RDDT $5M Dual Call Buy - Smart Money Betting Big on Reddit Earnings Bounce!

January 29, 2026 | Unusual Activity Detected

The Quick Take

Someone just deployed $5 MILLION across two RDDT call positions at 13:11:50 -- buying 1,709 contracts of the $190 call ($4M) AND 1,709 contracts of the $250 call ($1M), both expiring March 20th. The $190 call is slightly in-the-money at $191.56 spot, while the $250 call is a 31% out-of-the-money lottery ticket. With Reddit down -27% from its January all-time high of $265 and Q4 earnings hitting on February 11th, this trader is loading up on both near-term upside participation and explosive leverage. Translation: A well-capitalized buyer sees this pullback as a gift and is swinging for a major earnings-driven recovery.

Company Overview

Reddit, Inc. (RDDT) is a social media platform where users engage in conversations, explore, and create communities across over 100,000 active subreddits:

- Market Cap: $36.6 Billion

- Industry: Services - Computer Processing & Data Preparation

- Current Price: ~$191.56 (down ~27% from ATH of $265.30)

- Primary Business: Advertising revenue, AI data licensing, community-driven content platform (founded 2005)

The Option Flow Breakdown

The Tape (January 29, 2026 @ 13:11:50):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 13:11:50 | RDDT | MID | BUY | CALL $190 | 2026-03-20 | $4M | $190 | 1,700 | 303 | 1,709 | $191.56 | $23.40 |

| 13:11:50 | RDDT | MID | BUY | CALL $250 | 2026-03-20 | $1M | $250 | 1,700 | 2,800 | 1,709 | $191.56 | $5.85 |

What This Actually Means

This is a high-conviction dual call buy -- the trader is positioned for both moderate and explosive upside. Here is what went down:

- $4M on the $190 call: $23.40 per contract x 1,709 contracts. This strike is $1.56 in-the-money, giving immediate delta exposure. This is the "meat" of the trade -- the trader profits dollar-for-dollar once RDDT clears roughly $213 (breakeven).

- $1M on the $250 call: $5.85 per contract x 1,709 contracts. This strike is 31% out-of-the-money -- a pure lottery ticket that pays off massively if RDDT surges back toward January highs above $250. Breakeven at ~$256.

- Same timestamp, same size: Both legs executed simultaneously with identical contract counts (1,709), confirming this is a single institutional order, not a spread with offsetting legs.

- Volume vs OI on $190C: 1,700 volume against only 303 open interest -- this is clearly an opening position, not a roll or close.

- 50 days to expiration: March 20 captures the February 11 Q4 earnings catalyst plus a full month of post-earnings price action and potential S&P 500 inclusion speculation.

What is really happening here: This trader likely sees Reddit's 27% selloff from the $265 ATH as overdone. The $190 call captures upside if earnings spark any recovery at all. The $250 call is the "home run" bet -- if Q4 results blow past expectations (which Reddit has done every quarter since IPO), the stock could rip back toward $250+ and this $1M position becomes worth multiples of the entry. Think of it as buying both a first-class ticket and a Powerball ticket on the same flight.

Unusual Score: EXTREME -- Volume 1,700 vs OI 303 on the $190 call (5.6x OI turnover) with $5M total premium. This is a multi-million dollar opening position placed in a single clip on a stock that trades modest options volume. Clearly institutional.

Technical Setup / Chart Check-Up

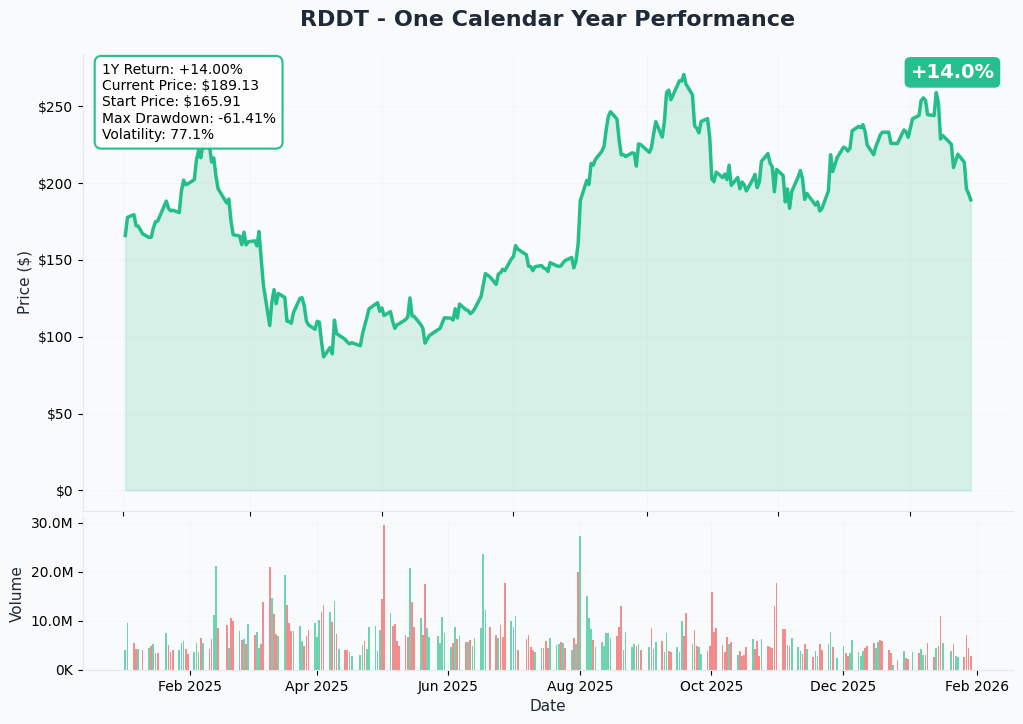

One Calendar Year Chart

RDDT is currently trading at ~$189.58, up +14.3% YTD but down sharply from its January 5 all-time high of $265.30. The chart tells a volatile growth story with a dramatic round trip:

Key observations:

- ATH breakout and reversal: Stock surged to $265.30 in early January on the back of 400% EPS growth and AI data monetization excitement, then sold off hard

- 27% drawdown from peak: The Cleveland Research ad growth warning and Google AI traffic concerns triggered a swift retreat from $265 to sub-$193

- Testing critical support zone: Current price sits near the $190 gamma support level, which could serve as a floor if it holds

- High volatility regime: Daily return standard deviation of 4.99% makes RDDT one of the most volatile large-cap names in the market

- Earnings inflection ahead: February 11 Q4 results represent a clear binary catalyst that could determine the next $30-50 move

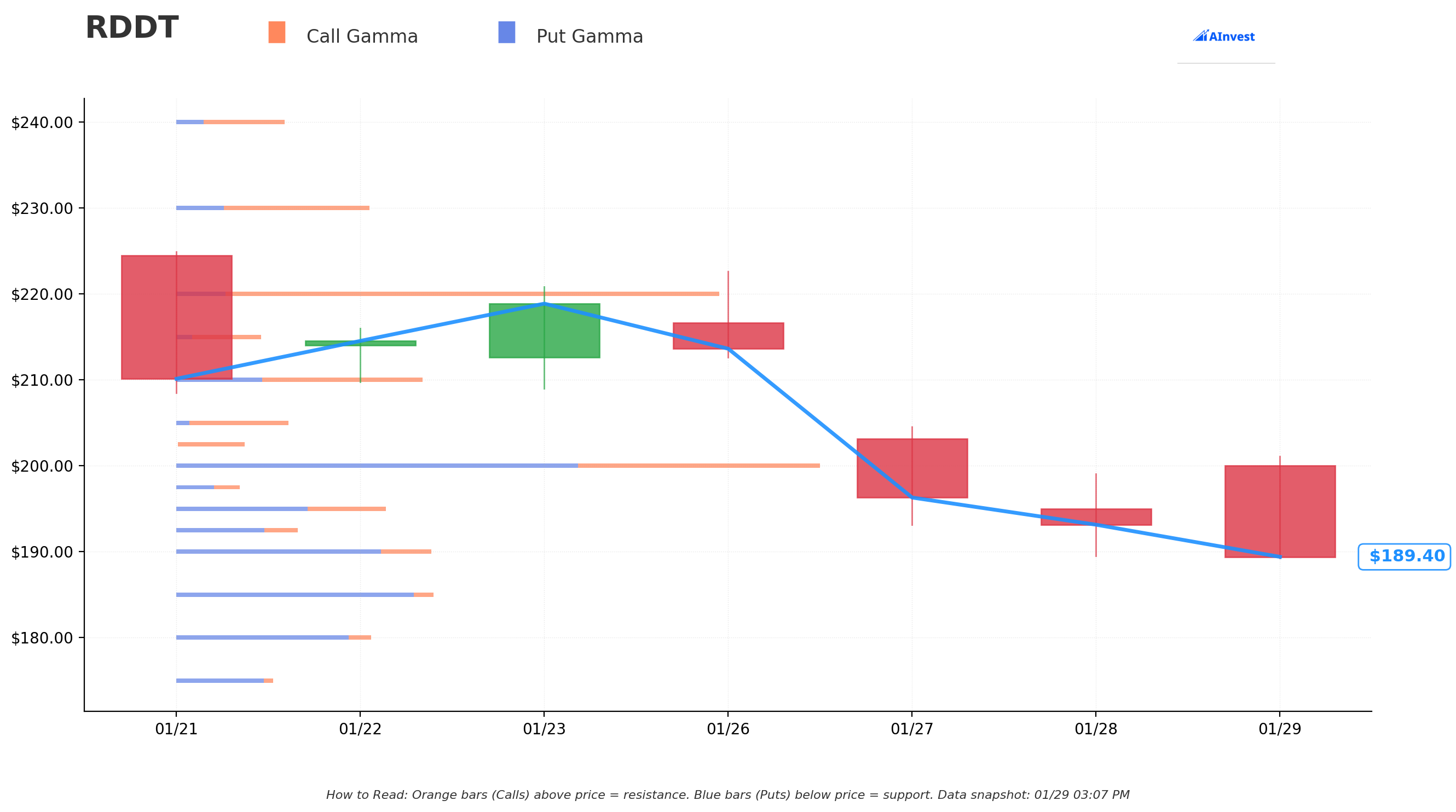

Gamma-Based Support & Resistance Analysis

Current Price: $189.74

The gamma exposure map reveals critical price levels that will govern near-term price action:

Support Levels (Put Gamma Below Price):

- $190 - Immediate support at current price level (being tested now)

- $185 - Secondary support if $190 breaks

- $180 - Major structural floor (break here signals deeper trouble)

- $175 - Extended support zone (disaster scenario)

Resistance Levels (Call Gamma Above Price):

- $192.50 - Immediate overhead resistance

- $195 - Near-term ceiling

- $200 - Psychological round number and key gamma level

- $205 - Secondary resistance

- $210 - Significant gamma wall

- $220 - Upper resistance zone

- $250 - Major strike target (the $250 call strike aligns here)

What this means for traders: RDDT is sitting right at the $190 support level, making this a technically interesting entry point. The call buyer is positioning right at support, which means limited downside to the next gamma level ($185) while having substantial upside room through multiple resistance levels. A strong earnings beat could trigger a breakout through $200, $210, and $220 in succession as dealers unwind hedges.

Notice this: The $190 call strike matches the current support level exactly. The trader is buying at a technically significant floor -- if $190 holds through earnings, the risk/reward is highly asymmetric. If it breaks, the next support is only $5-10 lower.

Net GEX Bias: Bullish -- Call gamma dominates above price, suggesting dealer positioning would amplify upside moves.

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 30 - 1 day): +/-2.7% (+/-$5.06) -- Range: $185.10 - $195.22

- Monthly OPEX (Feb 20 - 22 days): +/-14.2% (+/-$27.01) -- Range: $163.15 - $217.17

- Quarterly (Mar 20 - 50 days - THIS TRADE!): +/-18.9% (+/-$35.85) -- Range: $154.31 - $226.01

Translation for regular folks: Options traders are pricing in a modest 2.7% move by tomorrow, but a MASSIVE 14.2% move through the February OPEX that includes Q4 earnings on February 11th. The market expects significant volatility around this earnings report -- and for good reason. Reddit has beaten EPS estimates every quarter since its IPO, but the recent ad growth warnings and Google AI traffic fears have created genuine uncertainty.

The March 20th expiration (when both trades expire) has an implied range of $154 to $226. This means the $190 call (breakeven ~$213) sits comfortably within the upper half of the expected range. However, the $250 call (breakeven ~$256) is well BEYOND the 1-standard-deviation move -- the buyer needs a move exceeding +31% from current to profit on that leg. This is why it is a lottery ticket: low probability, huge payoff.

Key insight: The monthly implied move of 14.2% captures the earnings event premium. The jump from 2.7% (daily) to 14.2% (monthly) reflects the massive uncertainty around the February 11 report. Smart money is paying for exposure BEFORE this uncertainty resolves.

Catalysts

Immediate Catalysts (Next 14 Days)

Q4 2025 Earnings - February 11, 2026 (13 DAYS AWAY!)

Reddit reports fiscal Q4 results on Wednesday, February 11, 2026 after market close. This is THE catalyst that could validate or invalidate the call buyer's thesis. Wall Street consensus and key expectations:

- Revenue: $655-665M guided by management, consensus ~$660-670M (+53-55% YoY)

- EPS: $0.93-$0.97 consensus (+169% YoY growth)

- Adj. EBITDA Margin: 42% guided

- DAUq: Watch for trajectory toward 120M+ (was 116M in Q3, +20% YoY)

- Ad Revenue Growth Rate: Key concern -- will it decelerate from 74% (Q3) toward the 36% that Cleveland Research warned about?

- AI Data Licensing Revenue: Currently undisclosed as separate line item -- any breakout disclosure would be a major catalyst

Upside surprise potential: Reddit has beaten EPS estimates every single quarter since its March 2024 IPO. Q3 saw 400% EPS growth and 68% revenue growth that smashed consensus. Q4 benefits from holiday ad seasonality AND the first full quarter of Max Campaigns at scale -- early testers saw 27% more conversions and 2.3-4.7x ROAS improvement. If the ad growth deceleration fear proves overblown, this stock could rip back toward $230-250.

Downside risk factors: The Cleveland Research warning about ad growth deceleration and difficulty acquiring new advertisers could prove prescient. If DAUq growth slows or ad ARPU disappoints, the stock could break $180 support and test $165-170.

Historical precedent: Reddit has beaten estimates in every quarter since IPO, with post-earnings moves of +10% to +40% on beats. However, the stock has also shown it can sell off sharply on forward-looking concerns even when backward-looking numbers are strong.

Near-Term Catalysts (Q1-Q2 2026)

S&P 500 Inclusion - Potential Mid-2026

Reddit is approaching its fourth consecutive quarter of GAAP profitability, a key S&P 500 eligibility criterion. Inclusion would force passive index funds to purchase millions of shares, similar to the Tesla re-rating precedent:

- A strong Q4 earnings beat would cement the profitability track record needed for consideration

- Index inclusion typically catalyzes a 15-20% re-rating as passive flows create sustained buying pressure

- Timing aligns perfectly with the March 20 expiration on these call positions

- Remains speculative but is increasingly likely if earnings momentum continues

AI Data Licensing Expansion -- The Hidden Revenue Engine

Reddit is shifting toward "dynamic pricing" for AI training data -- charging based on frequency and utility of content in AI-generated answers:

- Reddit's archive of 1 billion posts and 16 billion comments over 18 years creates a unique moat

- Needham calls Reddit's 100% human-created content "irreplaceable" for LLM training

- Existing deals with Google and OpenAI for training data provide recurring high-margin revenue

- Any new major licensing announcement could serve as an independent catalyst

- Dynamic pricing model means revenue scales with AI industry growth without additional costs

Max Campaigns at Scale -- AI-Powered Ad Revolution

Reddit's "Max Campaigns" AI-powered advertising platform launched at scale in late 2025, with early results showing:

- 17% reduction in CPA (cost per acquisition)

- 27% more conversions for early testers

- ROAS improvements of 2.3x to 4.7x across most verticals

- ~40% cost per conversion reduction vs manually managed campaigns

- US ad spending on Reddit rose 46.3% YoY as of November 2025, outpacing every major social platform

Q4 represents the first full quarter of Max Campaigns operating at scale. If the numbers validate the early metrics, it could meaningfully accelerate advertiser adoption and ARPU growth.

International Expansion -- 35 New Countries

Reddit aims to roll out ad sales to 35 new countries in H2 2026. International revenue was $78.5M in Q1 2025 (+82% YoY), and international DAUq grew 31%. This represents a major untapped revenue opportunity that is not fully priced in.

Risk Catalysts (Negative)

Google AI Traffic Cannibalization -- THE EXISTENTIAL THREAT

Google's AI Overviews and AI Mode have reportedly slashed Reddit's organic traffic by 55% over three years:

- Google drives approximately 50% of Reddit's total traffic -- a structural dependency

- Wells Fargo analyst Gawrelski called this the "beginning of the end" for Reddit's traffic-dependent model, setting a $115 price target (street low)

- Analysts project a potential 30% DAU decline if zero-click search trends persist

- Wells Fargo revised 2026/2027 ad revenue forecasts down 6% and 14% respectively

- This is the single biggest risk to the bullish thesis

$60M Lawsuit -- Tamraz v. Reddit, Inc.

The Tamraz, Jr. v. Reddit, Inc. lawsuit alleges Reddit executives obscured the 55% traffic plunge and assured investors of "robust user growth" while logged-out users (50% of traffic) generated only 15% of ad revenue. This creates legal overhang and potential discovery risk.

Insider Selling -- 367 Consecutive Sales, Zero Purchases

Reddit insiders have executed 367 trades in the past 6 months -- all sales, zero purchases. While post-IPO selling is common, the complete absence of insider buying is a notable red flag for long-term conviction.

Cleveland Research Ad Growth Warning

Analyst Ross Walthall warned that Reddit may struggle to find new advertisers and existing advertisers are unlikely to increase spend. He projects 2026 revenue growth of 36% -- below consensus -- citing competition from TikTok, Snap, and OpenAI's ChatGPT for ad dollars. RDDT dropped 7.52% on this report alone.

Valuation Premium -- 125x+ Trailing P/E

At 125-138x TTM P/E, Reddit trades at extreme premiums versus the Interactive Media & Services industry average of 15.44x. Even on forward estimates ($3.86 FY2026E EPS), the stock trades at ~50x. There is zero margin for error at this valuation.

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the March 20th expiration:

Bull Case (30% probability)

Target: $230-$265

How we get there:

- Q4 earnings CRUSH expectations -- revenue $680M+ (above high-end guide), EPS $1.10+ (beating $0.97 consensus)

- Max Campaigns metrics validate the AI ad revolution -- advertisers increasing budgets, not pulling back

- DAUq hits 125M+ showing Google traffic fears are overblown (users coming directly to app)

- AI data licensing revenue disclosed for first time -- even $20-30M quarterly would reignite the narrative

- S&P 500 inclusion chatter intensifies as profitability streak extends

- Analyst upgrades cascade -- Needham's $300 target and Jefferies' $325 target attract momentum buyers

- Short covering amplifies the move as bears capitulate

- Stock breaks through $200, $210, $220 gamma resistance levels in succession

Key metrics needed:

- Ad revenue growth staying above 50% (disproving Cleveland Research thesis)

- DAUq acceleration showing Google dependency is declining

- Margin expansion continuing (42%+ EBITDA margin)

- International revenue growth above 80% YoY

$190 call P&L at $250: $60 intrinsic - $23.40 cost = $36.60 profit per contract x 1,709 = ~$6.3M gain (157% ROI) $250 call P&L at $265: $15 intrinsic - $5.85 cost = $9.15 profit per contract x 1,709 = ~$1.6M gain (156% ROI)

Base Case (45% probability)

Target: $185-$215 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- Q4 earnings meet or modestly beat consensus ($660-670M revenue, $0.95-1.00 EPS)

- Ad growth decelerates as expected but not as badly as Cleveland Research warned

- DAUq shows steady growth but nothing spectacular (118-122M range)

- Market gives credit for the beat but remains cautious on forward growth trajectory

- Stock bounces to $200-215 on earnings relief rally, then consolidates

- Google traffic concerns remain an overhang preventing full recovery to ATH

- Implied volatility crush post-earnings reduces option values

- Trading within gamma support ($185) and resistance ($210-220) bands

$190 call P&L at $210: $20 intrinsic - $23.40 cost = -$3.40 loss per contract (with some time value remaining, likely ~breakeven) $250 call P&L at $210: Likely worth $1-2 with time value remaining, loss of ~$4-5 per contract

Bear Case (25% probability)

Target: $150-$180 (BREAK BELOW SUPPORT)

What could go wrong:

- Q4 earnings show ad growth deceleration to 40-45% range -- validates Cleveland Research bearish thesis

- DAUq growth stalls at 116-118M -- Google AI traffic cannibalization confirmed in the data

- Management lowers 2026 guidance citing macro headwinds and competitive pressure

- Tamraz lawsuit discovery reveals internal metrics confirming traffic decline

- Additional insider selling accelerates post-lockup

- Break below $185 gamma support triggers cascade to $175, then $165

- Broader market selloff drags high-multiple growth stocks lower

- Wells Fargo's $115 bear case gains credibility

$190 call P&L at $165: Expires worthless, loss = $23.40 x 1,709 = -$4M (100% loss) $250 call P&L at $165: Expires worthless, loss = $5.85 x 1,709 = -$1M (100% loss) Total loss in bear case: -$5M (entire premium)

Trading Ideas

Conservative: Wait for Earnings Clarity, Buy the Dip

Play: Stay on sidelines until after February 11th earnings, then position on confirmed support

Why this works:

- Earnings in 13 days creates binary event risk with +/-14.2% implied move -- too dangerous to chase

- Implied volatility elevated pre-earnings -- options are EXPENSIVE right now

- Stock already down 27% from ATH -- could be catching a falling knife if Google fears are validated

- Better entry likely post-earnings after IV crush reduces option premiums by 30-50%

- The $190 gamma support level will either be confirmed or broken by earnings -- either outcome gives you clarity

Action plan:

- Watch February 11 earnings closely for: ad revenue growth rate (above or below 50%), DAUq trajectory (120M+ bullish, below 117M bearish), and any AI data licensing disclosure

- If earnings beat AND stock holds above $190: buy shares or the April $200 calls on the post-earnings pullback

- If earnings disappoint and stock breaks $180: do NOT try to catch the knife -- wait for stabilization at $165-170 gamma support

- If stock gaps to $220+ on blowout earnings: consider selling puts at $200 strike to get paid for waiting

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid the binary event risk entirely. Get clarity on whether the Google AI traffic fears are warranted before committing capital.

Balanced: Post-Earnings Bull Call Spread (Copy the Smart Money)

Play: After earnings, buy a call spread targeting the recovery

Structure: Buy $200 calls, sell $230 calls (March 20 expiration -- same as the institutional trade)

Why this works:

- IV crush after earnings makes spreads 30-50% cheaper -- buy AFTER volatility drops

- Defined risk spread ($30 wide = $3,000 max risk per spread minus premium received)

- Targets the recovery zone that institutional money is clearly betting on

- March 20 expiration gives 5+ weeks of post-earnings price action

- If Reddit beats (as it has every quarter since IPO), the stock should recover toward $210-230 minimum

- Essentially "following" the $5M institutional buyer at better post-IV-crush prices

Estimated P&L (adjust after seeing post-earnings IV):

- Pay ~$10-12 net debit per spread post-earnings (vs $15-18 now)

- Max profit: $18-20 if RDDT above $230 at March expiration (150-170% ROI)

- Max loss: $10-12 per spread (defined and limited)

- Breakeven: ~$210-212

Entry timing:

- Wait 1-2 days post-earnings (by Feb 13) for IV collapse

- Only enter if stock holds above $190 support (confirms floor)

- Skip if stock breaks below $180 (trend has changed)

Position sizing: Risk only 2-5% of portfolio. This is directional speculation, not a core holding.

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Pre-Earnings Lottery Ticket (ADVANCED ONLY!)

Play: Buy far OTM calls betting on an earnings blowout, similar to the institutional $250 call position

Structure: Buy April $250 calls (cheap OTM lottery ticket)

Why this could work:

- Reddit has beaten earnings EVERY quarter since IPO with massive upside surprises

- Q4 holiday seasonality + Max Campaigns at scale could produce a monster quarter

- Stock is down 27% from ATH -- a blowout beat could trigger violent short covering

- April expiration gives extra month vs March trade for thesis to play out

- S&P 500 inclusion speculation could layer on additional buying pressure

- At ~$3-5 per contract, the defined loss is small but the payoff on a 30%+ move is enormous

Why this could blow up (SERIOUS RISKS):

- THE GOOGLE PROBLEM: If AI Overviews are genuinely cannibalizing Reddit traffic, no earnings beat will save the stock

- INSIDER SELLING: 367 consecutive insider sales suggests the people who know the business best are not buying

- VALUATION: At 125x+ trailing P/E, even a beat might not push the stock to $250 if forward growth decelerates

- IV CRUSH: Even if stock moves 10-15%, the IV collapse post-earnings could still result in a LOSS on far OTM calls

- BINARY RISK: Need a 31%+ move to $250 just to break even -- this is well beyond the implied 18.9% move

- COMPLETE LOSS LIKELY: Probability of RDDT reaching $250 by March/April is well below 20%

Estimated P&L:

- Cost: ~$3-5 per contract (keep position small -- $500-2,000 max)

- Home run: RDDT at $270 = $20 intrinsic, profit = $15-17 per contract (300-400% ROI)

- Likely outcome: Expires worthless = 100% loss of premium paid

CRITICAL WARNING - DO NOT attempt unless you:

- Can afford to lose the ENTIRE premium (very likely outcome)

- Understand this is a <20% probability bet with asymmetric payoff

- Have experience with OTM option decay mechanics

- View this as entertainment/speculation, not investment

- Keep position sizing to 0.5-1% of total portfolio maximum

Risk level: EXTREME (expect to lose entire premium) | Skill level: Advanced only

Probability of profit: ~15-20% (significantly below 50%)

Risk Factors

Do not get caught by these potential landmines:

-

Q4 Earnings binary event in 13 days: Results Wednesday February 11th after close create MASSIVE volatility risk. Options pricing +/-14.2% implied move through February OPEX. Reddit has beaten estimates every quarter since IPO, but the Cleveland Research ad growth warning and Google traffic fears mean expectations are genuinely uncertain. A miss or weak guidance could send the stock below $170 quickly. A blowout beat could rip it back toward $230+. The implied move range of $163-$217 tells you the market sees both scenarios as realistic.

-

Google AI Overviews -- existential traffic threat: Google's AI features have allegedly slashed Reddit's organic traffic by 55% over three years. Google drives approximately 50% of Reddit's total traffic. If logged-out users continue declining, ad revenue could face structural headwinds that no amount of product innovation can overcome. Wells Fargo calls this the "beginning of the end" with a $115 target. This is not a fixable problem -- it is a platform dependency risk.

-

Insider selling pattern is alarming: 367 consecutive insider trades -- ALL SALES, zero purchases over the past 6 months. While post-IPO selling is normal, the complete absence of any insider buying at a stock that is down 27% from its highs is a meaningful signal. The people with the best information about the business are not putting their own money back in.

-

$60M lawsuit creates legal overhang: The Tamraz v. Reddit lawsuit alleges executives concealed the traffic decline and misrepresented user growth. Even if the suit is ultimately dismissed, discovery could reveal internal metrics that contradict public statements. Legal risk compounds the fundamental uncertainty.

-

Valuation leaves zero margin for error: At 125-138x trailing P/E and ~50x forward P/E, Reddit is priced for flawless execution. The stock needs to deliver 60%+ revenue growth in FY2025 and 24%+ in FY2026 just to maintain current multiples. Any deceleration below expectations -- which Cleveland Research is already flagging -- could trigger a multiple compression that sends the stock to $130-150. There is no valuation floor here.

-

The $250 call requires an extraordinary move: The options market implies an 18.9% move by March 20 (range $154-$226). The $250 strike requires a 31% move from current levels -- well beyond one standard deviation. While the $190 call is a reasonable directional bet, the $250 call has a high probability (80%+) of expiring worthless. The trader knows this -- they allocated $4M to the $190 call and only $1M to the $250 call, reflecting the probability weighting.

-

Ad competition intensifying: Cleveland Research flagged competition from TikTok, Snap, and OpenAI's ChatGPT for advertising budgets. As AI chatbots begin monetizing with ads (ChatGPT reportedly exploring ad-supported tiers), Reddit faces competition from BOTH traditional social platforms and emerging AI platforms. This is a two-front war.

-

Extreme volatility cuts both ways: With 4.99% daily return standard deviation, RDDT can move $10+ on no news. The 27% drawdown from ATH in just three weeks shows how fast sentiment can shift. Even if the fundamental thesis is correct, the volatility can shake out positions before the thesis plays out. Options buyers face time decay working against them every single day.

The Bottom Line

Real talk: Someone just spent $5 MILLION buying RDDT calls after the stock plunged 27% from all-time highs, positioning aggressively for a Q4 earnings recovery just 13 days before the report. This is a contrarian buy-the-dip trade with conviction -- the $190 call for near-term participation and the $250 call for explosive upside if the selloff proves to be an overreaction.

What this trade tells us:

- The buyer believes the Cleveland Research warning and Google AI traffic fears are OVERBLOWN relative to the selloff magnitude

- They expect Q4 earnings on February 11 to re-confirm Reddit's growth trajectory (as every prior quarter has done)

- The $190 call (ITM, $4M) is the core position -- this is a directional bet that RDDT recovers from current levels

- The $250 call (31% OTM, $1M) is the "what if it rips" position -- if S&P 500 inclusion or a monster beat sends the stock back to $250+, this $1M becomes worth $5-10M+

- The simultaneous execution with identical 1,709 contract size on both legs confirms a single institutional decision-maker

- The March 20 expiration captures earnings, post-earnings analyst reactions, and several weeks of potential momentum

This is a CONTRARIAN BET against the prevailing bearish sentiment -- not a sure thing.

If you own RDDT:

- This trade validates holding through earnings IF you believe in the long-term thesis

- The $190 support level is critical -- if it breaks on earnings, the next floor is $175-180

- Consider writing covered calls at $220-230 to generate income while waiting for recovery

- Set a mental stop at $175 -- below that level, the Google AI traffic thesis is winning

If you are watching from the sidelines:

- February 11th after close is the defining moment -- do NOT enter before earnings unless you are prepared for a 15%+ move either direction

- Post-earnings entry at $195-205 (on a beat with modest rally) offers better risk/reward than chasing here

- The analyst consensus target of $247-265 implies 30-37% upside, but that requires the growth story to remain intact

- Watch these Q4 metrics carefully: DAUq (120M+ = bullish), ad revenue growth rate (50%+ = bullish, <45% = concerning), and any AI data licensing disclosure

If you are bearish:

- Do NOT short ahead of earnings -- Reddit has beaten estimates every quarter since IPO and could squeeze bears violently

- Post-earnings put spreads (March $180/$160) offer defined-risk downside exposure after IV crush

- The $175-180 zone is the key level -- a break below that confirms the Google AI traffic bear thesis

- Wells Fargo's $115 target is the extreme bear case -- only realistic if multiple quarters of decelerating growth confirm structural decline

Mark your calendar -- Key dates:

- February 11 (Wednesday) after market close -- Q4 FY2025 earnings report (13 DAYS!)

- February 12 (Thursday) -- Post-earnings price action and analyst reactions

- February 20 -- Monthly OPEX (+/-14.2% implied move window closes)

- March 20 -- Quarterly OPEX, expiration of BOTH call positions in this trade

- Mid-2026 (estimated) -- S&P 500 inclusion decision window

- H2 2026 -- International ad sales rollout to 35 new countries

Final verdict: Reddit's growth story remains genuinely compelling -- 400% EPS growth, an irreplaceable AI data moat, Max Campaigns delivering 2-5x advertiser ROAS, and potential S&P 500 inclusion are all real catalysts. BUT, the Google AI traffic threat is equally real and potentially existential. The 27% selloff reflects genuine uncertainty, not an irrational panic. The $5M institutional call buy says one sophisticated player disagrees with the bears -- but 367 insiders selling says the people closest to the business are not as confident.

February 11 earnings will resolve this debate. Be patient. Let the data speak. The smart play is to position AFTER you see the Q4 numbers, not before.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The unusual options activity discussed reflects this specific trade's characteristics relative to RDDT's recent history -- it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 15%+ gaps either direction. The $250 call has a high probability (80%+) of expiring worthless. The institutional buyer may have portfolio context (hedges, stock positions, tax considerations) not applicable to retail traders.

About Reddit, Inc.: Reddit is a social media platform where users engage in conversations, explore, and create communities. Founded in 2005, it hosts over 100,000 active communities and generates revenue from advertising and AI data licensing, with a market cap of $36.6 billion in the Services - Computer Processing & Data Preparation industry.