RBLX Massive $1.5M CALL Bet - Bullish Strike at $80 Ahead of Q1 Catalysts

Date: January 7, 2026 | Unusual Activity Detected

The Quick Take

Someone just deployed $1.5 MILLION into RBLX calls this morning at 10:59:22! This aggressive bullish bet bought 2,000 contracts of $80 strike calls expiring March 20th - positioning for a 4.4% rally from current levels of $76.63. With RBLX's newly expanded advertising platform announced at CES 2026, upcoming Q4 2025 earnings in February, and March expiration capturing critical Q1 catalysts, smart money is betting on continued momentum. Translation: Institutional buyers are betting on advertising revenue growth and bullish sentiment into Q4 earnings!

Company Overview

Roblox Corporation (RBLX) is a pioneering force in the metaverse and user-generated gaming industry:

- Market Cap: $53.61 Billion (as of January 2026)

- Industry: Electronic Gaming & Multimedia / Communication Services

- Sector: Technology / Interactive Entertainment

- Current Price: $76.63

- 52-Week Range: $50.10 - $150.59

- Primary Business: User-generated gaming platform, creator economy, digital advertising, virtual goods marketplace

Roblox has evolved from a foundational game-building engine into a global destination for millions of users to play, create, and share experiences with friends. Founded in 2004 by David Baszucki and Erik Cassel, the platform reached 151.5 million daily active users (DAUs) in Q3 2025.

The Option Flow Breakdown

The Tape (January 7, 2026 @ 10:59:22):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:59:22 | RBLX | MID | BUY | CALL $80 | 2026-03-20 | $1.5M | $80 | 2,000 | 627 | 2,000 | $76.63 | $7.46 |

What This Actually Means

This is a directional bullish bet on RBLX's upside potential! Here's what went down:

- Huge premium paid: $1.5M ($7.46 per contract × 2,000 contracts × 100 shares)

- Bullish strike: $80 represents 4.4% upside from current price of $76.63

- Strategic timing: 72 days to expiration captures Q4 2025 earnings (Feb 5-18), advertising platform scaling, age verification rollout, and potential Russia resolution

- Size matters: 2,000 contracts represents 200,000 shares worth ~$15.3M at current prices

- New positions opening: Volume of 2,000 vs Open Interest of 627 = 3.19x ratio showing fresh institutional positioning

What's really happening here: This trader is making a BULLISH bet that RBLX will rally above $80 by March 20th. They're paying $7.46 per share for the March $80 calls with breakeven at ~$87.46 (assuming no early exit). The timing is critical - this captures the Q4 earnings catalyst in February where management will provide 2026 guidance and detail advertising revenue progress. If RBLX breaks above $80, these calls could deliver substantial returns.

Unusual Score: EXTREME (Z-Score: 35.44) - This is extraordinarily unusual activity, literally off-the-charts with Vol/OI ratio of 3.19x indicating HIGH_ACTIVITY. This level of buying represents sophisticated institutional positioning ahead of major catalysts.

Technical Setup / Chart Check-Up

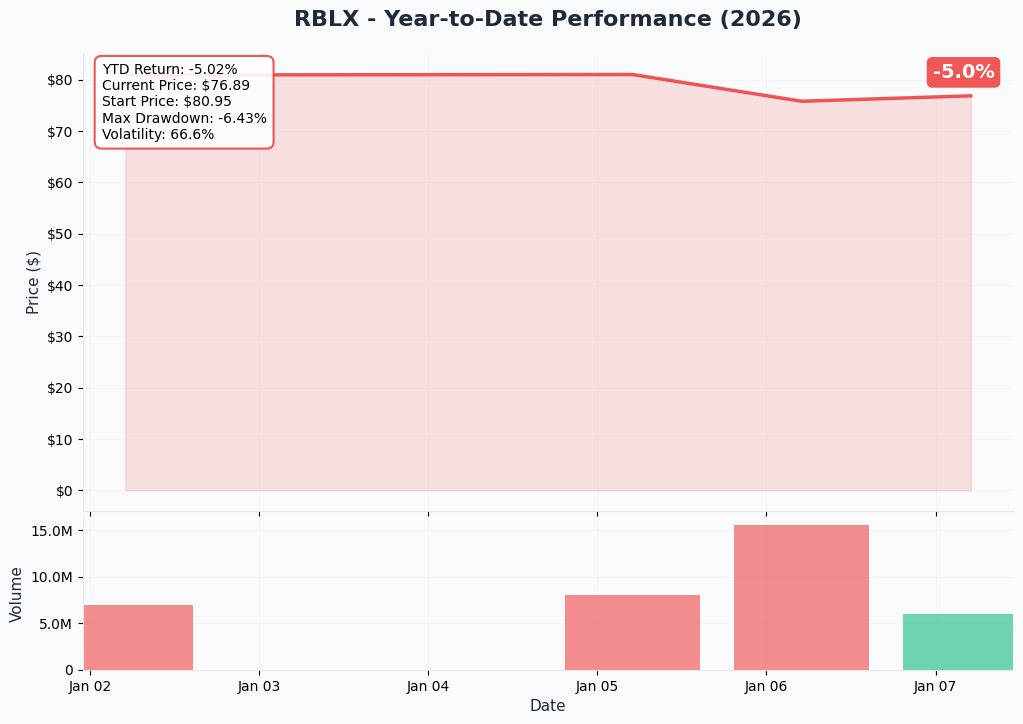

YTD Performance Chart

RBLX has shown volatility in 2025 with current price of $76.63 well below the 52-week high of $150.59 reached earlier in the year. The stock experienced significant downside following JPMorgan's downgrade in December and the Russia ban, declining from ~$84 to current levels (-8.3% over recent months).

Key observations:

- Major drawdown: Down ~49% from 52-week highs of $150.59, presenting potential value opportunity

- Recent consolidation: Trading in $76-77 range after bottoming around $50 in earlier weakness

- 3-month decline: Stock fell from $84 to $77 following JPMorgan downgrade and Russia ban news

- Bullish sentiment: Put/call ratio of 0.79 indicates more call buying than put buying

- Recovery potential: Current levels represent 33% off recent highs, creating asymmetric upside if catalysts materialize

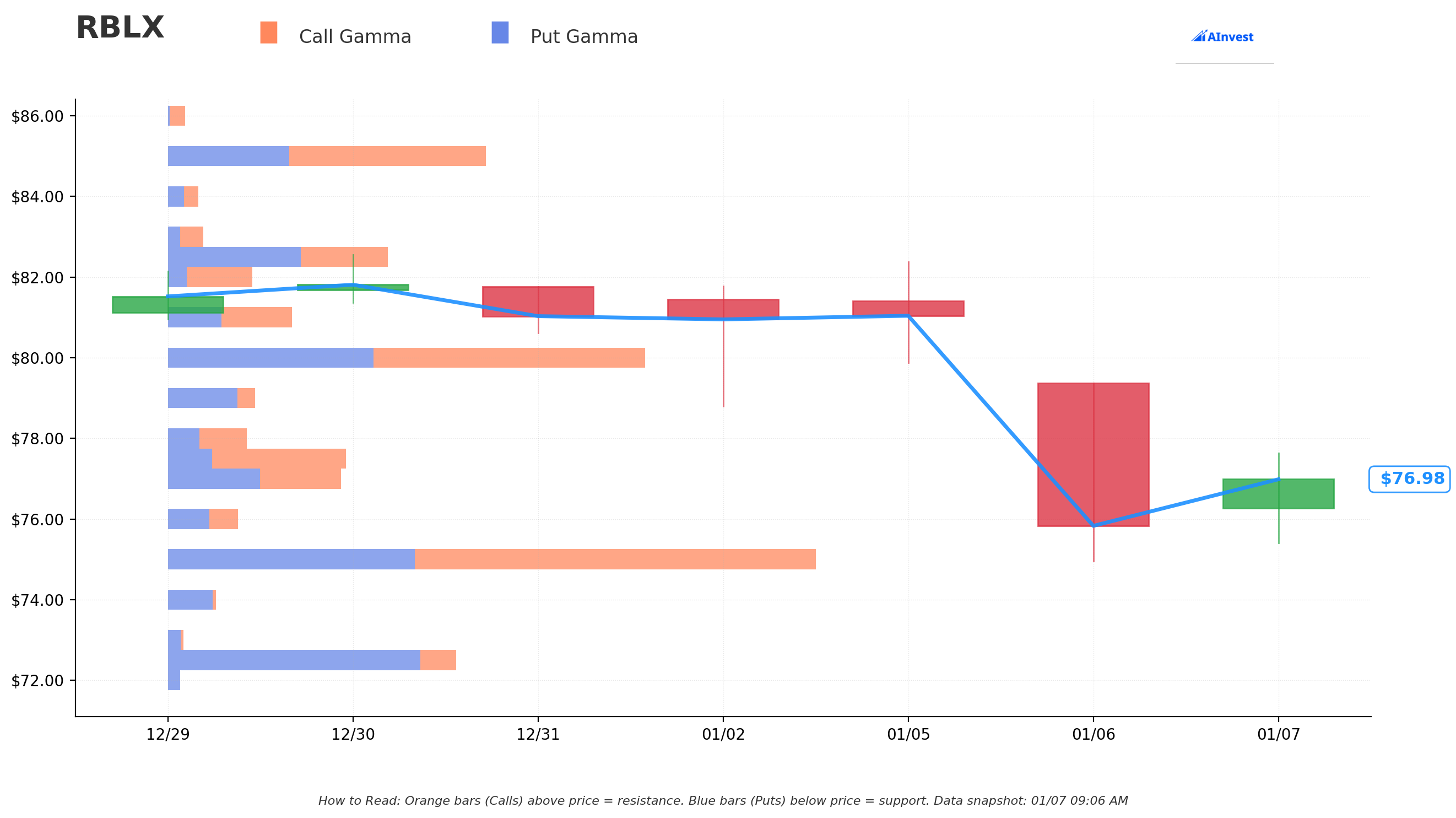

Gamma-Based Support & Resistance Analysis

Current Price: $76.63

The gamma exposure map reveals critical price magnets and barriers for near-term price action:

Support Levels (Put Gamma Below Price):

- $76 - Immediate support level (current trading near here)

- $74 - Secondary support zone

- $72 - Major structural floor (major round number psychological support)

Resistance Levels (Call Gamma Above Price):

- $78 - Immediate ceiling (+1.8% overhead)

- $80 - Major resistance (THIS CALL STRIKE! +4.4% rally required)

- $82 - Extended upside target (+7.0% rally)

What this means for traders: RBLX is trading just below the first resistance zone at $78. The call buyer struck at $80 which represents the second major gamma resistance level. This isn't coincidental - they're positioning for a breakout above the immediate $78 ceiling to reach the $80-82 zone. The setup suggests consolidation at current levels before the next directional move.

Notice anything? The call buyer struck EXACTLY at the $80 resistance level where significant call open interest creates natural resistance. They're betting that Q4 earnings and advertising platform momentum will be strong enough to push through this ceiling and drive the stock into the $80-85 range by March expiration.

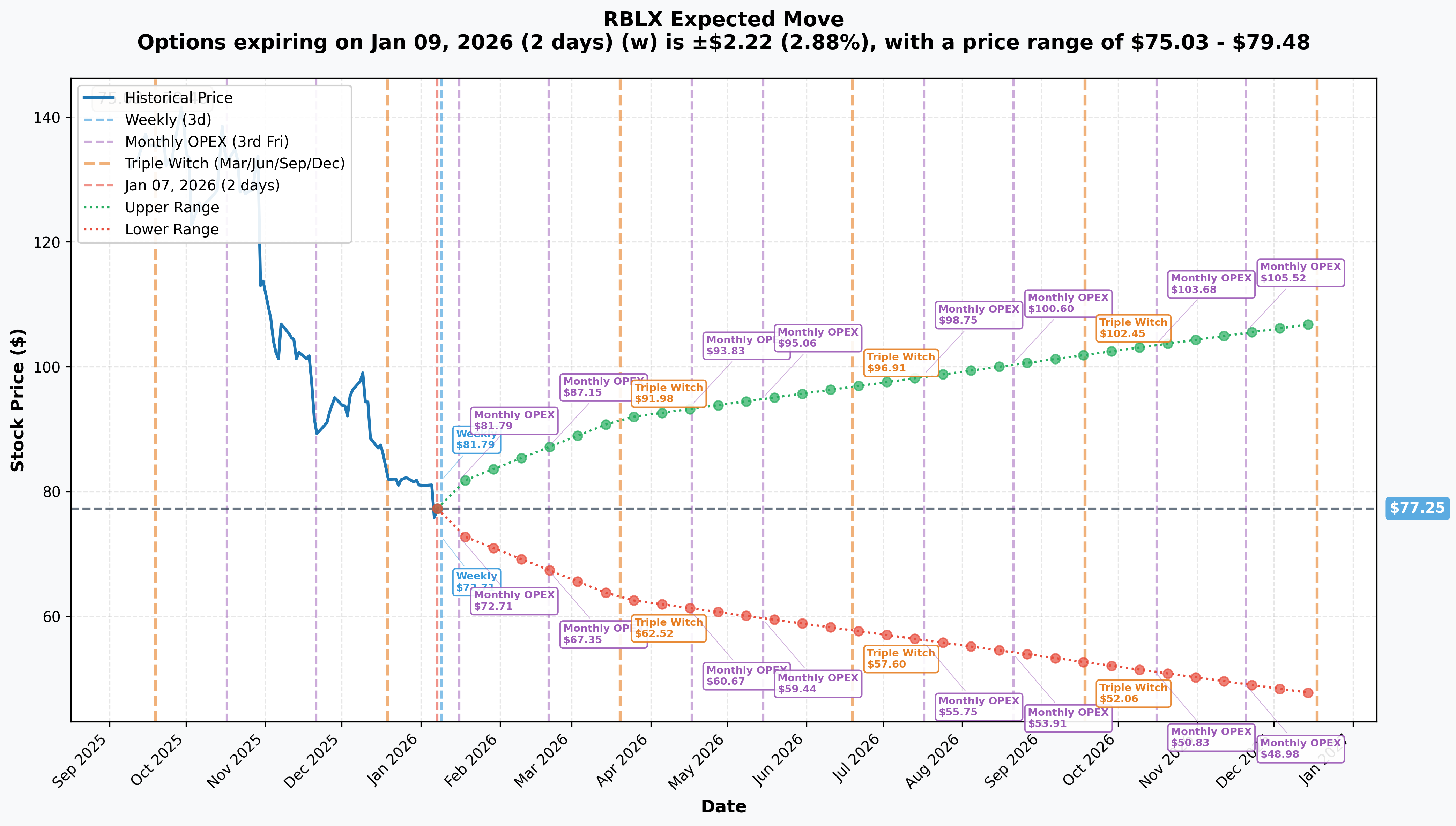

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 9 - 2 days): ±2.88% ($2.22) → Range: $75.03 - $79.48

- Monthly OPEX (Jan 16 - 9 days): ±5.45% ($4.21) → Range: $73.04 - $81.47

- Quarterly Triple Witch (Mar 20 - THIS TRADE!): ±18.70% ($14.45) → Range: $62.80 - $91.70

Translation for regular folks: Options traders are pricing in a 2.9% move ($2.22) by this Friday for weekly expiration, a 5.5% move ($4.21) through January OPEX (9 days away), and a MASSIVE 18.7% move ($14.45) through March expiration (72 days).

The March 20th expiration (when this $1.5M trade expires) has an upper range of $91.70 - meaning the market thinks there's a real possibility RBLX could trade as high as $92 over the next 72 days if catalysts materialize positively. This perfectly aligns with the call buyer's bullish thesis: capture a 15-20% rally from current levels if advertising revenue accelerates and earnings beat expectations.

Key insight: The sharp increase in implied volatility from 2.9% (weekly) to 18.7% (quarterly) reflects major catalyst uncertainty around Q4 earnings (February), advertising platform scaling, age verification impact, and potential Russia resolution. Smart money is positioning for significant upside movement.

Catalysts

The comprehensive catalyst analysis reveals both significant bullish drivers and material risks for RBLX. Below is a strategic summary focused on the March 20th expiration timeframe:

Immediate Catalysts (Next 60-90 Days)

Q4 2025 Earnings - February 5-18, 2026 (THE MAJOR CATALYST)

RBLX reports fiscal Q4 2025 results in mid-February. This is THE catalyst that determines whether this call bet pays off:

- Expected Revenue: ~$1.37 billion (guidance range $1.35-$1.40B, +37-42% YoY)

- Expected Bookings: Up to $2.05 billion (+51% YoY)

- Key Metrics to Watch:

- Advertising revenue breakdown: First detailed disclosure of new ad platform performance

- Russia ban DAU impact: Quantifying the ~8 million user loss

- Full-year 2026 guidance: Bookings growth, margin outlook, path to profitability

- Child safety lawsuit updates: Reserve/settlement implications

- MI300 series performance: Validation of 70% bookings growth sustainability

Upside surprise potential: Strong advertising adoption (90%+ completion rates, 1,000+ brands), successful age verification rollout, and Russia resolution could drive significant beat. Goldman Sachs has Street-high $180 price target implying 135%+ upside.

Downside risk: Any disappointment in bookings growth normalization (JPMorgan warns of "digestion year" with sub-20% growth), margin compression (~100bps expected contraction), or conservative 2026 guidance could trigger sharp selloff.

Advertising Platform Expansion (Current - Q1 2026)

RBLX's newly expanded advertising platform announced at CES 2026 represents a transformational revenue opportunity:

- Homepage Feature: New ad format in closed beta, scaling through Q1

- Programmatic Access: Expanded via Amazon DSP, Liftoff, Index Exchange, Magnite, PubMatic

- Rewarded Video Ads: Now in 400+ experiences including viral hits (Grow a Garden, Dress to Impress, Brookhaven)

- Brand Adoption: Over 1,000 brands using ads with 90%+ completion rates and 95%+ viewability

- Revenue Projection: Morgan Stanley projects $1.2B in ad revenue by end of 2026

- Google Partnership: Advertisers can purchase RBLX inventory through Google Ad Manager (launched April 2025)

Why this matters for the call trade: Ad revenue of $5-10 per user could add $560M-$1.1B in NEW revenue at significantly higher margins than Robux sales. This is an underappreciated revenue driver that could surprise positively in Q4 earnings and 2026 guidance. The March expiration captures initial advertising platform scaling metrics.

Age Verification Global Rollout (January 2026 - HAPPENING NOW)

RBLX's comprehensive age verification system addresses child safety concerns:

- Started: Australia, New Zealand, Netherlands in December 2025

- Global Rollout: Rest of world expansion in January 2026

- Age Segments: <9, 9-12, 13-15, 16-17, 18-20, 21+ with differentiated features

- Safety Features: Communication restrictions between adults and minors, AI facial estimation

Impact: Successfully addressing the ~60 active lawsuits and state AG investigations could remove regulatory discount from valuation. Age-appropriate features may INCREASE engagement and monetization among different age groups.

Russia Ban Resolution (Uncertain but Possible)

- Current Status: Roskomnadzor blocked RBLX in December citing extremist content and LGBT propaganda

- User Impact: ~8 million monthly users affected (up to 10M DAU per JPMorgan)

- Ongoing Talks: RBLX indicated willingness to comply with Russian regulations

- Timeline: Resolution possible within Q1 2026 if compliance achieved

- Upside: Could recover millions of DAUs and remove negative overhang

Medium-Term Catalysts (Q2-Q3 2026)

Creator Economy Momentum

RBLX exceeded $1 billion in creator payouts for the first time in 2025:

- Q3 2025 Payouts: $427.9M (+85% YoY)

- Top Creators: Top 1,000 averaged $1.1M (+40% YoY), Top 10 averaged $33.9M

- DevEx Program: 29,000+ creators in program with 8.5% rate increase

- Ecosystem Growth: More creators = more content = higher engagement = more monetization

AI Tool Releases

- 4D Object Creation: Limited release Q4 2025, expanding in 2026

- Real-time Voice Translation: English, Spanish, French, German

- Cube 3D: Foundation model for text-to-3D generation

- Impact: Lowers barrier to creation, accelerates content pipeline

Risk Catalysts (Downside Scenarios)

Growth Normalization "Digestion Year" (JPMorgan Warning)

- Analyst Concern: Multiple analysts (JPMorgan, UBS, Wolfe) warn 2026 is transition year

- Bookings Growth: Expected to slow from 52% (2025) to sub-20% (2026)

- Margin Compression: Adjusted EBITDA margins expected to contract ~100bps

- Engagement Cooling: UBS warns engagement cooling as viral hit momentum fades (Grow a Garden dependency)

- Profitability Path: Continued GAAP losses, may take "several more years" to reach profitability

Child Safety Litigation Risk

- Scale: ~60 active lawsuits nationwide alleging facilitation of child exploitation

- State AGs: Texas (November 2025), Tennessee (December 2025) lawsuits ongoing

- Tennessee AG Quote: Called RBLX "digital equivalent of creepy cargo van"

- Financial Impact: Unquantified settlement costs, potential regulatory fines

- Reputational Risk: Headline risk and user/parent trust concerns

Insider Selling Signals

- CEO David Baszucki: Sold $5.67M in stock on December 18, 2025

- Pattern: 53 sell transactions, 0 buys over past 5 years

- Net Selling: 9.95M shares sold over past 18 months

- Note: Sales under 10b5-1 pre-planned arrangement, but persistent selling raises questions

Valuation Concerns

- Current Metrics: Trading at significant premium after 2025 rally from Q3 earnings beat

- High Expectations: Already up significantly from 52-week lows, substantial gains captured

- Limited Margin for Error: Any execution misstep could trigger 15-25% correction

- Profitability Timeline: Still several years away from GAAP profitability despite revenue growth

Competitive Threats

- Epic Games: Expanding creator economy with 0% commission through 2026

- Fortnite: Creator Item Sales Program launched December 2025

- Revenue Sharing: Epic taking 50% after 2026 vs RBLX's ~71% take rate

- Developer Poaching Risk: Lower take rates could attract RBLX creators to competing platforms

For complete catalyst details and citations, see: RBLX_catalysts.md

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

Bull Case (35% probability)

Target: $85-$95

How we get there:

- Earnings BEAT: Q4 revenue at high-end of guidance ($1.40B+), bookings exceed $2.05B target

- Advertising Revenue Surprise: Detailed ad revenue disclosure shows $200M+ quarterly run rate, validating $1.2B 2026 target

- 2026 Guidance Strong: Management guides FY2026 bookings growth >25% (vs Street expecting sub-20%), citing advertising acceleration

- Margin Expansion: Gross margins improve vs expectations, showing operating leverage

- Russia Resolution: Compliance achieved, access restored, adding back millions of DAUs

- Age Verification Success: New safety features INCREASE engagement, positive user feedback

- Viral Hit Momentum Continues: New breakout game(s) emerge, sustaining high engagement rates

- Technical Breakout: Stock clears $80 gamma resistance, rallies to $85-90 range (upper implied move)

Key metrics needed:

- DAU growth rebounds despite Russia ban

- Bookings growth remains >20%

- Ad platform adoption accelerates

- Q1 2026 guidance strong

Probability assessment: 35% because it requires multiple catalysts aligning positively. However, advertising platform represents genuine upside surprise potential that Street may be underestimating. Goldman's $180 PT and 13 Buy ratings (vs 9 Hold, 1 Sell) suggest institutional bullishness remains. The $1.5M call bet implies sophisticated buyer sees >35% odds.

Call P&L in Bull Case:

- Stock at $90 on Mar 20: Calls worth $10.00, profit = $2.54/share × 200,000 = $508,000 gain (34% ROI)

- Stock at $95 on Mar 20: Calls worth $15.00, profit = $7.54/share × 200,000 = $1,508,000 gain (101% ROI!)

- Stock at $85 on Mar 20: Calls worth $5.00, loss = -$2.46/share × 200,000 = -$492,000 (33% loss)

Base Case (40% probability)

Target: $75-$82 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- Solid Earnings: Q4 results meet consensus ($1.35-1.37B revenue), no major surprises

- Advertising Progress: Ad revenue growing but not spectacular, steady adoption without blowout numbers

- Guidance In-Line: 2026 bookings growth guided to 15-20% range, matching cautious Street expectations

- Russia Remains Uncertain: No resolution by March, DAU impact persists

- Engagement Mixed: Some cooling from viral hit peaks, but stable core user base

- Litigation Ongoing: Child safety lawsuits progress but no major settlements or resolutions

- Trading Range-Bound: Consolidation in $75-82 range as market digests earnings and waits for next catalyst

- Volatility Crush: IV declines post-earnings, reducing option premium

This represents moderate success for the call buyer: Stock grinds higher toward $80-82 range, calls show some profit but not home run. The $1.5M is justified by 10-20% gains, but they may exit before expiration to capture profits and avoid theta decay.

Why 40% probability: This is the "muddle through" scenario where fundamentals remain solid (bookings growth continues, advertising shows promise) but valuation concerns and growth normalization prevent breakout. Most likely institutional position management - buy dips, sell resistance.

Call P&L in Base Case:

- Stock at $82 on Mar 20: Calls worth $2.00, loss = -$5.46/share × 200,000 = -$1,092,000 (73% loss)

- Stock at $80 on Mar 20: Calls worth $0.01, loss = -$7.45/share × 200,000 = -$1,490,000 (99% loss)

- Stock at $78 on Mar 20: Calls expire worthless, loss = -$7.46/share × 200,000 = -$1,492,000 (100% loss)

Bear Case (25% probability)

Target: $65-$75 (CALLS EXPIRE WORTHLESS)

What could go wrong:

- Earnings Disappoint: Q4 bookings miss, revenue at low-end of guidance, weak margins

- 2026 Guidance Weak: Management confirms "digestion year," guides bookings growth to mid-teens or lower

- Advertising Underwhelms: Ad revenue contribution minimal, slower adoption than expected

- Russia Ban Permanent: No resolution, DAU loss becomes structural headwind

- Engagement Decline Confirmed: Management admits viral hit dependency, cooling trends continuing

- Litigation Escalates: Major settlement announced, material financial impact

- Insider Selling Accelerates: More executive selling signals lack of confidence

- Margin Compression Worse: Developer payout increases and ad platform costs pressure margins beyond expectations

- Competitive Pressure: Epic Games creator program shows traction, developer defections begin

- Macro Headwinds: Broader tech weakness, consumer spending slowdown impacts bookings

- Break Below $72 Support: Technical selling accelerates decline to $65-70 range

Critical support levels:

- $76: Current level - MUST HOLD or momentum shifts bearish

- $74: Secondary support - break here targets $72

- $72: Major gamma floor - last line of defense before cascade to $65-70

Probability assessment: 25% because it requires multiple negative catalysts. However, the JPMorgan "digestion year" warning, persistent insider selling, margin compression expectations, and elevated litigation risks are real. At current valuation with expectations high, execution missteps would be punished severely.

Call P&L in Bear Case:

- Stock at $75 on Mar 20: Calls expire worthless, loss = -$7.46/share × 200,000 = -$1,492,000 (100% loss)

- Stock at $70 on Mar 20: Calls expire worthless, loss = -$7.46/share × 200,000 = -$1,492,000 (100% loss)

- Stock at $65 on Mar 20: Calls expire worthless, loss = -$7.46/share × 200,000 = -$1,492,000 (100% loss)

Trading Ideas

Conservative: Cash Gang Until Post-Earnings Clarity

Play: Wait on sidelines until after February earnings volatility settles

Why this works:

- Earnings Binary Risk: Q4 results in ~30-40 days create significant event risk with ±18.7% implied move through March

- Implied Volatility Elevated: Options expensive pre-earnings, IV crush likely post-announcement

- Recent Weakness: Stock down 8.3% over recent months from $84 levels, trend uncertain

- Insider Selling Concern: CEO sold $5.67M in December, persistent selling pattern

- Better Entry Likely: Post-earnings pullback to $70-75 support would offer superior risk/reward

- Catalyst Clarity: Earnings will reveal advertising traction, 2026 guidance, Russia impact, litigation status

Action plan:

- Watch February earnings for bookings ($2.05B+ target), ad revenue disclosure, 2026 guidance quality

- Look for pullback to $70-74 gamma support post-earnings for stock entry

- Need to see advertising platform validation and strong 2026 guidance before committing capital

- Monitor unusual options activity - if institutions add MORE calls, sentiment shifting positive

- Revisit after Q4 earnings clarity on growth trajectory

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 15-25% drawdown if earnings disappoint. Get better entry if stock consolidates post-earnings. Maintain optionality.

Balanced: Smaller Bullish Position (Copy The Trade, Smaller Size)

Play: Buy smaller position in same strike to mirror institutional positioning

Structure: Buy March 20 $80 calls (SAME as the $1.5M trade, but 5-10 contracts)

Why this works:

- Institutional Validation: Following smart money positioning with extremal Z-score

- Defined Risk: Known maximum loss per contract (~$746 per contract)

- Major Catalyst Capture: March expiration captures Q4 earnings, advertising scaling, age verification rollout

- Asymmetric Upside: If bull case plays out ($90-95), returns could be 50-100%+

- 75-day Time Value: Sufficient time for thesis to develop, multiple catalyst windows

- High Conviction Strike: $80 represents 4.4% rally, achievable with positive earnings

Estimated P&L:

- Cost: ~$746 per contract (current pricing $7.46 × 100 shares)

- Profit Scenario: Stock rallies to $90 = $10.00 intrinsic value, $254 profit per contract (34% gain)

- Home Run: Stock rallies to $95 = $15.00 intrinsic value, $754 profit per contract (101% gain!)

- Loss Scenario: Stock below $80 at expiration = lose entire premium ($746 per contract)

- Breakeven: ~$87.46 (strike + premium paid)

Entry timing:

- Enter NOW if you believe in advertising platform surprise and earnings beat

- OR wait until post-earnings if IV crushes and stock consolidates (may get better entry)

- Size appropriately: 5-10 contracts = $3,730-7,460 total risk

Position management:

- Take profits if stock hits $85-90 before expiration (don't be greedy)

- Cut losses if stock breaks below $72 support (thesis invalidated)

- Consider rolling to later expiration if stock consolidating near $80 at expiration

- Monitor earnings carefully - be ready to adjust based on guidance quality

Position sizing: Risk only 2-5% of options portfolio (this is directional speculation)

Risk level: Moderate (can lose 100% of premium) | Skill level: Intermediate

Aggressive: Call Spread to Reduce Cost (ADVANCED)

Play: Buy call spread to reduce cost while maintaining upside exposure

Structure: Buy $80 calls, Sell $90 calls (March 20 expiration)

Why this could work:

- Reduced Cost: Selling $90 calls offsets cost of buying $80 calls (estimated $3-4 net debit vs $7.46 for naked calls)

- Defined Risk AND Reward: Maximum loss = net debit, maximum gain = $10 spread width minus debit

- Still Bullish: Capturing move from $76.63 to $80-90 range (5-17% upside)

- Better Risk/Reward: Potentially 2:1 or 3:1 risk/reward vs 1:1 for naked calls

- Same Catalyst Exposure: March expiration still captures earnings and advertising platform scaling

Why this requires caution:

- Capped Upside: If stock runs to $95+, you only capture gains to $90 (leave money on table)

- Complexity: Two-legged position requires understanding of spreads

- Assignment Risk: Short call could be assigned early if stock moves deep ITM

- Wider Spreads: Lower liquidity may result in slippage on entry/exit

Estimated P&L (adjust based on actual pricing):

- Cost: ~$3-4 net debit per spread (buy $80 call $7.46, sell $90 call ~$3.50-4.50)

- Max Profit: $6-7 if RBLX above $90 at expiration (150-175% ROI!)

- Max Loss: $3-4 if RBLX below $80 at expiration (100% loss of debit)

- Breakeven: ~$83-84 (lower than naked call breakeven of $87.46)

Entry timing:

- Enter if you want upside exposure with less capital at risk

- Better suited for traders who think stock reaches $85-90 but unlikely to exceed $95

Position sizing: Risk only 3-5% of options portfolio

Risk level: Moderate-High (defined risk spread, requires spread knowledge) | Skill level: Advanced

CRITICAL WARNING - DO NOT attempt unless you:

- Understand vertical call spreads and maximum profit/loss mechanics

- Can monitor position and manage early assignment risk if stock moves deep ITM

- Accept that upside is capped at $90 even if stock rallies to $100+

- Have experience with multi-leg options strategies

Risk Factors

Don't get caught by these potential landmines:

-

Q4 Earnings Binary Event (30-40 days away): Results expected mid-February create MASSIVE volatility risk. Stock could gap 10-20% either direction based on bookings ($2.05B target), advertising revenue disclosure, and 2026 guidance. Implied move of 18.7% through March suggests market pricing significant uncertainty. Historical precedent shows gaming/metaverse stocks can move 15-30% on earnings surprises. Options pricing substantial risk.

-

JPMorgan "Digestion Year" Warning: Multiple analysts (JPMorgan, UBS, Wolfe) downgraded citing 2026 as transition year with bookings growth slowing from 52% (2025) to sub-20% (2026). Margin compression of ~100bps expected. Elevated expectations from 2025 viral hits (Grow a Garden) may not repeat. Street consensus average PT of $141 implies 84% upside, but recent downgrades show growing caution. Valuation requires continued execution.

-

Russia Ban Overhang: Loss of ~8 million monthly users (up to 10M DAU per JPMorgan) from December ban creates structural headwind. Resolution uncertain despite RBLX willingness to comply. Geopolitical tensions could prevent restoration of access. Lost engagement and revenue difficult to replace in near-term. If ban becomes permanent, represents 5-7% DAU headwind.

-

Child Safety Litigation Risk: ~60 active lawsuits nationwide plus state AG investigations (Texas, Tennessee) create headline risk and potential financial liability. Tennessee AG called RBLX "digital equivalent of creepy cargo van" - serious reputational damage. Unquantified settlement costs could be material. Age verification rollout addresses concerns but litigation takes years to resolve. Parent/user trust critical for platform growth.

-

Viral Hit Dependency: Q3/Q4 2025 exceptional growth driven by Grow a Garden (created by 16-year-old in 3 days, achieved 22.3M concurrent users). UBS warns engagement cooling as viral momentum fades. No certainty of future viral hits emerging. Platform relies on creator-generated content - unpredictable and difficult to forecast. 2026 could see engagement normalization.

-

Advertising Platform Unproven at Scale: While 1,000+ brands using ads with strong completion rates (90%+), total revenue contribution still small relative to Robux sales. Morgan Stanley $1.2B 2026 projection requires rapid scaling. Competition from established gaming ad platforms (Unity, AppLovin). Developer adoption of rewarded ads critical. Monetization per user needs validation at scale.

-

Developer Cost Inflation: Creator payouts rose 85% YoY in Q3 2025 ($427.9M), pressuring margins. DevEx rate increased 8.5% to $0.0038 per Robux. As platform grows, must pay creators more to retain talent. Epic Games offering 0% commission through 2026 creates competitive pressure. Revenue share dynamics could shift unfavorably, compressing margins beyond expected 100bps.

-

Insider Selling Signals: CEO David Baszucki sold $5.67M on December 18, 2025. Pattern of 53 sell transactions with 0 buys over 5 years. Net 9.95M shares sold over 18 months. While sales under 10b5-1 pre-planned arrangements, persistent selling raises questions about management confidence at current valuation. Optics concerning for retail investors.

-

Competitive Threats Intensifying: Epic Games expanding Fortnite creator economy with better revenue splits (50% take rate after 2026 vs RBLX ~71%). Minecraft maintaining comparable engagement. New metaverse platforms emerging. RBLX's 58% youth user base (<16 years old) vulnerable to platform switching as they age. Network effects strong but not impenetrable.

-

Profitability Timeline Uncertain: Despite revenue growth and positive cash flow ($442.6M free cash flow in Q3), GAAP profitability remains "several more years" away. Operating losses continue. Adjusted EBITDA margins expected to compress in 2026. At $53.6B market cap, investors paying for future profitability that keeps getting pushed out. Valuation vulnerable if path to profitability extends further.

-

Macro Headwinds: Consumer spending on virtual goods highly discretionary. Economic slowdown or recession would pressure bookings growth. Youth users dependent on parental spending. In-game purchases vulnerable to budget cuts. At current valuation, stock has minimal recession protection. Tech sector weakness could pressure growth stocks regardless of fundamentals.

-

Options Gamma Dynamics: Stock trading just below $78 resistance with major call resistance at $80 (this strike). Market makers hedging large call positions will sell into rallies, creating mechanical resistance. Breakout requires sustained buying pressure to overcome dealer hedging. Current positioning shows limited momentum.

The Bottom Line

Real talk: Someone just committed $1.5 MILLION to RBLX calls with a $80 strike 72 days out. This isn't a gamble - it's a calculated bet on RBLX's advertising platform transformation and Q4 earnings catalyst. With Z-score of 35.44 (EXTREME unusual activity) and Vol/OI ratio of 3.19x, this represents major institutional conviction.

What this trade tells us:

- Bullish on Advertising: Sophisticated player believes advertising revenue will surprise positively in Q4 earnings disclosure

- Earnings Confidence: Positioning ahead of February earnings suggests expectation of beat on bookings ($2.05B+) and strong 2026 guidance

- Technical Breakout Expected: $80 strike targets gamma resistance level, betting stock breaks through current $76-78 range

- 72-Day Timeline: March expiration captures Q4 earnings, advertising platform scaling, age verification rollout, potential Russia resolution

- High Conviction: $1.5M premium represents serious capital commitment, not a lottery ticket

This IS a "advertising platform breakout" signal - it's betting on underappreciated revenue driver materializing.

If you own RBLX:

- HOLD through earnings: This institutional call buy validates bullish thesis for Q4 results

- Watch for advertising revenue disclosure: First detailed breakdown could surprise positively

- Set upside targets: $80-85 range achievable if earnings beat and 2026 guide strong

- Protect downside: Mental stop at $72 support to limit risk if thesis breaks

- Consider adding: Pullback to $74-75 offers better entry to add to position

If you're watching from sidelines:

- February earnings is THE catalyst: Wait for results before major positioning

- Post-earnings clarity: Q4 results will reveal advertising traction, Russia impact, 2026 outlook

- Entry levels: Pullback to $72-74 support would offer excellent risk/reward (7-10% below current)

- Confirmation needed: Strong bookings growth (>$2.05B), advertising revenue validation, 2026 guidance >20% growth

- Longer-term catalysts: Advertising platform scaling ($1.2B 2026 potential), age verification success, creator economy growth all support bull case into 2026

If you're considering options:

- March $80 calls (copying this trade) offer asymmetric upside if earnings beat

- Smaller position sizing: 5-10 contracts ($3,730-7,460 risk) provides exposure without excessive risk

- Call spreads: Buy $80/sell $90 reduces cost, caps upside but improves risk/reward

- Wait for earnings: Post-earnings IV crush may offer better entry prices

- Defined risk critical: Only risk capital you can afford to lose completely

Mark your calendar - Key dates:

- February 5-18, 2026 - Q4 2025 earnings report (THE MAJOR CATALYST)

- February 2026 - Post-earnings analysis, advertising revenue disclosure, 2026 guidance

- January 2026 - Age verification global rollout completion

- March 20, 2026 - Options expiration for this $1.5M call trade

- Q1 2026 - Advertising platform scaling metrics, potential Russia resolution

Final verdict: RBLX's advertising platform represents a genuine transformation from pure virtual goods monetization to diversified revenue streams with higher margins. Morgan Stanley's $1.2B 2026 ad revenue projection, 1,000+ brand adoption, and 90%+ completion rates suggest early product-market fit. The $1.5M institutional call bet signals sophisticated buyers believe Street is underestimating advertising upside. However, execution risks remain (JPMorgan "digestion year," child safety litigation, Russia ban, viral hit dependency).

This is a high-conviction bullish bet on advertising platform success and Q4 earnings beat. The risk/reward favors patient bulls who can weather near-term volatility.

Position for the upside. Respect the risks. Let earnings reveal the path forward. The advertising opportunity is real - the question is timing and magnitude.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 35.44 reflects this specific trade's size relative to recent RBLX history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 15-20% gaps either direction. The call buyer may have complex portfolio objectives not applicable to retail traders.

About Roblox Corporation: Roblox Corporation operates a global online platform enabling users to create, share, and play games in a user-generated 3D environment. The company monetizes through virtual currency (Robux) sales, digital advertising, and licensing, with a market cap of $53.61 billion in the Electronic Gaming & Multimedia industry.

Sources:

- Roblox Market Cap - MacroTrends

- Roblox Market Cap - Companies Market Cap

- Roblox Market Cap - Stock Analysis

- Roblox Corporation Stock - Yahoo Finance

- RBLX Catalyst Research Report (internal analysis, January 7, 2026)