🌨️ SNOW Multi-Year AI Infrastructure Play - $25M LEAPS Bull Spread!

📅 December 11, 2025 | 🚨 EXTREMELY UNUSUAL - 300X+ Average Size

🏢 Company Overview

- Description: Cloud data platform leader enabling AI/ML analytics across AWS, Azure, and Google Cloud

- Market Cap: $76.92B (Source: Companies Market Cap)

- Sector: Cloud Infrastructure / Data Warehousing

- Current Price: $220.84

🎯 The Quick Take

Holy moly - someone just dropped $25 MILLION on a 3+ year bet that Snowflake will transform into an AI infrastructure powerhouse! This isn't a quick earnings flip - we're talking January 2028 LEAPS (3 years out!) structured as a bull call spread targeting the $200-$260 range. With Z-scores hitting 300x and 353x average activity, this is the kind of institutional conviction that makes you stop and pay attention. Big money is betting $15M that SNOW's AI transformation story is just getting started!

💰 The Option Flow Breakdown

📊 What Just Happened

The Epic LEAPS Trade (December 11, 2025):

| Side | Type | Expiration | Strike | Contracts | Premium | Action | Z-Score | Unusualness |

|---|---|---|---|---|---|---|---|---|

| BUY | CALL | 2028-01-21 | $200 | 2,000 | $15M | BTO | 300.35 | 🔥 EXTREMELY_UNUSUAL |

| SELL | CALL | 2028-01-21 | $260 | 2,000 | $10M | STO | 353.66 | 🔥🔥 EXTREMELY_UNUSUAL |

Net Debit: $5 million total ($2,500 per spread) Breakeven: $202.50 (current: $220.84) Max Profit: $10 million at $260+ (200% return on capital) Max Loss: $5 million if below $200 at expiry

🤓 What This Actually Means

This is a bull call debit spread - but not your typical earnings play. This is a multi-year strategic bet on Snowflake's AI transformation thesis:

- Long $200 strike calls: Paying $15M for the right to participate in upside above $200

- Short $260 strike calls: Collecting $10M premium, capping upside at $260

- Net position: $5M at risk for $10M potential profit (200% return if SNOW hits $260+)

- Time horizon: January 2028 - giving SNOW's AI initiatives 3+ years to play out!

Unusual Score: 🔥🔥 ABSOLUTELY INSANE - Z-scores of 300.35 and 353.66 mean these trades are 300x and 353x larger than average! We're talking top-tier institutional money making a multi-year conviction call. This happens maybe once or twice a year across the entire market.

The Thesis: Someone believes the $200M Anthropic partnership, AI revenue acceleration, and enterprise AI adoption will drive SNOW from $220 to $260+ over the next 3 years. That's only 18% upside needed - but they're betting $15M it happens!

📈 Technical Setup / Chart Check-Up

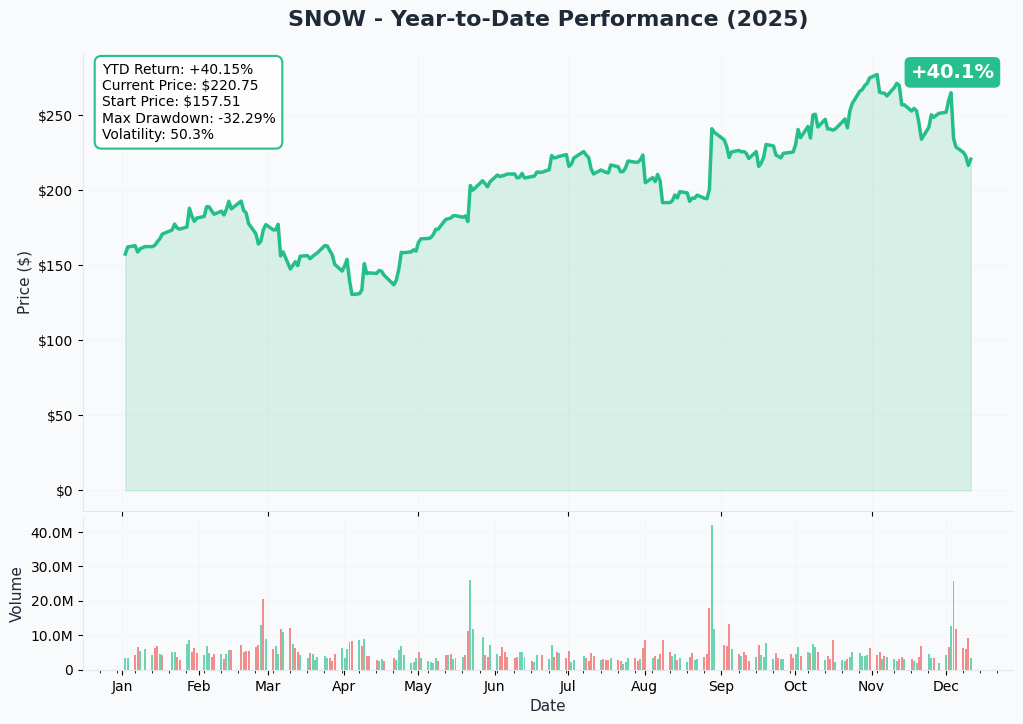

YTD Performance

📊 View Live SNOW Chart on AInvest

Snowflake has absolutely ripped in 2025 - up 48.76% YTD and a stunning 79% from April lows (Source: 24/7 Wall St.). The recent consolidation around $220 following November earnings suggests we're building a base for the next leg higher. The AI narrative is taking hold!

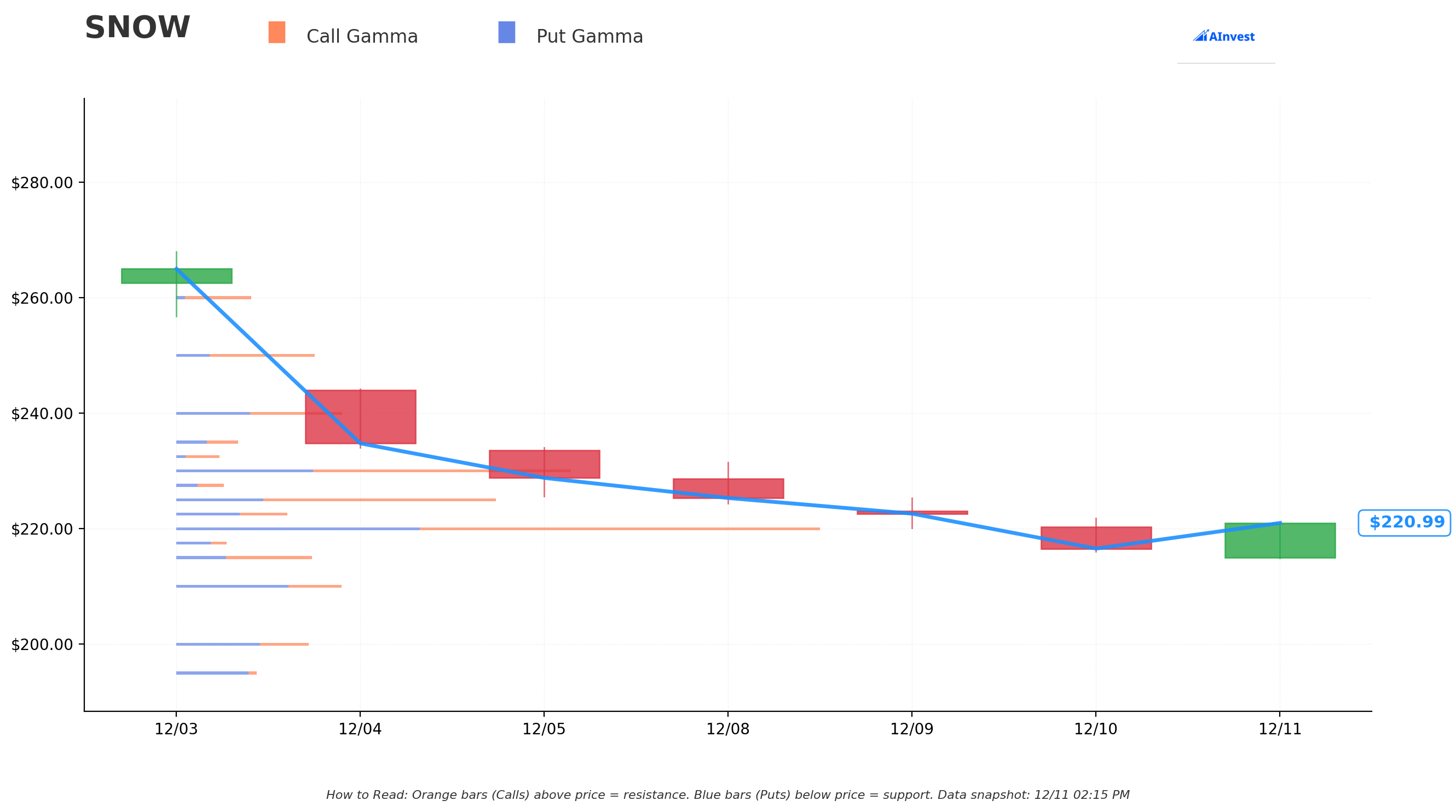

Gamma-Based Support & Resistance Analysis

Current Price: $220.84 (as of Dec 11, 2025)

The gamma exposure reveals why this LEAPS spread makes perfect sense:

🛡️ Support Levels (Put Gamma):

- $220: STRONGEST support with 23.69 total GEX (current level!)

- $215: Secondary support at 5.12 total GEX (2.6% down)

- $210: Solid floor at 6.04 total GEX (4.9% down)

- $200: LEAPS long strike - 4.85 total GEX (9.4% down) - this is the breakeven floor!

- $195: Deep support at 2.93 total GEX (11.7% down)

🚀 Resistance Levels (Call Gamma):

- $222.5: Immediate resistance at 4.04 total GEX (0.8% above)

- $225: First major wall at 11.44 total GEX (1.9% up)

- $230: MASSIVE resistance with 14.22 total GEX (4.1% up) - toughest level!

- $240: Strong ceiling at 5.97 total GEX (8.7% up)

- $250: Significant resistance at 5.02 total GEX (13.2% up)

- $260: LEAPS short strike - the profit target!

Net GEX Bias: BULLISH - Call GEX dominates at 64.10 vs Put GEX of 45.67

Key Insight: The $200-260 spread perfectly brackets the current gamma structure! The $200 strike sits at a major support level (strong put gamma), while $260 represents a clean 18% upside target. This trader expects SNOW to grind higher through multiple gamma resistance layers over 3 years as the AI story unfolds!

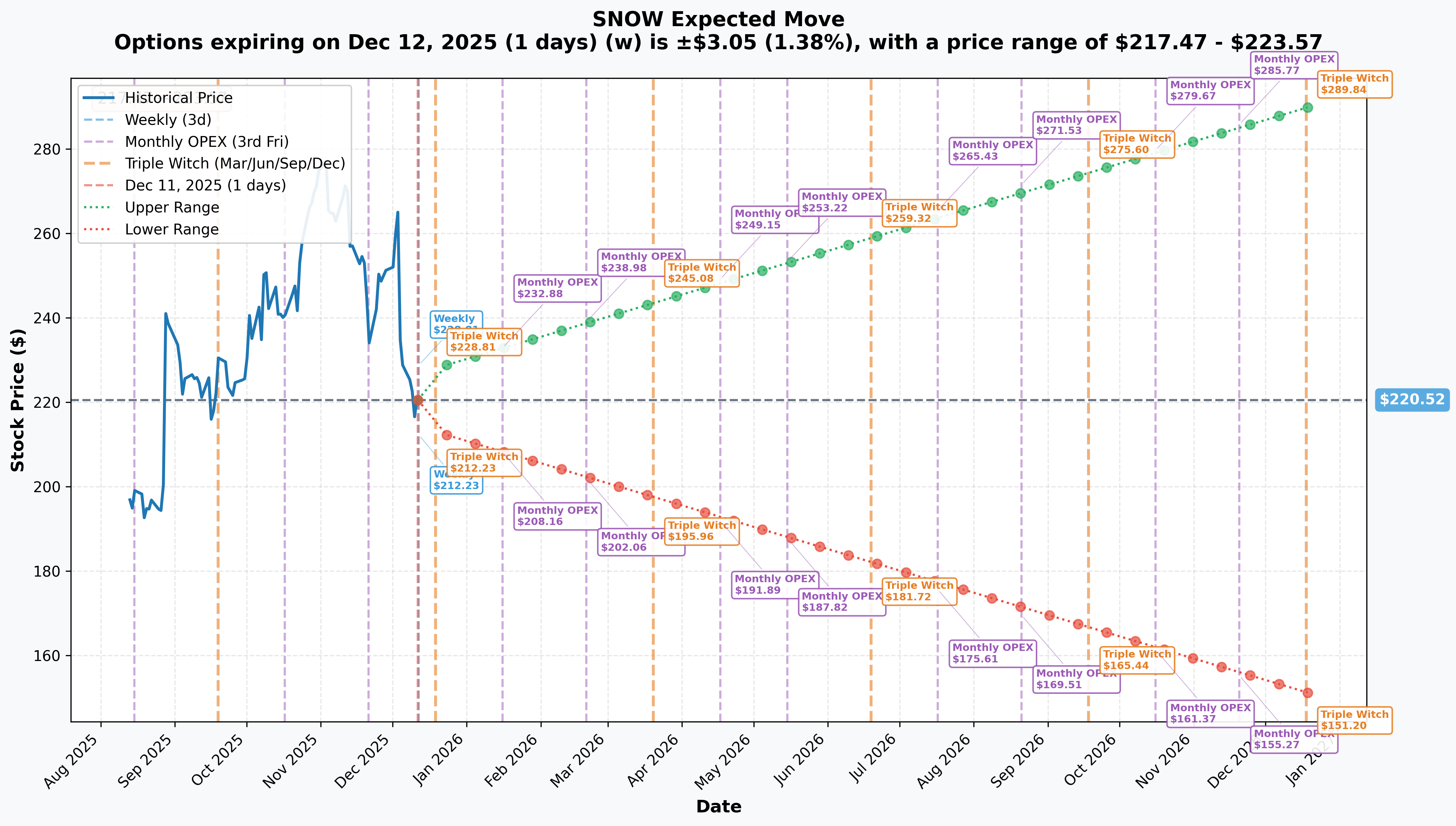

🌊 Implied Move Analysis

Let's contextualize this LEAPS bet against market expectations:

📅 Near-Term Expectations:

- Weekly (Dec 12): ±1.38% ($217.47-$223.57) - tight range

- Monthly OPEX (Dec 19): ±3.45% ($212.91-$228.13)

- LEAPS (Dec 2026): ±31.43% ($151.20-$289.84) - MASSIVE range!

The LEAPS Math:

- Current: $220.84

- Target: $260 (17.7% upside)

- 3-Year timeframe: January 2028

- Annualized return needed: ~5.6% per year to hit $260

Reality Check: The market is pricing a 31.43% implied move over just 1 year to Dec 2026. This trader needs only 17.7% over 3 YEARS to max out their profit! That's incredibly achievable if Snowflake's AI monetization plays out as management projects.

🎪 Catalysts - The 3-Year AI Transformation Story

Q4 FY2026 Earnings - March 4, 2026 (Next Major Event)

Consensus Estimates (Source: Nasdaq):

- Revenue: $1.195-1.2B product revenue (27% YoY growth)

- EPS: Consensus TBD

- What to watch:

- AI revenue progression beyond $100M quarterly run rate

- Operating margin recovery from guided 7% in Q4

- FY2027 initial guidance for growth and profitability

- Net revenue retention sustainability above 120%

The $200M Anthropic AI Partnership (December 4, 2025)

Game-Changer Alert (Source: Anthropic):

- Multi-year $200 million commitment to integrate Claude across 12,600+ Snowflake customers

- Claude powers Snowflake Intelligence enterprise AI agent

- Thousands of customers already processing trillions of Claude tokens monthly through Cortex AI

- Integration across Amazon Bedrock, Google Vertex AI, Microsoft Azure

Why This Matters for the LEAPS: This partnership creates a 3-year revenue runway from AI consumption. As enterprises adopt Claude-powered analytics, Snowflake's consumption revenue should accelerate substantially!

AI Revenue Acceleration (Q3 FY2026 Beat)

Recent Results (Source: Quarter Results):

- AI Revenue: $100M in Q3 - one full quarter ahead of projections!

- Product Revenue: $1.16B (+29% YoY) beating $1.18B consensus

- EPS: $0.39 vs $0.31 consensus (+25.8% beat)

- AI Initiatives: Contributing to 50% of new bookings

- Snowflake Intelligence: 1,200+ customers already using the platform

The Trajectory: If AI revenue hit $100M in Q3 and is accelerating, we could see $400-600M annual AI revenue by FY2027 - that's 10-15% of total revenue from AI alone!

Palantir Partnership (November 25, 2025)

Strategic Integration (Source: TechAfrica News):

- Integration with Palantir Foundry and AIP (Artificial Intelligence Platform)

- Bidirectional zero-copy interoperability through Iceberg Tables

- Eaton selected as early adopter building AI-enabled workflows

- Opens commercial and public sector markets for joint AI applications

Market Position & Competitive Dynamics

Market Leadership (Source: ProjectPro):

- Snowflake: 18.33% market share in cloud data warehouse ($3.8B run rate)

- Databricks: 8.67% market share ($2.6B revenue, but growing 57% vs SNOW's 27%)

- Market Growth: $36.31B (2025) → $155.66B (2034) at 17.55% CAGR

The Competitive Reality:

- Databricks threat is real - recently raised at $62B valuation with faster growth

- Hyperscaler integration advantage for AWS Redshift, Azure Synapse, Google BigQuery

- BUT: SNOW maintains SQL-first simplicity, multi-cloud architecture, and 125% net revenue retention

Why the LEAPS Still Makes Sense: Even if SNOW's growth slows from 29% to 20-25%, compounded over 3 years with AI monetization, you easily get to $260+!

Snowflake Summit 2026 (June 1-4, 2026)

Major Product Announcements Expected (Source: Moscone Center):

- Location: Moscone Center, San Francisco

- Focus: Next-generation AI features and partnerships

- Expected: New Cortex AI capabilities, additional AI partnerships, platform enhancements

- Historically a major catalyst for product momentum and customer enthusiasm

🎲 Price Targets & Probabilities (3-Year Horizon)

This isn't about next quarter - it's about January 2028! Here's the multi-year outlook:

🚀 Bull Case (40% probability)

Target: $260-320 by Jan 2028

- AI revenue grows to $800M-1B annually (20-25% of total)

- Anthropic partnership drives consumption surge across enterprise base

- Operating margins recover to 10-12% as AI products scale

- Net revenue retention stays above 120%

- Successfully fends off Databricks with SQL-first simplicity advantage

- Outcome: LEAPS spread maxes out at $10M profit ✅

😐 Base Case (35% probability)

Target: $230-260 by Jan 2028

- AI revenue grows to $500-700M annually (12-18% of total)

- Revenue growth moderates to 20-23% range but remains healthy

- Operating margins stabilize around 8-10%

- Competitive pressures from Databricks intensify but market share holds

- Outcome: LEAPS spread profits $3-10M depending on final price

😰 Bear Case (25% probability)

Target: $180-220 by Jan 2028

- AI monetization disappoints - hits only $300-400M annually

- Databricks wins significant market share in ML/AI workloads

- Hyperscalers bundle aggressively, pressuring pricing and margins

- Macro headwinds reduce enterprise IT spending growth

- Operating margins compressed below 7% due to competition

- Outcome: LEAPS spread loses partial to full $5M ❌

Expected Value Calculation:

- Bull: 40% × $10M = $4.0M

- Base: 35% × $6M = $2.1M

- Bear: 25% × -$3M = -$0.75M

- Total EV: +$5.35M on $5M risk = 107% expected return over 3 years!

💡 Trading Ideas - How to Play This Thesis

🛡️ Conservative: "Sell the Gamma Wall for Income"

Strategy: Sell short-term calls against resistance while SNOW grinds higher

Trade Setup:

- Sell SNOW Jan 2026 $230 calls for ~$8-10 premium

- Collect income while SNOW battles the massive 14.22 GEX wall at $230

- Rinse and repeat monthly to build long-term position

Rationale:

- Gamma resistance at $230 creates natural ceiling short-term

- Can collect 3-5% monthly premium while waiting for breakout

- Use premium to fund protective puts or build cash

Risk Management:

- Stock breaks above $235 → roll up and out for credit

- Cap assignment risk at acceptable level ($230 × 100 = $23,000/contract)

Why it works: Time decay and gamma resistance work in your favor while building income!

⚖️ Balanced: "The Mini LEAPS Spread"

Strategy: Replicate the institutional trade at retail scale

Trade Setup:

- Buy SNOW Jan 2027 $200 calls (2 years out)

- Sell SNOW Jan 2027 $260 calls

- Net debit: ~$25-30 per spread (estimated)

- Max profit: $60 per spread at $260+ (200% return)

- Position size: 5-10 spreads = $1,250-3,000 at risk

Rationale:

- Mirror the institutional conviction with defined risk

- 2-year timeframe gives AI story time to develop

- Breakeven around $230 - achievable with 5-6% annual growth

Risk Management:

- Only risk 2-5% of portfolio on this speculation

- Set calendar reminder for Q2 2026 to reassess AI traction

- Consider taking profits at 50-75% max gain if hit early

Why it works: Follow smart money with appropriate sizing for retail account!

🚀 Aggressive: "Long Stock + Sell Calls (Covered Call LEAPS)"

Strategy: Buy shares now and sell calls against gamma resistance

Trade Setup:

- Buy 100 shares of SNOW at $220.84 = $22,084 capital

- Sell SNOW Feb 2026 $240 calls for ~$12-15 premium monthly

- Collect 5-6% monthly income while stock appreciates

- If called away at $240, you've made 8.7% on stock + all call premiums

Advanced Variant:

- Sell multiple rounds of $230-240 calls over 3 years

- Collect $3,000-5,000 per 100 shares in premium annually

- If SNOW stays range-bound, premium income >> LEAPS spread return!

Rationale:

- Gamma walls at $230-240 make call selling attractive

- Build income while participating in AI transformation

- Lower risk than pure options - you own the stock!

Risk Management:

- Diversify - don't put >10% of portfolio in single name

- Be willing to hold through volatility (3-year horizon)

- If stock drops below $200, consider selling puts to average down

Why it works: Combine appreciation potential with income generation through the gamma structure!

⚠️ Risk Factors - The Bear Case Reality Check

Let's get real - here's what could absolutely wreck this trade:

🔥 Competition Intensification

- Databricks growing 2x faster (57% vs 27%) and valued at $62B - they're gunning hard for the AI/ML market

- Hyperscaler bundling: AWS, Azure, Google can offer integrated solutions with aggressive pricing

- Microsoft Fabric emerging as unified SaaS lakehouse competing directly

- Risk Level: HIGH - Could compress market share and pricing power

💰 Margin Compression Continuation

- Q4 FY2026 operating margin guided to 7% (down from 11% in Q3) (Source: GuruFocus)

- Stock-based compensation at 41% of revenue is unsustainable (Source: AInvest)

- If margins stay compressed at 5-7%, valuation multiples could collapse

- Risk Level: MEDIUM-HIGH - Path to profitability uncertain

📉 Valuation Vulnerability

- Trading at 165x forward P/E vs Datadog ~66x, MongoDB ~76x (Source: TS2 Tech)

- Price-to-FCF: 64.64x - extremely rich vs peers

- Still losing $689M despite $3.8B revenue scale

- Risk Level: EXTREME - Any growth slowdown = massive multiple compression

🌍 Macro Headwinds

- 67% of CIOs under cost-cutting pressure per industry surveys (Source: AInvest)

- Consumption-based model vulnerable to usage optimization during budget cuts

- Enterprises may delay AI project deployments if recession hits

- Risk Level: MEDIUM - Could slow growth from 27% to 15-20%

🤖 AI Monetization Uncertainty

- $100M in AI revenue sounds great but needs to hit $600M+ by FY2027 to justify thesis

- Hyperscalers commoditizing AI infrastructure could pressure pricing

- Agentic AI adoption still early - could take longer than 3 years to scale

- Risk Level: MEDIUM - Timeline and magnitude both uncertain

📊 Consumption Revenue Volatility

- Revenue only recognized when customers consume credits - not when sold (Source: SaaStr)

- Large deals with delayed consumption create quarterly unpredictability

- Could miss quarters even if underlying business healthy

- Risk Level: LOW-MEDIUM - Creates noise but not structural problem

Bottom Line on Risks: This is a HIGH RISK, HIGH CONVICTION bet. The margin compression + valuation + competition trifecta could absolutely crush the stock if execution falters. Only bet what you can afford to lose entirely!

🎯 The Bottom Line

Let's wrap this epic analysis up: When an institution drops $25 million on a 3-year LEAPS spread with Z-scores exceeding 300x average activity, you don't ignore it. This is a calculated, multi-year thesis on Snowflake's transformation into the central AI data infrastructure layer for enterprises globally.

The Bull Thesis in 30 Seconds:

✅ $200M Anthropic partnership creates 3-year AI consumption runway ✅ AI revenue hit $100M in Q3 - one quarter ahead of schedule ✅ 125% net revenue retention shows sticky, expanding customers ✅ 50% of new bookings influenced by AI initiatives ✅ Market growing 17.55% CAGR to $155.66B by 2034 ✅ Only needs 5.6% annual growth to hit $260 max profit

The Bear Thesis in 30 Seconds:

❌ Margins compressed from 11% to 7% guidance ❌ Databricks growing 2x faster at 57% vs 27% ❌ 165x forward P/E leaves zero room for error ❌ Still losing $689M with unclear path to profitability ❌ Hyperscaler competition intensifying with bundled offerings ❌ Macro risk - 67% of CIOs cutting budgets

My Take:

This trade makes sense IF you believe:

- The AI data analytics market will explode over 3 years (likely ✅)

- Snowflake can maintain 18% market share vs Databricks/hyperscalers (uncertain ⚠️)

- Operating margins recover to 10%+ as AI scales (questionable ❓)

- The Anthropic partnership drives meaningful consumption growth (probable ✅)

The math works: $260 target requires only 17.7% appreciation over 3 years (5.6% annually). Given 48.76% YTD gains and AI tailwinds, this is achievable - but far from guaranteed!

Your action plan depends on conviction level:

📍 High Conviction (I believe in SNOW's AI future):

- Replicate with smaller LEAPS spreads (Jan 2027 $200/$260)

- Buy shares and sell calls against gamma walls

- Target 5-10% portfolio allocation

📍 Medium Conviction (Interesting but risky):

- Sell near-term calls against $230 gamma wall for income

- Small LEAPS spread position (1-2% of portfolio)

- Monitor Q4 earnings and AI revenue trajectory

📍 Low Conviction (Too much uncertainty):

- Stay in cash or look for better risk/reward setups

- Wait for margin recovery evidence before entering

- Consider selling put spreads for premium if stock corrects

Key Dates to Monitor:

- March 4, 2026: Q4 FY2026 Earnings - AI revenue update critical!

- June 1-4, 2026: Snowflake Summit - major product announcements

- Q1-Q2 FY2027: Margin recovery inflection point (or warning sign)

- January 2028: LEAPS expiration - judgment day!

Final Warning: This institution can afford to lose $5 million testing a thesis. Can you? Position size appropriately - I'd recommend no more than 2-5% of portfolio in LEAPS speculation, even with compelling thesis. The valuation, competition, and execution risks are all REAL.

But damn... when smart money bets $15 million on a 3-year AI transformation play, it's hard not to pay attention! 🚀

📚 Additional Resources

Deep Dive on Snowflake's AI Strategy:

Competitive Analysis:

- Snowflake vs Databricks Comparison

- Cloud Data Warehouse Market Share

- Databricks Funding and Valuation

Risk Assessment:

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Options trading involves substantial risk of loss and is not suitable for all investors. The Z-scores and unusual activity metrics indicate statistical deviation from average activity but do not predict future price movements. Past performance is not indicative of future results. Always conduct your own due diligence and consult with a licensed financial advisor before making investment decisions. The author may or may not have positions in the securities discussed.

Options involve risk and are not suitable for all investors. Please read the Characteristics and Risks of Standardized Options before investing in options.