RCAT LEAP Bet - $3.2M Defense Drone Play!

📅 October 13, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $3.2M on Red Cat Holdings January 2027 calls - that's a 2+ year bet on this defense drone maker hitting $20+ (41% upside from current $14.15)! With the U.S. Army contract ramping up and earnings coming November 14th, this isn't retail speculation - it's a patient institutional play on America's drone revolution. Translation: Big money believes RCAT is just getting started! 🚀

📊 Company Overview

Red Cat Holdings, Inc. (RCAT) is a drone technology company building the hardware and software that powers military operations with:

- Market Cap: $1.55 Billion (Stock Analysis)

- Industry: Prepackaged Software / Defense Technology

- Employees: 115

- Primary Business: Military drones (Black Widow ISR systems), fixed-wing VTOL systems (Trichon), and precision strike FPV drones (FANG)

- Strategic Focus: Defense and government sectors after divesting consumer brands (Fat Shark, Roto Riot) in February 2024

This isn't your hobbyist drone company - RCAT builds battle-tested systems for the U.S. Army and NATO allies. Think of them as the picks-and-shovels play for modern warfare's shift to unmanned systems.

💰 The Option Flow Breakdown

The Tape (October 13, 2025):

| Time (ET) | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | Open Interest | Contract Size | Spot Price | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:58:51 AM | RCAT | MID | BUY | CALL | 2027-01-15 | $1,560,000 | $20.00 | 3,000 | 4,700 | 3,000 | $14.15 | $5.20 |

| 11:02:35 AM | RCAT | MID | BUY | CALL | 2027-01-15 | $1,560,000 | $20.00 | 3,000 | 4,700 | 3,000 | $14.16 | $5.20 |

Total Investment: $3,120,000 across 6,000 contracts (3,000 + 3,000)

🤓 What This Actually Means

This is a long-term bullish LEAP play - the sophisticated way to bet on a transformation story! The trader:

- Invested $3.2M in calls with 2+ years until expiration (January 15, 2027)

- Bet on RCAT climbing from $14.15 to $20+ (41% gain needed)

- Paid $5.20 per share = $520 per contract for the leverage

- Break-even at expiration: $25.20 ($20 strike + $5.20 premium)

- Maximum gain: Unlimited if RCAT takes off

- Maximum loss: $3.2M if RCAT stays below $20

Why this timeline matters: The 2027 expiration gives RCAT ample time to execute on its massive U.S. Army contract, scale production, and prove out the defense drone thesis. This isn't a quick flip - it's a calculated bet on America's shift to unmanned warfare systems.

Unusual Score: Significantly elevated activity - this type of multi-million dollar LEAP positioning happens a few times per year in small-cap defense names.

📈 Technical Setup / Chart Check-Up

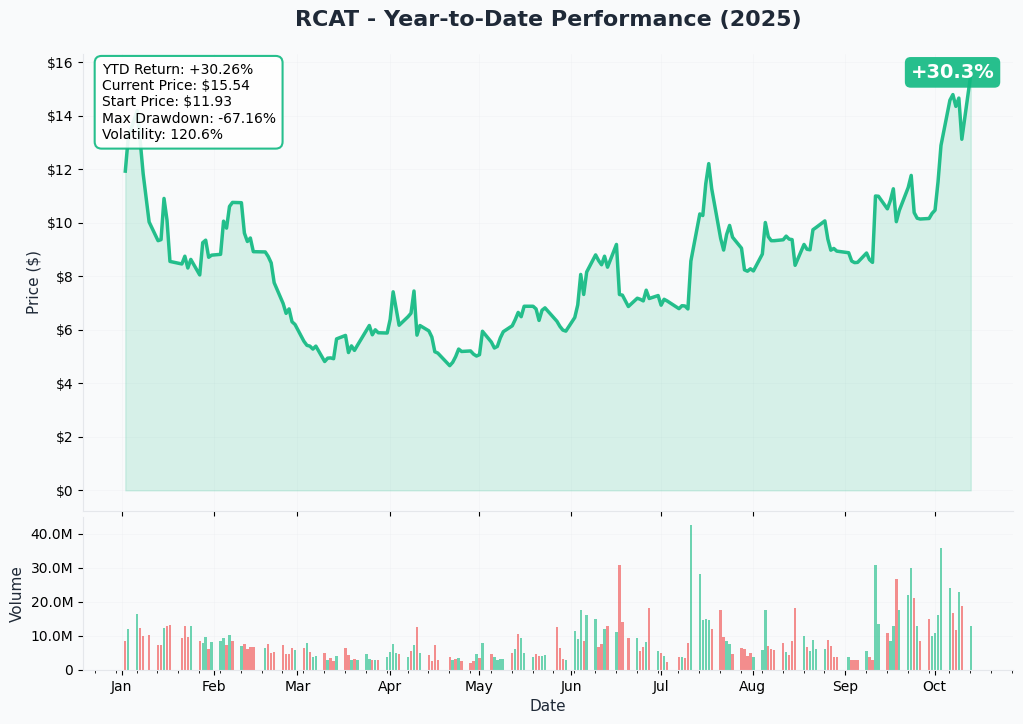

YTD Performance Chart

Red Cat has been on an absolute tear this year with +30.3% YTD performance! But here's where it gets interesting - this isn't a smooth ride. After starting the year around $11.93, RCAT rocketed to early highs near $13, then experienced a brutal -67.2% max drawdown bottoming around $5 in March.

Key observations:

- Extreme volatility: 120.6% implied volatility - this stock moves BIG

- Recovery pattern: Strong V-shaped recovery from March lows back to current $15.54

- 52-week range: Massive $2.66 - $16.70 range shows the wild swings

- Recent momentum: October surge bringing stock back to YTD highs

- Volume spikes: Institutional interest picking up significantly

The chart screams "high-beta defense play" - when it works, it works spectacularly. When it doesn't, buckle up for the ride down.

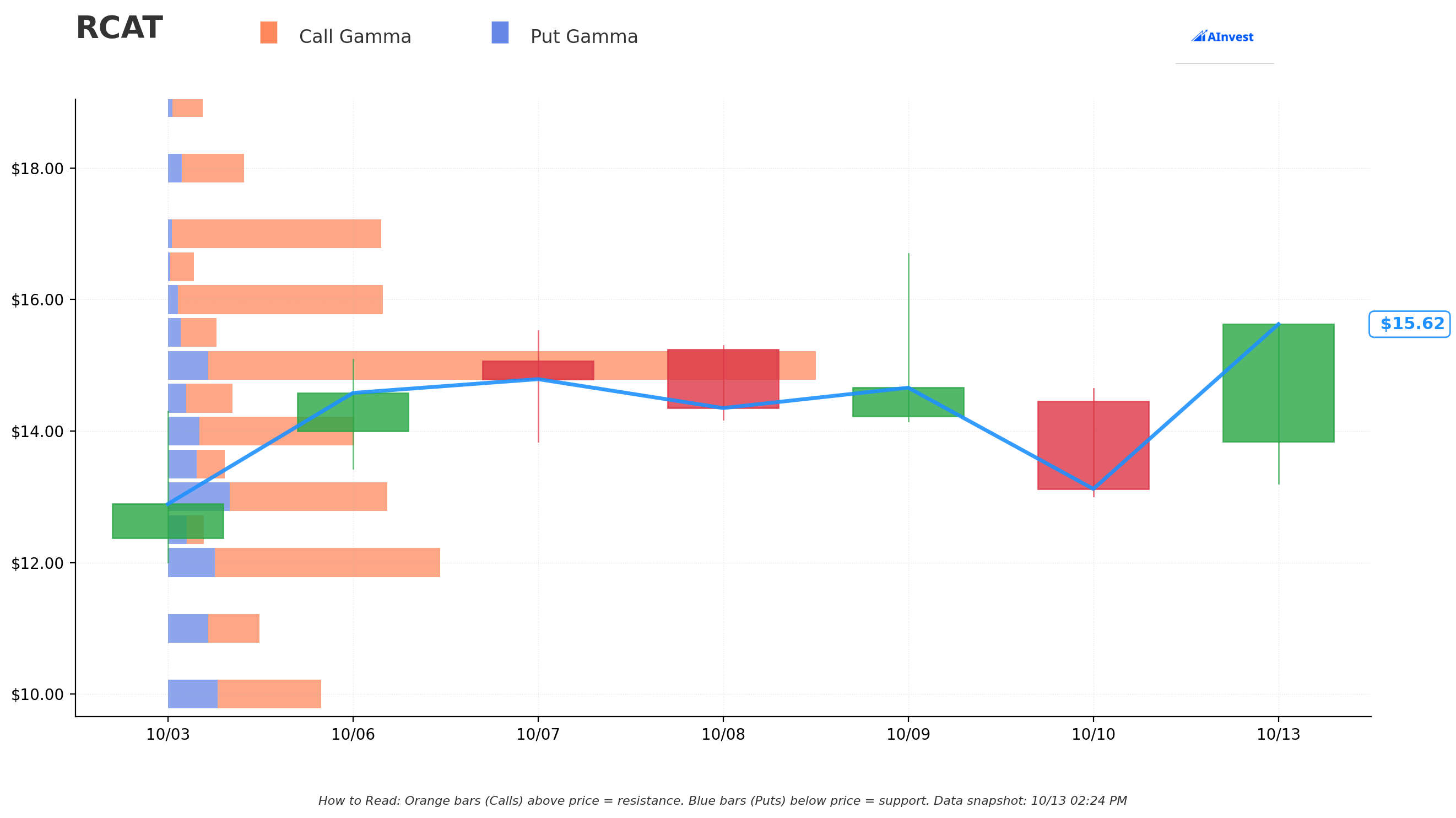

Gamma-Based Support & Resistance Analysis

Current Price: $15.62

The gamma landscape tells a fascinating story about where options traders are positioning:

🟠 Resistance Levels (Call Gamma Above Price):

- $16.00 - Nearest ceiling with 1.01M net GEX (2.4% away) - immediate test zone

- $17.00 - Major gamma wall with 1.05M net GEX (8.8% away) - key breakthrough level

- $18.00 - Secondary resistance at 0.25M net GEX (15.2% away) - bull case target

🔵 Support Levels (Put Gamma Below Price):

- $15.50 - Immediate floor with 0.12M net GEX (just 0.8% down) - holding strong

- $15.00 - Major support with 2.92M net GEX (4.0% down) - massive gamma cushion

- $14.50 - Secondary support at 0.14M net GEX (7.2% down)

- $13.00-$14.00 - Deep support zone with solid gamma concentration

What this means: The gamma setup shows a bullish bias with total call GEX of 12.34M versus put GEX of 2.41M. Market makers are long gamma, which means they'll dampen volatility near key strikes. The massive $15 support level (2.92M GEX) acts as a magnet - price wants to gravitate there. The $16-$17 resistance zone represents where market makers will start selling into rallies.

For the $20 call buyer, this gamma landscape suggests a grind higher rather than an explosive move - perfect for a LEAP that has time to work.

🎪 Catalysts

🔜 Upcoming Events

Q2 FY2025 Earnings - November 14, 2025

- Wall Street anxiously awaiting execution updates on the U.S. Army SRR contract

- Revenue guidance range: $80-120M for full year (potential 13x growth vs 2024)

- Q1 2025 guidance details

- Breakdown: $25-65M SRR Black Widow, $25M Non-SRR Black Widow, $25M Edge 130, $5M Fang FPV

- Key metrics: SRR production ramp, manufacturing scale-up with ESAero partnership

- Cash position: $66.9M in cash/receivables post $150M capital raise

- Analyst expectations: 39.3% revenue growth per annum, 32.6% earnings growth per annum

U.S. Army Full-Rate Production Decision - H2 2025

- Transition from Low Rate Initial Production (started January 2025) to full-rate manufacturing

- Contract target: Up to 5,880 Black Widow systems over 5 years

- July 2025: 690 SRR systems contract executed under TD3 LRP

- This is THE catalyst that could unlock the LEAP thesis

NATO International Sales Ramp - 2025-2026

- Black Widow approved for NATO NSPA catalogue in September 2025

- Streamlined procurement for 32 NATO member nations and partners

- Accelerates international sales cycles significantly

- International revenue could become a surprise catalyst

Palantir AI Integration Deployment - Ongoing

- Warp Speed manufacturing OS implementation for cost optimization

- GPS-free visual navigation technology for contested environments

- High-margin software revenue potential

- Expected to enhance drone capabilities and reduce manufacturing costs

Unmanned Surface Vessels (USV) Market Entry - 2025-2026

- Maritime domain expansion announced May 2025

- Multi-domain operations strategy (air, land, sea)

- Total addressable market (TAM) expansion opportunity

✅ Recently Completed

$150M Public Offering - September 2025

- Capital raise completed to fund production scale-up

- Strengthened balance sheet to $66.9M cash/receivables

- Additional $30M funding secured after Q1 2025

- Eliminates near-term funding risk

U.S. Army SRR Contract Win - November 2024

- Beat out Skydio to become Army's drone of choice

- Program of Record status = multi-year revenue visibility

- Already executing with 690 units under contract (July 2025)

Consumer Business Divestiture - February 2024

- Sold Fat Shark and Roto Riot brands to focus on defense

- Strategic pivot to higher-margin government contracts

- Simplified business model for defense-focused operations

🎲 Price Targets & Probabilities

Using gamma levels, catalyst timing, and defense sector dynamics:

🚀 Bull Case (30% chance)

Target: $20-$25 by January 2027

The Perfect Storm Scenario:

- U.S. Army contract hits full-rate production by Q1 2026

- International NATO sales exceed $50M annually by 2026

- Palantir integration creates high-margin software revenue stream

- Additional defense contracts awarded (Navy, Air Force, international)

- Stock reaches analyst price targets in 2025-2026, then extends to $20+ by late 2026

- Wall Street consensus: $16.50 average target (16.29% upside)

- Price target range: $15.00-$18.00

- Analyst ratings: 5 analysts with Strong Buy consensus (1 sell, 2 buy, 2 strong buy)

LEAP Outcome: Highly profitable - buyer makes 2-4x return on $3.2M investment

Why it could happen: Revenue guidance projects 13x growth, and defense spending on unmanned systems is a bipartisan priority

- Seeking Alpha: 13x revenue growth potential

- Simply Wall St: 39.3% revenue growth per annum forecasted

- If RCAT executes even 70% of guidance, the stock deserves a higher multiple

😐 Base Case (45% chance)

Target: $14-$18 range through 2026

The Steady Execution Scenario:

- Army contract ramps but faces typical defense program delays

- Revenue grows to $60-80M range (lower end of guidance)

- Stock trades sideways with volatility in $14-18 channel

- Gamma resistance at $16-17 caps upside moves

- Company remains unprofitable but shows path to breakeven

- Current cash position: $66.9M provides runway

LEAP Outcome: Modest gain or loss depending on exit timing - needs stock above $25 to fully profit

Why it's likely: Defense programs rarely execute perfectly on schedule. Current cash position is strong but profitability still distant

- Q2 2025 financial position

- Stock could chop around current levels as market waits for proof of execution

😰 Bear Case (25% chance)

Target: $8-12 retest of support

The Disappointment Scenario:

- Army contract delayed or scaled back due to budget constraints

- Manufacturing issues delay full-rate production approval

- Competition intensifies from Skydio or other defense contractors

- Broader market correction hits speculative defense names

- Another dilutive capital raise needed

LEAP Outcome: Total loss of $3.2M premium paid

Why it's possible: RCAT remains unprofitable with significant execution risk. The company experienced a -67% drawdown in 2025 already. Defense budgets can shift quickly with changing political winds. Small cap defense stocks are inherently volatile.

💡 Trading Ideas

🛡️ Conservative: Wait-and-See with Defined Risk

Play: Bull put spread (November 2025 expiration)

Cost: Collect $0.50-0.80 credit per spread Risk: $200 per spread max loss ($2 spread width - credit) Reward: Credit collected if RCAT stays above $12

Why this works: Massive gamma support at $13-15 levels provides cushion. You profit if RCAT stays above $12 (23% downside buffer from current). November earnings catalyst provides defined event to trade around.

⚖️ Balanced: Ride the Catalyst Wave

Play: Debit call spread (March 2026 expiration)

Cost: $1.50-2.00 per spread ($150-200 per contract) Risk: Premium paid Reward: $4.00 max profit ($2-2.50 net gain at $20)

Why this works: Targets the same $20 level as the whale trade but with defined risk and shorter timeline. Gives RCAT 5 months to hit Army production milestones and prove out the thesis. March 2026 timeframe captures H2 2025 full-rate production decision.

🚀 Aggressive: Follow the Smart Money LEAPs

Play: Buy January 2027 LEAPs

Buy $20 calls (same as whale trade) or $17.50 calls

Cost: $5.20 for $20 strikes, $6.50-7.00 for $17.50 strikes Risk: Premium paid (100% loss if RCAT doesn't perform) Reward: Unlimited upside, massive gains if RCAT hits $25-30

Why this works: You're literally copying a $3.2M institutional bet. The 2+ year timeline allows for inevitable defense program delays while capturing the full upside if the Army contract delivers. Lower strike at $17.50 gives you better delta and probability.

Position sizing: Risk no more than 1-2% of portfolio on this speculation. These are lottery tickets with institutional backing, not core positions.

⚠️ Risk Factors

Execution Risk (HIGH):

- Small company (115 employees) scaling to multi-million unit production

- Manufacturing complexity could delay Army contract timelines

- Already experienced -67% max drawdown in 2025 showing volatility risk

Competitive Threats (MEDIUM):

- Skydio and other defense contractors won't give up Army market share easily

- Technology cycles fast in drone warfare - today's winner could be tomorrow's also-ran

- Chinese drone manufacturers provide low-cost competition in commercial markets

Regulatory & Budget Risk (MEDIUM):

- Defense budgets subject to political changes and fiscal constraints

- Army program of record can be delayed, scaled back, or cancelled

- NDAA compliance requirements could change

Profitability Timeline (HIGH):

- Company currently unprofitable with cash burn

- $150M raise was dilutive to existing shareholders

- May need additional capital raises if contract ramp slower than expected

Valuation Risk (HIGH):

- $1.55B market cap on $3.2M quarterly revenue = extremely high multiple

- Stock priced for perfection on Army contract execution

- Any disappointment could trigger 30-50% selloff like seen in March 2025

Implied Volatility Crush (MEDIUM):

- 120.6% IV is extremely elevated - options are expensive

- Post-earnings or post-catalyst, IV could collapse 30-50%

- Time decay on LEAPs is slow but still erodes value

🏁 The Bottom Line

Real talk: This $3.2M LEAP bet is a sophisticated wager that Red Cat Holdings becomes a defense industry winner over the next 2 years. The thesis is compelling - America needs domestic drone manufacturing, RCAT beat Skydio for the Army contract, and revenue could grow 13x:

But let's be honest about what this is: A high-risk, high-reward bet on a tiny company executing flawlessly on a massive government contract. The -67% drawdown earlier this year shows what happens when the market loses confidence.

If you own RCAT stock: The gamma support at $15 is strong - consider riding it but have a stop loss at $13. November 14th earnings will be make-or-break.

If you're watching: Wait for November 14th earnings to get proof of execution. If RCAT hits guidance and confirms Army contract progress, the risk/reward improves dramatically.

If you're copying this trade: Only if you have a 2+ year time horizon and can afford to lose 100% of premium paid. This is venture capital-style risk with options leverage. Size accordingly (1-2% of portfolio max).

Mark your calendar:

- November 14, 2025 - Q2 earnings report (first major test)

- H2 2025 - U.S. Army full-rate production decision (KEY catalyst)

- January 15, 2027 - Option expiration (judgment day)

The whale placed their bet. Now we wait to see if America's drone revolution lifts all boats! 🚁

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. RCAT is a speculative small-cap security with extreme volatility.

About Red Cat Holdings: RCAT is a drone technology company integrating robotic hardware and software for military operations, with a $1.55 billion market cap in the prepackaged software sector. The company specializes in ISR drones (Black Widow), fixed-wing VTOL systems (Trichon), and precision strike FPV drones (FANG) for defense applications.