🐋 TEAM: Someone Just Dropped $1.3M on Atlassian Calls 25% Out of the Money -- Do They Know Something We Don't?

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just bought 2,400 TEAM call contracts at the $105 strike expiring 2026-05-15, paying $1.3M in premium -- with the stock sitting at just $83.91. That is a 25% out-of-the-money bet with a z-score of 310.57, meaning this level of activity is so rare it happens only a few times per year across the entire options market. With Atlassian coming off a blowout Q2, its first $1B cloud quarter, and analyst targets as high as $222, this trader is betting the massive gap between price and fundamentals closes fast.

🏢 Company Snapshot

Atlassian Corporation (NASDAQ: TEAM) builds the software that helps teams actually get things done. If you have ever used Jira, Confluence, Trello, or Bitbucket, you have used Atlassian. The company produces project planning, collaboration tools, and IT help desk solutions used by hundreds of thousands of organizations worldwide. Headquartered in San Francisco (originally founded in Sydney, Australia in 2002), TEAM has 13,813 employees and a $21.8B market cap. The company is classified under Prepackaged Software (SIC 7372) and has been publicly traded on NASDAQ since December 2015.

At $83.91, this stock is down roughly 74% from its all-time highs -- which is a striking number for a company that just posted record cloud revenue and is growing RPO at 44% year-over-year.

💰 The Option Flow Breakdown

📊 What Just Happened

| Field | Detail |

|---|---|

| 🕐 Time | March 6, 2026 at 11:11 AM ET |

| 📌 Ticker | TEAM |

| 📞 Type | CALL $105 (Bullish) |

| 🎯 Strike | $105 (25.1% above spot) |

| 📅 Expiration | 2026-05-15 (70 days out) |

| 📦 Size | 2,400 contracts |

| 💵 Premium Paid | $1.3M |

| 💲 Option Price | $5.30 per contract |

| 🏷️ Spot Price | $83.91 |

| 🔄 Side | MID -- Buy to Open |

| 📊 Volume vs OI | 3,000 volume / 87 OI (34.5x ratio) |

| 🔬 Z-Score | 310.57 (Extremely Unusual) |

| 🧩 Strategy | Long Call -- Standalone, new position |

🤓 What This Actually Means

Let me break this down because this is one of the most aggressive single-name call bets we have seen in a while.

Someone walked into the TEAM options market at 11:11 AM and bought 2,400 call contracts at a strike price that is a full 25% above where the stock is trading today. They paid $5.30 per contract, which is $1.3M of pure premium -- and every penny of that is time value. There is zero intrinsic value here. The stock needs to rally to $110.30 just for this trade to break even.

A few things jump off the screen:

✅ The z-score is 310.57 -- That is not a typo. This is over 310 standard deviations above the average trade size at this strike. To put it bluntly, the options market at this strike was practically dead (87 contracts of open interest) before this buyer showed up and purchased 2,400 contracts. Volume hit 3,000, making the vol/OI ratio 34.5x -- that is an entirely new position being built from scratch.

✅ Executed at mid -- They did not chase the ask. They placed at the midpoint, which tells you this is a patient, institutional-caliber execution. Retail does not do this.

✅ Deep OTM, maximum leverage -- At $5.30 per contract controlling shares worth $83.91, this buyer is getting roughly 16x leverage. If TEAM hits $130 by May 15, these calls would be worth $25 each -- a nearly 5x return on the $1.3M invested. If TEAM stays below $105, they lose everything.

✅ Timing through Q3 earnings -- The May 15 expiration sits just two weeks after the April 30 Q3 earnings date. This trader is betting that the next earnings report triggers a re-rating closer to where analysts think the stock should be.

Translation: Someone with deep pockets just made a high-conviction bet that Atlassian re-rates significantly higher over the next 70 days, likely triggered by Q3 earnings on April 30. They are comfortable losing $1.3M if they are wrong. That kind of conviction, backed by that kind of money, deserves attention.

📈 Technical Setup / Chart Check-Up

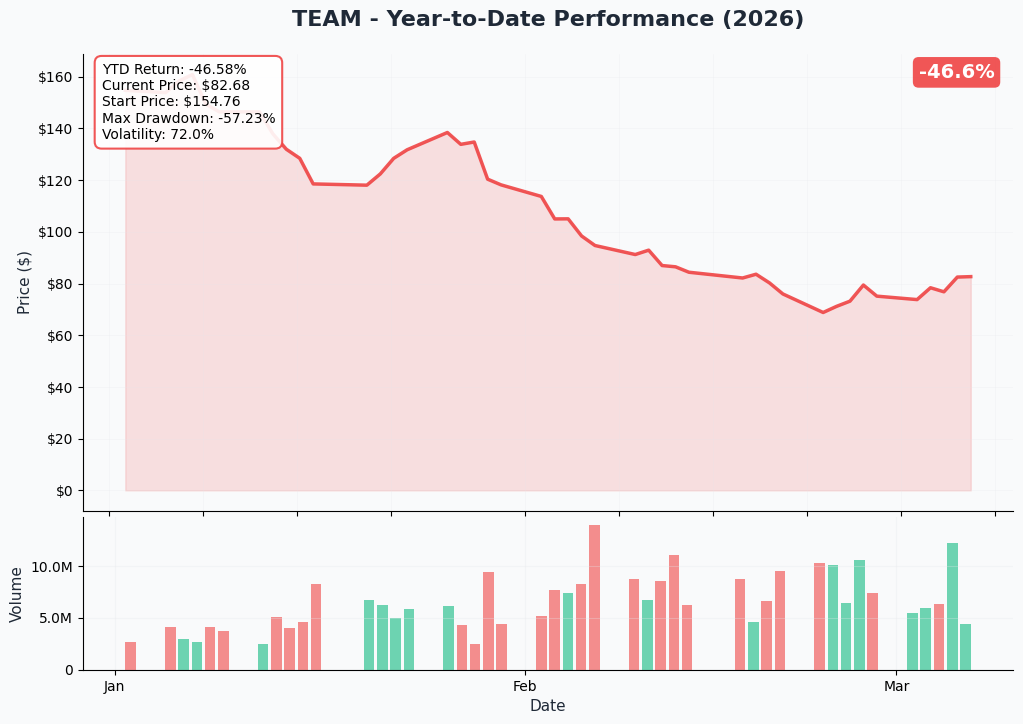

YTD Chart

TEAM has had a rough 2026 in terms of price action despite strong fundamentals. The stock is sitting at $83.91, down roughly 74% from its all-time highs, and has been grinding in a range that clearly does not reflect the company's accelerating growth metrics. On March 5, the stock popped 6.56% as investors started looking past AI disruption fears and focusing on the actual numbers Atlassian is putting up.

That March 5 rally is notable because it shows the kind of sudden move that can happen when sentiment shifts on deeply undervalued names. The stock went from feeling forgotten to making a noticeable move in a single session -- and today's $1.3M call bet suggests at least one big player thinks that was just the beginning.

Key Technical Levels: 📈 March 5 Pop: +6.56% -- first sign of life and momentum shift 📉 Current Price: $83.91 -- still deeply below analyst targets ⚖️ Near-Term Resistance: $85, $87.50, $90 (gamma levels) 🛡️ Near-Term Support: $82.50, $80 (gamma levels)

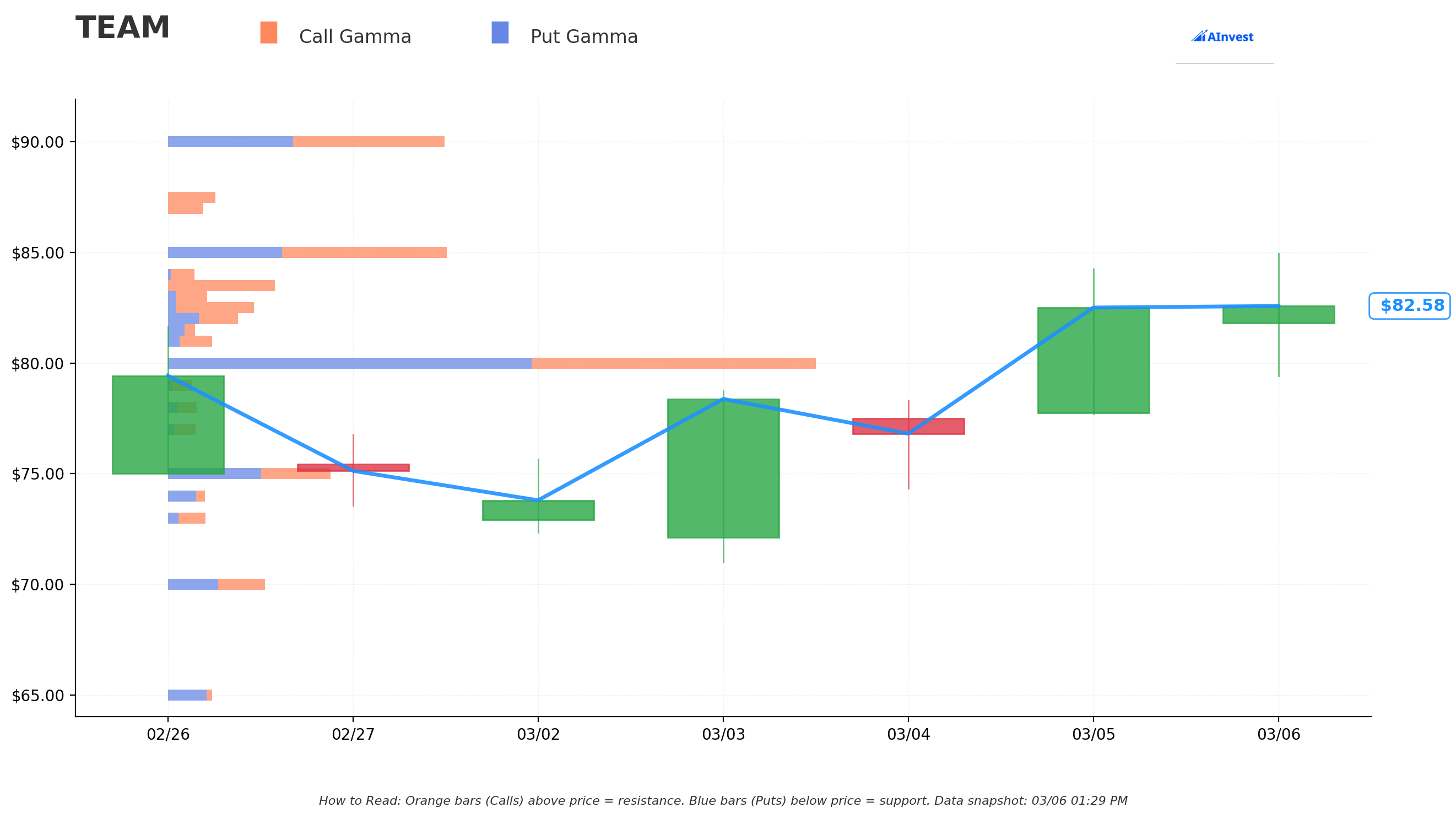

🔵🟠 Gamma-Based Support & Resistance

How to read this chart: The blue bars (put gamma) show support floors below the current price -- these are levels where options hedging activity creates buying pressure that tends to slow declines. The orange bars (call gamma) above the current price act as resistance ceilings. Bigger bars mean stronger levels.

Key gamma levels for TEAM:

🔵 $82.50 Support (0.19% below price) -- The strongest nearby support level with net gamma of 0.36. This is right under the current price and acts as a short-term floor. Dealer hedging activity here should provide a cushion.

🔵 $80 Support (3.2% below price) -- A significant gamma cluster with total GEX of 2.76. This is the "line in the sand" -- if TEAM breaks below $80, the next meaningful support is down at $75.

🟠 $85 Resistance (2.8% above price) -- The first real ceiling with total GEX of 1.29. Breaking above this level opens the door to higher strikes.

🟠 $90 Resistance (8.9% above price) -- A strong gamma wall with total GEX of 1.28. Getting above $90 would be a significant technical achievement and bring the $95 and eventually $105 targets into the conversation.

🟠 $95 Resistance (14.9% above price) -- Another notable call gamma level at 0.60 total GEX. This is the gateway to the $100+ zone where the whale's calls start getting interesting.

Overall GEX Bias: Bullish -- Total call gamma (8.94) significantly outweighs total put gamma (6.12), suggesting the market is positioned for upside. When call gamma exceeds put gamma, dealer hedging flows tend to support rallies.

Note: Gamma levels are dynamic and shift throughout the day as new trades open and close.

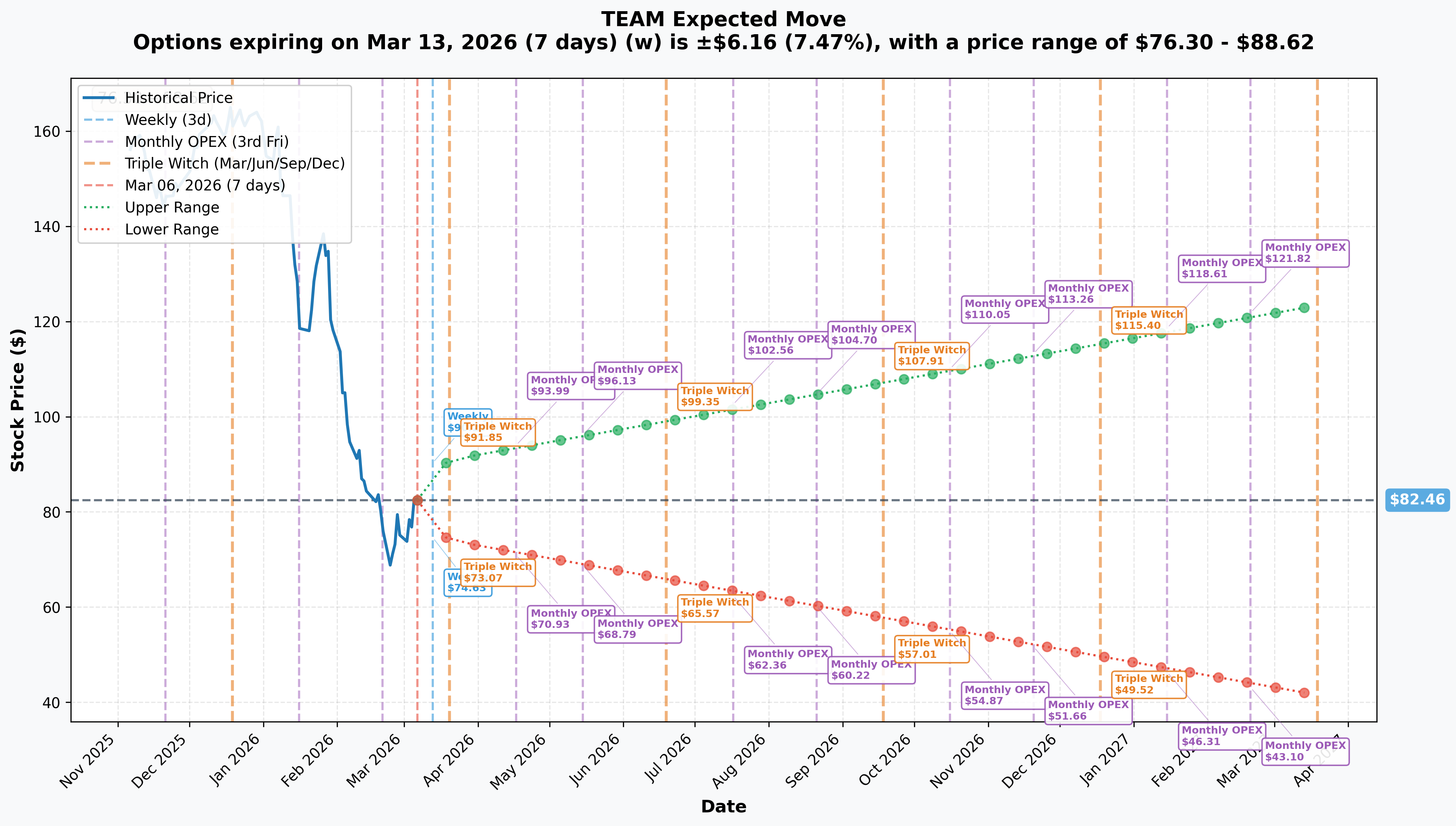

📐 Implied Move Analysis

The options market is pricing in significant volatility for TEAM -- which makes sense given the stock's recent behavior and upcoming earnings catalyst:

| Timeframe | Expiry | Implied Move | Range |

|---|---|---|---|

| 📅 Weekly | 2026-03-13 | ±7.5% (±$6.16) | $76.30 - $88.62 |

| 📅 Monthly (Triple Witch) | 2026-03-20 | ±10.3% (±$8.50) | $73.96 - $90.96 |

| 📅 April OPEX | 2026-04-17 | ~±13.4% | $70.93 - $93.99 |

| 📅 May OPEX (Whale's Expiry) | 2026-05-15 | ~±16.6% | $68.79 - $96.13 |

| 📅 LEAPS | 2027-03-19 | ±49.7% (±$40.97) | $41.49 - $123.43 |

Here is the important part for this trade: The implied move for the May 15 expiration (the whale's expiry) only reaches up to $96.13 on the upside. The whale's $105 strike is $9 above the market's expected upper range. This means the options market is pricing in roughly a sub-20% probability of this trade being profitable.

But here is the twist -- that implied move does NOT fully account for the Q3 earnings event on April 30, which falls right before expiration. Earnings events can and do produce moves well outside the "expected" range, especially for a stock this volatile that is 74% below its all-time high. If Atlassian delivers another blowout quarter, a gap to $105+ is far from impossible.

What this means for you: The market says this trade is a long shot. The whale is betting on a catalyst-driven gap that the implied move models are not fully capturing.

🎪 Catalysts

✅ Already Happened (Recent)

💥 Q2 FY2026 Earnings Beat (January/February): Atlassian absolutely crushed it. EPS came in at $1.22 vs $0.73 consensus -- a 67% beat. Revenue hit $1.59B vs $1.21B expected. The first-ever $1B cloud revenue quarter (up 26% YoY) was a milestone that confirmed the cloud migration thesis is working.

📈 RPO Growth of 44% YoY: Remaining Performance Obligations hit $3.8B, showing a massive pipeline of contracted future revenue. This is a forward indicator, and it is screaming growth.

📊 Net Revenue Retention Above 120%: For the third consecutive quarter, existing customers spent 20%+ more than the prior year. This kind of expansion rate is the hallmark of a sticky, mission-critical product.

🤖 Rovo AI Hits 5M MAU: Atlassian's AI product reached 5 million monthly active users, and over 1,000 customers upgraded to the Teamwork Collection (1M+ seats). AI agents launched in Jira -- positioning Atlassian as a serious player in enterprise AI.

💵 Surpassed $6B Annual Run Rate: The company crossed a major revenue milestone.

📈 March 5 Rally (+6.56%): Investors started looking past AI disruption fears and refocusing on fundamentals. This momentum shift set the stage for today's big call purchase.

📅 What's Coming Up

| Date | Event | Why It Matters |

|---|---|---|

| March 30 | New CFO James Chuong (ex-LinkedIn) starts | 🟡 Medium -- fresh leadership could signal strategic pivot, capital allocation changes |

| April 30 | Q3 FY2026 Earnings (Consensus EPS: $1.33) | 🔴 HIGH -- This is THE catalyst. Another beat could trigger re-rating toward analyst targets |

| TBD | Atlassian Team '26 Conference | 🟡 Medium -- Product announcements, Rovo AI updates, enterprise roadmap |

| Ongoing | Rovo AI adoption trajectory | 🟡 Medium -- Next MAU update will signal enterprise AI penetration rate |

| FY2026-FY2027 | Mid-term guidance: 20%+ CAGR revenue, 25%+ non-GAAP operating margin | 🟢 Steady -- long-term margin expansion story |

The April 30 earnings date is the linchpin for this trade. The May 15 call expiration gives the trader exactly 15 days of post-earnings runway for the stock to react and settle. If Q3 is anything like Q2 (which blew away expectations), a rapid re-rating is on the table.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, the catalyst calendar, and the sheer disconnect between price ($83.91) and analyst targets ($170-$222):

🐻 Bear Case: $75 - $80 (-5% to -10%)

📉 If the March rally fizzles and the broader market turns risk-off, TEAM could slide back to the $80 gamma support (total GEX of 2.76) or even the $75 level (GEX of 0.74). A tech selloff, disappointing CFO transition, or weaker-than-expected Q3 guidance could trigger this. The weekly implied move downside reaches $76.30, so a retreat to the mid-$70s is within the market's pricing.

Probability: ~20% -- The Q2 blowout and accelerating metrics make a further decline less likely, but macro risks and the 74% drawdown from ATH show the market is not fully trusting the recovery story yet.

⚖️ Base Case: $85 - $95 (+1% to +13%)

📊 TEAM breaks through the $85 gamma resistance, consolidates, and grinds toward the $90 gamma wall over the next few weeks. The new CFO starts March 30 and brings stability. Pre-earnings positioning builds into late April. The implied move range through May puts the upper end at ~$96. In this scenario, the whale's $105 calls lose significant time value but could still have some residual worth if momentum is building into earnings.

Probability: ~50% -- This is the most likely path. The fundamentals justify a higher price, but the market needs a catalyst (like Q3 earnings) to reprice the stock. Steady grinding higher with the gamma tailwind is the base expectation.

🚀 Bull Case: $105 - $130 (+25% to +55%)

📈 This is what the whale is betting on. Atlassian delivers another blowout Q3 on April 30 (beating the $1.33 consensus), raises guidance, shows Rovo AI adoption accelerating, and the new CFO signals confidence. Analysts start upgrading toward their $170-$222 price targets -- and the stock gaps through $100 and into the $105-$130 zone. Remember, this stock has a history of violent moves -- a 74% decline means it also has the capacity for rapid recoveries when sentiment shifts.

The math works: if TEAM traded at even the low end of analyst consensus ($140-$170), that is 67-100% upside from here. A gap to $105 would only represent a move to roughly 50% of the average price target -- still leaving enormous upside on the table.

Probability: ~30% -- This requires a catalyst-driven gap, most likely from Q3 earnings. Given the Q2 beat magnitude (67% EPS surprise), the RPO growth trajectory (44% YoY), and the $6B+ revenue run rate, another significant beat is very plausible. The key question is whether the market finally re-rates the stock toward fundamentals.

💡 Trading Ideas

🛡️ Conservative: "The New CFO Welcome Mat" -- Bull Put Spread

Structure: Sell TEAM $80 put / Buy TEAM $75 put, 2026-05-15 expiration

Why this works: You collect premium by betting TEAM does not fall below $80 -- a level that sits right at the major gamma support zone with total GEX of 2.76. The $75 long put limits your risk to $5/spread minus the credit. Even in the bear case, the $80 level has been a significant floor. You benefit from time decay and the bullish gamma bias without needing the stock to rally 25%.

📊 Estimated credit: ~$1.00-$1.50 per spread 📊 Max risk: ~$3.50-$4.00 per spread 📊 Max profit: Premium collected (if TEAM stays above $80) 📊 Win probability: ~70-75% 📊 Best for: Traders who are constructive on TEAM but do not want to bet on a 25% move

⚖️ Balanced: "The Earnings Bridge" -- Call Debit Spread

Structure: Buy TEAM $90 call / Sell TEAM $105 call, 2026-05-15 expiration

Why this works: This positions you for a rally through the $90 gamma resistance and up toward the whale's $105 strike, but at a fraction of the cost. You profit if TEAM breaks above the monthly implied move ceiling (~$96) and pushes toward $105 post-earnings. The April 30 Q3 report is the key catalyst, and the May 15 expiration gives you 15 days of post-earnings runway.

📊 Estimated cost: ~$2.50-$3.50 per spread 📊 Max profit: ~$15 per spread (at $105+) -- roughly a 4:1 reward-to-risk 📊 Breakeven: ~$92.50-$93.50 📊 Risk/reward: ~1:4 📊 Best for: Traders who believe Q3 earnings will catalyze a move to $100+ but want defined risk

🚀 Aggressive: "Follow the Whale" -- Long Call

Structure: Buy TEAM $100 call, 2026-05-15 expiration

Why this works: This is the closest you can get to following the whale without paying $5.30 per contract at the $105 strike. The $100 strike gives you a slightly lower breakeven and more delta exposure if the move materializes. You are betting that Q3 earnings on April 30 triggers a gap above $100 -- which would only require the stock to trade at roughly half of the average analyst price target. If TEAM hits $120, this call could be worth $20+ from an entry of ~$3-$4.

📊 Estimated cost: ~$3.00-$4.00 per contract 📊 Breakeven: ~$103-$104 📊 Max profit: Unlimited 📊 Risk: 100% of premium if TEAM stays below $100 📊 Best for: High-conviction traders who believe the fundamental gap to analyst targets will close. Only risk what you can afford to lose.

Pro tip: Consider sizing this at 1/4 to 1/2 of what you would normally trade. Deep OTM calls are asymmetric bets -- the win rate is low, but the payoff when it hits can be enormous. Treat this like a lottery ticket with much better odds than the Powerball.

⚠️ Risk Factors

❗ 74% Below All-Time Highs for a Reason: The massive drawdown may reflect a genuine structural re-rating of the business, not just temporary weakness. If the market is telling you Atlassian faces real secular headwinds (AI disruption, competition from Microsoft), no amount of quarterly beats may close the gap to prior highs.

❗ Data Center Decline: Management guided that the Data Center segment will decline "meaningfully" in FY2026. Cloud migration is the plan, but transition risk is real. If cloud growth decelerates before Data Center revenue fully rolls off, there could be a gap in the P&L.

❗ AI Disruption from Microsoft: Microsoft Copilot, GitHub Copilot, and Microsoft's broader enterprise AI suite directly compete with Atlassian's collaboration tools. If Microsoft's AI-native approach proves more compelling, Atlassian's moat could narrow. This is the biggest existential risk the market is pricing in.

❗ New CFO Transition: James Chuong (ex-LinkedIn) starts March 30. While his LinkedIn pedigree is impressive, CFO transitions always carry execution risk. Any changes to capital allocation, guidance methodology, or strategic direction could create near-term uncertainty.

❗ 25% OTM = High Hurdle: The stock needs to rally 25% just to reach the strike, and 31% to break even. While analyst targets support this, the options market is pricing in a sub-20% probability. You are fighting the odds with this trade.

❗ Macro Headwinds: Enterprise IT spending could slow in a recession scenario. If companies pull back on software subscriptions, Atlassian's net retention rate (currently 120%+) could compress. Conservative FY2026 guidance suggests management is already anticipating some softness.

❗ The Stock Can Stay Cheap Longer Than You Can Stay Solvent: Even if Atlassian is genuinely undervalued, the market can remain irrational for extended periods. A $1.3M bet with a 70-day expiration is a race against the clock.

🎯 The Bottom Line

Real talk: This is one of the most unusual trades we have seen on any single name in months. A z-score of 310 does not happen often. Someone with $1.3M to burn just bet that Atlassian, a stock that the broader market has left for dead, is about to wake up in a big way.

And honestly? The fundamental case is hard to argue with. A company that just posted its first $1B cloud quarter, beat EPS by 67%, grew RPO 44% year-over-year, and is running at a $6B+ annual revenue rate -- trading at $84 when analysts have price targets from $140 to $222. The disconnect is extreme.

If you are bullish on TEAM:

Mark your calendar for April 30 -- Q3 earnings is the event that could close the gap. The balanced call spread ($90/$105) gives you a 4:1 risk/reward through the earnings catalyst with defined risk. If you want more direct exposure, the $100 call gives you leverage into the event. Start small and add on a confirmed break above the $90 gamma wall.

If you are on the sidelines:

Watch the $85 resistance level. A convincing close above $85 with volume would confirm the March 5 momentum shift is real, not a one-day wonder. Then watch for the new CFO's first public comments after March 30 -- his tone on guidance and AI strategy could be a major tell. The Q3 earnings report on April 30 is the ultimate decision point.

If you are bearish:

The $80 gamma support is your line in the sand. A break below $80 opens the path to $75, and the LEAPS implied move down to $41.49 shows the market acknowledges deep downside risk exists. But be careful shorting here -- the combination of depressed valuation, accelerating fundamentals, and now a $1.3M institutional call bet means the snap-back risk is real.

The whale is making a bet that the market eventually wakes up to what Atlassian is actually doing. Whether it happens in 70 days or 70 weeks is the question. Size your positions accordingly. 👀

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Options trading involves significant risk of loss and is not suitable for all investors. You can lose more than your initial investment. Always do your own research and consider your risk tolerance before making any trading decisions. Past unusual options activity is not a reliable predictor of future stock price movement.

Analysis by Ainvest Option Labs | Data as of March 6, 2026