🛡️ SOXX $6.7M Bear Put Spread + 0DTE Premium Capture - Institutional Hedge on Semiconductors

📅 February 27, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated institutional trader just deployed a $6.7M three-legged put structure on SOXX - buying 7,000 March 20 $340 puts while simultaneously selling 7,000 March 20 $310 puts and 4,500 same-day $355 puts. The net cost after premium collected is approximately $2.4M for a bear put spread that profits if the semiconductor ETF drops 3.5-12% over the next three weeks, with today's 0DTE put sale partially financing the position. This is a textbook institutional hedge heading into a dense catalyst window: Broadcom earnings (March 4), NVIDIA GTC (March 16-19), and Micron earnings (March 18) - all while SOXX sits at 52-week highs with a 26.8x P/E.

📊 ETF Overview

iShares Semiconductor ETF (SOXX) is the go-to vehicle for broad semiconductor sector exposure:

- 🏭 What it tracks: ICE Semiconductor Index - approximately 30-35 U.S.-listed semiconductor stocks with modified cap-weighting (top 5 capped at 8%, rest at 4%)

- 💰 AUM: $22.89B

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$352

- 💎 Top Holdings: MU (8.82%), AMD (7.43%), NVDA (7.37%), AMAT (7.19%), AVGO (5.27%), QCOM (~4%), LRCX (~4%)

- 📈 YTD Return: +18.47% | 2025 Return: +41%

- 📊 P/E Ratio: 26.8x trailing

- 💵 Expense Ratio: 0.34%

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:07:19 | SOXX | MID | BUY | PUT $340 | 2026-03-20 | $6.7M | $340 | 7,000 | 330 | 7,000 | $352.55 | $9.56 | SOXX20260320P340 |

| 10:07:19 | SOXX | MID | SELL | PUT $355 | 2026-02-27 | $2.2M | $355 | 4,500 | 5,300 | 4,500 | $352.55 | $4.94 | SOXX20260227P355 |

| 10:07:19 | SOXX | MID | SELL | PUT $310 | 2026-03-20 | $2.1M | $310 | 7,000 | 81 | 7,000 | $352.55 | $3.07 | SOXX20260320P310 |

🤓 What This Actually Means

Let me break this three-legged put structure down in plain English:

Leg 1 - The Core Bet (Bought March 20 $340 Puts):

- 💸 $6.7 million spent: 7,000 contracts at $9.56 each ($9.56 x 100 x 7,000 = ~$6.69M)

- 📉 Strike $340 is 3.6% below current price - slightly out-of-the-money but close enough to become profitable on a moderate decline

- 📊 Volume/OI = 21.2x - volume is over 21 times the existing open interest of just 330 contracts. This is a completely new position, not rolling or adjusting

- ⏰ 21 days to expiration - covers the Broadcom earnings, GTC, and Micron earnings window

Leg 2 - The Financing Trade (Sold Same-Day $355 Puts):

- 💰 $2.2 million collected: 4,500 contracts at $4.94 each

- ⏰ Expires TODAY (February 27, 2026) - this is a 0DTE put sale, capturing pure time decay

- 📊 $355 strike is $2.45 above spot - slightly in-the-money, meaning the trader expects SOXX to either hold or rally into the close today, letting these expire near worthless or with minimal assignment risk

- 🤝 Purpose: Pure premium capture to reduce the cost of the bear put spread below

Leg 3 - Risk Cap (Sold March 20 $310 Puts):

- 💰 $2.1 million collected: 7,000 contracts at $3.07 each

- 📊 $310 strike is 12.1% below current price - this is deep out-of-the-money, capping the maximum downside protection

- 📊 Volume/OI = 86.4x - virtually zero prior open interest (only 81 contracts), confirming this is part of the same structured trade

- 🛡️ Purpose: Defines the floor of the bear put spread, turning an expensive outright put purchase into a cost-efficient spread

The Combined Structure:

| Component | Premium | Direction |

|---|---|---|

| Buy 7K Mar 20 $340 puts | -$6.69M | Paid |

| Sell 4.5K 0DTE $355 puts | +$2.22M | Collected |

| Sell 7K Mar 20 $310 puts | +$2.15M | Collected |

| Net Cost | ~$2.32M | Paid |

- 🎯 Max profit on the bear put spread: ($340 - $310) x 7,000 x 100 = $21M (if SOXX drops below $310 by March 20)

- 💸 Net cost after financing: ~$2.3M

- 📊 Risk/reward ratio: Risking $2.3M to potentially make $21M = roughly 9:1 payout at maximum

- 📉 Breakeven on the spread: $340 - ($2.32 net cost per spread / 100) = approximately $336.70 (4.5% below current)

- 🛡️ Max loss: The $2.3M net debit if SOXX stays above $340 at March 20 expiration

Why the 0DTE put sale is clever: The $355 puts sold for today's expiration are slightly in-the-money ($355 strike vs $352.55 spot), but with only hours left, the trader is capturing $2.2M in premium that decays to near-zero by close if SOXX doesn't collapse further. Even if assigned on some contracts, they're effectively getting long SOXX at $355 - $4.94 = $350.06, which is below current price. This is a sophisticated financing mechanism that institutional desks use to cheapen hedges.

What's the thesis here?

This trader is positioning for a 4-12% semiconductor pullback over the next three weeks. The timing is deliberate - the trade lands right before the three biggest semiconductor catalysts of Q1: Broadcom earnings on March 4, NVIDIA GTC on March 16-19, and Micron earnings on March 18. With SOXX at 52-week highs and a trailing P/E of 26.8x, this looks like an institutional portfolio hedge rather than an outright bearish bet - someone with significant long semiconductor exposure wants protection through a volatile catalyst window at a reasonable cost.

📈 Technical Setup / Chart Check-Up

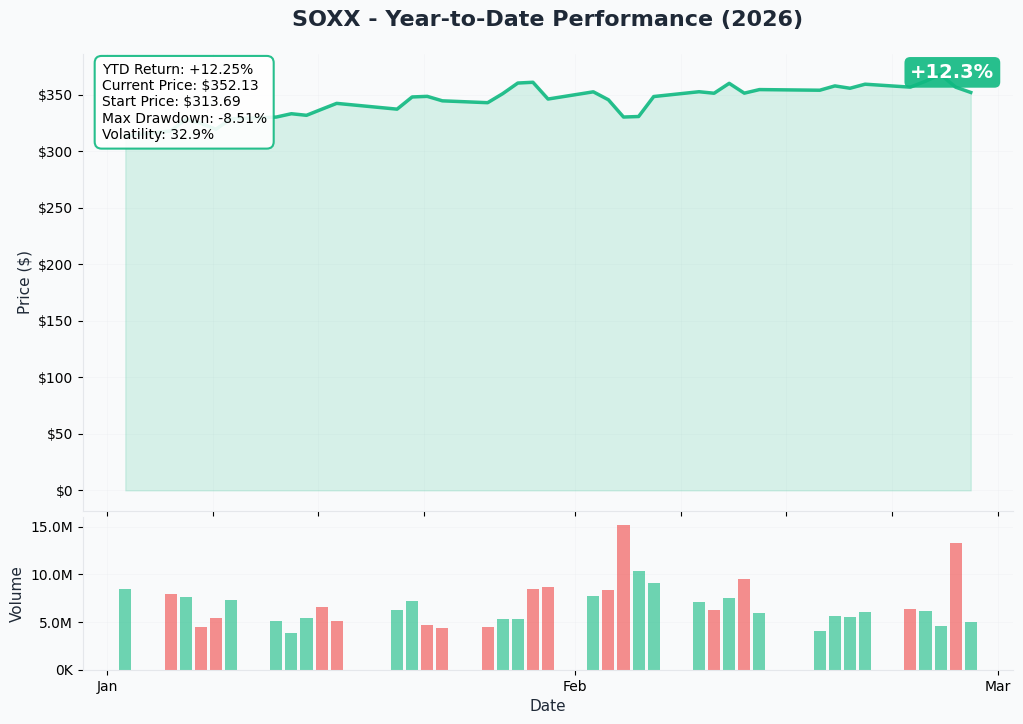

YTD Performance

SOXX is up +18.5% YTD with the current price around $352, starting 2026 near $297. The chart shows a strong uptrend with one notable pullback:

- 🚀 Steady climb: From ~$297 at the start of January to the $368.82 52-week high hit earlier today

- 📈 Well above moving averages: Trading above both the 50-day MA ($336.69) and 200-day MA ($298.40), confirming a strong bullish trend

- 📊 Institutional flows: $2.3 billion in net inflows over the past 3 months and $1.22B in the last month alone

- 🎢 DeepSeek V4 dip: The February 23 DeepSeek V4 release caused a brief pullback from the highs, but SOXX has largely recovered

- 💪 NVDA earnings lift: NVIDIA's record Q4 report on February 26 ($68.1B revenue, +73% YoY) provided a tailwind across the sector

Key takeaway: SOXX is near 52-week highs after a powerful rally driven by AI spending momentum and strong earnings across the semiconductor stack. This is precisely the type of setup where institutional investors layer on hedges - the uptrend is intact, but the risk of a pullback from extended levels is elevated, especially with three major catalysts approaching.

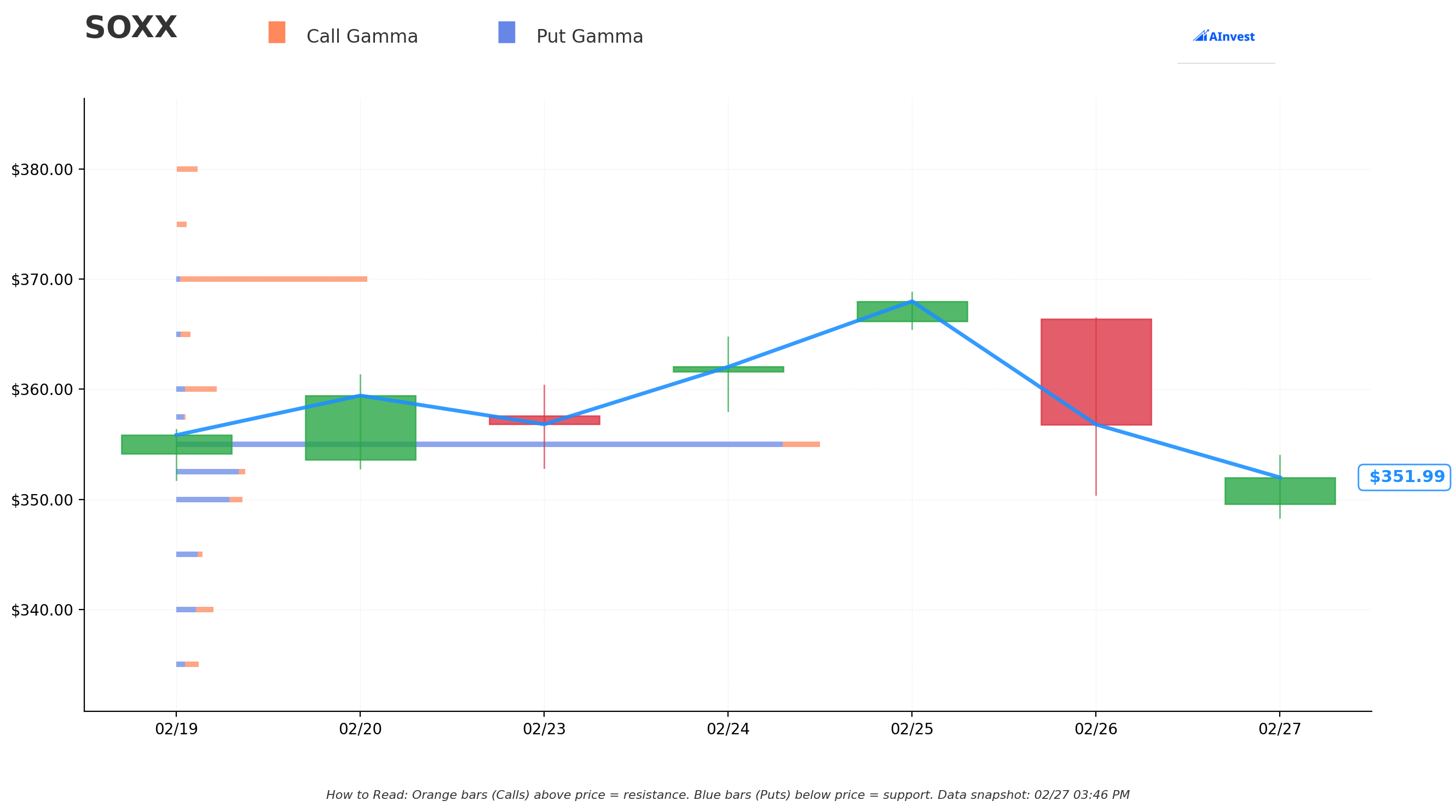

Gamma-Based Support & Resistance Analysis

Current Price: ~$352

The gamma exposure map reveals where options market makers have concentrated positions, creating natural price magnets and barriers:

🔵 Support Levels (Put Gamma Below Price):

- $350 - Strongest immediate support with 1.48B total gamma exposure (less than 1% below current - tight floor)

- $345 - Secondary support at 0.52B total gamma (1.9% below)

- $340 - Key level at 0.71B total gamma (3.3% below - THIS IS THE LONG PUT STRIKE)

- $330 - Deeper support at 0.43B gamma (6.2% below)

- $325 - Significant put gamma at 0.48B (7.6% below)

- $320 - Extended floor at 1.01B gamma (9.0% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $352.50 - Massive resistance with 4.06B total gamma (right at current price - acting as a magnet)

- $355 - Enormous resistance at 12.96B total gamma (0.9% above - THE BIGGEST GAMMA WALL ON THE BOARD)

- $360 - Moderate resistance at 0.77B gamma (2.3% above)

- $370 - Strong resistance at 3.60B gamma (5.2% above)

What this means for traders:

The gamma landscape is dominated by the massive put gamma concentration at $355, which is creating a strong magnetic effect on price. This is also the same strike as the 0DTE put that was sold - the trader clearly recognized that $355 is acting as a ceiling today. Net GEX bias is bearish, with total put gamma (24.2B) nearly three times total call gamma (8.0B). This means market makers are short puts in size, and their hedging activity will amplify moves to the downside if SOXX breaks below the $350 support zone.

The bear put spread's $340 long strike sits right at a gamma support level, and the $310 short strike is well below all significant gamma zones. If SOXX breaks below $350, the path toward $340 has relatively thin gamma support at $345, meaning a quick 2-3% down move is possible without much resistance.

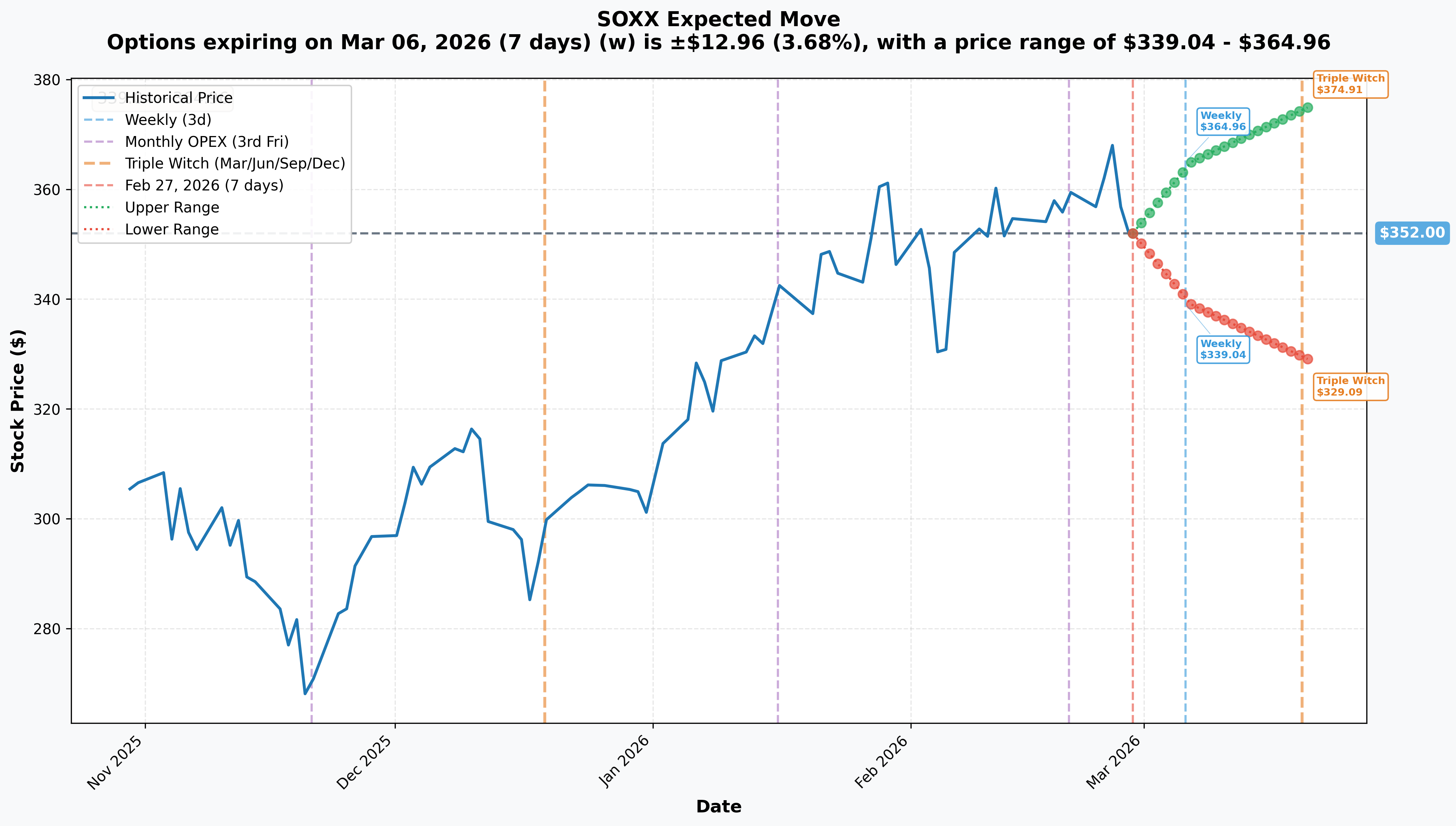

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 7 days): ±$12.96 (±3.68%) --> Range: $339.04 - $364.96

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 21 days): ±$22.91 (±6.51%) --> Range: $329.09 - $374.91

Translation:

The options market expects SOXX could move ±6.51% by the March 20 OPEX - the exact expiration of this bear put spread. The implied lower range of $329.09 sits between the spread's long strike ($340) and short strike ($310), meaning the market views a drop to $340 as well within the expected distribution. A decline to $310 would require a move beyond the implied range - possible but statistically unlikely (roughly a 1-standard-deviation overshoot).

Key insight: The bear put spread's $340 long strike is within the implied move lower bound. This means the trader is NOT making an extreme bet - they're positioning for a move the options market considers quite plausible. The $310 floor simply caps risk for an improbable scenario. This is a measured, institutional-grade hedge.

🎪 Catalysts

🔥 Upcoming Catalysts (Why the March 20 Expiration Matters)

The next three weeks contain the densest cluster of semiconductor catalysts in Q1 2026. This is exactly the window this hedge covers.

Broadcom Q1 FY2026 Earnings - March 4, 2026 (After Market Close) 📊

AVGO is SOXX's 5th largest holding at 5.27%. Consensus expects $19.1B revenue (+28% YoY) with AI revenue doubling to $8.2B. Key risk: gross margin compression of ~100 bps QoQ due to higher AI mix. Broadcom sets the tone for the entire AI semiconductor demand narrative. A miss here could send SOXX lower before the bigger events later in March.

Morgan Stanley TMT Conference - March 2-5, 2026 📢

Multiple semiconductor companies presenting at this major industry conference in San Francisco. Forward-looking commentary on AI demand, order books, and pricing could move the sector.

NVIDIA GTC 2026 - March 16-19, 2026 (San Jose) 🤖

This is the marquee semiconductor event of the quarter. CEO Jensen Huang promised to "unveil chips the world has never seen before" - expected announcements include Vera Rubin GPU architecture details (TSMC 3nm, HBM4), Blackwell Ultra GB300 deployment updates, and a Feynman architecture preview. GTC historically moves SOXX ±3-5%. A "sell the news" reaction after the recent 52-week highs is the kind of scenario this hedge protects against.

Micron Q2 FY2026 Earnings - March 18, 2026 📊

MU is SOXX's largest holding at 8.82%. Guidance calls for ~$18.7B revenue with 67% gross margin. Key watches: HBM4 ramp progress, DRAM pricing, and data center mix. Given MU's outsize weighting, any disappointment here disproportionately impacts the ETF. Memory stocks are historically the most cyclical segment of semiconductors - and 67% gross margin may be the cycle peak.

March 20, 2026 = TRIPLE WITCH OPEX 🧙

This isn't just a regular monthly expiration - it's quarterly triple witching (stock options + index options + index futures all expiring simultaneously). Triple witch sessions typically see elevated volatility and significant index rebalancing flows. The added turbulence of massive option expiration on top of the earnings/GTC catalyst window creates the perfect environment for a hedging trade.

✅ Recent Catalysts (Already Happened)

NVIDIA Q4 FY2026 Earnings Beat - February 26, 2026 📊

Record Q4 revenue of $68.1B (+73% YoY), data center revenue $62.3B (+75% YoY). Q1 FY2027 guidance of $78.0B was strong but notably excluded China Data Center compute revenue. Full fiscal year 2026 revenue was $215.9B (+65% YoY). The beat was already largely priced in given the recent rally to 52-week highs.

DeepSeek V4 Release - February 23, 2026 🤖

DeepSeek launched V4, renewing concerns about AI capex sustainability. The original DeepSeek shock in January 2025 sent SMH down ~10% in a single session. While 2025 spending ultimately did not slow, the pending R2 model release (delayed by Huawei Ascend chip difficulties) remains an overhang.

AMD Q4 2025 Record Results - February 3, 2026 📊

AMD (7.43% of SOXX) reported record Q4 revenue of $10.3B, data center segment $5.4B (+39% YoY). But China Instinct MI308 sales dropped from $390M to an expected $100M in Q1 due to export restrictions - a reminder that policy risk is real.

Section 232 Semiconductor Tariffs - January 15, 2026 🏛️

The 25% tariff on advanced computing chips is currently narrowly scoped with broad exemptions, but the White House stated it "may consider imposing significant tariffs on imports of semiconductors, semiconductor manufacturing equipment, and their derivative products." Escalation risk persists.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the catalyst calendar, here are the scenarios through the March 20, 2026 expiration:

📈 Bull Case (35% probability)

SOXX Target: $360-$375

How we get there:

- 🚀 Broadcom beats on AI revenue, raises guidance

- 💪 GTC delivers Vera Rubin excitement and new hyperscaler commitments

- 📊 Micron posts blowout numbers, guides HBM4 ramp ahead of schedule

- 📈 SOXX breaks through $355 gamma wall and rallies toward $370 resistance

- 🤖 Hyperscaler capex commitments of $660-690B continue to accelerate

Bear put spread P&L: Spread expires worthless. Loss = -$2.3M (100% of net debit). The 0DTE $355 put sale already collected $2.2M, so the total capital at risk on the residual bear put spread is relatively small for an institutional portfolio.

🎯 Base Case (40% probability)

SOXX Target: $340-$360 range

Most likely scenario:

- ✅ Broadcom and Micron meet expectations without major surprises

- 📊 GTC generates excitement but markets sell the news after the recent run

- ⚖️ SOXX consolidates around the $350 area, digesting the 18.5% YTD gain

- 🔄 Normal volatility around triple witch creates temporary dips but no sustained selloff

- 📉 Brief pullback to $340-345 gamma support before recovering

Bear put spread P&L at $340: Spread at max value on the long leg ($340 put at-the-money), but with the short $310 leg still far OTM, net spread value ~$9.56. After subtracting $2.32 net cost, profit = ~$5.0M per contract scaling (varies by SOXX closing level).

Bear put spread P&L at $350: Long $340 put still OTM, spread worth minimal. Small loss or near breakeven depending on residual time value.

📉 Bear Case (25% probability)

SOXX Target: $310-$335

What could go wrong:

- 😰 Broadcom misses on AI revenue, margin compression worse than expected

- 📉 GTC "sell the news" event after SOXX already at 52-week highs

- 🚨 Micron signals memory cycle peak - HBM4 ramp creates oversupply concerns

- 🏛️ Section 232 tariff escalation to broader semiconductor imports announced

- 🤖 DeepSeek R2 release triggers another AI capex repricing event

- 📊 Triple witch amplifies selling pressure, SOXX breaks through $340 support

- 🌍 China export controls tighten - bipartisan push for blanket equipment bans

Bear put spread P&L at $320: Long $340 put worth $20, short $310 put worth -$0 (still OTM). Spread worth $20. Net profit = ($20 - $3.31 net cost per contract) x 7,000 x 100 = ~$11.7M gain.

Bear put spread P&L at $310 or below: Max payout. Spread worth $30. Net profit = ($30 - $3.31) x 7,000 x 100 = ~$18.7M gain.

This is the scenario where the hedge pays off handsomely - a 10%+ correction in semiconductors during a packed catalyst window with triple witch amplification.

💡 Trading Ideas

🛡️ Conservative: "Hedge Your Chips" - March 20 Bear Put Spread

Play: Buy the SOXX March 20 $345 puts, sell the March 20 $325 puts

Structure: $345/$325 bear put debit spread, 21 days to expiration

Why this works:

- 📊 Follows the institutional thesis at a tighter, more cost-efficient strike width

- 🛡️ Defined risk: max loss is the net debit paid (roughly $7-9 per spread)

- 💰 Max profit: $20 per spread minus debit paid (~$11-13 gain) if SOXX below $325 at expiry

- ⏰ Captures the same catalyst window (Broadcom, GTC, Micron, triple witch)

- 📈 The $345 strike is only 2% below current price - starts profitable on even a modest decline

- 📉 The $325 level aligns with significant put gamma support (0.48B)

Position sizing: Risk no more than 2-3% of portfolio. 10 spreads at ~$8 each = ~$8,000 risk for ~$12,000 max profit.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

⚖️ Balanced: "Catalyst Calendar Collar" - Protect Long SOXX Shares

Play: If you already own SOXX shares, buy a March 20 $340 put and sell a March 20 $370 call per 100 shares

Why this works:

- 🎯 Protects against the downside catalyst risk without selling your long position

- 💸 The $370 call premium partially offsets the $340 put cost, reducing net outlay

- 📊 $370 matches the gamma resistance level - SOXX likely needs a significant catalyst to reach it

- ⏰ 21-day duration perfectly covers the Broadcom/GTC/Micron/triple witch window

- 🛡️ After March 20, you can reassess and remove the hedge if the catalysts pass without incident

- 📈 Still participate in upside to $370 (a 5.2% gain from here) before the call caps further upside

Position sizing: 1 collar per 100 shares of SOXX you own. Net cost: approximately $3-5 per share depending on timing.

Risk level: Low (protective hedge on existing position) | Skill level: Intermediate

🚀 Aggressive: "GTC Gamma Fade" - March Weekly Put Spread

Play: Buy the SOXX March 20 $350 puts, sell the March 20 $335 puts - entered the day BEFORE GTC (March 15)

Why this works (and why it's risky):

- 💥 Targets the "sell the news" risk after GTC - semiconductor stocks often fade after big announcements when expectations are already elevated

- 📊 GTC (March 16-19) + Micron earnings (March 18) + triple witch (March 20) = maximum volatility potential in a single week

- 🎯 $350 strike aligns with strongest gamma support - a break below triggers dealer hedging flows that accelerate the move

- 📉 If SOXX drops 5% post-GTC, the spread pays roughly $10 on a $6-7 debit (50%+ return)

- ⏰ Only 5 days of time decay if entered March 15 - efficient premium usage

Why it could blow up:

- 🚀 GTC could deliver genuinely surprising announcements (Vera Rubin specs, new partnerships) that send SOXX higher

- 📈 Micron beat + raise could negate any GTC selloff

- ⏰ Only 5 days means zero margin for error on timing

- 💸 IV crush post-event could erode spread value even if direction is correct

Position sizing: Risk ONLY what you can afford to lose completely. 20 spreads at ~$6-7 each = ~$12,000-$14,000 at risk for ~$16,000-$18,000 max profit.

Risk level: HIGH (short timeframe, event-dependent) | Skill level: Advanced

⚠️ Risk Factors

Key risks to keep in mind whether you follow this trade or not:

-

📉 This is likely a HEDGE, not a directional bet. The structure (bear put spread financed by 0DTE premium) is a classic institutional hedging pattern. The trader likely holds a significant long semiconductor portfolio and is buying insurance through the catalyst window. Following this trade as a standalone bearish bet changes the risk profile entirely - you'd be speculating where they're hedging.

-

🚀 SOXX could rip higher through the $355 gamma wall. The $660-690B in hyperscaler capex commitments for 2026 is the most powerful demand driver in technology. If Broadcom, GTC, and Micron all deliver positive surprises, SOXX could break through $355 resistance and sprint toward $370-$375, making the bear put spread worthless.

-

🤖 DeepSeek R2 is the wild card. The pending R2 model release has been delayed by Huawei Ascend training difficulties, but if it drops during the March catalyst window, it could trigger another AI capex repricing event similar to the January 2025 shock that sent SMH down ~10% in a day. This would be a windfall for the bear put spread.

-

🏛️ Tariff escalation remains a live risk. The White House explicitly stated broader semiconductor tariffs are under consideration. A surprise announcement during the March window would hit SOXX holdings that import chips from Taiwan, South Korea, and other Asian fabs. The U.S.-Taiwan $250B trade agreement provides some buffer but doesn't eliminate the risk.

-

📊 Valuation is stretched at 26.8x trailing P/E. After +18.5% YTD and +41% in 2025, SOXX prices in substantial growth. Any earnings shortfall from a top holding (MU at 8.82%, AMD at 7.43%, NVDA at 7.37%) could trigger a meaningful drawdown. The semiconductor industry's path to $1 trillion is widely expected - which means it's largely priced in.

-

⚖️ The 0DTE leg carries assignment risk. The sold $355 puts that expire today are slightly in-the-money. If SOXX closes below $355, some portion of the 4,500 contracts could be assigned, requiring the trader to buy SOXX shares at $355. For an institutional desk this is manageable, but retail traders should understand that selling in-the-money same-day options is not a beginner strategy.

-

🌍 Taiwan geopolitical tail risk. TSMC produces >90% of the world's most advanced chips. A quarantine or military action in the Taiwan Strait would be catastrophic for the entire semiconductor supply chain. TSMC's geographic diversification (U.S., Japan, Germany fabs) won't meaningfully reduce concentration before 2028-2029. This is the ultimate downside scenario for SOXX.

-

💾 Memory cycle peak risk at Micron. MU is SOXX's largest holding at 8.82%, and its 67% gross margin guidance may represent the cycle peak. Memory is historically the most cyclical semiconductor segment. If HBM4 ramp creates oversupply by late 2026 or DRAM pricing peaks sooner than expected, Micron could see significant multiple compression.

🎯 The Bottom Line

Here's the deal: A sophisticated institutional player just spent a net $2.3 million to buy downside protection on the semiconductor sector through the most catalyst-dense three weeks of Q1 2026. The structure - a bear put spread financed by same-day premium capture - is textbook risk management, not a panic trade.

What this trade tells us:

- 🎯 Smart money sees enough risk in the March catalyst window (Broadcom, GTC, Micron, triple witch) to spend seven figures on protection

- 📊 They chose SOXX rather than hedging individual names, suggesting broad sector risk concern rather than single-stock worry

- 💰 The 9:1 risk/reward structure (risking $2.3M to potentially make $21M) shows they view a pullback as a tail scenario worth insuring against, not a base case

- 🤝 The MID fills on all three legs and the three-legged structure confirm this is institutional - retail traders don't execute multi-million-dollar calendar structures at the midpoint simultaneously

- 📉 The $340 strike (3.5% below current) is within the implied move range, meaning the options market itself considers a move to this level quite plausible

If you're long semiconductors:

- ✅ This is a reminder to review your own hedging posture before March 4 (Broadcom earnings)

- 📊 The $350 gamma support is your near-term floor - set alerts if SOXX breaks below

- 🛡️ A collar strategy (long put + short call on existing shares) is the cleanest hedge through the catalyst window

- 📅 Mark March 4, March 16-19, and March 18 as key risk dates

If you're considering semiconductor exposure:

- 🎯 Waiting until after triple witch (March 20) may provide a better entry point

- 📊 The implied move lower range of $329 for the March 20 OPEX would represent a 6.5% pullback - a reasonable buyable dip if fundamentals remain intact

- 📈 The $1 trillion industry milestone and $660-690B hyperscaler capex remain powerful secular tailwinds

If you're bearish on semiconductors:

- ⚠️ Be careful betting against the strongest sector in the market with massive institutional inflows ($2.3B in 3 months)

- 📉 If you want to play the downside, use defined-risk spreads (like the institutional trader did) rather than outright put purchases

- ⏰ The GTC "sell the news" setup on March 16-19 is your highest-probability entry if you believe the sector is overextended

Key dates to mark:

- 📅 March 2-5, 2026 - Morgan Stanley TMT Conference (sector commentary)

- 📅 March 4, 2026 - Broadcom Q1 FY2026 earnings (after market close)

- 📅 March 16-19, 2026 - NVIDIA GTC 2026 (marquee AI/chip event)

- 📅 March 18, 2026 - Micron Q2 FY2026 earnings (largest SOXX holding)

- 📅 March 20, 2026 - TRIPLE WITCH OPEX - this trade expires

Final verdict: This is one of the most well-constructed hedging trades we've seen on the tape this week. The trader isn't predicting a semiconductor crash - they're insuring against one at an acceptable price during a high-risk window. The 9:1 payout structure means even a small allocation to this hedge can offset meaningful losses on a larger long portfolio. For retail traders, the takeaway isn't to copy this exact trade - it's to recognize that when institutions spend millions on protection at 52-week highs, the smart move is to at least review your own risk management. The semiconductor AI story remains intact, but the next three weeks will stress-test it.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Multi-leg option structures carry unique risks including assignment risk on short legs. Always do your own research and consider consulting a licensed financial advisor before trading.

About iShares Semiconductor ETF: SOXX tracks the ICE Semiconductor Index, providing exposure to approximately 30-35 U.S.-listed semiconductor companies across the compute, memory, equipment, and analog/mixed-signal value chain, with $22.89B in assets under management and a 0.34% expense ratio.