🌊 SE $28M Put Closure - Big Money Bails Out of Sea Limited After 26% Earnings Crash!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed out $28 MILLION in short put positions on $SE as the stock cratered 26% on an earnings miss -- the largest single-day drop since 2023. This is institutional risk management in real time: a trader who was bullish enough to sell puts at $120 and $100 is now paying up to escape before the damage gets worse. With $SE hitting a new 52-week low at $80.01, this is capitulation-level activity that often marks the final phase of forced institutional selling.

📊 Company Overview

Sea Limited (SE) is Southeast Asia's largest e-commerce, gaming, and fintech conglomerate:

- Market Cap: ~$46B (post-crash, estimated from ~$62B pre-earnings)

- Industry: E-Commerce, Digital Entertainment, Financial Services

- Exchange: NYSE (American Depositary Shares)

- Current Price: $87.85 (down ~26% intraday from prior close of ~$105.21)

- Employees: 80,700

- Primary Businesses: Shopee (e-commerce, 52% SEA market share), Garena/Free Fire (gaming, 100M+ daily players), Monee/SeaMoney (fintech, $9.2B loan book)

- Key Markets: Indonesia, Vietnam, Thailand, Malaysia, Philippines, Taiwan, Brazil, Singapore

Sea started as a gaming company (Garena) in 2015 and expanded into e-commerce through Shopee, now the dominant marketplace in Southeast Asia by gross merchandise value. Its third pillar, Monee (formerly SeaMoney), provides lending, payments, digital banking, and insurance across three licensed digital banking markets.

💰 The Option Flow Breakdown

The Tape (March 3, 2026):

| Time | Symbol | Side | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|

| 12:20:50 | SE | - | SELL | PUT | 2026-04-17 | $18M | $120 | 5,000 | SE20260417P120 |

| 12:20:50 | SE | - | SELL | PUT | 2026-06-18 | $10M | $100 | 5,000 | SE20260618P100 |

🤓 What This Actually Means

These are sell-to-close (STC) trades -- meaning an institution is closing out existing short put positions, not opening new ones. Here is the breakdown:

- 💸 Total premium paid to close: $28M across two legs

- 🎯 $120 PUT (April 17): Deep in-the-money by ~$35 with the stock near $84.64 at the time of trade. The $18M premium on 5,000 contracts means ~$36/contract. With only 45 days left and $35+ of intrinsic value, there is almost no extrinsic value left -- this was a pure "get me out" trade.

- 🎯 $100 PUT (June 18): In-the-money by ~$15. The $10M premium on 5,000 contracts means ~$20/contract. With 107 days to expiration, there is still some time value here, but the trader chose to eat the loss rather than wait.

- 📊 Position size: 10,000 total contracts = 1,000,000 shares of notional exposure (~$85M+)

- 🏦 Vol/OI ratio: 0.909 on the $120 strike -- nearly all of the open interest traded in this session

What is really happening here:

This trader originally sold these puts when $SE was trading much higher -- likely in the $120-$150+ range -- as either a bullish income strategy or cash-secured put accumulation plan. Today's 26% crash made the $120 puts deeply underwater, and the institution decided to cut losses rather than risk assignment or further deterioration. The simultaneous closure of both strikes at the exact same timestamp (12:20:50) confirms this was a coordinated risk reduction, not two separate traders.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-Score: 5.52 on the $120 strike) -- A trade this size relative to normal activity shows up only a handful of times per year. The 5,000-contract clip at this premium level screams institutional forced selling. The $100 strike registered as TYPICAL (-0.13 Z-Score), suggesting that strike sees more regular activity.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

$SE has been absolutely punished in 2026. After peaking near $199.30 (52-week high), the stock has been in a steep downtrend, and today's 26% crash on earnings sent it to a new 52-week low of $80.01. We are looking at a stock that has lost more than half its value from the highs. The YTD chart shows the severity -- this is not a gentle pullback, it is a waterfall decline that accelerated today.

Key observations:

- 📉 Freefall mode: The stock dropped from ~$105 to $77-$88 in a single session

- 💹 52-week low broken: $80.01 marks new territory -- no established support below

- 🎢 Post-earnings volatility: Implied vol will be elevated for weeks after a move this size

- 📊 Volume spike: Massive turnover as institutions rebalanced, stopped out, or capitulated

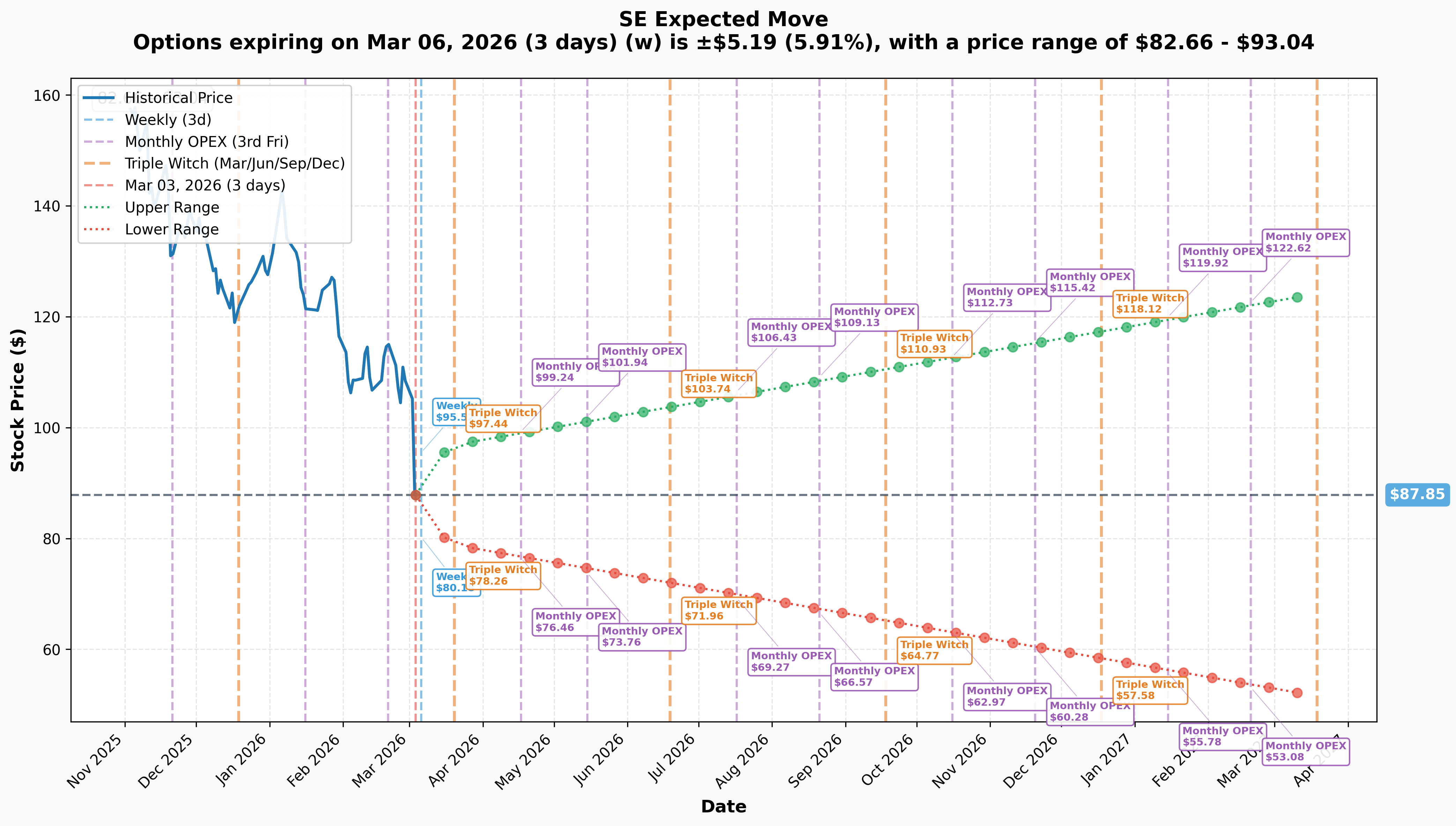

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (March 6 - 3 days): +/-5.91% (+/-$5.19) --> Range: $82.66 - $93.04

- 📅 Monthly OPEX / Triple Witch (March 20 - 17 days): +/-10.3% (+/-$9.05) --> Range: $78.80 - $96.90

- 📅 April OPEX (April 17 - 45 days): Range: $76.46 - $99.24

- 📅 June Triple Witch (June 19 - 108 days): Range: $71.96 - $103.74

- 📅 LEAPS (March 2027 - 381 days): +/-41.36% (+/-$36.34) --> Range: $51.51 - $124.19

Translation for regular folks:

Options traders are pricing in a nearly 6% move by Friday and a 10.3% swing through March expiration. That is enormous volatility -- the market is saying $SE could easily swing another $9 in either direction over the next two and a half weeks. For context, the April $120 put strike that just got closed out sits way above the upper implied range ($99.24), confirming it was completely underwater. The June $100 put strike sits right near the upper end of the June implied range ($103.74), meaning even with a recovery, that put would have stayed uncomfortably close to the money.

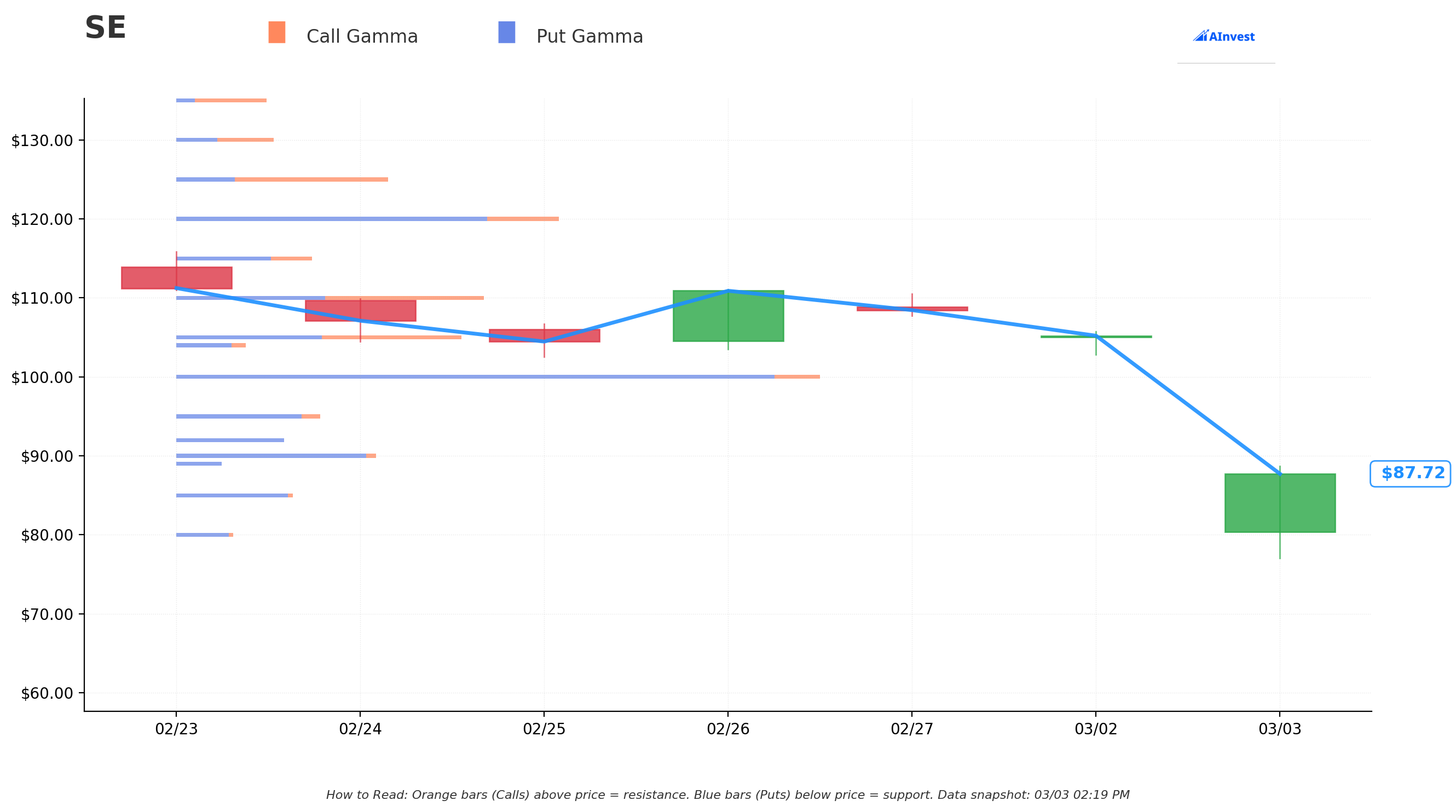

Gamma-Based Support & Resistance Analysis

Gamma-Based Support & Resistance Levels:

The gamma exposure data shows key strikes where options market makers have concentrated positioning. While net GEX values are relatively flat (indicating a low-gamma environment where dealers have less hedging pressure), the strike concentration tells us where the market is paying attention:

🔵 Support Levels (Put Gamma):

- $85 - Highest gamma concentration near current price; options activity clustered here

- $80 - Aligns with today's 52-week low ($80.01) -- psychological and options-based floor

- $75 - Next gamma level below; would represent a further ~15% decline from here

🟠 Resistance Levels (Call Gamma):

- $90-$95 - First cluster of gamma above current price; likely to see selling pressure here on any bounce

- $155-$170 - Major call gamma concentration far above -- these represent the "old world" when $SE was trading in the $100-$150 range

- $170 - Max gamma strike, reflecting heavy call positioning from before the crash

What this means for traders:

The gamma landscape is telling us that options positioning is still largely anchored to higher strikes -- the market has not yet adjusted to the new reality of $SE in the $80s. The low net GEX environment means market makers have less incentive to pin the stock at any particular level, which allows for wider price swings. This is consistent with the elevated implied volatility we see. The near-term support/resistance picture is dominated by round-number strikes ($80, $85, $90, $95, $100), which tend to act as magnets in high-volatility environments.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings Report - Expected Mid-May 2026 📊

Sea typically reports approximately 10 weeks after quarter-end, putting the next earnings around mid-May 2026. This will be the most important data point for the recovery thesis. Key metrics to watch:

- 📊 Shopee GMV trajectory (tracking toward 25% annual target or decelerating further?)

- 💳 Credit loss provision trend at Monee (stabilizing or worsening from the $393M Q4 spike?)

- 📈 Ad take rate progression (currently ~2%, long-term target 4-5%)

- 💰 Buyback execution progress on the $1B program

Free Fire Esports Events - March through July 2026 🎮

Free Fire Ramadan Cup 2026 is already underway (started February 21), with a new Clash Squad tournament launching in March and the Free Fire Esports World Cup in Riyadh, Saudi Arabia on July 15-18. These events drive user engagement and bookings for Garena, which delivered $3B in annual bookings in 2025.

$1B Share Buyback Execution 💰

Authorized in late 2025, the buyback program represents ~2.2% of the post-crash market cap at current prices. Management has flexibility on timing and method. The post-earnings crash creates an opportunity for aggressive buyback execution -- if management steps up, it could provide meaningful price support in the $75-$90 zone.

March 20 - Triple Witch OPEX 📅

Major options expiration could create elevated volatility and hedging flows. The implied move prices a $78.80-$96.90 range through this date.

⏪ Recent Catalysts (Already Happened)

Q4 2025 & Full Year 2025 Earnings (March 3, 2026) 💥

The trigger for today's crash. Revenue crushed expectations at $6.85B (+38.4% YoY) vs. $6.45B consensus, but EPS of $0.63 missed the $0.74-$0.80 consensus due to surging credit loss provisions ($393M in Q4, +67% YoY) and competitive spending. Full year revenue hit $22.9B (+36.4% YoY) with net income of $1.6B (+257% YoY). Shares plunged over 26% to a 52-week low.

2026 Guidance Disappointed 📉

Shopee GMV growth target of ~25% for 2026 signals deceleration from 26.8% achieved in 2025. EBITDA guided to "no lower than 2025 in absolute dollars" -- essentially flat, which spooked growth investors.

Analyst Price Target Cuts (March 3, 2026) 🔻

- Jefferies cut target to $150

- BofA cut target to $150 from $182, maintained Buy

- Even at the lowest analyst target ($135), that implies 73% upside from $77.89

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, earnings fallout, and upcoming catalysts:

📈 Bull Case (20% probability)

Target: $100-$120 by June 2026

How we get there:

- 🤝 $1B buyback program executes aggressively at these depressed levels, providing consistent buying support

- 📊 Q1 2026 earnings (mid-May) show credit loss provisions stabilizing and Shopee GMV tracking toward 25% target

- 🎮 Free Fire esports events drive engagement -- bookings momentum continues

- 💡 Ad take rate expansion accelerates (each 50bp increase on projected $159B GMV = ~$800M incremental revenue)

- 📈 30 out of 30 analysts recommend Buy with average targets of $180-$195 pre-earnings -- even post-revision targets stay well above $100

- 💪 The June implied move upper range reaches $103.74, and a catalyst-driven squeeze could push well beyond

Key risk to bulls: The earnings miss was not just a one-quarter blip -- credit provisions are structural as the loan book scales, and competitive spending against TikTok Shop and Temu may not ease.

🎯 Base Case (50% probability)

Target: $78-$97 range-bound through April OPEX

Most likely scenario:

- ✅ Stock stabilizes in the $80-$90 zone as the initial panic selling subsides

- 📊 Implied move ranges provide the guardrails: Weekly ($82.66-$93.04), Monthly ($78.80-$96.90)

- 🔄 No major new catalysts until Q1 earnings in mid-May, so the stock drifts and consolidates

- 💰 Buyback provides some floor support but is not enough to reverse the trend alone

- 📉 Analyst price target revisions filter in over the next 1-2 weeks, creating episodic volatility

- ⏰ Options market makers operate in a low-gamma environment, allowing wider daily ranges

This is the stabilization phase. After a 26% single-day crash, the stock typically needs 2-4 weeks to find a floor as forced sellers finish exiting and value buyers start nibbling.

📉 Bear Case (30% probability)

Target: $60-$75

What could go wrong:

- 😰 Follow-through selling in coming sessions as more institutions rebalance portfolios and index funds adjust weights

- 📉 Credit loss provisions at Monee continue surging -- if NPLs deteriorate materially on the $9.2B loan book, fintech segment profits evaporate entirely

- ⚖️ TikTok Shop and Temu competition intensifies, forcing even more spending to defend Shopee's 52% market share

- 💸 Growth-to-value rotation accelerates across tech sector, compressing multiples further

- 🛡️ $80 support breaks decisively: Today's 52-week low at $80.01 is the last line of defense. A break below opens up the LEAPS implied move lower bound at $51.51

- 📊 The LEAPS data prices in the possibility of $SE reaching as low as $51.51 over the next year -- the market is not ruling out a much deeper decline

This bear case is elevated because the EPS miss was driven by structural issues (credit provisions, competitive spending), not a one-time event. If the next quarter shows no improvement, the "growth at what cost?" narrative takes hold.

💡 Trading Ideas

🛡️ Conservative: The "Wait and Collect" Cash-Secured Put

Play: Sell June 18 $70 puts to collect premium while waiting for a potential entry below current levels

Why this works:

- 💰 $70 strike is 20%+ below current price -- you only get assigned if $SE drops another leg

- ⏰ 107 days of theta decay working in your favor

- 📊 $70 sits below even the June implied move lower bound ($71.96), giving probability on your side

- 🛡️ If assigned, you own $SE at an effective cost basis of $70 minus premium -- a level not seen since 2022

- 💸 Collect ~$2-4/contract depending on IV at entry (~3-6% return on cash secured)

Estimated P&L:

- 💰 Max profit: Full premium collected if $SE stays above $70 at June expiration

- 📉 Risk: Assignment at $70 minus premium; continue to own shares in a declining stock

- 🎯 Breakeven: ~$66-$68 (deep value territory)

Risk level: Low-Moderate | Skill level: Beginner-friendly

⚖️ Balanced: The "Dead Cat or Real Floor" Put Spread

Play: Sell April 17 put spread to collect premium while defining your risk

Structure: Sell $80 puts / Buy $70 puts (April 17 expiration)

Why this works:

- 🎯 $80 is today's 52-week low -- established as a psychological floor

- 📊 April implied range lower bound is $76.46, so $80 has a reasonable chance of holding

- ⏰ 45 days of time decay, expires well before Q1 earnings (mid-May)

- 💰 Collect ~$2.50-$4.00 per spread (~25-40% of width)

- 🛡️ Defined risk: Max loss $10 per spread minus premium collected

Estimated P&L:

- 💰 Max profit: ~$250-$400 per spread if $SE stays above $80

- 📉 Max loss: ~$600-$750 per spread if $SE below $70 at expiration

- 🎯 Breakeven: ~$76-$77.50 (near the implied move lower bound)

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: The "Capitulation Bounce" Call Spread

Play: Buy a call spread targeting the recovery bounce into Q1 earnings

Structure: Buy June 18 $90 calls / Sell June 18 $110 calls

Why this works:

- 📈 Post-crash bounces of 15-25% within 30-60 days are common after earnings-driven sell-offs of this magnitude

- 🤝 $1B buyback program provides floor support; management has every incentive to buy here

- 💰 Every analyst has a Buy rating with targets of $135-$195 -- even the lowest target implies 73% upside

- 📊 The June implied move upper range reaches $103.74, and the $90-$110 spread captures the sweet spot of a recovery

- 🎮 Free Fire esports events and Shopee ad monetization provide potential positive data points before June

Why this could go wrong:

- 💥 The earnings miss was structural, not a one-off -- credit provisions and competitive spending may worsen

- 📉 No major positive catalyst until Q1 earnings in mid-May, and the stock could drift lower in the meantime

- ⚠️ IV is elevated post-crash, meaning options are expensive -- you are paying up for this bet

Estimated P&L:

- 💰 Net debit: ~$4-$6 per spread

- 📈 Max profit: $14-$16 per spread ($20 width minus debit) if $SE above $110 at June expiration

- 📉 Max loss: Net premium paid (~$400-$600 per spread) if $SE stays below $90

- 🎯 Sweet spot: $SE at $100-$110 at June expiration (implied 14-25% recovery from crash levels)

Risk level: High (directional bet on recovery) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💳 Credit loss provisions are the real story: Monee's credit provisions surged 67% YoY to ~$393M in Q4 while the loan book grew 80% to $9.2B. This is the fastest-growing segment and the one with the most risk. If non-performing loans spike as the loan book seasons, provisions could consume fintech segment profits entirely -- and that is what spooked the market today.

-

🛒 Competitive spending pressure is not easing: TikTok Shop, Temu (PDD Holdings), and Lazada (Alibaba) are all pouring money into Southeast Asian e-commerce. TikTok Shop has 40%+ market share in Vietnam. Shopee's 52% regional share came at a cost -- logistics, marketing, and server expenses all grew faster than revenue in Q4.

-

📉 Guidance signals deceleration, not acceleration: The ~25% Shopee GMV growth target for 2026 is below the 26.8% achieved in 2025. EBITDA guided to "no lower than 2025" is essentially flat. For a stock that traded at 30x+ forward earnings, flat EBITDA growth kills the multiple.

-

🎮 Single-game concentration risk: Garena's $3B in bookings are overwhelmingly from Free Fire. Any user fatigue, regulatory action (India ban risk persists), or competitive displacement would be material to the entire gaming segment.

-

🌏 Regulatory and macro uncertainty: Indonesia tariffs of 100-200% on Chinese imports benefit Shopee's local-seller model but create policy uncertainty. Data sovereignty and AI regulation frameworks are evolving across multiple SEA markets. Rising interest rates in some SEA countries could pressure consumer lending demand at Monee.

-

📊 Institutional positioning reset in progress: With 62.4% institutional ownership including Tencent at 18.5%, forced rebalancing after a 26% crash day can create multi-day selling pressure. Index funds, quant models, and risk parity strategies all need to adjust -- that process typically takes 3-5 trading sessions.

🎯 The Bottom Line

Real talk: An institution just paid $28M to close out short puts on $SE the same day the stock crashed 26% on earnings. That is the financial equivalent of running for the exits. The Z-Score of 5.52 on the $120 put means a trade this abnormal shows up only a handful of times per year for this stock. This is forced risk management, not a directional bet -- and when institutions are scrambling to close positions at a loss, it typically signals we are in the late stages of a panic cycle.

What this trade tells us:

- 🎯 An institution that was previously bullish on $SE (selling puts = expecting the stock to stay above $120/$100) has completely reversed course

- 💰 They paid $28M to close rather than risk further losses or forced assignment on 1,000,000 shares

- ⚖️ The closing of risk (STC, not STO) is neutral-to-slightly-bullish for the stock -- it removes short put exposure from the system

- 📊 Extreme put activity on a massive down day often marks near-term capitulation

If you are bullish on $SE long-term:

- ✅ The fundamentals are not as bad as the stock price suggests -- revenue grew 38.4%, net income tripled to $1.6B, Shopee has 400M active buyers

- 📊 Forward P/E of ~18-20x is historically cheap for a company growing revenue 36%+ annually

- 🛡️ Wait for stabilization in the $78-$88 zone before entering -- catching a falling knife in the first 48 hours is risky

- ⏰ Q1 earnings in mid-May will be the real test of whether the growth story is intact

- 💪 The $1B buyback provides support, and even the lowest analyst target ($135) implies 73% upside

If you are watching from the sidelines:

- 🎯 A stabilization around $80-$85 (near today's intraday lows) would be the most attractive entry zone

- 📊 Wait for at least 3-5 days of trading to let the forced selling subside before sizing up

- 🤝 Watch for insider buying or accelerated buyback announcements -- those would be strong signals

- 💡 The implied move gives you guardrails: $78.80-$96.90 through March 20 OPEX

If you are bearish:

- 📉 The structural issues (credit provisions, competitive spending, decelerating growth) are real and not easily fixed in one quarter

- 🎯 Bear put spreads ($80/$70 for April) offer defined-risk downside plays

- ⚠️ Do not short a stock on the day of a 26% crash -- the initial bounce/dead cat phase often comes first

- ⏰ Better to wait for any relief rally to $90-$95 before initiating bearish positions

Mark your calendar -- Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $82.66-$93.04)

- 📅 March 20 - Triple Witch OPEX (implied range: $78.80-$96.90)

- 📅 March 2026 - New Free Fire Clash Squad tournament launch

- 📅 April 17 - Monthly OPEX (expiration of the $120 put that was closed today)

- 📅 Mid-May 2026 - Q1 2026 earnings report (the make-or-break catalyst)

- 📅 June 18 - June Triple Witch (expiration of the $100 put that was closed today)

- 📅 July 15-18 - Free Fire Esports World Cup in Riyadh

Final verdict: The $28M put closure is the sound of an institution tapping out. After a 26% crash, the smart money is reducing exposure and reassessing -- not doubling down. For retail traders, this means the dust has not settled yet. The earnings miss was driven by structural concerns (credit quality, competitive spending) that will not resolve overnight. But here is the other side: a company growing revenue 38% with $9.9B in cash and every analyst on Wall Street screaming Buy does not stay at these levels forever. Let the forced selling play out, watch the $80 support level like a hawk, and look for your entry when the panic subsides. The catalysts are lined up (buyback, Q1 earnings, esports events) -- you just need patience to wait for the right moment.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The Z-Score of 5.52 reflects this specific trade's unusualness relative to recent activity -- it does not imply the trade will be profitable or that you should follow it. $SE dropped 26% in a single day, which means volatility is extreme and position sizing should reflect that reality. Always do your own research and consider consulting a licensed financial advisor before trading.

About Sea Limited: Sea Limited is Southeast Asia's largest e-commerce, gaming, and fintech conglomerate with a ~$46B market cap, operating Shopee (52% SEA e-commerce market share, 400M active buyers), Garena/Free Fire (100M+ daily players, $3B annual bookings), and Monee/SeaMoney ($9.2B loan book, digital banking licenses in Singapore, Indonesia, and the Philippines).