🎵 SPOT: $5M Whale Accumulating March 2026 Calls - Spotify's Audiobook Gamble!

📅 December 9, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $5 MILLION in Spotify March 2026 $560 calls across two massive trades this morning! This is smart money closing previous positions (likely unwinding shorts) while the stock sits at $590, just days before December monthly OPEX and months before Q4 earnings on February 10, 2026. With US price hikes confirmed for Q1 2026 and the co-CEO transition happening January 1, institutional players are making their move.

🏢 Company Overview

Spotify Technology S.A. (NYSE: SPOT) is the world's leading music streaming service provider, dominating the audio streaming landscape with over 700 million monthly active users and 280 million paying subscribers. Beyond music, Spotify has aggressively expanded into podcasts and audiobooks, creating a multi-format platform strategy that competitors can't easily replicate.

Key Stats:

- 💰 Market Cap: $117.84 billion

- 👥 Employees: 7,691

- 📆 IPO Date: April 3, 2018

- 🌍 Business Model: Premium subscriptions ($11.99/month) + ad-supported free tier

- 🎧 Industry: Streaming audio platforms / digital entertainment

The company transformed from a perennial money-loser to posting its first full-year profit in 2024 with €1.5 billion in operating income. Now trading near all-time highs, Spotify is betting that price increases, audiobook adoption, and AI-powered discovery can drive margins even higher.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the institutional money printing trades that caught our eye:

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Spot Price | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-09 | 10:55:35 | SPOT | BUY | CALL | 2026-03-20 | $560 | 734 | $3.4M | $589.99 | $70 |

| 2025-12-09 | 10:31:56 | SPOT | BUY | CALL | 2026-03-20 | $560 | 233 | $1.6M | $587.65 | $69 |

Total Premium Deployed: $5.0 MILLION 💸

View Live Chart: SPOT March 2026 $560 Calls

🤓 What This Actually Means

Translation for us regular folks: This is a "Buy to Close" position - meaning someone who was SHORT these calls is now buying them back to exit. But here's the twist: 734 contracts traded when open interest is only 777 contracts. That's 94.5% of all existing contracts changing hands!

The Z-Score tells the story:

- First trade: Z-Score of 1.28 (Above Average)

- Second trade: Z-Score of 4.63 (Extremely Unusual) 🚨

This isn't some random retail degen. This is institutional positioning ahead of multiple catalysts: Q4 earnings (Feb 10), leadership transition (Jan 1), and US price hikes (Q1 2026).

What makes this interesting:

- 📈 Strike is $560 vs current price $590 → These are IN-THE-MONEY calls

- 📆 Expiration March 20, 2026 → 101 days out (captures Q4 earnings + price hike impact)

- 💵 Paying $70 per contract when stock is $590 → Essentially $30 premium for 3+ months of exposure

- 🎯 Strategy Type: Standalone (not part of spread - pure directional bet)

The buyer is betting Spotify stays above $630 at expiration to profit (strike $560 + premium $70 = breakeven $630). With analyst price targets averaging $761, there's room to run! 🚀

📈 Technical Setup / Chart Check-Up

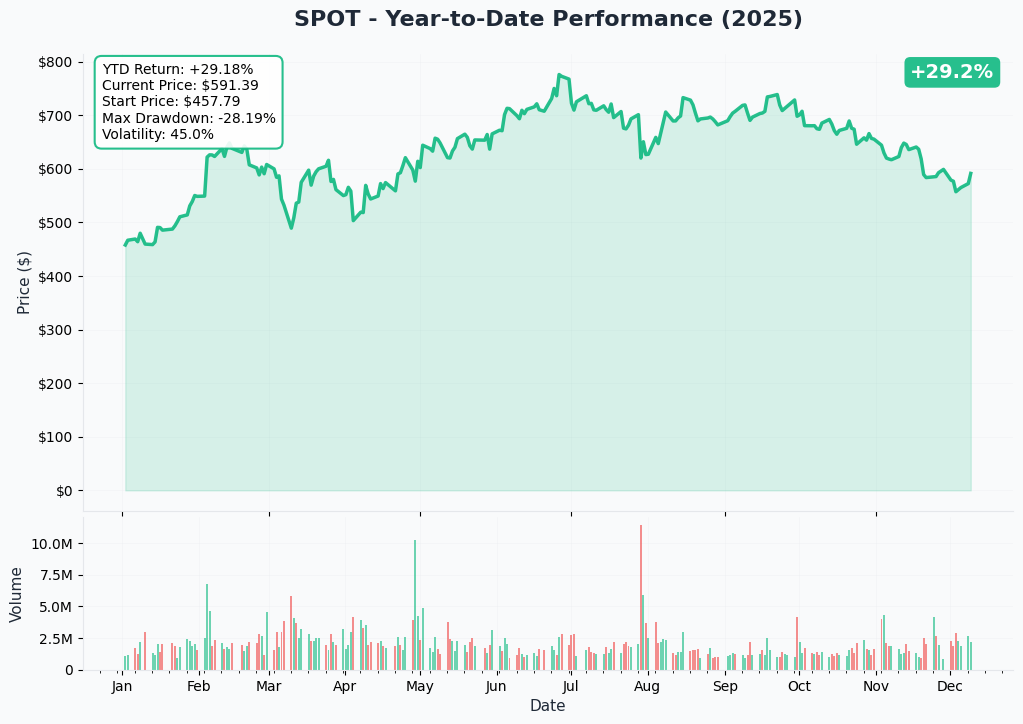

YTD Chart Analysis

Real talk: SPOT has been on an absolute tear in 2025. The stock bottomed around $421 in early 2025 and exploded to current levels near $590 - that's a 40% gain year-to-date! The rally accelerated after:

- ✅ Q3 2025 earnings beat (November 4) - surpassed 700M MAUs

- ✅ Audiobook expansion momentum in German markets (April 2025)

- ✅ Spotify Wrapped 2025 viral moment (December 3-4)

The chart shows a clear uptrend with higher lows, and the stock just consolidated around $580-600 range for the past few weeks. This sideways action after a big run? Classic setup for the next leg higher (or a rollover if catalysts disappoint).

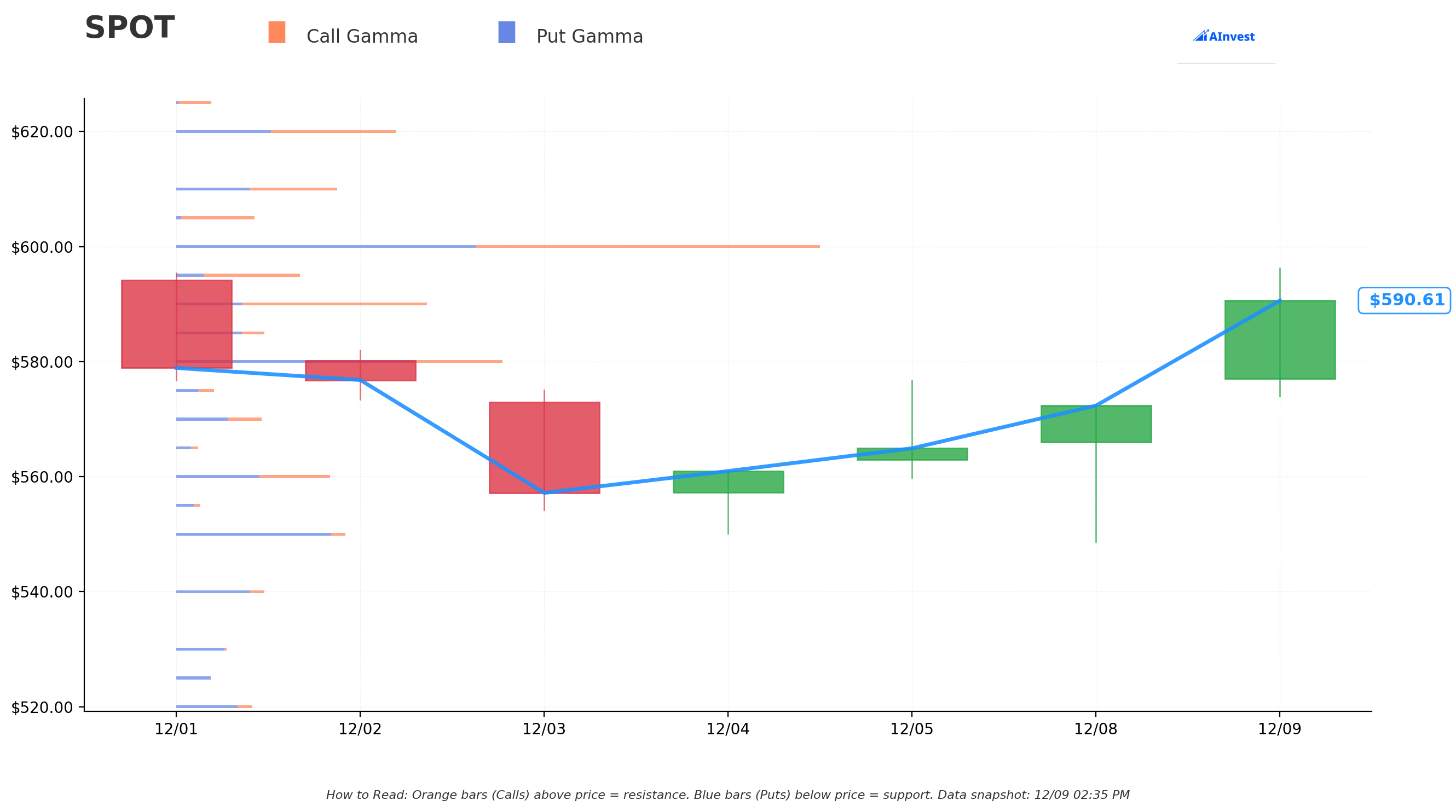

🎯 Gamma-Based Support & Resistance Analysis

What the options market is telling us:

The gamma exposure analysis shows critical price magnets where market makers need to hedge. Think of these like invisible force fields that pull the stock price:

Key Resistance Levels (Orange Bars = Call Gamma):

- 🔶 $600 → MASSIVE resistance with 3.78 GEX (biggest level on the board)

- This is THE line in the sand - stock needs to reclaim $600 to unlock upside

- Distance: Just 1.64% away

- 🔶 $630 → Strong resistance at 1.69 GEX

- Distance: 6.72% away

- This is where our whale's breakeven sits! 👀

- 🔶 $650 → Moderate resistance at 0.94 GEX

- Distance: 10.1% away

- Bull case target for March expiration

Key Support Levels (Blue Bars = Put Gamma):

- 🔵 $590 → Current price with 0.70 net GEX (slight bullish skew)

- 🔵 $580 → Major support with 1.93 total GEX (biggest support)

- Distance: 1.75% below

- This is the floor - break this and we're in trouble

- 🔵 $560 → Secondary support at 0.91 GEX

- Distance: 5.14% below

- Notice this is exactly where our whale bought calls! Not a coincidence 😏

- 🔵 $550 → Deep support at 1.00 GEX

- Distance: 6.83% below

- Bear case floor

Net GEX Summary:

- Total Call GEX: 14.03 (resistance above)

- Total Put GEX: 11.48 (support below)

- Net Bias: BULLISH with more call exposure

What this means: The options market is slightly skewed bullish, but that $600 wall is THICC. Once we break through, there's not much resistance until $630-650. Conversely, $580 is the critical support - lose that and we could flush to $560 quickly.

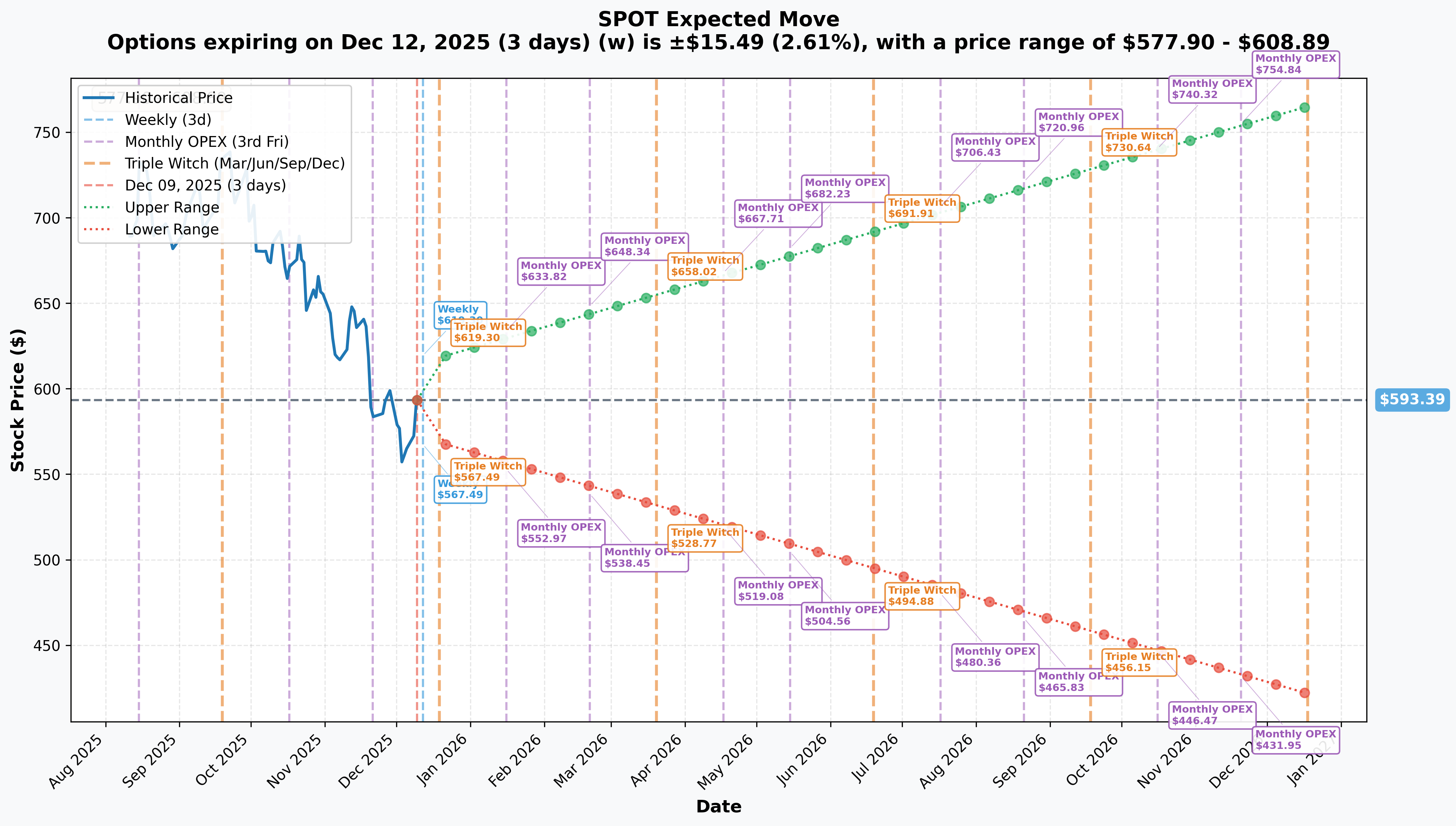

📊 Implied Move Analysis

The market's crystal ball (aka what options are pricing in):

Weekly OPEX (December 12 - This Friday!):

- 📉 Implied Move: ±2.61% (±$15.49)

- 📈 Upper Range: $608.89

- 📉 Lower Range: $577.90

- ✅ Reliability: HIGH

Monthly OPEX / Quarterly Triple Witch (December 19):

- 📉 Implied Move: ±4.23% (±$25.10)

- 📈 Upper Range: $618.49

- 📉 Lower Range: $568.30

- ✅ Reliability: HIGH

March 2026 OPEX (When our whale's calls expire!):

- 📉 Implied Move: ±10.76% estimated from spot price

- 📈 Upper Range: $658.02

- 📉 Lower Range: $528.77

- 🎯 This gives our whale nearly 100-point range to work with!

Yearly LEAPS (December 2026):

- 📉 Implied Move: ±28.97% (±$171.93)

- 📈 Upper Range: $765.33 (right in line with analyst targets!)

- 📉 Lower Range: $421.46

Translation: The market expects Spotify to stay choppy near-term (±4% by Dec 19), but is pricing in BIG moves by March 2026. That whale bet on $560 calls makes sense - even the implied move suggests $658 upside is possible by March expiration! 📈

🎪 Catalysts: What's Coming & What Just Happened

🚀 Upcoming Catalysts (Why This Trade Makes Sense)

1. Q4 2025 Earnings - February 10, 2026 (CONFIRMED) 📊

- Date: February 10, 2026, Before Market Open

- Consensus Estimates:

- 💰 Revenue: €4.5B (13% growth)

- 📈 EPS: $3.12

- 👥 Subscribers: 289M

- 🌍 MAUs: 745M

- Why it matters: First look at holiday season performance, Spotify Wrapped impact, and audiobook adoption metrics

- Catalyst Impact: 🔥🔥🔥 CRITICAL - Could send stock to $650+ on beat or $550 on miss

2. Co-CEO Leadership Transition - January 1, 2026 (CONFIRMED) 👔

- What's changing: Daniel Ek → Executive Chairman, Alex Norström & Gustav Söderström → Co-CEOs

- Why it matters: Designed to sustain execution at scale while reducing key-person risk

- Market reaction: Could be bullish (shows management depth) or bearish (uncertainty about new leadership)

- Catalyst Impact: ⚡ MODERATE - Watch for any early hiccups or smooth handoff

3. US Premium Price Hike - Q1 2026 (HIGH PROBABILITY) 💵

- Expected Timeline: As early as Q1 2026

- Potential Pricing: Individual plan from $11.99 → $12.99+

- Revenue Impact: Each $1 increase = ~$260M annual revenue (280M subscribers × $12)

- Historical Context: Previous price hikes in 2023 ($9.99→$10.99) and 2024 ($10.99→$11.99) showed minimal churn

- Why it matters: Third price increase in 3 years could test consumer patience OR prove Spotify's pricing power

- Catalyst Impact: 🔥🔥 HIGH - Directly impacts ARPU and margin expansion story

4. Q1 2026 Earnings - Late April/Early May 2026 📈

- Expected Timeline: April 29-30, 2026 (based on historical pattern)

- Key Metrics:

- First full quarter showing US price hike impact

- ARPU acceleration (currently €4.85, could hit €5.20+)

- Subscriber retention post-price increase

- Co-CEO performance report card

- Why it matters: This is when we'll know if the price increase worked without killing growth

- Catalyst Impact: 🔥🔥🔥 CRITICAL - Our whale's calls expire March 20, just before this

5. Audiobook Expansion Milestones (Ongoing) 📚

- Current Performance:

- Audiobooks+ users increased consumption 18% within first 30 days

- 36% YoY growth in people starting audiobooks

- Now available in 14 global markets with 500,000+ titles

- Why it matters: This is Spotify's differentiation vs Apple/Amazon - multi-format platform

- Catalyst Impact: ⚡ MODERATE - Slow burn story, but adds up over time

✅ Recent Catalysts (What Already Happened)

1. Q3 2025 Earnings Beat - November 4, 2025 💚

- Results:

- Subscribers: 281M (up 12% YoY) ✅

- MAUs: 713M (up 11% YoY, crossed 700M milestone) ✅

- Revenue: €4.3B (up 12% constant currency) ✅

- Operating Income: €582M (record profitability) ✅

- Stock Reaction: Rallied from ~$550 → $600 range

- Takeaway: Business is firing on all cylinders 🚀

2. Spotify Wrapped 2025 - December 3-4, 2025 🎉

- What happened: Annual viral marketing moment with 12 brand new AI features

- Reach: 184 markets worldwide

- Why it matters: Drives user engagement, app downloads, and social media buzz

- Impact: Positive brand momentum heading into Q4 close

3. Q4 2024 Full-Year Profitability - February 4, 2025 🎯

- Historic Milestone: First-ever full-year profitable year

- FY 2024 Net Income: €1.138B (vs €505M loss in 2023)

- FY 2024 Operating Profit: €1.5B (hit target!)

- Why it mattered: Validated transformation from growth-at-all-costs to sustainable business

- Stock Reaction: Multiple expansion - market started valuing as profitable tech vs money-losing growth stock

4. Spotify Partner Program Launch - January 2, 2025 💰

- What happened: Creator monetization program launched in US, UK, Canada, Australia

- Enrollment: 65%+ of eligible shows already enrolled

- Why it matters: Keeps creators on platform, drives video podcast growth (up 54% YoY)

- Impact: Sticky creator ecosystem = competitive moat

🎲 Price Targets & Probabilities

Using Gamma Levels + Implied Move + Catalyst Analysis:

🐂 Bull Case: $650-680 by March 2026 (35% probability)

Path to Victory:

- ✅ Q4 earnings beat on February 10 (subscriber growth continues, ARPU improves)

- ✅ US price hike announced in January with minimal pushback

- ✅ Co-CEO transition goes smoothly, no leadership drama

- ✅ Break through $600 gamma resistance → opens path to $630 → $650

Key Levels:

- $630 - Whale breakeven + gamma resistance = first target

- $650 - Major gamma resistance + top of implied move range

- $680 - Analyst average target approaching

What needs to happen: Beat earnings + prove pricing power + market stays risk-on for growth stocks

🎯 Base Case: $580-620 Range (45% probability)

Most Likely Scenario:

- 📊 Q4 earnings meet expectations (no major surprises)

- 💵 Price hike announced but muted reaction (priced in)

- 📈 Stock consolidates between gamma support ($580) and resistance ($600-620)

- ⚖️ Implied move plays out: choppy trading with occasional breakouts

Key Levels:

- $580 - Major gamma support (floor)

- $590-600 - Trading range (current consolidation)

- $620 - Upper resistance before breakout

What needs to happen: Status quo execution + no macro shocks

🐻 Bear Case: $520-560 (20% probability)

Path to Pain:

- ❌ Q4 earnings disappoint (subscriber churn accelerates)

- ❌ Price hike backlash → cancellations spike

- ❌ Co-CEO transition creates uncertainty or strategic shifts

- ❌ Break below $580 support → accelerates to $560 → $550

Key Levels:

- $560 - Whale's strike price = major support

- $550 - Deep gamma support

- $520 - Bottom of March implied move range

What needs to happen: Execution missteps + competitive pressure + macro risk-off

Note: Even in bear case, the whale's $560 calls have intrinsic value if stock stays above $560! That's the beauty of buying ITM calls vs OTM lottery tickets. 🛡️

💡 Trading Ideas

🛡️ Conservative: "Sleep Well at Night" Strategy

The Play: Ride the analyst upgrades and wait for $600 breakout

- 📈 Stock Entry: Buy SPOT shares at current levels ($590)

- 🎯 Price Target: $650 by March (10% gain)

- 🛑 Stop Loss: $570 (below key support)

- ⏰ Time Horizon: 3-6 months

Why this works:

- No options risk (theta decay, volatility crush)

- Company fundamentals are solid (profitable, growing, raising prices)

- Analyst consensus target $761 gives 29% upside over 12 months

- If you're wrong, you own a quality business, not worthless options

Who this is for: Long-term investors who want Spotify exposure without complexity

⚖️ Balanced: "Copy the Whale" (with a twist)

The Play: Debit spread to reduce cost

- 📞 Buy: March 2026 $580 calls @ ~$50 ($5,000 per contract)

- 📞 Sell: March 2026 $650 calls @ ~$25 ($2,500 per contract)

- 💰 Net Cost: $25 per spread ($2,500 total)

- 💵 Max Profit: $45 per spread ($4,500 total) if stock ≥ $650

- 📊 Return: 180% if stock hits $650 (vs current $590)

Breakeven: $605 at expiration (just 2.5% above current price)

Why this works:

- Cheaper than buying naked calls (cut cost in half)

- Still gives you $70 of upside per spread ($650 - $580)

- Captures the February 10 earnings move

- If stock consolidates at $620-630, you're profitable

Risk Management:

- Max loss: $2,500 (your debit paid)

- Consider closing early if stock hits $640+ before earnings (lock in 140%+ gains)

- Roll up the short call if stock explodes past $650

Who this is for: Swing traders with moderate risk tolerance and $2,500+ to deploy

🚀 Aggressive: "YOLO with Training Wheels"

The Play: ATM call spread with binary earnings bet

- 📞 Buy: February 2026 $590 calls @ ~$40 ($4,000)

- 📞 Sell: February 2026 $630 calls @ ~$22 ($2,200)

- 💰 Net Cost: $18 per spread ($1,800 total)

- 💵 Max Profit: $22 per spread ($2,200) if stock ≥ $630

- 📊 Return: 122% if stock hits $630

Breakeven: $608 at February expiration (captures Q4 earnings on Feb 10!)

Why this is the aggressive play:

- Expires February 20 (10 days after earnings) - pure catalyst play

- Cheaper than March expiration (less time value)

- $630 target is realistic on earnings beat (6.8% move)

- Risk/reward: Risk $1,800 to make $2,200

Risk Management:

- This is a binary bet on earnings - you need a beat and positive guidance

- Max loss: $1,800 (100% of premium if stock below $590)

- Consider buying 2-3 contracts and selling 1 after earnings to lock in gains

- Exit if stock breaks below $580 before earnings (cut losses)

Who this is for: Degens who believe in the Q4 earnings beat and have $2,000 to gamble

⚠️ Risk Factors: What Could Go Wrong

🔴 Execution Risks

1. Price Increase Backfires 💸

- Q1 2026 US price hike ($11.99 → $12.99+) could trigger subscriber churn

- This would be the third increase in 3 years (from $9.99 to $12.99 = 30% cumulative!)

- Competitors cheaper: Amazon Music at $8.99 for Prime members

- Impact: If churn spikes, stock could dump to $520-550 range 📉

2. Advertising Revenue Still Weak 📺

- Q1 2025 ad revenue dropped 22% QoQ (though up 8% YoY)

- Free tier (402M users) depends on ad monetization

- Digital ad market still uncertain heading into 2026

- Impact: Ad revenue weakness would pressure margins even with subscriber growth

3. Content Cost Inflation 💿

- Music licensing costs are biggest expense (~70% of revenue)

- Label negotiations ongoing - unfavorable terms could compress margins

- Recording agreement functionality clauses constrain innovation

- Impact: Rising content costs could offset ARPU gains from price increases

🔴 Competitive Risks

4. Feature Parity Lag 🎧

- Spotify STILL lacks HiFi/lossless audio tier (promised years ago, never delivered)

- Apple Music, Amazon Music, Tidal all offer lossless at no extra cost

- Audiophiles defecting to competitors for quality

- Impact: Losing premium subscribers to rivals = market share erosion

5. Platform Power Imbalance 🍎

- Apple and Google charge 30% app store commission on subscriptions

- Apple's anti-competitive behavior resulted in €1.8B EU fine, but limited remedy

- Competitors with hardware (Apple, Amazon, Google) have preloaded advantage

- Impact: Structural disadvantage in profitability vs vertically-integrated rivals

6. YouTube Music & Amazon Gaining Ground 📱

- YouTube Music and Amazon seeing faster growth than Spotify

- YouTube's video integration = sticky engagement

- Amazon's Prime bundle = pricing advantage

- Impact: Market share loss = slower growth = multiple compression

🔴 Regulatory & Reputation Risks

7. Artist Royalty Controversy 🎤

- April 2024 policy requiring 1,000 streams for royalty eligibility redirected $47M from small artists

- Spotify pays lowest per-stream: $3 per 1,000 streams vs $8.80 (Amazon), $6.20 (Apple)

- Public backlash risk + potential regulatory intervention

- Impact: Forced to increase artist payouts = margin compression

8. European Regulatory Complexity 🇪🇺

- CEO Daniel Ek warned that European laws designed for sovereignty achieving opposite effect

- Complex and incoherent AI regulation could impact algorithmic recommendations

- Data privacy compliance costs rising with geographic expansion

- Impact: Higher compliance costs + innovation slowdown in key markets

🔴 Macroeconomic Risks

9. Consumer Spending Pressure 💳

- Q1 2026 price increase coincides with potential economic uncertainty

- Discretionary entertainment spending vulnerable in recession

- CEO warned of economic "noise" in Q1 2025

- Impact: Economic downturn = subscriber churn + ad revenue collapse

10. Valuation Risk 📊

- Stock trading near all-time highs after 40% YTD run

- High expectations baked in (analyst target $761 = 29% upside still needed)

- Any execution misstep = sharp multiple compression

- Impact: Limited margin for error at current valuations

🎯 The Bottom Line

Real talk: This whale trade is a sophisticated play on Spotify's transformation story, but it's not without risk.

Here's the deal:

✅ If you OWN SPOT stock:

- Hold through Q4 earnings (February 10) - fundamentals are solid

- Set stop at $570 (below gamma support) to protect downside

- Take partial profits at $630-650 (whale's target zone)

- Watch January 1 co-CEO transition for any red flags

👀 If you're WATCHING from sidelines:

- Wait for $600 breakout with volume confirmation before entering

- Alternative: Wait for dip to $570-580 (strong support) for better entry

- Mark your calendar: February 10, 2026 (Q4 earnings) = make or break moment

- If price hike announced in January with positive guidance = bullish signal

🐻 If you're BEARISH:

- Short-term put spreads could work if stock fails at $600 resistance

- February $580/$560 put spread = bet on pre-earnings consolidation

- But be careful - fighting the profitability trend and analyst upgrades is dangerous

- Max risk: Don't overstay if stock breaks above $610 (momentum shifts bullish)

The whale's bet makes sense:

- ✅ Buying ITM calls ($560 strike vs $590 spot) = built-in downside protection

- ✅ Closing old positions = taking profits, managing risk (not blind speculation)

- ✅ March 2026 expiration = captures Q4 earnings + price hike announcement + leadership transition

- ✅ $5M size = conviction, but not crazy (This is 0.004% of market cap)

My take: The risk/reward favors bulls heading into Q4 earnings if you:

- Believe Spotify can execute on price increases without churn (historical data says yes)

- Think audiobook differentiation creates pricing power vs competitors

- Accept 2026 will be choppy but trend is profitable growth

But watch out for:

- Price increase backlash (third hike in 3 years = pushing consumer limits)

- Advertising revenue doesn't recover (kills margin expansion story)

- Co-CEO transition creates strategic uncertainty

Final verdict: 🎯 7/10 setup - Bullish bias with multiple catalysts, but need to see $600 breakout for confirmation. This is a "wait and see" on earnings, not a blind buy.

Position accordingly, manage your risk, and remember: Even smart money whales can be wrong. Trade your plan, not your emotions! 💪

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. Past performance does not guarantee future results. This analysis is for educational purposes only and is not investment advice. Always do your own research and consult with a licensed financial advisor before making any investment decisions.

Analysis compiled December 9, 2025. Data sources: Proprietary options flow analysis, company filings, analyst reports, market data providers. Stock price and Greeks are real-time as of market hours December 9, 2025.

🔗 Learn More: