⚡ SMR Nuclear Stock's Wild $10M Option Roll - Big Money Adjusts Strike Up After 75% Crash! 🔄

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated trader just executed a $10.1M "Roll Up" strategy on SMR, closing $8.3M worth of $15 calls and simultaneously opening $1.9M in $19 calls - both expiring this Friday! This isn't panic selling - this is tactical repositioning after NuScale's brutal 75% collapse from its October peak of $57.42 to $16.60. With the stock now bouncing back toward $18.78, smart money is betting on continued recovery while locking in gains from the original lower-strike position. Translation: Institutional player is staying bullish but raising their profit target!

📊 Company Overview

NuScale Power Corporation (SMR) is pioneering the next generation of nuclear power with small modular reactor (SMR) technology:

- Market Cap: $4.61 Billion

- Industry: Fabricated Plate Work (Nuclear Power Equipment)

- Headquarters: Corvallis, Oregon

- Current Price: $18.78 (recovering from $16.60 recent low)

- Primary Business: VOYGR Small Modular Reactor plants and E2 Energy Centers providing scalable, carbon-free nuclear power

- Key Advantage: ONLY U.S. company with NRC-approved SMR technology - first-mover in the nuclear renaissance driven by AI data center power demand

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 11:25:05):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Z_Score | Z_Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 11:25:05 | SMR | SELL | CALL | 2026-01-09 | $15 | 21,000 | $8,300,000 | STC | 3.96 | EXTREMELY_UNUSUAL |

| 2026-01-05 | 11:25:05 | SMR | SELL | CALL | 2026-01-09 | $19 | 23,000 | $1,900,000 | STO | 357.85 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means - The "Roll Up" Strategy Explained

This is a classic "Roll Up" adjustment - a sophisticated options maneuver that retail traders should understand! Here's what went down:

🔄 The Two-Part Trade:

- Close the winning position: Sold to close (STC) 21,000 contracts of $15 strike calls for $8.3M - these were already deep in-the-money (stock at $18.78, calls at $15)

- Open new higher strike: Sold to open (STO) 23,000 contracts of $19 strike calls for $1.9M - these are slightly out-of-the-money

💡 What's the point?

This trader likely bought the $15 calls weeks ago when SMR was much lower (possibly in the $12-14 range during December's selloff). Now with stock at $18.78:

- ✅ Those $15 calls are worth ~$3.95 each ($8.3M ÷ 21,000 = $395/contract)

- 🎯 They're taking profits and "rolling up" to $19 strike to capture more upside if stock keeps rallying

- 💰 Net credit received: $8.3M (close) - $1.9M (open) = $6.4M profit locked in!

- 📊 Slightly increased position size: 21K → 23K contracts shows continued bullishness

Translation for regular folks: Imagine you bought a concert ticket for $15 when the band was unknown. Now the band is huge and your ticket is worth $395. Instead of just selling it, you sell your $15 ticket for $395, then immediately buy a $19 ticket for $82.61. You pocket $312.39 profit per ticket AND you still get to go to the concert if prices keep rising! That's exactly what this trader did with 21,000-23,000 "tickets" to SMR's potential rally.

Unusual Score: 🔥🔥 DOUBLE EXTREME - Both legs show "EXTREMELY_UNUSUAL" classification!

- $15 Call Close: Z-Score of 3.96 (4 standard deviations above normal - happens a few times a year)

- $19 Call Open: Z-Score of 357.85 (literally OFF THE CHARTS - this is 358 standard deviations!)

The 357.85 Z-score on the $19 call opening is astronomically unusual. We're talking about activity that's 358x the normal size for SMR options - this is institutional-grade positioning, not retail speculation.

📈 Technical Setup / Chart Check-Up

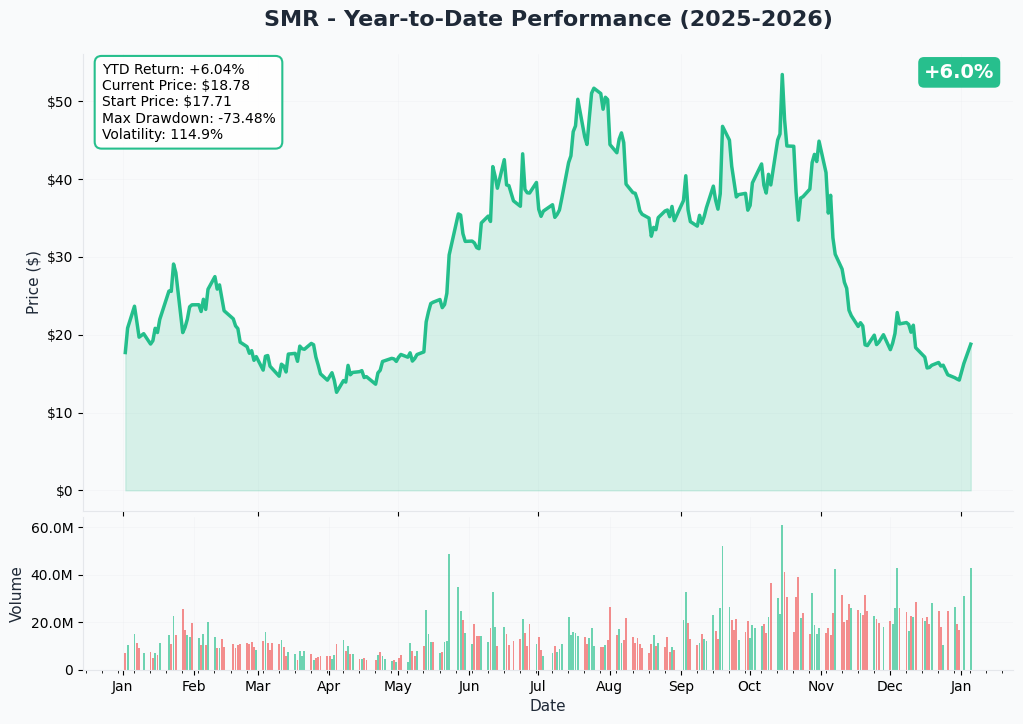

YTD Performance Chart

The Nuclear Rollercoaster Story:

SMR is showing one of the most volatile charts in the entire market - a perfect boom-bust-recovery cycle that tells the tale of AI data center euphoria meeting harsh reality:

📊 Key Price Levels:

- All-Time High: $57.42 (October 16, 2025) - peak AI/nuclear hype

- Recent Low: $11.08 (52-week low) - capitulation after Q3 earnings disaster

- Current Price: $18.78 (recovering +13% from $16.60 recent low)

- YTD Change: Started 2026 around $16-17, now trading $18.78

🎢 The Three Acts:

-

Act I - The Nuclear Renaissance (March-October 2025): Explosive rally from $20s to all-time high $57.42 driven by the landmark 6 GW TVA-ENTRA1 partnership announced September 2, 2025 and the U.S.-Japan $550B Framework Agreement on October 29, 2025 positioning ENTRA1 to receive up to $25B in funding. SMR gained 24.6% in October alone.

-

Act II - The Collapse (November-December 2025): Brutal 75% crash from $57.42 to ~$14-15 range. The trigger: Q3 2025 earnings miss on November 6th showed revenue of $8.24M vs $11.55M consensus, with massive -$1.85 EPS vs -$0.13 expected - a 1,323% negative surprise! The quarter posted $273M net loss and $538M operating loss, deepened by $502.2M increase in G&A expenses due to ENTRA1 milestone payments. November saw -55.4% decline, December added another -30%.

-

Act III - The Recovery Attempt (January 2026): Stock bounced +15.2% on January 2nd on renewed nuclear sentiment and technical rebound, with trading volume hitting 31.1M shares vs 21.89M average.

What the chart screams: This is NOT a stable investment - it's a high-beta speculation on the nuclear power renaissance. The sharp V-shaped recovery attempt from $14 to $18+ in just days shows bulls are trying to establish a higher low, but the question remains: was $57 a bubble, or $14 a gift?

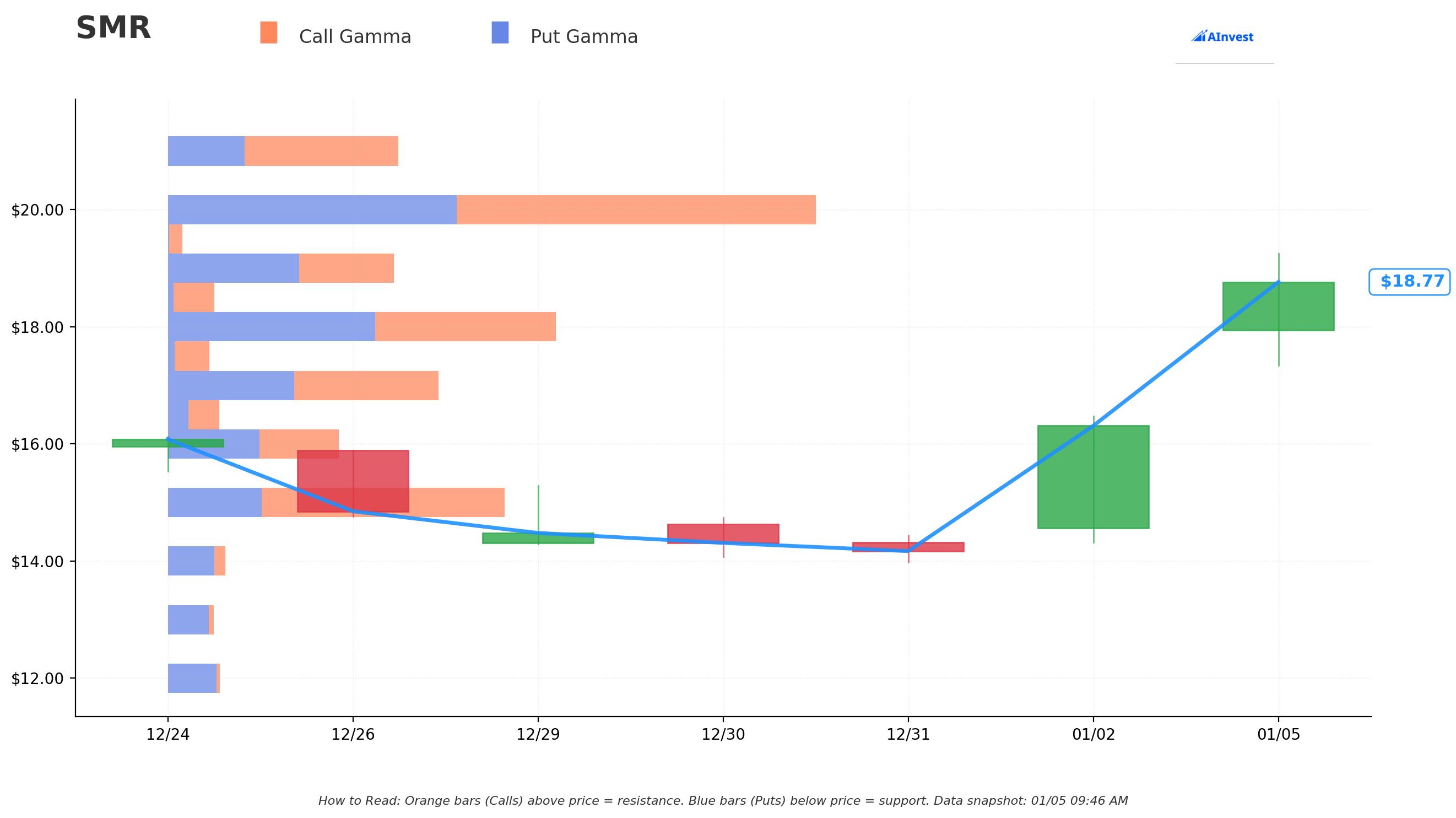

Gamma-Based Support & Resistance Analysis

Current Price: $18.78

The gamma exposure landscape reveals CRITICAL price magnets where options dealers will aggressively hedge their positions:

🔵 Support Levels (Put Gamma Below Price):

- $18.50 - Immediate floor with 0.45B total gamma exposure (1.5% below) - MUST HOLD to maintain recovery momentum

- $18.00 - Major support zone with 3.80B gamma (4.2% below) - strongest nearby put gamma level

- $17.50 - Secondary support at 0.40B gamma (6.8% below)

- $17.00 - Structural floor with 2.64B gamma (9.5% below)

- $16.50 - Deep support at 0.51B gamma (12.1% below)

- $16.00 - Disaster scenario at 1.68B gamma (14.8% below) - recent low territory

🟠 Resistance Levels (Call Gamma Above Price):

- $19.00 - Immediate ceiling with 2.22B gamma (1.2% overhead) - THIS IS WHERE THE ROLL UP CALL WAS STRUCK! 🎯

- $20.00 - Major resistance with 6.33B gamma (6.5% above) - STRONGEST SINGLE LEVEL in entire gamma map

- $21.00 - Extended resistance at 2.25B gamma (11.8% above)

- $22.00 - Heavy ceiling zone with 3.17B gamma (17.1% above)

What this means for traders:

The $19 strike where this trader sold calls sits at the FIRST major gamma resistance level (2.22B). This is NOT coincidental - they're betting stock struggles to break through $19 by Friday expiration. Even more importantly, the MASSIVE $20 strike (6.33B gamma - by far the largest level) acts as a brick wall overhead.

The gamma setup screams "range-bound this week": Strong $18.50 support below, formidable $19-20 resistance above. The options market expects SMR to trade in a tight $18-20 range through Friday's expiration - which is EXACTLY what the roll-up trader wants. If stock stays below $19, those $19 calls expire worthless and they keep the full $1.9M premium on top of the $6.4M already banked.

Net GEX Bias: Bullish (23.4B call gamma vs 18.0B put gamma) - Overall market positioning leans bullish, but immediate upside capped by heavy overhead gamma.

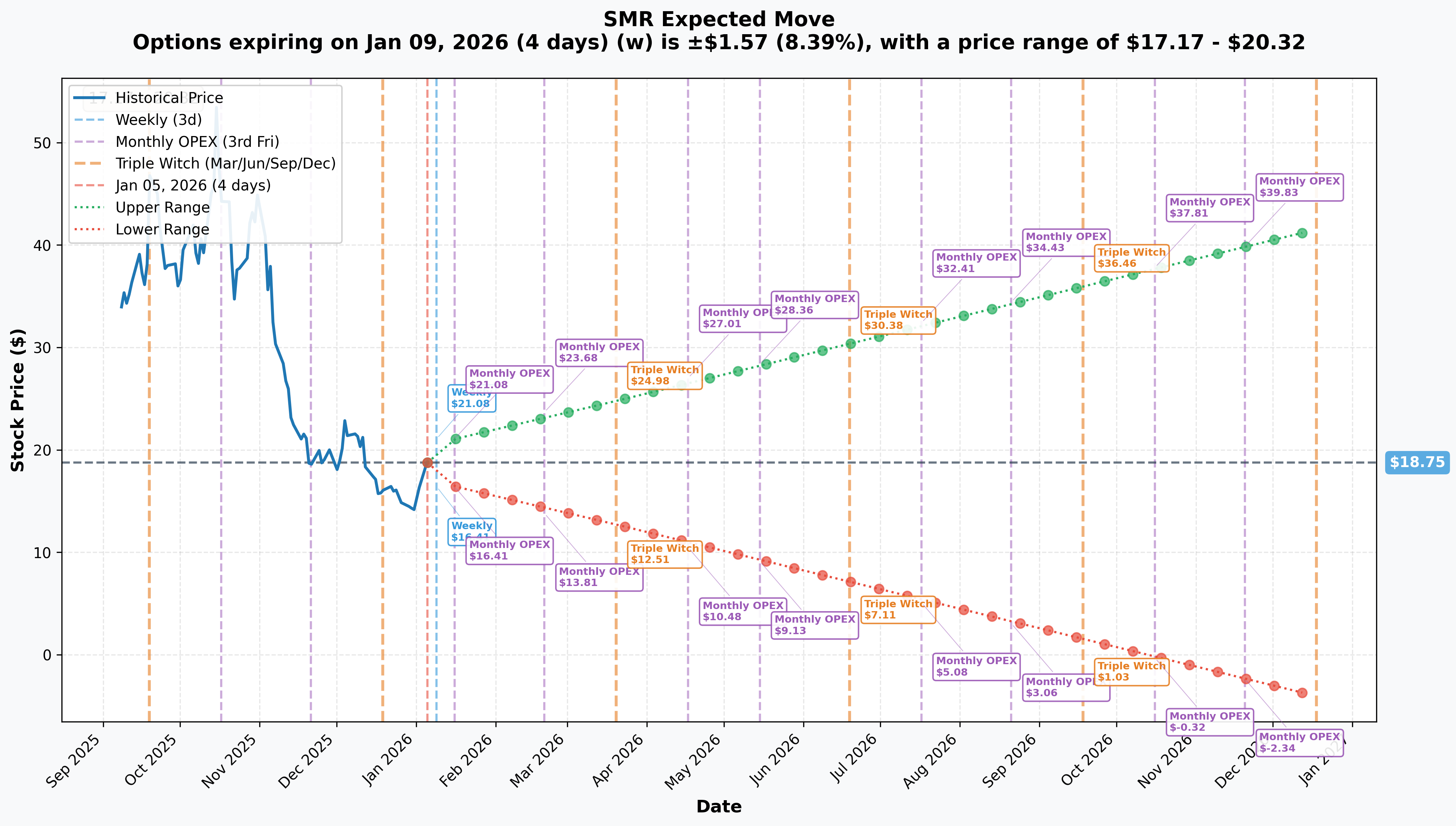

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days - THIS TRADE!): ±$1.57 (±8.39%) → Range: $17.17 - $20.32

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$2.33 (±12.45%) → Range: $16.41 - $21.08

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$6.06 (±32.31%) → Range: $12.69 - $24.80

- 📅 Yearly LEAPS (Dec 18 - 347 days): ±$22.80 (±121.64%) → Range: -$4.06 - $41.55

Translation for regular folks:

Options traders are pricing in an 8.4% move ($1.57) by Friday - that's HUGE for a 4-day window! The market expects SMR to trade somewhere between $17.17 and $20.32 by January 9th expiration. Notice the $19 call strike sits INSIDE this range but at the high end - the trader is betting stock doesn't quite reach $19 by Friday.

The MASSIVE 121.64% implied move for yearly LEAPS (literally suggesting stock could go to $41.55 or -$4.06) shows the extreme uncertainty around SMR's long-term prospects. This is one of the highest implied volatility profiles in the entire market - confirming this is pure speculation, not investment.

Key insight: The sharp decrease in implied move from 8.4% (weekly) to 12.5% (monthly) isn't as steep as typical - volatility stays elevated even weeks out, reflecting the Romania Final Investment Decision catalyst expected mid-to-late 2026 and Q4 earnings on March 12, 2026.

🎪 Catalysts

🔥 Upcoming Catalysts (What Could Move This Stock)

Romania RoPower Final Investment Decision - Mid-to-Late 2026 🇷🇴

This is THE make-or-break catalyst for near-term revenue generation:

- 📅 Timeline: Mid-to-late 2026 or early 2027 (already delayed from original late 2025 target) - source

- 🏗️ Project Scope: 6 x 77 MWe NuScale modules (462 MWe total capacity) at Doicesti site in Romania

- 💰 Partners: Nuclearelectrica, Nova Power & Gas (E-Infra), Samsung C&T, with Fluor as main contractor for FEED Phase 2

- 📊 Recent Progress: RoPower signed contract with Studsvik Scandpower for nuclear fuel analysis software in October 2025 - shows project advancing

- 💸 Revenue Impact: This would be NuScale's primary driver of near-term engineering services revenue, moving from MOU to binding contract

- ⚠️ Dependencies: Requires US Ex-Im Bank loan approval, Romanian government financing commitments, and delivery of Class 3 cost estimate

Why this matters: Without Romania FID, NuScale has essentially ZERO confirmed revenue-generating projects. The entire bull thesis depends on this moving from "partnership" to "actual contract with cash flow."

Q4 2025 Earnings - March 12, 2026 (66 days away!) 📊

Wall Street will be watching like a hawk after the Q3 disaster:

- 📅 Date: March 12, 2026 after market close - source

- 💰 Consensus Revenue: $11.19M (vs $8.24M actual in Q3)

- 📉 Consensus EPS: -$0.1519 (massive improvement vs -$1.85 in Q3)

- 🔍 Key Metrics to Watch:

- Progress toward binding customer contracts (CEO promised "hard contracts" with 2-3 major customers by end of 2025)

- Cash burn rate and ATM offering utilization

- RoPower FEED Phase 2 completion update

- ENTRA1 milestone payment accounting (this was the $495M hit in Q3)

Upside scenario: Any announcement of binding commercial contracts (especially data center operators) could trigger 20-30% rally Downside risk: Another earnings miss or delayed Romania FID timeline could retest $14-15 lows

Binding Commercial Contracts - 2026 Timeline 📝

CEO targeted "hard contracts" with 2-3 major U.S. customers by end of 2025 (likely extending into 2026):

- 🎯 Primary Prospects: Data center operators and hyperscalers (think Microsoft, Google, Amazon partnerships like they've done with other nuclear providers)

- 🏭 Standard Power Project: 24 modules (1,848 MWe) for Ohio/Pennsylvania data centers - still awaiting binding agreement beyond MOU stage

- 💡 Probability: Medium - Management has repeatedly emphasized this as top priority, but MOUs don't equal signed contracts

Why this is CRITICAL: The entire AI data center narrative depends on converting interest into actual purchase orders. Without binding contracts, NuScale remains a pre-revenue speculative stock burning $500M+ per quarter.

VOYGR-12 NRC Certification - 2026 Expected 📋

Larger-scale reactor configuration under NRC review since 2023:

- 🏭 Capacity: 12-module, 924 MWe configuration (vs current 77 MWe modules)

- ✅ Impact: Enables larger-scale deployments for utility and industrial customers, better competing with traditional nuclear plants

- 📅 Expected Decision: 2026 (exact date TBD)

- 🎯 Significance: Expands addressable market beyond niche SMR applications to full utility-scale projects

DOE $800M SMR Funding Initiative - December 2, 2025 💰

U.S. Department of Energy announced $800M to accelerate SMR deployment:

- 🎯 Purpose: Speed up SMR deployment across U.S.

- 🇺🇸 DOE Goal: At least 3 reactors achieve criticality by July 4, 2026 (ambitious!)

- 💸 NuScale Impact: Potential funding support to derisk project financing, though must compete with other SMR developers

- 🏆 Competitive Position: As ONLY NRC-certified SMR, NuScale has inside track for federal funding

Fluor Stake Monetization Completion - Q2 2026 📉

Fluor converting remaining Class B units and selling stake through structured agreement:

- 📅 Expected Completion: By end of Q2 2026

- 📊 Impact: Removes major shareholder overhang that's been pressuring stock

- ⚖️ Volume Restrictions: Structured sale with daily limits to prevent market flooding

- ✅ Positive: Once complete, eliminates constant selling pressure from large holder liquidation

⚠️ Past Catalysts (Already Happened - Context for Current Price)

TVA-ENTRA1 6 GW Partnership - September 2, 2025 🏆

The largest SMR deployment program in U.S. history:

- ⚡ Scale: 6 gigawatts across six plants on TVA sites in seven states

- 🏠 Capacity: Could power ~4.5M homes or ~60 data centers

- 💼 Structure: ENTRA1 Energy will finance, own, operate plants; sell output to TVA under future power purchase agreements

- ⏰ Timeline: Deployment possible by 2029-2030 (no specific dates announced)

- 💰 Revenue Impact: Potentially transformational, but revenue recognition 4-5 years away minimum

This was the catalyst that sent stock to $57.42 in October - pure speculative fervor around "what if this happens." Reality: No timeline, no costs disclosed, no binding contracts yet.

U.S.-Japan $550B Framework Agreement - October 29, 2025 🇺🇸🇯🇵

Bilateral agreement between President Trump and Prime Minister Takaichi:

- 💰 Funding: ENTRA1 Energy positioned to receive up to $25B investment capital for infrastructure buildout

- 🎯 Impact: Provides significant financial runway for SMR deployment, derisks funding concerns for TVA partnership

- 📈 Stock Reaction: This was the final catalyst pushing SMR to all-time high $57.42 on October 16, 2025

Q3 2025 Earnings Disaster - November 6, 2025 😱

The brutal reality check that triggered 75% collapse:

- 📉 Revenue: $8.24M vs $11.55M consensus - MASSIVE MISS

- 💀 EPS: -$1.85 vs -$0.13 consensus - 1,323% negative surprise

- 🔥 Net Loss: $273M for the quarter

- 💸 Operating Loss: Deepened 1,200% YoY to $538.44M

- 📊 G&A Expenses: Spiked $502.2M YoY due to $495M Milestone Contribution under ENTRA1 Partnership Agreement

- 💰 Cash Position: $753.8M (up from $489.9M in June), but burning >$500M/quarter

- 📈 ATM Offering: Sold 13.2M shares for $475.2M - significant dilution

Why the market freaked out: The ENTRA1 partnership milestone payment ($495M) showed up as an EXPENSE, not revenue. This isn't cash going out the door, but it highlighted that binding revenue is YEARS away while cash burn is immediate and massive.

NRC 77 MWe Design Approval - May 2025 ✅

Standard Design Approval (SDA) for US460 module completed 2 months ahead of schedule:

- ✅ Status: Completed May 2025, below cost thresholds

- 🏭 Enables: VOYGR-4 (308 MWe) and VOYGR-6 (462 MWe) plant configurations

- 🎯 Competitive Edge: Reinforces NuScale as ONLY U.S. company with NRC-certified SMR design

- 📊 VOYGR-12: 924 MWe configuration still under separate NRC review

Authorized Share Increase - December 2025 📈

Shareholders approved doubling authorized Class A shares from 332M to 662M:

- ⚠️ Dilution Risk: Provides capital-raising flexibility but reinforces fear of ongoing shareholder dilution

- 💸 ATM Context: Combined with $750M at-the-market offering announcement, signals continued heavy capital needs

- 📉 Stock Reaction: December saw -30% decline as dilution fears intensified

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through Friday's January 9th expiration (4 days):

📈 Bull Case (30% probability)

Target: $20-21

How we get there by Friday:

- 🚀 Positive news leak about Romania FID timeline acceleration or binding customer contract announcement

- 📰 Major hyperscaler (Microsoft, Amazon, Google) announces SMR partnership beyond ENTRA1

- 💰 Analyst upgrades emerge citing "overdone selloff" from $57 to $14 lows

- 📊 Technical breakout above $19 gamma resistance triggers short squeeze momentum to $20 level

- 🌐 Broader nuclear sector strength (uranium stocks rallying) lifts all boats

Key levels to watch:

- ✅ Break above $19 (current gamma resistance where roll-up calls struck) opens path to $20

- ✅ $20 is MAJOR gamma ceiling (6.33B) - needs explosive volume to breach

- 🎯 If $20 breaks, minimal resistance until $21-22 zone

Why only 30% probability: Stock needs 6-12% rally in just 4 days to reach $20-21, fighting against MASSIVE $20 gamma wall (6.33B - strongest level in entire map). The $19 call seller clearly doesn't expect this scenario, and they have access to information/modeling retail doesn't. Weekly implied move tops out at $20.32, so $21 would exceed even the optimistic options pricing.

Impact on the roll-up trade: If stock hits $20+, the $19 calls go in-the-money and trader faces assignment. However, they already banked $6.4M profit from closing $15 calls, so max loss would be ($20 - $19) × 23,000 = $2.3M, still netting $4.1M overall. Risk/reward still heavily in their favor.

🎯 Base Case (50% probability)

Target: $18-19 range (EXACTLY WHERE ROLL-UP WANTS IT!)

Most likely scenario through Friday:

- 📊 Stock consolidates in tight $18-19 range between gamma support ($18.50) and resistance ($19)

- 💤 No major catalysts hit before weekly expiration on January 9th

- 🤷 Market continues digesting Q3 earnings disaster vs long-term ENTRA1 potential

- 📉 Light profit-taking from recent bounce keeps stock from breaking $19

- ⚖️ Bulls and bears in stalemate - longs holding for Romania FID, shorts waiting for next earnings miss

- 🎢 Daily volatility within 8.4% implied move ($17.17-20.32 range) as expected

This is the PERFECT scenario for the roll-up trader:

- ✅ $19 calls expire worthless if stock stays below $19.00 → Keep full $1.9M premium

- ✅ Already locked in $6.4M profit from closing $15 calls

- ✅ Total P&L: $6.4M + $1.9M = $8.3M profit on a stock that's consolidating

Why 50% probability: The gamma setup SCREAMS range-bound action. Massive support at $18-18.50 (3.80B gamma), formidable resistance at $19-20 (2.22B + 6.33B gamma). Options market pricing 8.4% move puts midpoint right at $18.75 (current price $18.78). No major catalysts between now and Friday. This is the path of least resistance.

Trader's mindset: They rolled up to $19 strike because they expect stock to trade NEAR $19 but not ABOVE it. If they thought stock was going to $21+, they would've rolled to $21 or $22 strikes instead. If they thought stock was crashing to $15, they wouldn't have opened new calls at all. This positioning screams "I think we trade $18-19 this week."

📉 Bear Case (20% probability)

Target: $16-17 (TEST THE LOWS)

What could go wrong this week:

- 😰 Negative Romania FID news leaks (further delays announced, financing falling through)

- 🚨 Analyst downgrades citing unsustainable cash burn ($500M+ per quarter with minimal revenue)

- 💸 Secondary offering announced (more dilution fears after 662M authorized share increase)

- 📉 Broader market selloff drags speculative names lower (SMR trades with high beta)

- 🇨🇳 Macro headlines about nuclear regulatory delays or competition from Chinese SMR developers

- 🔨 Break below $18.50 gamma support triggers technical selling cascade to $18 → $17.50 → $17

Critical support levels:

- 🛡️ $18.50: Immediate floor (0.45B gamma) - first line of defense

- 🛡️ $18.00: Major support (3.80B gamma) - MUST HOLD or momentum shifts bearish

- 🛡️ $17.50: Secondary floor (0.40B gamma)

- 🛡️ $17.00: Deep support (2.64B gamma) - disaster scenario testing recent lows

Why only 20% probability: Stock just bounced hard from $14-15 lows and reclaimed $18+ with volume. Technical setup shows higher low forming. No obvious negative catalyst scheduled for this week. The $19 call seller isn't worried about downside (they're selling calls, not buying puts). Weekly implied move low end is $17.17, so drop to $16 would exceed even bearish expectations.

Impact on roll-up trade: If stock drops to $16-17, BOTH the $15 calls (already closed) and $19 calls (newly opened) expire worthless. Trader keeps full $6.4M profit from closing $15s PLUS full $1.9M from opening $19s = $8.3M total profit. This is actually the BEST scenario for them - maximum profit with zero risk of assignment.

💡 Trading Ideas

🛡️ Conservative: Wait for Romania FID Clarity

Play: Stay on sidelines until mid-2026 Romania Final Investment Decision

Why this works:

- ⏰ Stock trading on pure speculation until binding contracts materialize - too much binary risk

- 💸 Massive cash burn ($538M operating loss in Q3 alone) with minimal revenue ($8.24M) = unsustainable without dilution

- 📊 Valuation unclear: No P/E ratio possible with negative earnings, no revenue visibility

- 🎯 Romania FID is THE catalyst that converts "potential" to "actual" - everything else is noise

- 🔥 Better entry likely if FID delayed again (stock back to $12-14) OR better risk/reward if FID confirmed (pay up for certainty)

- 📉 Recent 75% crash from $57 to $14 shows how fast sentiment can turn on execution disappointment

Action plan:

- 👀 Monitor Romania FID news closely - currently expected mid-to-late 2026 or early 2027

- 📅 Mark calendar for Q4 2025 earnings on March 12, 2026 - need to see progress on binding commercial contracts

- ✅ Wait for CEO's promised "hard contracts with 2-3 major customers" to actually materialize with signatures

- 💰 If Romania FID confirmed with financing in place, stock could rerate 50-100% overnight - worth waiting for clarity

- ⚠️ If FID delayed beyond 2027 or financing falls through, stock likely retests $10-12 lows

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid 30-50% drawdown risk if execution stumbles. Get much better risk/reward entry if/when binding contracts announced. Nuclear revolution isn't going anywhere - you can afford to wait for proof.

⚖️ Balanced: Post-Earnings Stock Purchase with Tight Stop

Play: Buy shares after March 12th earnings IF results show progress, with disciplined $16.50 stop-loss

Why this works after earnings:

- 📊 Q4 earnings will show whether cash burn improved and if any binding contracts materialized

- 🎯 Better visibility after CEO's promise of "hard contracts with 2-3 customers by end 2025" deadline passes

- 📈 Positive earnings surprise (revenue >$11.19M, progress on contracts) could trigger 20-30% rally from technical oversold levels

- 🛡️ Defined risk: $16.50 stop-loss (recent support level) limits downside to ~12-15% from $18-19 entry

- ⏰ Hold through Romania FID catalyst mid-2026 for potential 100%+ upside if confirmed

- 💰 If ENTRA1 timeline clarifies or Standard Power binding agreement announced, stock has $30-40 potential

Entry criteria (ALL must be met):

- ✅ Q4 earnings revenue ≥$11M (shows sequential improvement from $8.24M disaster)

- ✅ Management provides Romania FID timeline update showing "on track" for mid-2026

- ✅ At least ONE binding commercial contract announced or "imminent within 30-60 days"

- ✅ Cash position still >$600M (enough runway for 3-4 quarters at current burn)

- ✅ Stock holding above $17.50 support technically

Position sizing:

- 📊 Risk only 3-5% of portfolio (this is speculative growth, not core holding)

- 🎯 Entry: $18-19 range post-earnings

- 🛡️ Stop-loss: $16.50 (firm - no exceptions!)

- 💰 Target 1: $25-27 (40-50% gain if Romania FID confirmed)

- 🚀 Target 2: $35-40 (if multiple binding contracts + ENTRA1 progress)

Why this is "Balanced" not Conservative:

- ⚠️ Still pre-revenue company burning massive cash - inherent risk remains high

- 📉 Dilution risk persists with 662M authorized shares and $750M ATM offering

- 🎢 Extreme volatility (see 75% crash) means even "right" thesis can suffer 30-40% drawdowns

- ⏰ Revenue recognition years away (2029-2030 for ENTRA1 deployment)

Risk level: Moderate (defined risk with stop-loss) | Skill level: Intermediate

Expected outcome: Participate in nuclear renaissance upside if execution delivers, while limiting downside to manageable loss if Romania/contracts fall through.

🚀 Aggressive: Copy the Roll-Up with Call Credit Spread (ADVANCED!)

Play: Sell $19/$20 call credit spread expiring January 9th (Friday)

Structure:

- 📉 Sell $19 calls (collect premium)

- 📈 Buy $20 calls (limit risk)

- 💰 Net credit: ~$0.30-0.40 per spread (adjust based on current pricing)

Why this could work (mirroring the institutional play):

- 🎯 Copying smart money positioning: They sold $19 calls for $1.9M because they expect stock below $19 by Friday

- 📊 Gamma resistance at $19 (2.22B) and MASSIVE wall at $20 (6.33B) creates natural ceiling

- ⏰ Only 4 days to expiration - massive time decay works in your favor ($0.07-0.10/day theta)

- 📈 Stock needs 6% rally in 4 days to breach $20 - unlikely without major catalyst

- 🛡️ Defined risk spread: Max loss = $1.00 width - $0.35 credit = $0.65 per spread

- ✅ Breakeven: $19.35 (stock can rally 3% from $18.78 and you still profit)

Why this could blow up (SERIOUS RISKS):

- 💥 Surprise Romania FID announcement (unlikely but possible) → Stock gaps to $21-22 overnight

- 🚀 Binding customer contract leaked → Short squeeze to $20+ on massive volume

- 📰 Broader nuclear sector catalyst (policy announcement, competitor news) → Sector-wide rally

- 😱 Assignment risk: If stock above $19 at expiration, short calls get assigned (you'd be short stock at $19 if protective $20 longs don't auto-exercise)

- 🎰 Gap risk: Stock could gap THROUGH your spread on news, locking in max loss before you can exit

Estimated P&L:

- 💰 Premium collected: ~$35-40 per spread (selling $19 call ~$0.65, buying $20 call ~$0.30)

- 📈 Max profit: $35-40 if stock below $19 at Friday close (100% of credit collected)

- 📉 Max loss: $60-65 if stock above $20 at Friday close (spread width $1.00 minus credit)

- 🎯 Breakeven: $19.35-19.40

- 📊 Risk/Reward: Risking $65 to make $35 (1.86:1 risk/reward) - not great, but high probability

Probability of profit: ~65-70% (stock needs to stay below $19.35, which gamma/implied move suggest is likely)

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Understand credit spreads and assignment mechanics (this isn't your first rodeo)

- ✅ Can monitor position daily and exit early if stock approaches $19 (don't be a hero)

- ✅ Have approved portfolio margin or enough cash to cover assignment if short call exercised

- ✅ Accept that surprise news could blow through your spread causing max loss

- ✅ Comfortable with 1.86:1 risk/reward (you're betting on high probability, not huge payout)

- ⏰ Plan to close position Thursday if profitable or if stock above $19 (don't hold to Friday expiration)

Position sizing:

- 🎲 Risk only 1-2% of portfolio max

- 📊 Example: $10K account → Max 2-3 spreads ($65 risk each = $130-195 total risk)

- ⚠️ DO NOT oversize - max loss can hit FAST on gap moves

Risk level: HIGH (unlimited gap risk on short calls if protective long doesn't cover) | Skill level: Advanced only

This is mimicking the $10.1M institutional trade at retail scale - you're betting the smart money is right about stock staying below $19.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Zero revenue with massive cash burn: Q3 showed just $8.24M revenue against $538M operating loss - company burning through ~$500M per quarter. Cash position of $753.8M provides only 3-4 quarters of runway at current burn rate without additional capital raises. Consensus projects breakeven requires ~$750M annual revenue - currently at $45M run rate. More dilution is INEVITABLE.

-

💸 Authorized shares doubled to 662M + $750M ATM offering: Shareholders approved increase from 332M to 662M authorized shares in December 2025, combined with massive $750M at-the-market offering announced. Already sold 13.2M shares for $475M in Q3. Dilution fears drove December's 30% decline. Expect CONTINUOUS equity issuance to fund operations through 2027-2029 deployment timeline.

-

🇷🇴 Romania FID already delayed, could slip further: Originally targeted late 2025, now pushed to mid-to-late 2026 or early 2027. Project requires US Ex-Im Bank loan approval, Romanian government financing, and Fluor's Class 3 cost estimate delivery. ANY further delay removes the ONLY near-term revenue catalyst, likely sending stock back toward $10-12 range. Remember Idaho CFPP project was CANCELED in 2023 when costs ballooned from $3.6B to $9.3B - projects can and do fall apart.

-

📉 Historical volatility of 75% crash shows sentiment fragility: Stock went from $57.42 (October 16, 2025) to ~$14-15 (December 2025) in just 6 weeks - a catastrophic 75% collapse triggered by single earnings miss. This shows how quickly "nuclear renaissance" narrative can evaporate when reality (cash burn, no binding contracts) hits. November alone saw -55.4% decline. Even if long-term thesis correct, stock can easily halve again on execution stumbles.

-

🏗️ ENTRA1 Partnership revenue recognition 4-5 years away minimum: 6 GW TVA-ENTRA1 deal announced September 2, 2025 with "deployment possible by 2029-2030" - that's FOUR TO FIVE YEARS from now! No specific timeline, no costs disclosed, no binding contracts yet. The $495M Milestone Contribution shown in Q3 was an EXPENSE (G&A hit), not revenue. Market got way ahead of reality valuing this at $57 in October.

-

⚠️ Fluor stake monetization adds selling pressure through Q2 2026: Fluor converting Class B units and selling through structured agreement - major shareholder systematically liquidating position creates constant overhead supply. Even with volume restrictions, this is significant selling pressure for a stock with $4.61B market cap and spotty liquidity.

-

💰 Nuclear economics challenge: Historical nuclear projects frequently exceed budgets 2-3x - Idaho CFPP ballooned from $3.6B to $9.3B before cancellation. Nuclear capex runs 5-10x natural gas ($6,417-$12,681/kW vs $1,290/kW) - customers will scrutinize ROI intensely. If early projects come in over-budget, future sales evaporate.

-

🎯 No binding customer contracts yet despite promises: CEO targeted "hard contracts" with 2-3 major U.S. customers by end of 2025 - deadline passed with no announcements. Standard Power's 24-module project for Ohio/Pennsylvania data centers remains MOU stage only. Until signatures on binding contracts with deposits/milestones, this is vaporware. MOUs mean NOTHING in terms of revenue recognition.

-

🏭 Competition emerging despite NRC advantage: While NuScale has ONLY NRC-certified SMR design currently, TerraPower expects NRC approval December 2026, GE Hitachi's BWRX-300 targeting same markets, and Oklo claims 14 GW customer pipeline despite no certification. First-mover advantage can evaporate quickly if execution stumbles or competitors deliver better economics.

-

📊 Q4 earnings March 12th is high-risk binary event: After Q3 disaster (revenue miss, -1,323% EPS surprise), market will have ZERO tolerance for another disappointment. Consensus $11.19M revenue and -$0.1519 EPS - any miss likely triggers 30-40% selloff retest of $12-14 lows. Even inline results might not rally stock without binding contract announcements.

-

🎰 Analyst ratings conflicted after 75% crash: Consensus rating: Hold (5 Buy, 5 Hold, 3 Sell) with average price target $33.32-$36.71 (100-135% upside implied). BUT recent downgrades include BNP Paribas to Underperform, Citi cut target 51% to $18.50, UBS slashed from $38 to $20. Wide dispersion shows NO CONSENSUS on valuation - pure speculation.

-

🌐 Macro recession risk with zero revenue buffer: If economy weakens in 2026-2027, discretionary data center build-outs and utility capex projects get CANCELED FIRST. NuScale has no existing revenue base to cushion a downturn. Enterprise customers will stick with proven natural gas/renewable solutions rather than risk billions on unproven SMR technology during recession.

🎯 The Bottom Line

Real talk: This $10.1M "Roll Up" trade is a MASTERCLASS in professional options trading. The institutional player locked in $6.4M profit from their original $15 calls, then turned around and sold $19 calls to collect another $1.9M - essentially betting stock consolidates in the $18-19 range this week. This is NOT a "buy SMR" signal - it's smart money managing a winning position after a massive bounce from $14 lows.

What this trade reveals:

- 💡 They made SERIOUS money on the bounce - $6.4M profit suggests they bought $15 calls when stock was in low teens during December's capitulation

- 🎯 They expect consolidation, not explosion - Selling $19 calls (only 1.2% above current price) says "rally is pausing here"

- ⏰ Friday expiration is strategic - Capturing quick premium decay with no major catalysts scheduled this week

- 📊 Gamma levels confirm their thesis - Massive resistance at $19-20 makes further upside unlikely short-term

- 🔄 They're staying in the game - Didn't close everything and walk away; still holding bullish exposure via short calls (unlimited upside risk past $19)

What SMR's story REALLY is:

SMR is a high-risk speculation on the nuclear renaissance thesis, NOT an investment. The company has:

- ✅ Real technology: Only NRC-certified SMR design, legitimate first-mover advantage

- ✅ Massive TAM: AI data center power demand is REAL, nuclear is part of the solution

- ✅ Credible partnerships: TVA-ENTRA1 6 GW deal, $25B U.S.-Japan funding, DOE $800M initiative

BUT also has:

- ❌ Zero binding revenue contracts - All partnerships are MOUs/framework agreements

- ❌ Massive cash burn - $538M operating loss on $8.24M revenue in Q3

- ❌ Years away from revenue - 2029-2030 at earliest for ENTRA1 deployment

- ❌ Inevitable dilution - 662M authorized shares, $750M ATM offering

- ❌ Execution risk - Romania FID already delayed, Idaho CFPP canceled

If you own SMR:

- 📊 Recognize you're holding a LOTTERY TICKET, not an investment

- 🎯 The move from $14 to $18+ is a 28% bounce - consider taking some profits

- ⏰ Next binary catalyst is Q4 earnings March 12, 2026 - will show if promised contracts materialized

- 🛡️ Set mental stop-loss at $16.50 (recent support) to protect against retest of lows

- 💰 If holding for Romania FID mid-2026, understand you're signing up for 6+ more months of volatility

- ⚠️ Diversify - this shouldn't be more than 5% of your portfolio given binary risk

If you're watching from sidelines:

- ✅ Wait for Romania FID clarity - THE catalyst that determines if this is real or vaporware

- 📅 Monitor March 12 earnings closely - Need to see binding contract progress, not more MOUs

- 🎯 Better entries will come - Stock has proven it can drop 75% in 6 weeks; be patient

- 💡 If Romania FID confirmed with financing → Stock easily $25-35+ (100% upside)

- 😰 If Romania FID delayed to 2027+ → Stock back to $10-12 (30-40% downside)

- 🌐 Long-term nuclear thesis intact - You don't need to buy at $18 when better entry likely at $14-15 or clear confirmation at $22-25

If you're bearish:

- 📉 Current bounce from $14 to $18 looks like dead-cat bounce into resistance

- 🎯 Short setup: Wait for failed breakout above $19-20, then short with $21 stop

- 📊 Put spreads post-March earnings offer defined-risk way to play downside

- ⚠️ Don't fight the nuclear narrative blindly - if binding contracts hit, short squeeze to $30+ possible

- ⏰ Timing matters - shorting at $15 near lows was suicide; shorting at $25+ near resistance makes sense

Mark your calendar - Key dates:

- 📅 January 9, 2026 (Friday) - Weekly options expiration (this roll-up trade expires!)

- 📅 January 16, 2026 - Monthly OPEX

- 📅 March 12, 2026 - Q4 2025 earnings (THE moment of truth for binding contracts)

- 📅 Mid-to-Late 2026 - Romania RoPower Final Investment Decision expected

- 📅 Q2 2026 - Fluor stake monetization completion (removes selling overhang)

- 📅 2029-2030 - ENTRA1 deployment timeline (actual revenue generation starts)

Final verdict: The nuclear renaissance thesis is LEGITIMATE - AI data centers need reliable baseload power and SMRs are part of the solution. NuScale has real first-mover advantage as the ONLY NRC-certified provider. BUT, the stock went from $57 to $14 (-75%) for good reason: no binding contracts, massive cash burn, and revenue 4-5 years away minimum.

The $10M roll-up trade shows smart money is playing the BOUNCE, not making a long-term bet. They're trading the range ($18-19), collecting premium, and staying nimble. Retail investors should do the same - wait for PROOF (Romania FID, binding contracts) before treating this as anything other than a trading vehicle.

Be smart. The nuclear revolution will still be here when SMR actually has customers with signatures. 💡

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The "Roll Up" strategy described is a professional institutional trade that may not be appropriate for retail traders. SMR is a pre-revenue company with extreme volatility - the 75% crash from $57 to $14 demonstrates the risks. Romania Final Investment Decision and binding customer contracts remain uncertain. Always do your own research and consider consulting a licensed financial advisor before trading. Options strategies like credit spreads carry assignment risk and can result in 100% loss of premium.

About NuScale Power Corporation: NuScale Power develops small modular reactor (SMR) technology delivering safe, scalable, cost-effective, and reliable carbon-free power through VOYGR Plants and E2 Centers, with a market cap of $4.61 billion in the Fabricated Plate Work industry. Headquartered in Corvallis, Oregon, the company holds the only U.S. Nuclear Regulatory Commission-approved SMR design.