💎 SHOP $30M Smart Money Exit - Taking Profits on E-Commerce Giant's 57% Rally! 🛡️

📅 December 30, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just UNLOADED $30 MILLION worth of SHOP call options at the $140 strike this morning! This monster exit sold 10,000 contracts expiring February 20th at $30.10 per share - locking in MASSIVE gains on a deep in-the-money position with the stock trading at $166.11. With Shopify up +57.6% YTD and sitting near all-time highs, smart money is clearly cashing out ahead of Q4 earnings on February 18th. Translation: The institutions that rode SHOP's incredible AI-commerce rally from $110 to $180 are taking their chips off the table!

📊 Company Overview

Shopify (SHOP) is the leading e-commerce platform powering modern commerce worldwide:

- Market Cap: $218.6 Billion (4th largest in software)

- Industry: Prepackaged Software Services - E-Commerce Platform

- Current Price: $166.11 (near all-time high of $182.19)

- Primary Business: Cloud-based multi-channel commerce platform for small/medium businesses - subscriptions, payments (Shop Pay), fulfillment, POS, B2B solutions

Shopify operates two revenue streams: subscription solutions (recurring revenue from merchants using the platform) and merchant solutions (payment processing, shipping, capital). With 8,100 employees serving merchants globally, SHOP dominates the direct-to-consumer space with 73% of top 800 DTC brands choosing their platform.

💰 The Option Flow Breakdown

The Tape (December 30, 2025 @ 12:55:30):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:55:30 | SHOP | BID | SELL | CALL $140 | 2026-02-20 | $30M | $140 | 10K | 40K | 10,000 | $166.11 | $30.10 |

🤓 What This Actually Means

This is a profit-taking exit on a massive winning position! Here's what went down:

- 💸 Huge profit realized: $30M collected ($30.10 per contract × 10,000 contracts)

- 🎯 Deep in-the-money: $140 strike is $26.11 below current price - these calls have $26.10 intrinsic value

- 💰 Original position likely purchased: Summer 2025 around $130-140 stock price (cost basis probably $15-20/contract)

- 📈 Estimated profit: If purchased at $15, selling at $30.10 = 100% gain on $15M → $30M position!

- ⏰ Strategic timing: 52 days before expiration and just 50 days before Q4 earnings (Feb 18, 2026)

- 🏦 Institutional de-risking: Selling rather than exercising suggests hedge fund profit-taking, not bearish conviction

What's really happening here: This trader likely accumulated these $140 calls when SHOP was trading around $130-140 during Q3 earnings in November. They rode the explosive rally to $180 (record-breaking BFCM sales, AI partnerships, Winter '26 Edition launch) and are now LOCKING IN GAINS near all-time highs. Rather than waiting 52 more days and risking Q4 earnings volatility, they're taking their $15-20M profit TODAY.

Why sell instead of exercise? Simple math: Selling the calls for $30.10 gives them $30.1M in cash. Exercising would require putting up $140M ($140 × 100 × 10,000 contracts) to buy the shares, then selling at $166.11 for net proceeds around $26M. They're actually getting MORE value by selling the options than exercising - that extra $4.10/share ($4.1M total!) represents time value and volatility premium.

Unusual Score: 🔥 EXTREMELY UNUSUAL (3.05 Z-score) - This trade is 305% larger than typical SHOP activity! While not "once-in-a-lifetime," this is definitely top-tier institutional flow that happens only a few times per year on SHOP. The moderate classification (rather than extreme) shows SHOP regularly sees large institutional trades, but 10,000 contracts at $30M notional is still MASSIVE.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Shopify has delivered an OUTSTANDING performance in 2025 - up +57.6% YTD with current price of $166.11 (started the year around $105). The chart tells a powerful AI-commerce growth story - after hitting all-time highs of $182.19 in late October/early November, SHOP has consolidated in a tight $165-175 range through December.

Key observations:

- 🚀 Multi-phase rally: Steady climb from $105 to $180 over 11 months with three distinct legs

- 📈 Breakout momentum: October surge from $155 to $180 (+16%) driven by Winter '26 Edition launch and analyst upgrades

- 🎢 Elevated volatility: Recent consolidation after parabolic Q4 run-up

- 📊 Institutional accumulation: Volume spikes in October/December showing smart money positioning

- ⚠️ Profit-taking zone: Current consolidation at $165-170 suggests digestion of gains before next catalyst

The stock has shown remarkable resilience, bouncing strongly from any dips below $160 throughout November-December. However, failure to break decisively above $175-180 resistance indicates market waiting for Q4 earnings catalyst.

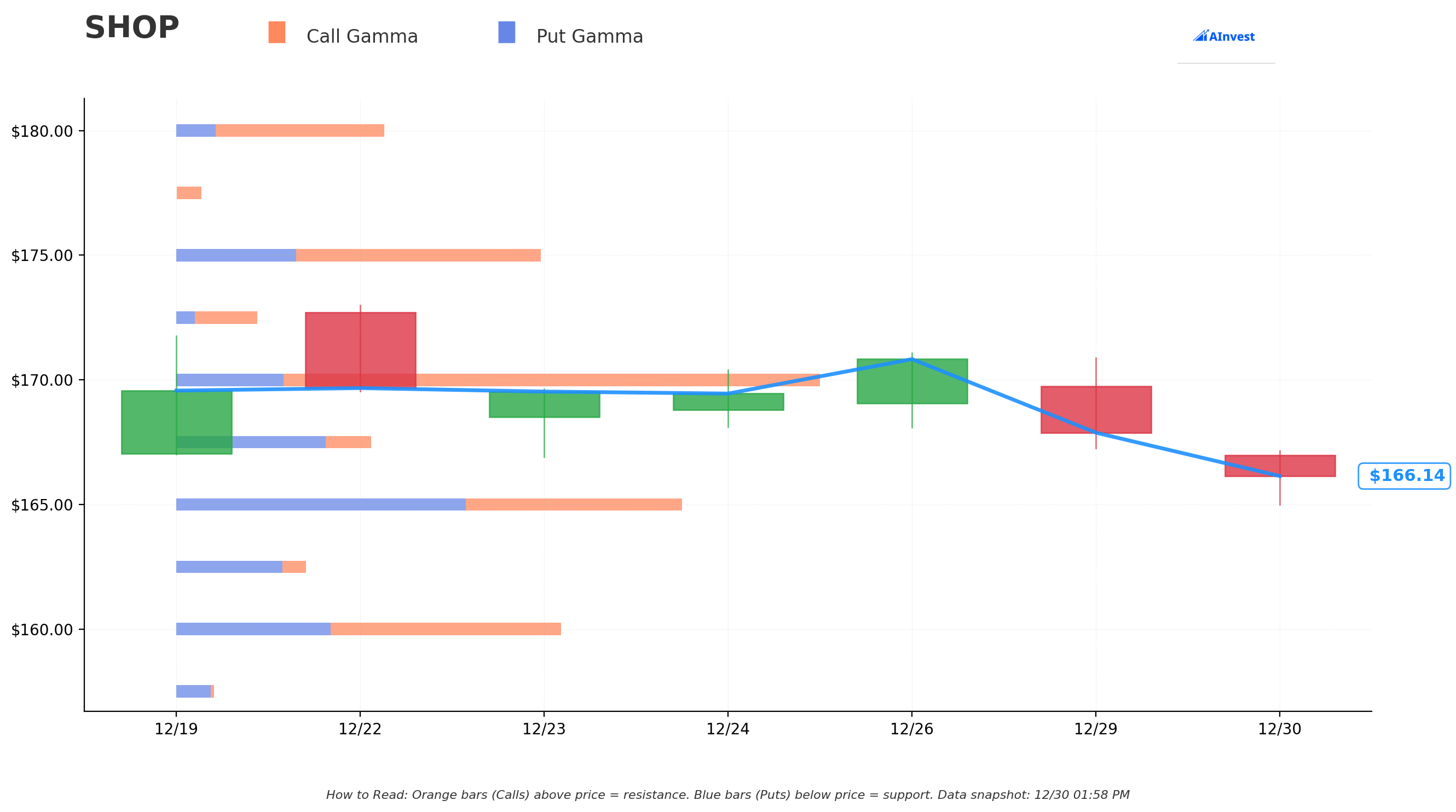

Gamma-Based Support & Resistance Analysis

Current Price: $166.03

The gamma exposure map reveals critical price magnets where options activity creates natural support and resistance:

🔵 Support Levels (Put Gamma Below Price):

- $165 - Immediate floor with 4.9B total gamma exposure (STRONG support - dealers buying dips here)

- $160 - Secondary support at 3.7B gamma (major psychological level + structural floor)

- $140 - Deep support wall at 6.2B gamma (STRONGEST PUT GAMMA - exactly where this call was struck!)

🟠 Resistance Levels (Call Gamma Above Price):

- $170 - Immediate ceiling with 6.2B gamma (STRONGEST RESISTANCE - massive call open interest creates selling pressure)

- $175 - Secondary resistance at 3.5B gamma (previous all-time high area from late 2024)

What this means for traders: SHOP is trading in a NARROW consolidation range between solid $165 support and stubborn $170 resistance. The gamma data shows the $170 level has the HIGHEST call gamma concentration (6.2B - matching the $140 put wall), creating natural mechanical selling as market makers hedge. This tight range screams "coiling spring" before the next major move.

Notice the $140 strike significance? That's the STRONGEST support level in the entire gamma profile (6.2B) - this call seller positioned at the absolute floor of SHOP's bullish structure. They're saying "even if SHOP drops to $140, these calls still have $26 of intrinsic value to protect me." But now at $166, with most of the move captured, they're cashing out.

Net GEX Bias: Slightly bullish but balanced (call gamma slightly higher) - Market is neutral-to-bullish but cautious ahead of earnings. The concentration at $170 suggests that's the "maximum pain" level where most options expire worthless.

Implied Move Analysis

Options market pricing for upcoming expirations:

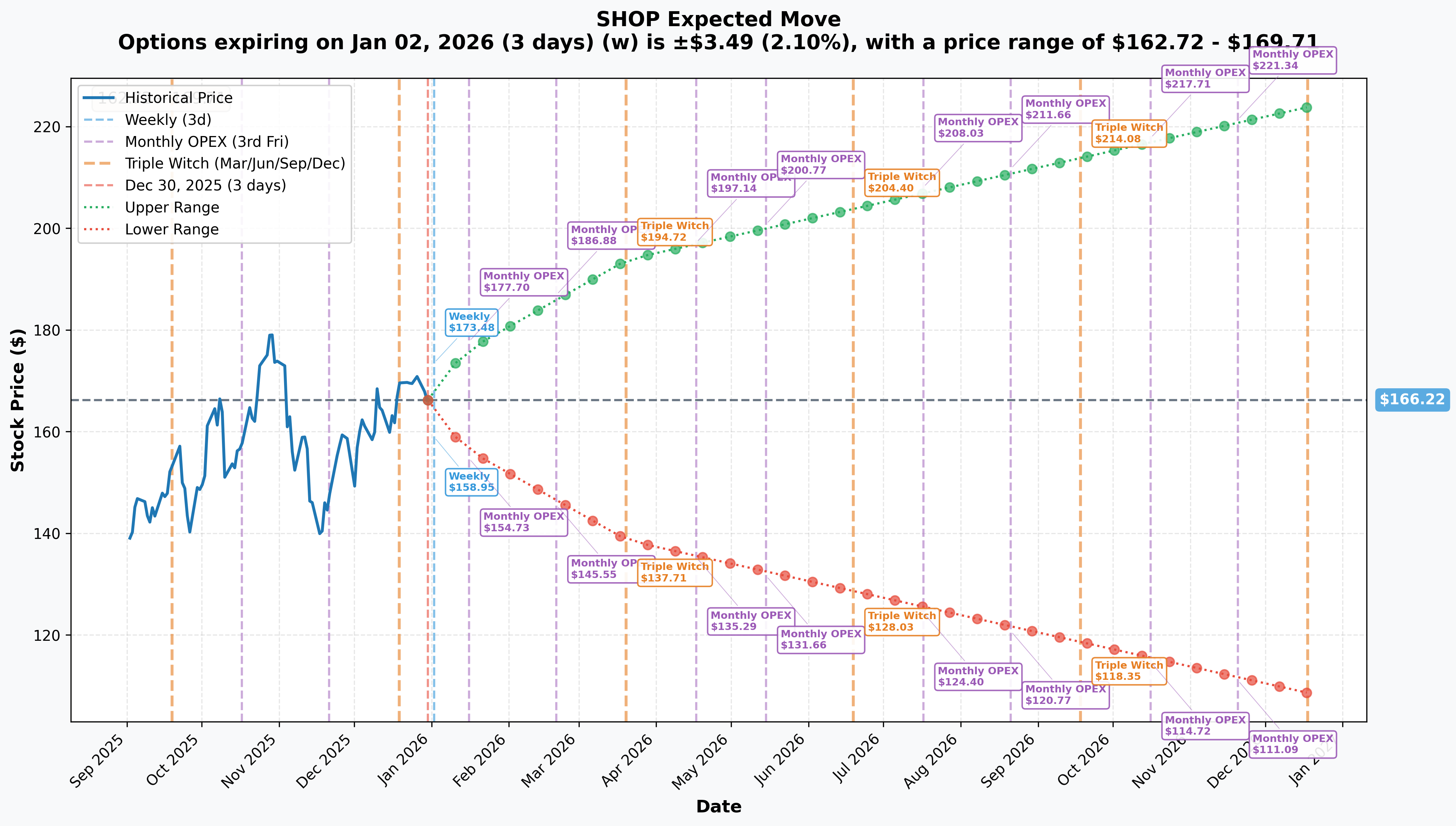

- 📅 Weekly (Jan 2 - 3 days): ±$3.49 (±2.1%) → Range: $162.72 - $169.71

- 📅 Monthly OPEX (Jan 16 - 17 days): ±$10.09 (±6.07%) → Range: $156.12 - $176.31

- 📅 Quarterly Triple Witch (Mar 20 - 80 days): ±$27.62 (±16.62%) → Range: $138.59 - $193.84

- 📅 February OPEX (Feb 20 - 52 days - THIS TRADE!): ±$20.77 (±12.5%) → Range: $145.55 - $186.88

Translation for regular folks: Options traders are pricing in a CALM 2.1% move ($3.49) by this Friday for year-end, but expect increasing volatility into January OPEX (6% move) as Q4 earnings approach. The February 20th expiration (when this $30M trade expires) has an implied range of $145-$187, suggesting the market sees a real possibility of an 11-12% swing in either direction.

Key insight: The sharp increase in implied volatility from 2.1% (weekly) to 12.5% (February) reflects MASSIVE earnings uncertainty on February 18th. The market is essentially saying "we expect SHOP to stay quiet until earnings, then FIREWORKS." The lower bound of $145.55 shows the market thinks there's a real (though low probability) scenario where SHOP gives back recent gains if holiday quarter disappoints.

Why the call seller chose February 20th expiration: They positioned AFTER earnings (Feb 18) intentionally - letting someone else deal with the binary event risk while collecting maximum premium. Smart! They captured the entire rally from $130-140 to $166, and now they're letting the next holder deal with earnings volatility.

🎪 Catalysts

🔥 Immediate Upcoming Catalysts (Next 60 Days)

Q4 2025 Earnings - February 18, 2026 (50 DAYS AWAY!) 📊

Shopify reports fiscal Q4 results on Tuesday, February 18, 2026 before market open. This is THE catalyst that will determine if the 57% YTD rally continues or consolidates. Wall Street consensus and key expectations:

- 📊 Revenue: $3.59 billion (consensus estimate) - representing the critical holiday quarter performance

- 💰 EPS: $0.40 (consensus estimate)

- 🛍️ Black Friday Cyber Monday Impact: Record-breaking $14.6B GMV (+27% YoY) needs to translate to strong revenue/margins

- 🤖 Agentic Storefronts Adoption: First metrics on ChatGPT/Perplexity/Copilot integrations (launched Dec 11)

- 📈 B2B GMV Growth: Continuation of 140% growth trajectory from 2024

- 💳 Shop Pay Penetration: Tracking toward 70%+ of GMV vs 65% in Q3

- 🌍 International Expansion: Europe now 21% of revenue - watching for acceleration

Upside surprise potential: Record BFCM at $14.6B (+27% YoY with +24% constant currency) provides significant visibility into Q4 strength. Analyst price targets recently raised to $190-198 range (Wells Fargo $198, DA Davidson $195) suggest Street sees upside bias. Winter '26 Edition's 150+ features could drive subscription upgrades.

Downside risk factors: Any disappointment in gross margins (need 54%+ to show operating leverage), slower-than-expected Agentic Storefront adoption, or conservative guidance on international expansion could trigger selloff. Brief system degradation during BFCM (resolved Monday evening) could raise reliability concerns. At 119-125x P/E, any miss means severe multiple compression.

🚀 Recent Catalysts (Already Happened - Driving Current Price)

Record-Breaking BFCM 2025 (November 29 - December 2) 🛍️

Shopify merchants generated record-breaking $14.6 billion in Black Friday Cyber Monday sales, validating platform strength:

- 🎯 Total Sales: $14.6B (+27% YoY, +24% constant currency) - MASSIVE beat

- ⚡ Peak Performance: $5.1M per minute at 12:01pm EST Black Friday

- 🎉 Black Friday Alone: ~$6.2 billion (+25% YoY)

- 🌎 Customer Reach: 81+ million customers worldwide

- 🏪 POS Growth: +33% YoY in global in-store sales (omnichannel strength)

- 🚀 New Merchants: 15,800+ entrepreneurs made their first sale

- 📊 Record Days: 94,900+ merchants had their highest-selling day ever

Why this matters: This validates Shopify's platform at SCALE during the most critical retail period. The 27% growth significantly outpaced broader e-commerce growth (~5-7% industry-wide), showing market share gains. However, brief system degradation impacting some merchant admins highlights infrastructure challenges at peak loads.

Winter '26 Edition Launch - Game-Changing AI Features (December 11, 2025) 🤖

Shopify launched 150+ new features including revolutionary AI capabilities:

- 🤖 Agentic Storefronts: Products now discoverable/purchasable directly in ChatGPT, Perplexity, Microsoft Copilot (FIRST-MOVER ADVANTAGE!)

- 🧠 Sidekick AI Enhancements: Now builds custom apps, automates workflows, generates analytics reports, edits images/emails

- 📊 Sidekick Pulse: Proactive AI monitoring with personalized market trend recommendations

- 🧪 SimGym Testing App: "Flight simulator" for testing storefront changes without affecting live conversion

- 📱 Tinker App: Launching early 2026 - consolidates premium AI tools into mobile platform

- 🔬 Native A/B Testing: Built directly into admin without external apps

- 💳 Shop Pay UK: Now available with terms up to 24 months

- 📦 Product Variants: Increased limit to 2,048 variants per product

This is HUGE: OpenAI partnership bringing commerce to ChatGPT conversations positions Shopify for the "agentic commerce" revolution where AI assistants become the primary shopping interface. Brands like Glossier, Spanx, Vuori, Away, Stanley 1913 already accessible via ChatGPT. This is Shopify's "iPhone moment" - defining the next platform shift.

Q3 2025 Results - Momentum Confirmed (November 12, 2025) 📈

Shopify crushed Q3 expectations, validating the growth trajectory:

- 💰 Revenue: $2.84B (+32% YoY), beating consensus $2.76B

- 📊 GMV: $92B (+32% YoY) - gross merchandise volume acceleration

- 💵 Free Cash Flow: $507M (18% FCF margin) - ninth consecutive quarter of double-digit FCF margins!

- 📈 Merchant Solutions: +38% YoY (payments, fulfillment strength)

- 🔄 Subscription Solutions: +15% YoY (steady recurring revenue)

- 🌍 International GMV: +41% YoY; Europe now 21% of revenue

- 💳 Shop Pay: 65% GMV penetration (up from 60% prior quarter)

- 🎯 Q4 Guidance: Mid-to-high 20% revenue growth projected

Analyst Activity - Wave of Upgrades (December 2025) 📊

Major firms raised price targets based on "agentic commerce" positioning:

| Firm | Rating | Price Target | Change |

|---|---|---|---|

| Wells Fargo | Overweight | $198 | Raised sharply |

| DA Davidson | Buy | $195 | Raised |

| UBS Group | - | $195 | New target |

| Morgan Stanley | - | $192 | Raised |

| Bank of America | - | $190 | From $185 |

Consensus: 26 Strong Buy, 2 Buy out of 44 analysts (59% Strong Buy) with average price target $168.69. Rationale focused on AI-driven commerce leadership, merchant mix recovery, and margin leverage into 2026.

📅 Upcoming Catalysts (Q1-Q2 2026)

Tinker App Launch - AI Creative Tools (Early 2026) 📱

AI-powered mobile creative tool for entrepreneurs launching early 2026 could drive incremental subscription revenue. This consolidates premium AI tools into mobile, potentially creating new high-margin revenue stream.

Shop Pay Installments International Expansion (H1 2026) 🌍

Affirm partnership expansion targeting UK, Australia, France, Germany, Netherlands:

- 💳 Premium Package: Up to 24-month installments on orders $50-$17,500

- 📈 Merchants report average 7% sales increase and 2.7% AOV increase

- 🎯 Could unlock significant European GMV growth (currently 21% of revenue)

- 🇨🇦 Canada rollout ongoing (launched April 2025) - watching adoption metrics

Shoptalk 2026 Conference (March 24-26) 🎤

Shopify confirmed as exhibitor/sponsor at Shoptalk 2026 in Las Vegas - potential platform for product announcements or customer wins.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing, here are scenarios through February 20th expiration (THIS TRADE!):

📈 Bull Case (30% probability)

Target: $185-$195

How we get there:

- 💪 Q4 earnings CRUSH with revenue toward $3.7-3.8B (high-end of guidance) driven by BFCM momentum

- 🤖 Agentic Storefronts showing early traction with 5-10% of merchants integrating ChatGPT commerce

- 💳 Shop Pay penetration accelerates to 70%+ of GMV, Installments Premium driving AOV gains

- 🌍 International growth accelerates above 40% with Europe expanding to 23-24% of revenue

- 📊 Gross margins expand to 55%+ showing operating leverage at scale

- 🚀 Breakout above $170-175 resistance triggers technical rally through gamma ceiling

- 💰 Additional analyst upgrades post-earnings drive price targets toward $200+

- 📱 Tinker app monetization details announced with attractive unit economics

Key metrics needed:

- GMV growth maintaining 30%+ trajectory

- Free cash flow margins sustaining above 17-18%

- B2B GMV continuing 100%+ growth rates

- Merchant churn remaining low despite economic uncertainty

Why 30% probability: Requires near-perfect execution on multiple fronts with stock already up 57% YTD at premium 119x P/E valuation. Gamma resistance at $170 creates mechanical headwinds. Amazon Buy with Prime remains competitive threat (8-18% revenue at risk per UBS). However, record BFCM at $14.6B provides strong foundation.

🎯 Base Case (50% probability)

Target: $160-$175 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus (~$3.5-3.6B revenue, $0.38-0.42 EPS)

- 📈 BFCM strength translates to respectable holiday quarter but not blowout

- 🤖 Agentic Storefronts showing promise but too early for material revenue impact (adoption takes time)

- ⚖️ Guidance for Q1 2026 in-line to slightly conservative (normal seasonal patterns)

- 💳 Shop Pay continuing steady 65-68% penetration, international rollout progressing on schedule

- 🔄 Trading within gamma support ($165) and resistance ($170-175) bands for weeks

- 📊 Market digests 57% YTD gains, waits for Tinker launch and international expansion proof points

- 💤 Volatility crush post-earnings (IV drops from elevated pre-earnings levels)

This aligns with the call seller's decision: They've captured most of the move from $140 to $166, see limited near-term upside given consolidation range, and prefer to lock in $30M profit rather than risk Q4 earnings binary event. Even if stock goes to $175 by February 20th, they're only leaving $9/share ($9M) on the table while protecting $30M already secured.

Why 50% probability: Stock at technical equilibrium - neither breaking out nor breaking down. Fundamentals solid (32% revenue growth, 18% FCF margins, AI leadership) but valuation rich (119x P/E). Most investors will hold through earnings but not aggressively add. The $165-175 range provides attractive risk/reward for consolidation.

📉 Bear Case (20% probability)

Target: $145-$160 (PULLBACK TO IMPLIED MOVE FLOOR)

What could go wrong:

- 😰 Q4 earnings disappoint with revenue below $3.5B or weak guidance for Q1 - even small miss triggers severe reaction at 119x P/E

- 🚨 System degradation issues during BFCM raise reliability concerns - customers mention switching to alternatives

- ⏰ Agentic Storefronts adoption slower than hoped - platform policy changes from OpenAI/others disrupt integration

- 🇨🇳 International expansion hits regulatory roadblocks in Europe (payment processing compliance delays)

- 💸 Broader tech selloff drags software stocks lower (SaaS multiple compression if rates rise)

- 📊 Competitive pressure: Amazon Buy with Prime gains traction, WooCommerce (39% market share) wins entry-level merchants

- 🤖 Margin compression from AI infrastructure investment without immediate revenue payoff

- 💰 Valuation reset: Market reprices SHOP from 119x to 80-90x P/E on growth deceleration concerns

- 🔨 Break below $165 gamma support triggers cascade to $160, then $155

Critical support levels:

- 🛡️ $165: Immediate floor (4.9B gamma) - MUST HOLD or momentum shifts bearish

- 🛡️ $160: Major psychological level (3.7B gamma) + round number support

- 🛡️ $145-155: Implied move lower range + February OPEX positioning

Why only 20% probability: Shopify's fundamentals remain STRONG (record BFCM, Q3 beat, AI first-mover advantage, 73% of top DTC brands). Execution risk exists but management track record solid (9 consecutive quarters of double-digit FCF margins). Regulatory risks real but manageable for company with compliance expertise across 30+ jurisdictions. Valuation stretched but can sustain if growth continues.

If this scenario plays out: The call seller looks BRILLIANT - they exited at $166 with $30M profit, avoiding a 10-15% drawdown to $145-150. Meanwhile, February $140 call buyers who purchased this position would see their $30.10 calls drop to $5-10 intrinsic value only = massive loss.

💡 Trading Ideas

🛡️ Conservative: Cash Gang with Watchlist

Play: Stay on sidelines until February 18th earnings clarity, then reassess

Why this works:

- ⏰ Earnings in 50 days creates binary event risk - options market pricing ±12.5% move ($21)

- 💸 Implied volatility elevated pre-earnings - options EXPENSIVE right now

- 📊 Stock in tight $165-175 consolidation range - limited upside before catalyst

- 🎯 Better entry likely post-earnings after IV crush reduces premiums significantly

- 📉 The $30M institutional call exit signals smart money taking profits at peak - follow the smart money!

- 🤔 At 119x P/E with 57% YTD gains already captured, risk/reward NOT favorable for new aggressive positioning

Action plan:

- 👀 Watch Q4 earnings February 18th closely for: revenue (need $3.6B+), GMV growth (maintain 30%+), margins (54-55%), Agentic Storefront metrics, international expansion progress

- 🎯 Look for pullback to $155-160 support post-earnings for stock entry with 8-10% margin of safety

- ✅ Need to see Tinker app monetization details and Shop Pay international expansion milestones before committing capital

- 📊 Monitor unusual options activity - if institutions add MORE selling/profit-taking, stay cautious

- ⏰ Revisit in Q2 2026 after Tinker launch and international Shop Pay data provides visibility

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 10-15% drawdown if earnings disappoint or guidance conservative. Preserve capital for better risk/reward entry. Let smart money's $30M profit-taking signal guide patience.

⚖️ Balanced: Post-Earnings Put Spread (Protect Against Pullback)

Play: After earnings volatility settles, structure bearish put spread betting on consolidation

Structure: Buy $165 puts, Sell $155 puts (February 20 expiration - SAME as this trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads MUCH cheaper - buy AFTER volatility drops 30-40%

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $160-165 where options activity concentrated

- 🤝 Essentially betting on "sell the news" consolidation after earnings event passes

- ⏰ February 20 expiration gives 2 days post-earnings for any negative momentum to develop

- 🛡️ Protects against valuation compression if growth trajectory shows any deceleration

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$3-4 net debit per spread post-earnings (vs $5-6 now)

- 📈 Max profit: $600-700 if SHOP below $155 at February 20 expiration (unlikely but protected)

- 📉 Max loss: $300-400 if SHOP above $165 (defined and limited)

- 🎯 Breakeven: ~$161-162

- 📊 Risk/Reward: ~1.5:1 to 2:1 which is attractive for defined-risk bearish play

Entry timing:

- ⏰ Wait 1-2 days post-earnings (by Feb 19-20) for IV collapse - don't fight elevated volatility

- 🎯 Only enter if stock trades $168-175 post-earnings (gives spread room to work)

- ❌ Skip if stock already below $162 (too close to strikes, poor risk/reward)

Position sizing: Risk only 2-3% of portfolio (this is tactical play, not core conviction)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

Expected outcome: Modest profit if SHOP consolidates $155-165 range in the two days between earnings and expiration. Worst case lose $300-400 per spread if stock stays strong above $165. This is a SHORT-TERM tactical play on post-earnings positioning.

🚀 Aggressive: Long Stock with Tight Stop (Ride the Momentum - RISKY!)

Play: Buy SHOP stock at current levels betting on earnings beat and continued rally

Structure: Buy shares at $166-168, set HARD STOP at $162.50 (below $165 gamma support)

Why this could work:

- 💥 Record BFCM at $14.6B (+27%) provides HIGH visibility into Q4 strength

- 🤖 Agentic Storefronts represent genuine AI-commerce innovation (first-mover advantage vs competition)

- 📊 Analyst price targets $190-198 suggest 15-20% upside potential if execution delivers

- 🚀 Gamma resistance at $170-175 could BREAK on strong earnings, triggering momentum to $185-195

- ⚡ Quarterly revenue growth accelerating (32% Q3) while maintaining 18% FCF margins = rare combination

- 📈 73% of top 800 DTC brands use Shopify - dominant positioning with network effects

Why this could blow up (SERIOUS RISKS):

- 💸 VALUATION STRETCHED: 119x P/E with zero margin for error - any guidance disappointment = -15-20% gap

- ⏰ BINARY EARNINGS RISK: February 18 earnings could gap stock $15-20 either direction overnight

- 😱 SMART MONEY EXITING: The $30M call sale signals institutions TAKING PROFITS, not adding - why fight the tape?

- 📊 CONSOLIDATION PATTERN: Stock stuck $165-175 for weeks - momentum has STALLED

- 🎢 Competition: Amazon Buy with Prime (8-18% revenue risk), WooCommerce (39% market share) eroding low-end

- ⚠️ Regulatory complexity: Operating across 30+ jurisdictions with payment/data compliance creates execution risk

- 💰 Already up 57% YTD: Much of the "easy money" already made - late entries often get trapped

Estimated P&L:

- 💰 Cost: $166-168 per share

- 📈 Target: $185-190 (10-14% gain) if earnings beat drives breakout = $18-22/share profit

- 🚀 Home run: $200+ (20% gain) if AI momentum accelerates = $32-34/share profit

- 📉 Stop loss: $162.50 (2-3% loss) = -$3.50-5.50/share loss if support breaks

- 💀 Disaster: Gap down to $150 on earnings miss = -$16-18/share loss (IF you don't respect stop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can handle 2-3% loss if stopped out (and WILL respect the stop discipline!)

- ✅ Understand this is HIGH-RISK momentum trade AGAINST institutional selling signal

- ✅ Accept that earnings binary event could gap you out below your stop (slippage risk)

- ✅ Have experience trading through earnings volatility

- ✅ Won't panic sell if stock whipsaws $10-15 intraday around earnings

- ⏰ Plan to take partial profits at $175-180 (50% position) to reduce risk

Position sizing: Maximum 5-8% of portfolio (this is SPECULATION, not investment!)

Risk level: HIGH (earnings binary event + valuation risk) | Skill level: Advanced only

Probability of profit: ~35-40% (fighting institutional selling + elevated valuation + binary event risk)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in 50 days: Results February 18th before market open create MASSIVE volatility risk. Stock could gap 10-15% either direction based on revenue ($3.5B vs $3.7B makes huge difference), margin performance (54% vs 52% changes narrative), and Agentic Storefront adoption metrics. Holiday quarter is make-or-break for annual performance. Options pricing ±12.5% implied move but actual moves could be larger given tight consolidation before earnings.

-

💸 Valuation at extreme levels: Trading at 119-125x forward P/E and 155x trailing P/E near all-time highs after 57% YTD gain. This is STRETCHED - stock priced for perfect execution of AI-commerce thesis. Simply Wall St estimates fair PE of ~50x based on growth outlook, suggesting 60-70% premium to fair value. Requires 40% of revenue from AI/new initiatives by 2027 to justify current multiple. Any disappointment magnified 3-4x at this valuation.

-

🤖 Agentic Storefronts execution risk: Revolutionary ChatGPT/Perplexity integration requires seamless operation with rapidly evolving AI platforms. Any platform policy changes (OpenAI changes commerce terms, Perplexity pivots strategy) could disrupt overnight. Adoption takes time - merchants need to integrate, test, optimize. Too early to know if this drives material revenue or just marketing buzz. Competitive risk if Amazon/others copy the approach.

-

🇨🇳 International expansion complexity: Shop Pay Installments rollout to UK, Europe, Australia requires regulatory compliance across multiple jurisdictions. Payment processing regulations complex and country-specific. GDPR, payment card network rules, anti-money laundering requirements create ongoing compliance burden. Any regulatory delays or fines could slow international GMV growth (currently 41% YoY but volatile).

-

⚖️ Amazon Buy with Prime competitive threat: Despite 2023 partnership allowing integration, Amazon's fulfillment capabilities and Prime customer base (200M+ members) remain structural competitive advantage. UBS estimates 8-18% of Shopify revenue potentially at risk if Amazon aggressively pushes Buy with Prime. Merchants may choose Amazon's ecosystem for better conversion rates despite losing customer data control.

-

🏪 WooCommerce market share threat: WooCommerce holds 33-39% global market share vs Shopify's 14.5-26.2%, driven by free/open-source model and WordPress integration. While Shopify dominates high-revenue merchants (73% of top DTC brands), WooCommerce erodes entry-level merchant base. Commoditization risk if platform switching costs decrease.

-

🛠️ BFCM system degradation incident: Brief "system degradation" during most critical weekend of the year highlights infrastructure scalability challenges. While resolved quickly, any future outages during peak periods would be CATASTROPHIC for merchant trust. At scale ($14.6B GMV in 4 days = $152M/hour), even 15-minute outage costs millions. Technical reliability is table stakes.

-

💰 Smart money exiting at peak: The $30M institutional call sale signals sophisticated players LOCKING IN GAINS rather than staying fully long into earnings. When funds managing hundreds of millions choose to exit $26-deep ITM calls with 52 days remaining, it's a caution flag. They're saying "we've made our money ($100%+ gain likely), time to derisk." Why fight the institutional flow?

-

📊 Insider selling activity: Recent insider sales include Kasra Nejatian selling 80,645 shares near $153, Harley Finkelstein multiple small sales at $150-156. While some selling is normal for equity compensation, concentration at current levels suggests executives see limited near-term upside or prefer to diversify.

-

🎢 Macro headwinds if consumer spending weakens: E-commerce growth tied directly to consumer discretionary spending. If recession emerges in 2026 or consumer confidence drops, merchant GMV suffers immediately. At 119x P/E, SHOP has ZERO recession protection. Small/medium business merchants are first to cut costs in downturn. Enterprise/B2B segment (101% growth) could slow if corporate IT budgets tighten.

-

💵 Currency volatility: Operating globally with Europe at 21% of revenue creates FX exposure. BFCM constant-currency growth of 24% vs 27% nominal shows currency headwinds can mask underlying strength or weakness. If USD strengthens significantly, reported revenue growth could disappoint even with strong underlying business performance.

🎯 The Bottom Line

Real talk: Someone just cashed out $30 MILLION in winning call options 50 days before Shopify's most important earnings report of the year. This isn't bearish on SHOP's long-term AI-commerce revolution story - it's smart profit-taking by institutions who've captured the 57% YTD rally from $105 to $180 and don't want to risk giving it back on a binary earnings event.

What this trade tells us:

- 🎯 Sophisticated player LOCKING IN 100%+ gains after riding Summer→Fall rally ($130-140 entry to $166 exit)

- 💰 They prefer $30.1M cash TODAY over risking earnings volatility for potentially $35-40M in 52 days

- ⚖️ The timing (50 days pre-earnings, 2 days post-expiration) shows they're letting someone else handle earnings risk

- 📊 Selling deep ITM calls ($140 strike, $26 intrinsic value) rather than exercising captures extra $4.10/share time value

- ⏰ February 20 expiration is just 2 days AFTER February 18 earnings - intentional positioning to collect max premium while avoiding earnings directly

This is a "take profits at the peak" signal, NOT a "sell everything" panic signal.

If you own SHOP:

- ✅ Consider trimming 20-30% at $165-170 levels if you're up significantly (lock in gains, reduce risk)

- 📊 If holding through earnings, set MENTAL STOP at $162.50 (below $165 gamma support) to protect capital

- ⏰ You've already won big if you own from $120-140 levels - protecting profits is SMART, not scared

- 🎯 If earnings beat AND stock breaks $175-180, could re-add trimmed shares on momentum

- 🛡️ Consider buying 1-2 protective puts per 100 shares if holding large position (insurance costs 2-3% but protects 10-15% downside)

If you're watching from sidelines:

- ⏰ February 18th before market open is the moment of truth - DO NOT enter before earnings!

- 🎯 Post-earnings pullback to $155-165 would be EXCELLENT entry (8-10% off highs with gamma support)

- 📈 Looking for confirmation of: BFCM translating to Q4 revenue, Agentic Storefront adoption metrics, Shop Pay 70%+ penetration, international acceleration

- 🚀 Longer-term (6-12 months), Agentic Storefronts execution, Tinker app monetization, and Shop Pay international expansion are legitimate catalysts for $190-200+ if execution delivers

- ⚠️ Current valuation (119x forward P/E) requires near-perfect execution - one stumble and it's back to $145-155

If you're considering bearish positions:

- 🎯 Wait for earnings before initiating - fighting 57% YTD momentum is dangerous

- 📊 Key support at $165 (gamma floor), major support at $160 (structural level)

- ⚠️ Post-earnings put spreads offer defined-risk way to play consolidation after IV crush

- 📉 Watch for break below $165 - that's the trigger for potential cascade to $155-160

- ⏰ Timing matters: Premature bearish bets risk getting run over; post-earnings offers better risk/reward

Mark your calendar - Key dates:

- 📅 February 18, 2026 (Tuesday) before market open - Q4 FY2025 earnings report (50 DAYS!)

- 📅 February 20, 2026 - Monthly OPEX, expiration of this $30M call trade

- 📅 Early 2026 (Jan-Feb) - Tinker app launch expected

- 📅 March 24-26, 2026 - Shoptalk 2026 conference (potential announcements)

- 📅 H1 2026 - Shop Pay Installments UK/Europe rollout

- 📅 June 2026 - Shopify Functions launch (Scripts replacement)

Final verdict: Shopify's long-term AI-commerce story remains INCREDIBLY compelling - record BFCM at $14.6B, first-mover Agentic Storefronts, 73% DTC market dominance, 32% revenue growth with 18% FCF margins. BUT, at 119x P/E after 57% YTD gain with earnings in 50 days, the risk/reward is NO LONGER favorable for aggressive new positioning. The $30M institutional call sale is a CLEAR signal: smart money is locking in triple-digit gains at the peak.

Be patient. Let earnings clear. Look for better entry $155-165. The AI-commerce revolution will still be here in 2-3 months, and you'll sleep better paying $160 instead of $168.

Protect your capital. Follow the smart money. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 3.05 Z-score unusual classification reflects this trade's size relative to recent SHOP history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 10-15% gaps either direction. The call seller may have complex portfolio management needs not applicable to retail traders.

About Shopify Inc.: Shopify operates a cloud-based commerce platform serving small and medium-sized businesses globally. The company provides subscription solutions (online sales across multiple channels) and merchant solutions (payment processing, shipping, capital), with a market cap of $218.6 billion in the prepackaged software services industry.