stock at $52 by May 15: Calls worth $0, total loss -$2.2M

- Stock at $57 by May 15: Calls worth minimal intrinsic value ~$0.50, loss ~-$2.0M (91% loss)

The call buyer would suffer devastating losses if the bear case plays out. This is a directional bet, not a hedge.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity

Play: Stay on sidelines until after Q4 earnings volatility settles in mid-February

Why this works:

- ⏰ Earnings in ~30 days creates binary event risk - let the dust settle first

- 📊 Stock already down 35% YTD but valuation not compelling without visibility into 2026 trajectory

- 🎯 Better entry likely post-earnings if guidance disappoints (could test $55 support) OR post-rally entry if guidance beats and stock runs to $68-70

- 📉 Implied volatility will crush post-earnings, making options cheaper for entry

- 🤔 The $2.2M call buy shows institutional optimism, but also shows big money using options (leverage) rather than buying stock (conviction)

- 💭 2026 "investment year" headwinds are real - need to see actual guidance numbers before committing

Action plan:

- 👀 Watch Q4 earnings closely for: revenue (need $8.8B+), transaction margin dollars (need stability), branded checkout commentary (stabilization critical), 2026 guidance (EPS $5.35+, transaction margin dollar growth 4%+)

- 🎯 If guidance disappoints, look for entry at $55 support (14.4B gamma floor) with 8-10% margin of safety

- 🚀 If guidance surprises positively, chase breakout above $62.50 only if accompanied by analyst upgrades

- 📊 Monitor insider buying/selling - CEO Chriss and CFO activity tells you if management truly confident

- ⏰ Revisit in March-April timeframe when bank charter updates may emerge

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 10-15% drawdown if earnings disappoint. Get better entry at clearer inflection point. Maintain optionality without tying up capital during uncertain period.

⚖️ Balanced: Post-Earnings Call Spread (Mini Version of the Trade)

Play: After earnings volatility settles, sell out-of-money call spread if stock stays range-bound

Structure: Buy $62.50 calls, Sell $67.50 calls (May 15 expiration - SAME as the $2.2M trade)

Why this works:

- 🎢 IV crush after earnings makes call spreads much cheaper - buy AFTER volatility drops

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets gamma resistance zone at $62.50-$67.50 where upside appears capped near-term

- 🤝 "Fading the rally" if stock pops on earnings but still faces 2026 headwinds

- ⏰ 90+ days to expiration gives time for any turnaround thesis to play out

- 🛡️ Lower risk than buying naked calls like the institutional trader

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$2.00-2.50 net debit per spread post-earnings (vs. $3.50-4.00 now)

- 📈 Max profit: $250-300 per spread if PYPL above $67.50 at May expiration

- 📉 Max loss: $200-250 if PYPL below $62.50 (defined and limited)

- 🎯 Breakeven: ~$64.50-$65.00

- 📊 Risk/Reward: ~1:1 to 1.2:1 (acceptable for defined-risk bullish play)

Entry timing:

- ⏰ Wait 3-5 days post-earnings (by mid-to-late February) for full IV collapse

- 🎯 Only enter if stock trades $60-62 range (gives room to work toward $67.50 target)

- ❌ Skip if stock already above $66 (spread too narrow) or below $58 (bullish thesis broken)

- ✅ Best scenario: Stock holds $59-61 post-earnings, you get cheap entry on reduced IV

Position sizing: Risk only 3-5% of portfolio on 3-5 spreads (total risk $600-1,250)

Exit strategy:

- 🎯 Take profit at 50-60% of max gain if reached early (don't get greedy)

- ⏰ Roll forward to July or August expiration if stock approaching $65-66 in April with momentum

- 🛡️ Cut loss at 50% if stock breaks below $57.50 support (thesis broken)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Whale - Long May Calls (ADVANCED)

Play: Copy the institutional trade structure but with smaller size

Structure: Buy $57.50 calls (May 15 expiration - EXACT SAME as the $2.2M trade)

Why this could work:

- 🐋 Following smart money - institutional player just put $2.2M on this exact trade

- 🎯 Strike at major gamma support ($57.50 = 14.0B gamma) provides floor

- 💥 Potential for explosive move if Q4 earnings + 2026 guidance surprise positively

- 📊 Captures multiple catalysts: Q4 earnings, bank charter updates, Q1 2026 earnings

- 🚀 Leverage to any move from $60 → $70 (17% stock move = potentially 150-200% option gain)

- ⏰ 130 days gives plenty of time for thesis to play out - not a weekly YOLO

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Premium likely $6.50-8.00 per contract ($650-800 each)

- ⏰ Theta decay: Losing $25-40 per contract per week as time passes

- 😱 Earnings risk: If Q4 disappoints, stock could gap to $55 and calls lose 40-60% overnight

- 📊 Directional bet: Need stock to rally - if it stays flat at $60, you lose money to time decay

- 🎯 Breakeven: Stock needs to be around $64-66 by May just to break even (8-10% rally required)

- ⚠️ 2026 headwinds: Even if Q4 good, poor 2026 guidance could cap upside

- 💀 All-or-nothing: Options can go to zero - very different risk profile than stock

Estimated P&L:

- 💰 Cost: ~$7.00 per call (using mid-market estimate)

- 📈 Profit scenario: Stock rallies to $70-75 range = $12.50-17.50 call value = +$5.50-10.50 gain (79-150% ROI)

- 🚀 Home run: Stock hits $78 (analyst target) = $20.50 call value = +$13.50 gain (193% ROI)

- 📉 Modest loss: Stock stays $60-63 = $2.50-5.50 call value = -$1.50 to -$4.50 loss (21-64% loss)

- 💀 Total loss: Stock drops below $57.50 = $0 call value = -$7.00 loss (100% loss)

Breakeven points:

- 📈 Need stock at ~$64.50 by May 15 just to break even (8% rally from current $59.66)

- 🎯 Real profitability requires $68+ (14% rally)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Fully understand that options can expire worthless (you could lose 100% of premium)

- ✅ Have traded single-leg calls before and understand theta decay

- ✅ Can afford to lose ENTIRE investment (only allocate 2-5% of portfolio MAX)

- ✅ Understand this is pure directional speculation, not investing

- ✅ Have conviction that Q4 earnings + 2026 guidance will positively surprise

- ⏰ Plan to actively manage - take profits at 50-80% gain if reached, cut losses at -50% if thesis breaks

- 📊 Accept that you're betting AGAINST the Morgan Stanley $51 bearish target

Entry timing:

- 🎯 Could enter now at current IV levels (copying whale exactly)

- OR wait until 1-2 weeks before earnings and buy on any dip toward $58 (better entry, less time decay)

- ❌ DO NOT buy day-of or day-before earnings (IV spike makes premiums too expensive)

Position sizing:

- Max 3-5 contracts for most retail traders ($2,100-3,500 total risk)

- Only if this represents 2-5% of total portfolio

- Size so that 100% loss doesn't materially impact your finances

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~40-45% (need 8%+ rally to breakeven, 14%+ to profit meaningfully)

🎯 The Bottom Line

Real talk: Someone just spent $2.2 MILLION on PYPL calls with 130 days to expiration, betting that the 35% YTD decline is overdone and PayPal's turnaround will surprise to the upside. This isn't a short-term trade - it's a strategic position capturing Q4 earnings, 2026 guidance, bank charter developments, and Q1 2026 results.

What this trade tells us:

- 🎯 Sophisticated player sees asymmetric risk/reward - December analyst downgrades (Morgan Stanley $51, BofA $68) created oversold conditions

- 💰 They're willing to pay $687.50 per contract for 130 days of exposure - that's serious conviction

- ⚖️ The $57.50 strike (3.6% below current price) sits at major gamma support (14.0B) - smart risk management

- 📊 They structured with May expiration to capture multiple earnings reports and bank charter timeline updates

- ⏰ Timing suggests they believe Q4 earnings (early-mid Feb) will be the inflection point

This is NOT a "buy everything now" signal - it's a "contrarian bet on turnaround" signal.

If you own PYPL:

- ✅ Hold through earnings if you bought below $55-60 (you have cushion)

- 📊 Consider trimming 20-30% if you're up significantly and want to derisk before earnings

- ⏰ Set mental stop at $55 support (14.4B gamma floor) to protect remaining position

- 🎯 If earnings beat AND 2026 guidance surprises positively, stock could run to $68-72 - hold winners

- 🛡️ Could buy 1-2 protective puts for every 100 shares if holding large position through earnings

If you're watching from sidelines:

- ⏰ Early-to-mid February Q4 earnings is the key catalyst - wait for this clarity!

- 🎯 Post-earnings dip to $55-58 would be excellent entry (10-15% margin of safety vs. $78 consensus target)

- 📈 Looking for confirmation of: branded checkout stabilization, 2026 EPS guidance $5.35+, transaction margin dollar growth 4%+, Venmo revenue $450M+ in Q4

- 🚀 Longer-term (6-12 months), bank charter approval, Venmo $2B revenue target by 2027, and Fastlane international expansion are legitimate catalysts for $75-85

- ⚠️ Current situation requires Q4 guidance to reset expectations - without that, stock could drift lower

If you're bearish:

- 🎯 Don't fight the tape into earnings - wait for the actual results and guidance

- 📊 If guidance confirms "investment year" headwinds with only 2-3% transaction margin dollar growth, stock could test $52-55

- ⚠️ First support at $59 (gamma), major support at $57.50 (call strike + gamma), deeper support at $55 (near 52-week low)

- 📉 Watch for break below $57.50 - that's the trigger for move toward Morgan Stanley's $51 target

- ⏰ Put spreads post-earnings (after IV crush) offer better risk/reward than naked puts now

Mark your calendar - Key dates:

- 📅 Early-to-mid February 2026 - Q4 FY2025 earnings report (THE CATALYST!)

- 📅 March 2026 - Next dividend ex-date and payment

- 📅 March 20 - Quarterly triple witch OPEX (±11.6% implied move window)

- 📅 April-May 2026 - Potential early signs of bank charter progress

- 📅 May 15, 2026 - Monthly OPEX, expiration of this $2.2M call trade

- 📅 Mid-2026 - Bank charter decision timeline begins (12-18 months from Dec 15, 2025 filing)

Final verdict: PayPal's turnaround story has genuine merit - bank charter application, Venmo monetization accelerating toward $2B, BNPL approaching $40B TPV, PayPal World differentiated platform, and aggressive $6B buyback program are all real. The 35% YTD decline has created a more reasonable valuation at 10x forward P/E.

BUT, the 2026 "investment year" headwinds are also real. Management explicitly warned about branded checkout deceleration and margin pressure from new investments. The December analyst downgrades from Morgan Stanley ($51 target) and Bank of America reflect legitimate concerns, not just noise.

The $2.2M call buyer is making a contrarian bet that Q4 earnings and 2026 guidance will dispel these fears. They could be right - if branded checkout stabilizes and guidance shows a path back to "linear" margin expansion, stock could easily rally 20-30% toward the $76 consensus target.

Be patient. Let Q4 earnings provide the roadmap. The PayPal turnaround will still be here in March, and you'll make better decisions with more information.

Options are leverage - use them wisely. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 174.04 Z-score reflects this specific trade's unusual size relative to recent PYPL option flow - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 10-15% moves either direction. The institutional call buyer may have complex portfolio objectives not applicable to retail traders. PayPal's 2026 "investment year" guidance creates near-term earnings uncertainty.

About PayPal Holdings: PayPal Holdings provides electronic payment solutions to merchants and consumers globally, operating 438 million active accounts including the Venmo peer-to-peer payment service, with a market cap of $54.4 billion in the Business Services industry. PayPal was spun off from eBay in 2015 and is headquartered in San Jose, California.