🐻 RIVN: $2.1M Bearish Bet Before Critical R2 Launch Phase!

📅 December 19, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.1 MILLION on RIVN put options betting the stock falls 11% below $22.44 to $20 by February! This isn't a retail trader's weekend experiment - this is a massive institutional-sized bearish bet (36.64 z-score, meaning this trade size is 555 times the normal average) positioned strategically ahead of Q1 2025 earnings and the critical R2 validation builds. The trader is betting RIVN stumbles into year-end, despite the stock's recent recovery to $22.44. Let's decode what they see that we might be missing... 👀

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Symbol | Side | Type | Expiration | Strike | Premium | Volume | OI | Size |

|---|---|---|---|---|---|---|---|---|---|

| 10:49:51 | RIVN | BUY | PUT | 2026-02-20 | $20 | $2.1M | 11K | 2.3K | 10,500 |

- ⚡ Z-Score: 36.64 (EXTREMELY UNUSUAL - happens only a few times per year)

- 🔥 Volume/OI Ratio: 4.783 (HIGH ACTIVITY - 5x normal open interest)

- 📍 Strategy: Long Put (STANDALONE) - Pure directional bearish bet

- 🎯 Breakeven: $18.03 at expiration ($20 strike - $1.97 premium paid)

- ⏰ Time to Expiration: 63 days (2 months of theta decay)

- 💸 Cost Basis: $1.97 per contract ($197 per share of downside protection)

🤓 What This Actually Means

Real talk: This trader just paid nearly $200 per share to protect against or profit from RIVN dropping below $20 by late February. The February 20 expiration gives them two full months covering:

- ✅ Year-end delivery data (early January release)

- ✅ Q1 2025 earnings (likely late April, but sentiment builds before)

- ✅ R2 validation build updates (expected end of 2025)

- ✅ Potential tariff developments and cash burn updates

- ✅ Any Georgia plant or VW partnership news flow

The $20 strike is 11% below the current $22.44 price - this isn't a crash bet, it's positioning for a modest pullback to $20 or a hedge against deteriorating fundamentals. With reduced 2025 delivery guidance (40,000-46,000 vehicles) representing a potential 17.5% decline from 2024's 51,579 deliveries, this trader might be bracing for disappointment.

🏢 Company Overview

Rivian Automotive (RIVN) is a battery electric vehicle automaker that sells its vehicles in the US and Canada, manufacturing luxury trucks (R1T), full-size SUVs (R1S), and delivery vans. The company also develops autonomous driving software and electronic control units through a Volkswagen joint venture.

- 💼 Market Cap: $24.86 billion

- 🏭 Industry: Motor Vehicles & Passenger Car Bodies

- 🤝 Key Partners: Amazon (20,000 delivery vans deployed), Volkswagen ($5.8B joint venture)

- 🚗 Product Line: R1T pickup, R1S SUV, commercial vans, upcoming R2 midsize SUV (2026)

- 💰 Milestone: Achieved first-ever quarterly gross profit of $170M in Q4 2024

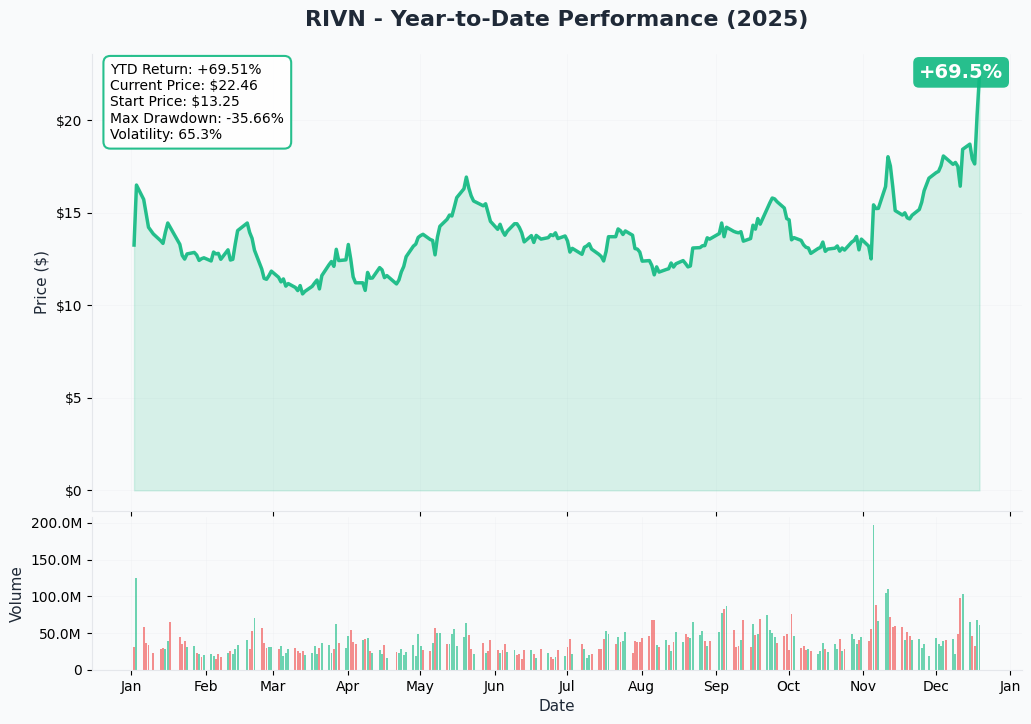

📈 Chart Check-Up

YTD Performance Overview

RIVN has staged a dramatic recovery over the past year, climbing from lows around $10 to the current $22.44 level - a +40% gain over 12 months according to Yahoo Finance data. The stock exploded higher following the Q4 2024 delivery beat on January 3, 2025 (best single-day performance ever at +24.5%), validating the production recovery story after Q3's Enduro motor shortage disaster.

However, recent price action shows consolidation around $22-23, suggesting the market is now digesting whether RIVN can sustain momentum into 2025. The $2.1M put buyer clearly thinks the answer is "no."

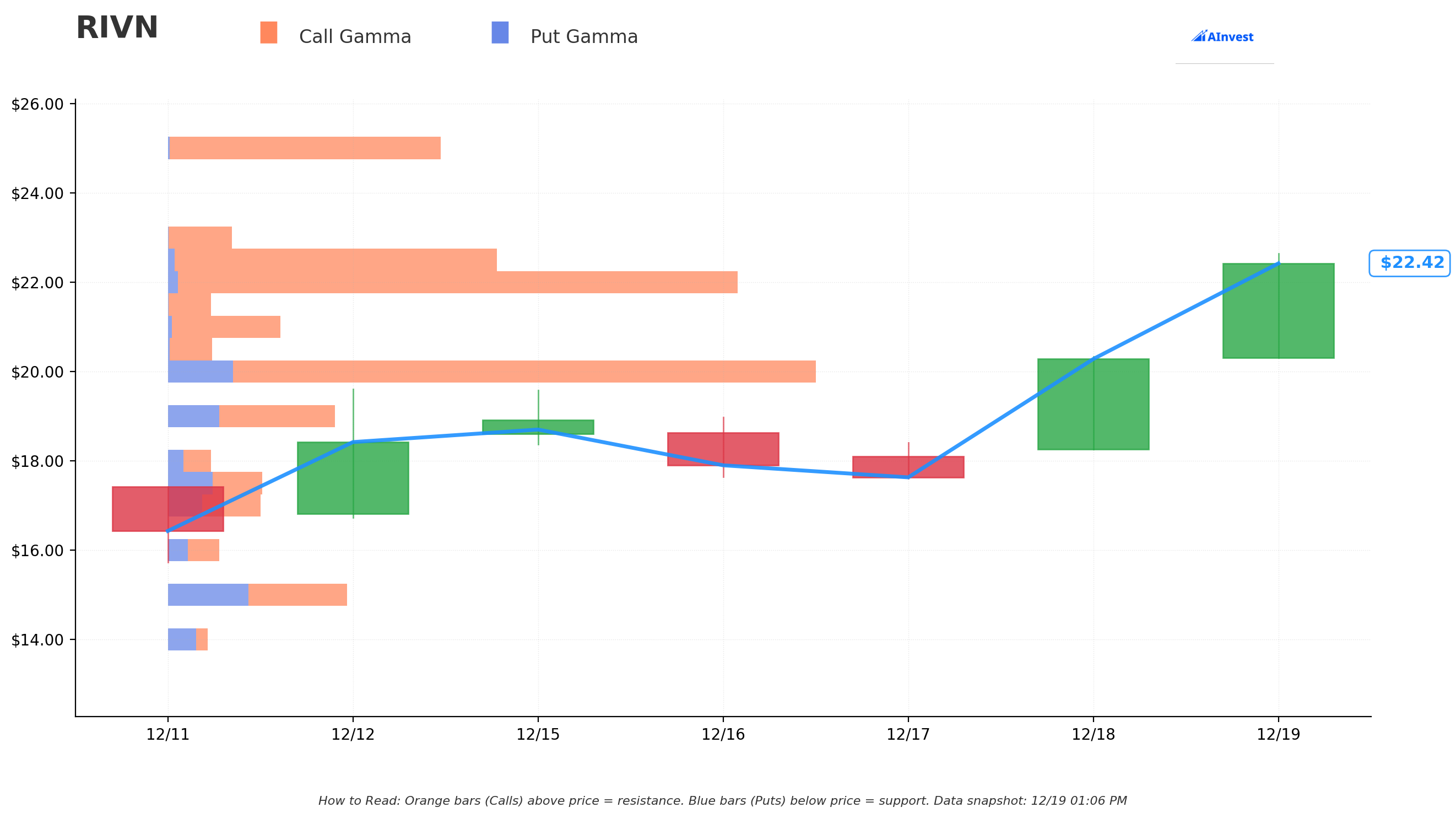

Gamma-Based Support & Resistance Analysis

Critical Gamma Levels:

-

🔵 $22 Support (Very Strong): Net GEX of 27.55M - This is an absolutely massive put gamma wall just below current prices. Market makers need to hedge this level aggressively, creating buying pressure if RIVN approaches $22. This is THE line in the sand for bulls.

-

🟠 $22.50 Resistance (Very Strong): Net GEX of 15.80M - Call gamma ceiling capping upside. Breaking through $22.50 would trigger dealer hedging that accelerates moves higher, but for now this acts as a lid on the stock.

What This Means:

RIVN is trapped in a tight $22-$22.50 range with massive gamma walls on both sides creating a magnetic pin zone. The stock is essentially stuck in dealer hedging quicksand. For the $2.1M put buyer to profit, RIVN needs to break down through the $22 support wall - which would then accelerate selling as dealers unwind hedges. That's a meaningful technical hurdle to overcome.

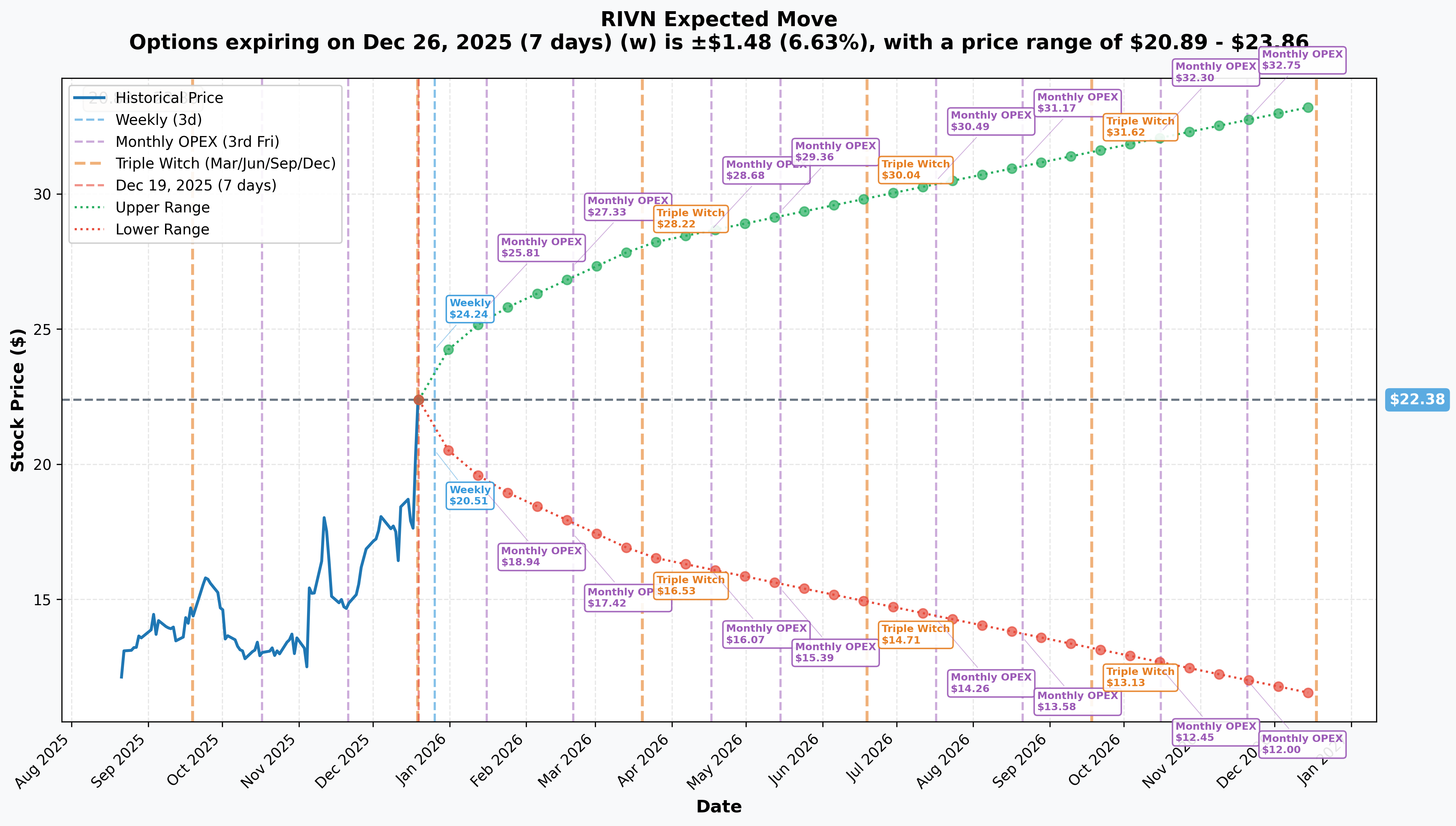

Implied Move Analysis

Market-Implied Price Ranges:

- 📅 Weekly (Dec 26): ±6.63% → $20.89 - $23.86

- 📅 Monthly OPEX (Jan 16): ±13.83% → $19.28 - $25.47

- 📅 February OPEX (Feb 20): ±25.74% → $17.42 - $27.33 (trader's expiration)

- 📅 Quarterly (Mar 20): ±25.74% → $16.62 - $28.13

Critical Insight for the $20 Put:

The February implied move suggests the market expects RIVN to trade between $17.42 and $27.33 by the February 20 expiration. The $20 strike sits right at the lower end of the 1-standard deviation range ($17.42 floor), meaning options pricing gives roughly 16-20% probability of RIVN closing below $20 at expiration.

For context, the trader paid $1.97 in premium, so the true breakeven is $18.03 - which falls below the implied move floor. Translation: This is an out-of-the-money bet that requires RIVN to move more than the market currently expects. Either this trader has conviction in a specific catalyst (earnings miss, R2 delays, cash burn concerns) or this is expensive disaster insurance.

🎪 Catalysts

🔮 Upcoming Events (Next 2 Months)

Q1 2025 Earnings (Late April/Early May 2025)

Expected Date: April 30 - May 7, 2025 based on historical reporting patterns

Why It Matters: This is THE catalyst the put buyer is positioned for. Key metrics to watch:

-

💰 Gross Profit Sustainability: Can RIVN maintain the positive gross margin achieved in Q4 2024 ($170M profit), or was it a one-time blip? Any regression to negative gross profit would be catastrophic.

-

🏭 Production Volume Recovery: Q4 2024 produced only 12,727 vehicles. Expectations are for sequential improvement, but reduced 2025 guidance (40,000-46,000 deliveries) already signals weakness.

-

💸 Cost Per Vehicle Progress: Management claims they removed $31,000 in automotive COGS per vehicle in Q4 2024. Any stalling in this cost reduction roadmap undermines the profitability thesis.

-

🎯 2025 Guidance Updates: Wall Street is already skeptical about the 40,000-46,000 delivery target. Further downward revisions would trigger selling.

Bear Case Risk: Tariff impacts could add $2,000 loss per vehicle sold, potentially wiping out Q4's gross profit gains. If RIVN reports negative gross margins again, this stock could crater toward $18-20 quickly.

R2 Validation Builds (End of 2025)

Timeline: Validation builds expected by end of 2025, pre-production starts early 2026, customer deliveries in H1 2026.

Why It Matters: The R2 is RIVN's path to survival - a $45,000 mass-market SUV targeting 155,000 annual unit capacity (3x current R1 production). Any delays in the validation build timeline would:

- ⏰ Push back 2026 profitability targets

- 💸 Extend the $2.0-2.25B annual cash burn runway

- 😰 Trigger concerns about RIVN's ability to scale to mass-market volumes

Bear Scenario: If RIVN announces validation build delays or technical issues with the R2 platform in late December or early January updates, the stock could gap down toward $20. The put buyer is positioned perfectly for this.

Year-End 2025 Delivery Data (Early January 2026)

Based on past patterns, RIVN should report Q4 2025 production and delivery figures in early January 2026.

Bull vs Bear:

- 🐂 Bull Case: Deliveries exceed the reduced 40,000-46,000 guidance, showing demand resilience

- 🐻 Bear Case: Deliveries fall short even of reduced guidance, confirming weakening demand and execution issues

Given the current guidance already represents a 17.5% decline from 2024's 51,579 deliveries, even meeting the lowered bar might not be enough to satisfy bulls.

✅ Recent Events (Already Happened)

Q4 2024 Earnings - HISTORIC MILESTONE (February 20, 2025)

RIVN achieved its first-ever quarterly gross profit of $170 million in Q4 2024, beating consensus estimates with:

- 📊 Revenue: $1.73B (beat $1.4B consensus by +23.6%)

- 💰 EPS: Loss of $0.46 (beat consensus loss of $0.68 by 32.4%)

- 🎯 Net Loss: $743M vs. $1.52B YoY (-51.1% improvement)

- 🏭 Production: 12,727 vehicles

- 🚗 Deliveries: 14,183 (beat expectations of 13,472)

Stock Reaction: +24.5% on January 3, 2025 - best single-day performance ever since IPO.

Volkswagen Joint Venture - $5.8B Partnership (November 12, 2024)

Rivian and VW officially launched the joint venture "Rivian and VW Group Technologies, LLC" with a total deal size of up to $5.8 billion by 2027. VW is funding 75% of shared platform costs, providing critical capital relief.

Strategic Importance:

- 💻 Developing Software-Defined Vehicle (SDV) architecture for both companies

- 🚙 First VW vehicles using Rivian tech expected as early as 2027

- 👥 Development team has grown to over 1,500 employees internationally

- 🎯 Potential to become "the Android of cars" licensing platform to other OEMs

DOE Loan - $6.6B Georgia Plant Funding (November 25, 2024)

The U.S. Department of Energy announced conditional commitment for a $6.6 billion loan with final closing in January 2025 - the second-largest DOE loan ever.

Georgia Facility Details:

- 🏗️ Capacity: Up to 400,000 vehicles annually

- 📐 Size: 9 million square feet on 1,744-acre site

- 🚗 Models: R2 and R3 midsize platform vehicles

- ⏰ Timeline: Groundbreaking Q2 2026, production starting 2028

- 👷 Jobs: 7,500 operations jobs through 2030

🎲 Price Targets & Probabilities

Based on gamma levels, implied move ranges, and fundamental catalysts, here's the realistic scenario analysis through February 20 expiration:

🐻 Bear Case: $18-20 (Put Buyer's Target)

Probability: 25-30%

How We Get There:

- ❌ Q1 2025 earnings show gross margin turning negative again due to tariff impacts

- ❌ Year-end 2025 deliveries miss even reduced guidance of 40,000-46,000

- ❌ R2 validation build delays announced or technical issues surface

- ❌ Cash burn accelerates beyond $2.0-2.25B forecast, raising dilution concerns

- ❌ Short interest (currently 14.28% but peaked at 20%+) rebuilds as momentum fades

Key Price Levels:

- Break below $22 gamma support triggers dealer unwinding → accelerates to $20

- $20 psychological level is the put strike - major battle zone

- $19.28 is the January OPEX implied move floor

- $18.03 is the put buyer's true breakeven

Catalyst Timeline: Year-end delivery data (early Jan) disappoints → stock gaps to $21 → further weakness into late January → earnings fears build → test $20 by mid-February.

⚖️ Base Case: $21-24 (Range-Bound Chop)

Probability: 50-55%

How We Get There:

- ✅ Mixed results: Deliveries in-line, but gross margins pressured by tariffs

- ✅ R2 validation builds proceed on schedule (no news is good news)

- ✅ Market digests reduced 2025 guidance but gives credit for VW/DOE funding cushion

- ✅ Gamma walls at $22-$22.50 keep stock pinned in tight range

- ✅ Institutional holders (Amazon 13.3%, VW 12.3%) provide price stability

Key Price Levels:

- $22 gamma support holds as floor

- $22.50 gamma resistance caps upside

- Stock oscillates in 2% range through expiration

- Theta decay accelerates in final 30 days, crushing put value

Catalyst Timeline: Moderate news flow, no major surprises, volatility collapses as we approach February OPEX.

🐂 Bull Case: $25-28 (Breakout Higher)

Probability: 20-25%

How We Get There:

- ✅ Year-end deliveries exceed reduced guidance, showing demand resilience

- ✅ R2 validation builds complete successfully with positive updates

- ✅ Analyst upgrades follow (like Baird's December upgrade to $25 target)

- ✅ VW partnership announces accelerated timeline or expanded scope

- ✅ Trump administration clarifies EV policy reduces uncertainty

Key Price Levels:

- Break above $22.50 gamma resistance triggers dealer hedging → accelerates to $24

- $25.47 is the January OPEX implied move ceiling

- $27.33 is the February OPEX implied move ceiling

- $28 represents +25% move from current levels

Catalyst Timeline: Strong delivery beat in early January → positive R2 updates late January → momentum builds → test $25 by mid-February.

Impact on Put Buyer: Put expires worthless, $2.1M loss. But if this was a hedge, the underlying long position gains offset the premium loss.

💡 Trading Ideas

🛡️ Conservative: Wait for Confirmation

The Play: Don't fight the $2.1M whale just yet. Wait for RIVN to break below the $22 gamma support wall before entering bearish positions. If it breaks, the momentum accelerates quickly.

Entry Point: $21.80 (confirmed break of $22 support on volume)

Position:

- Buy RIVN March 2026 $20 Puts (~$2.50 premium, further out in time)

- Alternative: Sell RIVN shares short at $21.80 with $23.50 stop loss

Risk Management:

- ✅ Max loss: $250 per put contract or 8% on short position

- ✅ Stop loss: Close if RIVN reclaims $22.50 (invalidates breakdown)

- ✅ Take profit: $20 initial target, $19 stretch target

Why This Works: You're avoiding the mistake of catching a falling knife. Let the $22 support break first, then ride the dealer hedging cascade lower. The March expiration gives you an extra month vs. the whale's February expiration, reducing theta decay risk.

⚖️ Balanced: Put Credit Spread (Income Strategy)

The Play: If you think RIVN stays above $20 through February (base case scenario), sell puts and collect premium from the elevated IV caused by the $2.1M whale trade.

Position Structure:

- Sell RIVN Feb 20, 2026 $20 Put (collect ~$1.97)

- Buy RIVN Feb 20, 2026 $18 Put (pay ~$1.10)

- Net Credit: ~$0.87 per spread ($87 per contract)

Max Profit: $87 if RIVN closes above $20 at expiration Max Loss: $113 if RIVN closes below $18 ($2 spread width - $0.87 credit)

Probability of Profit: ~70-75% (RIVN stays above $20)

Risk Management:

- ✅ Close spread if RIVN breaks $21 (take small loss before it becomes large loss)

- ✅ Take profit at 50% credit captured ($0.44) if reached in first 30 days

- ✅ Maximum position size: 5-10 spreads ($435-870 credit, $565-1,130 risk)

Why This Works: You're betting against the whale's bearish view while defining your risk. The gamma wall at $22 supports your thesis that RIVN won't reach $20. Even in mixed scenarios, you profit as long as RIVN doesn't collapse.

🚀 Aggressive: Follow the Whale with Cheaper Strikes

The Play: If you have conviction the whale is right about RIVN declining, but want cheaper entry and more leverage, buy further out-of-the-money puts.

Position:

- Buy RIVN Feb 20, 2026 $18 Puts (~$1.10 premium)

- Alternative: Buy 2x RIVN Feb 20, 2026 $17 Puts (~$0.60-0.70 each)

Breakeven: $16.90 for $18 puts, $16.30-16.40 for $17 puts

Risk/Reward:

- 💸 Max loss: Premium paid ($110 per contract for $18 puts)

- 💰 Potential profit: 200-500%+ if RIVN collapses to $15-16 on major negative news

- ⚡ Delta: Lower delta than $20 strike, but higher gamma for explosive moves

Catalyst Requirements: This only works if one of these happens:

- ❌ Catastrophic earnings miss with gross margins turning deeply negative

- ❌ R2 delays of 6+ months announced

- ❌ Emergency capital raise at dilutive terms

- ❌ Major customer loss (Amazon reduces order size)

Why This Is Aggressive: You need a disaster scenario to profit - RIVN must drop 20-25% from current levels. The whale's $20 strike is more conservative (only needs 11% decline). But if you're right, the payoff is exponentially higher due to the cheaper entry cost and higher leverage.

Risk Management:

- ✅ Position size: No more than 1-2% of portfolio (this is lottery ticket territory)

- ✅ Exit rule: Cut loss if RIVN rallies above $24 (invalidates bearish thesis)

- ✅ Profit taking: Scale out at 100%, 200%, 300% gains if move develops

⚠️ Risk Factors

What Could Go Wrong for Bears (Put Buyer Loses)

1. R2 Execution Exceeds Expectations

If RIVN announces ahead-of-schedule R2 validation builds or surprisingly strong pre-order numbers for the $45,000 mass-market SUV, the stock could rally hard. The Baird upgrade to $25 target specifically cited R2 as a "demand driver" - if that thesis proves correct, bulls control the narrative through February.

Probability: 20-25% Impact: RIVN rallies to $25-27, put expires worthless

2. VW Partnership Expansion or Acceleration

The joint venture has grown to 1,500+ employees and could announce:

- 🚗 Additional OEM customers licensing Rivian's SDV platform

- 💰 Accelerated VW funding tranches (front-loading the $3.5B remaining)

- 🎯 2027 VW vehicle launch timeline moved earlier

Any of these developments validate RIVN's technology platform and reduce cash burn concerns.

Probability: 15-20% Impact: RIVN rallies to $24-26, put value collapses

3. Gamma Pin at $22-$22.50

The massive gamma walls create a "magnetic pin effect" where dealers' hedging activity keeps RIVN trapped in a tight range. If volatility collapses and the stock just oscillates between $22-23 for two months, theta decay annihilates put value even though the directional thesis (modest decline) might eventually prove correct.

Probability: 50-55% (base case) Impact: Put loses 60-80% of value by expiration even if RIVN only at $21-22

4. Short Squeeze Risk

With short interest having peaked above 20% of float in December 2024 (now 14.28%), any unexpected positive catalyst could trigger covering. The combination of Amazon (13.3%) and VW (12.3%) ownership limits available float, amplifying squeeze potential.

Probability: 10-15% Impact: Violent rally to $26-28 crushes puts

What Could Go Wrong for Bulls (Put Buyer Wins)

1. Tariff Impacts Destroy Q1 Gross Margins

CFO Claire McDonough already warned tariffs could add $2,000 additional loss per vehicle sold. If Q1 2025 earnings show gross profit swinging back to deeply negative territory, it invalidates the entire "path to profitability" thesis that drove the stock's 2024-2025 recovery.

Updated U.S. tariffs of 25% on imported auto parts could increase costs by up to $10,000 per vehicle according to some estimates.

Probability: 30-35% Impact: RIVN gaps down to $19-20 on earnings

2. Cash Burn Accelerates Beyond Forecast

Current forecast: Adjusted EBITDA loss of $2.0-2.25 billion in 2025, up from earlier $1.7-1.9B estimate. If actual burn exceeds $2.5B, questions arise about:

- 💸 Whether $7.7B liquidity is sufficient through R2 ramp

- ⏰ Dilutive capital raise timing (kills stock)

- 🏗️ Georgia plant construction funding adequacy

CFRA analysts already flagged "highly concerning cash burn" as a key risk.

Probability: 25-30% Impact: RIVN declines to $18-20 on dilution fears

3. 2025 Delivery Guidance Cut Again

Current guidance: 41,500-43,500 vehicles (Q3 2025 narrowed range). This already represents a 17.5% decline from 2024's 51,579 deliveries. If RIVN cuts guidance further to below 40,000, it confirms:

- 📉 Demand weakening (not just supply chain)

- 💰 Revenue shortfall threatens profitability timeline

- 🎯 R2 launch becomes even more critical (binary event)

Probability: 20-25% Impact: RIVN drops to $20-21 on volume concerns

4. R2 Delays or Technical Issues

Any announcement that validation builds scheduled for end of 2025 are delayed or encountering problems would be catastrophic. The R2 is RIVN's only path to:

- Scaling to 155,000 annual units (3x current)

- Achieving positive unit economics by end of 2026

- Justifying the $24.86B market cap

Probability: 15-20% Impact: RIVN collapses to $16-18 on broken story

🎯 The Bottom Line

Real talk: The $2.1M put buyer is making a calculated bet that RIVN's impressive Q4 2024 gross profit milestone ($170M) was the high-water mark rather than the beginning of sustained profitability. They're positioned for a 11% decline to $20 over the next two months, banking on one or more of these scenarios:

- 💸 Tariff impacts destroy Q1 gross margins, reversing the profitability narrative

- 🚗 Year-end delivery data disappoints even reduced 40,000-46,000 guidance

- ⏰ R2 validation build delays or technical issues surface in late December/early January

- 💰 Cash burn acceleration beyond $2.0-2.25B raises dilution fears

- 📉 Momentum fades as short interest rebuilds and gamma pin creates downside bias

The case FOR the puts:

- Tariff risk is real - $2,000 loss per vehicle wipes out fragile gross margins

- 2025 deliveries down 17.5% YoY raises demand questions in slowing EV market

- R2 execution is binary - any delay destroys thesis, and this is Rivian's first mass-market vehicle (high risk)

- Stock trading at $22.44 vs $15.23 average analyst price target suggests expectations ahead of fundamentals

- Reduced 2025 guidance already admits challenges, more cuts likely

The case AGAINST the puts:

- $22 gamma support wall is massive (27.55M GEX) - breaking it requires sustained selling pressure

- VW partnership ($5.8B) and DOE loan ($6.6B) provide ample liquidity cushion through R2 ramp

- Q4 gross profit achievement shows operational progress is real, not just accounting magic

- Amazon (13.3%) and VW (12.3%) ownership creates "strategic holder" base resistant to selling

- R2 pre-orders and validation builds proceeding on schedule (no negative news yet)

Our Take:

This is a smart hedging position rather than a reckless directional gamble. If you own RIVN shares or have bullish exposure, buying $20 puts at $1.97 (8.8% of stock price) is reasonable disaster insurance covering the next critical 60 days of catalysts. The February 20 expiration captures year-end delivery data, earnings sentiment building, and any R2 development updates.

For traders without existing exposure, we lean toward the base case (range-bound $21-24) where theta decay crushes both puts and calls. The gamma walls at $22/$22.50 create a powerful pin effect that's hard to overcome without major news catalysts.

Action Plan:

-

📊 If you own RIVN stock (bullish): Consider buying $20 or $21 puts as portfolio insurance (2-5% position size). The whale's trade validates this isn't paranoid - there are real risks ahead.

-

⚖️ If you're neutral/watching: Sell put credit spreads ($20/$18) to collect premium from elevated IV while defining risk. Profit if RIVN stays above $20.

-

🐻 If you're bearish: Wait for confirmation - don't front-run the $22 support break. If RIVN closes below $22 on volume, then load $20-21 puts for the move to $18-19.

Mark your calendar:

- 🗓️ Early January 2026: Year-end 2025 delivery data release

- 🗓️ Late December 2025: R2 validation build status updates

- 🗓️ Late January 2026: Earnings date announcement and sentiment building

- 🗓️ February 20, 2026: Option expiration and OPEX gamma unwind

The next 60 days will define whether RIVN's profitability story is sustainable or a fleeting mirage. The $2.1M whale is betting on mirage - but they're hedging smartly, not speculating recklessly. 💭

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. The analysis above is for educational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Always conduct your own research and consider consulting with a licensed financial advisor before making investment decisions. Option values can decline to zero, resulting in total loss of premium paid.

📊 Data Sources:

- Options Flow: Ainvest

- Company Data: Polygon.io

- Gamma Analysis: Proprietary GEX calculations

- Implied Move: Options-derived volatility models

- Catalyst Research: Company filings, news sources, analyst reports

🔗 Further Reading: