🛡️ RIVN $4.8M Bear Put Spread - Smart Money Hedging Before R2 Launch! 🚨

📅 December 5, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed a $4.8 MILLION Bear Put Spread on Rivian this morning at 11:38:32! This sophisticated hedge bought 11,000 contracts at both $10 and $8 strike puts expiring December 17, 2027 - a LEAP position betting on significant downside over the next 2 years. With RIVN at $18.06, trading near 52-week highs after strong Q3 results, institutional money is buying deep protection ahead of the make-or-break R2 launch in H1 2026. Translation: Smart money expects volatility and wants downside insurance as RIVN approaches its critical profitability inflection point!

📊 Company Overview

Rivian Automotive (RIVN) is an electric vehicle manufacturer focused on adventure vehicles and commercial delivery vans:

- Market Cap: $22.14 Billion (mid-cap growth story)

- Industry: Motor Vehicles & Passenger Car Bodies

- Current Price: $18.06 (near 52-week high of $18.10)

- Primary Business: R1T electric truck, R1S SUV, Electric Delivery Vans (EDV) for Amazon, upcoming R2 midsize SUV

- Employees: 14,861

- Key Products: R1 platform vehicles, R2 launching H1 2026 at $45,000 starting price

💰 The Option Flow Breakdown

The Tape (December 5, 2025 @ 11:38:32):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:38:32 | RIVN | ASK | BUY | PUT $10 | 2027-12-17 | $2.8M | $10 | 11,000 | 14,000 | 11,000 | $18.06 | $2.50 |

| 11:38:32 | RIVN | ASK | BUY | PUT $8 | 2027-12-17 | $2.0M | $8 | 11,000 | 6,000 | 11,000 | $18.06 | $1.81 |

🤓 What This Actually Means

This is a Bear Put Spread - a classic bearish hedge structure! Here's the breakdown:

- 💸 Total premium paid: $4.8M ($2.8M for $10 puts + $2.0M for $8 puts)

- 🎯 Net debit per spread: $4.31 ($2.50 - $1.81) × 11,000 contracts = $4.74M

- 🛡️ Long-dated protection: 742 days to expiration (December 17, 2027)

- 📊 Strike selection: $10 strike = 44.6% below current price, $8 strike = 55.7% below

- 🏦 Max profit: $2.00 per spread × 11,000 = $2.2M (if RIVN below $8 at expiration)

- 📉 Max loss: $4.31 per spread × 11,000 = $4.74M (if RIVN above $10 at expiration)

- ⚖️ Breakeven: $10.00 - $4.31 = $5.69 (68.5% below current price!)

What's really happening here: This trader is betting on or hedging against a SEVERE downside scenario for RIVN over the next 2 years. By buying the $10 strike puts and simultaneously buying $8 strike puts, they're creating a defined-outcome spread that profits if RIVN falls below $10 by December 2027. The 2-year timeframe covers critical catalysts: R2 launch (H1 2026), Georgia factory construction, path to 2027 profitability target, and potential cash burn concerns.

This is likely either:

- Portfolio protection - Hedging a large long equity or call position accumulated during the 66% rally from April lows

- Directional bet - Bearish thesis that RIVN execution risks outweigh upside potential

- Volatility play - Locking in protection before R2 launch uncertainty

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score 16.64 and 5.07) - The $10 strike saw 11,000 volume against 14,000 open interest, while the $8 strike saw 11,000 volume against just 6,000 OI. Both trades are classified as "EXTREMELY_UNUSUAL" with Vol/OI ratios of 0.786 and 1.833 respectively. This is HIGH_ACTIVITY signaling institutional positioning, not retail speculation.

📈 Technical Setup / Chart Check-Up

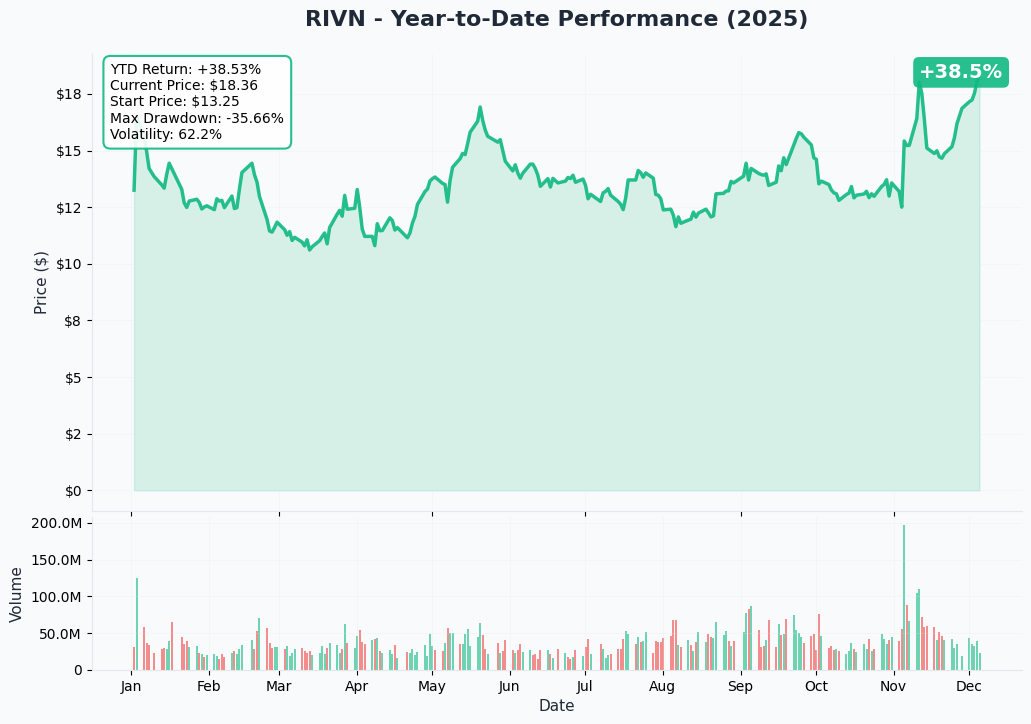

YTD Performance Chart

RIVN has rallied hard from the April lows - up 66% from $10.86 to $18.06 and sitting just below the 52-week high of $18.10. The stock started 2025 at $13.92, making it up +29.7% YTD. However, the broader picture shows significant volatility with a 52-week range of $10.36 to $18.10.

Key observations:

- 🚀 Strong Q3 rally: Vertical move from $13 in September to $18+ in December on Q3 earnings beat

- 📈 Breakout confirmed: Smashed through $16 resistance in November, holding above

- ⚠️ Still down 85% from IPO peak: Traded near $180 post-IPO in November 2021, massive correction since

- 📊 Volume spike: Institutional accumulation visible in October-November following VW partnership news

- 🎢 High volatility: This isn't a stable stock - moves 5-10% on single news items regularly

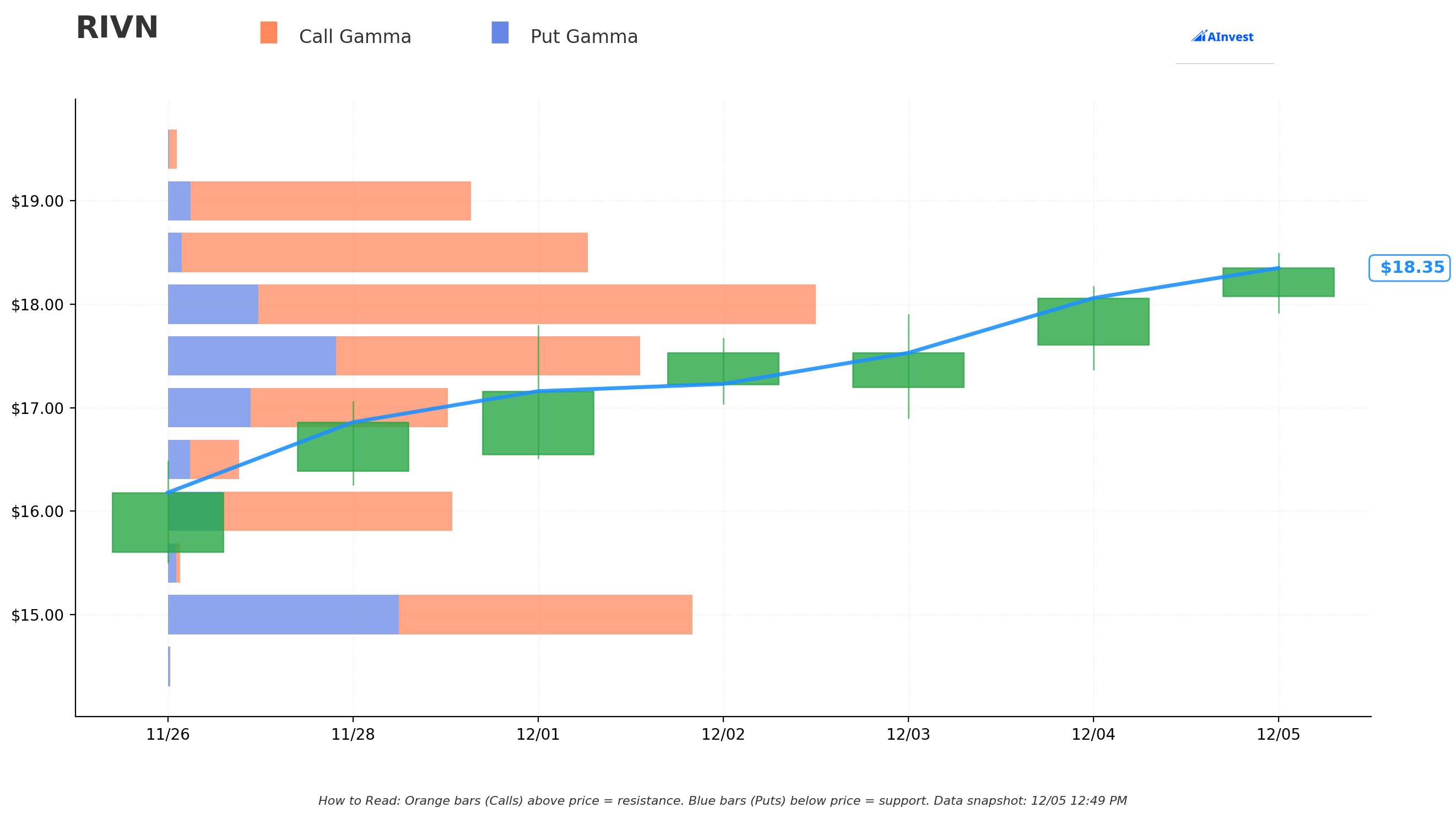

Gamma-Based Support & Resistance Analysis

Current Price: $18.43

The gamma exposure map reveals critical price magnets that will govern near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $18.00 - Immediate support with 26.29M total gamma (strongest nearby floor) - 2.3% below

- $17.50 - Secondary support at 22.72M gamma (dealers buying dips here) - 5.0% below

- $17.00 - Solid floor with 12.52M gamma - 7.8% below

- $16.50 - Minor support at 3.36M gamma - 10.5% below

- $16.00 - Important structural level with 12.34M gamma - 13.2% below

- $15.00 - Major floor with 24.86M gamma (second-highest put level) - 18.6% below

🟠 Resistance Levels (Call Gamma Above Price):

- $18.50 - Immediate ceiling with 21.10M gamma (very close!) - 0.4% above

- $19.00 - Secondary resistance at 15.73M gamma - 3.1% above

- $20.00 - Major ceiling zone with 33.95M gamma (STRONGEST RESISTANCE) - 8.5% above

- $21.00 - Extended upside at 3.25M gamma - 13.9% above

What this means for traders: RIVN is trading in a narrow band just below $18.50 resistance and above $18.00 support. The massive $20.00 resistance level (33.95M gamma - the single largest concentration) creates natural selling pressure and will be difficult to break without major catalysts. The stock is effectively range-bound between $18-20 in the near term.

Net GEX Bias: Bullish (168.95M call gamma vs 55.86M put gamma) - Overall positioning remains bullish with nearly 3:1 call/put ratio, suggesting market makers are positioned for upside. However, this also means gamma resistance above will be fierce.

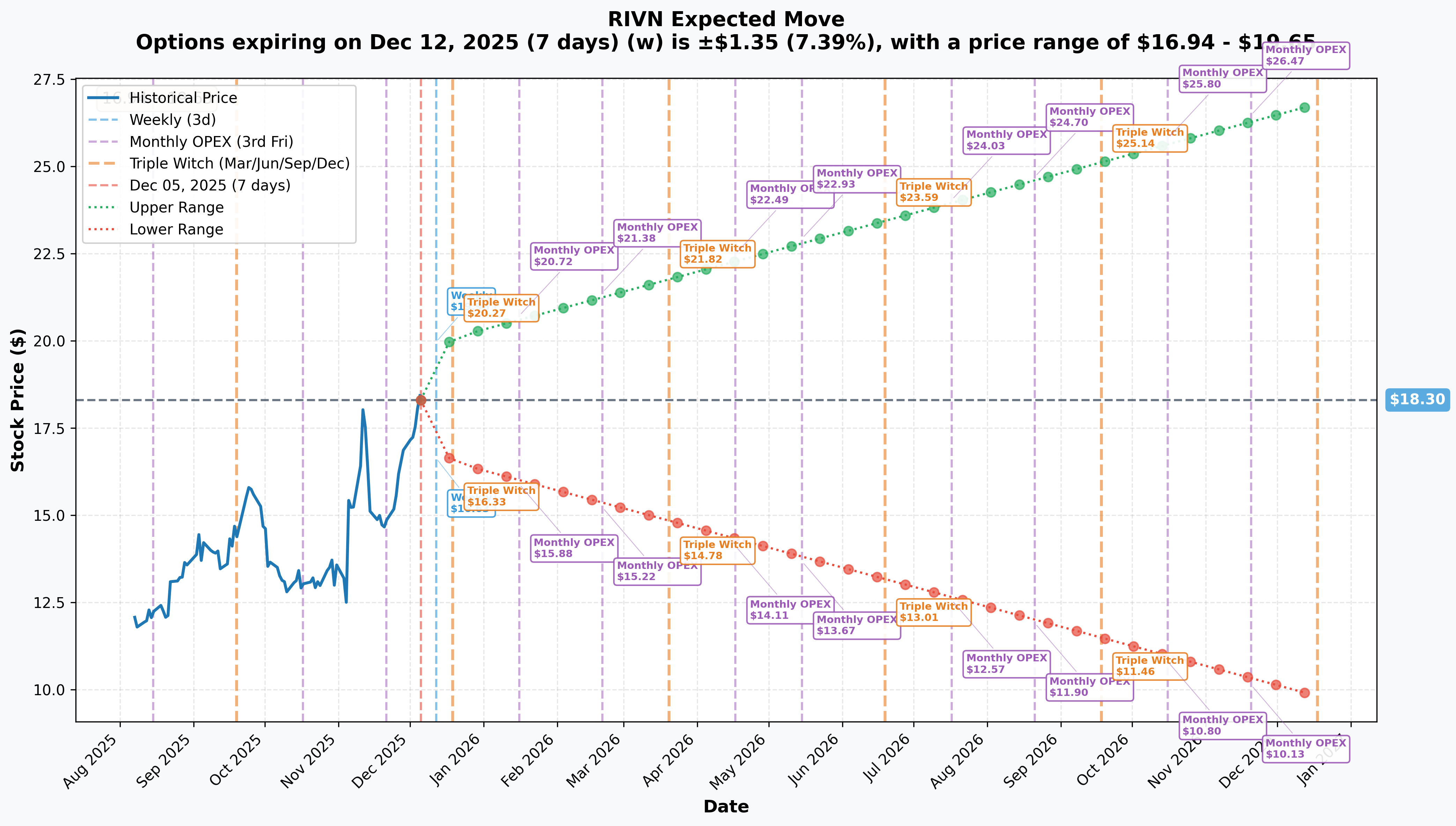

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 7 days): ±$1.35 (±7.39%) → Range: $16.94 - $19.65

- 📅 Monthly OPEX (Dec 19 - 14 days): ±$1.79 (±9.78%) → Range: $16.51 - $20.09

- 📅 Quarterly Triple Witch (Dec 19 - 14 days): ±$1.79 (±9.78%) → Range: $16.51 - $20.09

- 📅 Yearly LEAPS (Dec 18, 2026 - 378 days): ±$8.50 (±46.46%) → Range: $9.80 - $26.80

Translation for regular folks: Options traders are pricing in a 7.4% move ($1.35) by next week and nearly 10% move ($1.79) through December OPEX. That's substantial volatility for a mid-cap stock! The yearly LEAPS show a MASSIVE 46.5% implied move over the next year, with a lower bound of $9.80 - meaning the market sees a real possibility RIVN could trade in single digits within 12 months if execution falters.

Key insight: The 46.5% annual implied volatility and $9.80 lower range for 1-year LEAPS aligns PERFECTLY with the bear put spread positioning. The put buyer is betting on the lower end of this range materializing - if RIVN falls to $9.80 or below, these spreads become highly profitable. The market is essentially confirming this downside risk is real, not just bearish speculation.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Last 3 Months)

Q3 2025 Earnings Beat - November 4, 2025 📊

Rivian delivered its best quarter ever, posting the company's first quarterly gross profit and crushing Wall Street expectations:

- 💰 Loss per share: $0.65 adjusted vs. $0.72 expected (beat by 10%)

- 📈 Revenue: $1.56 billion vs. $1.5 billion expected (up 78% YoY)

- 🎯 Gross Profit: $24 million vs. consensus of -$38.6M loss (major inflection!)

- 🚗 Deliveries: 13,201 vehicles (up 32% YoY) - highest quarterly total in 2025

- 🏭 Production: 10,720 vehicles in Q3

The gross profit milestone included $130M automotive loss offset by $154 million from VW joint venture and software/services revenue. This validates the business model is working, though automotive operations aren't yet profitable standalone.

Stock reaction: RIVN rallied from $13 pre-earnings to $18+ post-earnings on the beat and raised confidence in R2 timeline.

Volkswagen Joint Venture One-Year Anniversary - November 2025 🤝

The Rivian-VW joint venture (RV Tech) hit its first anniversary with major progress:

- 💰 Total deal value: Up to $5.8 billion from VW Group

- 👥 Team size: Over 1,500 employees across U.S., Canada, Sweden, Serbia, Berlin

- 🎯 First milestone: R2 launch in H1 2026 will showcase software-defined vehicle platform

- 🚗 VW timeline: First VW vehicle using RV Tech platform will be ID.Every1 in 2027; electric Golf in 2029

However, reports surfaced of tensions over software customization and ICE vehicle adaptation, with Audi and Porsche programs experiencing delays. This partnership is CRITICAL for cash flow but execution remains uncertain.

Amazon EDV Expansion - October-November 2025 📦

- 🇨🇦 50 Rivian EDVs deployed in Vancouver area - first fleet outside U.S.

- 🇺🇸 More than 20,000 Rivian vans operating domestically

- 📊 Over 1.5 billion packages delivered globally, on track for 100,000 vans by 2030

Major EDV Recall - December 2025 ⚠️

Rivian recalled 34,824 electric delivery vehicles (2022-2025 EDVs) due to seat belt pretensioner cable damage. Zero incidents reported but requires OTA software update and potential hardware replacement. Not a major financial impact but raises quality control questions.

DOE Loan Closure & Georgia Groundbreaking - September 2025 🏭

- 💰 Closed $6.6 billion DOE loan to finance Georgia manufacturing facility

- 🏗️ Groundbreaking at Stanton Springs North site - deep utilities installation began August 2025

- 📅 Funds accessible through September 2028 once construction resumes

Federal EV Tax Credit Loss - January 2025 💸

Rivian vehicles lost eligibility for $7,500 federal EV tax credit effective January 1, 2025, as battery components no longer meet sourcing requirements. R1T/R1S previously qualified for $3,750 in 2024. This creates competitive disadvantage vs. eligible rivals and pressures demand.

🚀 Upcoming Catalysts (Next 6 Months - THE CRITICAL PERIOD!)

R2 Production Launch - Q1 2026 (MAKE OR BREAK!) 🎯

This is THE catalyst that determines Rivian's future. The $45,000 midsize SUV represents the company's transition from luxury to mass market:

- 🏭 Manufacturing validation builds: Begin end of 2025 (IMMINENT!)

- 🚗 Customer deliveries: First half of 2026

- 💰 Starting price: $45,000 maintained despite tariff pressures

- 📊 Production capacity: 215,000 units annually at expanded Normal, IL facility

- 🎯 Target market: Direct Model Y competitor targeting mainstream buyers

R2 Specifications:

- Range: 270-330+ miles depending on battery pack

- Performance: Tri-motor 0-60 in under 3.0 seconds

- Charging: 10-80% in under 30 minutes; NACS (Tesla) compatible

- Size: 15.2" shorter than R1S, competitive with Model Y

Why this matters for the put trade: ANY R2 delays, quality issues, production ramp problems, or cost overruns would be catastrophic. The 2027 expiration puts capture the entire R2 launch and ramp phase. If R2 flops or underdelivers, RIVN could easily trade to $10 or below, making these spreads highly profitable.

Q4 2025 Earnings - Late January/Early February 2026 📊

Rivian will report full-year 2025 results with critical updates on:

- ✅ Final 2025 delivery numbers (guidance: 41,500-43,500 units)

- 💰 Gross profit performance vs. breakeven target

- 🏭 R2 pre-production status and any timeline updates

- 📈 2026 financial guidance including R2 ramp expectations

Georgia Factory Construction - Q1 2026 🏗️

- 🏭 Vertical construction begins: Q1 2026 following September 2025 groundbreaking

- 📊 Project scale: 16 million sq ft on 1,800-acre campus in two 200,000-unit phases

- 💰 Investment: $5 billion total, creating 7,500 jobs by 2030

- 🚗 Vehicle production: R2 and R3 starting 2028

- 🎯 Combined capacity: 615,000 annual units between Normal + Georgia by 2028

The Georgia factory won't produce vehicles until 2028, but construction progress (or delays) will be closely watched as a leading indicator of execution capability.

R3/R3X Crossover Production - 2027-2028 🚗

Smaller, more affordable R3 launching after R2 ramp:

- 📅 Production start: After R2 stabilizes, likely 2027-2028

- 🏭 Manufacturing: Georgia facility

- 💰 Target: More affordable than R2's $45K price point

- 🎯 Variants: R3 standard + performance-oriented R3X

⚠️ Risk Catalysts (What Could Make These Puts Print)

Cash Burn Sustainability 💸

CFRA described Rivian's cash burn as "highly concerning":

- 💰 Current cash: $7.1 billion as of Q3 2025

- 🔥 Annual burn: ~$3.8-4.15B ($2.0-2.25B EBITDA loss + $1.8-1.9B CapEx)

- ⏰ Runway: 18-20 months at current burn rate WITHOUT VW/DOE funding

- 🎯 Profitability target: EBITDA breakeven by 2027 IF R2 succeeds

If R2 delays or underperforms, Rivian may need dilutive capital raise that crushes share price.

Weakening EV Demand 📉

Rivian's 2025 delivery guidance implies 17% decline vs. 2024:

- 📊 2025 guidance: 41,500-43,500 units vs. ~51,000 in 2024

- 🚗 R1T/R1S demand softening as market matures

- 💰 Tax credit loss creates $7,500 competitive disadvantage

- ⚖️ Macro uncertainty could pressure luxury EV purchases

Tesla Competition & Price War 🥊

Tesla Model Y remains dominant with declining but still massive market share:

- 📊 Tesla U.S. EV share: 48.5% in Q2 2025 (down from 51% in Q1)

- 💰 Model Y price cuts could pressure R2 pricing/margins

- 🔌 Supercharger network advantage over Rivian's third-party charging

- 🏭 Tesla's scale and cost structure far superior

Valuation Risk 📊

At $18.06, RIVN trades at:

- 💰 Market cap: $22.14 billion

- 🔥 Price/Sales: ~5.7x (for unprofitable company!)

- 📉 Still burning $2B+ annually

- ⚠️ No path to profitability until 2027 - everything depends on R2

Analysts have mixed ratings with average price target of $14.30-14.83 - BELOW current price! This suggests current rally may be overextended.

VW Joint Venture Tensions 🤝

Reports of friction over software customization and Audi/Porsche program delays raise questions about the $5.8B partnership's viability. If VW reduces scope or timeline, Rivian loses critical near-term cash flow.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through December 2027 expiration:

📈 Bull Case (20% probability)

Target: $25-30+ (Puts expire worthless)

How we get there:

- 🚀 R2 launch CRUSHES expectations - production ramp smooth, demand strong, margins better than expected

- 🏭 Manufacturing execution flawless - 215K annual capacity achieved by late 2026

- 💰 Path to profitability accelerates - EBITDA breakeven by 2026 instead of 2027

- 🤝 VW partnership expands - additional revenue streams, technology licensing to other OEMs

- 🇺🇸 Government support increases - additional DOE funding, EV incentives restored

- 📊 Market share gains in adventure/lifestyle EV segment - brand loyalty strengthens

- 🌍 International expansion successful - European/other markets open up

Key metrics needed:

- R2 deliveries >50,000 in 2026, >150,000 in 2027

- Gross margins turn positive by late 2026

- Cash burn reduced to <$1B annually by 2027

- Stock breaks above $20 gamma resistance sustainably

Probability assessment: Only 20% because requires PERFECT execution across all fronts over 2 years. Rivian has never achieved sustained profitability. Competition fierce. Macro uncertain.

🎯 Base Case (50% probability)

Target: $12-20 range (Puts lose value but don't expire worthless)

Most likely scenario:

- ✅ R2 launches on time in H1 2026 but ramp is slower than hoped (production issues, supplier constraints)

- 📊 Deliveries solid but not spectacular - 30-40K R2s in 2026, ramping to 80-100K in 2027

- 💰 Gross profit achieved but path to EBITDA breakeven extends to 2028

- 🔥 Cash burn continues at $1.5-2B annually - requires tapping VW/DOE funding

- 🤝 VW partnership progresses but with some delays and scope reductions

- 🏭 Georgia factory construction on schedule but production timeline conservative

- ⚖️ Stock consolidates in $12-20 range as market waits for proof of profitability

- 📉 Periodic selloffs to $12-14 on negative news, rallies to $18-20 on positive catalysts

Put P&L in Base Case:

- Stock at $15 on Dec 2027: $10 put worth $0 (OTM), $8 put worth $0 (OTM) = Total loss -$4.31M

- Stock at $12 on Dec 2027: $10 put worth $0 (OTM), $8 put worth $0 (OTM) = Total loss -$4.31M

Why 50% probability: This is the "muddle through" scenario where Rivian executes adequately but not brilliantly. The stock trades in a range reflecting uncertainty about profitability timeline. The put spread loses money but doesn't blow up completely.

📉 Bear Case (30% probability)

Target: $5-10 (PUTS PRINT!)

What could go wrong:

- 😰 R2 launch delays to H2 2026 or later - production problems, quality issues, cost overruns

- 🚨 R2 demand disappoints - pricing pressure from Tesla, consumer preference shifts

- 💸 Cash crisis emerges - forced to raise capital at depressed prices, massive dilution

- 🇨🇳 Macro recession hits luxury EV demand - R1 sales collapse, R2 DOA

- 🤝 VW partnership scales back or terminates - removes critical funding source

- 📊 Path to profitability extends to 2029+ or never achieved

- 🏭 Georgia factory delayed or canceled - removes long-term capacity expansion

- ⚖️ Competition intensifies - Tesla, traditional OEMs, Chinese EVs squeeze Rivian out

- 💰 Regulatory credit revenue dries up - removes key near-term cash source

- 🔨 Stock breaks below $15 support, cascades to $10, then single digits

Critical support levels:

- 🛡️ $18.00: Immediate gamma floor - already tested, MUST HOLD

- 🛡️ $15.00: Major support (24.86M gamma) - break triggers momentum selling

- 🛡️ $10.00: This put strike - psychological floor, likely heavy buying

- 🛡️ $8.00: Deep floor at second put strike - disaster scenario

Put P&L in Bear Case:

- Stock at $10 on Dec 2027: $10 put worth $0 (ATM), $8 put worth $0 (OTM) = Breakeven

- Stock at $8 on Dec 2027: $10 put worth $2, $8 put worth $0 (ATM) = Profit $2 - $4.31 = -$2.31 loss

- Stock at $6 on Dec 2027: $10 put worth $4, $8 put worth $2 = Profit $6 - $4.31 = +$1.69 gain (+39% ROI)

- Stock at $5 on Dec 2027: $10 put worth $5, $8 put worth $3 = Profit $8 - $4.31 = +$3.69 gain (+85% ROI)

- Stock at $3 on Dec 2027: $10 put worth $7, $8 put worth $5 = Profit $12 - $4.31 = +$7.69 gain (+178% ROI!)

Probability assessment: 30% because multiple negative catalysts would need to align, but execution risk is VERY real. Rivian has never made annual profit, cash burn is extreme, and R2 success is far from guaranteed. The put buyer clearly sees meaningful downside risk.

💡 Trading Ideas

🛡️ Conservative: Stay Away Until R2 Clarity

Play: Avoid RIVN until R2 launch proves successful

Why this works:

- ⏰ Too much binary execution risk over next 6-12 months

- 💸 Cash burn of $2B+ annually creates existential risk if R2 fails

- 📊 Stock at 52-week highs with no margin of safety - all good news priced in

- 🎯 Better entry likely post-R2 launch if successful (dips to $15-16) or much lower if it fails

- 🔥 The $4.8M institutional bear put spread signals smart money is WORRIED

- 📉 Implied volatility of 46.5% annually shows massive uncertainty - why fight it?

Action plan:

- 👀 Monitor R2 production validation builds (Dec 2025 - Jan 2026)

- 🎯 Watch Q4 2025 earnings (late Jan/early Feb) for R2 timeline updates

- ✅ Need to see first customer deliveries (H1 2026) and initial quality/demand feedback

- 📊 Look for pullback to $12-15 range for stock entry IF R2 proves successful

- ⏰ Revisit mid-2026 after R2 ramp demonstrates viability

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -50-70% drawdown if R2 fails. Get better entry if execution proves successful. Preserve capital.

⚖️ Balanced: Small Put Position Copying Smart Money

Play: Buy smaller version of institutional bear put spread after any rally above $19

Structure: Buy $10 puts, Buy $8 puts (December 17, 2027 expiration - SAME as this $4.8M trade)

Why this works:

- 🎯 Defined risk spread - maximum loss is premium paid ($4.31 per spread currently)

- 📊 2-year duration captures all critical catalysts (R2 launch, ramp, profitability path)

- 🤝 Essentially "copying" sophisticated institutional positioning at same strikes/expiration

- 🛡️ Protection against catastrophic downside if R2 fails or cash crisis emerges

- ⏰ Enough time for thesis to play out - not a short-term speculation

Estimated P&L (current pricing):

- 💰 Pay ~$4.31 net per spread ($431 per 1-contract spread)

- 📈 Max profit: $1.69 per spread if RIVN below $8 at Dec 2027 expiration (+39% ROI)

- 📉 Max loss: $4.31 per spread if RIVN above $10 at expiration (-100%)

- 🎯 Breakeven: Stock must fall to ~$5.69 (68.5% decline from current price!)

Entry timing:

- ⏰ Wait for rally to $19-20 area (near gamma resistance) for better entry

- 🎯 Only enter if you have high conviction R2 will face major problems

- ❌ Skip if stock already below $16 (spread won't provide good risk/reward)

Position sizing: Risk only 1-3% of portfolio maximum (this is tail risk hedge, not core holding)

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Critical warning: Breakeven requires 68.5% decline - this is a LOW probability bet! Only makes sense if you believe catastrophic scenario has >30% chance.

🚀 Aggressive: AVOID - Risk/Reward Terrible (DON'T DO THIS!)

Play: N/A - We do NOT recommend aggressive bullish plays on RIVN at current levels

Why we're passing:

- 💸 Stock at 52-week highs after 66% rally - all good news priced in

- 🔥 Burning $2B+ cash annually with no profitability until 2027 at earliest

- 📊 Valuation stretched at $22B market cap for pre-revenue scaling company

- ⚠️ R2 execution is make-or-break binary event - too much risk

- 🎢 46.5% annual implied volatility shows options are EXPENSIVE

- 💀 Even call options would be paying huge premium for time value over 2 years

Alternative aggressive play (if you insist):

- Wait for pullback to $13-15 range

- Buy small position in stock (not options to avoid time decay)

- Set tight stop loss at $12

- Target $25-30 if R2 wildly succeeds

Risk level: EXTREME | Skill level: Don't attempt this

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🚨 R2 execution is make-or-break: Everything depends on H1 2026 launch going PERFECTLY. Any delays, quality issues, cost overruns, or demand shortfalls would be catastrophic. This is a company with ZERO profitable quarters ever attempting to launch mass-market vehicle while burning $2B+ annually. Historical precedent shows new vehicle launches frequently face problems - battery issues, supplier delays, manufacturing complexity, software bugs. The $45,000 price point leaves minimal margin for error.

-

💸 Cash burn is existential threat: With $7.1B cash and $3.8-4.15B annual burn, Rivian has 18-20 months runway WITHOUT tapping VW/DOE funding. If R2 delays or underperforms, company forced into dilutive capital raise at depressed prices. CFRA's "highly concerning" assessment not hyperbole - this is real risk. Georgia factory construction adds $5B additional capital need through 2028-2029.

-

🥊 Tesla competitive moat remains massive: Model Y sold 1.2M+ units globally in 2024 vs. Rivian's 51K total deliveries. Tesla's 48.5% U.S. EV market share (though declining) dwarfs Rivian's <1%. Tesla can cut Model Y price to $35-40K to defend share, has Supercharger network advantage, and superior cost structure from scale. R2 success requires taking share from established leader willing to compete fiercely.

-

📉 EV demand weakening broadly: 2025 guidance of 41.5-43.5K implies 17% decline vs. 2024. This isn't just Rivian - broader EV market facing headwinds from interest rates, macro uncertainty, charging infrastructure concerns. Loss of $7,500 federal tax credit creates competitive disadvantage vs. eligible alternatives. Luxury EV buyers especially rate-sensitive.

-

🤝 VW partnership not guaranteed success: Reports of tensions over software customization and Audi/Porsche program delays suggest integration harder than expected. VW could reduce scope, delay timelines, or even walk away if Rivian execution falters. The $5.8B total value assumes multi-year collaboration succeeds - not certain.

-

📊 Valuation offers no margin of safety: At $22.14B market cap for company with 2025 revenue ~$6B and massive losses, RIVN trades at 3.7x sales. Comparable profitable automakers trade 0.3-0.8x sales. The premium assumes rapid path to profitability and scale - any deviation crushes multiple. Analysts' average price target of $14.30-14.83 is 20%+ BELOW current price!

-

🏭 Georgia factory is distraction not solution: Construction beginning Q1 2026 but no vehicle production until 2028. This is $5B capital sink over next 3-4 years that generates ZERO revenue/cash flow. Meanwhile company needs to achieve profitability at Normal, IL facility first. Georgia is important long-term but near-term further strains already stretched resources.

-

⚠️ Quality/recall risk: December 2025 recall of 34,824 EDVs demonstrates quality control challenges. For young company trying to scale, product issues can be existential - look at Tesla's Model X falcon wing door problems or Fisker's total collapse. R2 MUST launch with high quality or brand permanently damaged.

-

🌍 Macro recession scenario: If U.S. enters recession in 2026-2027, discretionary purchases like $45K electric SUVs get deferred first. Rivian has zero recession track record. Cash burn accelerates, access to capital markets closes, death spiral begins. The 2-year put timeframe captures this tail risk.

🎯 The Bottom Line

Real talk: Someone just spent $4.8 MILLION on a 2-year bear put spread betting Rivian could fall to single digits by December 2027. This isn't random speculation - this is sophisticated institutional money buying deep protection on a stock trading at 52-week highs after posting its first quarterly profit.

What this trade tells us:

- 🎯 Smart money sees SIGNIFICANT execution risk around R2 launch and profitability path

- 💰 They're willing to pay $4.31 per spread (24% of current stock price!) for protection - that's EXPENSIVE insurance they clearly think is worthwhile

- ⚖️ The 2-year timeframe captures all critical catalysts: R2 launch, ramp, path to profitability, potential cash crisis

- 📊 Striking at $10 and $8 (44.6% and 55.7% below current) shows they see realistic probability of catastrophic downside

- ⏰ Z-scores of 16.64 and 5.07 mean EXTREMELY UNUSUAL activity - this is material institutional positioning

This is NOT "Rivian is doomed" signal - it's "risk is asymmetric and we want protection" signal.

If you own RIVN:

- ✅ Consider trimming 30-50% at $18-19 levels (take profits after 66% rally from April lows)

- 📊 Set MENTAL STOP at $15 gamma support to protect remaining position

- ⏰ Don't hold through R2 launch without hedges if position is large (>5% of portfolio)

- 🎯 If R2 succeeds and stock breaks $20, could re-enter trimmed shares on momentum

- 🛡️ Consider buying small put protection if holding concentrated position (1-2 puts per 100 shares)

If you're watching from sidelines:

- ⏰ DO NOT chase at $18+ near 52-week highs - wait for catalysts to play out

- 🎯 Q4 2025 earnings (late Jan/early Feb 2026) will provide R2 timeline updates - watch closely

- 📈 Best entry likely AFTER R2 launches if successful - look for pullback to $13-16 on post-launch volatility

- 🚀 Long-term (3-5 years), if R2 succeeds, Georgia factory operational, and profitability achieved, stock could be $30-50+

- ⚠️ But near-term (6-18 months), execution risk extreme with binary outcomes

If you're bearish:

- 🎯 Current setup at $18 offers reasonable risk/reward for bearish positioning

- 📊 Gamma resistance at $20 creates natural ceiling - rallies above $20 likely fade

- ⚠️ Consider copying institutional bear put spread structure after any rally to $19-20

- 📉 First support at $18.00 (gamma), major support at $15.00, catastrophic break below $12

- ⏰ Don't short stock outright (borrow costs high, unlimited risk) - use defined-risk puts/spreads

Mark your calendar - Key dates:

- 📅 December-January 2025 - R2 manufacturing validation builds begin

- 📅 Late January/Early February 2026 - Q4 2025 earnings (critical R2 timeline updates!)

- 📅 Q1 2026 - Georgia factory vertical construction begins

- 📅 H1 2026 - R2 customer deliveries begin (MAKE OR BREAK!)

- 📅 Q2-Q3 2026 - R2 production ramp progress becomes visible

- 📅 2027 - EBITDA breakeven target (IF R2 succeeds)

- 📅 2028 - Georgia factory vehicle production begins, R3 launch expected

- 📅 December 17, 2027 - These $4.8M bear put spreads expire

Final verdict: Rivian's long-term story is INCREDIBLY compelling IF - and this is a massive IF - they execute flawlessly on R2 launch, achieve production ramp, and reach profitability by 2027. The VW partnership, Amazon commitment, $6.6B DOE loan, and strong brand positioning are all real assets. BUT, at $18.06 with $22B market cap after 66% rally, burning $2B+ annually, with NO path to profitability until 2027, and ALL dependent on R2 success... the risk/reward is NO LONGER favorable for aggressive new positioning.

The $4.8M institutional bear put spread is a CLEAR signal: execution risk is extreme and smart money wants protection.

Be patient. Let R2 launch. Look for better entry points if successful ($13-16) or avoid completely if it fails. The EV revolution will still be here in 12-18 months, and you'll sleep better paying $14 than $18 for a company that might not exist in 3 years if execution falters.

This is survival of the fittest in the EV wars. Not all will make it. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual Z-scores reflect these specific trades' size relative to recent RIVN history - they do not imply the trades will be profitable or that you should follow them. Bear put spreads have limited profit potential and can lose 100% of premium paid if stock remains above higher strike. R2 launch represents binary execution risk with potential for major price volatility in either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Rivian Automotive: Rivian develops and manufactures electric vehicles along with related software and services through two segments: Automotive (primary revenue from EV production and regulatory credits) and Software & Services (supporting vehicle maintenance, remarketing, and electrical architecture development), with a market cap of $22.14 billion in the Motor Vehicles & Passenger Car Bodies industry.