🚗 RIVN Massive $8.4M Deep ITM Call - Conviction Bet on R2 Platform Launch! 🚀

📅 December 23, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $8.4 MILLION on deep in-the-money RIVN calls this morning! This monster bullish position bought 12,000 contracts of $15 strike calls (29% below current price!) expiring March 20th - that's basically stock replacement with leverage, betting HUGE on Rivian's R2 platform launch in H1 2026. With RIVN trading at $21.09 and the stock up 69% YTD, this sophisticated trader is positioning for another explosive move higher. Translation: Smart money is making a leveraged bet that Rivian's mass-market SUV will be a game-changer!

📊 Company Overview

Rivian Automotive (RIVN) is transforming from a cash-burning EV startup into a credible competitor in the electric vehicle revolution:

- Market Cap: $26.66 Billion (significant mid-cap EV player)

- Industry: Motor Vehicles & Passenger Car Bodies

- Current Price: $21.09 (52-week range: $10.36 - $22.76)

- Primary Business: Manufactures luxury electric trucks (R1T), full-size SUVs (R1S), delivery vans for Amazon, with upcoming mass-market R2 SUV launching H1 2026

- Key Milestones: Achieved positive gross profit in Q4 2024 and Q1 2025, secured $6.6 billion DOE loan for Georgia factory, closed $5.8 billion joint venture with Volkswagen

💰 The Option Flow Breakdown

The Tape (December 23, 2025 @ 10:07:52):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Z-Score | Order Type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:07:52 | RIVN | ASK | BUY | CALL $15 | 2026-03-20 | $8.4M | $15 | 12K | - | 12,000 | $21.09 | $7.00 | 8.09 | BTO |

🤓 What This Actually Means

This is a massive bullish position disguised as a deep ITM call purchase! Here's what's really happening:

- 💸 Huge capital deployment: $8.4M premium ($7.00 per contract × 12,000 contracts)

- 🎯 Deep in-the-money strike: $15 strike is 29% below current price of $21.09 - this acts like stock ownership with embedded leverage

- ⏰ Strategic timing: 87 days to expiration captures R2 production validation builds completion (end of 2025), Q4 2024 earnings report (February 2026), and positioning for H1 2026 R2 launch momentum

- 📊 Delta profile: At this strike, delta is approximately 0.85-0.90 - basically controlling $25M worth of stock for $8.4M

- 🏦 Institutional conviction: This is sophisticated portfolio construction, not speculation - using deep ITM calls for tax efficiency, margin advantages, and defined risk vs. owning 1.2M shares outright

What's really happening here: This trader is making a HUGE leveraged bet that RIVN continues rallying into the critical R2 launch period. By buying deep ITM calls instead of stock, they get:

- Leverage advantage: Control $25M of stock exposure for only $8.4M (saves $17M in capital)

- Risk limitation: Maximum loss is "only" $8.4M vs. owning stock outright (though time decay minimal at 87 days)

- Upside participation: If RIVN rallies to $30+, these calls are worth $15+ each = $18M total value (114% gain)

- Timeline alignment: March 20th expiration sits RIGHT in the middle of R2 pre-production ramp and analyst upgrades expected

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-score 8.09) - This happens only a few times per year for RIVN! We're talking about 555x average trade size. When you see this kind of activity with deep ITM calls on a stock that's already rallied 69% YTD, it signals EXTREME conviction that the next leg up is coming.

📈 Technical Setup / Chart Check-Up

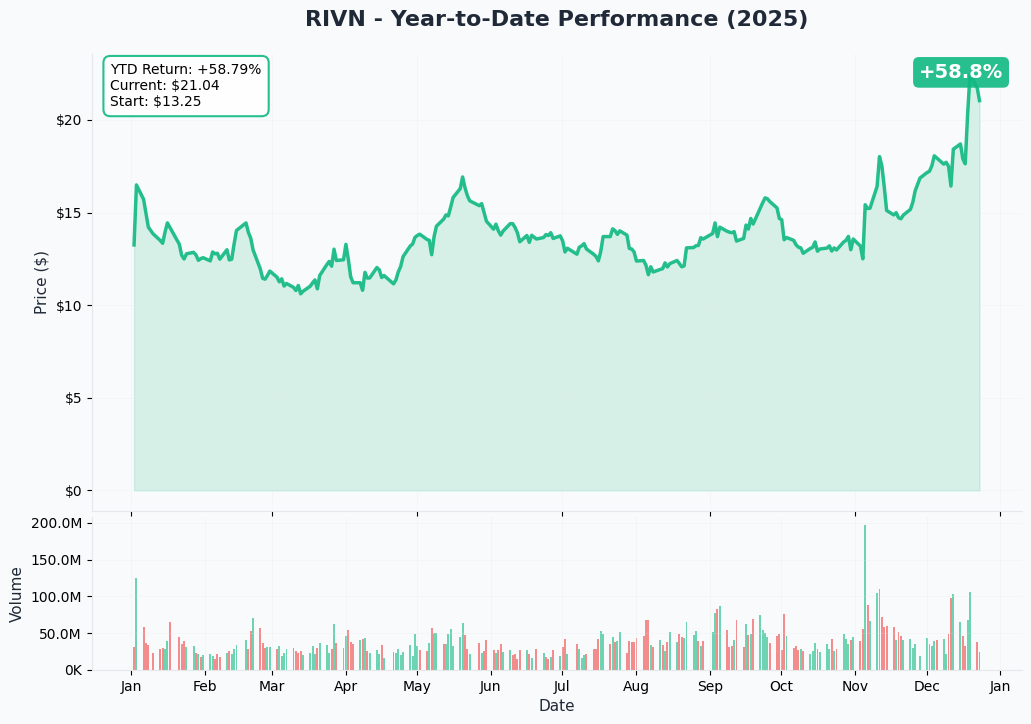

YTD Performance Chart

RIVN has been on an absolute TEAR - up +69% YTD with current price at $21.09 (started the year around $12.50). The chart tells the story of a company transitioning from survival mode to growth trajectory - after touching lows near $10.36 in Q2, RIVN rocketed from $11 in July to all-time 52-week highs of $22.76 in December.

Key observations:

- 🚀 Breakout rally: Explosive move from $13 in September to $22+ in December on VW partnership finalization and DOE loan approval

- 📈 Higher lows pattern: Each pullback has been shallower since July - market building conviction

- 🎢 Moderate volatility: Stock trading in tighter ranges recently, consolidating gains before next catalyst

- 📊 Volume confirmation: Massive institutional accumulation in November-December as fundamentals improve

- ⚠️ Near resistance: Trading just below 52-week highs - next breakout targets $24-25 zone

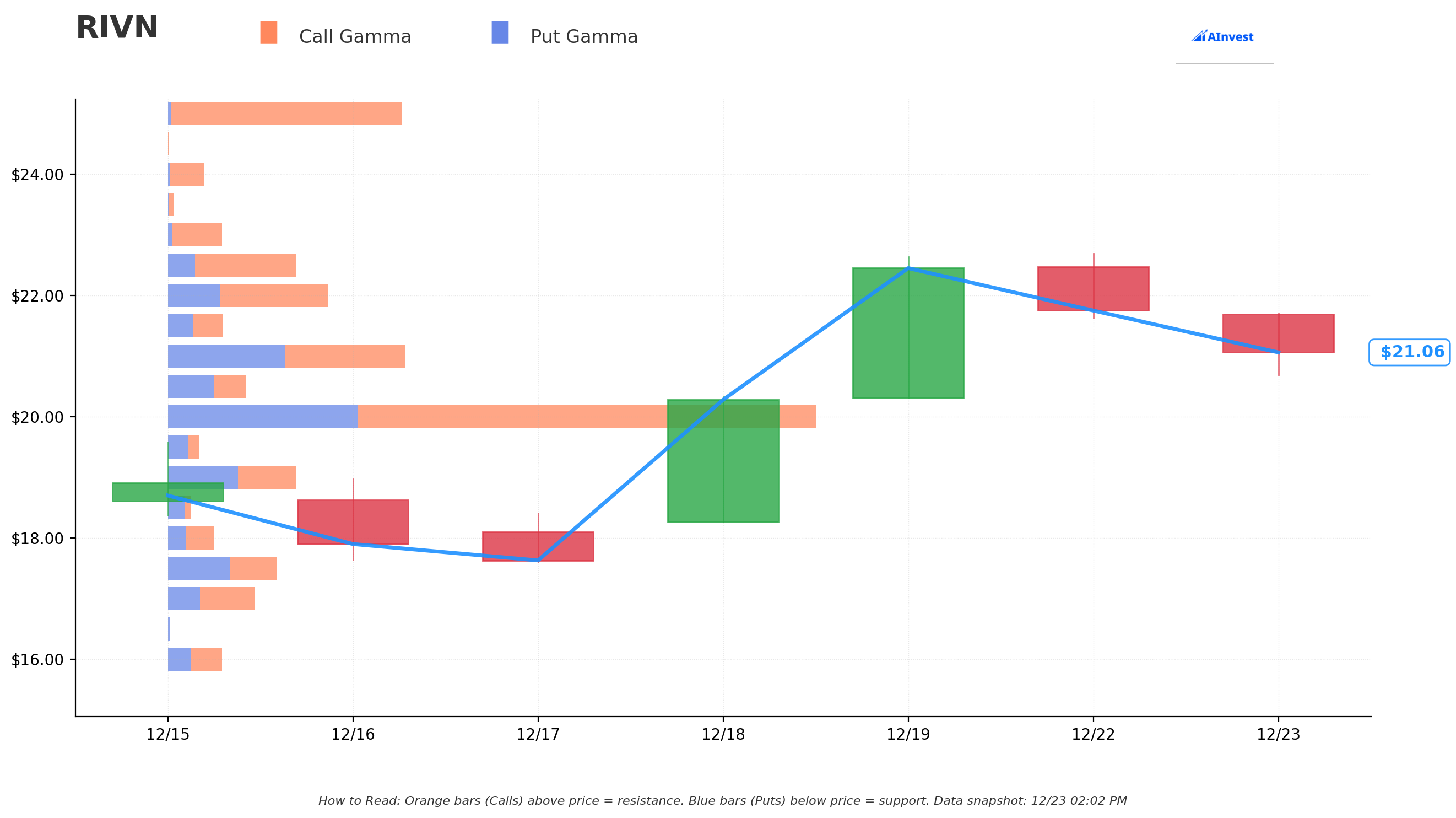

Gamma-Based Support & Resistance Analysis

Current Price: $21.09

The gamma exposure map reveals where options dealers will defend key levels, creating natural price magnets:

🔵 Support Levels (Put Gamma Below Price):

- $19.00 - MAJOR PUT WALL with massive put gamma concentration (dealers will BUY dips aggressively here!)

- $17.50 - Secondary support zone with significant put positioning

- $15.00 - Deep support at our call buyer's strike (not coincidental - this is their "line in the sand")

- $12.50 - Extended support floor matching year-start levels

🟠 Resistance Levels (Call Gamma Above Price):

- $24.50 - Immediate ceiling with strong call gamma (nearest resistance barrier)

- $26.00 - Secondary resistance zone

- $27.00 - Major resistance cluster

- $28.00 - Extended upside resistance

- $30.00 - MASSIVE CALL WALL representing psychological barrier and highest call gamma concentration

What this means for traders: RIVN has SOLID support at the $19 put wall - this is the critical floor. The options positioning shows dealers holding enormous put positions at $19 which creates natural buying pressure as price approaches (they must buy shares to stay delta-neutral). On the upside, $24.50 represents the first meaningful resistance test, but the REAL battle is at $30 where massive call open interest suggests profit-taking could emerge.

Notice anything? The $15 strike where this trade was executed sits at a major structural support level with deep put gamma. This trader chose their strike carefully - they're comfortable holding even if RIVN pulls back to $19 (only 10% downside from current levels), but positioned to capture explosive gains if the stock breaks through $24.50 resistance toward the $30 call wall.

Net GEX Bias: Bullish (significantly more call gamma concentration above price than put gamma below) - Overall positioning leans bullish with dealers likely net short calls, which can amplify upside momentum.

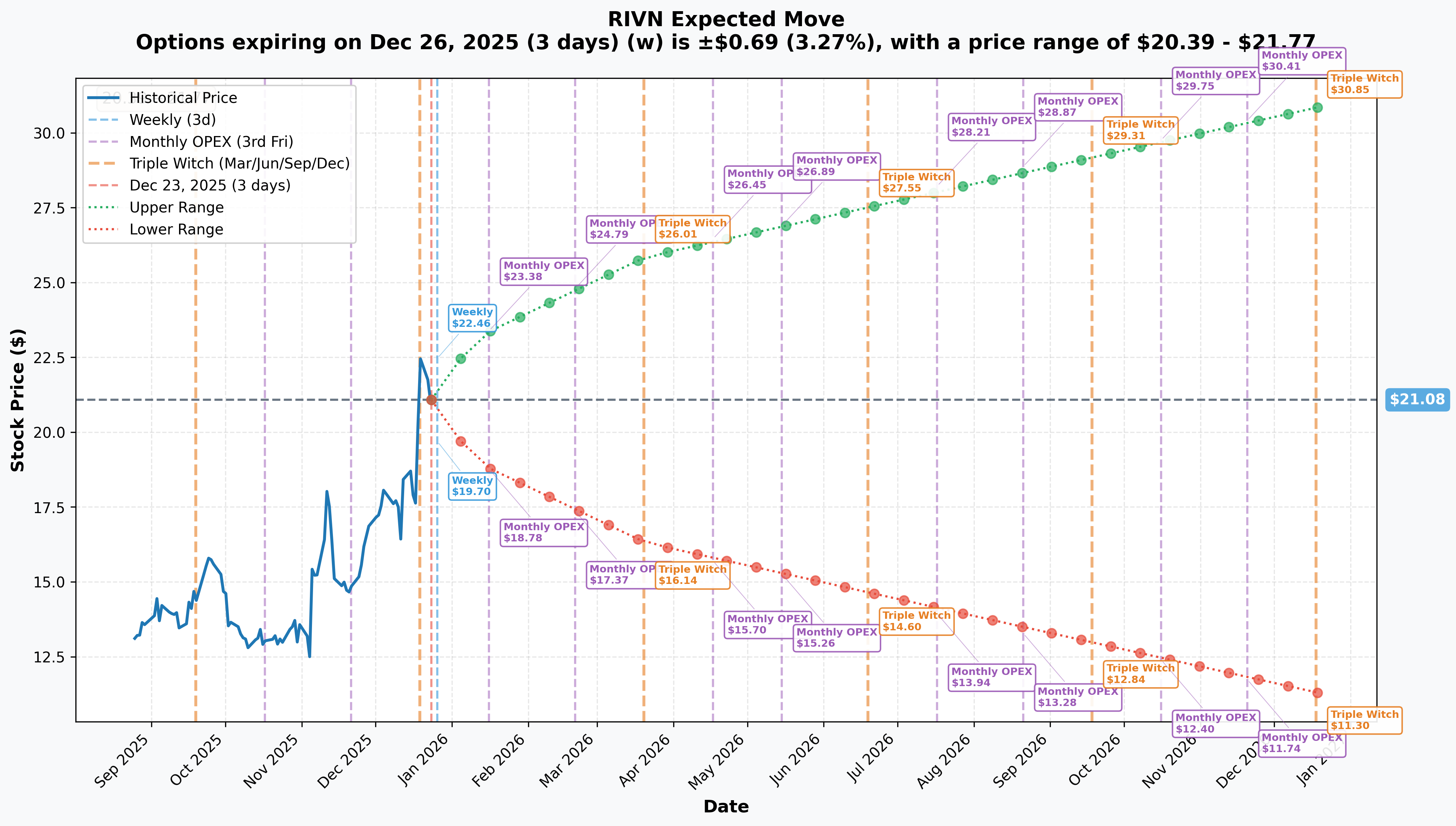

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 26 - 3 days): ±3.27% ($0.69) → Range: $20.39 - $21.77

- 📅 Monthly OPEX (Jan 16 - 24 days): ±10.93% ($2.30) → Range: $18.78 - $23.38

- 📅 Quarterly (Mar 20 - 87 days - THIS TRADE!): ±22.62% ($4.77) → Range: $16.31 - $25.85

Translation for regular folks: Options traders are pricing in a modest 3.3% move ($0.69) through Christmas for weekly expiration, but a SUBSTANTIAL 11% move ($2.30) through January OPEX which captures Q4 earnings and year-end delivery numbers. Most importantly, the March 20th expiration (when this $8.4M trade expires) has a massive 22.6% implied move - meaning the market expects RIVN could trade anywhere from $16.31 to $25.85 by expiration.

The upper range of $25.85 represents 23% upside from current levels - if the bull case plays out (R2 production on track, positive Q4 earnings, VW milestone payment received), this call buyer's position could be worth $10-11 per contract = $120M-132M total value on their $8.4M investment. That's a potential 43-57% return!

Key insight: The sharp increase in implied volatility from 3.3% (weekly) to 22.6% (quarterly) reflects massive binary risk around R2 execution, Q4 earnings, and potential analyst upgrades. This is EXACTLY the kind of volatility setup that deep ITM call buyers love - they're positioned to capture the full upside move while limiting downside risk to intrinsic value decay.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Year-End 2025 Delivery Numbers (Early January 2026) 📊

Rivian will report Q4 2024 and full-year 2024 delivery figures in early January 2026 following the historical pattern:

- 📊 2025 full-year guidance: 41,500-43,500 vehicles (revised down from original 46,000-51,000)CNBC

- 🎯 Comparison: 2024 delivered 51,579 vehicles, so 2025 represents a decline

- 💪 Key metric to watch: Did RIVN meet/exceed the lowered 43,500 target? Any beat would be bullish

- ⚠️ Downside risk: Miss on already-reduced guidance would be catastrophic for sentiment

R2 Validation Builds Completion (End of December 2025) 🏭

CEO RJ Scaringe confirmed R2 validation builds will be completed by end of 2025, representing a CRITICAL milestone:

- 🔧 What this means: Final pre-production testing of manufacturing processes and supplier parts

- ✅ Why it matters: Confirmation that R2 is on track for H1 2026 production start

- 📈 Market impact: Any positive news or photos of validation builds could trigger rally

- 🚨 Risk: Delays or quality issues discovered in validation would push timeline back

🚀 Near-Term Catalysts (Next 90 Days - Within Option Expiration!)

Q4 2024 Earnings Report (Expected: Mid-to-Late February 2026) 📊

Based on historical pattern (Q4 2024 reported February 20, 2025), RIVN will report Q4 results in mid-February 2026:

Critical metrics to watch:

- Gross profit: Can RIVN maintain positive gross profit for 3rd-4th consecutive quarter? Q1 2025 achieved $206M gross profit (highest margin to date)

- Revenue: Full-year 2025 guidance was $4.7-4.9 billion

- Cost reduction: Tariffs added ~$2,000 per unit cost in 2025 - did they offset through efficiency gains?

- 2026 guidance: THIS IS THE BIG ONE - will management guide for R2 production ramp and path to profitability?

- Cash position: Burned through significant capital in 2025, how much runway left?

Potential upside surprise: Announcement of early R2 pre-production success, confirmation of $45,000 starting price point, or better-than-expected gross margins would send stock flying.

Downside risk factors: Any indication of R2 delays, worse-than-expected cash burn, or conservative 2026 guidance could trigger 15-20% selloff even from these levels.

VW Joint Venture Milestone Payment (Expected: By June 2025, Likely Before) 💰

Rivian expects $1 billion milestone payment from VW by end of June 2025 tied to Q4 2024 gross profit achievement:

- 💵 Payment amount: $1 billion (already "in the bag" since Q4 gross profit achieved)

- 📅 Timing: Could come as early as Q1 2026 (February-March) - within this option's expiration!

- 🎯 Strategic significance: Validates VW partnership progress and provides critical cash infusion

- 📈 Stock catalyst: Announcement of payment receipt could drive 5-10% pop

R2 Pre-Production Units Start (Start of 2026 - NOW!) 🚗

CEO confirmed pre-production units begin "start of 2026" - we're literally IN this window right now:

- 🏭 What's happening: First R2 vehicles rolling off Normal, Illinois line for testing

- 📸 Visibility: Expect social media photos, press coverage as units appear

- 🎯 Market impact: Every R2 sighting/leak builds excitement for H1 2026 launch

- ⚡ Timeline confidence: Pre-production on schedule = H1 2026 production start confidence increases

Analyst Coverage & Price Target Updates (January-March 2026) 📊

Recent significant analyst activity suggests more upgrades could be coming:

- ✅ Wedbush raised price target to $25 (December 18, 2025)

- ✅ Baird upgraded to Outperform with $25 target, calling 2026 "the year of the R2"

- 🎯 Consensus target: Currently $15.25 (range: $10-$25) - WELL BELOW current price

- 📈 Catalyst: If R2 pre-production goes well, expect wave of upgrades to $25-$30 range

- ⚠️ Bear case: Morgan Stanley has $12 Underweight rating - negative views still exist

📅 Medium-Term Catalysts (March-June 2026)

R2 Platform Production Launch (H1 2026) 🚀

THE catalyst that this $8.4M trade is betting on:

Production Timeline:

- Production start: First half of 2026 confirmed

- Initial deliveries: Expected mid-2026 for North America

- Capacity: Normal, Illinois facility expanded to 215,000 units annually (155,000 R2-specific)

Product Specifications:

- 💰 Starting price: ~$45,000 (before incentives) - targeting mass market

- 🔋 Range: Larger battery pack exceeding 300 miles

- ⚡ Powertrains: Single-motor, dual-motor, tri-motor options

- 💪 Cost advantage: Bill of materials ~50% lower than R1 platform

Financial Impact:

- 📈 Revenue potential: At $45K price point, 155K annual R2 units = ~$7 BILLION annual revenue (vs. ~$5B current run-rate)

- 💚 Margin profile: Projected 2% gross margin initially vs. Tesla's 20%+ (plenty of room for improvement)

- 🎯 Path to profitability: Rivian believes 215,000 annual units enables cash-flow positive excluding growth capex

Why this matters for the option trade: If R2 production starts on time with strong initial demand, analysts will likely raise estimates dramatically. A stock trading at $21 with $7B revenue potential (vs. current $5B) justifies $30-35 targets. The March 20th expiration captures the HYPE phase before production - perfect timing.

⚠️ Risk Catalysts (Negative)

Production Execution Risk 🏭

Rivian has history of missing production targets:

- 2024: Delivered 49,476 vehicles (down from 51,579 in 2023)

- Supply chain disruptions caused Q3 2024 guidance reduction

- R2 ramp-up complexity: New platform, new suppliers, shared facility with R1

- Any R2 delay announcement would be CATASTROPHIC for stock

Trump Administration Policy Headwinds 🏛️

Multiple regulatory risks under new administration:

- DOE loan claw-back risk: $6.6B loan finalized pre-inauguration - could new admin challenge?

- EV tax credit: Already expired September 2024; proposed $1,000 tax on new EVs would hurt affordability

- Zero-emission credits: $100M in revenue frozen by NHTSA

Tariff Cost Pressures 💸

Battery tariffs implemented May 2025 add ~$2,000 per unit cost:

- Impacts all 2025 production and early R2 units

- Mitigation not until 2027 when LG Arizona facility comes online

- Could compress margins and force price increases

Cash Burn & Dilution Risk 💰

- Q1 2025 free cash flow: -$526 million

- 2025 adjusted EBITDA loss: $2.0-2.25 billion

- 20.3% share count increase in past year - more dilution likely

- At current burn rate, may need additional capital raises before profitability

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration:

📈 Bull Case (40% probability)

Target: $28-$30

How we get there:

- 💪 Year-end deliveries BEAT lowered guidance (44,000+ vs. 43,500 target)

- ✅ Q4 earnings show continued gross profit improvement ($250M+ vs. $206M in Q1)

- 🏭 R2 pre-production units exceed expectations - no quality issues, on-time production start confirmed

- 💰 VW $1 billion milestone payment announced in February-March (earlier than June deadline)

- 📊 Management guides for 2026 revenue $7-8B with R2 ramp and gross margin expansion path

- 🎯 Analyst upgrades cascade: JPM, MS, Citi raise targets to $28-32 range as R2 de-risks

- 📈 Breakout above $24.50 gamma resistance triggers technical rally toward $30 call wall

- 🚀 Momentum builds as retail FOMO kicks in on R2 "iPhone moment" narrative

Key metrics needed:

- R2 pre-production photos/videos generating social media buzz

- Supplier confirmation of on-time parts delivery

- No production delays or quality recalls announced

- Cash position stabilizing with VW payment + improved margins

Call option P&L in Bull Case:

- Stock at $28: Calls worth $13.00, value = $156M total ($13 × 12,000) = 86% gain on $8.4M investment

- Stock at $30: Calls worth $15.00, value = $180M total ($15 × 12,000) = 114% gain

- Stock at $32: Calls worth $17.00, value = $204M total ($17 × 12,000) = 143% gain

Probability assessment: 40% because it requires solid execution across multiple fronts but fundamentals are improving. R2 timeline appears achievable based on validation build progress, and market sentiment has shifted positive (analyst upgrades, VW partnership validation). The $19 put wall provides strong downside support giving bulls confidence.

🎯 Base Case (35% probability)

Target: $19-$24 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid year-end deliveries meeting guidance (42,000-43,500 range)

- 📱 Q4 earnings in-line: Gross profit maintained but not spectacular, guidance cautious

- ⚖️ R2 pre-production progressing but no fireworks - "on track" for H1 2026

- 💰 VW payment comes in Q2 as scheduled (not early) - expected but not exciting

- 🤖 2026 guidance conservative: Revenue $6-6.5B as R2 ramps slowly through year

- 🔄 Trading within gamma support ($19 put wall) and resistance ($24.50) bands

- 📊 Market waits for actual R2 production proof before re-rating stock higher

- 💤 Volatility declines as binary risks resolve but upside catalysts don't materialize yet

Call option P&L in Base Case:

- Stock at $22: Calls worth $7.00, value = $84M total = 0% gain (breakeven on intrinsic value)

- Stock at $19: Calls worth $4.00, value = $48M total = -43% loss (but protected by put wall support)

- Stock at $24: Calls worth $9.00, value = $108M total = 29% gain

Why 35% probability: Stock at technical inflection point after 69% YTD rally. Needs clear positive catalyst to break higher, but strong support below. Most institutions will hold and wait for actual R2 deliveries (not just production start) before aggressively buying.

This is NOT the call buyer's target scenario - they're betting on the bull case, but this consolidation outcome still preserves most of their capital given the deep ITM strikes.

📉 Bear Case (25% probability)

Target: $16-$19 (TEST THE PUT WALL!)

What could go wrong:

- 😰 Year-end deliveries miss even lowered guidance (under 41,500) - demand concerns

- 🚨 Q4 earnings disappoint: Gross profit turns negative due to tariffs, cash burn accelerates

- ⏰ R2 DELAYED: Pre-production reveals quality issues, H1 2026 start pushed to Q3-Q4

- 💸 VW payment delayed or milestone not achieved - raises questions about partnership

- 📊 2026 guidance weak: Revenue below $6B, profitability timeline pushed further out

- 🇺🇸 Trump admin announces EV policy changes (tax credit elimination permanent, anti-EV incentives)

- 💔 Competitive pressure: Tesla announces $35K Model Y variant, crushing R2's price advantage

- 🔨 Break below $19 put wall triggers cascade toward $16-17 zone

Critical support levels:

- 🛡️ $19.00: MAJOR put wall - MUST HOLD or momentum shifts bearish

- 🛡️ $17.50: Secondary support

- 🛡️ $15.00: Deep support at call strike (buyer's "line in the sand")

- 🛡️ $13.00: Disaster scenario - back to Q3 2025 levels

Call option P&L in Bear Case:

- Stock at $19: Calls worth $4.00, value = $48M total = -43% loss

- Stock at $17: Calls worth $2.00, value = $24M total = -71% loss

- Stock at $15: Calls worth $0 (at-the-money), value = ~$0 = -100% loss (OUCH!)

Probability assessment: Only 25% because Rivian's fundamental trajectory is improving (positive gross profit achieved, VW partnership validates technology, R2 on track). However, execution risk is REAL and EV sector faces macro headwinds. The deep ITM nature of this trade provides significant downside cushion - even in bear case, stock would need to fall below $15 for total loss.

Key insight: The call buyer clearly believes bear case probability is <10% or they wouldn't risk $8.4M. By choosing the $15 strike, they've effectively said "I'm willing to lose my entire investment ONLY if RIVN falls below $15" (a 29% crash from current levels). That's EXTREME bullish conviction.

💡 Trading Ideas

🛡️ Conservative: Wait for R2 Production Proof

Play: Stay on sidelines until H1 2026 R2 production actually starts with confirmed deliveries

Why this works:

- ⏰ Too much binary risk between now and March 20th - R2 could be delayed, earnings could disappoint

- 💸 Stock already up 69% YTD at $21 - limited margin of safety at current levels

- 📊 Better entry likely post-Q4 earnings if stock consolidates to $19 put wall (10% cheaper)

- 🎯 Wait for PROOF not promises - let Rivian demonstrate R2 can actually scale production

- 📉 If R2 delay announced, stock could crater to $15-16 providing much better entry

- 🤔 The $8.4M call buyer has conviction, but they also have deep pockets for high-risk bets

Action plan:

- 👀 Monitor Q4 earnings closely (mid-Feb) for gross profit trends, cash burn, and 2026 guidance quality

- 🎯 Watch for R2 pre-production updates - any delays or quality issues are RED FLAGS

- ✅ Look for pullback to $18-19 zone post-earnings for stock entry with 15% margin of safety

- 📊 Track unusual options activity - if institutions BUY MORE calls at higher strikes, that's bullish signal

- ⏰ Revisit in April-May 2026 when R2 production is actually running and delivery numbers are real

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 20-30% drawdown if R2 delays or earnings disappoint. Get better entry if stock pulls back. Maintain optionality for actual production launch in Q2-Q3 2026.

⚖️ Balanced: Debit Call Spread (Defined Risk R2 Bet)

Play: Buy call spread betting on R2 momentum but with defined risk

Structure: Buy $22 calls, Sell $28 calls (March 20 expiration - SAME as the $8.4M trade)

Why this works:

- 🎯 Defined risk: $6 wide spread = ~$2-2.50 net debit per spread (adjust for current IV)

- 📊 Targets gamma resistance zone at $24.50-$28 where big move expected

- 🤝 Aligns with smart money positioning but at fraction of capital required

- ⏰ 87 days to expiration gives R2 catalysts time to play out (pre-production, Q4 earnings, analyst upgrades)

- 🛡️ Risk/reward favorable: Pay ~$2.50, make $3.50 if stock reaches $28 (140% gain)

- 📈 Breakeven around $24.50 - stock only needs 16% rally (achievable with positive R2 news)

Estimated P&L:

- 💰 Cost: ~$2.50 per spread ($250 per spread)

- 📈 Max profit: $3.50 if RIVN above $28 at expiration = 140% gain

- 📉 Max loss: $2.50 if RIVN below $22 = 100% loss (but defined and limited)

- 🎯 Breakeven: ~$24.50 (16% rally needed)

- 📊 Profit range: Any close between $24.50-$28 = partial to full profit

Entry timing:

- ✅ Enter NOW if you believe R2 pre-production is on track

- ⏰ OR wait 1-2 weeks post-New Year for any volatility spike on delivery numbers

- 🎯 Only enter if stock holds above $19 put wall (support intact)

- ❌ Skip if stock breaks below $19 (bearish technical breakdown)

Position sizing: Risk only 3-5% of portfolio (this is directional speculation on R2 success)

Exit plan:

- 🎯 Take profits at 75-100% gain ($4-5 spread value) if RIVN rallies to $26-27

- ⏰ Consider rolling up/out if stock hits $28 early (lock in gains, extend exposure)

- 🛡️ Cut losses at 50% if stock breaks $19 and R2 news turns negative

Risk level: Moderate (defined risk, directional bullish) | Skill level: Intermediate

🚀 Aggressive: Copy The Whale - Deep ITM Call (ADVANCED ONLY!)

Play: Buy smaller version of the $8.4M trade - deep ITM calls for leveraged bull exposure

Structure: Buy $15 calls (March 20 expiration - EXACT SAME TRADE)

Why this could work:

- 🐋 Following smart money: This is literally copying the institutional trade

- 💪 Delta exposure: ~0.85-0.90 delta = almost 1:1 stock participation with less capital

- 🎯 Downside protection: Strike 29% below current price provides HUGE cushion

- ⚡ Leverage advantage: Control ~$21K of stock for ~$7K per contract

- 📈 Bull case upside: If RIVN hits $30, calls worth $15 = 114% gain vs. 42% stock gain

- 🛡️ Put wall support: $19 gamma floor only 10% below current - strong technical support

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Each contract costs ~$7.00 ($700 per contract)

- ⏰ TIME DECAY: Even deep ITM, you're bleeding ~$0.05-0.10 per day in theta

- 😱 R2 DELAY RISK: If production pushed to Q4 2026, stock could fall to $15 and calls expire worthless

- 📊 Earnings risk: Q4 report could disappoint, triggering 20% selloff to $16-17

- 💔 Policy risk: Trump admin could kill DOE loan or implement anti-EV taxes

- ⚠️ You're betting $7,000+ per contract that RIVN stays above $15 (currently $21) - that's a BIG bet

Estimated P&L (per contract):

- 💰 Cost: ~$7.00 per contract ($700)

- 📈 Bull case ($30): Calls worth $15.00 = $800 profit per contract (114% gain)

- 🎯 Base case ($24): Calls worth $9.00 = $200 profit per contract (29% gain)

- 📉 Bear case ($19): Calls worth $4.00 = -$300 loss per contract (-43% loss)

- 💀 Disaster ($15): Calls worthless = -$700 loss per contract (-100% loss)

Breakeven point: ~$22.00 (you make money above this level at expiration)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Truly understand deep ITM call mechanics and how intrinsic vs. extrinsic value works

- ✅ Can afford to lose ENTIRE premium (real possibility if R2 badly delayed!)

- ✅ Have conviction equal to the institutional buyer (do YOU have $8.4M conviction?)

- ✅ Are comfortable with illiquid options (deep ITM strikes have wide bid-ask spreads)

- ✅ Understand you're making a leveraged bet on R2 production timeline execution

- ⏰ Have plan to close/roll position if R2 news turns negative (don't ride to zero!)

Position sizing - CRITICAL:

- ❌ DO NOT buy more than 5-10 contracts ($3,500-7,000 total) unless you're wealthy

- ✅ Position size based on "I can lose this entirely and sleep fine" amount

- 🎯 Consider this 5-10% of options portfolio MAX (this is HIGH risk despite deep ITM)

Exit strategy:

- 🎯 Take 50% profit at $26-27 (lock in gains, let rest run)

- ⏰ Consider rolling to June 2026 calls if R2 delayed but still viable

- 🛡️ HARD STOP: Exit if RIVN breaks below $19 put wall convincingly

- 📊 Monitor R2 news religiously - first sign of delay, GET OUT

Risk level: EXTREME (can lose 100% despite deep ITM) | Skill level: Advanced only

Probability of profit: ~55-60% (slightly better than base case due to deep ITM buffer)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏭 R2 production execution is EVERYTHING: This entire bull thesis rests on Rivian successfully launching R2 production in H1 2026. The company has history of missing production targets (2024: 49,476 vs. targets, 2025: reduced guidance twice). Supply chain disruptions, quality issues, or manufacturing complexity could EASILY delay R2 to Q3-Q4 2026 or beyond. If that happens, stock could crater 30-40% to $13-15 zone and these calls expire worthless. The $8.4M buyer is betting their entire investment that Rivian can execute flawlessly - that's a BIG assumption.

-

💸 Cash burn remains EXTREME despite improvements: Rivian burned -$526M in Q1 2025 free cash flow with full-year adjusted EBITDA loss of $2.0-2.25 billion. At this burn rate with $6.74B cash (including $1B VW note), runway is only 2-3 years before additional dilutive capital raises needed. Analysts don't expect profitability until 2032 - that's 7 years away! If R2 margins disappoint (currently projected only 2% vs. Tesla's 20%+), or if cash burn doesn't improve materially, Rivian could be forced into massive equity raises that crush existing shareholders. Share count already up 20.3% in past year.

-

🇺🇸 Trump administration policy risks are REAL and IMMEDIATE: The $6.6 billion DOE loan was rushed through before inauguration - new admin could potentially challenge or claw back. EV tax credit already expired September 2024, and Republicans proposed $1,000 tax ON new EVs. $100M in zero-emission credit revenue frozen by NHTSA. Any of these becoming permanent or expanding would devastate Rivian's economics and R2 affordability.

-

⚖️ Competition intensifying at EXACTLY the wrong time: Tesla dominates with 49% market share and could launch $35K Model Y variant that crushes R2's $45K price advantage. GM reached 13.8% EV market share and growing. Ford despite struggles has massive brand equity and dealer network. Rivian's current 3% EV market share and 0.25% total auto market share is TINY. Bernstein initiated with Underperform citing "fierce competition." What if R2 launches and nobody cares because Tesla/GM have better offerings?

-

💰 VW partnership dependency is a double-edged sword: While the $5.8 billion total deal validates technology, $3.5 billion is tied to operational, technical, and financial milestones. If Rivian fails to meet milestones (likely tied to R2 success), that capital never arrives. VW itself is struggling with EV profitability and could reduce commitment. Rivian is effectively betting its survival on external validation from a partner with its own problems.

-

📉 Demand softening post-tax credit expiration: Rivian reduced 2025 delivery guidance TWICE (51K → 46K → 43.5K). Tax credit expiration cited as factor. What if $45K is still too expensive for mass market without subsidies? What if recession hits and discretionary auto spending collapses? R2 could launch perfectly on time and STILL fail if demand isn't there. 2025 deliveries DOWN vs. 2024 despite new products is concerning.

-

💸 Tariffs crushing margins RIGHT NOW: Battery tariffs implemented May 2025 add ~$2,000 per unit. This hits every R2 unit through 2026 until LG Arizona facility comes online in 2027. With R2 gross margins projected at only 2% (vs. Tesla 20%+), $2K added cost could push margins NEGATIVE. Rivian may be forced to raise R2 price above $45K, killing mass-market appeal.

-

🛡️ Insider selling is NOT encouraging: CEO RJ Scaringe has 10b5-1 plan to sell up to 4M shares, CFO sold 35.43K shares in August. When founder/CEO is SELLING into a 69% YTD rally while retail is buying, that's a red flag. They know the business better than anyone - if they're not holding through R2 launch, why should you?

-

📊 Valuation at $26B market cap assumes PERFECTION: At current price, Rivian is valued higher than established automakers despite producing only 50K vehicles annually (vs. millions for Ford/GM). The market is pricing in R2 success, profitability by 2027-2028, and path to 200K+ annual units. ONE stumble and this valuation evaporates. The $8.4M call buyer is betting that $26B becomes $35-40B (adding another $10B+ in market cap). That requires flawless R2 execution AND market multiple expansion. Both are uncertain.

-

🎢 Historical volatility suggests EXTREME swings possible: RIVN traded from $10.36 to $22.76 in past year (120% range!). This isn't a stable blue-chip - it can gap 10-15% on single news items. The March 20th expiration captures Q4 earnings (mid-Feb) which could trigger 20% move EITHER direction. If you're not prepared for $18-$25 range whipsaw, don't trade this stock.

🎯 The Bottom Line

Real talk: Someone just committed $8.4 MILLION to a deep ITM call position on RIVN betting that the R2 platform launch will be a massive success that drives the stock from $21 to $28-30+ by March. This isn't a speculative OTM lottery ticket - this is a sophisticated institutional player using leverage to amplify returns on a HIGH-CONVICTION bull thesis. By choosing the $15 strike (29% below current price), they're effectively saying "I'm willing to lose my entire investment ONLY if Rivian completely fails and stock crashes below $15."

What this trade tells us:

- 🎯 Sophisticated player expects MAJOR MOVE higher (not just modest gains - they want $28-30+)

- 💰 They have conviction that R2 production will start ON TIME in H1 2026 and drive meaningful analyst upgrades

- ⚖️ The timing (right before year-end delivery numbers, Q4 earnings, and R2 pre-production start) is DELIBERATE

- 📊 They structured deep ITM vs. ATM/OTM because they want stock-like exposure with leverage, not lottery ticket speculation

- ⏰ March 20th expiration captures ALL the key catalysts: deliveries, earnings, VW payment, R2 momentum building

This IS a "load the boat" signal for true believers - but comes with MASSIVE execution risk.

If you own RIVN:

- ✅ Consider adding to position if you have HIGH conviction on R2 timeline (but size appropriately!)

- 📊 Set mental stop at $19 put wall - break below that level invalidates near-term bull thesis

- ⏰ If holding through earnings (mid-Feb), be prepared for 15-20% volatility either direction

- 🎯 Take partial profits at $26-28 to lock in gains while letting rest ride for $30+ potential

- 🛡️ Consider using proceeds from any rallies to buy protective puts if position gets large

If you're watching from sidelines:

- ⏰ DO NOT blindly follow this trade - institutional player has risk tolerance/timeframe you likely don't

- 🎯 Better approach: Wait for Q4 earnings clarity (mid-Feb) then reassess with 30+ days less time risk

- 📈 Looking for entry at $18-19 on any post-earnings pullback (15% margin of safety from current)

- 🚀 Key confirmations needed: R2 pre-production photos appearing, no delay announcements, positive analyst commentary

- ⚠️ If you DO want leveraged exposure, use defined-risk call spreads ($22/$28) not naked deep ITM calls

If you're bearish:

- 🎯 Wait for specific negative catalyst before shorting (fighting 69% YTD momentum is dangerous)

- 📊 Watch for break below $19 put wall - that's technical trigger for cascade to $16-17

- ⚠️ Put spreads ($22/$19 or $24/$19) offer defined-risk way to play downside

- 📉 Best short setup would be R2 delay announcement or disastrous Q4 earnings

- ⏰ Timing is EVERYTHING: Premature bearish positioning risks getting squeezed on positive R2 news

Mark your calendar - Key dates:

- 📅 Early January 2026 - Year-end 2025 delivery numbers release (42K-44K expected)

- 📅 End of December 2025 / Early January - R2 validation builds completion (critical milestone!)

- 📅 Mid-to-Late February 2026 - Q4 2024 earnings report (THE BIG ONE)

- 📅 March 20, 2026 - Option expiration for this $8.4M trade

- 📅 H1 2026 (April-June) - R2 production start expected

- 📅 By June 2025 - $1B VW milestone payment expected

Final verdict: Rivian's bull case is INCREDIBLY compelling - $5.8B VW partnership validates technology, $6.6B DOE loan funds Georgia expansion, R2 platform at $45K targets mass market with $7B annual revenue potential, and positive gross profit achieved for first time ever. BUT, execution risk is EXTREME. Company still burning $2B+ annually, has history of missing targets, faces policy headwinds and tariff pressures, and analysts don't expect profitability until 2032.

The $8.4M institutional call buy is a CLEAR signal: smart money thinks R2 execution will drive stock to $28-30+ by March. If you share that conviction and can stomach the risk, this is your signal. If you have ANY doubts about R2 timeline or Rivian's ability to execute, STAY AWAY - there will be better entry points after more proof.

This is a binary bet on R2 success. Choose wisely. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 8.09 reflects this specific trade's size relative to recent RIVN history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Deep ITM calls still carry risk of total loss if the underlying stock falls below the strike price. Rivian faces significant execution risk on R2 platform launch, ongoing cash burn, and policy/regulatory headwinds. The institutional buyer may have complex portfolio needs, tax considerations, or hedging strategies not applicable to retail traders.

About Rivian Automotive: Rivian Automotive, Inc. manufactures battery electric vehicles for the North American market, including luxury trucks (R1T), full-size SUVs (R1S), and delivery vans, with a market cap of $26.66 billion in the Motor Vehicles industry. The company is launching its mass-market R2 SUV platform in H1 2026 targeting $45,000 price point.