SNOW $6M Diagonal Put Spread - Institutional Bearish Bet Targets Near-Term Downside!

January 29, 2026 | Unusual Activity Detected

The Quick Take

An institutional trader just deployed a $6M diagonal put spread on Snowflake at 14:19:33 - buying 8,800 contracts of the $195 puts (Feb 20 expiration) while simultaneously selling 8,700 contracts of the $165 puts (Apr 17 expiration) for a net debit of ~$1.2M. With SNOW trading at $199.27 and the $195 strike sitting right on the strongest gamma support level, this trader is betting Snowflake drops in the near term, then recovers before April. The short $165 put funds most of the trade, creating a capital-efficient bearish position ahead of what could be a pivotal Q4 FY2026 earnings report in early March. Translation: Smart money sees near-term weakness for Snowflake, but not a total collapse.

Company Overview

Snowflake Inc. (SNOW) is the leading cloud-native data platform powering enterprise analytics and AI workloads:

- Market Cap: $73.9 Billion

- Industry: Services-Prepackaged Software

- Current Price: ~$197.76 (up +25.6% YTD)

- Primary Business: Fully managed cloud data platform consolidating data across AWS, Azure, and Google Cloud for centralized analytics, governance, and increasingly AI/ML workloads

The Option Flow Breakdown

The Tape (January 29, 2026 @ 14:19:33):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:19:33 | SNOW | MID | BUY | PUT $195 | 2026-02-20 | $6M | $195 | 8,800 | 9,700 | 7,910 | $199.27 | $7.56 |

| 14:19:33 | SNOW | MID | SELL | PUT $165 | 2026-04-17 | $4.8M | $165 | 8,700 | 159 | 7,910 | $199.27 | $6.08 |

What This Actually Means

This is a diagonal put spread - a sophisticated bearish time spread! Here is the breakdown:

- Net debit: ~$1.2M ($6M paid for Feb $195 puts minus $4.8M received from Apr $165 puts)

- Near-term leg (Feb 20 $195 puts): Only 2% out-of-the-money with 22 days to expiration. This is the directional bet - the trader expects SNOW to drop below $195 before February monthly OPEX.

- Far-dated leg (Apr 17 $165 puts): 17% out-of-the-money with 78 days to expiration. This is the financing leg - collecting $6.08 per contract in premium to offset the cost of the near-term puts.

- Size matters: 7,910 contracts represents 791,000 shares of exposure worth ~$157M notional

- OI context: The Feb $195 put had 9,700 open interest, and 8,800 volume traded today. The Apr $165 put had only 159 open interest before this 8,700-contract block - this trader IS the market in that strike.

- Execution: Both legs filled at the MID, indicating an institutional desk working the order for best execution

What is really happening here: This trader believes SNOW faces near-term downside - likely targeting the Q4 FY2026 earnings report estimated around March 4, 2026. The Feb 20 expiration captures the pre-earnings volatility window. By selling the longer-dated $165 puts, they are expressing a view that SNOW will NOT collapse to $165 or below by April - they expect a pullback, not a crash. The diagonal structure also benefits from time decay working differently on each leg: the near-term put decays faster if the stock drops quickly, while the far-dated short put decays slowly, allowing the trader to potentially close the short put at a profit after the near-term move plays out.

Unusual Score: EXTREME - The Apr $165 put had only 159 open interest before this 8,700-contract block. This single trade represents approximately 55x the existing open interest at that strike. The coordinated execution of both legs at the same timestamp on the MID confirms institutional origin.

Technical Setup / Chart Check-Up

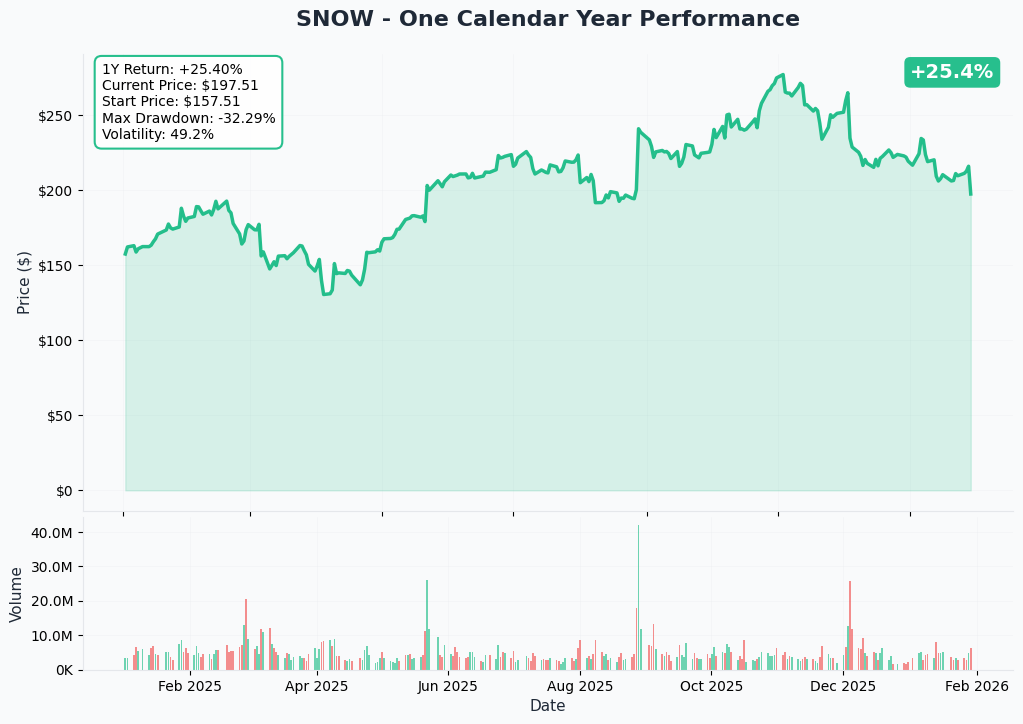

One Calendar Year Chart

SNOW is up +25.6% YTD with a current price around $197.76. The stock has been range-bound in the $190-$215 area after peaking near its 52-week high of $215. Notably, shares fell after the Q3 FY2026 earnings beat in December 2025, signaling the market is demanding more than just meeting expectations.

Key observations:

- Range-bound action: SNOW has been consolidating between $190-$215 since the December earnings reaction

- Failed breakout: The stock tested $215 (52-week high) but could not hold, suggesting distribution

- $200 psychological resistance: Price is struggling to maintain levels above $200 - this round number is acting as a ceiling

- Volume profile: Institutional participation has been mixed - partnership announcements generate pops that fade quickly

- YTD context: +25.6% is solid but lags hyper-growth peers, reflecting the growth deceleration narrative

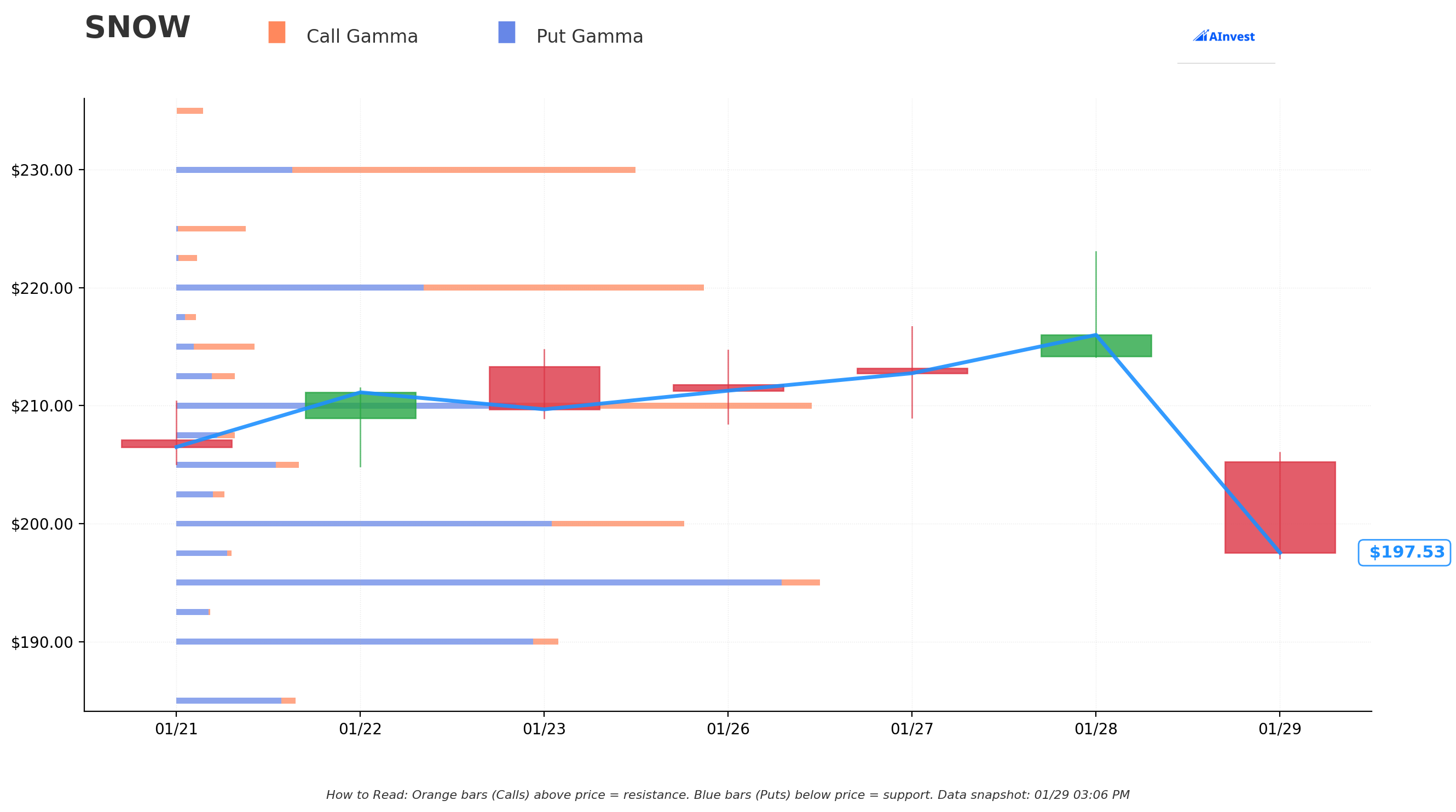

Gamma-Based Support & Resistance Analysis

Current Price: $197.93

The gamma exposure map reveals critical price levels that will govern near-term price action:

Support Levels (Put Gamma Below Price):

- $195 - Immediate and STRONGEST gamma support (this is EXACTLY where the long put is struck!)

- $190 - Secondary support level with significant put gamma concentration

- $185 - Additional support providing a deeper floor

- $180 - Major structural support level

- $170 - Deep support zone (close to the $165 short put strike)

Resistance Levels (Call Gamma Above Price):

- $200 - Immediate overhead resistance (psychological round number + gamma wall)

- $205 - Secondary resistance level

- $210 - Significant call gamma concentration

- $220 - Major overhead ceiling

- $230 - Extended upside target with elevated call gamma

What this means for traders: SNOW is trading just above its strongest gamma support at $195, with heavy resistance at the $200 round number. The bearish net GEX bias means market makers are positioned in a way that could amplify downside moves. If $195 support breaks, the next meaningful gamma level is $190, then $185 - creating potential for a quick flush.

Notice the strike selection: The put buyer chose $195 PRECISELY at the strongest gamma support level. If this level breaks, dealer hedging flows will accelerate the move lower. Meanwhile, the short $165 put sits near the $170 gamma support - the trader believes that even in a selloff, $165-$170 will hold as the ultimate floor.

Net GEX Bias: Bearish - This is significant. When net gamma exposure is negative, market maker hedging AMPLIFIES price moves in both directions. A break below $195 could trigger a cascade of dealer selling that pushes the stock toward $185-$190 rapidly.

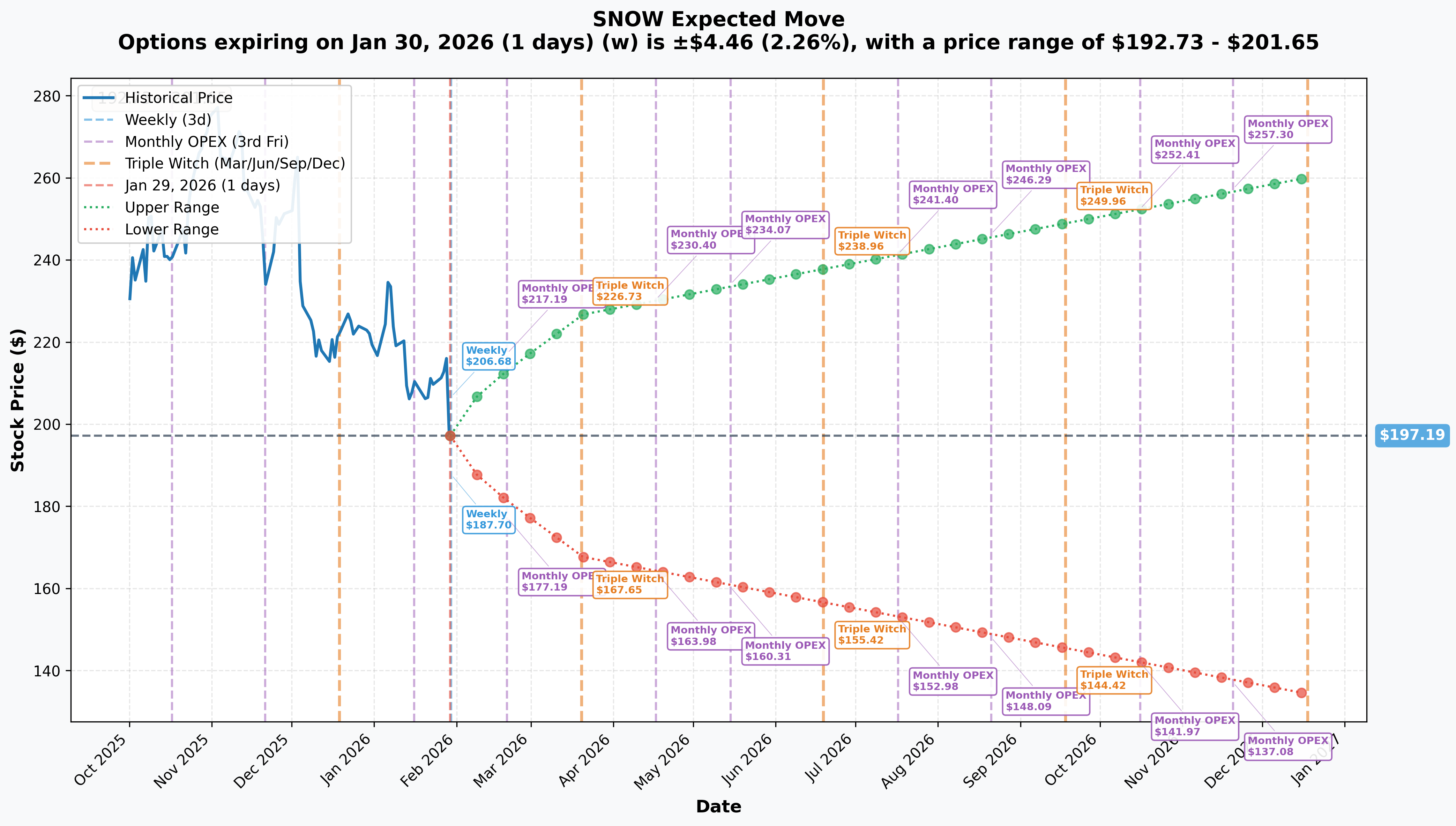

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 30 - 1 day): +/-2.3% (+/-$4.46) -> Range: $192.73 - $201.65

- Monthly OPEX (Feb 20 - 22 days - LONG PUT EXPIRATION!): +/-8.2% (+/-$16.19) -> Range: $181.00 - $213.38

- Quarterly (Mar 20 - 50 days): +/-15.0% (+/-$29.54) -> Range: $167.65 - $226.73

Translation for regular folks: The options market expects SNOW could move about 2.3% by tomorrow, but a much larger 8.2% move ($16) through the February OPEX on the 20th. That means the market sees a realistic scenario where SNOW trades as low as $181 or as high as $213 over the next three weeks.

The February 20 expiration (when the $195 long put expires) has a lower range of $181 - well below the $195 strike. This means the options market itself is pricing in a meaningful probability that SNOW trades below $195 before mid-February.

The March 20 quarterly range extends down to $167.65 - essentially right at the $165 short put strike. The diagonal spread is structured so that the short put sits just below the quarterly implied move floor, giving the trader a cushion against assignment risk.

Key insight: The 8.2% monthly implied move for February captures Q4 FY2026 earnings uncertainty even though earnings are expected around March 4 (just after the Feb 20 expiration). Pre-earnings volatility will elevate the February puts, and the diagonal structure lets the trader profit from near-term price weakness while the longer-dated short put decays more slowly.

Catalysts

Immediate Catalysts (Next 30 Days)

Pre-Earnings Positioning Window - Now through Late February

SNOW enters its quiet period ahead of the Q4 FY2026 earnings report estimated for March 4, 2026. During this window, the stock is vulnerable to:

- Sector rotation away from high-multiple cloud software names

- Pre-earnings de-risking by institutional holders

- Technical breakdown if $195 gamma support fails

- Competitive noise from a potential Databricks IPO filing which could reprice SNOW downward

Near-Term Catalysts (Q1 2026)

Q4 FY2026 Earnings - Estimated March 4, 2026 (THE KEY EVENT)

This is the dominant catalyst for the stock and likely the reason behind this diagonal put spread:

- Product Revenue Guidance: $1.195B - $1.2B (+27% YoY) - decelerating from 29% in Q3

- Consensus EPS: $0.27 (non-GAAP)

- FY2027 guidance will be the single most important data point - market expects 25%+ product revenue growth to justify ~15x revenue valuation

- Key metrics to watch: AI revenue run rate trajectory beyond $100M achieved in Q3, net revenue retention trend (125% in Q3), operating margin expansion, and Observe acquisition integration update

- Growth deceleration concern: Product revenue growth has decelerated every quarter - 34% (Q1) -> 30% (Q2) -> 29% (Q3) -> 27% guided (Q4). If FY2027 guidance implies sub-25% growth, the stock could sell off sharply.

- Historical precedent: Shares fell after the Q3 beat, signaling the market demands acceleration, not just beats

Why this matters for the put spread: The Feb 20 long put expires BEFORE the March 4 earnings, meaning the trader profits from pre-earnings anxiety and volatility build-up. If SNOW drops to $190 or below on pre-earnings jitters, the $195 put pays off handsomely. The Apr 17 short put survives through earnings, collecting premium whether or not earnings disappoint.

Anthropic Partnership ($200M Agreement) - January 2026

- Multi-year $200M agreement making Anthropic Claude models available natively in Snowflake platform

- Thousands of customers already processing trillions of Claude tokens per month through Cortex AI

- Focus on deploying AI agents for complex, multi-step enterprise analysis

- Supports the narrative that SNOW is building a model-neutral AI platform - but market wants revenue proof, not just partnerships

Google Cloud Gemini 3 Integration - January 6, 2026

- Gemini 3 models now available natively within Snowflake Cortex AI

- Platform now live on Google Cloud in Saudi Arabia with Melbourne launch upcoming

- SNOW rose 5.6% on the announcement - but gains have since faded, illustrating the "pop and drop" pattern

Observe Acquisition Closing - Expected Q1 2026

- Definitive agreement to acquire Observe for AI-powered observability capabilities

- Integration with AI Data Cloud to enable 10x faster issue resolution for AI agents

- Adds another revenue stream but creates integration execution risk and potential margin pressure

Medium-Term Catalysts (Q2 2026)

Potential Databricks IPO (H1 2026)

This is arguably the biggest risk catalyst for SNOW over the next six months:

- Databricks CEO indicated potential IPO at $100B+ valuation

- A public Databricks creates a direct comparable: Databricks growing 50% vs. SNOW 29%, with NRR >140% vs. SNOW 125%

- Databricks has 50 customers spending >$10M annually - demonstrates stronger enterprise penetration

- Analysts note Databricks AI revenue advantage is "structural, not cyclical"

- If Databricks IPOs at a comparable or lower revenue multiple despite faster growth, it could force a re-rating of SNOW downward

FY2027 Guidance (at Q4 Earnings)

- Consensus expects ~$5.89B revenue for FY2027 (+24% YoY)

- This guidance number will determine whether SNOW can maintain its premium valuation or faces a growth-to-value re-rating

- Market needs to see 25%+ growth and a clear path to GAAP profitability

AI Revenue Monetization Inflection

- AI revenue run rate was $100M in Q3, achieved ahead of schedule

- Analysts watching for acceleration to $200M+ by mid-FY2027

- 50% of bookings influenced by AI in Q3 - but conversion to actual consumed revenue remains the question

- Cortex AI now integrates Gemini 3 + Claude + open-source models, positioning SNOW as the model-neutral enterprise AI platform

Competitive Landscape

Databricks: The Primary Competitive Threat

- Both at ~$4B ARR, but Databricks growing 50% vs. Snowflake 29%

- Databricks raised at $100B valuation (61% jump from prior round)

- Analysts note Databricks has "easily eaten into Snowflake's warehouse revenue"

- Cloud providers (AWS, Azure, GCP) also increasingly competitive with native solutions

Snowflake's Defensive Moats

- Ease of use and cost-effectiveness as enterprise data platform

- Model-neutral AI platform approach (Gemini, Claude, open-source all integrated)

- Strong data sharing and governance capabilities

- Multi-cloud neutral positioning vs. native cloud provider tools

- 766 Forbes Global 2000 customers and 688 customers paying >$1M annually

- RPO of $7.88B (+37% YoY) provides strong revenue visibility

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the February 20 (long put) and April 17 (short put) expirations:

Bull Case (20% probability)

Target: $210-$230

How we get there:

- Broader market rally lifts all cloud software names into February

- Positive analyst commentary or price target raises ahead of Q4 earnings

- AI partnership announcements (Anthropic, Gemini) generate renewed institutional buying interest

- Short covering as bears capitulate ahead of potentially strong Q4 results

- Breakout above $200 gamma resistance triggers momentum to $210, then $220

Key metrics needed:

- Sustained close above $200 with volume

- Positive channel checks on Snowflake consumption trends

- No Databricks IPO filing before February OPEX

- Broader market cooperation (no risk-off rotation out of tech)

Probability assessment: Only 20% because the stock failed to hold gains after the Q3 beat, bearish net GEX bias creates headwinds, $200 resistance is formidable, and the growth deceleration narrative weighs on sentiment. Pre-earnings positioning typically favors de-risking, not accumulation.

Put spread P&L: Both puts expire worthless or near-worthless. Trader loses most of the $1.2M net debit.

Base Case (50% probability)

Target: $185-$200 range (DRIFT LOWER THEN STABILIZE)

Most likely scenario:

- SNOW drifts lower toward $190-$195 as pre-earnings positioning and growth deceleration fears weigh on sentiment

- $195 gamma support initially holds but weakens with repeated tests

- IV builds as Q4 earnings (March 4) approaches, benefiting the long put holder

- Stock finds support in the $185-$190 zone from longer-term value buyers

- No major catalyst to break the range before February OPEX

- Post-Feb expiration, stock stabilizes in $185-$200 range ahead of earnings

This is the diagonal put buyer's sweet spot: The $195 put moves into-the-money or stays near-the-money with elevated IV, generating significant profit on the near-term leg. The $165 short put stays comfortably out-of-the-money, decaying slowly and remaining manageable. The trader collects on both legs.

Why 50% probability: Growth deceleration is a confirmed trend (34% -> 29% -> 27%), the stock fell on a Q3 beat, $200 resistance is holding, and bearish GEX bias supports downward drift. Pre-earnings periods for high-multiple names often see defensive positioning.

Bear Case (30% probability)

Target: $165-$185 (BREAK BELOW SUPPORT)

What could go wrong:

- $195 gamma support breaks, triggering dealer hedging cascade toward $185-$190

- Databricks IPO filing surfaces, causing re-rating of cloud data platform valuations

- Leaked channel checks suggest Q4 consumption weakness or customer churn

- Broader tech selloff drags high-multiple software names lower

- Cloud spending deceleration fears (enterprise IT budget cuts)

- Microsoft bundling competitive pressure reduces new customer wins

- Pre-earnings guidance whisper numbers circulate below consensus

- GAAP net loss of $291.6M in Q3 raises profitability concerns in a higher-rate environment

Critical support levels:

- $195: Strongest gamma support - MUST HOLD or momentum accelerates bearish

- $190: Secondary gamma floor - psychological round number

- $185: Deeper structural support

- $180: Major gamma level - represents a ~9% decline from current

- $170: Near the short put strike ($165) - extreme bear scenario floor

Probability assessment: 30% because multiple bearish factors are aligning: confirmed growth deceleration, stock weakness on earnings beats, bearish GEX bias, $200 resistance overhead, and Databricks competitive threat. The diagonal put buyer clearly assigns meaningful probability to this scenario given the $6M gross position.

Put spread P&L in Bear Case:

- Stock at $185 on Feb 20: Long put worth $10.00, profit = ~$2.44/share x 8,800 = $21.5M (short put still OTM, manageable)

- Stock at $180 on Feb 20: Long put worth $15.00, profit = ~$7.44/share x 8,800 = $65.5M gain

- Stock at $195 on Feb 20: Long put worth ~$2-3 (time value), roughly breakeven on net position

Trading Ideas

Conservative: Watch and Wait for the Earnings Setup

Play: Stay on the sidelines until Q4 FY2026 earnings volatility clears around March 4, 2026

Why this works:

- Growth deceleration is a confirmed trend - no urgency to buy a stock decelerating from 34% to 27%

- The stock FELL on a Q3 earnings beat - that is a major red flag for sentiment

- Pre-earnings drift tends to be negative for high-multiple names when growth is slowing

- Implied volatility is elevated, making options expensive for new positions

- A $6M institutional put spread signals sophisticated players see near-term downside risk

- Better entry likely post-earnings after IV crush and potential pullback to $175-$185 if guidance disappoints

Action plan:

- Watch for $195 gamma support to hold or break in the next 1-2 weeks

- Monitor Databricks IPO filing news - any filing could create a buying opportunity in SNOW AFTER the initial re-rating selloff

- If Q4 earnings show growth stabilization at 27%+ with strong FY2027 guidance ($5.9B+), look for entry in the $175-$185 support zone

- Track AI revenue run rate - acceleration from $100M toward $200M+ would be the bullish catalyst the stock needs

- Set alerts at $195 (support break), $185 (potential entry zone), and $210 (bull case invalidation)

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 10-15% drawdown if pre-earnings positioning and growth concerns push the stock lower. Preserve capital for better risk/reward entry after the March 4 earnings report.

Balanced: Feb/Mar Put Calendar Spread (Ride the Pre-Earnings Vol Build)

Play: Buy a put calendar spread to profit from rising implied volatility ahead of March 4 earnings

Structure: Buy March 20 $190 puts, Sell February 20 $190 puts

Why this works:

- March expiration captures Q4 earnings (March 4) while February does not - creating a volatility term structure edge

- As March 4 approaches, March puts will gain IV faster than February puts, widening the spread value

- $190 strike is near secondary gamma support - likely to see action if the stock weakens

- Defined risk: maximum loss is the net debit paid

- Mirrors the institutional thinking behind today's diagonal - time spread that profits from volatility differential

- If SNOW sits near $190 at February expiration, the front put expires and you own the March put outright heading into earnings

Estimated P&L (adjust based on current market prices):

- Pay ~$3-4 net debit per spread

- Max profit scenario: SNOW at $190 on Feb 20 with elevated March IV = spread worth $7-9

- Max loss: Net debit paid ($3-4 per spread) if stock moves sharply away from $190

- Best case ROI: 75-125% if stock gravitates toward $190 by February OPEX

Entry timing:

- Enter within the next 1-2 weeks while volatility term structure slope is manageable

- Only enter if SNOW is trading $195-$205 (near the strike zone)

- Skip if stock already below $185 (spread already deep in-the-money, less edge)

Position sizing: Risk 2-3% of portfolio maximum. This is a volatility play, not a directional conviction trade.

Risk level: Moderate (defined risk, volatility-focused) | Skill level: Intermediate

Aggressive: Short-Dated $195/$185 Put Spread (Copy the Institutional Thesis)

Play: Buy a bearish put spread targeting a break of $195 gamma support into February OPEX

Structure: Buy Feb 20 $195 puts, Sell Feb 20 $185 puts

Why this could work:

- Directly mirrors the institutional flow - following a $6M bearish bet by sophisticated money

- $195 is the strongest gamma support - a break here triggers dealer hedging that accelerates the downside

- Bearish net GEX bias means market makers amplify downside moves

- Growth deceleration confirmed (34% -> 27%), stock fell on Q3 beat, $200 resistance overhead

- Pre-earnings anxiety typically builds 3-4 weeks before major reports

- Defined risk: $10 wide spread with known max loss

- The 8.2% implied move for February supports the possibility of a move to $185

Why this could fail (REAL RISKS):

- $195 gamma support could HOLD and bounce the stock back toward $200-$205

- Broader market rally could lift all boats, overriding the bearish thesis

- Positive Snowflake news (new partnership, analyst upgrade) could squeeze shorts

- Time decay works against you - 22 days is short, stock needs to move quickly

- If stock stays $197-$200, you lose most of the premium to theta decay

- Pre-earnings positioning is a CROWDED trade - everyone sees the same deceleration

Estimated P&L:

- Pay ~$3.50-4.50 net debit per spread

- Max profit: $5.50-6.50 per spread if SNOW below $185 at Feb 20 OPEX (120-150% ROI)

- Max loss: $3.50-4.50 per spread if SNOW above $195 (100% loss of premium)

- Breakeven: ~$191-$191.50

- Probability of max profit: ~25-30% based on implied move data

IMPORTANT WARNING - Understand these risks before entering:

- This is a DIRECTIONAL BET that requires SNOW to break below key support within 22 days

- You can lose 100% of the premium paid

- The institutional trader who put this on has a much larger portfolio and different risk tolerance

- Following institutional flow does not guarantee profit - their breakeven and time horizon differ from yours

- Consider sizing this at 1-2% of portfolio MAXIMUM

Risk level: HIGH (directional, time-limited) | Skill level: Intermediate to Advanced

Risk Factors

Do not ignore these potential landmines:

-

Growth deceleration is confirmed and accelerating: Product revenue growth has dropped every quarter - 34% (Q1) -> 30% (Q2) -> 29% (Q3) -> 27% guided (Q4). At ~15x forward revenue, SNOW is priced for durable 25%+ growth. If FY2027 guidance implies sub-25% growth, the multiple compression could be severe. The stock already FELL on a Q3 beat - the bar is rising while growth is slowing.

-

Databricks competitive threat is structural, not cyclical: Databricks growing 50% vs. SNOW 29% with NRR >140% vs. 125% and has "easily eaten into Snowflake's warehouse revenue" per analysts. A potential Databricks IPO at $100B+ could create direct valuation pressure on SNOW if the market assigns similar or lower multiples to the faster-growing competitor.

-

AI revenue is still tiny relative to the hype: AI revenue run rate hit $100M in Q3 - but that is less than 2% of $4.4B annual product revenue. While 50% of bookings are AI-influenced, converting that to actual consumed revenue is unproven at scale. The Anthropic and Gemini partnerships generate headlines but the market wants revenue proof.

-

Still GAAP unprofitable with declining near-term margins: GAAP net loss of $291.6M in Q3 and Q4 operating margin guided at 7% (down from 11% in Q3) suggests the company is investing heavily, extending the path to profitability. In a higher-rate environment, the market has less patience for unprofitable growth stories.

-

Bearish gamma positioning amplifies downside: Net GEX bias is bearish, meaning dealer hedging flows AMPLIFY price moves lower. If $195 support breaks, market maker selling could cascade the stock toward $185-$190 rapidly. The $200 resistance overhead creates a natural ceiling, trapping the stock in a bearish channel.

-

Cloud spending sensitivity: Enterprise cloud budgets face scrutiny as companies optimize AI spend. If macro conditions weaken or enterprises consolidate cloud vendors, SNOW's consumption-based model becomes a headwind rather than a tailwind - customers can reduce spending instantly by reducing queries.

-

Institutional money is positioning bearish: A $6M diagonal put spread is not a casual trade. This is a calculated institutional position targeting near-term SNOW weakness. Combined with the stock falling on a Q3 earnings beat, the signal is clear: sophisticated players see risk that the consensus is not pricing in.

-

Valuation leaves no room for error: At ~$73.9B market cap and ~15x forward revenue on 27% growth, SNOW trades at a significant premium. Any stumble - whether Q4 miss, soft FY2027 guidance, or Databricks IPO re-rating - could trigger a 15-25% correction. The consensus price target of $269 implies upside, but Evercore ISI's $170 target shows the bear case is real.

The Bottom Line

Real talk: An institutional player just put $6M into a diagonal put spread on SNOW, buying near-term $195 puts and selling longer-dated $165 puts. This is a sophisticated time spread that profits from near-term weakness while expressing confidence that the stock will not collapse to $165. The structure tells us this trader expects a pullback - not a crash - and is positioning ahead of Q4 FY2026 earnings.

What this trade tells us:

- The trader expects SNOW to trade below $195 before February 20 - that is only a 2% decline from current levels, well within the 8.2% implied move

- The $195 strike was chosen precisely at the strongest gamma support - a break here means dealer hedging accelerates the move

- The $165 short put with only 159 prior OI tells us this strike was specifically selected - they do NOT expect a catastrophic decline

- The diagonal structure (different expirations) shows they are playing the time decay differential - sophisticated, not a panic trade

- Bearish GEX bias and $200 resistance overhead support the directional thesis

- Growth deceleration from 34% to 27% and the stock falling on a Q3 beat provide fundamental backing

This is a "controlled bearish" signal - not a "sell everything" alarm.

If you own SNOW:

- Consider trimming 20-30% of your position near $200 resistance - lock in some of the 25.6% YTD gains

- Set a mental stop at $190 (secondary gamma support) if holding through the pre-earnings window

- Watch the $195 gamma level closely - if it breaks on volume, the stock could flush to $185 quickly

- If holding into Q4 earnings (March 4), understand this is a binary event with elevated risk given the growth deceleration trend

- Consider buying protective puts (Feb or Mar expiry) to hedge your stock position through earnings

If you are watching from the sidelines:

- Do NOT rush in to buy the dip at $195-$200 - institutional flow and technicals both point to more downside

- Post-earnings pullback to $175-$185 would be a much better entry with 10-15% margin of safety

- Looking for confirmation of: growth stabilization at 27%+, FY2027 guidance implying $5.9B+ revenue, AI revenue acceleration toward $200M run rate

- The Databricks IPO catalyst could create a buying opportunity if it causes an overreaction selloff in SNOW

- Long-term thesis remains intact: RPO of $7.88B (+37% YoY), model-neutral AI platform, 688 enterprise customers >$1M ARR

If you are bearish:

- The institutional diagonal put spread validates the near-term bearish thesis

- First target is $195 gamma support, then $190, then $185 if momentum builds

- Put spreads (Feb $195/$185 or Mar $190/$175) offer defined-risk bearish exposure

- Watch for $195 break on volume as your entry trigger - do not front-run the support level

- Be ready to cover if stock reclaims $205 with conviction - that would invalidate the near-term thesis

Mark your calendar - Key dates:

- January 30 (Tomorrow) - Weekly OPEX, +/-2.3% implied move

- February 20 - Monthly OPEX, $195 long put expiration - this is when the near-term leg resolves

- ~March 4, 2026 - Q4 FY2026 earnings + FY2027 guidance (THE catalyst)

- April 17 - $165 short put expiration - the financing leg resolves

- H1 2026 - Potential Databricks IPO filing (competitive/valuation catalyst)

- ~June 2026 - Q1 FY2027 earnings + Snowflake Summit 2026

Final verdict: SNOW is at an inflection point. The AI platform story is compelling - Anthropic, Gemini, Palantir partnerships, and 50% of bookings AI-influenced are real. But growth is decelerating, the stock fell on a beat, Databricks is gaining share faster, and the company is still GAAP unprofitable at a $73.9B valuation. The $6M diagonal put spread confirms what the technicals are showing: near-term risk is skewed to the downside. This does not mean Snowflake is broken - it means the risk/reward for new buyers is not favorable until we see Q4 results and FY2027 guidance in early March.

Be patient. Let earnings clarify the growth trajectory. If you want exposure, look for $175-$185 post-earnings entry with a 12+ month holding period. The data cloud revolution will still be here - you do not need to catch every tick.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The diagonal put spread described reflects institutional activity that may involve portfolio hedging strategies not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for significant gaps in either direction. The options described have specific expiration dates and strike prices that may not match your risk profile.

About Snowflake Inc.: Snowflake is a fully managed cloud data platform that consolidates data hosted on different public clouds for centralized analytics and governance. Its cloud-native architecture allows unlimited storage and compute scaling. Market cap of $73.9 billion in the Services-Prepackaged Software industry.