$18.3M SMH Put Wall - Institutions Layering Bearish Protection Across Timeframes

January 29, 2026 | Unusual Activity Detected

The Quick Take

Smart money just loaded up on $18.3 MILLION in SMH puts across two distinct timeframes today -- $15.5M on January 2027 LEAP $370 puts and $2.8M on near-term February 13 $405 puts. This is a layered hedge structure: near-term ATM protection for the next 15 days PLUS long-term insurance nearly a full year out. With SMH up +69.3% YTD at $414.41 and the semiconductor sector facing a convergence of tariff escalation, AI capex uncertainty, and NVIDIA earnings risk on February 25, institutions are clearly paying up for downside protection. Translation: Someone managing a massive semiconductor portfolio just bought a multi-million dollar insurance policy at the exact moment the AI chip trade looks most crowded.

ETF Overview

VanEck Semiconductor ETF (SMH) is the premier semiconductor sector ETF tracking the MVIS US Listed Semiconductor 25 Index:

- Net Assets: $35.6 Billion

- Expense Ratio: 0.35%

- P/E Ratio (TTM): 42.62x

- Current Price: ~$414.41 (near all-time highs)

- Primary Exposure: NVIDIA (19.17%), TSMC (10.68%), Broadcom (7.59%), ASML (5.60%), Lam Research (5.48%), Micron (~5%), AMD (~4.5%)

Top Holdings Concentration: The top 5 holdings represent 48.5% of the fund -- meaning SMH is essentially a leveraged bet on NVIDIA, TSMC, and Broadcom with diversification around the edges. StockAnalysis - SMH Holdings

The Option Flow Breakdown

The Tape (January 29, 2026):

Trade 1 & 2: LEAP Puts (Jan 2027 $370 Strike)

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:09:50 | SMH | MID | BUY | PUT $370 | 2027-01-15 | $11M | $370 | 3,200 | 285 | 3,200 | $414.54 | $34.75 |

| 14:14:11 | SMH | ASK | BUY | PUT $370 | 2027-01-15 | $4.5M | $370 | 4,500 | 285 | 1,300 | $414.54 | $34.75 |

Trade 3 & 4: Near-Term Puts (Feb 13 $405 Strike)

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:56:45 | SMH | MID | BUY | PUT $405 | 2026-02-13 | $1.5M | $405 | 1,300 | 78 | 1,198 | $405.94 | $12.19 |

| 10:56:45 | SMH | MID | BUY | PUT $405 | 2026-02-13 | $1.3M | $405 | 2,300 | 78 | 1,039 | $405.94 | $12.18 |

What This Actually Means

This is a multi-timeframe bearish hedge on the semiconductor sector. Here is the full breakdown:

LEAP Component ($15.5M - Jan 2027 $370 Puts):

- $15.5M total premium ($34.75 per contract x 4,500 contracts)

- Protection strike at $370, which is 10.7% below current price

- 11.5 months to expiration -- gives nearly a full year of downside coverage

- Volume of 7,700 contracts vs open interest of just 285 = clearly opening new positions (27x OI!)

- 4,500 contracts = 450,000 shares of exposure worth ~$186M at current prices

- The second tranche hit the ASK (paid up for fills), signaling urgency

- This is NOT a short-term trade -- this is structural portfolio insurance

Near-Term Component ($2.8M - Feb 13 $405 Puts):

- $2.8M total premium ($12.18-12.19 per contract x 2,237 contracts)

- Struck at $405 -- essentially ATM when purchased (SMH was at $405.94)

- Only 15 days to expiration -- this is short-dated, aggressive protection

- Volume of 3,600 contracts vs open interest of just 78 = clearly opening (46x OI!)

- 2,237 contracts = 223,700 shares of exposure worth ~$91M at current prices

- Bought in the morning session, hours before the LEAP purchases -- suggesting the trader assessed near-term risk first, then added long-term protection

The Strategy: Layered Insurance

This trader is building a two-layer hedge. The near-term $405 puts protect against an immediate drawdown (think: NVIDIA earnings miss on Feb 25, tariff escalation, or broader tech weakness). The LEAP $370 puts provide insurance against a larger structural downturn in semiconductors over the next year -- covering tariff escalation deadlines, AI capex sustainability concerns, and potential multiple compression from current 42.6x P/E.

Combined exposure: $18.3M protecting approximately $277M in semiconductor holdings. That is a 6.6% insurance cost -- meaningful but not extreme for institutional risk management on a position this size.

Technical Setup / Chart Check-Up

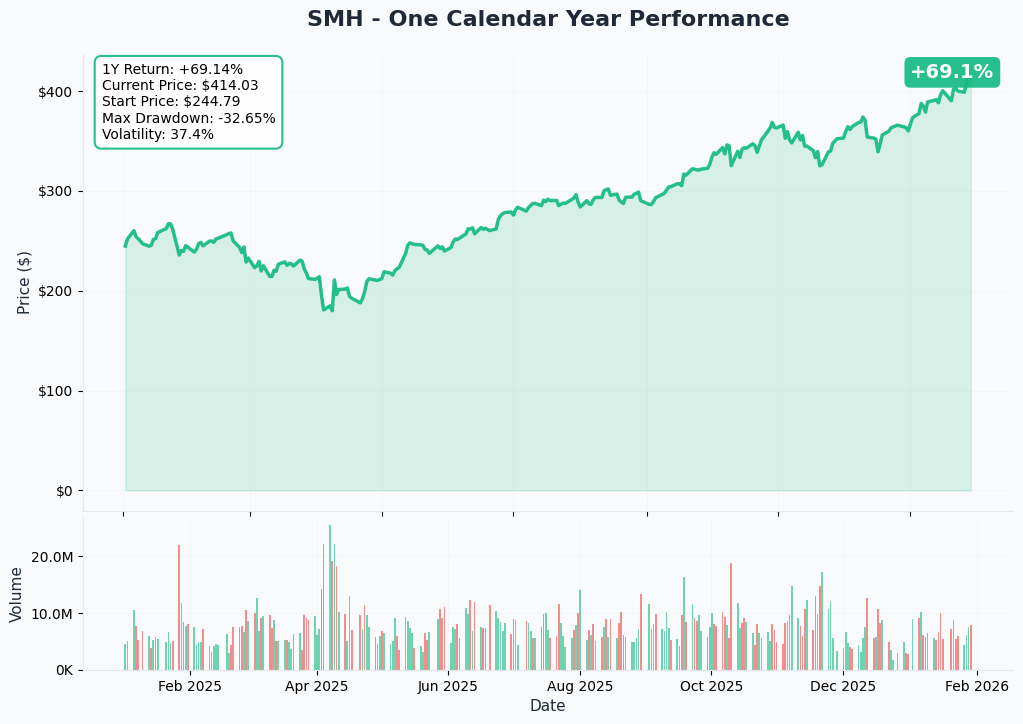

One Calendar Year Chart

SMH has been a monster -- up +69.3% YTD with the current price near $414.41 after touching all-time highs above $405 earlier this month. The ETF has been the primary vehicle for capturing the AI chip supercycle, with NVIDIA alone contributing roughly a third of returns.

Key observations:

- Relentless uptrend: Consistent higher highs and higher lows throughout 2025, accelerating into January 2026

- All-time highs: Price currently trading above the prior January 2026 high of ~$405.31

- Concentration risk: NVIDIA's 19.17% weighting means a single stock drives nearly 1/5 of performance

- Parabolic character: The acceleration from $300 to $414 in the past few months shows late-cycle momentum

- Volume profile: Strong institutional accumulation visible in ETF flows ($3.85B in 1-year net inflows)

- Overbought signals: Extended move from any reasonable moving average suggests mean-reversion risk

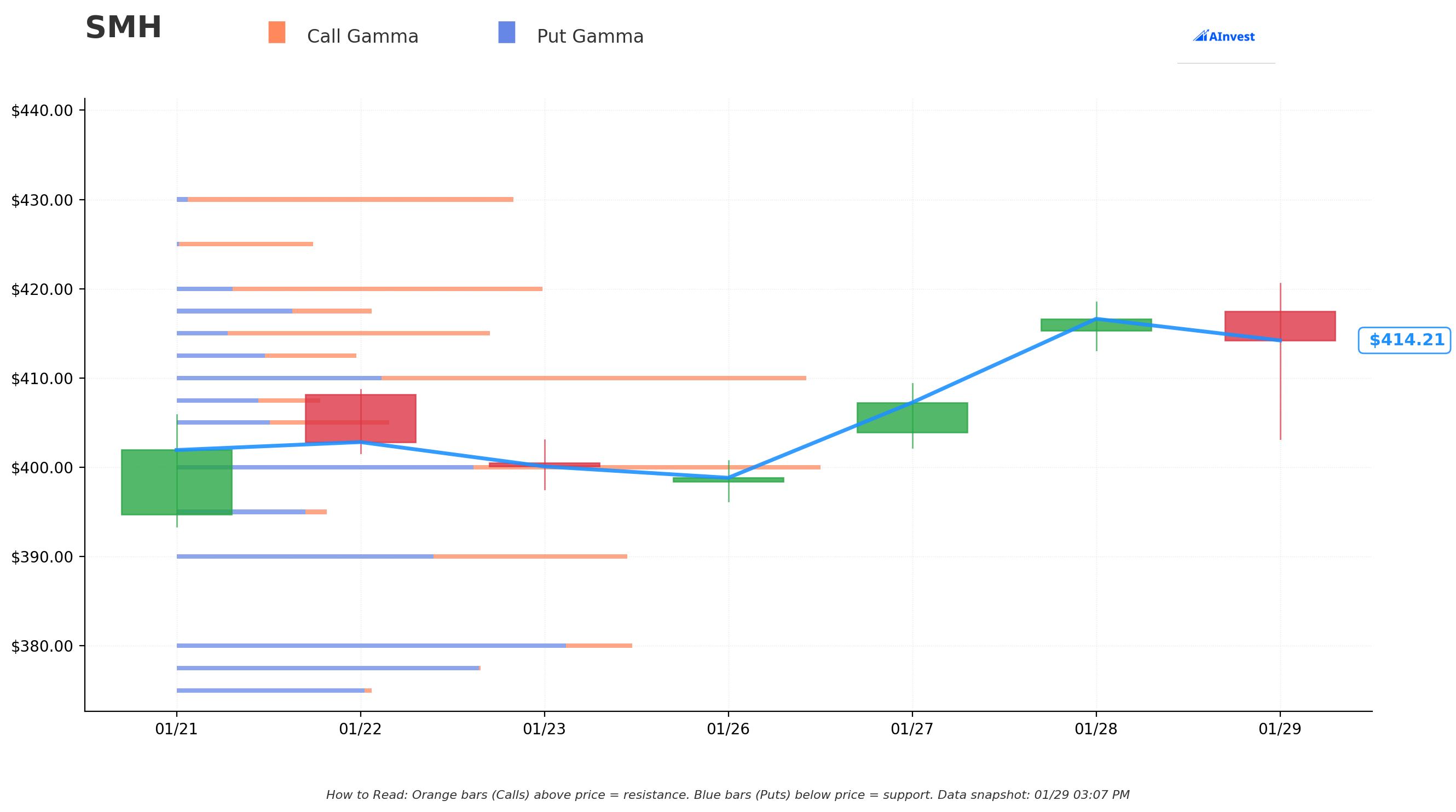

Gamma-Based Support & Resistance Analysis

Current Price: $414.44

The gamma exposure map reveals critical price magnets and barriers for near-term price action:

Support Levels (Below Price):

- $410 - First support. Mild gamma cushion from nearby put positions

- $405 - Major structural support. This is exactly where the near-term put buyer struck, and aligns with the prior breakout level. Heavy put gamma here acts as a floor

- $400 - Psychological round number with significant options positioning

- $390 - Secondary support zone with moderate gamma exposure

- $380 - Extended floor. Break below here shifts sentiment decisively bearish

- $377.50 - Deep support level with notable put positioning

- $370 - LEAP put strike level. This is where the $15.5M in LEAP puts are struck -- NOT a coincidence that it aligns with a key gamma support zone

Resistance Levels (Above Price):

- $415 - Immediate overhead ceiling. Market makers likely selling into rallies here

- $420 - Secondary resistance with call gamma creating mechanical selling

- $430 - Extended upside target requiring sustained buying pressure

What this means for traders: SMH is trading just below the $415 resistance level with declining momentum. The gamma structure shows a clear asymmetry -- support levels are stacked from $370 to $410, but resistance above is thin, meaning a breakout above $420 could accelerate higher, while a breakdown below $405 could cascade through multiple levels.

The $370 LEAP put strike EXACTLY matches a gamma support level. This is textbook institutional positioning -- the trader placed their long-term protection at a structural price floor where market maker hedging activity would create natural buying support. If $370 breaks, it means the gamma floor has failed and the move lower is likely to accelerate.

Net GEX Bias: Bearish -- more put gamma than call gamma at current levels suggests dealer hedging flows will amplify downside moves and dampen upside moves.

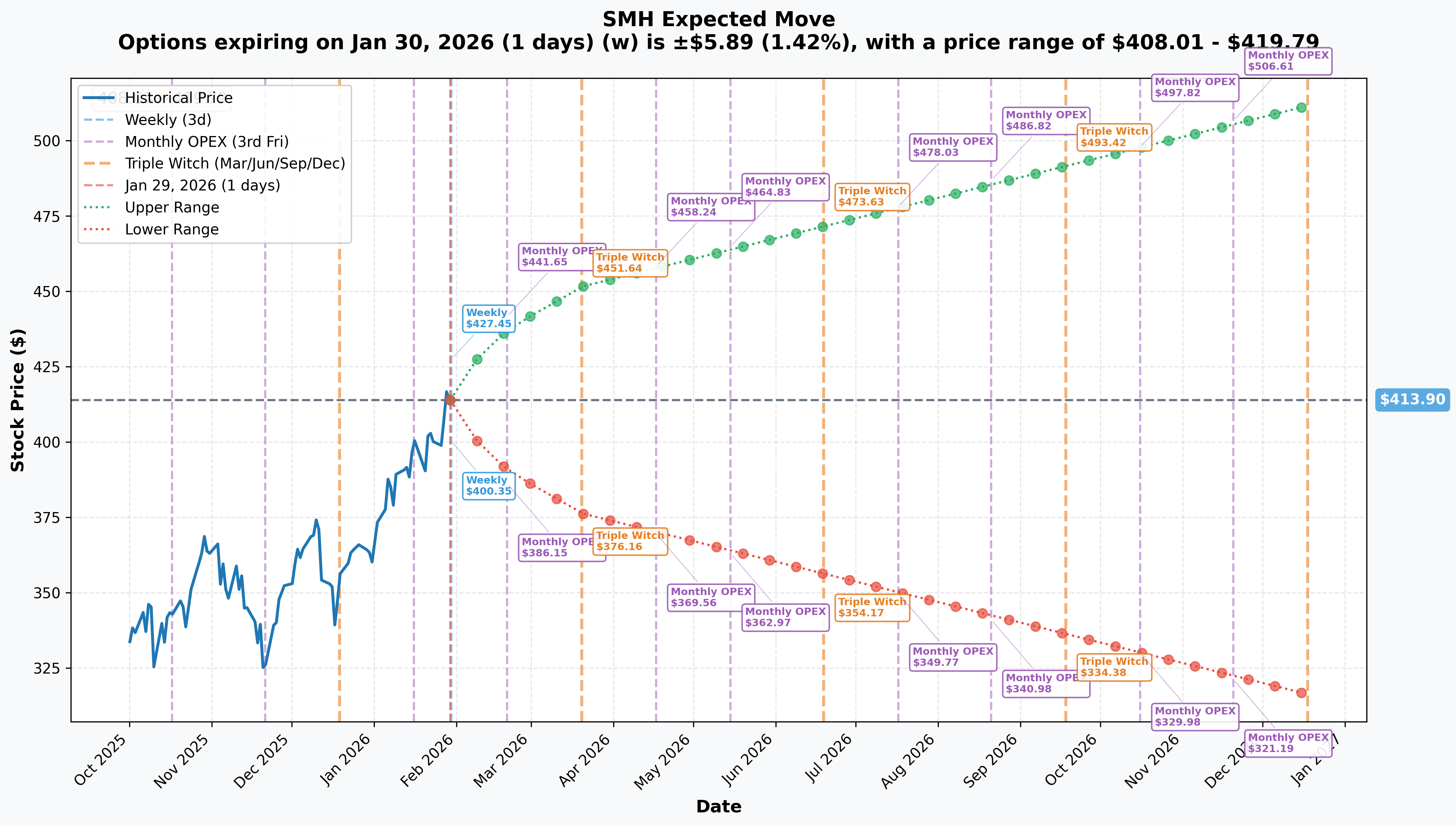

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 30 - 1 day): +/-$5.89 (+/-1.4%) -> Range: $408.01 - $419.79

- Monthly OPEX (Feb 20 - 22 days): +/-$23.76 (+/-5.7%) -> Range: $390.14 - $437.66

- Quarterly (Mar 20 - 50 days): +/-$37.74 (+/-9.1%) -> Range: $376.16 - $451.64

- Yearly LEAPs: +/-$97.77 (+/-23.6%) -> Range: $316.13 - $511.67

Translation for regular folks: The options market is pricing in modest daily movement (+/-1.4%), but a SIGNIFICANT +/-5.7% move through February OPEX. That monthly range of $390-$438 encompasses NVIDIA earnings on February 25 -- the single biggest event risk for semiconductors. The quarterly range extends down to $376, which is very close to the LEAP put strike of $370.

Looking at the LEAP horizon, the market thinks SMH could trade anywhere from $316 to $512 over the next year. That $316 lower bound represents a potential -24% drawdown from current levels -- confirming there is real institutional concern about extended downside in a risk-off scenario.

Key insight: The near-term $405 puts are positioned right at the lower end of the weekly implied range. The LEAP $370 puts sit just inside the quarterly implied move boundary ($376). This trader is NOT buying way-out-of-the-money lottery tickets -- they are buying puts within the market's expected range, which is sophisticated positioning.

Catalysts

Immediate Catalysts (Next 2 Weeks)

Apple (AAPL) Earnings - January 29, 2026 (TODAY)

Apple reports fiscal Q1 results today after the close. While Apple is not a top-10 SMH holding, iPhone chip demand signals from TSMC's largest customer provide read-through for the semiconductor supply chain. CNBC

Amazon + Alphabet Earnings - February 4-5, 2026

Two of the largest hyperscaler AI spenders report earnings next week. Their capex guidance updates will directly impact sentiment on AI chip demand:

- Amazon Web Services (AWS) cloud growth trajectory and AI infrastructure spending plans

- Alphabet's AI capex direction following its $900B tensor processing unit (TPU) project -- which threatens NVIDIA's dominance Motley Fool

Feb 13 Expiration -- Near-Term Put Deadline

The $2.8M in near-term $405 puts expire February 13 -- just 15 days away. This creates a natural decision point: if SMH is below $405 by then, the puts are in-the-money. If above, they expire worthless and the trader absorbs the $2.8M as insurance cost.

Critical Near-Term Catalyst

NVIDIA Q4 FY2026 Earnings - February 25, 2026

This is THE event for SMH. NVIDIA represents 19.17% of the ETF -- meaning a 10% NVIDIA move translates to roughly a 2% SMH move mechanically, with sentiment effects amplifying further. NVIDIA Earnings Date - StockTitan

What analysts expect:

- Revenue consensus: ~$44-46B (driven by Blackwell GPU ramp)

- Confirmation of Blackwell shipment schedule reaching full volume by end of April quarter

- Guidance on Rubin (R100) next-gen architecture timeline (late 2026 launch confirmed at CES)

- Impact of new 25% tariff and China H200 export licensing framework on margins

- Any commentary on customer demand durability vs. potential capex digestion period

TheStreet - NVIDIA Vera Rubin | Wall Street Horizon

Why this matters for the put buyer: The near-term $405 puts expire February 13 -- 12 days BEFORE NVIDIA earnings. This means the near-term puts are NOT designed to capture NVIDIA earnings. They are hedging against everything else: tariff noise, Microsoft cloud slowdown contagion, and general sector rotation risk. The LEAP $370 puts DO capture NVIDIA earnings and every subsequent catalyst for 11 months.

Major Macro Catalyst

Trump 25% Semiconductor Tariff (Enacted January 15, 2026)

President Trump signed a national security proclamation imposing a 25% tariff on advanced AI semiconductors (specifically targeting NVIDIA H200 and AMD MI325X chips) under Section 232 of the Trade Expansion Act. White House Proclamation | White House Fact Sheet

Key details:

- Effective January 15, 2026 -- already in force

- Exemptions for U.S. data centers, consumer uses, R&D, startups, and public sector

- Part of a deal allowing NVIDIA to sell H200 chips to China (capped at 50% of U.S. sales)

- White House explicitly signaled additional tariffs may follow

- 90-day negotiation deadline (mid-April) for broader deals with foreign chip producers

Impact on SMH holdings: NVIDIA designs in California but manufactures via TSMC in Taiwan. Every H100/H200/Blackwell chip is subject to tariff risk. With NVIDIA running 70% gross margins, a 25% cost increase cannot be fully absorbed without price hikes or margin compression. 24/7 Wall St

90-Day Tariff Escalation Deadline (Mid-April 2026)

U.S. Trade Representative Greer and Commerce Secretary Lutnick were directed to negotiate semiconductor trade agreements and report in 90 days. Trump stated he could impose "significant tariffs" beyond the initial 25% depending on negotiations. This creates persistent uncertainty for the entire sector through mid-April -- well within the LEAP put timeframe. White House

U.S.-Taiwan $250B Chip Investment Deal

Taiwan's semiconductor companies (led by TSMC) committed to investing $250B in U.S. chip production capacity in exchange for a tariff cap of 15% (down from the reciprocal 20%). However, most AI chips still come from Taiwan -- Arizona fabs are ramping but represent a fraction of total capacity. Nasdaq | Supply Chain Dive

U.S.-South Korea Tariff Tensions

Trump announced plans to raise tariffs on South Korean goods (including semiconductors) from 15% to 25%, triggering concerns about Samsung and SK Hynix memory supply. Micron (~5% of SMH) and other memory-exposed names face read-through risk. AInvest

Microsoft Cloud Slowdown Signal (January 28, 2026)

Microsoft plunged 12% yesterday after reporting slowing Azure cloud growth and issuing soft margin guidance. This is a direct read-through for AI chip demand -- cloud hyperscalers are the primary buyers of NVIDIA and AMD GPUs. If Azure growth decelerates, it raises questions about the sustainability of $527B in projected 2026 AI capex. CNBC

Counterpoint: Meta announced $115-135B in 2026 capex (nearly 2x 2025), reinforcing demand from the social media side. The AI capex story is not monolithic -- some hyperscalers may slow while others accelerate. CNBC - Meta Earnings

DeepSeek Efficiency Overhang

One year after DeepSeek's January 2025 shock (which wiped ~$1T from U.S. tech market cap in a single day), the "do more with less compute" thesis remains a lingering concern. The original shock saw NVIDIA -17%, Broadcom -17%, Marvell -19%. Wedbush's Dan Ives warns "more shocks are coming" from upcoming DeepSeek model releases. CNBC | Morningstar

TSMC Q4 2025 Blowout (January 15 -- Already Reported)

TSMC reported revenue of $33.7B (+20.5% YoY), net income of $16.3B (+35% YoY), and guided 2026 capex to $52-56B (+27-37% vs 2025). This initially lifted semiconductor stocks broadly, with AMD +2%, Broadcom +1%, Micron +5%. However, the rally has stalled as tariff and macro concerns weighed on sentiment. CNBC

AI Capex Spending Cycle

Goldman Sachs projects global AI-related data center capex of $527B in 2026. Inference workloads expected to account for 2/3 of total AI compute by 2026 (up from 1/3 in 2023), creating durable, non-episodic demand. However, yesterday's Microsoft miss calls the sustainability of this projection into question. Motley Fool | Nasdaq

Global Semiconductor Market Approaching $1 Trillion

The World Semiconductor Trade Statistics (WSTS) autumn forecast projects global semiconductor revenue of $975.4B in 2026 (+26.3% YoY), nearing the historic $1 trillion mark. Bitget

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the LEAP put expiration (January 15, 2027):

Bull Case (25% probability)

Target: $450-$510

How we get there:

- NVIDIA Q4 earnings crush expectations with $46B+ revenue and strong Blackwell ramp commentary

- Tariff negotiations resolve favorably by mid-April with reduced or eliminated semiconductor tariffs

- AI capex continues accelerating -- Amazon and Alphabet guide higher in February earnings

- Global semiconductor market hits $1T milestone, lifting all boats

- SMH top-10 holdings deliver on 126.8% expected earnings growth through 2027 Seeking Alpha

- NVIDIA Rubin architecture launch in late 2026 creates next upgrade cycle catalyst

- No further DeepSeek-type efficiency shocks

Key metrics needed:

- NVIDIA revenue growth sustaining 40%+ YoY

- Hyperscaler capex guidance continues increasing

- Tariff resolution removes 25% cost overhang

- P/E multiple sustained at 40x+ on earnings growth

Probability assessment: Only 25% because it requires everything to go right -- tariffs resolved, AI capex accelerating, no efficiency shocks, and NVIDIA executing flawlessly. The 42.6x P/E leaves zero margin for error.

Put P&L: Both the near-term and LEAP puts expire worthless. Total loss = $18.3M (100% of premium). This is the "insurance cost" the buyer willingly accepts.

Base Case (50% probability)

Target: $370-$430 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- NVIDIA earnings meet consensus but guidance is cautious due to tariff uncertainty

- Tariff negotiations drag on past mid-April deadline without clear resolution

- Mixed hyperscaler signals: some accelerate capex (Meta), others slow (Microsoft)

- SMH trades in a wide range as bulls and bears battle over AI capex sustainability

- P/E compresses from 42.6x toward 30-35x as earnings catch up to price

- Periodic selloffs on tariff headlines followed by recoveries on strong earnings

- Sector rotation between AI winners and losers creates choppy price action

This is the put buyer's expected scenario: The near-term $405 puts may pay off modestly if SMH dips in the next 15 days. The LEAP $370 puts serve as insurance that may or may not be needed, but provide peace of mind through a year of uncertainty. If SMH consolidates around $400-420, the LEAPs lose time value but still provide a floor.

Why 50% probability: The bull and bear cases both require extreme outcomes. The most likely path is messy consolidation as the market digests 69% YTD gains, processes tariff uncertainty, and waits for AI capex commitments to flow through to actual semiconductor revenue.

Bear Case (25% probability)

Target: $300-$370 (SIGNIFICANT CORRECTION)

What could go wrong:

- NVIDIA misses on Q4 earnings or guides below consensus, triggering sector-wide selloff (19.17% weight = outsized impact)

- Tariff escalation beyond 25% at mid-April deadline -- broader semiconductor tariffs enacted

- Azure cloud slowdown spreads to AWS and Google Cloud, signaling AI capex pullback across hyperscalers

- DeepSeek releases new model demonstrating further efficiency gains, repricing compute demand lower

- Taiwan geopolitical tensions escalate, threatening TSMC supply chain (Taiwan produces ~44% of advanced chips) Motley Fool

- P/E multiple compression from 42.6x to 25x as growth expectations reset

- Broader macro recession fears drive risk-off rotation out of expensive growth sectors

Critical support levels:

- $405: Near-term put strike / prior breakout level. First line of defense

- $390: Secondary support. Break below signals trend reversal

- $370: LEAP put strike / gamma support level. Major structural floor

- $340: Extended bear target if multiple negative catalysts converge

- $300: Disaster scenario -- requires sustained tariff escalation + AI capex collapse

Put P&L in Bear Case:

- SMH at $370 on Jan 2027 expiry: LEAP puts at breakeven, near-term puts already expired

- SMH at $340 on Jan 2027 expiry: LEAP puts worth $30.00, profit = -$4.75/share x 4,500 = net loss of $2.1M (but offset $13.4M of portfolio losses)

- SMH at $300 on Jan 2027 expiry: LEAP puts worth $70.00, profit = $35.25/share x 4,500 = $15.9M gain (102% ROI on LEAPs alone)

- Near-term puts at $395 on Feb 13: Puts worth $10.00, profit = -$2.19/share x 2,237 = net loss of $490K (but offset $42K per $1 in portfolio losses)

Trading Ideas

Conservative: Wait for NVIDIA Earnings Clarity

Play: Stay on sidelines until after February 25th NVIDIA earnings settle

Why this works:

- NVIDIA is 19.17% of SMH -- its earnings report will determine sector direction for weeks

- Microsoft's -12% crash yesterday shows the market is punishing even slight disappointments at premium valuations

- Implied volatility elevated heading into NVIDIA earnings -- options are expensive right now

- The $18.3M institutional put buy signals sophisticated players are concerned about near-term risk

- SMH is up 69% YTD at 42.6x P/E -- all the good news is priced in at these levels

- Better entry points likely after NVIDIA earnings volatility and tariff noise create pullbacks

Action plan:

- Watch Amazon/Alphabet earnings Feb 4-5 for AI capex signals

- Monitor NVIDIA closely on February 25 for revenue ($44-46B target), Blackwell commentary, and tariff impact

- If NVIDIA beats and SMH breaks above $430, consider buying the breakout with tight stops

- If NVIDIA disappoints, look for entry at $390-400 gamma support with 5-10% margin of safety

- Track tariff negotiation headlines through mid-April deadline

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 5-10% drawdown if NVIDIA disappoints or tariffs escalate. Preserve capital for better risk/reward entry.

Balanced: Put Spread Targeting NVIDIA Earnings (Copy The Pros)

Play: Buy a put spread on SMH expiring in March to capture NVIDIA earnings risk and tariff deadline

Structure: Buy March 20 $405 puts, Sell March 20 $380 puts ($25-wide spread)

Why this works:

- Captures both NVIDIA earnings (Feb 25) and tariff escalation risk through mid-March

- Defined risk structure limits maximum loss to the net debit paid

- $405 strike mirrors the institutional near-term positioning (they bought Feb $405 puts)

- $380 short strike aligns with gamma support zone, providing natural floor

- March expiration gives 50 days of coverage vs the institutional trader's 15-day near-term window

- Spread structure reduces cost compared to outright put purchases

Estimated P&L:

- Pay ~$8-10 net debit per spread (adjust based on current pricing)

- Max profit: $15-17 if SMH below $380 at March expiration

- Max loss: $8-10 (net debit paid) if SMH above $405

- Breakeven: ~$395-397

- Risk/Reward: ~1.5:1 to 1.7:1

Entry timing:

- Enter in the first week of February after Amazon/Alphabet earnings provide capex clarity

- If both report strong AI spending, skip this trade (bullish signal outweighs)

- If either reports softer capex guidance, the put spread thesis strengthens significantly

Position sizing: Risk only 2-5% of portfolio. This is a defined-risk directional trade, not a core position.

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Aggressive: LEAP Put Calendar (Longer-Term Structural Hedge)

Play: Buy January 2027 $370 puts on SMH, partially financing by selling March $370 puts

Structure: Buy Jan 2027 $370 puts, Sell March 20 $370 puts (diagonal put calendar)

Why this could work:

- This is a cheaper way to replicate the institutional LEAP put position

- Selling the short-dated $370 put collects premium to reduce the cost of the LEAP put

- The short March put is far OTM ($370 vs $414 current = 10.7% OTM) with only 50 days, so likely expires worthless

- Net cost reduced to approximately $28-30 per spread (vs $34.75 for outright LEAP)

- Provides 11.5 months of downside protection at a structural support/gamma level

- If semiconductors correct 15-20% on tariff escalation or AI capex slowdown, the LEAP puts could double

Why this could fail:

- SMH continues grinding higher and the LEAP puts lose all time value

- Theta decay is relentless on 11.5-month puts -- loses ~$0.10-0.15 per day

- Requires a sustained move below $370 to generate meaningful profit

- The short March put creates assignment risk if SMH crashes quickly (but this is a low probability at $370)

- At $28-30 per spread, still an expensive trade ($2,800-3,000 per calendar)

- Need SMH below $340 at January 2027 expiration for 100%+ return

Estimated P&L:

- Net cost: ~$28-30 per calendar spread

- Breakeven at LEAP expiry: ~$340-342

- If SMH at $300 in Jan 2027: LEAP worth $70, profit = ~$40 per spread (133% ROI)

- If SMH at $370 in Jan 2027: LEAP worth ~$5-8 (time value), loss = ~$22-25 per spread

- If SMH at $430 in Jan 2027: Both legs expire worthless, loss = full $28-30 premium

IMPORTANT: This is an advanced strategy requiring:

- Familiarity with calendar spread mechanics and Greek exposure

- Ability to manage the short leg if it approaches in-the-money

- Willingness to hold a position for 11+ months

- Capital you can afford to lose entirely

Risk level: HIGH (can lose 100% of premium, complex structure) | Skill level: Advanced only

Risk Factors

Do not ignore these potential landmines:

-

NVIDIA concentration creates single-stock risk: At 19.17% of SMH, NVIDIA earnings on February 25 is effectively a binary event for the entire ETF. A 15% NVIDIA move translates to ~3% SMH move mechanically, with sentiment amplification potentially doubling that. Buying SMH is NOT diversified semiconductor exposure -- it is a leveraged NVIDIA bet with a side of TSMC and Broadcom.

-

Tariff escalation is "phase one": The current 25% tariff on advanced AI chips is explicitly described as a first step. The White House threatened "significant" additional tariffs if negotiations fail by mid-April. NVIDIA cannot absorb 25% cost increases on 70% gross margins without price hikes or margin compression. Further escalation to 35-50% would fundamentally change the semiconductor cost structure. White House

-

Microsoft cloud slowdown signals potential AI capex peak: Yesterday's 12% Microsoft crash on slowing Azure growth raises serious questions about whether $527B in projected 2026 AI capex is sustainable. If the largest cloud provider is decelerating, GPU demand assumptions may be too optimistic. The LEAP put buyer may be positioning for exactly this scenario -- an AI capex cycle that peaks in 2026 rather than accelerating into 2027. CNBC

-

42.6x P/E leaves zero margin of safety: SMH trades at 42.6x trailing earnings after a 69% YTD rally. While forward P/E compresses to ~24x on 126.8% expected earnings growth, this requires flawless execution across ALL top holdings simultaneously. One major miss -- whether NVIDIA, TSMC, or Broadcom -- can trigger rapid multiple compression. At these levels, the stock market is paying for perfection and penalizing any imperfection. StockAnalysis - SMH

-

Taiwan geopolitical risk is structural and unhedgeable: Taiwan produces approximately 44% of advanced chips imported into the U.S. TSMC (10.68% of SMH) operates its leading-edge fabs exclusively in Taiwan despite the Arizona buildout. Any military escalation before 2027 could cut global chip supply by more than half. TSMC's $250B U.S. investment deal helps long-term but does not address near-term vulnerability. Motley Fool

-

DeepSeek efficiency thesis threatens demand growth: The January 2025 DeepSeek shock demonstrated that AI models can achieve comparable performance with significantly less compute. While no 2026 repeat has occurred, the thesis that "more efficient AI = fewer chips needed" remains a structural risk. Wedbush warns of further model releases that could reprice AI infrastructure demand assumptions. CNBC | Morningstar

-

$18.3M institutional put accumulation at all-time highs: When sophisticated institutions spend $18.3M on put protection at the peak of a 69% rally, it is a meaningful signal. The multi-timeframe structure (near-term + LEAP) shows this is not a quick tactical trade -- it is deliberate, layered risk management. Volume far exceeded open interest on BOTH strikes (27x OI on LEAPs, 46x OI on near-term), confirming these are entirely NEW positions.

-

Bearish GEX bias amplifies downside moves: The current negative gamma exposure bias means market makers are positioned to sell into declines (hedging their short put positions) rather than buy dips. This creates a self-reinforcing downside feedback loop during selloffs -- exactly the opposite of what bulls want to see.

-

South Korea tariff tensions add memory supply risk: Trump's plans to raise tariffs on South Korean goods from 15% to 25% threaten Samsung and SK Hynix -- critical suppliers of HBM memory chips needed for AI GPUs. Micron (~5% of SMH) and other memory-exposed names face pricing and supply disruption risk. AInvest

The Bottom Line

Real talk: Someone just spent $18.3 MILLION building a multi-layer put hedge on the semiconductor sector at its all-time highs. They bought near-term ATM puts for the next 15 days AND long-term LEAP puts for nearly a full year. This is NOT someone betting on a crash -- this is someone with a massive semiconductor portfolio buying insurance against a sector that has gotten too extended, too fast, with too many unresolved risks.

What this trade tells us:

- The multi-timeframe structure signals concern about BOTH near-term catalysts (NVIDIA earnings, tariff headlines) AND longer-term structural risks (AI capex sustainability, tariff escalation, DeepSeek efficiency)

- The near-term $405 puts were bought ATM at $405.94 -- this trader expects SMH could dip below $405 within 15 days

- The LEAP $370 puts align EXACTLY with a gamma support level -- institutional-grade strike selection

- Volume vs OI ratios (27x on LEAPs, 46x on near-term) confirm 100% of this flow is opening new positions

- The second LEAP tranche hit the ASK side, meaning the trader paid up for fills rather than waiting -- urgency signal

- Total exposure of $277M in notional protection suggests a fund managing $500M+ in semiconductor holdings

This is NOT a "sell everything" signal -- it is a "the risk/reward has shifted and smart money is adjusting" signal.

If you own SMH or semiconductor stocks:

- Consider trimming 20-30% at current levels to lock in gains from the 69% YTD run

- Set a mental stop at $405 (near-term put strike / prior breakout) -- if that level breaks, risk management becomes critical

- Do NOT add to positions ahead of NVIDIA earnings on February 25 -- wait for the event to pass

- If holding through February, consider buying 1-2 protective puts per 100 shares to hedge downside

- Monitor tariff headlines closely through mid-April deadline -- escalation beyond 25% would be bearish

If you are watching from the sidelines:

- Do NOT chase SMH at $414 after a 69% YTD rally at 42.6x P/E -- the risk/reward is unfavorable

- Wait for pullback to $390-400 (gamma support zone) for a better entry with 3-5% margin of safety

- NVIDIA earnings on February 25 will set the direction for the next 2-3 months -- let that catalyst clear

- Watch Amazon/Alphabet capex guidance (Feb 4-5) for early signals on AI spending trajectory

- If all hyperscalers confirm strong AI capex and NVIDIA beats, $430+ becomes achievable -- but wait for confirmation

If you are bearish:

- The institutional put buyer validated your thesis with $18.3M in capital

- Put spreads (March $405/$380 or $400/$370) offer defined-risk bearish exposure at reasonable cost

- The bearish GEX bias works in your favor -- downside moves will be amplified by dealer hedging

- First target is $405 (near-term put strike), then $390, then $370 (LEAP put strike / gamma floor)

- Do NOT short the ETF outright -- use defined-risk options to limit exposure to short squeezes

Mark your calendar -- Key dates:

- January 29 (TODAY) - Apple earnings (chip demand signal)

- February 4-5 - Amazon + Alphabet earnings (AI capex guidance)

- February 13 - Near-term $405 put expiration (decision point for this trade)

- February 20 - Monthly OPEX (+/-5.7% implied move window closes)

- February 25 - NVIDIA Q4 FY2026 earnings (THE catalyst for SMH)

- March 18-19 - FOMC meeting (rate decision)

- March 20 - Quarterly expiration (+/-9.1% implied move window)

- Mid-April - 90-day tariff negotiation deadline (broader tariffs possible)

- May-June - Intel Foundry updates (U.S. fab progress)

- Late 2026 - NVIDIA Rubin (R100) architecture launch

- January 15, 2027 - LEAP $370 put expiration

Final verdict: The semiconductor sector has delivered extraordinary returns driven by the AI infrastructure supercycle. But at 42.6x P/E with tariff uncertainty, a potential AI capex deceleration signal from Microsoft, and NVIDIA earnings in 27 days, the risk/reward has tilted toward caution. The $18.3M institutional put hedge is a clear signal that sophisticated money is protecting profits rather than adding risk at these levels.

The AI chip story is real. The semiconductor demand is real. But the price you pay matters -- and right now, you are paying all-time-high prices at peak enthusiasm with unresolved macro risks. Patience will be rewarded.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The unusual options activity discussed reflects specific trades by institutional investors whose portfolio context, risk tolerance, and hedging needs may differ entirely from yours. ETFs carry concentration risk -- SMH's top 5 holdings represent 48.5% of the fund. Tariff policies can change without warning. Always do your own research and consider consulting a licensed financial advisor before trading.

About VanEck Semiconductor ETF (SMH): SMH tracks the MVIS US Listed Semiconductor 25 Index, providing exposure to the 25 largest U.S.-listed semiconductor companies. Top holdings include NVIDIA (19.17%), TSMC (10.68%), Broadcom (7.59%), ASML (5.60%), and Lam Research (5.48%). Net assets of $35.6 billion, 0.35% expense ratio, 42.62x trailing P/E.