🔴 SMH Massive $68M Put Buy - Institutional Mega-Hedge on Semiconductors! 🛡️

📅 February 12, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $68 MILLION on a single put position in the semiconductor ETF! This isn't your average hedge - we're talking 42,000 contracts of $400 strike puts expiring March 20th. With SMH trading at $419.88 and NVIDIA earnings in 13 days, a sophisticated institution is paying serious premium to protect against downside risk in the AI chip trade. Translation: Big money is buying insurance against a potential semiconductor selloff!

📊 ETF Overview

VanEck Semiconductor ETF (SMH) is the premier semiconductor industry ETF, providing concentrated exposure to the AI chip supercycle:

- Current Price: $419.88 (near recent highs)

- AUM: ~$25 billion

- Industry: Semiconductor Equipment & Materials

- YTD Performance: +46.23% total return

- 52-Week Performance: +66.68%

Top 5 Holdings (74.4% of assets):

| Rank | Company | Ticker | Weight |

|---|---|---|---|

| 1 | NVIDIA | NVDA | 18.32% |

| 2 | Taiwan Semiconductor | TSM | 10.76% |

| 3 | Broadcom | AVGO | 7.14% |

| 4 | Micron Technology | MU | 6.40% |

| 5 | ASML Holding | ASML | 5.91% |

💰 The Option Flow Breakdown

📊 The Tape (February 12, 2026)

| Time | Symbol | Option Symbol | Side | Type | Expiration | Strike | Volume | Premium | OI Signal | Z-Score | Vol/OI | Strategy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 13:39:13 | SMH | SMH20260320P400 | BUY | PUT | 2026-03-20 | $400 | 42,000 | $68M | UNKNOWN | 0 | 10.0x | Single Leg PUT |

🤓 What This Actually Means

This is a massive institutional hedge or outright bearish bet! Here's what went down:

- 💸 Enormous premium paid: $68M for downside protection ($1,619 per contract average)

- 🎯 5% out-of-the-money: $400 strike with SMH at $419.88 = betting on 4.7%+ decline

- ⏰ 36 days to expiration: March 20th expiration captures NVIDIA earnings (Feb 25)

- 📊 Monster position size: 42,000 contracts = 4.2 million shares of exposure

- 🐋 Whale-scale trade: Definitely NOT your neighbor Bob's Robinhood account

- 🔥 HIGH ACTIVITY signal: Vol/OI ratio of 10.0x indicates heavy new positioning

What's really happening here:

This trade screams institutional hedging ahead of critical semiconductor catalysts. With NVIDIA reporting earnings on February 25th and Trump tariff uncertainty creating headline risk, someone with a massive long semiconductor portfolio is buying protection. At $68M, this is likely a pension fund, sovereign wealth fund, or mega-cap hedge fund protecting billions in semiconductor exposure.

Alternative interpretation: This could be an outright bearish bet from someone who believes the AI chip rally is overextended. After a 46% YTD run and semiconductors approaching 50% of industry revenue from AI alone, a correction to the $400 level would only be a 5% pullback - healthy consolidation rather than catastrophe.

📈 Technical Setup / Chart Check-Up

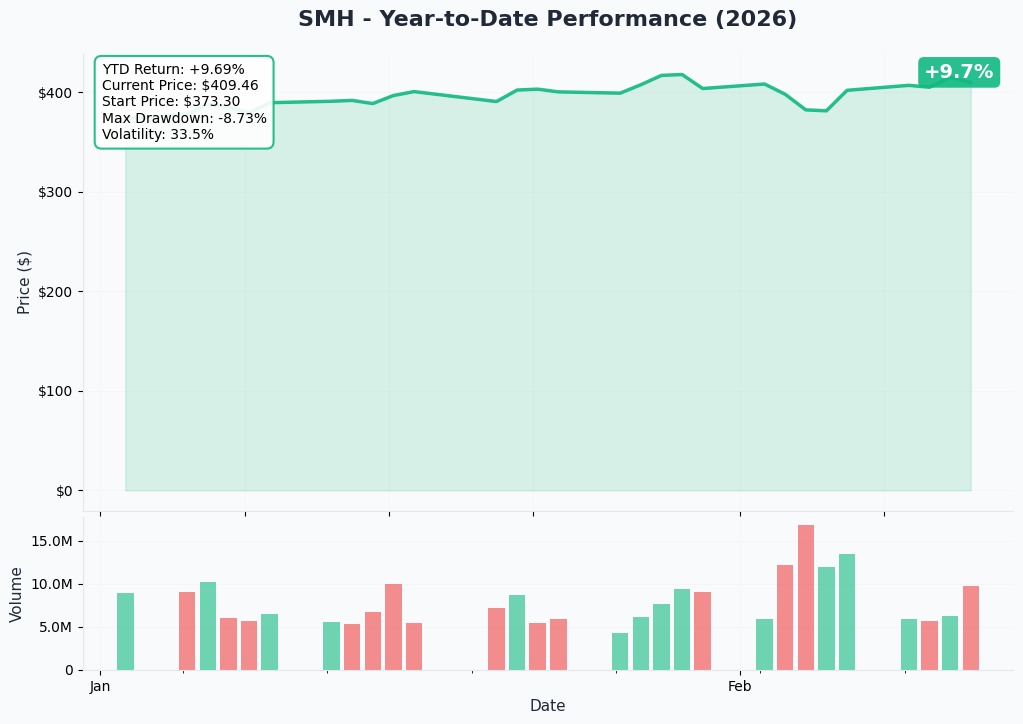

YTD Performance Chart

SMH has been on an absolute tear, rallying nearly 50% in 2025 alone driven by the AI infrastructure buildout and hyperscaler capital expenditure acceleration. The ETF is trading near the top of its recent range ($404.76 - $420.31 over the past week).

Key observations:

- 📈 Strong momentum: Consistent uptrend throughout 2025-2026

- 💹 Near resistance: Trading at $419.88, close to recent highs around $420

- 🎢 Elevated volatility: AI narrative creates significant intraday swings

- 📊 Volume expansion: Increased activity ahead of NVIDIA earnings

Note: Gamma and implied move charts are not available for this analysis.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 30 Days)

NVIDIA Q4 FY2026 Earnings - February 25, 2026 (13 DAYS AWAY!) 📊

This is THE event for semiconductors. NVIDIA represents 18.32% of SMH, making this single company's results the primary driver of near-term ETF performance.

- 📊 Consensus expects: Continued revenue acceleration following Q3's $57.0B record quarter

- 🚀 Key metrics to watch: Blackwell ramp trajectory, China H200 shipment volumes, data center revenue mix

- 🎯 Analyst targets: $250 median, $352 bull case (Evercore ISI)

- ⚠️ Risk factor: Any disappointment from the AI leader could drag the entire sector

HBM4 Mass Production Ramp - Q1-Q2 2026

Memory is the bottleneck for AI chips, and HBM4 production is ramping:

- 🏭 SK Hynix begins commercial HBM4 production in February 2026, four months ahead of schedule

- 📈 SK Hynix targeting 70% market share for NVIDIA Rubin platform

- 💰 Samsung and SK Hynix increased HBM3E prices by 20% for 2026 deliveries

Trump Tariff Policy Uncertainty

The wild card for semiconductors:

- 📉 25% tariff enacted on certain advanced chips including NVIDIA H200 and AMD MI325X

- ✅ Exemptions for US data centers, R&D, startups - Big Tech carve-outs expected

- ⚠️ Policy volatility creates headline risk and could trigger sudden moves

📅 Recent Catalysts (Past 3 Months)

NVIDIA Q3 FY2026 (October 2025) - CRUSHED IT 🚀

- 💰 Record $57.0B quarterly revenue, up 62% YoY

- 🎯 CEO Jensen Huang: "Blackwell sales are off the charts, and cloud GPUs are sold out"

- 🇨🇳 Chinese tech firms ordered 2M+ H200 GPUs for 2026 - potential $54B revenue

TSMC Record Performance (January 2026)

- 📈 January revenue NT$401.3B, up 36.8% YoY - highest monthly sales EVER

- 💹 Q4 gross margin hit record 62.3%, net profit margin 48.3%

- 🇺🇸 $100B additional US investment announced - total commitment now $165B

Broadcom AI Surge (Q1 FY2026)

- 🚀 AI semiconductor revenue surged 74% YoY

- 🎯 Q1 guidance: AI revenue to double YoY to $8.2B

- 📊 Projected 60% market share in AI Server ASIC design through 2027

🎲 Price Targets & Probabilities

📈 Bull Case (25% probability)

Target: $450-$475

How we get there:

- 💪 NVIDIA earnings crush expectations, guidance raised significantly

- 🇨🇳 China H200 shipments ramp faster than expected

- 🏭 HBM4 production solves memory bottleneck, AI capacity expands

- 📊 Semiconductor industry on track to hit $975B in 2026

- 🎯 Analyst consensus price target of $496.83 achieved

🎯 Base Case (50% probability)

Target: $400-$430 range

Most likely scenario:

- ✅ NVIDIA delivers solid quarter, guidance meets expectations

- 📱 AI chip demand remains strong but priced in

- ⚖️ Tariff exemptions limit damage, policy noise continues

- 🔄 ETF consolidates near current levels after massive YTD run

- 📊 93% of industry leaders expect growth - fundamentals intact but valuations stretched

This is likely why the trade was placed: The put buyer is protecting against normal consolidation after a 46% run, not betting on catastrophe. A pullback to $400 is only 4.7% downside - healthy profit-taking rather than crisis.

📉 Bear Case (25% probability)

Target: $360-$385

What could go wrong:

- 😰 NVIDIA earnings disappoint or guidance weak

- 🇨🇳 China-Taiwan tensions escalate - TSMC produces 90% of advanced chips

- 💰 Trump expands tariffs beyond current exemptions

- 📉 Intel foundry struggles weigh on sector sentiment

- 🎢 AI hype cycle peaks, rotation out of semiconductor names

- 💥 Potential economic impact: $10T global loss from full Taiwan conflict

In this scenario: The $68M put position pays off massively. $400 puts would be deep in-the-money with SMH at $360-$385.

💡 Trading Ideas

🛡️ Conservative: Mirror the Hedge (Sleep Well Strategy)

Play: Buy protective puts on existing semiconductor positions

Structure: Buy SMH $400 puts, March 20 expiration (same as the whale trade)

Why this works:

- 🛡️ Following smart money's playbook - if institutions are hedging, there's a reason

- ⏰ Captures NVIDIA earnings risk (Feb 25) - biggest near-term catalyst

- 📊 5% OTM strike provides cushion against normal volatility

- 💰 Cost: ~$1,600 per contract (protects 100 shares worth ~$42,000)

- 🎯 Think of it as portfolio insurance - pays off if things go wrong

Entry timing: Now or before NVIDIA earnings on February 25

Risk level: Low (defined risk) | Skill level: Beginner-friendly

⚖️ Balanced: Put Spread Hedge

Play: Buy a put spread to reduce cost of downside protection

Structure: Buy SMH $400 puts / Sell SMH $380 puts (March 20 expiration)

Why this works:

- 💸 Significantly cheaper than outright puts - $20 wide spread for ~$8-10 debit

- 🎯 Max profit if SMH drops to $380 or below

- 📊 Defined risk: Max loss limited to premium paid (~$800-$1,000 per spread)

- ⚖️ Protection through NVIDIA earnings without massive premium outlay

- 🏆 Sweet spot: Profitable if SMH drops 5-10% from current levels

Estimated P&L:

- 📈 Max profit: $2,000 per spread (if SMH below $380)

- 📉 Max loss: ~$800-$1,000 (premium paid)

- 🎯 Breakeven: ~$392

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Bearish Put Position (HIGH CONVICTION ONLY!)

Play: Outright put purchase betting on semiconductor pullback

Structure: Buy SMH $410 puts (March 20 expiration) - closer to the money for more delta

Why this could work:

- 📉 After 46% YTD run, mean reversion is overdue

- 😰 NVIDIA carries enormous expectations - any disappointment triggers selloff

- ⚠️ Trump tariff policy creates headline risk

- 🌍 China-Taiwan geopolitical risk always lurking

- 📊 Following $68M institutional bet with conviction

Why this could blow up (SERIOUS RISKS):

- 🚀 NVIDIA crushes earnings and raises guidance - sector rips higher

- 💸 Premium decay: Time is enemy if SMH stays flat

- 📈 Momentum continues - fighting the trend is dangerous

- 🎢 AI narrative remains strong through 2026

Estimated P&L:

- 💰 Cost: ~$2,500-$3,000 per contract

- 📈 Potential profit: 100-300% if SMH drops 10%+ by March 20

- 📉 Max loss: 100% of premium if SMH stays above $410

Risk level: HIGH (can lose entire premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🚀 NVIDIA earnings in 13 days: The biggest catalyst for semiconductors is right around the corner. NVIDIA represents 18.32% of SMH - a strong beat could send the entire sector higher, crushing put positions. Record $57B Q3 revenue sets high expectations.

-

📈 Fighting strong momentum: SMH is up 46% YTD and 67% over 52 weeks. Betting against this kind of trend is dangerous. 93% of industry leaders expect continued growth - the fundamental backdrop remains bullish.

-

💸 Premium decay risk: Put options lose value every day (theta decay). If SMH consolidates sideways, the $68M position bleeds premium daily. Time is the enemy of option buyers.

-

🌍 Geopolitical tail risks cut both ways: While China-Taiwan tensions could hurt semiconductors, any resolution or de-escalation would be massively bullish for TSMC and the sector.

-

💰 Tariff exemptions likely: Big Tech firms expected to receive carve-outs tied to TSMC's US investment. The worst tariff scenarios may not materialize.

-

🏭 HBM4 production could exceed expectations: SK Hynix four months ahead of schedule suggests memory constraints easing. Samsung boosting capacity 50%. Could accelerate AI chip production.

-

📊 This could simply be portfolio insurance: The $68M trade may be hedging a much larger long position. Doesn't mean the trader expects SMH to crash - just prudent risk management before a major catalyst.

-

🎢 Concentration risk works both ways: Top 5 holdings = 49.8% of assets. Strong results from NVIDIA, TSMC, or Broadcom could drive outsized gains.

🎯 The Bottom Line

Real talk: Someone just paid $68 MILLION for downside protection on semiconductors with NVIDIA earnings 13 days away. This is either the most expensive insurance policy of the year or a high-conviction bearish bet from someone who thinks the AI chip rally is overextended.

What this trade tells us:

- 🛡️ Smart money is hedging: After 46% YTD gains, institutions are protecting profits

- ⏰ NVIDIA earnings is THE catalyst: Feb 25 will make or break the near-term semiconductor trade

- 📊 $400 is the line in the sand: That's where institutional support should kick in (only 5% below current price)

- 💰 Not a crash call: This is hedging against consolidation, not betting on catastrophe

If you own semiconductor positions:

- ✅ Consider adding protective puts following this institutional playbook

- 📊 $400 strike provides reasonable cushion while maintaining upside

- ⏰ Make your hedging decision BEFORE February 25 NVIDIA earnings

- 🎯 If holding through earnings, size positions appropriately for 5-10% potential drawdown

- 🛡️ This trade gives you "permission" to hedge - if the big boys are doing it, you should too

If you're watching from the sidelines:

- ⏰ February 25 after close is judgment day for semiconductors - mark your calendar

- 🎯 Pullback to $400 (the put strike) would be an attractive entry point

- 📈 Looking for confirmation that AI chip demand remains robust through NVIDIA results

- 🚀 Longer-term, semiconductor industry approaching $1 trillion by year-end supports bullish thesis

- ⚠️ Avoid FOMO buying at 52-week highs ahead of binary earnings event

If you're bearish on semiconductors:

- 🎯 This $68M trade validates your thesis - smart money agrees risk exists

- 📊 Consider put spreads to manage premium costs ($400/$380 for defined risk)

- ⚠️ Size conservatively - fighting 46% YTD momentum is dangerous

- ⏰ Best entry may be AFTER NVIDIA earnings if results disappoint expectations

- 📉 First real support at $400 (gamma from this monster trade), then $385

Mark your calendar - Key dates:

- 📅 February 25, 2026 (13 days) - NVIDIA Q4 FY2026 earnings - THE catalyst

- 📅 March 20, 2026 - Put expiration date - resolution of this trade

- 📅 Q1-Q2 2026 - HBM4 mass production ramp

- 📅 H2 2026 - NVIDIA Vera Rubin chip launch expected

Final verdict: This is a classic institutional hedge ahead of a major catalyst. With semiconductors up 46% YTD and NVIDIA representing nearly a fifth of SMH, someone with a massive long book is buying insurance before earnings. The message isn't "sell everything" - it's "the easy money has been made, protect your gains." Follow the smart money's lead and consider adding protection before February 25. If NVIDIA crushes it, you lose some premium but your longs rip. If NVIDIA disappoints, your hedge pays off. That's risk management, not market timing.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The trade size ($68M) reflects institutional-scale positioning that may not be appropriate for retail accounts. Always do your own research and consider consulting a licensed financial advisor before trading. NVIDIA earnings create binary event risk with potential for significant gaps in either direction.

About VanEck Semiconductor ETF (SMH): SMH is the leading semiconductor industry ETF with ~$25 billion in assets under management, providing concentrated exposure to the AI chip supercycle through holdings in NVIDIA (18.32%), TSMC (10.76%), Broadcom (7.14%), Micron (6.40%), and ASML (5.91%). The ETF has delivered +66.68% total returns over the past 52 weeks.